- US Dollar Index struggles for direction below 94.00 ahead of key data

Market news

US Dollar Index struggles for direction below 94.00 ahead of key data

- DXY navigates a tight range in the 93.80 region on Thursday.

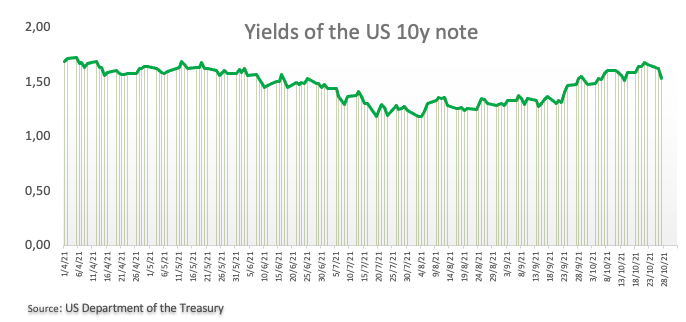

- US 10y yields drop to the sub-1.55% area, 2y yields rise further.

- Flash Q3 GDP, weekly Claims next of note in the docket.

The greenback keeps the cautious note and hovers around the 93.80 region when measured by the US Dollar Index (DXY).

US Dollar Index now focuses on data

The index alternates gains with losses following Wednesday’s downtick and always looking to the performance of the US cash markets and the broad risk appetite trends.

Indeed, while yields in the front end of the curve extend the advance well north of the 0.50% yardstick - levels last seen back in March 2020 - the belly of the curve navigates the area below 1.55% and the long end dropped well past the 2.00% mark.

Very interesting session data wise in the US, where advanced Q3 GDP figures will take centre stage along with the usual Initial Claims and seconded by Pending Home Sales. In addition, market participants are expected to closely follow the ECB event, where consensus remains tilted towards a somewhat dovish message from Chairwoman Lagarde.

What to look for around USD

The index gives away some ground following the lack of follow through after the recent surpass of the 94.00 hurdle. The positive performance of US yields, supportive Fedspeak regarding the start of the tapering process as soon as in November or December (also bolstered by latest comments by Chief Powell) and the rising probability that high inflation could linger for longer remain as key factors behind the constructive outlook for the buck in the near-to-medium term.

Key events in the US this week: Flash Q3 GDP, Initial Claims, Pending Home Sales (Thursday) – PCE, Core PCE, Personal Income/Spending, Final Consumer Sentiment (Friday).

Eminent issues on the back boiler: Discussions around Biden’s multi-billion Build Back Better plan. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. Debt ceiling debate. Geopolitical risks stemming from Afghanistan.

US Dollar Index relevant levels

Now, the index is losing 0.03% at 93.83 and a break above 94.17 (weekly high Oct.18) would open the door to 94.56 (2021 high Oct.12) and then 94.74 (monthly high Sep.25 2020). On the flip side, the next down barrier emerges at 93.48 (monthly low October 25) followed by 93.32 (55-day SMA) and finally 92.98 (weekly low Sep.23).