Noticias del mercado

-

21:56

U.S.: Total Vehicle Sales, mln, January 16.7 (forecast 17.0)

-

21:00

S&P 500 2,039.88 +19.03 +0.94%, NASDAQ 4,705.86 +29.17 +0.62%, Dow 17,615.35 +254.31 +1.46%

-

18:02

European stocks close: stocks closed higher on Greek plans to renegotiate its debt

Stock indices closed higher on Greek plans to renegotiate its debt. The new Greece government outlined its plans to renegotiate the terms of its bailout, retreating from demands for a debt haircut. Greek Finance Minister Yanis Varoufakis has proposed debt swaps.

Eurozone's producer price index dropped 1.0% in December, missing expectations for a 0.7% decrease, after a 0.4% decline in November.

Markit's and the Chartered Institute of Purchasing & Supply's construction purchasing managers' index (PMI) for the U.K. rose to 59.1 in January from 57.6 in December, beating expectations for a decline to 56.9.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,871.8 +89.25 +1.32 %

DAX 10,890.95 +62.94 +0.58 %

CAC 40 4,677.9 +50.23 +1.09 %

-

18:00

European stocks closed: FTSE 100 6,871.8 +89.25 +1.32%, CAC 40 4,677.9 +50.23 +1.09%, DAX 10,890.95 +62.94 +0.58%

-

17:40

Oil rose for a fourth day

Oil rose for a fourth day, the longest run of gains since August, amid speculation reduced investment will curb production.

BP Plc said today it will cut spending by 13 percent after oil slumped. U.S. drillers idled 94 rigs last week, the most in data starting in 1987, according to Baker Hughes Inc. Hedge funds and other speculators held the largest number of short contracts in WTI in four years last week. A U.S. refinery strike, which started Feb. 1, has halted one plant while management has taken control of operations at six others.

Brent crude is poised to enter a bull market after rebounding from a collapse. Prices are down 52 percent since June. Chevron Corp. and Royal Dutch Shell Plc lowered their spending targets for this year as the industry cut more than $40 billion from budgets since Nov. 1. Futures rose as much as 4 percent in New York, extending a 2.8 percent gain yesterday.

"We're rising for a fourth consecutive day as the market corrects after its huge decline," Gene McGillian, a senior analyst at Tradition Energy in Stamford, Connecticut, said by phone. "The BP spending plans are probably putting the focus on the rig count and what that'll mean for future output."

West Texas Intermediate for March delivery rose $1.59, or 3.2 percent, to $51.16 a barrel at 10:29 a.m. on the New York Mercantile Exchange. Futures touched $51.55, the highest level since Jan. 5. WTI closed at $44.45 on Jan. 28, the lowest since March 2009. The volume of all futures traded was 59 percent above the 100-day average for the time of day.

Brent for March settlement climbed $1.35, or 2.5 percent, to $56.10 a barrel on the London-based ICE Futures Europe exchange. That's 20 percent higher than its Jan. 13 close of $46.59, the lowest in almost six years. A gain of 20 percent in closing prices is commonly referred to as a bull market. Volume was about twice the 100-day average. The North Sea crude is heading for the longest stretch of gains since May.

The European benchmark oil grade traded at a $4.94 premium to WTI.

BP expects to cut spending to $20 billion this year, compared with previous guidance of $24 billion to $26 billion. It spent about $23 billion in 2014.

Oil will probably trade from $40 to $60 a barrel for the next three years, BP Plc Chief Executive Officer Bob Dudley said in an interview with Bloomberg Television on Tuesday.

-

17:32

Foreign exchange market. American session: the U.S. dollar traded lower against the most major currencies after the weaker-than-expected U.S. factory orders

The U.S. dollar traded lower against the most major currencies after the weaker-than-expected U.S. factory orders. Factory orders in the U.S. dropped 3.4% in December, missing expectations for a 1.8% decrease, after a 1.7% decline in November. That was the fifth straight decline.

November's figure was revised down from a 0.7% fall.

Manufacturing in the U.S. is cooling due to weak global demand and falling oil prices.

The euro rose against the U.S. dollar as the new Greece government outlined its plans to renegotiate the terms of its bailout, retreating from demands for a debt haircut. Greek Finance Minister Yanis Varoufakis has proposed debt swaps.

Eurozone's producer price index dropped 1.0% in December, missing expectations for a 0.7% decrease, after a 0.4% decline in November.

The British pound traded higher against the U.S. dollar. Markit's and the Chartered Institute of Purchasing & Supply's construction purchasing managers' index (PMI) for the U.K. rose to 59.1 in January from 57.6 in December, beating expectations for a decline to 56.9.

