Noticias del mercado

-

23:43

GBP/USD Price Analysis: Downside looks favored as US PCE data supports more rates from Fed

- GBP/USD is looking vulnerable above 1.1940 amid the risk-off market mood.

- The USD Index is gathering strength to reclaim the immediate resistance of 105.00 amid hawkish Fed bets.

- Downward-sloping 20-and 50-period EMAs add to the downside filters.

The GBP/USD pair is displaying a volatility contraction around 1.1940 in the early Tokyo session. The Cable looks set to deliver further weakness as a fresh renewal in the Federal Reserve’s (Fed) hawkish bets has strengthened the US Dollar.

S&P500 futures witnessed immense pressure last week on hopes that more rates are in pipeline by the Fed as the United States inflation has turned persistent due to the strong labor market. The US Dollar Index (DXY) is gathering strength to reclaim the immediate resistance of 105.00. A jump in the monthly US core Personal Consumption Expenditure (PCE) price index by 0.6% sent 10-year US Treasury yields to near 3.95%.

GBP/USD is auctioning in an Inverted Flag chart pattern on an hourly scale. The chart pattern indicates a sheer consolidation that is followed by a breakdown. Usually, the consolidation phase of the chart pattern serves as an inventory adjustment in which those participants initiate shorts, which prefer to enter an auction after the establishment of a bearish bias.

It is worth noting that the Inverted Flag is forming around the horizontal support plotted from February 17 low at 1.1915. An inventory adjustment near crucial support indicates that bulls US Dollar bulls are gathering strength to discover more losses.

Downward-sloping 20-and 50-period Exponential Moving Averages (EMAs) at 1.2007 and 1.975 respectively, add to the downside filters.

The Relative Strength Index (RSI) (14) is oscillating in the 20.00-40.00 range, which indicates that the downside momentum is active.

A confident break below February 17 low at 1.1915 will drag the Cable firmly towards January 5 low at 1.1875 followed by the round-level support at 1.1800.

On the contrary, a move above February 24 high at 1.2040 will drive the asset towards February 23 high around 1.2080. A breach of the latter will expose the asset to February 21 high of around 1.2140.

GBP/USD hourly chart

-

23:38

UK PM Sunak may have obtained significant concessions in a looming Brexit deal – The Times

“UK Prime Minister Rishi Sunak has launched a private charm offensive to win around influential Conservative Brexiteers to his compromise Northern Ireland Brexit deal,” said The Times on Sunday.

“Sunak may have obtained significant concessions in a looming Brexit deal,” the news adds.

Also read: UK’s Raab: UK on cusp of new Brexit deal with EU over Northern Ireland

The news arrives ahead of the UK Sunak and European Commission President Ursula von der Leyen’s announcement of a new Brexit deal for Northern Ireland on Monday if the two can agree final details during lunchtime talks in Britain.

"The Prime Minister wants to ensure any deal fixes the practical problems on the ground, ensures trade flows freely within the whole of the UK, safeguards Northern Ireland’s place in our Union and returns sovereignty to the people of Northern Ireland," a statement from Sunak's office said per Reuters.

Key quotes

The prime minister has spent the past few days in one-to-one meetings with senior Brexiteer backbenchers taking them through the outline of the deal that he will announce today and trying to assuage their concerns.

Yesterday senior cabinet ministers were enlisted to ring around other members of the Tory parliamentary party to brief them on the key elements of the agreement before the formal announcement today.

GBP/USD tries to pushback bears

GBP/USD struggles to overcome the bearish bias as it picks up bids to 1.1950 by the press time.

Also read: GBP/USD Weekly Forecast: Pound Sterling bears eye a sustained move below 1.2000

-

23:22

UK’s Raab: UK on cusp of new Brexit deal with EU over Northern Ireland

“The UK ‘is on the cusp’ of securing a new Brexit deal on Northern Ireland,” British Deputy Prime minister Dominic Raab told BBC’s Laura Kuenssberg on Sunday.

More comments

The government had made ‘great progress’ negotiating with the European Union.

