Noticias del mercado

-

21:00

Dow +0.08% 16,789.06 +12.63 Nasdaq -0.85% 4,740.66 -40.60 S&P -0.43% 1,978.47 -8.58

-

18:44

International Monetary Fund’s World Economic Outlook: the lender cuts its global growth forecast for 2015 and 2016

The International Monetary Fund (IMF) released its World Economic Outlook on Tuesday. The IMF lowered its global economic growth forecasts due to a weaker growth in advanced economies and the slowdown in emerging economies.

The global economy will expand 3.1% in 2015, down from the previous forecast of 3.3%, and 3.6% in 2016, down from the previous forecast of 3.8%, according to the IMF.

"Six years after the world economy emerged from its broadest and deepest postwar recession, the holy grail of robust and synchronized global expansion remains elusive," Maurice Obstfeld, the IMF Economic Counsellor and Director of the Research Department, said.

The IMF cut its growth forecasts in advanced economies to 2.0% in 2015, down from 2.1%, and to 2.2% in 2016, down from 2.4%, while emerging markets expected to expand 4.0% in 2015, down from 4.2%.

The lender kept unchanged its growth forecast for the Eurozone for 2015 at 1.5%, while upgraded to 1.6% for next year from 1.5%.

The U.S. economy is expected to grow at 2.6% in 2015 and 2.8% in 2016.

-

18:29

Canada’s Ivey purchasing managers’ index drops to 53.7 in September

Canada's seasonally adjusted Ivey purchasing managers' index plunged to 53.7 in September from 58.0 in August. Analysts had expected the index to decrease to 54.0.

A reading above 50 indicates a rise in the pace of activity, below 50 indicates a contraction in the pace of activity.

The supplier deliveries index was up 49.8 in September from 48.2 in August, while employment index climbed to 57.1 from 56.3.

The prices index was fell to 64.4 in September from 66.3 in August, while inventories increased to 52.1 from 42.4.

-

18:23

U.S. trade deficit widens to $48.33 billion in August

The U.S. Commerce Department released the trade data on Tuesday. The U.S. trade deficit widened to $48.33 billion in August from $41.81 billion in July, missing expectations for a rise to $47.4 billion. July's figure was revised down from a deficit of $41.90 billion.

The rise of a deficit was driven by a rise in imports and a decline in exports. Exports declined 2% in August, while imports increased 1.2%.

-

18:13

Canada's trade deficit widens to C$2.53 billion in August

Statistics Canada released the trade data on Tuesday. Canada's trade deficit widened to C$2.53 billion in August from a deficit of C$0.82 billion in July. July's figure was revised up from a deficit of C$0.59 billion.

Analysts had expected a trade deficit of C$1.2 billion.

The increase in deficit was driven by a drop in exports. Exports slid 3.6% in August.

Exports of energy products dropped by 14.7% in August, exports of consumer goods dropped 8.0%, exports of motor vehicles and parts rose 3.1%, while exports of metal ores and non-metallic minerals were up 15.7%.

Imports climbed 0.2% in August.

Imports of aircraft and other transportation equipment and parts plunged by 14.4% in August, imports of metal and non-metallic mineral products climbed 6.0%, while imports of electronic and electrical equipment and parts declined 7.9%.

-

18:04

Germany's construction PMI rises to 52.4 in August

Markit Economics released construction purchasing managers' index (PMI) for Germany on Tuesday. Germany's construction purchasing managers' index (PMI) climbed to 52.4 in September from 50.3 in August.

A reading above 50 indicates expansion in the sector.

The index was driven by a rise in work on residential building projects.

Employment and purchasing activity also rose in September.

"Output rose at the strongest rate in six months, largely a result of sustained growth in residential building activity. Encouragingly, firms also reported a pick-up in purchasing activity, suggesting that companies are likely to remain busy in coming months," an economist at Markit, Oliver Kolodseike, said.