The Canadian dollar traded higher against the U.S. dollar despite the weaker-than-expected Canadian raw materials purchase price index. The Raw Materials Price Index (RMPI) dropped 7.6% in December, missing expectations for a 4.6% fall, after a 5.7% decline in November. November's figure was revised up from a 5.8% decrease.

The drop was driven by lower prices for crude energy products.

The Swiss franc traded higher against the U.S. dollar. Switzerland's trade surplus narrowed to CHF1.5 billion in December from CHF3.8 billion in November.

Exports rose 7.2% in December, while imports declined 0.2%.

The New Zealand dollar increased against the U.S. dollar. In the overnight trading session, the kiwi fell against the greenback in the absence of any major economic reports from New Zealand. The interest rate cut by the Reserve Bank of Australia (RBA) weighed on the kiwi.

The Australian dollar traded higher against the U.S. dollar. In the overnight trading session, the Aussie dropped against the greenback as the RBA cut its interest rate to a new record low of 2.25%, down from 2.50%. The RBA said that the Aussie remains overvalued.

The RBA Governor Glenn Stevens said in a statement that the Australian dollar remains "above most estimates of its fundamental value", despite the recent decline. He pointed out that a lower exchange rate is needed "to achieve balanced growth in the economy".

Australia's trade deficit narrowed to A$0.44 billion in December from A$1.02 billion in November. November's figure was revised down from a deficit of A$0.93 billion. Analysts had expected the trade deficit to decrease to A$0.85 billion.

Exports increased 1.0% in December, while imports declined 1.0%.

Building approvals in Australia declined 3.3% in December, beating expectations for a 4.8% decline, after a 7.7% increase in November. November's figure was revised up from a 7.5% gain.

The Japanese yen traded lower against the U.S. dollar. In the overnight trading session, the yen traded higher against the greenback. Japan's monetary base increased 37.4% in January, missing expectations for a 40.1% rise, after a 38.2% gain in December.

-

17:20

Gold fell

Gold declined markedly amid hopes of avoiding conflict between the new government of Greece and its international lenders.

Appetite for safe assets weakened after the Greek government signaled plans to revise the terms of the debt with its creditors, departing from the requirements to take them off.

Greek Finance Minister Janis Varufakis suggested "list of debt swaps" to ease the debt burden of the country, according to which creditors are invited to exchange debt for new bonds tied to economic growth.

This offer is easing concerns over a conflict that could lead to a Greek exit from the euro zone.

On Tuesday, the main stock index in Athens jumped more than 8%, providing significant support to the growth of European equities. Yields on 10-year Greek government bonds also fell sharply.

Gold rose early in the session, as optimism about the US economy weakened when data released on Monday showed that consumer spending in the country fell in December at the fastest pace since September 2009, undermining optimism about the health of the US economy.

A separate report showed that construction spending in the US rose in December, less than expected, while industrial production growth slowed.

Last week, another report showed that in the fourth quarter, the US economy grew less than expected by 2.6% after 5.0% in the previous quarter.

Today in the US were published data on factory orders. The number of production orders declined significantly at the end of December, registering with the fifth consecutive monthly fall. At the same time the cost of business drop was less than previously estimated, and it should support the sector in the coming months.

Ministry of Commerce announced new orders for manufactured goods fell by 3.4 percent due to a drop in demand in the industrial sector.

Market participants are also preparing for Friday's report on employment in the US non-farm payrolls to obtain additional information regarding the strength of the recovery in the labor market.

Analysts predict that in January, the US economy added 231,000 jobs in December after 252,000, while the unemployment rate is projected to remain unchanged at 5.6%.

Strong employment rates in the non-agricultural sector, are likely to increase speculation about the timing recovery rates by the Federal Reserve System, while the weak values can contribute to the growth of gold, weakening incentives for early recovery rates.

April futures price of gold on the COMEX today fell to 1256.50 dollars per ounce.

-

17:03

Switzerland's trade surplus reaches a record high in 2014

The Swiss Federal Customs Administration released its trade data figures for Switzerland on Tuesday. Switzerland's trade surplus narrowed to CHF1.5 billion in December from CHF3.8 billion in November.

Exports rose 7.2% in December, while imports declined 0.2%.

For 2014 as whole, Switzerland's trade surplus increased to a record high of CHF30.0 billion in 2014 from CHF23.6 billion in 2013.

The increase was led by a 3.5% rise in exports, driven by pharmaceuticals, chemicals and watches. Imports declined 0.4% in 2014.

-

16:35

U.S. factory orders dropped 3.4% in December

The U.S. Commerce Department released factory orders data on Tuesday. Factory orders in the U.S. dropped 3.4% in December, missing expectations for a 1.8% decrease, after a 1.7% decline in November. That was the fifth straight decline.

November's figure was revised down from a 0.7% fall.

