Noticias del mercado

-

23:54

IEA’s Birol: China's oil demand bounce may push producers to reconsider output

“Oil producers may have to reconsider their output policies following a demand recovery in China, the world's second-largest oil consumer,” International Energy Agency (IEA) Executive Director Fatih Birol said on the sidelines of the India Energy Week conference on Sunday per Reuters.

Key comments

We expect about half of the growth in global oil demand this year will come from China.

If demand goes up very strongly, if the Chinese economy rebounds, then there will be a need, in my view, for the OPEC+ countries to look at their (output) policies.

Price caps on Russian oil have achieved the objectives of both stabilizing oil markets and reducing Moscow's revenues from oil and gas exports.

Fuel markets might face difficulties in the short term as global trade routes ‘reshuffle’ to accommodate Europe drawing on more imports from China, India, the Middle East and the United States.

That could force other markets such as Latin America to scout for alternative imports.

Fuel market balance could improve from the second half as more refining capacity is added globally.

WTI bears take a breather

The news allowed WTI crude oil bears to take a breather at the one-month low surrounding $73.50, following a three-day downtrend.

-

23:46

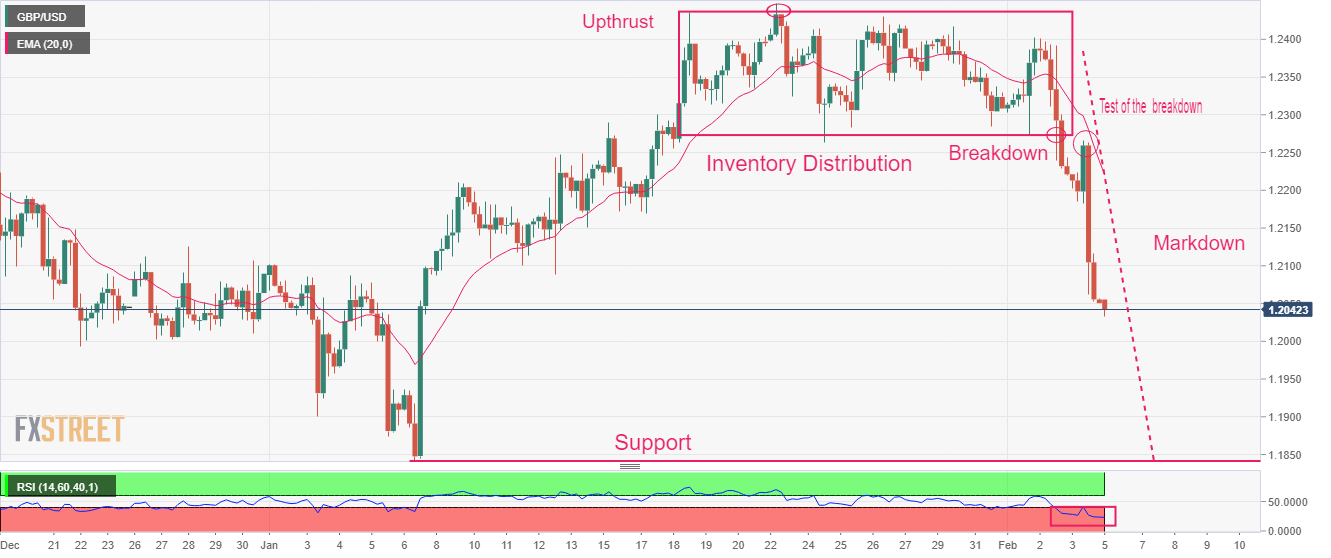

GBP/USD Price Analysis: Sees continuation of its downside journey below 1.1850

- GBP/USD witnessed significant selling pressure after testing the inventory distribution breakdown around 1.2268.

- The Cable is in a Wyckoff’s markdown phase and may find support near 1.1850.

- A 20.00-40.00 range oscillation by the RSI (14) indicates more weakness ahead.

The GBP/USD pair has dropped below the critical support of 1.2050 in the early Tokyo session on expectations that the Federal Reserve (Fed) will continue hiking interest rates due to upbeat United States official employment data. The market mood has turned risk-averse as further interest rate hiking by Fed chair Jerome Powell will deepen recession fears.

S&P 500 futures tumbled after a three-day winning streak, portraying a sheer decline in the risk appetite of the market participants. The 10-US Treasury yields have recovered above 3.51% as the inflation projections are set to rebound further.