-

18:04

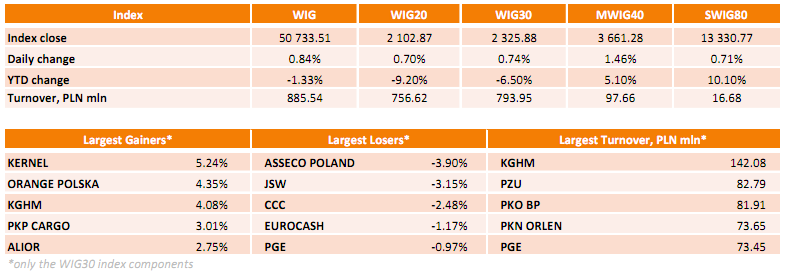

WSE: Session Results

Polish equity market closed higher on Tuesday. The broad market measure, the WIG Index, rose by 0.84%. Sector-wise, telecommunications (+4.32%) performed best, while informational technologies (-0.98%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, added 0.74%. Within the indicator's components, KERNEL (WSE: KER) and ORANGE POLSKA (WSE: OPL) were the biggest advancers, jumping by 5.24% and 4.35% respectively. KGHM (WSE: KGH) and PKP CARGO (WSE: PKP) also produced noticeable gains, up 4.08% and 3.01%. On the other side of the ledger, ASSECO POLAND (WSE: ACP) was the worst-performing name, correcting by 3.90% after four days of gains. It was followed by JSW (WSE: JSW) and CCC (WSE: CCC), slumping by 3.15% and 2.48% respectively.

-

18:00

European stocks closed: FTSE 100 6,326.16 +27.24 +0.43% CAC 40 4,660.64 +43.74 +0.95% DAX 9,902.83 +88.04 +0.90%

-

18:00

European stocks close: stocks closed higher as oil prices jumped

Stock indices closed higher as oil prices jumped. Oil prices increased more than 4% on speculation that oil production will decline and on a weaker U.S. dollar.

Meanwhile, the economic data from the Eurozone was negative. Destatis released its factory orders data for Germany on Tuesday. German seasonal adjusted factory orders dropped 1.8% in August, missing expectations for a 0.5% increase, after a 2.2% fall in July. July's figure was revised down from a 1.4% decrease.

The decline was driven by a drop in foreign and domestic orders. Foreign orders decreased by 1.2% in August, while domestic orders fell by 2.6%.

New orders from the Eurozone rose 2.5% in August, while orders from other countries slid 3.7%.

Orders of the intermediate goods fell by 0.4% in August, capital goods orders were down 2.8%, while consumer goods orders decreased 1.5%.

Halifax released its house prices data for the U.K. on Tuesday. House prices in the U.K. decreased 0.9% in September, after a 2.7% rise in August.

On a yearly basis, house prices climbed 8.6% in the three months to September, after a 9.0% increase in the three months to August.

"Housing demand has been strengthening recently, underpinned by economic growth, rising real earnings and very low mortgage rates. Increasing demand is combining with very low supply to drive robust underlying house price growth," Halifax's housing economist Martin Ellis said.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,326.16 +27.24 +0.43 %

DAX 9,902.83 +88.04 +0.90 %

CAC 40 4,660.64 +43.74 +0.95 %

-

17:52

Oil prices rise more than 4%

Oil prices increased more than 4% on speculation that oil production will decline and on a weaker U.S. dollar. The U.S. Energy Information Administration said on Tuesday that oil production was 120,000 barrels a day lower in September than in August.

Comments by OPEC Secretary-General Abdalla Salem el-Badri also supported oil prices. He said on Tuesday that oil prices will rebound due to lower oil investments. el-Badri expects global oil investments to drop by 22.4% this year.

Comments by Russian Energy Minister Alexander Novak still supported oil prices. He said on Saturday that Russia is ready to talks with the Organization of Petroleum-Exporting Countries (OPEC) to discuss oil prices. Novak added that Russia and Saudi Arabia planned a meeting for the end of the month.

Oil prices were also supported by concerns over the escalation of the conflict in Syria. Russia started air strikes against Islamic State targets in Syria on last Wednesday.

WTI crude oil for November delivery rose to $48.40 a barrel on the New York Mercantile Exchange.

Brent crude oil for November climbed to $51.54 a barrel on ICE Futures Europe.

-

17:33

Gold price climbs on a weaker U.S. dollar

Gold price rose on a weaker U.S. dollar. The U.S. dollar declined after the release of the weaker-than-expected U.S. trade deficit. The U.S. trade deficit widened to $48.33 billion in August from $41.81 billion in July, missing expectations for a rise to $47.4 billion. July's figure was revised down from a deficit of $41.90 billion.

Exports declined 2% in August, while imports increased 1.2%.

