Noticias del mercado

-

21:00

S&P 500 2,110.84 +6.34 +0.30 %, NASDAQ 4,991.36 +27.83 +0.56 %, Dow 18,240.92 +108.22 +0.60 %

-

18:00

European stocks closed: FTSE 100 6,935.07 -11.59 -0.17 %, CAC 40 4,917.5 -33.98 -0.69 %, DAX 11,409.69 +8.03 +0.07 %

-

18:00

European stocks close: most stocks closed lower despite positive inflation data from the Eurozone

Most stock indices closed lower despite positive inflation data from the Eurozone. The inflation in the Eurozone rose to an annual rate of -0.3% in February from -0.6% in January. Analysts had expected a 0.5% drop.

Eurozone's unemployment rate fell to 11.2% in January from 11.3% in December. Analysts had expected the unemployment rate to climb to 11.4%. December's figure was revised up from 11.4%.

Eurozone's final manufacturing purchasing managers' index (PMI) fell to 51.0 in February from a preliminary reading of 51.1. Analysts had expected the final index to remain unchanged at 51.1.

Germany's final manufacturing PMI increased to 51.1 in February from a preliminary reading of 50.9. Analysts had expected the final index to remain unchanged at 50.9.

France's final manufacturing PMI decreased to 47.6 in February from a preliminary reading of 47.7. Analysts had expected the final index to remain unchanged at 47.7.

Net lending to individuals in the U.K. increased by £2.4 billion in January, after a £2.1 billion gain in December, missing expectations for a rise by £2.8 billion. December's figure was revised down from a £2.2 billion increase.

The number of mortgages approvals in the U.K. increased by 60,786 in January, after a gain by 60,349 in December.

The U.K. manufacturing PMI increased to 54.1 in February from 53.1 in January. January's figure was revised up from 53.0.

The U.K. house price index decreased 0.1% in January, after a 0.3% rise in December.

On a yearly basis, the U.K. house price inflation fell to 5.7% in January from 6.8% in December.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,940.64 -6.02 -0.09 %

DAX 11,410.36 +8.70 +0.08 %

CAC 40 4,917.32 -34.16 -0.69 %

-

17:39

Foreign exchange market. American session: the U.S. dollar traded mixed to higher against the most major currencies after the mixed U.S. economic data

The U.S. dollar traded mixed to higher against the most major currencies after the mixed U.S. economic data. The Institute for Supply Management's manufacturing purchasing managers' index declined to 52.9 in February from 53.5 in January, missing expectations for a decline to 53.4. That was the lowest reading since January 2014.

A reading above 50 indicates expansion, below indicates contraction.

Most components of the index fell, showing a slow growth in the manufacturing sector.

Personal spending decreased 0.2% in January, after a 0.3% fall in December.

Consumer spending makes more than two-thirds of U.S. economic activity.

The decline was driven by lower gasoline prices.

Personal income climbed 0.3% in January, after a 0.3% rise in December.

The personal consumption expenditures (PCE) price index excluding food and energy rose 0.1% in January, in line with expectations, after a flat reading in December.

On a yearly basis, the PCE price index excluding food and index rose 1.3% in January, after a 1.3% increase in December.

The euro fell against the U.S. dollar. The inflation in the Eurozone rose to an annual rate of -0.3% in February from -0.6% in January. Analysts had expected a 0.5% drop.

Eurozone's unemployment rate fell to 11.2% in January from 11.3% in December. Analysts had expected the unemployment rate to climb to 11.4%. December's figure was revised up from 11.4%.

Eurozone's final manufacturing purchasing managers' index (PMI) fell to 51.0 in February from a preliminary reading of 51.1. Analysts had expected the final index to remain unchanged at 51.1.

Germany's final manufacturing PMI increased to 51.1 in February from a preliminary reading of 50.9. Analysts had expected the final index to remain unchanged at 50.9.

France's final manufacturing PMI decreased to 47.6 in February from a preliminary reading of 47.7. Analysts had expected the final index to remain unchanged at 47.7.

The British pound decreased against the U.S. dollar. Net lending to individuals in the U.K. increased by £2.4 billion in January, after a £2.1 billion gain in December, missing expectations for a rise by £2.8 billion. December's figure was revised down from a £2.2 billion increase.

The number of mortgages approvals in the U.K. increased by 60,786 in January, after a gain by 60,349 in December.

The U.K. manufacturing PMI increased to 54.1 in February from 53.1 in January. January's figure was revised up from 53.0.

The U.K. house price index decreased 0.1% in January, after a 0.3% rise in December.

On a yearly basis, the U.K. house price inflation fell to 5.7% in January from 6.8% in December.

The Canadian dollar traded lower against the U.S. dollar after the weaker-than-expected Canadian current account data. Canadian current account deficit widened to C$13.9 billion in the fourth quarter from a deficit of C$9.6 billion in the third quarter. The third quarter figure was revised down from a deficit of C$8.4 billion.