GBP/USD witnessed a massive sell-off after delivering a downside break of the Inventory Distribution formed on a two-hour scale. The formation of Upthrust around January 23 high at 1.228 indicates the presence of significant selling interest. The Cable has shifted into a markdown phase after testing the downside break of Wyckoff’s inventory distribution.

The 20-period Exponential Moving Average (EMA) at 1.2224 will act as a major barricade for the Pound Sterling bulls.

Meanwhile, the Relative Strength Index (RSI) (14) is oscillating in the bearish range of 20.00-40.00, which indicates that the downside momentum is active.

A further decline in the Cable below the intraday low at 1.2033 will drag the asset toward January 3 low at 1.1900 followed by horizontal support placed from January 6 low around 1.1841.

On the contrary, a break above January 24 low at 1.2263 will support a bullish reversal and will drive the Cable towards February 2 high around 1.2400. A breach of the latter will send the major toward January 23 high at 1.2448.

GBP/USD two-hour chart

-

23:40

Japan’s Suzuki: Have not heard anything about nomination of Amamiya as BoJ Governor

“I have not heard anything about nomination of Amamiya as BoJ Governor,” said Japan's Finance Minister Shunichi Suzuki per Reuters.

Also read: Japan sounds out BoJ deputy Amamiya for central bank governor

The policymaker further added that he won’t comment on each candidate for BoJ Governor.

“Aware of media report overnight that Government arranging to nominate Amamiya,” stated Japan FinMin Suzuki.

Japan’s Suzuki also stated that he has been “out of the loop” on BoJ nomination.

USD/JPY grinds higher

Following the news, the USD/JPY pair defends Friday’s recovery moves around 131.85, up nearly half a percent intraday.

It’s worth noting that Bank of Japan (BoJ) Governor Haruhiko Kuroda is up for leaving his place in April 2023 and hence the rush for the next BoJ leader is active. Also highlighting the importance of the discussions are the latest pressure on the BoJ policymaker to shift from the ultra-easy monetary policy.

-

23:36

USD/CAD bulls attack 1.3400 amid downbeat Oil price, focus on BoC’s Macklem, Canada employment data

- USD/CAD begins the key week on a firmer footing, mildly bid during three-day uptrend.

- Upbeat US data, geopolitical tension propelled US Dollar, weighed on Oil price of late.

- BoC Governor Macklem’s speech, Canada jobs report for January will be crucial for immediate directions.

USD/CAD prints mild gains around 1.3415 as bulls keep the reins at the start of the key week for Loonie traders. In doing so, the quote prints three-day uptrend while justifying firmer US Dollar and the downbeat prices of Oil, Canada’s main export item.

Be it the unimpressive interest rate hikes by the European Central Bank (ECB) and the Bank of England (BoE) or the strong US data, the US Dollar had it all to recover from the multi-month low. That said, the US Dollar Index (DXY) managed to post the biggest weekly gains since September 2022, not to forget snapping three-week downtrend, in the last.

On Thursday, the ECB and the BoE both matched market forecasts by announcing 0.50% hike in their respective benchmark rates. The policymakers also tried to sound hawkish but couldn’t hide the receding inflation fears, which in turn suggested lesser need for strong rate increases. The same joined downbeat tech earnings reports and helped the DXY to rebound from the lowest levels since April 2022.

Following that, the US Bureau of Labor Statistics (BLS) surprised markets by revealing that the Nonfarm Payrolls (NFP) rose by 517K in January, versus 185K expected and 260K (upwardly revised) prior. It’s worth noting that the Unemployment Rate also dropped to 3.4% from 3.5% prior and 3.6% expected but the Average Hourly Earnings eased during the stated month.

Other than the headline US job numbers, the rebound in the US ISM Services PMI from 49.2 to 55.2, versus 50.4 expected, also underpinned the rebound in the United States Treasury bond yields and the US Dollar. That said, the benchmark US 10-year Treasury bond yields jumped the most since late September 2022 to regain 3.52% level by the volatile week’s end.

Additionally helping the US Dollar are the recent fears emanating from surrounding the US and China. “A US military fighter jet shot down a suspected Chinese spy balloon off the coast of South Carolina on Saturday, a week after it first entered US airspace and triggered a dramatic -- and public -- spying saga that worsened Sino-US relations,” said Reuters.

