Noticias del mercado

-

23:46

PBOC's Shuqing: China growth to be back on track soon

“The world’s second-largest economy is expected to quickly rebound because of the country’s optimized Covid-19 response and after its economic policies continue to take effect,” Bloomberg quotes an interview from Guo Shuqing, party secretary of the People’s Bank of China (PBOC), to People’s Daily published on Sunday.

Additional comments

As China's government gives households and private businesses greater financial support to aid in their recovery now that the Covid Zero policy has ended, China's economic growth will resume its "normal" course.

The key to the economic recovery is to convert current total income to consumption and investment to the largest possible extent.

Incomes will be boosted.

Financial sector should enhance products to enable car, home purchases.

Monetary policy to provide more support for private sector firms to expand credit growth and enable access to more funding.

Yuan will continue to fluctuate, to appreciate in the mid to long term.

PBOC to monitor inflation developments, imported inflation.

Market implications

The news should help the Gold price in keeping the latest advances due to China’s status as one of the world’s biggest XAU/USD consumers.

Also read: Gold Price Forecast: XAU/USD grinds higher ahead of United States Inflation

-

23:32

Japan PM Kishida vows to debate government BOJ roles with new central bank head

Japanese Prime Minister Fumio Kishida said on Sunday his government and the central bank must discuss their relationship in guiding economic policy after he names a new Bank of Japan (BOJ) governor in April, reported Reuters.

The news also adds that the remark heightens the chance the government may revise its a decade-long blueprint with the central bank that focuses on beating deflation, a move that would lay the groundwork for an exit from the BOJ's ultra-loose monetary policy.

"The government and the BOJ must work closely together, but also each play its own role" in achieving price stability and higher wage growth, Kishida said in a program on public broadcaster NHK.

Additional comments

Under the new BOJ governor, we must discuss the relationship between the government and the BOJ.

In guiding monetary policy, policymakers must have a view on the outlook for the economy. There needs to be careful communication and dialogue with markets.

While communicating closely with markets, the BOJ needs to make its policy more flexible with an eye on an eventual normalization of monetary policy.

Market implications

USD/JPY reacts to the diplomatic comments by extending Friday’s pullback from a three-week high, depressed around 132.00 by the press time.

-

23:32

AUD/USD advances to near 0.6880 amid upbeat market mood, more upside seems favored

- AUD/USD is aiming to explore above 0.7000 as risk-on impulse hogs limelight.

- A sheer decline in US Average Hourly Earnings has triggered volatility in the US Dollar Index.

- The Australian Dollar will remain in action ahead of the release of the monthly CPI data and Retail Sales data.

The AUD/USD pair is expected to turn sideways after a juggernaut rally to near the crucial resistance of 0.6880. For further upside, more buying interest will be required from the investing community to push the Australian Dollar above the aforementioned hurdle. Positive market sentiment will continue to provide support to the risk-sensitive currencies.

The risk appetite of investors soared heavily after a downside revision of the Average Hourly Earnings data, released on Friday. Risk-perceived assets like S&P500 witnessed immense buying interest from the market participants as downbeat wage inflation provided the message ‘loud and clear’ that the United States Consumer Price Index (CPI) will continue its downside momentum ahead. Things are falling in place as desired by the Federal Reserve (Fed), therefore the central bank won’t be needed to hike terminal rate projections.

The US Dollar Index (DXY) is expected to re-test its six-month low at around 103.05 amid a soaring market mood. Also, the demand for US government bonds escalated, which led to a decline in 10-year US Treasury yields to 3.56%.

Going forward, the Australian Dollar will remain in action ahead of the release of the monthly CPI data, which is scheduled for Wednesday. As per the consensus, the annual CPI (Nov) will escalate to 7.3% vs. the prior release of 6.9%. Also, the Australian Retail Sales data will hog the limelight, which is seen higher at 0.7% against the former figure of -0.2%.

AUD/USD technical outlook

On a four-hour scale, AUD/USD is hovering around the horizontal resistance plotted from December 13 high around 0.7000. Advancing 20-and50-period Exponential Moving Average (EMAs) at 0.6813 and 0.6790 respectively add to the upside filters.