Analysts had expected a deficit of C$7.4 billion.

The decline was driven by lower exports as oil price dropped in the fourth quarter.

The Swiss franc traded lower against the U.S. dollar. The manufacturing purchasing managers' index in Switzerland dropped to 47.3 in February from 48.2 in January.

The New Zealand dollar traded lower against the U.S. dollar. In the overnight trading session, the kiwi declined against the greenback despite the overseas trade index from New Zealand. New Zealand's overseas trade index decreased 1.9% in the fourth quarter, after a 4.3% drop in the third quarter. The third quarter's figure was revised up from a 4.4 decline.

The Australian dollar traded mixed against the U.S. dollar. In the overnight trading session, the Aussie fell against the greenback after the mostly negative data from Australia. Company operating profits in Australia decreased 0.2% in the fourth quarter, missing expectations for a 9.7% rise.

Australia's new home sales climb 1.8% in January, after a 1.9% drop in December.

The AIG manufacturing index decreased to 45.4 in February from 40.0 in January.

The Japanese yen declined against the U.S. dollar. In the overnight trading session, the yen traded lower against the greenback. Japan's final manufacturing PMI climbed to 51.6 in February.

Capital spending in Japan climbed 2.8% in the fourth quarter, after a 5.5% in the third quarter.

-

16:35

ISM manufacturing purchasing managers’ index falls to 52.9 in February

The Institute for Supply Management released its manufacturing purchasing managers' index for the U.S. on Monday. The index declined to 52.9 in February from 53.5 in January, missing expectations for a decline to 53.4. That was the lowest reading since January 2014.

A reading above 50 indicates expansion, below indicates contraction.

Most components of the index fell, showing a slow growth in the manufacturing sector.

Energy industry was hurt by lower oil prices.

The new orders index fell to 52.5 in February from 52.9 in January.

The prices paid index remained unchanged at 35 in February. The employment index decreased to 51.4 from 54.1.

-

16:00

U.S.: ISM Manufacturing, February 52.9 (forecast 53.4)

-

16:00

U.S.: Construction Spending, m/m, January -1.1%

-

15:57

U.S. personal spending dropped 0.2% in January

The U.S. Commerce Department released personal spending and income figures on Monday. Personal spending decreased 0.2% in January, after a 0.3% fall in December.

Consumer spending makes more than two-thirds of U.S. economic activity.

The decline was driven by lower gasoline prices.

Personal income climbed 0.3% in January, after a 0.3% rise in December.

The personal consumption expenditures (PCE) price index excluding food and energy rose 0.1% in January, in line with expectations, after a flat reading in December.

On a yearly basis, the PCE price index excluding food and index rose 1.3% in January, after a 1.3% increase in December.

The PCE index are below the Fed's 2% inflation target. The PCE index is the Fed's preferred measure of inflation.

-

15:45

U.S.: Manufacturing PMI, February 55.1 (forecast 54.3)

-

15:36

U.S. Stocks open: Dow +0.18%, Nasdaq +0.27%, S&P +0.09%

-

15:12

Stocks before the bell

(company / ticker / price / change, % / volume)

International Business Machines Co...

IBM

162.00

+0.04%

5.9K

Ford Motor Co.

F

16.35

+0.06%

139.1K

Wal-Mart Stores Inc

WMT

83.99

+0.07%

27.9K

Nike

NKE

97.20

+0.08%

3.1K

Intel Corp

INTC

33.28

+0.09%

35.9K

Boeing Co

BA

151.00

+0.10%

10.7K

Walt Disney Co

DIS

104.25

+0.16%

1.1K

Home Depot Inc

HD

115.00

+0.22%

3.4K

Google Inc.

GOOG

560.00

+0.29%

2.2K

Procter & Gamble Co

PG

85.39

+0.31%

11.8K

Facebook, Inc.

FB

79.25

+0.35%

4.0K

Twitter, Inc., NYSE

TWTR

48.25

+0.35%

31.4K

American Express Co

AXP

81.90

+0.38%

44.7K

General Motors Company, NYSE

GM

37.45

+0.38%

0.1K

Apple Inc.

AAPL

128.98

+0.40%

337.6K

ALCOA INC.

AA

14.85

+0.41%

96.3K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

21.74

+0.51%

35.6K

Hewlett-Packard Co.