Manufacturing in the U.S. is cooling due to weak global demand and falling oil prices.

Factory orders excluding transportation fell 2.3% in December, the biggest decline since March 2013.

-

16:00

U.S.: Factory Orders , December -3.4% (forecast -1.8%)

-

15:57

Reserve Bank of Australia cut its interest rate to a new record low of 2.25%

The Reserve Bank of Australia (RBA) released its interest rate decision on Tuesday. The RBA cut its interest rate to a new record low of 2.25%, down from 2.50%. The RBA said that the Aussie remains overvalued.

The RBA Governor Glenn Stevens said in a statement that Australia's economy grows below trend, and domestic demand growth is overall weak. He noted that the unemployment rate increased over the past year.

Stevens pointed out that the central bank expects that "output growth will probably remain a little below trend for somewhat longer, and the rate of unemployment peak a little higher, than earlier expected".

The RBA governor also said that the inflation in Australia showed the lowest rise for several years in 2014, driven by falling oil prices at the end of the year and the removal of the price on carbon.

Stevens noted that the Australian dollar remains "above most estimates of its fundamental value", despite the recent decline. He pointed out that a lower exchange rate is needed "to achieve balanced growth in the economy".

-

15:37

U.S. Stocks open: Dow +0.51%, Nasdaq +0.58%, S&P +0.77%

-

15:30

Before the bell: S&P futures +0.29%, Nasdaq futures +0.18%

U.S. stock-index futures rose as oil prices rallied for a fourth day and Staples Inc. and Office Depot Inc. surged on merger speculation.

Global markets:

Nikkei 17,335.85 -222.19 -1.27%

Hang Seng 24,554.78 +70.04 +0.29%

Shanghai Composite 3,205.55 +77.25 +2.47%

FTSE 6,854.1 +71.55 +1.05%

CAC 4,669.24 +41.57 +0.90%

DAX 10,901.05 +73.04 +0.67%

Crude oil $50.84 (+2.62%)

Gold $1267.70 (-0.71%)

-

15:18

Canadian industrial product and raw materials price indexes dropped in December

Statistics Canada released its industrial product and raw materials price indexes on Tuesday. The Industrial Product Price Index (IPPI) dropped 1.6% in December, missing forecasts for a 0.3% increase, after a 0.5% decrease in November. November's figure was revised down from a 0.4% decline.

That was the fourth straight monthly fall and the biggest decline since December 2008.

The decline was driven by lower prices for energy and petroleum products.

The Raw Materials Price Index (RMPI) dropped 7.6% in December, missing expectations for a 4.6% fall, after a 5.7% decline in November. November's figure was revised up from a 5.8% decrease.

That was the sixth straight monthly decline.

The drop was driven by lower prices for crude energy products.

-

15:09

Stocks before the bell

(company / ticker / price / change, % / volume)

McDonald's Corp

MCD

92.55

+0.04%

0.3K

Visa

V

255.50

+0.06%

0.4K

Nike

NKE

92.00

+0.09%

7.5K

Apple Inc.

AAPL

118.77

+0.12%

197.1K

International Business Machines Co...

IBM

154.95

+0.19%

1.2K

Caterpillar Inc

CAT

81.00

+0.20%

11.3K

Merck & Co Inc

MRK

61.00

+0.20%

4.8K

American Express Co

AXP

82.30

+0.21%

4.0K

Intel Corp

INTC

33.72

+0.21%

4.7K

AT&T Inc

T

33.65

+0.27%

4.1K

Hewlett-Packard Co.

HPQ

36.57

+0.27%

0.4K

Goldman Sachs

GS

176.00

+0.29%

1.0K

Pfizer Inc

PFE

31.75

+0.32%

34.6K

ALTRIA GROUP INC.

MO

53.99

+0.35%

2.4K

General Electric Co

GE

24.30

+0.37%

15.6K

Travelers Companies Inc

TRV

105.00

+0.40%

0.4K

Microsoft Corp

MSFT

41.45

+0.41%

25.7K

Facebook, Inc.

FB

75.32

+0.44%

83.3K

Procter & Gamble Co

PG

85.50

+0.45%

35.7K

Verizon Communications Inc

VZ

47.20

+0.47%

8.5K

JPMorgan Chase and Co

JPM

55.76

+0.52%

0.8K

Ford Motor Co.

F

15.35

+0.52%

9.5K

General Motors Company, NYSE

GM

33.29

+0.54%

13.0K

Citigroup Inc., NYSE

C

48.00

+0.59%

7.8K

Yahoo! Inc., NASDAQ

YHOO

44.95

+0.59%

36.5K

Twitter, Inc., NYSE

TWTR

37.69

+0.61%

8.7K

Google Inc.

