Market news

-

23:31

Australia: AIG Services Index, March 51.7

-

22:28

Commodities. Daily history for Apr 04’02’2017:

(raw materials / closing price /% change)

Oil 51.13 +0.20%

Gold 1,258.00 -0.03%

-

22:27

Stocks. Daily history for Apr 04’2017:

(index / closing price / change items /% change)

Nikkei -172.98 18810.25 -0.91%

TOPIX -12.49 1504.54 -0.82%

Hang Seng +149.89 24261.48 +0.62%

CSI 300 +19.29 3456.05 +0.56%

Euro Stoxx 50 +8.72 3481.66 +0.25%

FTSE 100 +39.13 7321.82 +0.54%

DAX +25.14 12282.34 +0.21%

CAC 40 +15.22 5101.13 +0.30%

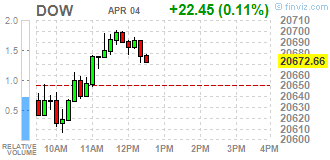

DJIA +39.03 20689.24 +0.19%

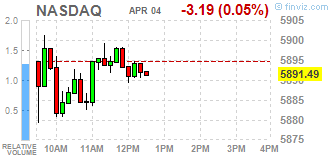

NASDAQ +3.93 5898.61 +0.07%

S&P/TSX +84.68 15669.08 +0.54%

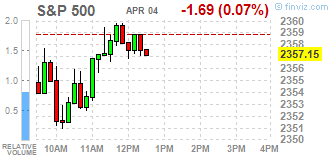

S&P 500 +1.32 2360.16 +0.06%

-

22:27

Currencies. Daily history for Apr 04’2017:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0678 +0,10%

GBP/USD $1,2443 -0,32%

USD/CHF Chf1,0016 +0,02%

USD/JPY Y110,69 -0,14%

EUR/JPY Y118,19 -0,04%

GBP/JPY Y137,74 -0,46%

AUD/USD $0,7565 -0,52%

NZD/USD $0,6973 -0,59%

USD/CAD C$1,3401 +0,18%

-

21:59

Schedule for today,Wednesday, Apr 05’2017 (GMT0)

07:50 France Services PMI (Finally) March 56.4 58.5

07:55 Germany Services PMI (Finally) March 54.4 55.6

08:00 Eurozone Services PMI (Finally) March 55.5 56.5

08:30 United Kingdom Purchasing Manager Index Services March 53.3 53.5

12:15 U.S. ADP Employment Report March 298 185

13:45 U.S. Services PMI (Finally) March 53.8 53.1

14:00 U.S. ISM Non-Manufacturing March 57.6 57

14:30 U.S. Crude Oil Inventories March 0.867

18:00 U.S. FOMC meeting minutes

22:40 Australia RBA Assist Gov Debelle Speaks

-

20:08

he main US stock indexes finished the session above the zero mark

The main US stock indexes rose, but only slightly, as investors are concerned about the possibility of President Donald Trump to implement his policy, and on the eve of a potentially tense meeting with Chinese President Xi Jinping, scheduled for April 6-7 in Florida.

The market moved away from session lows after Trump stated that infrastructure costs in the US could exceed $ 1 trillion and that his administration was working on major changes in Dodd-Frank banking regulation, reviving some of his campaign promises.

In addition, according to a report from the Department of Commerce, the US trade deficit in February fell more than expected, as exports increased to a two-year high, and a slowdown in domestic demand was due to imports. According to the report, the trade deficit decreased by 9.6% to $ 43.6 billion. Economists predicted a reduction in the trade deficit to $ 44.9 billion in February.

At the same time, production orders rose in February for the seventh time in eight months, which was a sign of a recovery in the manufacturing industry. Production orders rose by 1%, the Commerce Ministry said, which corresponds to a consensus forecast. The release in January was raised to 1.5%.

The components of the DOW index have mostly grown (19 out of 30). More shares fell NIKE, Inc. shares. (NKE, -0.97%). Caterpillar Inc. (CAT, + 2.12%) was the growth leader.

The sectors of the S & P index showed multidirectional dynamics. The conglomerate sector fell most of all (-0.5%). The leader of growth was the sector of basic materials (+ 0.7%).