Elsewhere, WTI crude oil dropped in the last three consecutive days to $73.45 as firmer US Dollar and fresh fears surrounding the gap for the Fed doves before they retake control, due to the strong data, weigh on the commodity prices.

Moving on, Tuesday becomes the key day for the USD/CAD pair as Bank of Canada (BoC) Governor Tiff Macklem and Federal Reserve (Fed) Chairman Jerome Powell both will appear for speeches. Following that, Friday’s Canada jobs report for January and the US UoM Consumer Sentiment Index for February, as well as the University of Michigan's 5-year Consumer Inflation expectations, will be crucial for fresh impulse.

Technical analysis

Although an upward-sloping support line from June 2022, around 1.3310 by the press time, defends USD/CAD buyers, the Loonie pair’s upside remains elusive until the quote stays below the 50-DMA level of near 1.3500.

-

23:16

Gold Price Forecast: XAU/USD bears flex muscles as United States Treasury bond yields rebound

- Gold price justifies downside break of key support line as sellers attack one-month low.

- Strong United States data underpinned recovery in US Treasury bond yields, US Dollar and weighed on XAU/USD.

- US-China tussles add strength to geopolitical tension and favor Gold sellers.

Gold price (XAU/USD) holds lower ground near $1,865, after declining to the fresh one-month low the previous day. The metal’s latest weakness could be linked to the strong United States data renewing inflation fears, as well as downbeat rate hike performances of the European Central Bank and the Bank of England (BoE). Also exerting downside pressure on the XAU/USD is the fresh geopolitical tension surrounding the US-China ties. Above all, the recovery in the US Treasury bond yield renewed the US Dollar and recalled the Gold bears after a month-long absence.

United States data propel yields and Gold bears

Although the United States Federal Reserve (Fed) announced a dovish rate hike, the strong US economics surrounding jobs and activities renewed inflation fears and favored the odds of further rate increases from the Fed.

On Friday, the US Bureau of Labor Statistics (BLS) surprised markets by revealing that the Nonfarm Payrolls (NFP) rose by 517K in January, versus 185K expected and 260K (upwardly revised) prior. It’s worth noting that the Unemployment Rate also dropped to 3.4% from 3.5% prior and 3.6% expected but the Average Hourly Earnings eased during the stated month.

Other than the headline US job numbers, the rebound in the US ISM Services PMI from 49.2 to 55.2, versus 50.4 expected, also underpinned the rebound in the United States Treasury bond yields and the US Dollar.

That said, the benchmark US 10-year Treasury bond yields jumped the most since late September 2022 to regain 3.52% level by the volatile week’s end. The same propelled the US Dollar to recover from the lowest levels since April 2022 and weigh on the Gold price.

Downbeat European Central Bank, Bank of England also tease XAU/USD sellers

Last week, the European Central Bank (ECB) announced a 0.50% interest rate hike by matching the market expectations.

Following the interest rate announcements, ECB President Christine Lagarde said, “We haven't reached the peak in rate, we have ground to cover.” The policymaker also signaled that the risks to inflation and growth are more balanced.

On the other hand, the Bank of England (BoE) announced a 0.50% interest rate hike by matching the market expectations. Following the interest rate announcements, BoE Governor Andrew Bailey said, “BoE's forecast suggests inflation will come down, fall quite sharply.”

Asked if rates might have peaked, says "we have changed the language we used." BoE’s Bailey also added, "Change in language reflects a turning in the corner but very early days."

On a different pate, BoE Chief Economist Huw Pill told Times Radio on Friday that it's important for the BoE to not do "too much" on monetary policy, per Reuters.

US-China tension is extra burden for Gold

Other than the United States data and monetary policy moves at the European Central Bank (ECB), as well as at the Bank of England (BoE), the latest geopolitical tension surrounding the US and China also exerts downside pressure on the Gold price.

“A US military fighter jet shot down a suspected Chinese spy balloon off the coast of South Carolina on Saturday, a week after it first entered US airspace and triggered a dramatic -- and public -- spying saga that worsened Sino-US relations,” said Reuters.

Federal Reserve Chair Jerome Powell’s speech, Sentiment data are the key

Looking forward, Gold traders should pay attention to Federal Reserve Chairman Jerome Powell’s speech and preliminary readings of the UoM Consumer Sentiment Index for February, as well as the University of Michigan's 5-year Consumer Inflation expectations, for fresh impulse. If Fed’s Powell manages to regain his hawkish bias, based on the recently firmer US data, the XAU/USD has a further downside to track.

