- Asian session: The dollar advanced as a safe haven

Market news

15 March 2011

Asian session: The dollar advanced as a safe haven

The yen rose against all of its 16 major counterparts as Japan’s Prime Minister Naoto Kan said the danger of further radiation leaks from a crippled nuclear power station is increasing, boosting speculation domestic investors will repatriate overseas assets.

The dollar advanced as a safe haven as Kan appealed for calm in a televised address and said his government was doing its utmost to contain the radioactive leak at Tokyo Electric Power Co.’s Fukushima Dai-Ichi plant following last week’s earthquake and tsunami. The greenback also rose versus most of its peers before reports this week forecast to show an expansion in industrial production.

EUR/USD: the pair shown low in the field of $1,3890.

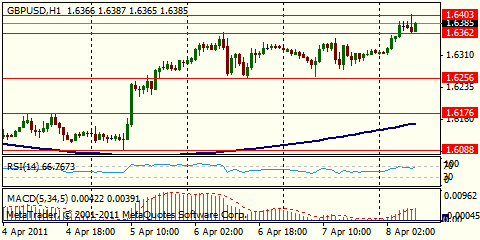

GBP/USD: the pair shown low in the field of $1,6050.

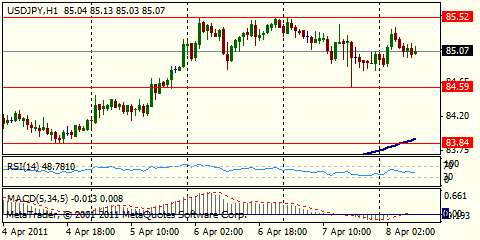

USD/JPY: the pair bargained within the limits of Y81.20-Y82.00.

The main EMU data release will be the German ZEW survey, at 1000GMT, where the expectations index is expected to edge up to a reading of 16.0 and the current conditions index is expected to edge up to 85.4.

US data starts at 1145GMT with the weekly ICSC-Goldman Store Sales data. This is followed at 1230GMT by the Import & Export Price Index as well as the Empire State Index, which is expected to increase to a reading of 16.0 in March after also rising in February. The Empire index has been lagging other manufacturing surveys which have been trending up. The weekly Redbook Average then follows, at 1255GMT, shortly followed at 1300GMT by the latest Treasury International Capital System (TICS) data. US data continues at 1400GMT with the NAHB Housing Market Index, while at the same time, US Treasury Secretary Tim Geithner testifies on the future of housing finance before the Senate Banking Committee in Washington.

The decision and statement from the latest FOMC meeting is due at 1815GMT although market expectations are for nothing major to come out of the meeting. MNI's Steve Beckner writes Monday there has been a subtle shift in Fed officials' thinking and commentary on the economy and inflation -- not just a more upbeat tone on the outlook for growth and jobs, but also slightly more acknowledgement of public inflation concerns.

The decision and statement from the latest FOMC meeting is due at 1815GMT although market expectations are for nothing major to come out of the meeting. MNI's Steve Beckner writes Monday there has been a subtle shift in Fed officials' thinking and commentary on the economy and inflation -- not just a more upbeat tone on the outlook for growth and jobs, but also slightly more acknowledgement of public inflation concerns.

Market Focus

Open Demo Account & Personal Page