The International Monetary Fund (IMF) lowered its global growth forecasts for this year and next. The global economy is expected to expand 3.1% in 2015, down from the previous estimate of 3.3%, and 3.6% in 2016, down from the previous estimate of 3.8%.

December futures for gold on the COMEX today increased to 1150.20 dollars per ounce.

-

16:53

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Tuesday, with a surge in DuPont (DD) helping the Dow inch higher and a decline in health care stocks weighing on the Nasdaq.

Dow stocks mixed (16 in negative area, 14 in positive). Top looser - UnitedHealth Group Incorporated (UNH, -1.80%). Top gainer - E. I. du Pont de Nemours and Company (DD, +10.57%).

S&P index sectors also mixed. Top looser - Healthcare (-1.4%). Top gainer - Basic Materials (+1,2%).

At the moment:

Dow 16698.00 +39.00 +0.23%

S&P 500 1973.25 -1.50 -0.08%

Nasdaq 100 4296.25 -15.00 -0.35%

10 Year yield 2,05% -0,01

Oil 47.52 +1.26 +2.72%

Gold 1148.90 +11.30 +0.99%

-

16:00

Canada: Ivey Purchasing Managers Index, September 53.7 (forecast 54)

-

15:45

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1170(E200mn), $1.1225(E200mn)

USD/JPY: Y119.90($250mn),Y120.00($1.1bn), Y120.05($250mn)

USD/CAD: Cad1.3150/65($425mn)

USD/CHF: Chf1.000(520mn)

AUD/USD: $0.6900(A$636mn), $0.7200(A$350mn)

EUR/JPY: Y132.50(E440mn)

NZD/USD: $0.6640(NZ$602mn)

-

15:37

U.S. Stocks open: Dow +0.15%, Nasdaq -0.13%, S&P -0.07%

-

15:32

Before the bell: S&P futures -0.23%, NASDAQ futures -0.26%

U.S. stock-index futures retreated.

Nikkei 18,186.1 +180.61 +1.00%

Hang Seng 21,831.62 -22.88 -0.10%

FTSE 6,316.98 +18.06 +0.29%

CAC 4,643.09 +26.19 +0.57%

DAX 9,873.59 +58.80 +0.60%

Crude oil $46.34 (+0.17%)

Gold $1138.50 (+0.08%)

-

14:58

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

E. I. du Pont de Nemours and Co

DD

54.50

6.28%

52.8K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.37

1.70%

285.8K

FedEx Corporation, NYSE

FDX

151.00

0.72%

5.2K

Cisco Systems Inc

CSCO

26.99

0.52%

41.0K

Barrick Gold Corporation, NYSE

ABX

6.87

0.29%

1.5K

Walt Disney Co

DIS

104.05

0.19%

3.0K

International Business Machines Co...

IBM

149.26

0.15%

0.1K

The Coca-Cola Co

KO

41.04

0.07%

2.0K

General Motors Company, NYSE

GM

31.75

-0.03%

0.8K

AT&T Inc

T

33.41

-0.06%

2.5K

Procter & Gamble Co

PG

73.15

-0.10%

0.1K

Exxon Mobil Corp

XOM

76.70

-0.14%

1.5K

Chevron Corp

CVX

83.90

-0.15%

46.6K

Apple Inc.

AAPL

110.61

-0.15%

159.5K

Caterpillar Inc

CAT

69.07

-0.16%

0.8K

Wal-Mart Stores Inc

WMT

65.75

-0.18%

0.4K

JPMorgan Chase and Co

JPM

61.90

-0.19%

0.5K

ALCOA INC.

AA

10.39

-0.19%

0.8K

Verizon Communications Inc

VZ

43.90

-0.23%

0.3K

Starbucks Corporation, NASDAQ

SBUX

58.90

-0.24%

5.2K

Amazon.com Inc., NASDAQ

AMZN

542.20

-0.27%

5.7K

Hewlett-Packard Co.

HPQ

27.10

-0.29%

4.0K

Goldman Sachs

GS

180.15

-0.30%

02.K

General Electric Co

GE

26.74

-0.30%

22.8K

Visa

V

72.00

-0.32%

0.1K

Home Depot Inc

HD

118.81

-0.33%

2.1K

Intel Corp

INTC

31.10

-0.35%

3.0K

Ford Motor Co.