Gold price technical analysis

Gold price broke key support lines stretched from November during the last week and pushed back the bullish bias, at least for now.

The downside expectations also take clues from the below 50 Relative Strength Index (RSI) line, placed at 40, as well as bearish signals from the Moving Average Convergence and Divergence (MACD) indicator.

That said, the XAU/USD declines to the 50-Day Moving Average (DMA), currently around $1,845, appear imminent. However, multiple tops marked during the last December near $1,825-23 could act as the last defense of the Gold buyers.

Alternatively, an upward-sloping trend line from November 23, previous support surrounding $1,878, guards immediate recovery of the Gold price. Following that, a three-month-old support-turned-resistance line could challenge the XAU/USD bulls near $1,925.

Overall, Gold price is likely to witness further downside but the trend reversal is far from sight.

Gold price: Daily chart

Trend: Further downside expected

-

23:10

EUR/USD retreats from 1.0800 as Fed pause bets fade post mammoth US NFP report

- EUR/USD has faced barricades around 1.0800 the risk-off impulse inspired by upbeat US NFP is still solid.

- The 10-year US Treasury yields have scaled up 3.51% again amid a rebound in US inflation projections.

- Higher US NFP might offset the impact of a decline in the employment cost index.

The EUR/USD pair has sensed selling interest after a pullback move to near the round-level resistance of 1.0800 in the early Asian session. The major currency pair has resumed its downside journey as the stronger-than-anticipated United States Nonfarm Payrolls (NFP) reports have dismantled the expectations of a pause in the interest rate escalation by the Federal Reserve (Fed) after reaching 4.50-4.75%. The street considered that a meaningful declining trend in the inflationary pressures is sufficient to pause interest rate hiking for a period of time to assess the impact of policy tightening till done.

S&P500 witnessed a massive sell-off a gigantic jump in the additions to the US labor force might force a rebound in inflation projections, portraying a risk-aversion theme. Three-day winning spree in the 500-stock basket terminated on expectations that further increases in interest rates would deepen recession fears ahead. The US Dollar Index (DXY) displayed a juggernaut rally to near 102.60 and is expected to continue its upside journey as mammoth employment generation has cleared that battle against inflation is far from over.

A significant jump in the US employment numbers weakened the demand for US government bonds, which led to a jump in the 10-year US Treasury yields above 3.51%.

The United States economy has added fresh 517K, extremely higher than the consensus of 185K and the former release of 260K. The Unemployment Rate was trimmed to a multi-decade low of 3.4% lower than the expectations and the prior release of 3.6% and 3.5% respectively. Apart, from that Average Hourly Earnings have dropped to 4.4% from 4.9% released earlier. A decline in earnings data might keep inflation projections in check as lower liquidity with households will not allow them to increase spending.

On the Eurozone front, investors are keeping an eye on Retail Sales data, which is scheduled for Monday. The contraction in the economic data is expected to trim to 2.7% from the prior contraction of 2.8%. A spree of contraction in consumer spending might trim projections for the Consumer Price Index (CPI), which will delight the European Central Bank (ECB) ahead.

-

23:01

Japan sounds out BoJ deputy Amamiya for central bank governor

The Nikkei reported that Japan's government has approached Bank of Japan Deputy Gov. Masayoshi Amamiya as a possible successor to central bank chief Haruhiko Kuroda while Tokyo prepares for the first change of leadership at the BOJ in a decade.

''Government and ruling coalition officials said the subject had been discussed with Amamiya. The 67-year-old career central banker is the architect of most BOJ policies under Kuroda.''

USD/JPY update

USD/JPY has popped and is targeting 13250 in the open with eyes on 132.80 and the 134.70s thereafter following Friday's strong US Nonfarm Payrolls report. The United States added 517,000 jobs in January, well more than the average analyst estimate for a 187,000-job rise. The robust increase showed the US economy continues to surge despite rising interest rates. the key here is that the data arrived at a time when markets were positioning for a Fed pivot.