We're not there yet, but it would be a really important deal.

I think it would mark a paradigm shift first and foremost for the communities in Northern Ireland, but I think it would be a significant achievement.

If there are any new rules that would apply in relation to Northern Ireland, it must be right that there is a Northern Irish democratic check on that.

The UK wants to see a move away from checks on every consignment of goods coming into Northern Ireland from the rest of the UK.

GBP/USD stays pressured

GBP/USD remains depressed around 1.1940, following a three-day downtrend.

Also read: GBP/USD Weekly Forecast: Pound Sterling bears eye a sustained move below 1.2000

-

23:20

New Zealand Retail Sales ex Autos (QoQ) came in at -1.3% below forecasts (1.7%) in 4Q

-

23:16

New Zealand Retail Sales (QoQ) came in at -0.6% below forecasts (1.5%) in 4Q

-

23:15

Gold Price Forecast: Strong US Dollar signals XAU/USD fall towards sub-$1,800 zone

- Gold price remains pressured near two-month low, following consecutive four weekly declines.

- Strong United States data underpin US Dollar strength and weigh on XAU/USD.

- Firmer US Treasury bond yields, geopolitical fears also exert downside pressure on Gold price.

- More clues of US inflation will be eyed for short-term XAU/USD direction.

Gold price (XAU/USD) stays depressed at the lowest levels in two-months after declining in the last five consecutive days, as well as printing four-week south-run. That said, the yellow metal begins the week’s trading on a back foot around $1,810 as bears cheer strong US Dollar amid upbeat United States economics. Among the US data, the Federal Reserve (Fed) favored inflation gauge offered major blow to the XAU/USD price.

Gold price slumps as US Dollar jumps

Gold price dropped in the last four consecutive weeks, as well as five days in a row, as the US Dollar marked the biggest weekly jump since September 2022. That said, the US Dollar Index (DXY) marked four-week uptrend by the end of Friday, grinding near the highest levels in seven weeks of late, on strong United States data, especially relating to the inflation, underpinned hawkish Federal Reserve concerns.

On Friday, the Personal Consumption Expenditures (PCE) Price Index rose to 5.4% YoY versus 5.3% prior and 4.9% market forecasts. Further, the more relevant Core PCE Price Index, known as Fed’s favorite inflation gauge, rose to 4.7% YoY, compared 4.6% prior and analysts' forecast of 4.3%.

Prior to that, the second reading of the Gross Domestic Product Annualized, better known as Real GDP, eased to 2.7% for the fourth quarter (Q4) versus 2.9% first forecasts. Further, the Personal Consumption Expenditure (PCE) Price and Core PCE for the said period rose to 3.7% and 4.3% QoQ versus 3.2% and 3.9% respective first estimations.

Additionally, the Chicago Fed National Activity Index improved to 0.23 in January from -0.46 (revised), versus 0.03 analysts’ estimates. On the same line, Initial Jobless Claims also eased to 192K for the week ended on February 17 from 195K (revised) prior, compared to 200K expected.

Hawkish Federal Reserve talks also weigh on XAU/USD

While tracing upbeat US data, the Federal Reserve (Fed) officials were also hawkish and backed the US Dollar bulls, as well as weighing on the Gold price.

Cleveland Fed President Loretta Mester told CNBC on Friday that his funds rate was above the median in December and still thinks they need to be somewhat above 5%. The policymaker also added that inflation risks still tilted to the upside. On the same line, Federal Reserve Bank of Boston President Susan Collins said, “More rate hikes needed to deal with 'too high' inflation.” Furthermore, Governor Philip Jefferson said, “Wage growth in the US is running too high to be consistent with a timely and sustainable return to the Federal Reserve's 2% inflation objective.”

Not only the Fed talks but US Treasury Secretary Janet Yellen also backed inflation fears on the sideline of the Group of 20 (G20) meetings on Friday. “Inflation is coming down if you measure it on a 12-month basis, but still core inflation, which I think will fall further, remains higher than is consistent with 2%,” said the diplomat.

