Noticias del mercado

-

23:57

USD/CAD trades with mild losses near 1.4300 as tariff worries ease

- USD/CAD trades with mild negative bias around 1.4315 in Wednesday’s late Amercian session.

- Canada posts its first trade surplus in 10 months in December as exports continue to expand.

- US ISM Services PMI eased to 52.8 in January vs. 54.3 expected.

The USD/CAD pair posts modest losses near 1.4315 during the late American session on Wednesday. The Canadian Dollar (CAD) edges higher as Canada's trade balance shifted into surplus and US President Donald Trump delayed his orders to impose 25% tariffs on Canada for 30 days.

Canada in December reported its first trade surplus in ten months, with exports outpacing imports due to US businesses building up inventory ahead of potential tariffs, supporting the Loonie. Additionally, US tariffs provided relief from the looming trade war threat. Trump on Monday agreed to a 30-day pause on his tariff threats against Mexico and Canada as trading partners took steps to appease his concerns about border security and drug trafficking.

"Tariff worries are easing - for now, at least - which is allowing the CAD to stabilize,” said Shaun Osborne, chief currency strategist at Scotiabank. "Unless trade talks deteriorate significantly again, there is a chance that the USD-CAD peak reached Monday near 1.48 will represent a significant high-water mark for spot,” added Osborne.

Data released by the Institute for Supply Management (ISM) on Wednesday showed that the US Services Purchasing Managers' Index (PMI) declined to 52.8 in January from 54.0 (revised from 54.1) in December. This reading came in weaker than the estimation of 54.3.

The US Dollar (USD) weakens in an immediate reaction to the downbeat US economic data. The US labor market data on Friday will be in the spotlight. In case of the stronger-than-expected outcome, this could boost the Greenback against the CAD in the near term.Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

-

23:33

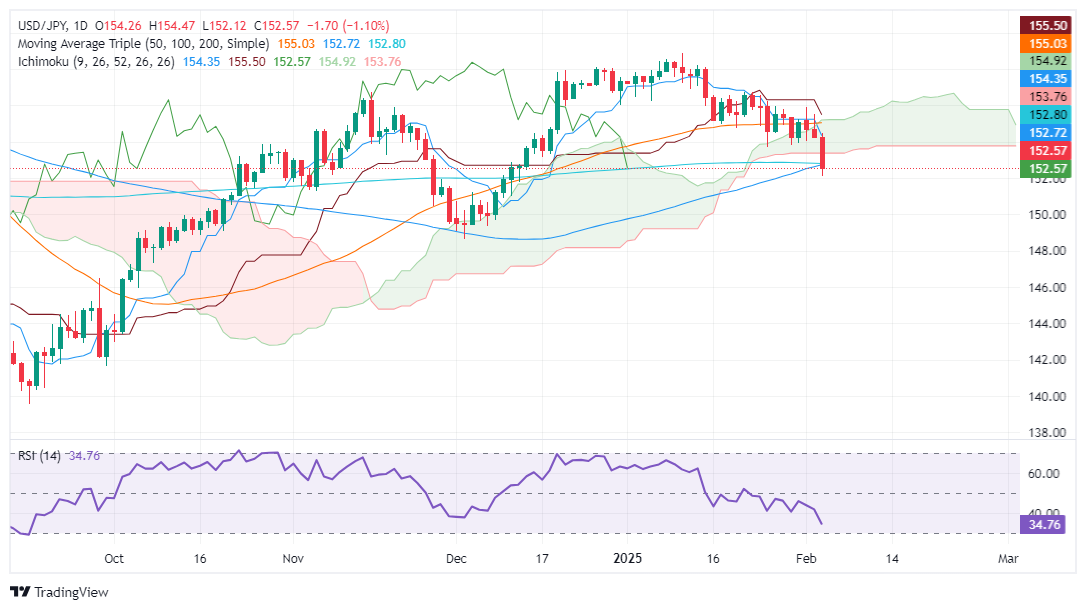

USD/JPY Price Forecast: Turns bearish, breaches Ichimoku Cloud and 200-DMA

- USD/JPY sinks 1.13%, falling sharply to 152.59 as it moves decisively below the 200-day SMA and Kumo.

- Potential recovery hinges on reclaiming the 153.00 level, with resistance near the Kumo's lower edge at 153.35/40.

- Continued downtrend could target longer-term supports at December lows of 149.36 and 148.65.

The USD/JPY plummeted 175 pips on Wednesday, posting losses of over 1.13% as the pair cleared the Ichimoku Cloud (Kumo). This cements the pair's downtrend, with the Japanese Yen (JPY) set to appreciate in the short term. At the time of writing, the pair trades at 152.59.

USD/JPY Price Forecast: Technical outlook

Bears stepped in on Wednesday, pushing the USD/JPY below the Kumo and breaching the 200-day Simple Moving Average (SMA) at 152.80. This has opened the door for further downside.

Despite this, a leg-up is on the cards, if buyers clear the 153.00 figure, which could pave the way to test the bottom of the Kumo at 153.35/40, offering sellers a better entry price. However, if it surpassed, the next resistance would be the 154.00 mark, followed by the February 5 high at 154.46.

If the downtrend continues, the USD/JPY first support would be the December 6 low of 149.36, followed by the December 3 low of 148.65.

USD/JPY Price Chart – Daily

Japanese Yen PRICE Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the Australian Dollar.

USD EUR GBP JPY CAD AUD NZD CHF USD 0.02% -0.01% -0.09% -0.00% 0.04% 0.04% 0.00% EUR -0.02% -0.03% -0.10% -0.02% 0.04% 0.03% -0.04% GBP 0.01% 0.03% -0.10% 0.01% 0.03% 0.07% 0.00% JPY 0.09% 0.10% 0.10% 0.07% 0.12% 0.10% 0.11% CAD 0.00% 0.02% -0.01% -0.07% 0.03% 0.05% 0.01% AUD -0.04% -0.04% -0.03% -0.12% -0.03% -0.01% -0.05% NZD -0.04% -0.03% -0.07% -0.10% -0.05% 0.01% -0.03% CHF -0.01% 0.04% -0.01% -0.11% -0.01% 0.05% 0.03% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

-

23:02

NZD/USD Price Analysis: Pair extends rally, approaching the 0.5700 mark

- NZD/USD advances nearly 0.70% on Wednesday, climbing to 0.5685.

- The pair maintains its position above the 20-day SMA, reinforcing bullish momentum.

- Bulls must conquer the 0.5700 area to confirm a recovery.

The NZD/USD pair extended its winning streak on Wednesday, posting a 0.67% gain to reach 0.5685. This upward move follows a breakout above the 20-day Simple Moving Average (SMA), which now acts as a key support level. The bullish sentiment appears to be strengthening, with the pair eyeing further gains toward the 0.5700 psychological threshold.