The Relative Strength Index (RSI) (14) is looking to shift into the bullish range of 60.00-80.00, which will trigger a bullish momentum ahead.

-

23:30

Latest talks of Fed officials flash mixed signals for markets

Having witnessed firmer US employment numbers and a disappointment from the ISM Services PMI for December, multiple Federal Reserve (Fed) officials opined for the US economic conditions and the central bank’s next move.

Notable among them were Atlanta Federal Reserve President Raphael Bostic, Outgoing Chicago Fed President Charles Evans, Kansas City Fed President Esther George and Richmond Federal Reserve Bank President Thomas Barkin.

Firstly, the Wall Street Journal (WSJ) quoted Chicago Fed President Evans saying, “It was possible the economic data would support raising the policy rate by 25 basis points at the Fed's next gathering.”

“The Fed is in a good spot having stepped down to a 50-basis-point increase in December,” added Fed’s Evans per WSJ reported Reuters.

The news also mentioned Chicago Fed President as saying, "If they step it down again to 25 basis points that allows a little more time - as they continue to increase the funds rate to the same point that I was expecting - to let the data evolve.”

Following him were the additional comments from Atlanta Fed President Bostic who mentioned that the holiday shopping numbers could influence rate decision, “if consumers proved more or less resilient”. The policymaker previously raised possibilities of the US economic slowdown on Friday.

Also read: Fed's Bostic: US economy is definitely slowing

Additionally, Kansas City Fed President Esther George signalled that the longer inflation stays high, the greater the chance it will get embedded and will be more costly to combat. The policymaker also stated that the renewed inflation pressures from energy, crop prices are ‘very real risk’. “How much additional policy tightening will be needed is an ‘essential aspect’ of deliberations,” per Fed’s George.

Richmond Fed President Barkin praised the last two months of inflation reports by terming them as “a step in the right direction,” but marked fears from the higher median figures. “Studies forecast 6-12 months before pullbacks in demand quiet the rate of inflation,” added Fed’s Barkin.

The policymaker also stated that more gradual interest rate path should limit harm to economy while also adding, “(It) makes sense to steer more deliberately on rates in context of policy lags.”

Market implications

Despite the mixed comments from the Fed officials, the majority of them do support softer rate hikes, which in turn suggests further hardships for the US Dollar.

Also read: EUR/USD Weekly Forecast: US Dollar starts off 2023 on the right foot

-

23:28

UK PM Sunak: Open to discussing pay rises for nurses

British Prime Minister Rishi Sunak said on Sunday he was willing to discuss pay rises for nurses in a bid to end strikes that have deepened a crisis within the health service the day before the government meets with trade union leaders, reported Reuters.

The government was willing to have conversations with union leaders about pay, despite ministers previously refusing to reopen talks about this year's deal.

"We want to have a reasonable, honest, two-way conversation about pay," Sunak told the BBC per Reuters. "The door has always been open to talk about the things that nurses want to talk about, and the unions want to talk about more generally."

Additional comments

As a general policy I wouldn’t ever talk about me or my family’s healthcare situation. It’s not really relevant.

You have to continue to be disciplined and make the right responsible decisions in order to bring inflation down.

It's really important that we do. Its (inflation) not an abstract thing. Its impacting people.

Market implications

The news should help the GBP/USD pair to extend the latest run-up towards crossing the 1.2130 hurdle, around 1.2090 by the press time.

Also read: GBP/USD Weekly Forecast: Will Pound Sterling sellers retain control?

-

23:24

Gold Price Forecast: XAU/USD grinds higher ahead of United States Inflation

- Gold price makes rounds to seven-month high as bulls take a breather.

- Mixed data from United States weighed on Treasury bond yields, US Dollar and propelled XAU/USD price.

- Upbeat signals from China also underpinned Gold price upside.

- Firmer US inflation data could probe XAU/USD bulls.

Gold price (XAU/USD) seesaws around the highest levels since June, close to $1,866 by the press time, after printing the biggest daily jump in five weeks the previous day.