GOOG

531.75

+0.62%

0.5K

Starbucks Corporation, NASDAQ

SBUX

88.24

+0.65%

1.3K

Chevron Corp

CVX

106.90

+0.79%

6.7K

UnitedHealth Group Inc

UNH

108.15

+0.80%

0.2K

Exxon Mobil Corp

XOM

90.40

+0.92%

35.0K

ALCOA INC.

AA

16.22

+0.93%

13.5K

Walt Disney Co

DIS

92.85

+1.00%

3.8K

Tesla Motors, Inc., NASDAQ

TSLA

214.50

+1.69%

22.9K

Yandex N.V., NASDAQ

YNDX

15.20

+1.95%

4.2K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

18.08

+3.61%

69.5K

Cisco Systems Inc

CSCO

26.79

-0.15%

2.1K

Boeing Co

BA

146.00

-0.18%

0.1K

Amazon.com Inc., NASDAQ

AMZN

363.50

-0.27%

4.9K

Barrick Gold Corporation, NYSE

ABX

12.85

-0.31%

22.2K

-

15:05

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Freeport-McMoRan (FCX) downgraded from Buy to Neutral at BofA/Merrill

Other:

United Tech (UTX) target raised from $132 to $137 at Argus

Cisco Systems (CSCO) tarted raised from $27 to $29 at Oppenheimer

-

14:48

Company News: United Parcel Service, Inc. (UPS) reported better than expected fourth quarter revenue, but earnings missed forecasts

United Parcel Service, Inc. (UPS) earned $1.25 per share in the fourth quarter, missing analysts' estimate of $1.28. Revenue in the fourth quarter increased 6.1% year-over-year to $15.89 billion, beating analysts' estimate of $15.77 billion.

The company released its forecasts for 2015. EPS is expected to be $5.05-$5.30 (analysts' estimate: $5.29).

United Parcel Service, Inc. (UPS) shares decreased to $99.50 (-0.63%) prior to the opening bell.

-

14:45

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1200-10(E520mn), $1.1300(E552mn), $1.1400 (E270mn)

USD/JPY: Y115.00($5.0bn), Y116.00($9.5bn), Y116.45-50($1.5bn), Y117.00($848mn), Y118.00($3.05bn), Y118.30-40($1.5bn), Y119.00($1.7bn)

AUD/USD: $0.7750(A$470mn), $0.7800(A$691mn), $0.7900(A$677mn), $0.8000(A$230mn)

NZD/USD: $0.7300(NZ$200mn), $0.7350(NZ$201mn), $0.7390(NZ$259mn), $0.7400(NZ$367mn)

USD/CAD: C$1.2400($270mn)

-

14:30

Canada: Raw Material Price Index, December -7.6% (forecast -4.6%)

-

14:30

Canada: Industrial Product Prices, m/m, December -1.6% (forecast +0.3%)

-

14:00

Orders

EUR/USD

Offers $1.1500, $1.1450/60, $1.1400, $1.1380/85

Bids $1.1260, $1.1220, $1.1200, $1.1100

GBP/USD

Offers $1.5200, $1.5145/50, $1.5115, $1.5100

Bids $1.4955, $1.4900

AUD/USD

Offers $0.7900, $0.7850, $0.7830, $0.7800, $0.7700

Bids $0.7600, $0.7500

EUR/JPY

Offers Y135.00, Y134.45/50, Y133.90

Bids Y132.20, Y132.00, Y130.15

USD/JPY

Offers Y119.00, Y118.50, Y118.00

Bids Y116.90, Y116.50, Y115.85

EUR/GBP

Offers stg0.7715, stg0.7700, stg0.7600

Bids stg0.7490, stg0.7440, stg0.7400

-

14:00

Foreign exchange market. European session: the British pound traded higher against the U.S. dollar after the better-than-expected construction PMI from the U.K.

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

00:30 Australia Building Permits, m/m December +7.7% Revised From +7.5% -4.8% -3.3%

00:30 Australia Building Permits, y/y December +10.1% +8.8%

00:30 Australia Trade Balance December -1.02 Revised From -0.93 -0.85 -0.44

03:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50% 2.25%

03:30 Australia RBA Rate Statement

07:00 Switzerland Trade Balance December 3.87 1.5

09:30 United Kingdom PMI Construction January 57.6 56.9 59.1

10:00 Eurozone Producer Price Index, MoM December -0.4% -0.7% -1.0%

10:00 Eurozone Producer Price Index (YoY) December -1.6% -2.7%

The U.S. dollar traded mixed against the most major currencies ahead of the U.S. factory orders. Factory orders in the U.S. are expected to decline 1.8% in December, after a 0.7% drop in November.