Technical indicators confirm the ongoing bullish trend. The Relative Strength Index (RSI) has surged to 58, indicating growing buying pressure, while the Moving Average Convergence Divergence (MACD) histogram continues to print rising green bars, reflecting a steady acceleration in momentum.

Looking ahead, NZD/USD faces an initial resistance zone at 0.5700, with a further upside target at 0.5735. On the downside, the 20-day SMA, currently near 0.5635, should act as the first line of support, followed by 0.5600 if a correction takes place. As long as the pair holds above the 20-day SMA, the short-term outlook remains in favor of the bulls.

NZD/USD daily chart

-

22:43

Gold price refreshes all-time high on risk aversion

- Gold price is poised to reach $2,900 amid an uncertain environment triggered by Trump’s policies.

- US businesses in the services industry are cooling, indicating an ongoing slowdown.

- Fed officials turned unease on Trump tariffs, putting inflation ahead of employment.

Gold price is set to extend its gains, rising more than 0.90% on Wednesday, sponsored by US Dollar weakness and falling US Treasury bond yields. The escalation of the China-US trade war keeps investors flocking to Gold’s safety appeal, and the XAU/USD trades near $2,870 as bulls target $2,900.

US President Donald Trump's rhetoric and policies continued to drive investors toward the golden metal, which is in unchartered territory. Traders are eyeing the $2,900 mark. Economic data revealed that the labor market remains solid after January’s ADP Employment Change report, which showed that private companies hired more people than foreseen.

However, not everything was positive on the data front. Business activity revealed by S&P Global and the Institute for Supply Management (ISM) showed that the services sector is cooling.

In the meantime, Federal Reserve (Fed) officials had crossed the wires and shown that they were uncertain about the impact of tariffs on inflation. Yet Chicago’s Fed President Austan Goolsbee said that ignoring tariffs' potential impact would be a mistake.

“If we see inflation rising or progress stalling in 2025, the Fed will be in the difficult position of trying to figure out if the inflation is coming from overheating or if it's coming from tariffs,” Goolsbee said.

Given the backdrop that Trump delayed 25% tariffs on Mexico and Canada for 30 days but levied 10% duties on China, uncertainty has kept investors uneasy about the potential disruption to global trade. Hence, they continued to seek the safety of the precious metals and ditched the Greenback.

Daily digest market movers: Gold remains underpinned by falling US yields

- The US Dollar Index (DXY), which tracks the buck’s performance versus a basket of six currencies, drops 0.38% and sits at 107.58 after hitting a three-week high at 109.88.

- The US 10-year Treasury bond yield plunges over nine basis points, down to 4.244%.

- US real yields, which correlate inversely to Bullion prices, dropped three basis points from 2.10% to 2.07%, a tailwind for XAU/USD.

- In January, the US ADP National Employment Change reported an increase in private sector jobs, rising from 176K to 183K and surpassing estimates of 150K.

- Concurrently, the ISM Services PMI for January registered at 52.9, slightly above forecasts of 52.8, although it decreased from December’s 54.0. Additionally, the S&P Global Services PMI decreased from 56.8 to 52.9 for the same period, still outperforming the anticipated 52.8.

- Money market fed funds rate futures are pricing in 52 basis points (bps) of easing by the Federal Reserve in 2025.

XAU/USD technical outlook: Gold prices set to challenge $2,900

After printing a new all-time high of $2,882, the yellow metal is set to challenge $2,890 ahead of the psychological $2,900 figure. Momentum remains bullish, and although the Relative Strength Index (RSI) has pushed well into overbought territory, it hasn’t reached the most extreme level above 80, which could pave the way for a mean-reversion trade.

On the other hand, if Gold tumbles below the $2,800 figure, the first support would be the January 27 swing low of $2,730, followed by $2,700.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

-

21:56

Australian Dollar climbs as mixed US data boosts risk sentiment

- Aussie nears 0.6300 amid cautious optimism on Wednesday.

- Investors eye possible February rate cut from RBA.

- Mid-tier US data came in mixed and weighed on the USD.

The Australian Dollar (AUD/USD) edges toward 0.6300, buoyed by mixed United States data that softened the Greenback and lifted broader risk assets. Nonetheless, anticipation of a dovish Reserve Bank of Australia (RBA) move next month tempers upside potential. Ongoing US-China trade tensions further cloud the outlook, restraining a more decisive rally in the Aussie.

Daily digest market movers: Aussie climbs amid mixed US data

- President Donald Trump’s additional tariff on Chinese imports remains in effect, prompting China’s plan for new countermeasures and an antitrust investigation into Alphabet.

- The United States has postponed a 25% duty on Canadian and Mexican imports for 30 days, contingent on border security commitments.

- The ADP Employment Change report surprised with 183,000 new private-sector jobs, surpassing market estimates of 150,000.

- Revised data from S&P Global show January Services at 52.9 and Composite at 52.7, both up from previous figures.

- The Institute for Supply Management’s Services PMI declined to 52.8, missing the 54.3 forecast, while the Prices Paid component dropped to 60.4.

- Markets are expecting that the Federal Reserve might hold rates steady in March, especially after mixed economic signals.

- On the other hand, speculation of a 25 bps cut by the RBA in February weighs on the Aussie since inflation remains subdued.

AUD/USD technical outlook: Pair flirts with key resistance near 0.6300

The pair’s advance above the 20-day Simple Moving Average (SMA) around 0.6230 highlights recovering momentum, with the Aussie rising 0.67% to near 0.6300. The Relative Strength Index (RSI) stands at 58, hinting at growing bullish pressure, while the Moving Average Convergence Divergence (MACD) histogram’s decreasing green bars suggest lingering caution. Although improved risk sentiment encourages short-term gains, market bets on a February RBA rate cut and persistent trade disputes could cap upside potential.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

-

21:09

Fed's Goolsbee: Can't ignore threats to supply chains like tariffs

Federal Reserve (Fed) Bank of Chicago President Austan Goolsbee noted on Wednesday that it is difficult for central banks to generally estimate the fallout of things like tariffs, and could complicate the Fed's ability to accomplish its task of bringing inflation down to 2%.

Key highlights

If inflation rises or progress stalls, US central bank will need to figure out if it's from overheating or tariffs.

Inflation has come down and is approaching Fed's 2% goal.

US has a strong economy and plausibly full employment.

Distinguishing the cause of any inflation will be critical for deciding when or even if the Fed should act.

COVID-19 pandemic experience shows supply chain disruptions can have a material impact on inflation.

Ignoring potential consequences of new threats to supply chains, like tariffs, would be a mistake.

Opinions differ widely on how much tariffs would get passed into prices, suppliers may have to eat the cost.

Tariffs this time may be broader and higher than in 2018; impact could be larger and longer-lasting.

-

20:49

Forex Today: The BoE is expected to ease its monetary stance

The US Dollar continued its slide on Wednesday, retesting multi-day lows against its peers amid a steady unravelling of positions and lingering uncertainty over Trump’s trade policies.