At closing:

DJIA + 0.19% 20.689.18 +38.97

Nasdaq + 0.07% 5,898.61 +3.93

S & P + 0.05% 2,360.11 +1.27

-

19:00

DJIA +0.12% 20,675.67 +25.46 Nasdaq -0.02% 5,893.28 -1.40 S&P -0.02% 2,358.39 -0.45

-

16:34

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Tuesday, trading in a tight range, as investors fretted over the ability of President Donald Trump to deliver on his policy plans, and ahead of his potentially tense meeting with Chinese President Xi Jinping. However, the market moved off session lows after Trump said the U.S. infrastructure bill may top $1 trillion and that his administration was working on a major "haircut" on the Dodd-Frank banking regulation, rekindling some of his campaign promises.

Most of Dow stocks in positive area (18 of 30). Top loser - Cisco Systems, Inc. (CSCO, -0.77%). Top gainer - Caterpillar Inc. (CAT, +2.29%).

S&P sectors mixed. Top loser - Conglomerates (-0.3%). Top gainer - Basic Materials (+0.5%).

At the moment:

Dow 20620.00 +30.00 +0.15%

S&P 500 2354.00 -2.00 -0.08%

Nasdaq 100 5431.50 -3.00 -0.06%

Oil 51.09 +0.85 +1.69%

Gold 1258.00 +4.00 +0.32%

U.S. 10yr 2.36 +0.01

-

16:00

European stocks closed: FTSE 100 +39.13 7321.82 +0.54% DAX +25.14 12282.34 +0.21% CAC 40 +15.22 5101.13 +0.30%

-

14:33

Change in GDT Price Index from previous event +1.6%, Average price (USD/MT, FAS) $3,005

-

14:03

US factory orders rose 1% in Feb, as expected

New orders for manufactured durable goods in February increased $3.9 billion or 1.7 percent to $235.4 billion, the U.S. Census Bureau announced today. This increase, up two consecutive months, followed a 2.3 percent January increase. Excluding transportation, new orders increased 0.4 percent. Excluding defense, new orders increased 2.1 percent. Transportation equipment, also up two consecutive months, led the increase, $3.3 billion or 4.3 percent to $80.4 billion.

Shipments of manufactured durable goods in February, up three of the last four months, increased $0.6 billion or 0.3 percent to $239.2 billion. This followed a 0.1 percent January decrease. Machinery, also up three of the last four months, led the increase, $0.3 billion or 0.9 percent to $31.1 billion.

-

14:00

U.S.: Factory Orders , February 1% (forecast 1%)

-

13:36

Russian PM Medvedev says anti-corruption allegations made against him are "nonsense" - TASS

-

Allegations are politically motivated, attempt to get people onto the streets

-

-

13:34

U.S. Stocks open: Dow -0.06%, Nasdaq -0.17%, S&P -0.16%

-

13:29

Before the bell: S&P futures -0.40%, NASDAQ futures -0.47%

U.S. stock-index futures as investors fretted over the ability of President Donald Trump to deliver on his policy plans, and the outcome of his potentially tense meeting with the President of the People's Republic of China Xi Jinping later this week.

Stocks:

Nikkei 18,810.25 -172.98 -0.91%

FTSE 7,312.94 +30.25 +0.42%

CAC 5,081.54 -4.37 -0.09%

DAX 12,245.28 -11.92 -0.10%

Crude $50.55 (+0.62%)

Gold $1,260.90 (+0.55%)

-

12:53

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

34.21

-0.01(-0.03%)

2256

ALTRIA GROUP INC.

MO

71.5

-0.12(-0.17%)

354

Amazon.com Inc., NASDAQ

AMZN

889.75

-1.76(-0.20%)

14899

AMERICAN INTERNATIONAL GROUP

AIG

61.51

-0.28(-0.45%)

315

Apple Inc.

AAPL

143.35

-0.35(-0.24%)

55122

Barrick Gold Corporation, NYSE

ABX

19.53

0.22(1.14%)

56367

Caterpillar Inc

CAT

93.89

1.62(1.76%)

22148

Chevron Corp

CVX

107.4

-0.40(-0.37%)

420

Citigroup Inc., NYSE

C

59.1

-0.58(-0.97%)

9130

Facebook, Inc.

FB

141.73

-0.55(-0.39%)

47100

Ford Motor Co.

F

11.37

-0.07(-0.61%)

64419

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

13.6

0.36(2.72%)

179329

General Electric Co

GE

29.8

-0.08(-0.27%)

3786

General Motors Company, NYSE

GM

33.93

-0.24(-0.70%)

21625

Goldman Sachs

GS

227

-1.96(-0.86%)

5073

Google Inc.

GOOG

830.5

-8.05(-0.96%)

3536

Hewlett-Packard Co.