F

14.14

-0.35%

70.9K

Facebook, Inc.

FB

93.66

-0.37%

23.7K

Citigroup Inc., NYSE

C

50.95

-0.41%

2.2K

Microsoft Corp

MSFT

46.41

-0.47%

3.2K

Yahoo! Inc., NASDAQ

YHOO

30.69

-0.52%

0.1K

ALTRIA GROUP INC.

MO

55.28

-0.81%

2.6K

Twitter, Inc., NYSE

TWTR

27.88

-0.96%

32.9K

Yandex N.V., NASDAQ

YNDX

11.99

-2.04%

12.9K

Tesla Motors, Inc., NASDAQ

TSLA

239.75

-2.60%

45.7K

-

14:51

Upgrades and downgrades before the market open

Upgrades:

FedEx (FDX) upgraded to Buy from Hold at Stifel

Downgrades:

Other:

Tesla Motors (TSLA) target lowered to $450 from $465 at Morgan Stanley

Cisco Systems (CSCO) initiated with a Buy at Citigroup; target $30

-

14:30

Canada: Trade balance, billions, August -2.53 (forecast -1.2)

-

14:30

U.S.: International Trade, bln, August -48.33 (forecast -47.4)

-

14:00

Orders

EUR/USD

Offers 1.1225-30 1.1250 1.1265 1.1280 1.1300 1.1330 1.1350

Bids 1.1180-85 1.1155-60 1.1135 1.1120-25 1.1100

GBP/USD

Offers 1.5170 1.5185 1.5200 1.5235 1.5250 1.5265 1.5280 1.5300

Bids 1.5130-35 1.5115 1.5100 1.5080-85 1.5060 1.5030 1.5000

EUR/GBP

Offers 0.7400 0.7405-10 0.7420 0.7435 0.7450 0.7485 0.7500

Bids 0.7375-80 0.7360 0.7350 0.7330-35 0.7300

EUR/JPY

Offers 135.00 135.25 135.50 135.85 136.00 136.30 136.50

Bids 134.40 134.25 134.00 133.75 133.50 133.30 133.00

USD/JPY

Offers 120.50 120.65 120.85 121.00 121.30 121.50

Bids 120.00 119.80-85 119.65 119.40 119.25 119.10 119.00

AUD/USD

Offers 0.7135 0.7150 0.7185 0.7200 0.7225-30 0.7250

Bids 0.7100 0.7080-85 0.7060 0.7040 0.7020-25 0.7000 0.6980 0.6950

-

12:00

European stock markets mid session: stocks traded mixed after the negative factory orders data from German

Stock indices traded mixed after the negative factory orders data from Germany. Destatis released its factory orders data for Germany on Tuesday. German seasonal adjusted factory orders dropped 1.8% in August, missing expectations for a 0.5% increase, after a 2.2% fall in July. July's figure was revised down from a 1.4% decrease.

The decline was driven by a drop in foreign and domestic orders. Foreign orders decreased by 1.2% in August, while domestic orders fell by 2.6%.

New orders from the Eurozone rose 2.5% in August, while orders from other countries slid 3.7%.

Orders of the intermediate goods fell by 0.4% in August, capital goods orders were down 2.8%, while consumer goods orders decreased 1.5%.

Halifax released its house prices data for the U.K. on Tuesday. House prices in the U.K. decreased 0.9% in September, after a 2.7% rise in August.

On a yearly basis, house prices climbed 8.6% in the three months to September, after a 9.0% increase in the three months to August.

"Housing demand has been strengthening recently, underpinned by economic growth, rising real earnings and very low mortgage rates. Increasing demand is combining with very low supply to drive robust underlying house price growth," Halifax's housing economist Martin Ellis said.

Current figures:

Name Price Change Change %

FTSE 100 6,293.88 -5.04 -0.08 %

DAX 9,858.37 +43.58 +0.44 %

CAC 40 4,639.14 +22.24 +0.48 %

-

11:45

Australia's trade deficit widens to A$3.1 billion in August

The Australian Bureau of Statistics released its trade data on Tuesday. Australia's trade deficit widened to A$3.1 billion in August from A$2.79 billion in July, missing expectations for a decline to a deficit of A$2.55 billion. July's figure was revised up from a deficit of A$2.46 billion.