Here is what you need to know on Thursday, February 6:

The US Dollar Index (DXY) dropped for the third day in a row, extending the breakdown of the 108.00 support helped by lower yields across the board and intense risk-on mood. The usual Initial Jobless Claims are due, along with Challenger Job Cuts, and advanced Unit Labor Costs. In addition, the Fed’s Jefferson, Waller, and Daly are all due to speak.

EUR/USD rose to three-day peaks and looked to consolidate the recent breakout of the 1.0400 barrier. The HCOB Construction PMI is due in the euro area and Germany, seconded by Factory Orders in Germany, and Retail Sales in the bloc. Additionally, the ECB’s Nagel is expected to speak.

Another solid day saw GBP/USD advance to three-week highs past the 1.2500 hurdle in response to further weakness hurting the US Dollar. The BoE gathering will take centre stage, seconded by the S&P Global Construction PMI and the speech by Governor Bailey.

USD/JPY weakened further and put the 200-day SMA to the test near the 152.50 zone amid extra appreciation of the Japanese yen. The weekly Foreign Bond Investment figures will be published, will the BoJ’s Tamura will also speak.

AUD/USD climbed to multi-day highs, extending its weekly rebound to the boundaries of the key 0.6300 barrier. The Balance of Trade results for the month of December will be in the spotlight Down Under.

Prices of WTI resumed their downtrend, rapidly leaving behind Tuesday’s uptick and refocusing on the key $70.00 mark per barrel amid tariffs uncertainty.

Prices of Gold rose to an all-time peak near $2,880 per ounce troy on the back of safe haven demand and further selling pressure in the Greenback. Silver prices retreated marginally soon after hitting three-month highs around $32.50 per ounce.

-

20:35

Canadian Dollar continues to drift higher on Wednesday

- The Canadian Dollar added a thin 0.5% as the Greenback drifts lower.

- Upbeat US employment data is sending risk appetite higher.

- Meaningful Canadian data remains limited until Friday.

The Canadian Dollar (CAD) tested higher against the Greenback on Wednesday, chalking in a scant one-fifth of one percent gain following the early week’s sharp recovery from multi-decade lows. Us data dominated market headlines during the midweek market session, and a general improvement in trader risk appetite is stepping down on the US Dollar, giving the Loonie a leg up.

Economic data from Canada is strictly low-tier until Friday’s labor print. US Purchasing Managers Index (PMI) figures missed the market on Wednesday, but the key reading for US data came from ADP jobs change data, which showed a potential upswing in US net job gains. Traders are keeping a close eye on employment preview numbers in the run-up to Friday’s Nonfarm Payrolls (NFP) report.

Daily digest market movers: Canadian Dollar gains ground on sentiment uptick

- The Canadian Dollar gained a few points on easing Greenback flows.

- Canadian Trade Balance numbers for December rebounded, but less than expected. Markets overwhelmingly overlooked the data print.

- US ISM Services PMI survey results from January softened to 52.8 from a revised 54.0, missing the forecast 54.3.

- US ADP Employment Change swung higher to 183K, stepping over the previous revised 176K and beating the 150K forecast.

- Canadian labor figures are due on Friday, but market attention will be fully focused on US NFP jobs figures due at the same time.

Canadian Dollar price forecast

The Canadian Dollar (CAD) managed to eke out thin gains on Wednesday, dragging USD/CAD back down to the 50-day Exponential Moving Average (EMA) near the 1.4300 handle. Loonie traders remain aware that any gains on the CAD side are coming from generalized weakness in USD flows, but gains are gains and the Loonie has recovered solidly from 21-year lows set earlier this week.

The downside of the CAD’s rebound is USD/CAD is once again back into a congestion range as the pair grinds through a volatile but immovable sideways channel. Momentum is unlikely to meaningful break through the bottom near 1.4000, and the technical ceiling remains in place near 1.4500, albeit with some new holes.

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

-

19:37

Mexican Peso tumbles brushes aside broad US Dollar weakness across the board

- The Mexican Peso depreciates as USD/MXN climbs above 20.50 as trade tensions between the US and Mexico ease.

- Mixed investment data and anticipated Banxico rate cut further pressure on the Mexican Peso.

- The White House clarifies trade measures with Mexico, focusing on anti-drug efforts.

The Mexican Peso (MXN) dropped for the second straight day versus the US Dollar (USD) as trade war fears began to fade. Upbeat United States (US) jobs data pressured the Mexican currency, which has failed to capitalize on broad US Dollar weakness. The USD/MXN trades at 20.57, up by 0.45%.

Mexico’s economic docket revealed mixed Gross Fixed Investment figures in November. The data underscores the ongoing economic slowdown and undermines the already battered Mexican Peso, which could weaken further as the Banco de Mexico (Banxico) is expected to lower interest rates by at least 25 basis points from 10% to 9.75% on Thursday.

Although trade disputes between the US and Mexico have found common ground, USD/MXN traders should know that there is a 30-day pause and that tensions could arise throughout the end of February. Peter Navarro, a trade adviser for the White House, said that Canada misunderstood that it is not a “trade war” but a drug war.

Therefore, tariffs on Mexico will remain paused if the Government improves on its fight against drug cartels.

In the US, data keeps the Greenback on the back foot. The Institute for Supply Management (ISM) revealed that business activity in the US services sector cooled down in January. Other data showed that the jobs market remains solid as traders prepare for the release of US Nonfarm Payrolls numbers on Friday.

Daily digest market movers: Mexican Peso remains heavy amid broad USD weakness

- Gross Fixed Investment in Mexico rose 0.1% MoM in November, down from 0.3% in October, but exceeded forecasts of -0.1%. On a yearly basis, it improved from -2.6% contraction to -0.7%.

- Mexico’s Business Confidence in January showed signs of improvement, though business activity contracted, according to S&P Global. The manufacturing sector contracted for the seventh straight month in January, indicating that the economy is slowing down

- Banxico’s private economists survey showed that Mexico’s economy is expected to grow by 1% in 2025, down from 1.2% in the December survey. Inflation is expected to tick higher from 3.80% to 3.83%, while core prices are foreseen at 3.74%, up from 3.72%.

- Economists estimate the USD/MXN pair exchange rate to finish the year at 20.90, up from 20.53 in December, and estimate 150 basis points of easing from Banxico.

- The US ADP National Employment Change in January grew from 176K to 183K, exceeding estimates of 150K.

- The ISM Services PMI, for the same period as the ADP, rose 52.9 and exceeded forecasts of 52.8 but dipped compared to December’s 54.0.

- S&P Global featured Services PMI for January, which dipped from 56.8 to 52.9, better than the 52.8 expected.

- Money market fed funds rate futures are pricing in 52 basis points (bps) of easing by the Federal Reserve in 2025.

USD/MXN technical outlook: Mexican Peso weakens past 20.50 as buyers target 20.90

USD/MXN rose 0.265, recovering from a weekly low of 20.30 on Monday. Nevertheless, buyers' inability to achieve a daily close below the 50-day Simple Moving Average (SMA) of 20.41 sponsored the buck’s recovery to the detriment of the Peso.