HPQ

17.54

-0.05(-0.28%)

679

Intel Corp

INTC

36.1

-0.06(-0.17%)

5722

International Business Machines Co...

IBM

173.59

-0.91(-0.52%)

1880

JPMorgan Chase and Co

JPM

86.5

-0.52(-0.60%)

21554

Nike

NKE

55.25

-0.31(-0.56%)

4520

Pfizer Inc

PFE

34.06

-0.18(-0.53%)

971

Tesla Motors, Inc., NASDAQ

TSLA

297.5

-1.02(-0.34%)

80161

Twitter, Inc., NYSE

TWTR

14.79

-0.05(-0.34%)

17496

United Technologies Corp

UTX

112.08

0.15(0.13%)

2012

Verizon Communications Inc

VZ

49.08

-0.10(-0.20%)

2673

Wal-Mart Stores Inc

WMT

71.73

-0.10(-0.14%)

922

Walt Disney Co

DIS

112.95

-0.25(-0.22%)

1564

Yandex N.V., NASDAQ

YNDX

22.12

-0.01(-0.05%)

1100

-

12:50

Following three consecutive monthly surpluses, Canada's merchandise trade balance posted a $972 million deficit in February

Exports were down 2.4%, with decreases in 8 of 11 sections. Imports edged up 0.6%, on higher imports of special transactions trade and motor vehicles and parts.

After reaching a record high in January, total exports fell 2.4% to $45.3 billion in February on lower volumes. Year over year, exports were up 4.4%. There were lower exports of farm, fishing and intermediate food products, aircraft and other transportation equipment and parts, as well as consumer goods. In February, exports excluding energy products were also down 2.4%.

Following a record high in January, exports of farm, fishing and intermediate food products fell 10.6% to $2.7 billion in February, returning to December levels. Canola contributed the most to the decline in February, down 33.7% to $552 million. This followed three consecutive monthly increases during which exports of canola more than doubled, reflecting higher Chinese demand for Canadian canola. Overall, volumes were down 10.2% and prices declined 0.5%.

-

12:48

US trade balance deficit declined slightly in February

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $43.6 billion in February, down $4.6 billion from $48.2 billion in January, revised. February exports were $192.9 billion, $0.4 billion more than January exports. February imports were $236.4 billion, $4.3 billion less than January imports.

The February decrease in the goods and services deficit reflected a decrease in the goods deficit of $4.6 billion to $65.0 billion and an increase in the services surplus of less than $0.1 billion to $21.4 billion.

Year-to-date, the goods and services deficit increased $2.8 billion, or 3.1 percent, from the same period in 2016. Exports increased $25.8 billion or 7.2 percent. Imports increased $28.6 billion or 6.4 percent.

-

12:44

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

NIKE (NKE) downgraded to Hold from Buy at Argus

Bank of America (BAC) downgraded to Neutral from Buy at Citigroup

Alphabet A (GOOGL) downgraded to Market Perform from Outperform at BMO Capital

Other:

Caterpillar (CAT) added to Conviction Buy List at Goldman

United Tech (UTX) added to US 1 List at BofA/Merrill; maintain Buy, target $130

IBM (IBM) initiated with a Sell at Berenberg; target $140

Cisco Systems (CSCO) initiated with a Hold at Berenberg

Hewlett Packard Enterprise (HPE) initiated with a Hold at Berenberg

-

12:30

Canada: Trade balance, billions, February -0.97 (forecast 0.55)

-

12:30

U.S.: International Trade, bln, February -43.6 (forecast -44.9)

-

12:00

Orders

EUR/USD

Offers: 1.0665 1.0680-85 1.0700 1.0730 1.0750

Bids: 1.0630 1.0600 1.0580 1.0565 1.0550

GBP/USD

Offers: 1.2450 1.2465 1.2485 1.2500 1.2520 1.2550-55 1.2585 1.2600

Bids: 1.2420 1.2400 1.2375-80 1.2350 1.2330 1.2300 1.2280 1.2250

EUR/JPY

Offers: 117.85 118.00 118.20 118.50 118.65 118.80 119.00

Bids: 117.50 117.30 117.00 116.85 116.50 116.00

EUR/GBP

Offers: 0.8585 0.8600 0.8630 0.8650

Bids: 0.8545-50 0.8525-30 0.8500 0.8485 0.8465 0.8450

USD/JPY

Offers: 110.65 110.80 111.00 111.20 111.50 111.80 112.00

Bids: 110.25-30 110.00 109.85 109.65 109.50 109.00

AUD/USD

Offers: 0.7575-80 0.7600 0.7620 0.7650

Bids: 0.7550 0.7530 0.7500 0.7485 0.7450

-

11:30

Far-right's Le Pen to get 26 pct (+1) in 1st round of French election, Macron 24 pct (unchanged), Fillon 20 pct (+1) - Opinionway poll