HPQ

35.14

+0.86%

68.7K

Citigroup Inc., NYSE

C

52.88

+0.88%

71.8K

Barrick Gold Corporation, NYSE

ABX

13.14

+0.92%

28.3K

Visa

V

275.25

+1.45%

38.3K

3M Co

MMM

168.65

0.00%

0.7K

Caterpillar Inc

CAT

82.90

0.00%

5.7K

E. I. du Pont de Nemours and Co

DD

77.85

0.00%

31.7K

Johnson & Johnson

JNJ

102.51

0.00%

2.9K

McDonald's Corp

MCD

98.90

0.00%

50.6K

Pfizer Inc

PFE

34.32

0.00%

77.0K

United Technologies Corp

UTX

121.91

0.00%

28.4K

Verizon Communications Inc

VZ

49.45

0.00%

3.8K

Deere & Company, NYSE

DE

90.60

0.00%

19.7K

International Paper Company

IP

56.41

0.00%

20.1K

ALTRIA GROUP INC.

MO

56.29

0.00%

34.5K

Starbucks Corporation, NASDAQ

SBUX

93.49

0.00%

24.9K

Amazon.com Inc., NASDAQ

AMZN

380.00

-0.04%

1.7K

Merck & Co Inc

MRK

58.51

-0.05%

49.9K

AT&T Inc

T

34.53

-0.09%

80.1K

General Electric Co

GE

25.96

-0.12%

12.5K

AMERICAN INTERNATIONAL GROUP

AIG

55.25

-0.14%

0.1K

Microsoft Corp

MSFT

43.77

-0.18%

48.6K

Chevron Corp

CVX

106.46

-0.21%

1.8K

The Coca-Cola Co

KO

43.21

-0.21%

48.1K

Yahoo! Inc., NASDAQ

YHOO

44.18

-0.23%

4.3K

HONEYWELL INTERNATIONAL INC.

HON

102.53

-0.24%

19.9K

JPMorgan Chase and Co

JPM

61.11

-0.28%

6.1K

Exxon Mobil Corp

XOM

88.26

-0.32%

3.3K

Tesla Motors, Inc., NASDAQ

TSLA

202.51

-0.41%

10.6K

Goldman Sachs

GS

189.00

-0.42%

1.7K

Yandex N.V., NASDAQ

YNDX

16.34

-0.67%

0.9K

UnitedHealth Group Inc

UNH

112.78

-0.75%

41.6K

-

15:08

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

IBM downgraded to Underweight from Neutral at Atlantic Equities, target $140

Other:

Twitter (TWTR) initiated with a Buy at Axiom Capital, target $60

-

15:07

Canadian current account deficit widened to C$13.9 billion in the fourth quarter

Statistics Canada released current account data on Monday. Canadian current account deficit widened to C$13.9 billion in the fourth quarter from a deficit of C$9.6 billion in the third quarter. The third quarter figure was revised down from a deficit of C$8.4 billion.

Analysts had expected a deficit of C$7.4 billion.

The decline was driven by lower exports as oil price dropped in the fourth quarter.

-

14:45

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1000(E909mn), $1.1200(E673mn), $1.1300(E594mn), $1.1320-25(E908mn), $1.1340(E415mn)

USD/JPY: Y117.50($650mn), Y118.00($1.0bn), Y118.90($1.7bn), Y120.00($1.57bn), Y121.50($700mn)

GBP/USD: $1.5500(Gbp311mn)

AUD/USD: $0.7750(A$520mn), $0.7800(A$489mn), $0.7910(A$747mn)

-

14:31

U.S.: Personal Income, m/m, January +0.3%

-

14:31

U.S.: Personal spending , January -0.2%

-

14:31

U.S.: PCE price index ex food, energy, m/m, January +0.1% (forecast +0.1%)

-

14:31

U.S.: PCE price index ex food, energy, Y/Y, January +1.3%

-

14:30

Canada: Current Account, bln, Quarter IV -13.9 (forecast -7.4)

-

14:05

Foreign exchange market. European session: the euro traded higher against the U.S. dollar after the positive inflation data from the Eurozone

Economic calendar (GMT0):

00:00 Australia HIA New Home Sales, m/m January -1.9% +1.8%

00:30 Australia Company Operating Profits Quarter IV +0.4% Revised From +0.5% +0.7% -0.2%

01:35 Japan Manufacturing PMI (Finally) February 51.5 51.5 51.6

01:45 China HSBC Manufacturing PMI (Finally) February 50.1 50.1 50.7

05:30 Australia Commodity Prices, Y/Y February -19.2% Revised From -20.4% -20.6%

07:00 United Kingdom Nationwide house price index February +0.3% -0.1%

07:00 United Kingdom Nationwide house price index, y/y February +6.8% +5.7%

08:30 Switzerland Manufacturing PMI February 48.2 47.3

08:50 France Manufacturing PMI (Finally) February 47.7 47.7 47.6

08:55 Germany Manufacturing PMI (Finally) February 50.9 50.9 51.1

09:00 Eurozone Manufacturing PMI (Finally) February 51.1 51.1 51.0

09:30 United Kingdom Mortgage Approvals January 60.3 61.0 60.7

09:30 United Kingdom Purchasing Manager Index Manufacturing February 53.1 Revised From 53.0 54.1

09:30 United Kingdom Net Lending to Individuals, bln January 2.1 2.8 2.4

10:00 Eurozone Unemployment Rate January 11.3% Revised From 11.4% 11.4% 11.2%

10:00 Eurozone Harmonized CPI, Y/Y (Preliminary) February -0.6% -0.5% -0.3%

The U.S. dollar traded mixed against the most major currencies ahead the U.S. economic data. The ISM manufacturing purchasing managers' index is expected to decline to 53.4 in February from 53.5 in January.