For a bullish resumption, buyers must clear the previous year-to-date (YTD) peak of 20.90, ahead of the 21.00 figure. Further upside lies above the current YTD peak of 21.29.

Conversely, if sellers push USD/MXN below 20.30, it could fall to the 100-day SMA at 20.15. ahead of the 20.00 figure.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

-

19:29

US Dollar struggles as mixed data weighs on sentiment

- DXY remains under pressure, testing 107.35 support despite upbeat ADP and S&P Global PMI data.

- ISM Services PMI disappoints, signaling weaker than expected service sector growth and moderating price pressures.

- US 10-year yield rebounds, hovering around 4.40% after touching a yearly low.

The US Dollar Index (DXY), which measures the USD against a basket of currencies, struggled to recover losses on Wednesday and declined against most major peers. Despite stronger than expected ADP Employment and S&P Global PMI data, the ISM Services PMI fell short of forecasts, casting doubt on the strength of the US economy.

The Fed Sentiment Index, which previously sat at 130.00, has cooled off, signaling a less hawkish tone from policymakers. As a result, traders are reassessing the Federal Reserve’s (Fed) rate path, contributing to the DXY’s weak price action around 107.35 support.

Daily digest market movers: US Dollar struggles as mixed data weighs on sentiment

- ADP Employment Report showed that private sector employment jumped by 183,000 in January, exceeding the 150,000 forecast. Consumer-facing industries drove job creation, while manufacturing saw weaker gains.

- S&P Global PMI data revealed that the final readings for January saw minor upward revisions with the Services PMI at 52.9 (vs. 52.8 expected) and the Composite PMI at 52.7 (vs. 52.4 prior).

- ISM Services PMI: Disappointed at 52.8, missing the expected 54.3, while the Prices Paid index eased to 60.4 from 64.4, indicating softer inflationary pressures.

- All eyes are now on Friday Nonfarm Payrolls for January, which is seen printing a weak result that might add more weakness to the USD.

DXY technical outlook: Bears eye 107.00 support

The DXY's momentum indicators reflect a shift toward bearish traction. The Fed Sentiment Index cooling off from 130.00 aligns with weaker ISM data, weighing on the USD.

The Relative Strength Index (RSI) has dropped below 50, while the index has fallen beneath the 20-day Simple Moving Average (SMA) at 108.50. If downside pressure persists, the next key level to watch is the psychological support at 107.00.

Employment FAQs

Labor market conditions are a key element in assessing the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels because low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given their significance as a gauge of the health of the economy and their direct relationship to inflation.

-

18:56

Dow Jones Industrial Average grinds higher on Wednesday

- The Dow Jones added another 120 points during calm Wednesday markets.

- US ADP payroll figures point to net job gains that are better than expected.

- US ISM PMI figures came in softer than expected, but investors are shrugging off the bad print.

The Dow Jones Industrial Average (DJIA) climbed 120 points on Wednesday, bolstered by a general improvement in market sentiment. Firmer-than-expected prints in jobs preview data ahead of Friday’s upcoming Nonfarm Payrolls (NFP) report helped to keep markets buoyed, adding to gains as investors recover from an early-week plunge sparked by trade war threats from US President Donald Trump that came up empty for a third time in a row.

The ADP Employment Change amount from January exceeded expectations, suggesting 183K net new jobs were added according to payroll services provider ADP. The figure came in above the revised print of 176K from December, flouting the median market forecast of 150K.

US ISM Services Purchasing Managers Index (PMI) survey results missed the mark, easing to 52.8 from a revised 54.0, flubbing the market’s expected uptick to 54.3. The softer figure dampened sentiment somewhat, but only briefly as traders look for reasons to hit the buy button.

Dow Jones news

Most of the Dow Jones is testing into the high side as broad-market sentiment generally improves. Familiar market favorites Amgen (AMGN) and Nvidia (NVDA) are climbing on Wednesday, gaining 5.5% and 4.5%, respectively. Amgen beat the street on Q4 financial results, reported late on Tuesday, and the biotech firm is trading back above $300 per share.

Dow Jones price forecast

The Dow Jones is grinding its way back toward 44,800, with price action drifting into the top-end after kicking the trading week off just south of the 44,000 major price handle. The Dow is set to snap its latest pullback with a three-straight bull run, and the immediate target for bidders will be the 45,000 handle that lies ahead.

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

-

17:36

ECB's Centeno: May need to go below neutral to sustain inflation

European Central Bank (ECB) Governing Board Member Mario Centeno noted that deflationary pressures within the European economy are becoming a concern for policymakers. Dropping interest rates below neutral in order to stimulate the economy may be necessary, according to Centeno.

Key highlights

Undershooting 2% inflation is a risk if investment doesn't pick up.

We may need to go below neutral rate to sustain inflation at 2%.

Pretty clear, we need to keep downward trajectory of interest rates.

I'm ok with gradual rate cuts of 25 bps.

Europe must be united in face of potential tariffs; I see negotiations ahead.

-

17:13

EUR/USD Price Analysis: Pair extends gains above 20-day SMA, sustaining bullish momentum

- EUR/USD climbs to 1.0420 on Wednesday, extending its upward trend.

- The pair surges past the 20-day SMA, reinforcing a stronger short-term outlook.

The EUR/USD pair continued its bullish advance on Wednesday, rising by 0.39% to 1.0420 as buyers maintained control. With the latest price action, the pair has decisively climbed above the 20-day Simple Moving Average (SMA), a key resistance level that had previously limited upside attempts. This breakout signals a potential shift in sentiment, favoring further gains in the short term.

Momentum indicators align with the pair’s continued strength. The Relative Strength Index (RSI) has risen sharply to 53, signaling increased buying interest and a stronger bullish bias. Meanwhile, the Moving Average Convergence Divergence (MACD) histogram prints rising green bars, reflecting a sustained increase in momentum.

For EUR/USD to build on its recent gains, the next resistance levels to watch stand at 1.0450 and 1.0485. A break above these levels could open the door for a move toward 1.0520. On the downside, the 20-day SMA, now acting as support, is positioned near 1.0365, followed by a stronger support zone around 1.0350. Holding above the 20-day SMA will be key for the pair to sustain its positive trajectory.

EUR/USD daily chart

-

17:00

Russia Industrial Output climbed from previous 3.7% to 8.2% in December

-

16:30

United States EIA Crude Oil Stocks Change above forecasts (3.2M) in January 31: Actual (8.664M)

-

16:09

GBP/USD surges amid easing US trade tensions, ahead of BoE’s decision

- GBP/USD rises maintaining position above the 50-day SMA as market digests US tariff negotiations.

- US labor market shows strength with ADP employment figures surpassing expectations, spotlight on Nonfarm Payrolls.

- UK economic indicators show slight downturn, with market eyes on BoE's anticipated rate cut.