-

Macron seen beating Le Pen in run-off vote by 61 pct

-

Fillon would beat Le Pen in run-off vote by 56 pct to 44 pct if Fillon made it through to second round

-

-

10:11

Le pen and Macron tied on 25 pct in first round of French election, Fillon with 17 - Le Monde/Cevipof poll

-

09:29

U.S. non-farm payrolls likely to increase in March - Danske Bank

"We estimate that unemployment remained at 4.7 percent and average hourly earnings increased 0.2 percent m/m, implying an increase in the wage growth rate of 2.7 percent y/y. We continue to expect the service sector to be the main driver of job creation and expect it contributed 160,000 new jobs. Manufacturing has been on a positive trend in terms of job creation, but we expect it slowed somewhat in March (also due to bad weather). Thus, we expect 15,000 new jobs were created in manufacturing".

-

09:07

Euro zone retail sales rose 0.7% in Feb due to rises of non-food products

In February 2017 compared with January 2017, the seasonally adjusted volume of retail trade rose by 0.7% in both the euro area (EA19) and the EU28, according to estimates from Eurostat, the statistical office of the European Union. In January the retail trade volume increased by 0.1% in the euro area and by 0.2% in the EU28. In February 2017 compared with February 2016, the calendar adjusted retail sales index increased by 1.8% in the euro area and by 2.2% in the EU28.

-

09:00

Eurozone: Retail Sales (MoM), February 0.7% (forecast 0.5%)

-

09:00

Eurozone: Retail Sales (YoY), February 1.8% (forecast 1.4%)

-

08:32

March data revealed a slowdown in growth across the UK construction sector - Markit

March data revealed a slowdown in growth across the UK construction sector, led by a weaker rise in residential building activity. The latest survey also pointed to only a marginal increase in new work, which contributed to slower employment growth and a slight decline in input buying.

The seasonally adjusted Markit/CIPS UK Construction Purchasing Managers' Index (PMI) dropped from 52.5 in February to 52.2 in March, to signal the joint-slowest upturn in overall construction output since the current period of expansion began in September 2016. Softer growth primarily reflected a loss of momentum in housing activity, which offset a rebound in both commercial and civil engineering activity. The latest increase in work on civil engineering projects was the fastest so far in 2017 and the strongest of the three subcategories monitored by the survey in March.

-

08:30

United Kingdom: PMI Construction, March 52.2 (forecast 52.4)

-

07:49

Major stock exchanges in Europe trading in the green zone: FTSE 7313.61 +30.92 + 0.42%, DAX 12250.99 -6.21 -0.05%, CAC 5091.19 +5.28 + 0.10%

-

07:22

Spanish unemployment has decreased more than expected in March

The number of unemployed registered in the offices of the Public Employment Services has decreased in March by 48,559 people in relation to the previous month. In the last 8 years unemployment has increased in March, on average, by 11,585 people. During the first quarter of the year unemployment fell by 657 people. It is the first time it has decreased in this period since the year 1999 In this way, the total number of unemployed registered is 3,702,317 people, and remains at its lowest level of the last 7 years.

-

06:37

Options levels on tuesday, April 4, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0839 (555)

$1.0808 (1080)

$1.0765 (462)

Price at time of writing this review: $1.0658

Support levels (open interest**, contracts):

$1.0618 (502)

$1.0577 (755)

$1.0526 (1682)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 46787 contracts, with the maximum number of contracts with strike price $1,1450 (3939);

- Overall open interest on the PUT options with the expiration date June, 9 is 53192 contracts, with the maximum number of contracts with strike price $1,0400 (4518);

- The ratio of PUT/CALL was 1.14 versus 1.09 from the previous trading day according to data from April, 3

GBP/USD

Resistance levels (open interest**, contracts)

$1.2710 (837)

$1.2614 (368)

$1.2519 (858)

Price at time of writing this review: $1.2437

Support levels (open interest**, contracts):

$1.2386 (579)

$1.2289 (325)

$1.2192 (541)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 14908 contracts, with the maximum number of contracts with strike price $$1,3000 (1281);