The yellow metal cheered broad US Dollar selling, despite a mostly upbeat United States employment report, while posting the gains on Friday. The reason could be linked to the downbeat prints of the US ISM Services PMI as well as the Factory Orders that drowned the Treasury bond yields. On the contrary, price-positive updates from China helped the XAU/USD to remain firmer.

United States economics weigh on Treasury bond yields, propel Gold price

On Friday, United States Nonfarm Payrolls (NFP) rose by 223,000 in December compared to the market expectations of 200,000 and November's increase of 256,000 (revised from 263,000). Further details of the US December jobs report revealed that the Unemployment Rate declined to 3.5% from 3.6% in November and 3.7% expected. More importantly, the Average hourly earnings rose 0.3% in December versus 0.4% prior while the YoY figures eased to 4.6% from 4.8% in November.

Further, US ISM Services PMI slumped to the lowest levels in 31 months while suggesting a contraction in activities with 49.6 figures for December, versus the market expectations of 55 and 56.5 marked in November. On the same line, US Factory Orders also slumped, falling 1.8% in November after gaining 0.4% in October.

Despite the mixed readings of the key US data, Atlanta Federal Reserve bank president Raphael Bostic stated that the US economy is definitely slowing, which in turn drowned the key US Treasury bond yields and the US Dollar. That said, the US 10-year Treasury yields dropped 16 basis points (bps) to 3.56%, the lowest levels in three weeks, whereas the US Dollar Index (DXY) marked the biggest daily slump since November 11. Given the inverse relationship between the Gold price and the US Dollar, the yellow metal managed to refresh the multi-day high afterward.

China-linked optimism adds strength to XAU/USD upside

Considering China’s status as one of the world’s biggest Gold consumers, recent positive developments from the dragon nation seemed to also have underpinned the XAU/USD upside.

On Sunday, China opened air, land and sea borders for travelers after a three-year shutdown and marked the last effort to unlock the Covid-led economy. “After three years, mainland China opened sea and land crossings with Hong Kong and ended a requirement for incoming travelers to quarantine, dismantling a final pillar of a zero-COVID policy that had shielded China's 1.4 billion people from the virus but also cut them off from the rest of the world,” mentioned Reuters.

Additionally, the dragon nation’s recent piling of the Gold holdings also favors the XAU/USD bulls. As per the latest updates from the People's Bank of China (PBOC) website, China increased its holdings of gold by 30 tonnes in December to 2,010 tonnes. That said, Beijing previously added 32 tonnes in November. It should be noted that such high levels of Gold inflows were earlier spotted in September 2019 and October 2016.

US inflation is the key

The mixed US data and a slump in the United States Treasury bond yields recently pushed multiple Federal Reserve (Fed) officials to flag recession fears. However, a firmer US Consumer Price Index (CPI) for December, up for publishing on Thursday, won’t hesitate to shift the market’s focus on the Fed rate hike concerns and could propel the US Dollar, which in turn will challenge the Gold buyers.

Also read: Gold Price Weekly Forecast: Bulls retain control ahead of key US inflation data