The euro traded higher against the U.S. dollar after the positive inflation data from the Eurozone. The inflation in the Eurozone rose to an annual rate of -0.3% in February from -0.6% in January. Analysts had expected a 0.5% drop.

Eurozone's unemployment rate fell to 11.2% in January from 11.3% in December. Analysts had expected the unemployment rate to climb to 11.4%. December's figure was revised up from 11.4%.

Eurozone's final manufacturing purchasing managers' index (PMI) fell to 51.0 in February from a preliminary reading of 51.1. Analysts had expected the final index to remain unchanged at 51.1.

Germany's final manufacturing PMI increased to 51.1 in February from a preliminary reading of 50.9. Analysts had expected the final index to remain unchanged at 50.9.

France's final manufacturing PMI decreased to 47.6 in February from a preliminary reading of 47.7. Analysts had expected the final index to remain unchanged at 47.7.

The British pound traded lower against the U.S. dollar after the mostly negative economic data from the U.K. Net lending to individuals in the U.K. increased by £2.4 billion in January, after a £2.1 billion gain in December, missing expectations for a rise by £2.8 billion. December's figure was revised down from a £2.2 billion increase.

The number of mortgages approvals in the U.K. increased by 60,786 in January, after a gain by 60,349 in December.

The U.K. manufacturing PMI increased to 54.1 in February from 53.1 in January. January's figure was revised up from 53.0.

The U.K. house price index decreased 0.1% in January, after a 0.3% rise in December.

On a yearly basis, the U.K. house price inflation fell to 5.7% in January from 6.8% in December.

The Canadian dollar traded slightly higher against the U.S. dollar ahead of Canadian current account data. Canadian current account deficit is expected to narrow to C$7.4 billion in the fourth quarter from a deficit of C$8.4 billion in the third quarter.

EUR/USD: the currency pair rose to $1.1240

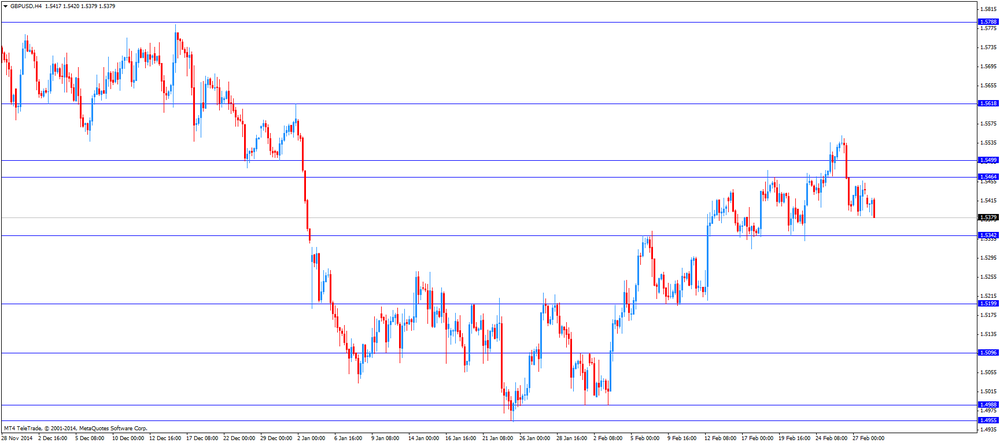

GBP/USD: the currency pair declined to $1.5379

USD/JPY: the currency pair fell to Y119.66

The most important news that are expected (GMT0):