The Pound Sterling remains bid for the third consecutive day, edges up 0.34% as the GBP/USD trades at 1.2519 above the 50-day Simple Moving Average (SMA) at 1.2501.

GBP/USD ascends modestly, bolstered by positive market sentiment

The Greenback has erased most of its Monday’s gains, spurred by the US imposing tariffs on Mexico and Canada. However, both countries reached agreements with Washington. Therefore, investors who once seemed uncertain about US trade policies are confident that US President Donald Trump is using tariffs as a “tool” to negotiate with allies and adversaries.

Data has taken a backseat, with traders eyeing the release of US Nonfarm Payroll figures for January. Wednesday’s US docket featured ADP National Employment Change for January. The numbers exceeded estimates of 150K and rose by 183K, an indication of strength in the labor market.

At the same time, business activity continued to deteriorate. S&P Global featured Services PMI for January, which dipped from 56.8 to 52.9, better than the 52.8 expected. Up next, the Institute for Supply Management (ISM) will feature the Non-Manufacturing PMI, foreseen to increase from 54.1 to 54.3.

Across the pond, January's UK S&P Global Services PMI dipped from 51.1 to 50.8 as economic conditions worsened. Traders await the Bank of England’s (BoE) monetary policy decision on Thursday, poised to reduce rates by 25 basis points (bps) from 4.75% to 4.50%, according to Prime Market Terminal data.

Source: Prime Market Terminal

GBP/USD Price Forecast: Technical outlook

The GBP/USD cleared the January 27 peak of 1.2523, a strong resistance level, and reached a new four-week peak at 1.2549. Although bullish, a daily close above the former would open the door to challenge the year-to-date (YTD) high of 1.2575 and the 1.2600 figure.

If there is a failure to clear 1.2550, sellers could be set to push GBP/USD lower, with trades eyeing 1.2400. Further downside lies underneath the January 2 low of 1.2351, followed by the February 3 low of 1.2248.

British Pound PRICE Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the strongest against the US Dollar.

USD EUR GBP JPY CAD AUD NZD CHF USD -0.42% -0.25% -1.23% -0.20% -0.39% -0.66% -0.45% EUR 0.42% 0.19% -0.78% 0.22% 0.03% -0.25% -0.02% GBP 0.25% -0.19% -0.97% 0.04% -0.15% -0.42% -0.21% JPY 1.23% 0.78% 0.97% 1.04% 0.84% 0.56% 0.78% CAD 0.20% -0.22% -0.04% -1.04% -0.19% -0.45% -0.25% AUD 0.39% -0.03% 0.15% -0.84% 0.19% -0.27% -0.08% NZD 0.66% 0.25% 0.42% -0.56% 0.45% 0.27% 0.22% CHF 0.45% 0.02% 0.21% -0.78% 0.25% 0.08% -0.22% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

-

16:03

US ISM Services PMI declines to 52.8 in January vs. 54.3 expected

- US ISM Services PMI in the US declined slightly to begin the new year.

- The US Dollar Index stays deep in negative territory below 107.50.

The economic activity in the US service sector continued to expand in January, albeit at a softer pace than in December, with the ISM Services PMI declining to 52.8 from 54. This reading came in below the market expectation of 54.3.

Other details of the report showed that the Prices Paid Index, the inflation component, dropped to 60.4 from 64.4, while the Employment Index edged higher to 52.3 from 51.3.

Market reaction

The US Dollar stays under selling pressure following these data. At the time of press, the US Dollar Index was down 0.6% on the day at 107.35.

-

16:00

United States ISM Services PMI came in at 52.8 below forecasts (54.3) in January

-

16:00

United States ISM Services Employment Index rose from previous 51.4 to 52.3 in January

-

16:00

United States ISM Services New Orders Index fell from previous 54.2 to 51.3 in January

-

16:00

United States ISM Services Prices Paid: 60.4 (January) vs previous 64.4

-

15:45

United States S&P Global Composite PMI above forecasts (52.4) in January: Actual (52.7)

-

15:45

United States S&P Global Services PMI registered at 52.9 above expectations (52.8) in January

-

15:43

Silver Price Forecast: XAG/USD gives up gains after upbeat US ADP Employment data

- Silver price gives up a majority of intraday gains after the release of the upbeat US private employment data for January.

- Strong labor demand would force the Fed to maintain the status quo for longer.

- Investors expect the trade war would be limited between the US and China.

Silver price (XAG/USD) surrenders almost its entire intraday gains and falls back to near $32.00 in Wednesday’s North American session. The white metal faces selling pressure as the US Dollar (USD) attempts to gain ground on the back of upbeat United States (US) ADP Employment Change data for January. The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, finds buyers’ demand near 107.40 but is still over 0.4% down intraday.

The agency reported that 183K new workers were hired by the private sector last month, which were significantly higher than estimates of 150K, and the prior release of 176K, revised significantly higher from 122K.

Signs of strong labor demand would force Federal Reserve (Fed) officials to keep interest rates at their current levels for longer. Last week, Fed Chair Jerome Powell said that they will make monetary policy adjustments only after seeing “real progress in inflation or at least some weakness in labor market”. Technically, the Fed’s stance for keeping interest rates steady weighs on precious metals, such as Silver.

Meanwhile, investors are also doubting the Silver outlook amid receding fears of a lethal global trade war. Market participants expect the trade war to remain restricted between China and the US. Investors have interpreted President Donald trump’s tariff agenda as more a negotiating tool after his decision of suspending the order of imposing 25% tariffs on Canada and Mexico.

While 10% tariffs on China have come into effect from February, and in retaliation, China has also imposed levies on the US.

Silver technical analysis

Silver price strives to break above the immediate resistance of $32.50, which is plotted from the December 9 high. The outlook of the white metal remains bullish as the 20-day Exponential Moving Average (EMA) is sloping higher near $30.90.

The 14-day Relative Strength Index (RSI) oscillates in the 60.00-80.00 range, suggesting that the momentum is bullish.

Looking down, the upward-sloping trendline from the August 8 low of $26.45 will be the key support for the Silver price around $29.50. While, the October 31 high of $33.90 will be the key barrier.

Silver daily chart

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.

Silver is widely used in industry, particularly in sectors such as electronics or solar energy, as it has one of the highest electric conductivity of all metals – more than Copper and Gold. A surge in demand can increase prices, while a decline tends to lower them. Dynamics in the US, Chinese and Indian economies can also contribute to price swings: for the US and particularly China, their big industrial sectors use Silver in various processes; in India, consumers’ demand for the precious metal for jewellery also plays a key role in setting prices.

Silver prices tend to follow Gold's moves. When Gold prices rise, Silver typically follows suit, as their status as safe-haven assets is similar. The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, may help to determine the relative valuation between both metals. Some investors may consider a high ratio as an indicator that Silver is undervalued, or Gold is overvalued. On the contrary, a low ratio might suggest that Gold is undervalued relative to Silver.