It’s worth noting that the hawkish United States data and hawkish Federal Reserve (Fed) talks underpin markets bets of higher Fed rates and weigh on the Gold price. As per the latest reading of the FEDWATCH tool, market players price a year-end effective fed funds rate at 5.3%, versus 5.1% signalled by the US central bank in its December meeting.

Geopolitical risks also please Gold bears

Other than the United States data and the hawkish Fed bets, geopolitical fears surrounding Russia and China also weigh on the Gold price. Recently, China released its 12-point peace plan but failed to gain accolades due to its ties with Russia.

Following this, “There cannot be any business as usual with Russia as long as this war continues,” Germany’s Finance Minister Christian Lindner said on the sidelines of the G20 finance ministers and central bank governors' meeting on Friday.

On the same line, European Commission President Ursula von der Leyen on Friday, “sanctions are sharply eroding Russia's economic base.” EU’s von der Leyen also stated that China has already taken side for Russia, they have to view their principles in that light.

More inflation clues eyed

Given the absence of the United States employment data, more signals for the US inflation will be eyed for near-term directions of the Gold price. Among them, the US Durable Goods Orders and ISM PMIs for February will be eyed closely. As most of the top-tier US releases have backed the inflation fears, the odds of the further XAU/USD declines can’t be ruled out.

Gold price technical analysis

Gold price remains inside a three-week-old bearish channel, poking late 2022 lows of late.

That said, the quote’s downside break of a one-week-old horizontal support line, around $1,817, joins the bearish signals from the Moving Average Convergence and Divergence (MACD) indicator to strength the downside bias.

However, lower line of the stated channel joins oversold conditions of the Relative Strength Index (RSI) line, placed at 14, hints at limited downside room, which in turn highlights $1,790 as the short-term key support.

In a case where the Gold price remains bearish past $1,790, multiple supports near $1,775-80 could challenge the XAU/USD sellers.

On the flip side, the aforementioned one-week-old horizontal support-turned-resistance guards the immediate Gold price upside near $1,818.

More importantly, the XAU/USD buyers remain off the table unless the precious metal remains below $1,834-35 resistance confluence, encompassing the 50-Simple Moving Average (SMA) and top line of the stated channel.

Gold price: Four-hour chart

Trend: Limited downside expected

-

23:06

EUR/USD eyes more downside below 1.0540 as US PCE propels hawkish Fed bets

- EUR/USD is expected to show further weakness below 1.0540 as US inflation has rebounded.

- Higher-than-anticipated US consumer spending resulted in an intense sell-off in the US equities.

- ECB Lagarde has reiterated that a 50 bps interest rate hike announcement is on the table.

The EUR/USD pair is juggling in a narrow range above 1.0540 in the early Asian session. The major currency pair is likely to show more weakness after surrendering the immediate support of 1.0540 ahead. The downside bias for the shared currency pair is escalating after a surprise rebound in the United States Personal Consumption Expenditure (PCE) Price Index. A revival in the households’ spending in January has propelled the expectations that the Federal Reserve (Fed) will continue hiking rates till summer.

Investors dumped US equities after a higher-than-anticipated jump in consumer spending in January fueled the risk of more policy tightening by Fed chair Jerome Powell in March. S&P500 futures settled the week with losses of around 2.60%, portraying a risk-aversion theme.

Fed’s preferred inflation tool reported a surprise jump to 4.7% vs. the consensus of 4.3% and the former release of 4.7% on an annual basis. Consumer spending has jumped by 0.6% in January against a jump of 0.4% recorded in December. A strong employment cost index due to the tight labor market has fueled consumer spending due to higher funds with households for disposal.

The US Dollar Index (DXY) looks set to reclaim the critical resistance of 105.00 ahead amid the risk-off market mood. Meanwhile, rising expectations of more policy tightening by the Fed sent US Treasury yields higher. The return provided on 10-year US government bonds scaled to near 3.95%.