13:30 Canada Current Account, bln Quarter IV -8.4 -7.4

13:30 U.S. Personal Income, m/m January +0.3%

13:30 U.S. Personal spending January -0.3%

13:30 U.S. PCE price index ex food, energy, m/m January 0.0% +0.1%

13:30 U.S. PCE price index ex food, energy, Y/Y January +1.3%

15:00 U.S. ISM Manufacturing February 53.5 53.4

-

14:01

Orders

EUR/USD

Offers 1.1245 1.1260 1.1285 1.1300 1.1325 1.1350-60 1.1385

Bids 1.1150 1.1130 1.1100

GBP/USD

Offers 1.5455 1.5475-80 1.5500 1.5530 1.5550-55 1.5580 1.5600

Bids 1.5375-80 1.5360 1.5340 1.5325 1.53001.5285 1.5260

EUR/JPY

Offers 134.30 134.50 134.80 135.00 135.50

Bids 133.40 133.00 132.85 132.50

USD/JPY

Offers 120.00 120.25-30 120.50

Bids 119.50 119.00 118.85 118.60 118.40 118.20 118.00 117.85

EUR/GBP

Offers 0.7300 0.7320-25 0.7345-50 0.7385 0.7400

Bids 0.7230 0.7200-10 0.7180-85 0.7160

AUD/USD

Offers 0.7800 0.7825-30 0.7840 0.7880 0.7900-10 0.7930

Bids 0.7740 0.7720 0.7700 0.7640

-

13:00

European stock markets mid-session: DAX and FTSE retreat from fresh all-time highs

European stocks mostly declined over the course of the day. The FTSE and the DAX retreated from all-time highs set earlier in the session.

U.K.'s Nationwide House Price Index for February declined to the lowest in in 17 months in February from a previous reading of +0.3% by -0.1%. Year on year the index rose +5.7% compared to +6.8% last year.

France, Germany and the Eurozone reported Manufacturing PMIs. February data from France showed a decline from previous 47.7 to 47.6 below estimates of an unchanged reading. The German PMI rose to 51.1, beating estimates of on unchanged reading of 50.9. Manufacturing PMI for the Eurozone declined to 51.0 coming from a previous reading of 51.1 and 0.1 points below estimates.

The Unemployment Rate in the Eurozone declined to the lowest level since April 2012, Eurostat reported today. The number of people unemployed fell to a seasonally adjusted 11.2% in January from 11.3% in December (revised down from 11.4%). Analyst expected a reading of 11.4%. In December. Germany has the lowest Unemployment Rate with 4.7% followed by Austria with 4.8% whereas Greece and Spain have the highest.

Although data for Consumer Price Inflation came in higher-than-expected at -0.3% compared to estimates at -0.5% and a previous reading of -0.6% inflation remained in negative territory for a third consecutive month, preliminary data showed. Given the reading far below the targeted inflation rate of the ECB around 2%, concerns over deflation in the Eurozone persist. Low oil prices kept inflation low.

U.K Mortgage Approvals came in below expectations of 61 at 60.7. The Purchasing Manager Index Manufacturing improved from revised 53.1 (previous reading of 53) to 54.1 in February. Net Lending to Individuals rose from 2.2 billion to 2.4 billion. Analyst expected a rise to 2.6 billion.

The FTSE 100 index is currently trading +0.01% quoted at 6,947.39. Germany's DAX 30 added +0.10% trading at 11,413.23, close to its new all-time high. France's CAC 40 is currently trading at 4,924.40 points, -0.55%.

-

12:20

Oil: Prices decline on record U.S. stockpiles – number of active U.S. rigs delcines

Oil prices declined on Monday as U.S. stockpiles are at record highs. However, Baker Hughes, an industry research group, reported on Friday that the number of active drilling rigs in the U.S. further declined by 33 to 986, the lowest count since 2011. A poll conducted by Reuters, showed that the price of oil is likely to have found the bottom and may start to grow in the second half of 2015, since the fall in 2014 caused a decline in production. On Sunday Iraqi oil minister said he sees oil prices rising to USD65 a barrel.

Brent Crude declined by -1.17%, currently trading at USD61.85 a barrel. On January 13th Crude hit a low at USD45.19. West Texas Intermediate lost -1.17% currently quoted at USD49.18, back below USD50 a barrel.

Although prices stabilized recently worldwide supply still exceeds demand in a period of low global economic growth limiting the impact of positive macroeconomic news.

-

12:00

Gold trades higher after PBoC lowered interest rates on Saturday

Gold booked gains in today's trading for a fourth consecutive day rebounding from lows hit on February 24th at USD1,190.40 after the Peoples Bank of China cut benchmark interest rates last Saturday for the second time in three months by a quarter percentage point to 5.35% to spur economic growth and ward of deflation in the world's second largest economy. Lower interest rates a positive for gold as the relative cost of owning the precious metal decreases.

A stronger U.S. dollar and the prospect for higher U.S. rates recently weighed on the precious metal, even though the start of an interest rate hike may be delayed, as the precious metal is dollar-denominated and not yield-bearing.

The precious metal is currently quoted at USD1,216.70, +0,35% a troy ounce. On Thursday the 22nd of January gold reached a five-month high at USD1,307.40.