-

14:48

NZD/USD Price Forecast: Posts fresh weekly high near 0.5700

- NZD/USD refreshes weekly high near 0.5700 as receding global trade war risks have improved the safe-haven demand.

- The USD strives to gain ground on the back of upbeat US ADP Employment data for January.

- The NZ economy will also face the consequences of the US-China trade war.

The NZD/USD pair posts a fresh weekly high near 0.5700 in Wednesday’s North American session. The Kiwi pair gains as the US Dollar (USD) has remained under pressure due to receding risks of a global trade war.

Investors expect the trade war to remain between the United States (US) and China as the latter has imposed tariffs on a few items from the US economy in retaliation to President Donald Trump’s decision of a 10% levy on all imports from China.

The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, refreshes weekly low to near 107.40. However, the Greenback has got some buying interest after the release of the United States (US) ADP Employment Change data, which showed that the private sector hired 183K workers in January, higher than estimates of 150K and the prior release of 176K, revised significantly higher from 122K.

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Canadian Dollar.

USD EUR GBP JPY CAD AUD NZD CHF USD -0.21% -0.26% -0.78% -0.19% -0.28% -0.51% -0.22% EUR 0.21% -0.05% -0.59% 0.02% -0.06% -0.29% -0.01% GBP 0.26% 0.05% -0.56% 0.07% -0.02% -0.25% 0.04% JPY 0.78% 0.59% 0.56% 0.61% 0.52% 0.27% 0.57% CAD 0.19% -0.02% -0.07% -0.61% -0.08% -0.32% -0.03% AUD 0.28% 0.06% 0.02% -0.52% 0.08% -0.23% 0.05% NZD 0.51% 0.29% 0.25% -0.27% 0.32% 0.23% 0.29% CHF 0.22% 0.01% -0.04% -0.57% 0.03% -0.05% -0.29% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Meanwhile, the outlook of the New Zealand Dollar (NZD) remains uncertain as the impact of a trade war between the US and China will also be borne by the New Zealand economy, being one of the leading trading partners of China.

On the monetary policy front, market participants expect the Reserve Bank of New Zealand (RBNZ) to continue reducing its cash rate to reduce deepening risks of inflation undershooting their target of 2%.

NZD/USD rebounds strongly from the support zone plotted around 0.5500 on a weekly timeframe. However, the outlook of the Kiwi pair is still bearish as the 20-week Exponential Moving Average (EMA) near 0.5800 is sloping downwards.

The 14-week Relative Strength Index (RSI) attempts to return inside the 40.00-60.00 range. A fresh bearish momentum would trigger if the RSI fails to do the same.

The Kiwi pair could decline to nears round-level supports of 0.5400 and 0.5300 if it breaks below the 13-year low of 0.5470.

On the flip side, a decisive break above the November 29 high of 0.5930 could drive the pair to the November 15 high of 0.5970 and the psychological resistance of 0.6000.

NZD/USD weekly chart

US-China Trade War FAQs

Generally speaking, a trade war is an economic conflict between two or more countries due to extreme protectionism on one end. It implies the creation of trade barriers, such as tariffs, which result in counter-barriers, escalating import costs, and hence the cost of living.

An economic conflict between the United States (US) and China began early in 2018, when President Donald Trump set trade barriers on China, claiming unfair commercial practices and intellectual property theft from the Asian giant. China took retaliatory action, imposing tariffs on multiple US goods, such as automobiles and soybeans. Tensions escalated until the two countries signed the US-China Phase One trade deal in January 2020. The agreement required structural reforms and other changes to China’s economic and trade regime and pretended to restore stability and trust between the two nations. However, the Coronavirus pandemic took the focus out of the conflict. Yet, it is worth mentioning that President Joe Biden, who took office after Trump, kept tariffs in place and even added some additional levies.

The return of Donald Trump to the White House as the 47th US President has sparked a fresh wave of tensions between the two countries. During the 2024 election campaign, Trump pledged to impose 60% tariffs on China once he returned to office, which he did on January 20, 2025. With Trump back, the US-China trade war is meant to resume where it was left, with tit-for-tat policies affecting the global economic landscape amid disruptions in global supply chains, resulting in a reduction in spending, particularly investment, and directly feeding into the Consumer Price Index inflation.

-

14:30

Canada International Merchandise Trade came in at $0.71B, below expectations ($0.75B) in December

-

14:30

Canada Imports rose from previous $66.43B to $68.76B in December

-

14:30

United States Goods and Services Trade Balance registered at $-98.4B, below expectations ($-96.6B) in December

-

14:30

United States Goods Trade Balance dipped from previous $-122.1B to $-123B in December

-

14:30

Canada Exports climbed from previous $66.11B to $69.46B in December

-

14:19

BoE expected to cut 25bps Thursday – Scotiabank

Final January UK PMI data were revised lower but both Services and Composite activity remained in expansion territory (at 50.8 and 50.6 respectively), Scotiabank's Chief FX Strategist Shaun Osborne notes.

GBP firmer through low 1.25s

"The Pound Sterling (GBP) gains are stretching a little ahead of most of its G10 peers on the day so far. Thursday’s BoE policy decision is widely expected to result in a 25bps cut and signs that more cuts are coming."

"The technical 'damage' to the pound inflicted by the weekend volatility in the USD was less severe than some of its peers and Cable’s improvement from Monday’s low suggests the strengthening in the pound’s technical tone that was developing in late January is getting back on track."

"Spot is trading at a minor new cycle high today, holding gains above its 40-day MA and bear trendline resistance in place since late September. Cable may push on to 1.26001/0. Support is 1.2490/95 and 1.2400/10."

-

14:19

US ADP private sector employment rises 183,000 in January vs. 150,000 expected

- Employment in the US private sector rose at a stronger pace than expected in January.

- US Dollar Index stays deep in negative territory near 107.50.

Private sector employment in the US rose 183,000 in December and annual pay was up 4.7% year-over-year, the Automatic Data Processing (ADP) reported on Wednesday. This reading followed the 176,000 (revised from 122,000) increase recorded in December and came in above the market expectation of 150,000.

Assessing the survey's findings, “we had a strong start to 2025 but it masked a dichotomy in the labor market,” said Nela Richardson, chief economist, ADP. “Consumer-facing industries drove hiring, while job growth was weaker in business services and production.”

Market reaction

The US Dollar Index struggles to stage a rebound after this data and was last seen losing 0.42% on the day at 107.55.

-

14:16

EUR stretches rebound to low 1.04s – Scotiabank

Weaker than expected PMIs from Spain, downward revisions to French data and a minor upgrade for the German Composite index saw the final Eurozone January Services index marked lower than the preliminary release at 51.3 (from 51.4) while the Composite Index was unchanged at 50.1, Scotiabank's Chief FX Strategist Shaun Osborne notes.

Tariff focus may soon shift to EU

"Details reflected firmer orders and new business but the outlook for sluggish growth and somewhat lower ECB interest rates remains. Monday’s 'hammer' low signal got some confirming support from additional gains in the EUR Tuesday and a further pick up in the EUR today is getting hard to ignore."