Exports were flat in August, while imports rose 0.1%.

-

11:40

House prices in the U.K. fall 0.9% in September

Halifax released its house prices data for the U.K. on Tuesday. House prices in the U.K. decreased 0.9% in September, after a 2.7% rise in August.

On a yearly basis, house prices climbed 8.6% in the three months to September, after a 9.0% increase in the three months to August.

"Housing demand has been strengthening recently, underpinned by economic growth, rising real earnings and very low mortgage rates. Increasing demand is combining with very low supply to drive robust underlying house price growth," Halifax's housing economist Martin Ellis said.

-

11:33

Switzerland’s consumer price inflation rises 0.1% in September

The Swiss Federal Statistics Office released its consumer inflation data on Friday. Switzerland's consumer price index rose 0.1% in September, in line with expectations, after a 0.2% drop in August.

The increase was driven by higher prices for clothing and vegetables. Prices for clothing and shoes rose 5.3% in September.

On a yearly basis, Switzerland's consumer price index remained unchanged at -1.4% in September, in line with forecasts. It was the biggest fall since July 1959.

-

11:23

German seasonal adjusted factory orders drop 1.8% in August

Destatis released its factory orders data for Germany on Tuesday. German seasonal adjusted factory orders dropped 1.8% in August, missing expectations for a 0.5% increase, after a 2.2% fall in July. July's figure was revised down from a 1.4% decrease.

The decline was driven by a drop in foreign and domestic orders. Foreign orders decreased by 1.2% in August, while domestic orders fell by 2.6%.

New orders from the Eurozone rose 2.5% in August, while orders from other countries slid 3.7%.

Orders of the intermediate goods fell by 0.4% in August, capital goods orders were down 2.8%, while consumer goods orders decreased 1.5%.

-

11:20

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1170(E200mn), $1.1225(E200mn)

USD/JPY: Y119.90($250mn),Y120.00($1.1bn), Y120.05($250mn)

USD/CAD: Cad1.3150/65($425mn)

USD/CHF: Chf1.000(520mn)

AUD/USD: $0.6900(A$636mn), $0.7200(A$350mn)

EUR/JPY: Y132.50(E440mn)

NZD/USD: $0.6640(NZ$602mn)

-

11:08

Reserve Bank of Australia keeps unchanged its interest rate at 2.00%

The Reserve Bank of Australia (RBA) kept unchanged its interest rate at 2.00% on Tuesday. This decision was expected by analysts.

The RBA Governor Glenn Stevens said that the board' decision was appropriate at this meeting.

He noted that Australia's economy continued to expand moderately.

The RBA governor also said that there is a degree of spare capacity, and the Australian dollar is adjusting to lower commodity prices.

Stevens pointed out that "monetary policy needs to be accommodative", and it "will most effectively foster sustainable growth and inflation consistent with the target".

The central lowered its interest rate twice this year.

-

10:58

New Zealand’s business confidence drops to -14% in the third quarter

The New Zealand Institute of Economic Research (NZIER) released its Quarterly Survey of Business Opinion on late Monday evening. New Zealand's business confidence dropped to -14% in the third quarter from +5% in the second quarter, reaching its lowest level in more than four years.

"The drought and the slowing growth in China and the potential impact on the New Zealand economy - that has made a lot of business uneasy about what's going to be happening in the New Zealand economy in the coming months but as yet they haven't seen the effects in their business," NZIER senior economist Christina Leung said.

-

10:46

International Monetary Fund: China can manage its economic slowdown

The International Monetary Fund (IMF) said on Monday that China can manage its economic slowdown. The IMF noted should implement effective governance.

"This will require, in particular, hardened budget constraints for both state-owned and private firms, and continued strengthening of the financial supervision framework," the lender said.

The IMF also said that a slowdown in the Chinese economy could have a negative impact on its neighbours.

"Spillovers have been magnified by forces that extend beyond China's border - including falling commodity prices and the prospect of an increase in U.S. interest rates - which could produce downward pressure on Asian neighbours," the lender said.

-

10:40

The United States, Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam signs a trade pact

The United States, Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam reached a trade pact, which is known as the Trans-Pacific Partnership. The pact should boost trade between the countries. The countries account for 40% of world gross domestic product.

"This partnership levels the playing field for our farmers, ranchers, and manufacturers by eliminating more than 18,000 taxes that various countries put on our products," U.S. President Obama said in a statement on Monday.