-

11:24

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1000(E909mn), $1.1200(E673mn), $1.1300(E594mn), $1.1320-25(E908mn), $1.1340(E415mn)

USD/JPY: Y117.50($650mn), Y118.00($1.0bn), Y118.90($1.7bn), Y120.00($1.57bn), Y121.50($700mn)

GBP/USD: $1.5500(Gbp311mn)

AUD/USD: $0.7750(A$520mn), $0.7800(A$489mn), $0.7910(A$747mn)

-

11:20

Eurozone: Unemployment Rate declines, Harmonized CPI higher-than-expected but still negative

The Unemployment Rate in the Eurozone declined to the lowest level since April 2012, Eurostat reported today. The number of people unemployed fell to a seasonally adjusted 11.2% in January from 11.3% in December (revised down from 11.4%). Analyst expected a reading of 11.4%. In December. Germany has the lowest Unemployment Rate with 4.7% followed by Austria with 4.8% whereas Greece and Spain have the highest.

Although data for Consumer Price Inflation came in higher-than-expected at -0.3% compared to estimates at -0.5% and a previous reading of -0.6% inflation remained in negative territory for a third consecutive month, preliminary data showed. Given the reading far below the targeted inflation rate of the ECB around 2%, concerns over deflation in the Eurozone persist.

-

11:00

Eurozone: Unemployment Rate , January 11.2% (forecast 11.4%)

-

11:00

Eurozone: Harmonized CPI, Y/Y, February -0.3% (forecast -0.5%)

-

10:31

United Kingdom: Mortgage Approvals, January 60.7 (forecast 61.0)

-

10:31

United Kingdom: Net Lending to Individuals, bln, January 2.4 (forecast 2.8)

-

10:30

United Kingdom: Purchasing Manager Index Manufacturing , February 54.1

-

10:20

Press Review: Near Fed majority backs June liftoff Yellen hasn't yet endorsed

BLOOMBERG

Watch Out for BOJ in April, Says Economist Who Saw October Move

(Bloomberg) -- Watch out for another surprise from Bank of Japan Governor Haruhiko Kuroda this April, says Yuji Shimanaka, an economist who correctly predicted the unexpected expansion in monetary easing in October.

Shimanaka, at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo, is among a minority of analysts who forecast that further stimulus will come so early. According to the 59-year-old, who has been a market economist for more than three decades, one of several gauges of consumer prices could approach zero or even decline by March, challenging the central bank's outlook for inflation to accelerate in the year ahead and forcing its hand.

While 26 of 35 economists in a Feb. 5-10 survey by Bloomberg News forecast the BOJ will expand monetary stimulus this year, only seven expect a move in April, with Oct. 30 the most popular pick.

REUTERS

Eurogroup head: Greek reforms could prompt bailout payment in March(Reuters) - Greece's international creditors could pay part of the 7.2 billion euros remaining in its bailout pot as early as this month if Athens starts adopting necessary reforms, the head of the euro zone finance ministers' group said.

"My message to the Greeks is: try to start the program even before the whole renegotiation is finished," Dutch Finance Minister Jeroen Dijsselbloem told the Financial Times in an interview.

"There are elements that you can start doing today. If you do that, then somewhere in March, maybe there can be a first disbursement. But that would require progress and not just intentions," he was quoted as saying.

Source: http://www.reuters.com/article/2015/03/02/us-eurozone-greece-eurogroup-idUSKBN0LY0I120150302

REUTERS

Near Fed majority backs June liftoff Yellen hasn't yet endorsed(Reuters) - Janet Yellen's premium on consensus may lead to a Federal Reserve decision the chair hasn't yet endorsed, as a near majority aligns in favor of a possible June interest rate hike.

Seven of the Fed's current 17 members have now said they at least want the option of a June tightening on the table, or have pushed in general for an earlier increase amid an expectation that wages and inflation will turn higher.

By contrast, there's a dwindling core of officials who say publicly that the economy and labor markets in particular still have a long way to go -- only four Fed members have in recent weeks clearly said that rate hikes won't be appropriate until much later in the year or even into 2016.

Source: http://www.reuters.com/article/2015/03/02/us-usa-fed-liftoff-insight-idUSKBN0LY0D920150302

-

10:00

Eurozone: Manufacturing PMI, February 51.0 (forecast 51.1)

-

10:00

European Stocks. First hour: European indices open higher – Eurozone data in the focus

European stocks open mostly higher on Monday led by the financial and mining sector.

U.K.'s Nationwide House Price Index for February declined to the lowest in in 17 months in February from a previous reading of +0.3% by -0.1%. Year on year the index rose +5.7% compared to +6.8% last year.

France, Germany and the Eurozone reported Manufacturing PMIs. February data from France showed a decline from previous 47.7 to 47.6 below estimates of an unchanged reading. The German PMI rose to 51.1, beating estimates of on unchanged reading of 50.9. Manufacturing PMI for the Eurozone declined to 51.0 coming from a previous reading of 51.1 and 0.1 points below estimates.

Later in the session Eurozone Unemployment Rate and Preliminary Harmonized CPI will be in the focus (10:00 GMT). In the U.S. a set of data including the ISM Manufacturing Index, Personal Income and Spending is will be closely watched.