"The EUR has closed the gap on the short-term chart which was left open by the volatile market swings over the weekend which may pave the way for spot gains to extend to 1.0450/75 in the short run. Support is 1.0350/55."

-

14:15

United States ADP Employment Change above forecasts (150K) in January: Actual (183K)

-

14:14

CAD extends recovery to 1.43 area – Scotiabank

Tariff worries are easing—for now, at least—which is allowing the CAD to stabilize. The hefty swing lower in the USD from the early week peak may not extend much further for now but the sell-off is material, Scotiabank's Chief FX Strategist Shaun Osborne notes.

Firm USD support likely in mid/upper 1.42s

"Unless trade talks deteriorate significantly again, there is a chance that the USD/CAD peak reached Monday near 1.48 will represent a significant high-water mark for spot. Spot has priced in some tariff risk over the past few weeks (perhaps something in the region of 10%-plus) so investors could start to price that risk out again in the coming weeks *if* confidence grows that the US will not resort to any additional tariff action."

"That’s still a pretty big “if” though. Short-term spreads are about 50bps wider than early November, however, and the huge US/Canada interest rate differential will limit just how much of a rebound the CAD will see in the next few weeks at least. Spot fair value has eased to 1.4391, driving a minor, and unusual by recent standards, CAD overvaluation relative to its estimated equilibrium."

"CAD-positive signals are piling up on the charts. After Monday’s big, daily reversal signal, price action through the middle of the week reflects a potential bearish weekly reversal as well. Spot closed below its 40-day MA for the first time since early October yesterday. But there were a number of CAD-positive technical developments evident on the charts through late January which yielded no CAD improvement so markets may not buy into the idea of a big CAD rally too willingly just yet. The early January low at 1.4260 represents major support ahead of a push back to 1.40/1.41. Resistance is 1.4350/75."

-

14:11

USD slides as trade fears ease – Scotiabank

The USD continues to retreat, leaving the DXY more than 2% below Monday’s peak, Scotiabank's Chief FX Strategist Shaun Osborne notes.

USD trades broadly lower

"There is little fresh news to explain the US Dollar’s (USD) slide. Rather, investors are ditching long USD positions as trade war risks ease, at least for the moment. Global stocks are soft and major bond markets are firmer, with Treasurys underperforming slightly. Commodities are trading a little lower overall on the session. Generally, soft stocks, relatively firmer US yields and weak commodities would all tilt risks towards a somewhat stronger USD. But that’s not the case today."

"This is perhaps where the preponderance of long USD positioning evident in recent data helps explain price action. Also, technical signals are leaning quite obviously bearish for the DXY on the week so far, given the scale of the sell-off, but it’s hard to buy into the idea of a sharp USD fall with trade war risks clearly still seemingly high. Beyond recent developments, President Trump has yet to confront European allies with tariffs—something that he has promised is 'absolutely' coming—and investors should not get too comfortable with the appearance of Trump rolling over easily after minimal concessions from Mexico and Canada won temporary reprieves."

"More volatility seems very likely across markets in the coming weeks as the Trump team tries to reset the global trade picture. US data releases this morning include ADP jobs, final Services and Composite PMIs and the January Services ISM data. Fed speakers include Barkin, Goolsbee, Bowman and Jefferson."

-

14:06

Fed's Barkin: Still think policy rate is modestly restrictive

In an interview with Bloomberg on Wednesday, Richmond Federal Reserve President Thomas Barkin said that he still thinks the policy rate is modestly restrictive, per Reuters.

Key takeaways

"Looking forward, it is hard to know what specific tariffs are coming."

"Uncertainty goes beyond tariffs to immigration, regulation, other issues."

"Baseline data has been favorable."

"Expecting 12 month inflation numbers to come down nicely."

"Still leaning towards cuts this year."

"Would never take any policy move off the table, but hikes would require an economy overheating."

"No evidence of overheating at this point."

"Recalibrated to a place that is more sensible to where the economy is now."

"Bias is to see what happens and react to it."

Market reaction

The US Dollar stays under bearish pressure following these comments. At the time of press, the USD Index was down 0.48% on the day at 107.48.

-

13:41

US Dollar extends correction as global trade war fears ease

- The US Dollar slides lower against most major peers and looks for support on Wednesday.

- Economic data and risk premium unwind in the Greenback is triggering a correction.

- The US Dollar Index (DXY) falls below 108.00 and tests major support at 107.50.

The US Dollar Index (DXY), which tracks the performance of the US Dollar against six major currencies, dives lower and trades near 107.50 at the time of writing on Wednesday ahead of the US Purchase Managers Index (PMI) releases from both S&P Global and the Institute for Supply Management (ISM). Tensions in markets over the United States (US) President Donald Trump’s tariffs are unwinding now that levies on Mexico and Canada slapped over the weekend have been paused. This coincides with some US Dollar (USD) risk premium easing this Wednesday while Chinese traders head back to their desks after the Chinese New Year, with a surge in trading volumes.

As mentioned above, the economic data calendar shows a bulk of PMI releases on Wednesday. In Europe, the aggregate Eurozone, German, French, and Spanish PMI data have already been released earlier in the day, with final readings for January falling roughly in line to below their preliminary readings. In the US, S&P Global is set to release its reading in the early American session, with the ISM data specifically for the Services sector set to be issued just minutes thereafter.

Daily digest market movers: Data takes over from tariffs

- At 13:15 GMT, the ADP Employment Change for the private sector will be released. Expectations are for an increase of 150,000 new jobs in January compared to 122,000 previously.

- At 14:45 GMT, S&P Global will release its final reading for the Services and Composite PMI for January. No changes are expected from preliminary readings, with Services standing at 52.8 and the Composite at 52.4.

- At 15:00 GMT, the ISM will release its January reading for the Services sector:

- Services PMI is expected to tick up to 54.3 from 54.1 in December.

- The Prices Paid component has no forecast and was at 64.4 in the previous release.

- At 18:00 GMT, Chicago Fed President Austan Goolsbee delivers a speech on the current economy at the Chicago Fed's 31st Annual Automotive Insights Symposium, held at the Bank's Detroit Branch.

- Near 20:00 GMT, Federal Reserve Governor Michelle Bowman delivers a speech on Brief Economic Update and Bank Regulation at the 2025 Kansas Bankers Association Harold A. Stones Government Relations Conference.

- Equities are in deep red numbers, with Chinese traders returning to markets after the Chinese New Year holidays and having a lot to catch up with. Where losses in Europe are still contained, US futures are seeing the Nasdaq down by 1%.

- The CME FedWatch tool projects an 83.5% chance of the Fed keeping interest rates unchanged in the next meeting on March 19.

- The US 10-year yield is trading around 4.474%, just a sigh away from its yearly low of 4.46% seen on Monday.