-

22:37

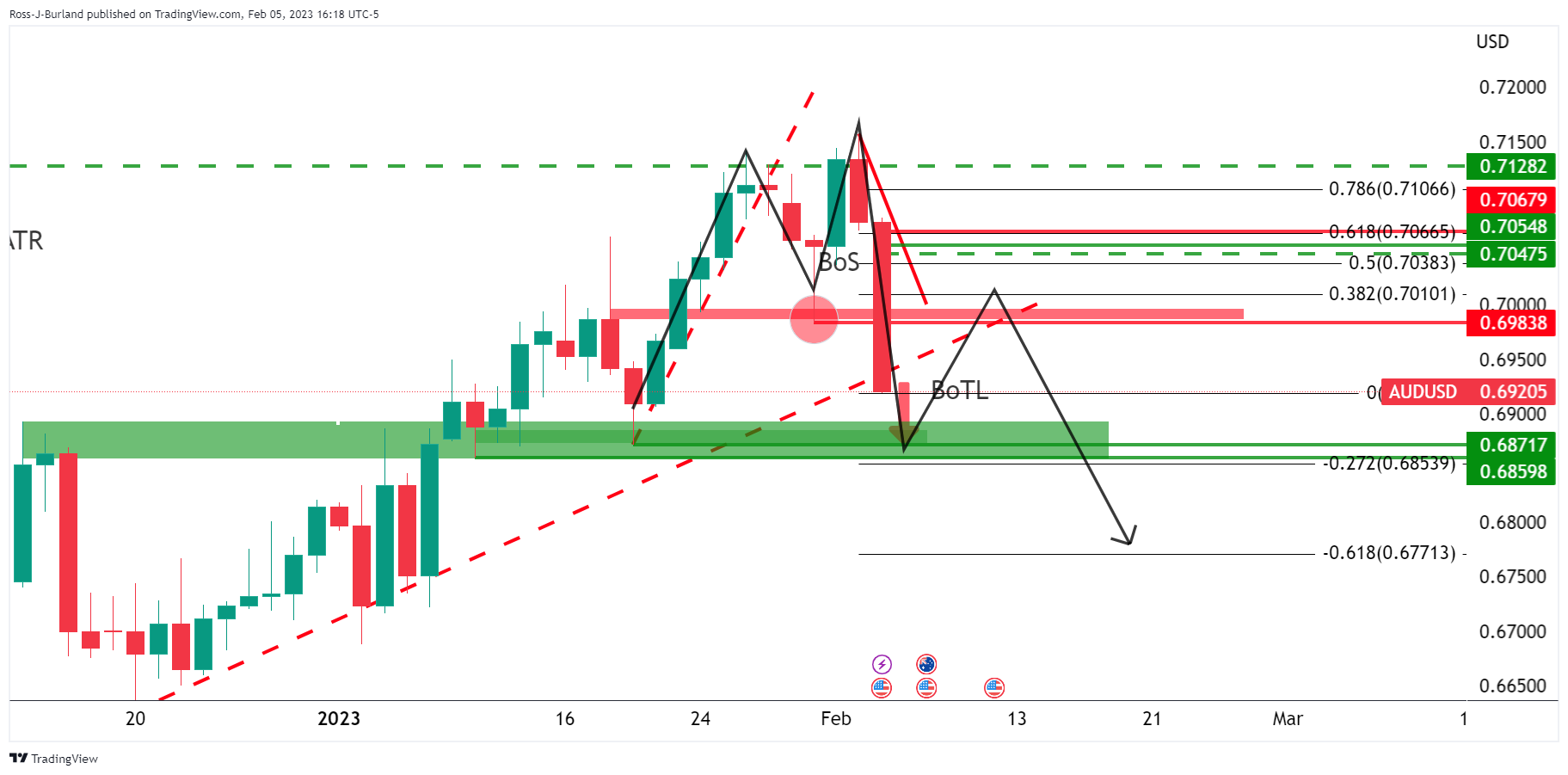

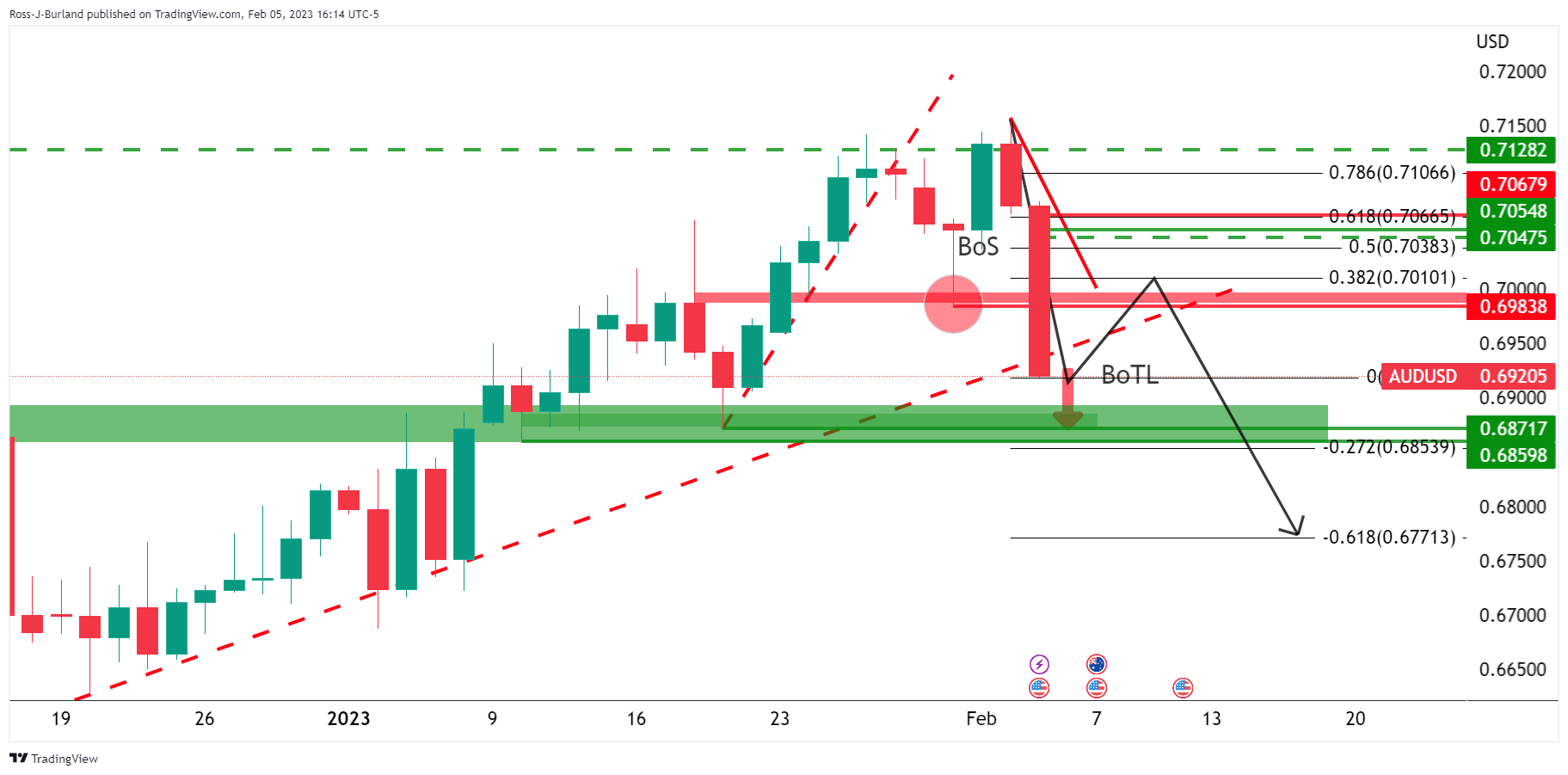

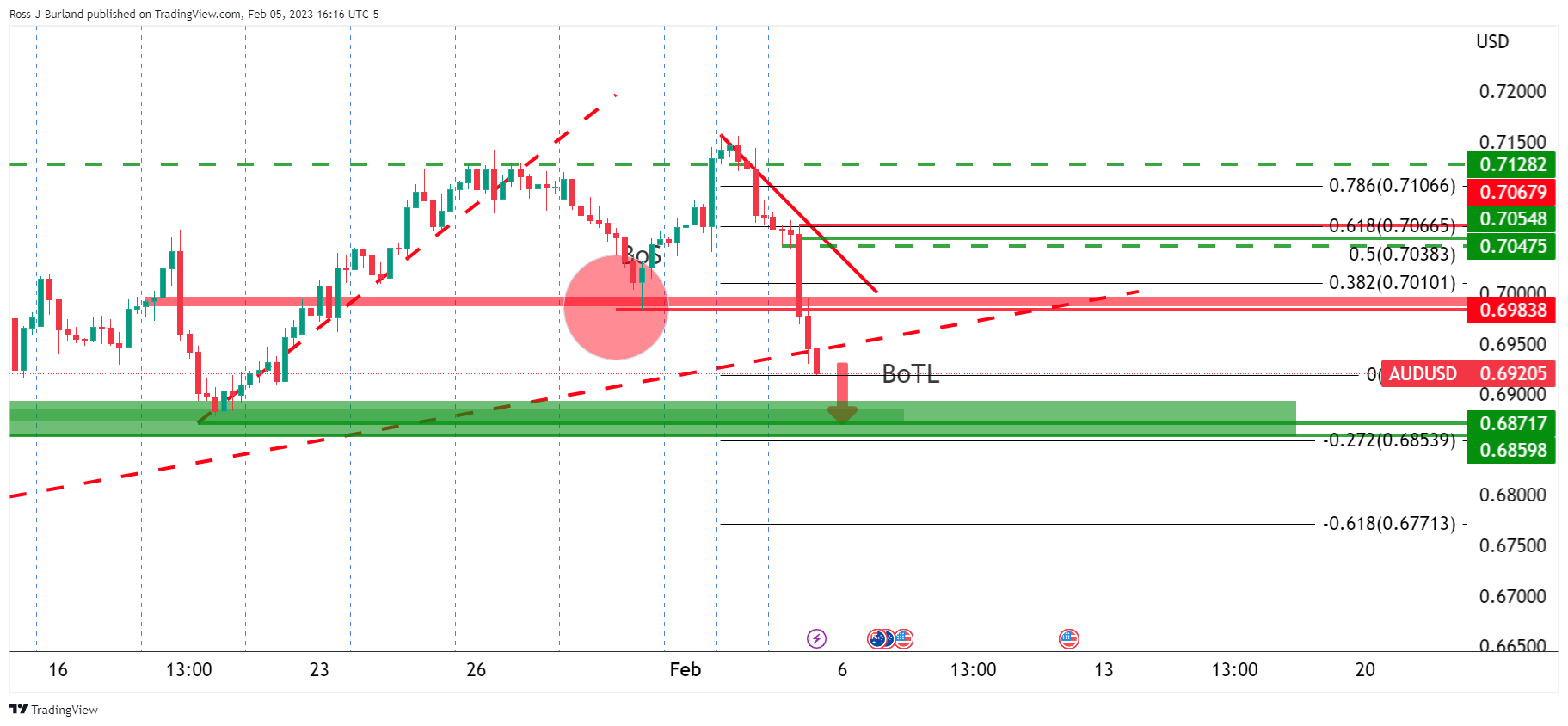

AUD/USD Price Analysis: Bears under a 78.6% target area ahead of RBA

- AUD/USD bears eye support structure for the open.

- Bulls look to 100 pips higher for a corrective opportunity.

AUD/USD sold off in a huge way at the end of last week and has broken critical breakout structures along the way as the following will illustrates. The price dropped to close below a 78.6% target area:

The culprit was outstanding results in the US jobs sector that took the market off guard that was backed up by some pretty impressive Services data as well.

The United States added 517,000 jobs in January, well more than the average analyst estimate for a 187,000-job rise. The robust increase showed the