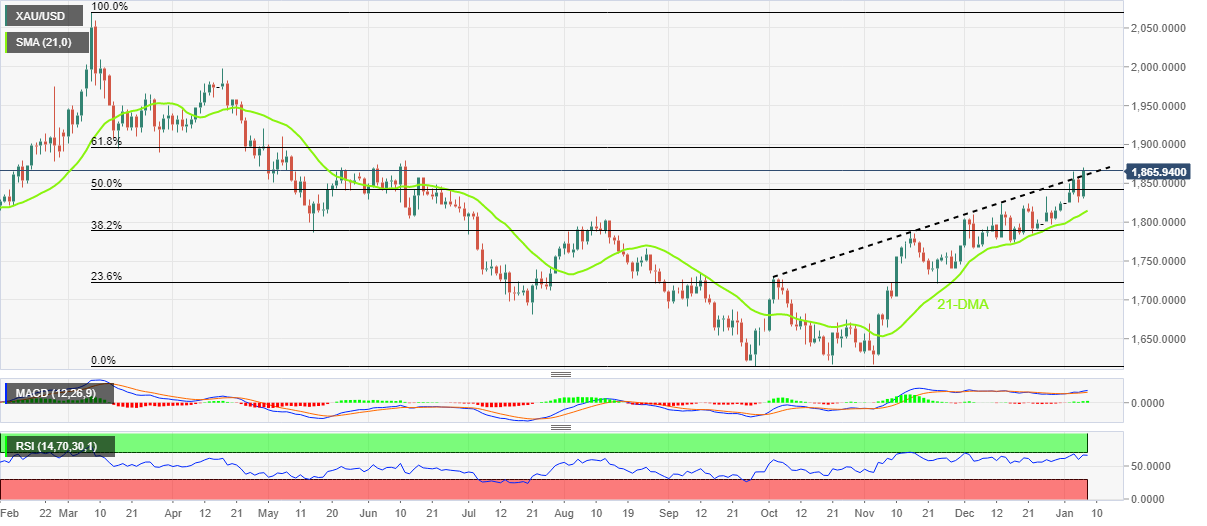

Gold price technical analysis

Gold price grinds near a multi-day high after crossing an upward-sloping resistance line from early October 2022, now immediate support around $1,860. The upside momentum also takes clues from the Moving Average Convergence and Divergence (MACD) indicator’s bullish signals and the firmer Relative Strength Index (RSI) line, placed at 14.

It’s worth noting, however, that the RSI line is near the overbought territory and also portrays a lower-high formation since early November, which in turn suggests a limited upside room for the XAU/USD.

As a result, June’s high near $1,880 and the 61.8% Fibonacci Retracement level of the Gold’s March-September 2022 downturn, near $1,897, quickly followed by the $1,900 threshold, gain the market’s attention.

In a case where the Gold price remains firmer past $1,900, multiple hurdles surrounding $1,915, $1,935 and $1,965 could challenge the buyers before directing them to the $2,000 psychological magnet.

Alternatively, a downside break of the $1,860 resistance-turned-support could drag the XAU/USD to the 50% Fibonacci retracement level of $1,842. However, the 21-Day Moving Average (DMA) and August month’s high, respectively around $1,811 and $1,807, could restrict the Gold price downside afterward.

Overall, Gold seems to have a limited upside room even if the bullish bias remains intact.

Gold price: Daily chart

Trend: Further upside expected

-

23:01

EUR/USD sees more upside above 1.0650 despite upbeat US NFP

- EUR/USD is expected to extend a rally above 1.0650 on less-hawkish Fed bets.

- A sheer drop in US Average Hourly Earnings will be added to the downside inflation filters.

- The USD Index witnessed a bloodbath, dropping to 103.50 amid the risk-on market mood.

The EUR/USD pair is hovering around 1.0650 in the early Asian session after a juggernaut rally on Friday. The major currency pair picked a sheer demand despite the release of the upbeat United States Nonfarm Payrolls (NFP) data. As per the US official employment data, the United States economy added 223K fresh jobs in December month, much higher than the consensus of 200K but lower than the former release of 256K.

The sentiment of the market participants turned highly positive as the impact of upbeat NFP was already discounted after solid Automatic Data Processing (ADP) Employment Change data. Apart from that, the catalyst that triggered the risk-appetite theme was the decline in the Average Hourly Earnings (Dec). S&P500 had a ball as the index soared more than 2.25%.

The Average Hourly Earnings dropped to 4.6% vs. the consensus of 5.0% and the former release of 4.8%. Investors were worried about the fact that a rise in labor demand would be offset by higher wage inflation as firms would offer higher wages to attract talent. Higher wage growth might lead to a rebound in overall inflation and will force the Federal Reserve (Fed) to either hike terminal rate projections or continuation of maintaining hawkish monetary policy beyond CY2023 or both.

The US Dollar Index (DXY) witnessed a bloodbath, dropping heavily from 105.00 to critical support around 103.50. The USD Index is highly expected to continue its downside momentum further. While the 10-year US Treasury yields dropped to 3.56%.

On the Eurozone front, the annual Harmonized Index of Consumer prices (HICP) (Dec) dropped to 9.2% vs. the expectations of 9.7% and the former release of 10.1%. Inflationary pressures dropped in Eurozone led by falling energy prices, which are delighting the European Central Bank (ECB).

-