- Gold hits another fresh all-time high above $2,875, with investors fleeing equities and bonds, heading into bullion.

US Dollar Index Technical Analysis: Safe haven excludes Dollar

The US Dollar Index (DXY) extends correction and dives lower on Wednesday. Traders and investors are heading to safe havens like Gold and the Swiss Franc (CHF). For once, the Greenback is not part of the rescue party, as risk-premium gained at the beginning of the week after President Trump slapped Mexico and Canada with tariffs over the weekend is starting to ease, no longer supporting an elevated US Dollar.

On the upside, the first barrier at 109.30 (July 14, 2022, high and rising trendline) was briefly surpassed but did not hold on Monday. Once that level is reclaimed, the next level to hit before advancing further remains at 110.79 (September 7, 2022, high).

On the downside, the October 3, 2023, high at 107.35 acts is trying to hold support and withstand the selling pressure this Wednesday. For now, that looks to be holding, though the Relative Strength Index (RSI) still has some room for the downside. Hence, look for 106.52 or even 105.89 as better levels.

US Dollar Index: Daily Chart

US-China Trade War FAQs

Generally speaking, a trade war is an economic conflict between two or more countries due to extreme protectionism on one end. It implies the creation of trade barriers, such as tariffs, which result in counter-barriers, escalating import costs, and hence the cost of living.

An economic conflict between the United States (US) and China began early in 2018, when President Donald Trump set trade barriers on China, claiming unfair commercial practices and intellectual property theft from the Asian giant. China took retaliatory action, imposing tariffs on multiple US goods, such as automobiles and soybeans. Tensions escalated until the two countries signed the US-China Phase One trade deal in January 2020. The agreement required structural reforms and other changes to China’s economic and trade regime and pretended to restore stability and trust between the two nations. However, the Coronavirus pandemic took the focus out of the conflict. Yet, it is worth mentioning that President Joe Biden, who took office after Trump, kept tariffs in place and even added some additional levies.

The return of Donald Trump to the White House as the 47th US President has sparked a fresh wave of tensions between the two countries. During the 2024 election campaign, Trump pledged to impose 60% tariffs on China once he returned to office, which he did on January 20, 2025. With Trump back, the US-China trade war is meant to resume where it was left, with tit-for-tat policies affecting the global economic landscape amid disruptions in global supply chains, resulting in a reduction in spending, particularly investment, and directly feeding into the Consumer Price Index inflation.

-

13:00

Brazil Industrial Output (YoY) came in at 1.6%, above expectations (1.1%) in December

-

13:00

Brazil Industrial Output (MoM) above expectations (-0.5%) in December: Actual (-0.3%)

-

13:00

United States MBA Mortgage Applications up to 2.2% in January 31 from previous -2%

-

12:47

AUD/USD soars to near 0.6300 as market sentiment turns cheerful

- AUD/USD rallies to near 0.6300 as the market sentiment becomes favorable for risk-sensitive assets.

- The risk-appetite of investors improves on the assumption that the scope of the trade war will be limited between the US and China.

- US-China trade war and RBA dovish bets would limit the Australian Dollar’s upside.

The AUD/USD pair surges to near the key level of 0.6300 in Wednesday’s European session. The Aussie pair strengthens as the risk appetite of investors has improved amid expectations that the trade war won’t be global and will be limited between the United States (US) and China.

S&P 500 futures are slightly down in European trading hours but have recovered their losses significantly. The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, declines sharply to near 107.50, the lowest level in more than a week.

Market participants are anticipating a lethal trade war between the US and China as the latter has retaliated with levies of 15% on coal and LNG and 10% for crude oil, farm equipment, and some autos against US President Donald Trump’s decision to impose 10% tariffs on them.

Though a steady market environment has offered some relief to the Australian Dollar (AUD), investors expect the relief would be short-term as Australia would be the victim of the US-China trade war, being a leading trading partner of China.

Apart from that, firm market expectations that the Reserve Bank of Australia (RBA) will pivot to policy normalization from the policy meeting on February 18 would also weigh on the Australian Dollar.

In Wednesday’s session, investors will focus on the US ADP Employment Change and the ISM Services Purchasing Managers’ Index (PMI) data for January.

US-China Trade War FAQs

Generally speaking, a trade war is an economic conflict between two or more countries due to extreme protectionism on one end. It implies the creation of trade barriers, such as tariffs, which result in counter-barriers, escalating import costs, and hence the cost of living.

An economic conflict between the United States (US) and China began early in 2018, when President Donald Trump set trade barriers on China, claiming unfair commercial practices and intellectual property theft from the Asian giant. China took retaliatory action, imposing tariffs on multiple US goods, such as automobiles and soybeans. Tensions escalated until the two countries signed the US-China Phase One trade deal in January 2020. The agreement required structural reforms and other changes to China’s economic and trade regime and pretended to restore stability and trust between the two nations. However, the Coronavirus pandemic took the focus out of the conflict. Yet, it is worth mentioning that President Joe Biden, who took office after Trump, kept tariffs in place and even added some additional levies.

The return of Donald Trump to the White House as the 47th US President has sparked a fresh wave of tensions between the two countries. During the 2024 election campaign, Trump pledged to impose 60% tariffs on China once he returned to office, which he did on January 20, 2025. With Trump back, the US-China trade war is meant to resume where it was left, with tit-for-tat policies affecting the global economic landscape amid disruptions in global supply chains, resulting in a reduction in spending, particularly investment, and directly feeding into the Consumer Price Index inflation.

-

12:31

India M3 Money Supply: 9.6% (January 20) vs previous 10.1%

-

12:22

Growth below expectations to remain a structural drag for CNH – Société Générale

USD/CNH is heavy near 7.2700. China’s private sector services growth traction unexpectedly slowed in January, Société Générale's FX analysts note.

Growth to remain well below expectations

"The Caixin services PMI fell to a four-month low at 51.0 (consensus: 52.4) vs. 52.2 in December. Earlier this week, the Caixin January manufacturing PMI showed the factory sector at a virtual standstill. China’s steady drip feed of stimulus has done little to improve the economy’s medium-term outlook, which we believe hinges crucially on boosting consumption spending."

"Until that has been accomplished, growth will remain well below expectations and a structural drag for CNH."

-

12:20

Markets continue to imply another RBNZ 50bps rate cut in February – Société Générale

NZD/USD is consolidating recent gains triggered by broad USD weakness, Société Générale's FX analysts note.

NZ-US 2-year bond yield spreads can further weigh on NZD/USD

"New Zealand labor market conditions further weakened in Q4, largely matching expectations. The unemployment rate rose three ticks to a four-year high at 5.1% (consensus & RBNZ: 5.1%). Employment dipped -0.1% q/q (consensus: -0.2%, RBNZ: -0.3%) vs. -0.6% in Q3 (revised down from -0.5%). Private sector wages grew 0.6% q/q (consensus: 0.6%, RBNZ: 0.5%) vs. 0.6% in Q3."