On the Eurozone front, European Central Bank (ECB) President Christine Lagarde reiterated the need for further interest rate hike by 50 basis points (bps) in March. ECB Lagarde cited “More tightening will be required if fiscal cooperation is absent.” She further added ''There is every reason to believe that we will do another 50 basis points in March.”

-

22:59

NZD/USD crushed on a firmer US Dollar and hawkish US data

- NZD/USD sent to the backfoot on hawkish US data.

- US Dollar firms on US PCE and rate hike outlook.

NZD/USD was pressured at the end of last week due to a late surge in the USD as demand for the currency took off, sending the DXY index through 105 in the wake of a stronger-than-expected US core PCE deflator.

This was the Fed’s preferred measure of inflation, and the data companies a slew of prior inflationary data outcomes from the US calendar over the past few weeks.

The data's reacceleration has sent shockwaves through US markets, which analysts at ANZ Bank explained ''which are now pricing in a 5.4% peak in the fed funds rate and are in the process of pricing out cuts in H2 2023.''

The analysts said that they've discussed this potential for some time, and it is now materialising. ''But while it speaks to a stronger-than-otherwise USD, unlike in 2022, the Fed isn’t outpacing all other central banks, and locally, risks are now tilted towards the RBNZ also having more work to do,'' the analysts argued. ''That may in time make the NZD more resilient to USD strength than other currencies, but that wasn’t evident overnight.''

Meanwhile, New Zealand Retail Sales for the fourth quarter came in at -0.6% vs the prior 0.4%. For the year, it arrived at -4%.

-

22:50

ECB Lagarde: We will do another 50 basis points in March

More tightening will be required if fiscal cooperation is absent, Christine Lagarde, president of the European Central Bank said as reported in The Economic Times.

Largde said, ''there is every reason to believe that we will do another 50 basis points in March. After that, we will see. We are data dependent.''

She added, ''we will do more hikes if necessary to return inflation to our target of 2% in a timely manner. It will take what it will take. What I know is that we will return inflation to 2%. And we want to not only return it to 2%, but to keep it there sustainably.''

-

21:34

EU states have backed new sanctions on Russia

Politico reported that Western countries have ''slapped a new round of sanctions on Russia in the nick of time on Friday, striving to present a united front as the world marked the first anniversary of Vladimir Putin’s invasion of Ukraine.''

The article reported that ''in a show of solidarity with Kyiv, both the US and the UK imposed sanctions earlier on Friday.''

It has been confirmed today that EU states have backed new sanctions after a clash between Poland and Italy held up the process for days.

For a list of new sanctions, see here. Among them, they include about ''120 individuals and entities on the sanction list. New export restrictions have been introduced on sensitive dual-use and advanced technologies that contribute to Russia's military capabilities and technological enhancement, based on information received from Ukraine, our Member States and our partners. Today's package imposes import bans on the following Russian high-revenue goods:

- Bitumen and related materials like asphalt; and

- Synthetic rubber and carbon blacks.

Three Russian banks have been added to the list of entities subject to the asset freeze and the prohibition to make funds and economic resources available. Today's package imposes new reporting obligations on Russian Central Bank assets.''

-

21:23

Fed’s Mester: New inflation data affirms case for more hikes

Federal Reserve Bank of Cleveland leader Loretta Mester said it will take more tightening for the Fed to get inflation back to 2%.

Key comments

''Data shows inflation not yet on trend to get back sustainably to 2% target.''

''Strong inflation pressures are ‘still with us’.''

''Focus on 25bps versus 50bps misses bigger picture.''

''Will need to go above 5% funds rate, stay there for a while.''

''Needs to keep at rate hikes until inflation trend breaks lower.''

''Declines to say what size rate rises needed at March FOMC.''

''View on inflation and economy remain unchanged by latest data.''

US Dollar update

The US Dollar climbed to seven-week peaks on Friday after data showed US inflation accelerated while consumer spending rebounded last month.

A correction could be on the cards for the days ahead.