The euro traded mixed against the U.S. dollar after the producer price index from the Eurozone. Eurozone's producer price index dropped 1.0% in December, missing expectations for a 0.7% decrease, after a 0.4% decline in November.

The British pound traded higher against the U.S. dollar after the better-than-expected construction PMI from the U.K. Markit's and the Chartered Institute of Purchasing & Supply's construction purchasing managers' index (PMI) for the U.K. rose to 59.1 in January from 57.6 in December, beating expectations for a decline to 56.9.

The Canadian dollar traded higher against the U.S. dollar ahead of Canadian raw materials purchase price index. Canada's raw materials purchase price index is expected to decline 4.6% in December, after a 5.8% drop in November.

EUR/USD: the currency pair traded mixed

GBP/USD: the currency pair rose to $1.5081

USD/JPY: the currency pair increased to Y117.53

The most important news that are expected (GMT0):

13:30 Canada Raw Material Price Index December -5.8% -4.6%

15:00 U.S. Factory Orders December -0.7% -1.8%

21:45 New Zealand Employment Change, q/q Quarter IV +0.8% +0.8%

21:45 New Zealand Unemployment Rate Quarter IV 5.4% 5.3%

23:00 New Zealand RBNZ Governor Graeme Wheeler Speaks

-

13:34

Australia's trade deficit narrowed to A$0.44 billion in December

The Australian Bureau of Statistics released its trade date on Tuesday. Australia's trade deficit narrowed to A$0.44 billion in December from A$1.02 billion in November. November's figure was revised down from a deficit of A$0.93 billion. Analysts had expected the trade deficit to decrease to A$0.85 billion.

Exports increased 1.0% in December, while imports declined 1.0%.

For 2014 as whole, Australia's trade deficit narrowed to A$9.9 billion from A$10.3 billion in 2013. Exports climbed 2% in 2014, while imports were up 2%.

-

13:00

European stock markets mid-session: Hopes on Greek debt plan lift indices

European indices are trading higher today on hopes that there will be an agreement on the Greek debt standoff. The new Greek government retreated from a plan for a write-off of its debt and proposed a new debt arrangement to reach a compromise with its international creditors on the terms of its bailout. Finance Minister Varoufakis reassured in London that Greece is not seeking a standoff with the European Union. Upbeat quarterly earnings reports further lend support.

U.K. construction PMI expanded unexpectedly. Activity in the construction sector rose more-than-expected in January data showed on Tuesday. After the lowest reading in 17 months in December the index climbed from 57.6 points to 59.1 points, beating forecasts predicting a decline to 56.9. A reading of above 50 indicates expansion of the sector.

The commodity heavy FTSE 100 index is currently trading +1.31% quoted at 6,871.28 points. Energy shares rallied on climbing oil prices, led by BP who beat profit forecast. Germany's DAX 30 added +1.21% trading at 10,958.80 extending its all-time high. France's CAC 40 is currently trading at 4,687.51 points, +1.29%.

-

12:20

Oil: prices extend rally for a third day

Oil has continued to rally adding to gains of over 10% in the last two days after a 7th consecutive month of falling prices. Today Brent crude and West Texas Intermediate are further extending gains. Brent Crude added +3.32%, currently trading at USD56.57 a barrel, back far above the important USD50 level. On January 13th Crude hit a low at USD45.19. West Texas Intermediate added +2.95% currently quoted at USD51.03. Disappointing data from China and the U.S. weigh recently on prices. China and the U.S. are the world's largest consumers of oil. Concerns over future output from U.S. shale drillers drives prices up. The number of U.S. oil drilling rigs has declined the most in a week in 30 years. Morgan Stanley warns about over interpreting the significance of the number of rigs active as they don't give an exact indication on overall output. Ongoing strikes on U.S. plants give a further boost to prices.

Worldwide supply still exceeds demand in a period of low global economic growth and the OPEC refusing to cut output rates to stabilize prices. Smaller OPEC members want to cut production but the organisation, responsible for 40% of worldwide production focuses on its fight for market share.

-

12:00

Gold prices edge higher

Gold is trading higher today on Tuesday as investors look ahead to important data on the U.S. economy later in the week. On Monday optimism weakened as data showed U.S. consumer spending fall at the fastest pace since 2009 and data last week that showed the U.S. economy grew by a weaker-than-expected 2.6%. Today market participants await data on U.S. Factory Orders.

The new Greek government retreated from a plan for a write-off of its debt and proposed a new debt arrangement to reach a compromise with its international creditors on the terms of its bailout. Finance Minister Varoufakis reassured in London that Greece is not seeking a standoff with the European Union.