-

10:25

Former Fed Chairman Ben Bernanke: there is no hurry to start raising interest rates

Former Fed Chairman Ben Bernanke said in an interview with CNBC on Monday that there is no hurry to start raising interest rates.

"The goal post was 2 percent inflation. We're not there yet," he said.

"If you raised rates too early and kill the economy, that doesn't help you," he added.

Bernanke pointed out that slow productivity growth weighs on the U.S. economy.

-

10:11

Japanese investment bank Nomura lowers its 2016 GDP growth forecast for China

Japanese investment bank Nomura lowered its GDP growth forecasts for China to 5.8% for next year on Monday, down from the previous estimate of a 6.7% growth. Yang Zhao, Nomura's economist, said that the Chinese economy slowed more sharply than anticipated. He added that the main reason is slowing property investment growth.

-

09:15

Switzerland: Consumer Price Index (YoY), September -1.4% (forecast -1.4%)

-

09:15

Switzerland: Consumer Price Index (MoM) , September 0.1% (forecast 0.1%)

-

09:01

Oil prices climbed

West Texas Intermediate futures for November delivery slightly climbed to $46.29 (+0.06%), while Brent crude rose to $49.38 (+0.26%) amid hopes for a meeting between world's major oil producers.

Russian Energy Minister Alexander Novak told the Sochi-2015 international investment forum October 3 that Russia is ready to discuss oil markets with the Organization of the Petroleum Exporting Countries. However for now there is no information about a confirmed meeting.

Investors are also cautious ahead of U.S. inventory data. Some analysts believe that crude inventories rose further, because refinery activity decreased (89.8% last week compared to 91% in the week before).

-

08:39

Gold retreated, but remained near Friday level

Gold retreated to $1,136.50 (-0.10%), but stayed near a one-week high amid expectations that weak jobs data and recent reports, which also missed expectations, will prevent the Federal Reserve from raising interest rates in 2015. Analysts also said that in the near future bullion might decline due to profit taking after Friday's 2.2% gain.

SPDR Gold Trust, the biggest gold-backed exchange-traded fund in the world, reported a small outflow of 0.22 tonnes on Monday (the first outflow in two weeks).

-

08:37

Global Stocks: U.S. indices continued rising

U.S. stock indices rose on Monday as several disappointing economic reports suggested that the Federal Reserve will postpone a rate hike.

The Dow Jones Industrial Average rose 304.06 points, or 1.9%, to 16,776.43. The S&P 500 gained 35.69, or 1.8%, to 1,987.05 (all of its 10 sectors closed higher). The Nasdaq Composite Index added 73.49, or 1.6%, to 4,781.26.

A report by the Institute for Supply Management showed that the pace of growth in the U.S. services sector slowed in September. The ISM Non-Manufacturing index declined to 56.9 last month from 59 in August, while economists had expected a reading of 58. Three out of four sub-indices fell, while the employment sub-index rose. Despite a weaker-than-expected result the index remained above the 0 threshold, which separates expansion and contraction.

This morning in Asia Hong Kong Hang Seng climbed 0.12%, or 27.23, to 21,881.73. The Nikkei rose 1.31%, or 236.51, to 18,242.00. Markets in China are on holiday until Wednesday.

Asian indices advanced amid expectations that the Federal Reserve will not raise rates this year. Stable oil prices also supported stocks.

Japanese stocks rose on news that the U.S., Japan and 10 other countries reached an agreement on Trans Pacific Partnership. These 12 countries account for 40% of the world economy. The deal includes tariff barrier cutting, investor protection and other aspects.

-

08:34

Foreign exchange market. Asian session: the euro declined

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:30 Australia Trade Balance August -2.79 Revised From -2.46 -2.55 -3.1

03:30 Australia Announcement of the RBA decision on the discount rate 2.0% 2% 2.0%

03:30 Australia RBA Rate Statement

06:00 Germany Factory Orders s.a. (MoM) August -1.4% 0.5% -1.8%

The euro declined slightly against the U.S. dollar ahead of today's release of German industrial production data. Analysts expect the index to fall. Slower growth in China and the scandal around Volkswagen might have weighed on the country's exports.