The commodity heavy FTSE 100 index is currently trading +0.33% quoted at 6,969.43 points boosted by mining stocks. Germany's DAX 30 is trading +0.36 at 11,443.04 points. Both, DAX and FTSE100 are set new all-time highs in today's trading session. France's CAC 40 declined by -0.03%, currently trading at 4,949.80 points.

-

09:55

Germany: Manufacturing PMI, February 51.1 (forecast 50.9)

-

09:50

France: Manufacturing PMI, February 47.6 (forecast 47.7)

-

09:31

Switzerland: Manufacturing PMI, February 47.3

-

09:00

Global Stocks: Wall Street declines on mixed data, Nikkei extends 15-year high, Chinese stocks gain on PBoC rate cuts

U.S. stocks closed lower on Firday on mixed U.S. economic data. The U.S. revised GDP grew 2.2% in the fourth quarter, lower than the previous estimated growth of 2.6%. Analysts had expected U.S. GDP to rise 2.1%. The Chicago purchasing managers' index declined to 45.8 in February from 59.4 in January, missing expectations for a fall to 58.4. That was the lowest level since July 2009. The final University of Michigan's consumer sentiment index was 95.4 in February, beating expectations for a decline to 94.2, down from the preliminary estimate of 98.2. The S&P 500 closed -0.30% with a final quote of 2,104.50 points. The DOW JONES index declined by -0.45% closing at 18,132.70 points. Despite Friday's losses U.S. indices ended the month near record highs and posted the biggest monthly gains since October 2011.

Chinese stocks traded higher after the Peoples Bank of China cut benchmark interest rates for the second time in three months by a quarter percentage point to 5.35% to spur economic growth and ward of deflation. The HSBC Manufacturing PMI in Asia's biggest economy further expanded into positive territory and rose to 50.7 compared to 50.1 in the previous month. Analysts expected the index to remain at 50.1 points. Hong Kong's Hang Seng is trading +0.12% at 24,853.19 points. China's Shanghai Composite closed at 3,336.14 points +0.78%.

The Nikkei continues extending its 15-year high on Monday on a weaker Japanese yen and the rate cut of the PBoC. The Nikkei closed +0.15% with a final quote of 18,826.88 points. Data on the Japanese Manufacturing PMI for February came in at 51.6, better than the expected 51.5 and the previous reading of 51.1 points.

-

08:30

Foreign exchange market. Asian session: U.S. dollar traded higher against its major peers

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:00 Australia HIA New Home Sales, m/m January -1.9% +1.8%

00:30 Australia Company Operating Profits Quarter IV +0.5% +0.7% -0.2%

01:35 Japan Manufacturing PMI (Finally) February 51.5 51.5 51.6

01:45 China HSBC Manufacturing PMI (Finally) February 50.1 50.1 50.7

05:30 Australia Commodity Prices, Y/Y February -19.2% -20.6%

07:00 United Kingdom Nationwide house price index February +0.3% -0.1%

07:00 United Kingdom Nationwide house price index, y/y February +6.8% +5.7%

The U.S. dollar traded higher against its major peers despite mixed data published on Friday. The U.S. revised GDP grew 2.2% in the fourth quarter, lower than the previous estimated growth of 2.6%. Analysts had expected U.S. GDP to rise 2.1%. The Chicago purchasing managers' index declined to 45.8 in February from 59.4 in January, missing expectations for a fall to 58.4. That was the lowest level since July 2009. The final University of Michigan's consumer sentiment index was 95.4 in February, beating expectations for a decline to 94.2, down from the preliminary estimate of 98.2.

The Australian dollar declined versus the greenback before the upcoming policy meeting on Tuesday. HIA New Home Sales rose by +1.8% in January after a decline of -1.9% in December. Company Operating Profits for the fourth quarter declined by -0.2%, below the estimated growth of +0.7%. Last quarters reading was revised down from +0.5% tp +0.4%. Commodity prices declined year on year by -20.6% in February.

On Saturday the Peoples Bank of China cut benchmark interest rates for the second time in three months by a quarter percentage point to 5.35%. The HSBC Manufacturing PMI in Asia's biggest economy further expanded into positive territory and rose to 50.7 compared to 50.1 in the previous month. Analysts expected the index to remain at 50.1.

New Zealand's dollar lost against the greenback in the absence any major economic reports from New Zealand.

The Japanese yen traded lower against the greenback on Monday. Data on the Japanese Manufacturing PMI for February came in at 51.6, better than the expected 51.5 and the previous reading of 51.1 points.