In January gold prices increased by almost 8% as the precious metal was sought after as safe-haven asset. Expectations that the FED is going to hike interest rates in mid-2015 as the U.S. economy is growing and the labour market is improving might decrease if the upcoming data fails to show that the economy is on track. A future interest rate hike puts pressure on gold. Higher interest rates make gold less attractive as the metal is not yield-bearing. A stronger greenback recently also weighed on the dollar-denominated precious metal as it makes it more expensive for holders of other currencies.

The precious metal is currently quoted at USD1,281.60, +0,52% a troy ounce. On Thursday the 22nd of January gold reached a five-month high at USD1,307.40.

-

11:22

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1200-10(E520mn), $1.1300(E552mn), $1.1400 (E270mn)

USD/JPY: Y115.00($5.0bn), Y116.00($9.5bn), Y116.45-50($1.5bn), Y117.00($848mn), Y118.00($3.05bn), Y118.30-40($1.5bn), Y119.00($1.7bn)

AUD/USD: $0.7750(A$470mn), $0.7800(A$691mn), $0.7900(A$677mn), $0.8000(A$230mn)

NZD/USD: $0.7300(NZ$200mn), $0.7350(NZ$201mn), $0.7390(NZ$259mn), $0.7400(NZ$367mn)

USD/CAD: C$1.2400($270mn)

-

11:05

U.K. construction PMI unexpectedly expanded to 59.1 in January

Activity in the construction sector rose more-than-expected in January data showed on Tuesday. After the lowest reading in 17 months in December the index climbed from 57.6 points to 59.1 points, beating forecasts predicting a decline to 56.9. A reading of above 50 indicates expansion of the sector.

The British pound is trading lower against the greenback despite the upbeat data currently quoted at 1.5028 after hitting lows at 1.4988 today.

-

11:00

Eurozone: Producer Price Index (YoY), December -2.7%

-

11:00

Eurozone: Producer Price Index, MoM , December -1.0% (forecast -0.7%)

-

10:30

United Kingdom: PMI Construction, January 59.1 (forecast 56.9)

-

10:00

European Stocks. First hour: Indices gain on Greek hopes

European stocks climbed in early trading on hopes that there will be an agreement on the Greek debt standoff. The new Greek government retreated from a plan for a write-off of its debt and proposed a new debt arrangement to reach a compromise with its international creditors on the terms of its bailout. Finance Minister Varoufakis reassured in London that Greece is not seeking a standoff with the European Union. Upbeat quarterly earnings reports further lend support.

The commodity heavy FTSE 100 index is currently trading +0.88% quoted at 6,842.26 points fuelled by sharp gains in the mining and energy sector. Germany's DAX 30 skyrocketed by +0.90% trading at 10,925.00 extending its all-time high. France's CAC 40 added +0.94%, currently trading at 4,671.40 points.

-

09:00

Global Stocks: U.S. and Chinese indices post gains, Nikkei down

U.S. markets closed higher on Monday reversing early session losses on hopes for a Greek debt deal and an end to the stand-off with international creditors. Rising oil prices helped the energy sector. Earlier the mostly weaker-than-expected U.S. economic data led shares lower. The Institute for Supply Management's manufacturing purchasing managers' index for the U.S. declined to 53.5 in January from 55.5 in December, missing expectations for a decline to 54.9.

Personal spending decreased 0.3% in December, missing expectations for a 0.1% decline, after a 0.5% rise in November. November's figure was revised down from a 0.6% increase. That was the largest decline since September 2009.Personal income climbed 0.3% in December, exceeding expectations for 0.2% increase, after a 0.3% rise in November. November's figure was revised down from a 0.4% gain. The personal consumption expenditures (PCE) price index excluding food and energy was flat in December, in line with expectations, after a flat reading in November.

The DOW JONES index added +1.14%, closing at 17,361.04 points. The S&P 500 rose by +1.30% in late trading with a final quote of 2,020.85 points. The S&P declined by 3.1% in January, the biggest loss since January 2014.

Chinese stock markets closed higher on Tuesday. Hong Kong's Hang Seng is trading +0.19% at 24,531.60 points. China's Shanghai Composite closed at 3,205.55 points +2.47% almost erasing yesterday's losses. Market participants anticipate further monetary easing from the PBoC after data on manufacturing showed a contraction in January.

Japan's Nikkei posted losses on Tuesday, closing -1.27% with a final quote of 17,335.85 as the results of the Japanese bond auction were disappointing and weaker economic data from the U.S. and China raised concerns on global growth. Uncertainty over the fate of Greece in the Eurozone further added to risk aversion. A stronger Japanese Yen weighed on exporter shares. A rally in oil prices had a negative effect on airlines and the energy sector.