Market participants are also waiting for ECB President Mario Draghi speech. Also today the International Monetary Fund will report on global economic outlook. If the IMF's report shows clear signs of slowing growth investors might take profits in stock markets. This could support the euro.

This week Portugal will hold elections. Prime Minister Pedro Passos Coelho, who supports austerity, is likely to win.

The Australian dollar rose sharply after the Reserve Bank of Australia left its benchmark rate unchanged at 2%. The central bank noted that the Australian economy continued to expand moderately and it still has spare capacity. Stock markets' volatility did not harm financial markets.

EUR/USD: the pair fell to $1.1170 in Asian trade

USD/JPY: the pair traded within Y120.35-55

GBP/USD: the pair rose to $1.5165

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

07:15 Switzerland Consumer Price Index (MoM) September -0.2% 0.1%

07:15 Switzerland Consumer Price Index (YoY) September -1.4% -1.4%

09:00 Eurozone ECOFIN Meetings

09:00 Eurozone Eurogroup Meetings

12:30 Canada Trade balance, billions August -0.59 -1.2

12:30 U.S. International Trade, bln August -41.86 -47.4

14:00 Canada Ivey Purchasing Managers Index September 58 54

17:00 Eurozone ECB President Mario Draghi Speaks

20:30 U.S. API Crude Oil Inventories September 4.6

21:30 U.S. FOMC Member Williams Speaks

22:30 Australia AiG Performance of Construction Index September 53.8

-

08:25

Options levels on tuesday, October 6, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1400 (5310)

$1.1314 (3243)

$1.1247 (2501)

Price at time of writing this review: $1.1182

Support levels (open interest**, contracts):

$1.1117 (1894)

$1.1081 (3293)

$1.1040 (3062)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 56701 contracts, with the maximum number of contracts with strike price $1,1400 (5310);

- Overall open interest on the PUT options with the expiration date October, 9 is 67169 contracts, with the maximum number of contracts with strike price $1,1000 (5757);

- The ratio of PUT/CALL was 1.18 versus 1.23 from the previous trading day according to data from October, 5

GBP/USD

Resistance levels (open interest**, contracts)

$1.5400 (1469)

$1.5301 (737)

$1.5203 (1576)

Price at time of writing this review: $1.5154

Support levels (open interest**, contracts):

$1.5097 (2716)

$1.4999 (2105)

$1.4900 (1035)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 24967 contracts, with the maximum number of contracts with strike price $1,5500 (1686);

- Overall open interest on the PUT options with the expiration date October, 9 is 23752 contracts, with the maximum number of contracts with strike price $1,5100 (2716);

- The ratio of PUT/CALL was 0.95 versus 0.95 from the previous trading day according to data from October, 5

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:00

Germany: Factory Orders s.a. (MoM), August -1.8% (forecast 0.5%)

-

05:30

Australia: Announcement of the RBA decision on the discount rate, 2.0% (forecast 2%)

-

02:30

Australia: Trade Balance , August -3.1 (forecast -2.55)

-

00:30

Commodities. Daily history for Sep Oct 5’2015:

(raw materials / closing price /% change)

Oil 46.20 -0.13%

Gold 1,135.10 -0.22%

-

00:30

Stocks. Daily history for Sep Oct 5’2015:

(index / closing price / change items /% change)

Nikkei 225 18,005.49 +280.36 +1.58 %

Hang Seng 21,854.5 +348.41 +1.62 %

S&P/ASX 200 5,150.53 +98.52 +1.95 %

Topix 1,463.92 +19.00 +1.31 %

FTSE 100 6,298.92 +168.94 +2.76 %

CAC 40 4,616.9 +158.02 +3.54 %

Xetra DAX 9,814.79 +261.72 +2.74 %

S&P 500 1,987.05 +35.69 +1.83 %

NASDAQ Composite 4,781.26 +73.49 +1.56 %

Dow Jones 16,776.43 +304.06 +1.85 %

-

00:29

Currencies. Daily history for Oct 5’2015:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1183 -0,26%

GBP/USD $1,5147 -0,22%

USD/CHF Chf0,9759 +0,49%

USD/JPY Y120,47 +0,48%

EUR/JPY Y134,73 +0,23%

GBP/JPY Y182,48 +0,25%

AUD/USD $0,7082 +0,51%

NZD/USD $0,6485 +0,62%

USD/CAD C$1,3081 -0,55%

-