EUR/USD: the euro traded lower against the greenback

USD/JPY: the U.S. dollar traded higher against the yen

GPB/USD: Sterling traded lower against the U.S. dollar

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

08:30 Switzerland Manufacturing PMI February 48.2

08:50 France Manufacturing PMI (Finally) February 47.7 47.7

08:55 Germany Manufacturing PMI (Finally) February 50.9 50.9

09:00 Eurozone Manufacturing PMI (Finally) February 51.1 51.1

09:30 United Kingdom Mortgage Approvals January 60.3 61.0

09:30 United Kingdom Purchasing Manager Index Manufacturing February 53.0

09:30 United Kingdom Net Lending to Individuals, bln January 2.2 2.8

10:00 Eurozone Unemployment Rate January 11.4% 11.4%

10:00 Eurozone Harmonized CPI, Y/Y (Preliminary) February -0.6% -0.5%

13:30 Canada Current Account, bln Quarter IV -8.4 -7.4

13:30 U.S. Personal Income, m/m January +0.3%

13:30 U.S. Personal spending January -0.3%

13:30 U.S. PCE price index ex food, energy, m/m January 0.0% +0.1%

13:30 U.S. PCE price index ex food, energy, Y/Y January +1.3%

14:45 U.S. Manufacturing PMI (Finally) February 53.9 54.3

15:00 U.S. Construction Spending, m/m January +0.4%

15:00 U.S. ISM Manufacturing February 53.5 53.4

23:50 Japan Monetary Base, y/y February +37.4%

-

08:11

Options levels on monday, March 2, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1366 (2435)

$1.1327 (2404)

$1.1365 (1426)

Price at time of writing this review: $1.1170

Support levels (open interest**, contracts):

$1.1152 (2742)

$1.1130 (5762)

$1.1101 (2974)

Comments:

- Overall open interest on the CALL options with the expiration date March, 6 is 110802 contracts, with the maximum number of contracts with strike price $1,1500 (6212);

- Overall open interest on the PUT options with the expiration date March, 6 is 116403 contracts, with the maximum number of contracts with strike price $1,1100 (6712);

- The ratio of PUT/CALL was 1.05 versus 1.02 from the previous trading day according to data from February, 27

GBP/USD

Resistance levels (open interest**, contracts)

$1.5700 (1136)

$1.5601 (2677)

$1.5504 (2884)

Price at time of writing this review: $1.5396

Support levels (open interest**, contracts):

$1.5298 (2246)

$1.5199 (1957)

$1.5100 (1593)

Comments:

- Overall open interest on the CALL options with the expiration date March, 6 is 30423 contracts, with the maximum number of contracts with strike price $1,5500 (2884);

- Overall open interest on the PUT options with the expiration date March, 6 is 35926 contracts, with the maximum number of contracts with strike price $1,5300 (2246);

- The ratio of PUT/CALL was 1.18 versus 1.19 from the previous trading day according to data from February, 27

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:00

United Kingdom: Nationwide house price index , February -0.1%

-

08:00

United Kingdom: Nationwide house price index, y/y, February +5.7%

-

03:02

Nikkei 225 18,823.54 +25.60 +0.14 %, Hang Seng 24,920.6 +97.31 +0.39 %, Shanghai Composite 3,330.34 +20.04 +0.61 %

-

02:46

China: HSBC Manufacturing PMI, February 50.7 (forecast 50.1)

-

02:35

Japan: Manufacturing PMI, February 51.6 (forecast 51.5)

-

01:30

Australia: Company Operating Profits, Quarter IV -0.2% (forecast +0.7%)

-

01:01

Australia: HIA New Home Sales, m/m, January +1.8%

-

00:50

Japan: Capital Spending, Quarter IV +2.8%

-

00:32

Commodities. Daily history for Feb 27’2015:

(raw materials / closing price /% change)

Oil 49.76 +3.30%

Gold 1,213.70 +0.05%

-

00:31

Stocks. Daily history for Feb 27’2015:

(index / closing price / change items /% change)

Nikkei 225 18,797.94 +12.15 +0.06 %

Hang Seng 24,823.29 -78.77 -0.32 %

Shanghai Composite 3,310.72 +12.36 +0.37 %

FTSE 100 6,946.66 -3.07 -0.04 %

CAC 40 4,951.48 +40.86 +0.83 %

Xetra DAX 11,401.66 +74.47 +0.66 %

S&P 500 2,104.5 -6.24 -0.30 %

NASDAQ Composite 4,963.53 -24.36 -0.49 %

Dow Jones 18,132.7 -81.72 -0.45 %

-

00:30

Currencies. Daily history for Feb 27’2015:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1189 -0,07%

GBP/USD $1,5437 +0,21%

USD/CHF Chf0,9532 +0,07%

USD/JPY Y119,63 +0,18%

EUR/JPY Y133,86 +0,12%

GBP/JPY Y184,66 +0,38%

AUD/USD $0,7813 +0,23%

NZD/USD $0,7562 +0,40%

USD/CAD C$1,2501 -0,10%

-