-

08:30

Foreign exchange market. Asian session: U.S. dollar flat against euro, lower aginst yen

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:30 Australia Building Permits, m/m December +7.5% -4.8% -3.3%

00:30 Australia Building Permits, y/y December +10.1% +8.8%

00:30 Australia Trade Balance December -0.93 -0.85 -0.44

03:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50% 2.25%

03:30 Australia RBA Rate Statement

07:00 Switzerland Trade Balance December 3.87 1.5

The U.S. dollar traded mixed higher against the most major currencies, except the Japanese yen, recovering from declines after the mostly weaker-than-expected U.S. economic data yesterday. The Institute for Supply Management's manufacturing purchasing managers' index for the U.S. declined to 53.5 in January from 55.5 in December, missing expectations for a decline to 54.9. The data added to concerns over the economic outlook of the U.S. after data showed that the world's biggest economy expanded at a slower pace in the fourth quarter, growing at 2.6%. The greenback traded almost flat against the euro as there is hope that the new Greek government will reach a compromise on the terms of its bailout.

The Australian dollar slumped more than 1% to a six-year low after the Reserve Bank of Australia cut benchmark interest rates unexpectedly to a record low to 2.25% by 25 basis points at its policy meeting in order to support the economy and to keep the aussie low. Reserve Bank of Australia Governor Glenn Stevens said in a statement in a statement that lower interest rates are expected to add some further support to demand, help to achieve sustainable growth and to assure that inflation is consistent with the target. Earlier data on Australia's Trade Balance rose more than expected to a -0.44 billion from -1.02 billion in the previous month. Analysts expected -0.85 billion. Building Permits declined less-than-expected by 3.3% compared to a forecast of -4.8% in December. Data for November was revised to +7.7%. On a yearly basis Building Permits rose less with +8.8% compared to +10.1%.

New Zealand's dollar against fell sharply against the greenback in Asian trade continuing a recent slide. The kiwi lost 6% against the U.S. dollar in January. The Reserve Bank of New Zealand opened the door for a possible rate cut at its policy meeting on Wednesday. Today a set of data is due including Employment Change, the Unemployment rate and late in the day RBNZ Governor Graeme Wheeler Speaks.

The Japanese yen traded higher against the greenback on Tuesday as shares declined and investors sought a safe haven. Japan's Monetary Base rose less-than-expected by +37.4%. Economists predicted an increase by +40.1%.

EUR/USD: the euro traded almost flat against the greenback

USD/JPY: the U.S. dollar lost against the yen

GPB/USD: Sterling traded slightly weaker against the U.S. dollar

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

09:30 United Kingdom PMI Construction January 57.6 56.9

10:00 Eurozone Producer Price Index, MoM December -0.4% -0.7%

10:00 Eurozone Producer Price Index (YoY) December -1.6%

13:30 Canada Industrial Product Prices, m/m December -0.4% +0.3%

13:30 Canada Raw Material Price Index December -5.8% -4.6%

15:00 U.S. Factory Orders December -0.7% -1.8%

19:30 U.S. Total Vehicle Sales, mln January 16.9 17.0

21:30 U.S. API Crude Oil Inventories January +12.7

21:45 New Zealand Employment Change, q/q Quarter IV +0.8% +0.8%

21:45 New Zealand Unemployment Rate Quarter IV 5.4% 5.3%

22:30 Australia AIG Services Index January 47.5

23:00 New Zealand RBNZ Governor Graeme Wheeler Speaks

-

08:00

Switzerland: Trade Balance, December 1.5

-

07:24

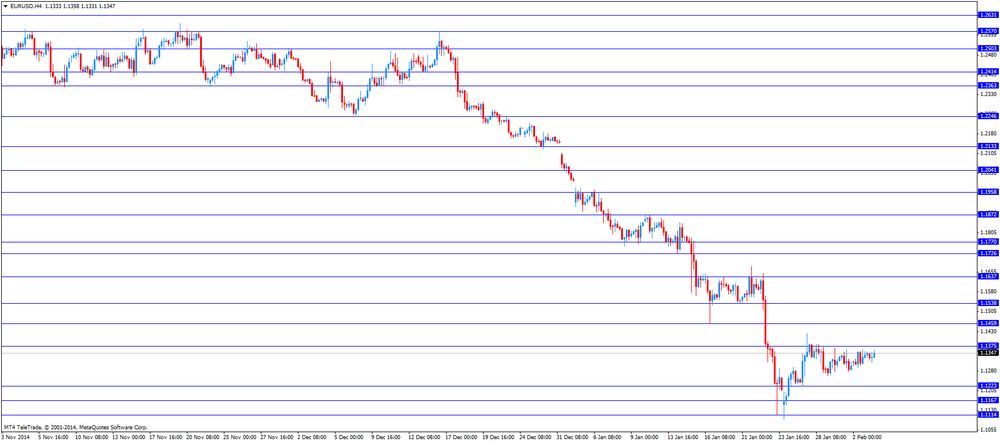

Options levels on tuesday, February 3, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1520 (3280)