- Overall open interest on the PUT options with the expiration date June, 9 is 16959 contracts, with the maximum number of contracts with strike price $1,1500 (3056);

- The ratio of PUT/CALL was 1.14 versus 1.12 from the previous trading day according to data from April, 3

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

06:26

South Africa's rand falls 1 percent against dollar to 13.8200/$ a day after S&P downgrade

-

06:07

Moody's has placed the Baa2 long-term issuer and senior unsecured bond ratings of the government of South Africa on review for downgrade

The decision to initiate a review for downgrade was prompted by the abrupt change in leadership of key government institutions. That action has raised questions regarding:

- progress on reforms previously identified as essential to sustain South Africa's fiscal and economic strength, and the effectiveness of South Africa's policymaking institutions; and

- the more immediate implications for growth and public debt given the potentially negative impact on fragile domestic and external investor confidence.

The review will allow Moody's to assess these risks and if the changes in leadership signal a weakening in the country's institutional, economic and fiscal strength.

South Africa's (P)Baa2 Senior Unsecured Shelf and MTN program ratings were also placed under review for downgrade, as was the (P)P-2 Senior Unsecured Short-Term rating.

In a related rating action, Moody's has also placed on review for downgrade the Baa2 senior unsecured rating of the ZAR Sovereign Capital Fund Propriety Limited, which is fully and unconditionally guaranteed by the Republic of South Africa

-

06:05

RBA hold the interest rate at 1.50%. Said recent data consistent with ongoing moderate growth

"At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

Conditions in the global economy have improved over recent months. Both global trade and industrial production have picked up. Labour markets have tightened in many countries. Above-trend growth is expected in a number of advanced economies, although uncertainties remain. In China, growth is being supported by higher spending on infrastructure and property construction. This composition of growth and the rapid increase in borrowing mean that the medium-term risks to Chinese growth remain. The improvement in the global economy has contributed to higher commodity prices, which are providing a significant boost to Australia's national income.

Headline inflation rates have moved higher in most countries, partly reflecting the higher commodity prices. Core inflation remains low. Long-term bond yields are higher than last year, although in a historical context they remain low. Interest rates have increased in the United States and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively.

The Australian economy is continuing its transition following the end of the mining investment boom. Recent data are consistent with ongoing moderate growth. Most measures of business confidence are at, or above, average and non-mining business investment has risen over the past year. At the same time, some indicators of conditions in the labour market have softened recently. In particular, the unemployment rate has moved a little higher and employment growth is modest. The various forward-looking indicators still point to continued growth in employment over the period ahead. Wage growth remains slow".

-

06:04

BoJ Gov Kuroda: BoJ's ETF purchases are part of policy to meet 2 pct inflation target

-

Too early to talk about exit strategy from current monetary policy, which includes ETF purchases

-

-

05:57

Australian trade balance registered a bigger than expected surplus

In trend terms, the balance on goods and services was a surplus of $3,320m in February 2017, an increase of $545m (20%) on the surplus in January 2017.

In seasonally adjusted terms, the balance on goods and services was a surplus of $3,574m in February 2017, an increase of $2,071m on the surplus in January 2017.

In seasonally adjusted terms, goods and services credits rose $469m (1%) to $32,405m. Non-monetary gold rose $352m (33%) and non-rural goods rose $236m (1%). Rural goods fell $195m (5%). Net exports of goods under merchanting remained steady at $41m. Services credits rose $76m (1%).

-

05:28

Global Stocks

Stocks across Europe closed with losses Monday, as they start a new quarter with a heavy week of data, including from the European Central Bank. While German equities finished lower, they initially got help from the final March manufacturing PMI for Europe's largest economy being confirmed at a 71-month high at 58.3. The overall eurozone final March manufacturing PMI was also confirmed at a 71-month high, at 56.2.

U.S. stocks closed lower Monday, but off session lows, to kick off the second quarter as disappointing vehicle sales and lackluster economic data amplified concerns that lofty equity valuations won't be buttressed by commensurately strong corporate quarterly results in coming weeks.

Asian equities pulled back Tuesday as investors turned risk averse again amid growing investor uncertainty about U.S.-China trade and monetary policy in Japan and Europe. The yen rose against the dollar through the U.S. session, and has continued to strengthen in Asian trade.

-

04:30

Australia: Announcement of the RBA decision on the discount rate, 1.5% (forecast 1.5%)

-

01:30

Australia: Trade Balance , February 3.57 (forecast 1.8)

-