US economy continues to surge despite rising interest rates. the key here is that the data arrived at a time when markets were positioning for a Fed pivot. A more hawkish stance could now come back into play in terms of sentiment even after it raised interest rates by just 25 basis points on Wednesday, the smallest hike since it began tightening rates to slow inflation.

Meanwhile, the Aussie had been boosted by the re-opening of the Chinese economy as well as the surprising strength of Australia’s December inflation release that landed recently and had firmly put the risk of another 25 bp rate hike from the RBA on the table for February 7. ''Accelerating services inflation locks in a 25bps hike,'' analysts at TD Securities said. ''We forecast a follow-up 25bps hike in March taking the terminal to 3.6%.''

However, markets will be looking for the statement to open the door to pausing here. And this is a sangue into the charts below because we might have seen a high for the year so far if this were to be the case:

AUD/USD daily chart

The price is breaking the trendline.

However, we have an M=formation on the charts as illustrated above.

This could therefore lead to a bullish correction to test the neckline of the M-pattern with 0.70 eyed.

However, it can't be taken away from the bears that the momentum is to the downside and we could just see a continuation of the initial balance for the week and open as early prices suggest, downs some 50 pips to 0.6880 from Friday's 0.6929 close.

If this plays out in the official open in Syden, then taking 0.6870 as a floor, the 38.2% Fibo retracement on the daily comes in at around 0.6980:

-