$1.1447 (3418)

$1.1396 (1839)

Price at time of writing this review: $1.1328

Support levels (open interest**, contracts):

$1.1254 (3212)

$1.1182 (4325)

$1.1139 (2680)

Comments:

- Overall open interest on the CALL options with the expiration date February, 6 is 86203 contracts, with the maximum number of contracts with strike price $1,2100 (6527);

- Overall open interest on the PUT options with the expiration date February, 6 is 78278 contracts, with the maximum number of contracts with strike price $1,1700 (6670);

- The ratio of PUT/CALL was 0.91 versus 0.92 from the previous trading day according to data from February, 2

GBP/USD

Resistance levels (open interest**, contracts)

$1.5301 (669)

$1.5202 (1254)

$1.5104 (922)

Price at time of writing this review: $1.5017

Support levels (open interest**, contracts):

$1.4994 (1071)

$1.4897 (1911)

$1.4799 (1200)

Comments:

- Overall open interest on the CALL options with the expiration date February, 6 is 17610 contracts, with the maximum number of contracts with strike price $1,5200 (1254);

- Overall open interest on the PUT options with the expiration date February, 6 is 17529 contracts, with the maximum number of contracts with strike price $1,4900 (1911);

- The ratio of PUT/CALL was 0.99 versus 1.00 from the previous trading day according to data from February, 2

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

04:30

Australia: Announcement of the RBA decision on the discount rate, 2.25% (forecast 2.50%)

-

03:01

Nikkei 225 17,529.96 -28.08 -0.16%, Hang Seng 24,574.02 +89.28 +0.36%, Shanghai Composite 3,156.09 +27.79 +0.89%

-

01:32

Australia: Building Permits, y/y, December +8.8%

-

01:30

Australia: Building Permits, m/m, December -3.3% (forecast -4.8%)

-

01:30

Australia: Trade Balance , December -0.44 (forecast -0.85)

-

00:52

Japan: Monetary Base, y/y, January +37.4% (forecast +40.1%)

-

00:44

Commodities. Daily history for Feb 2’2015:

(raw materials / closing price /% change)

Light Crude 49.57 +2.76%

Gold 1,276.90 -0.18%

-

00:32

Stocks. Daily history for Feb 2’2015:

(index / closing price / change items /% change)

Nikkei 225 17,558.04 -116.35 -0.66%

Hang Seng 24,484.74 -22.31 -0.09%

Shanghai Composite 3,128.3 -82.06 -2.56%

FTSE 100 6,782.55 +33.15 +0.49%

CAC 40 4,627.67 +23.42 +0.51%

Xetra DAX 10,828.01 +133.69 +1.25%

S&P 500 2,020.85 +25.86 +1.30%

NASDAQ Composite 4,676.69 +41.45 +0.89%

Dow Jones 17,361.04 +196.09 +1.14%

-

00:30

Currencies. Daily history for Feb 2’2015:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1340 +0,36%

GBP/USD $1,5038 -0,15%

USD/CHF Chf0,9278 +1,06%

USD/JPY Y117,55 +0,13%

EUR/JPY Y133,35 +0,52%

GBP/JPY Y176,78 -0,01%

AUD/USD $0,7802 +0,26%

NZD/USD $0,7304 +0,27%

USD/CAD C$1,2562 -1,16%

-

00:00

Schedule for today, Tuesday, Feb 3’2015:

(time / country / index / period / previous value / forecast)

00:30 Australia Building Permits, m/m December +7.5% -4.8%

00:30 Australia Building Permits, y/y December +10.1%

00:30 Australia Trade Balance December -0.93 -0.85

03:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50%

03:30 Australia RBA Rate Statement

07:00 Switzerland Trade Balance December 3.87

09:30 United Kingdom PMI Construction January 57.6 56.9

10:00 Eurozone Producer Price Index, MoM December -0.4% -0.7%

10:00 Eurozone Producer Price Index (YoY) December -1.6%

13:30 Canada Industrial Product Prices, m/m December -0.4% +0.3%

13:30 Canada Raw Material Price Index December -5.8% -4.6%

15:00 U.S. Factory Orders December -0.7% -1.8%

19:30 U.S. Total Vehicle Sales, mln January 16.9 17.0

21:30 U.S. API Crude Oil Inventories January +12.7

21:45 New Zealand Employment Change, q/q Quarter IV +0.8% +0.8%

21:45 New Zealand Unemployment Rate Quarter IV 5.4% 5.3%

22:30 Australia AIG Services Index January 47.5

23:00 New Zealand RBNZ Governor Graeme Wheeler Speaks

-