-

21:03

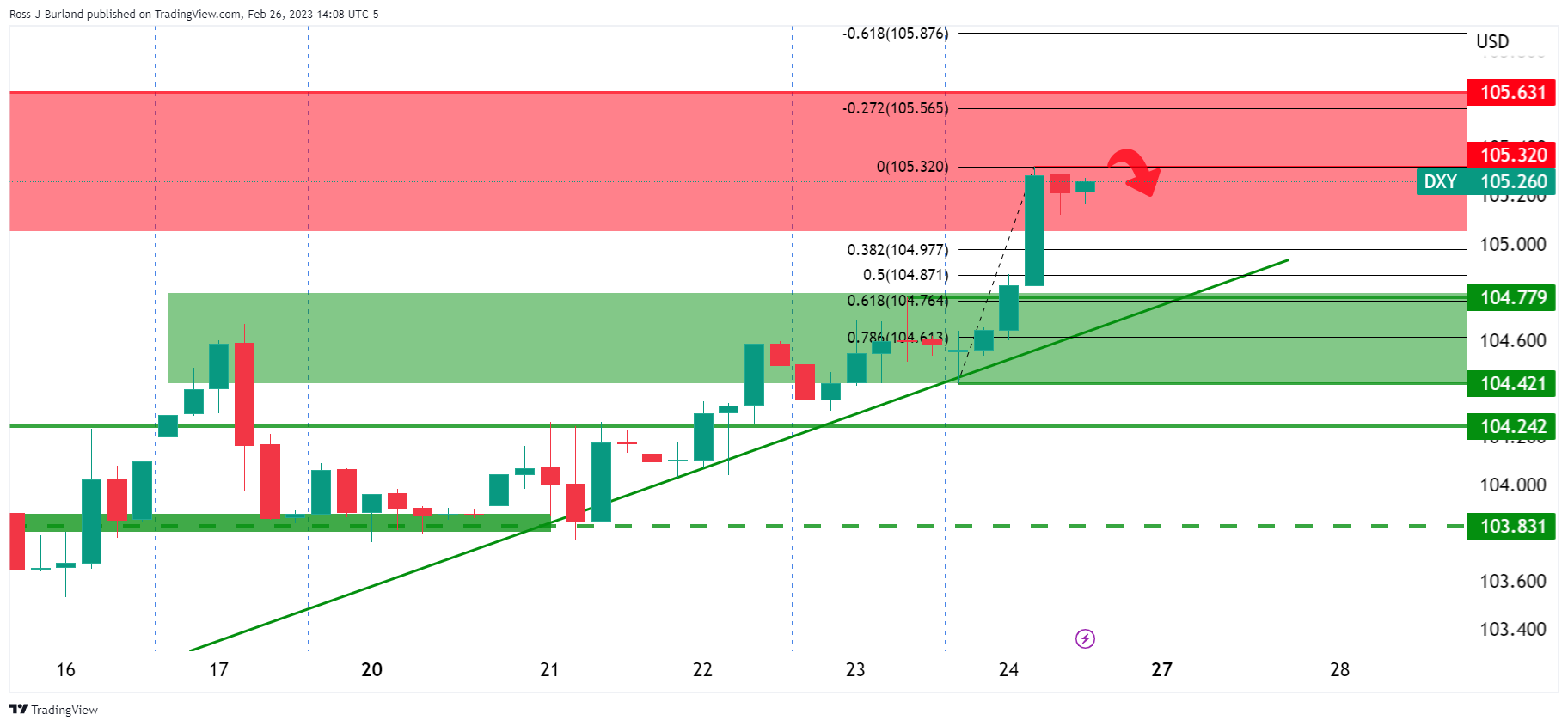

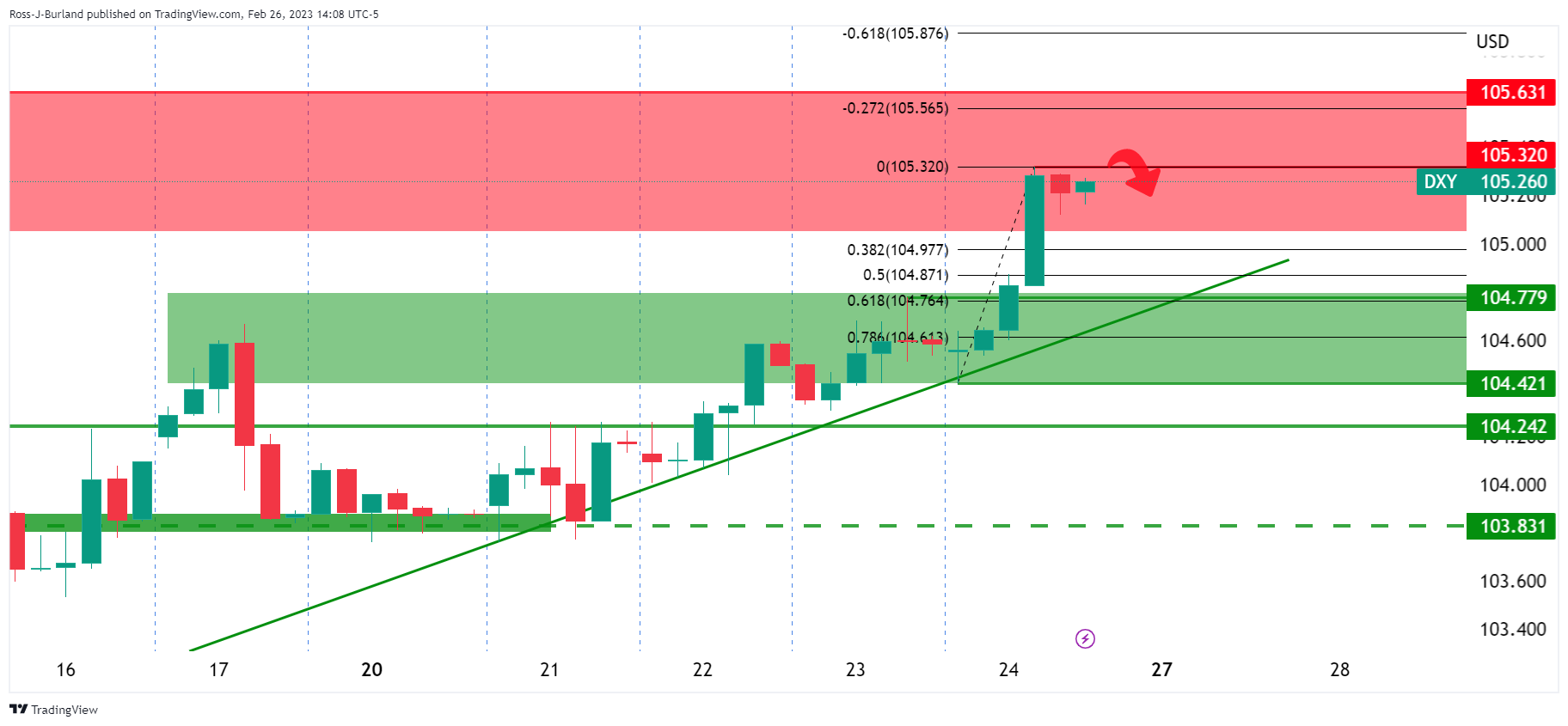

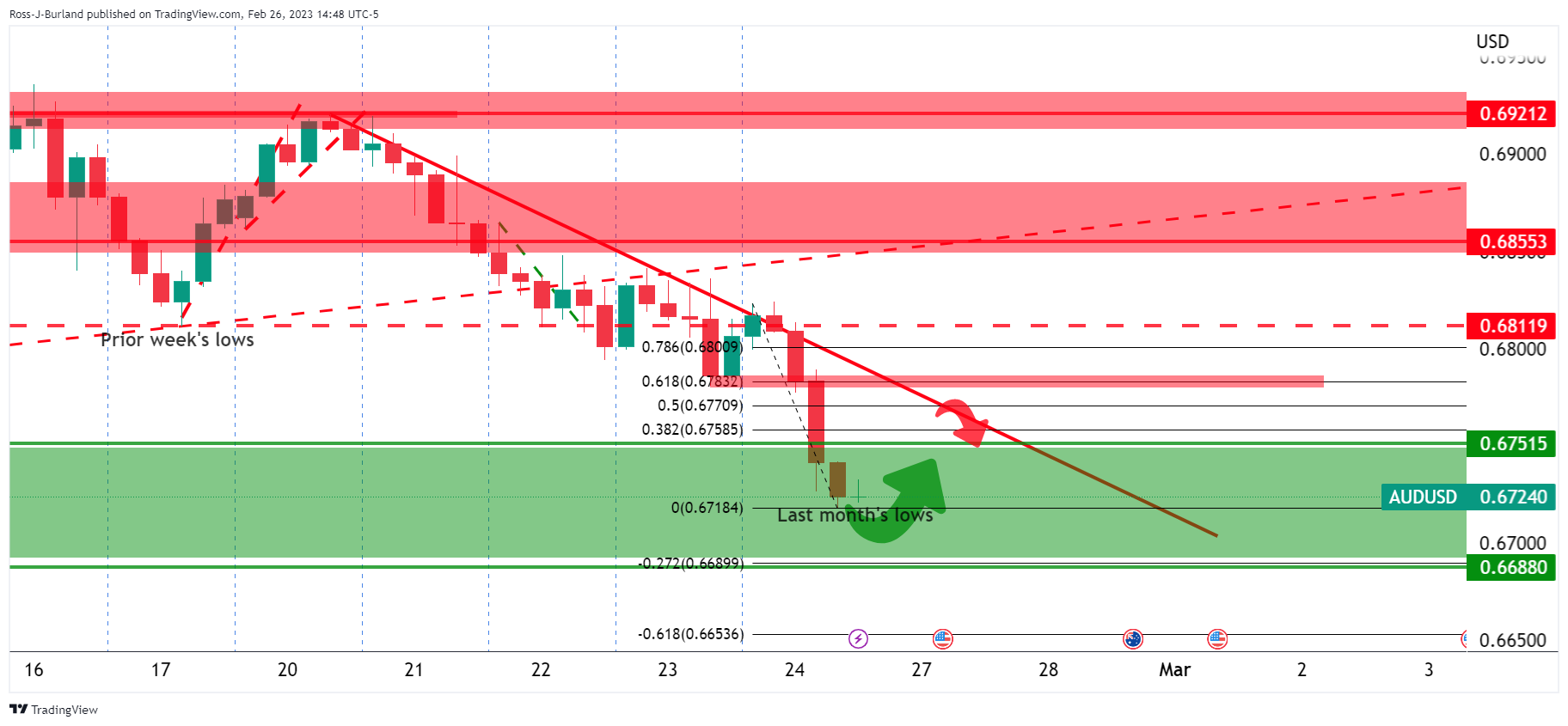

AUD/USD Price Analysis: Bulls eye a correction to test dynamic resistance

- AUD/USD bulls are lurking for the initial balance this week.

- US Dollar is sky-high and could be due for a correction.

The US Dollar climbed to seven-week peaks on Friday, leaving the Aussie on the backfoot after data showed US inflation accelerated while consumer spending rebounded last month.

With the Federal Reserve sentiment in the driving seat, the data will be key this week ahead of the second Friday of the month's US Nonfarm Payrolls. ISM surveys will follow last Friday's Personal Consumption Expenditures (PCE) price index, tracked by the Fed for monetary policy which rose 0.6% last month after gaining 0.2% in December. In the 12 months through January, the PCE price index accelerated 5.4% after rising 5.3% in December. This sent the US Dollar heavily bid as follows:

US Dollar charts

However, we are now in correction territory on the US Dollar which makes for a bullish outlook for the initial balance this week for AUD/USD.

AUD/USD H4 charts

AUD/USD, while potentially on course for a full test of last month's lows, is now in a correction zone and the trendline resistance is compelling for a target of liquidity.

-