Noticias del mercado

-

23:07

South Korea Export Price Growth (YoY): 10.7% (December) vs 7%

-

22:49

NZD/USD Price Analysis: mild bounce overshadowed by multi-year lows

- NZD/USD edges up 0.11% on Tuesday, hovering near 0.5600 after a brief recovery attempt.

- MACD histogram shows decreasing green bars, pointing to limited follow-through despite the rebound.

The NZD/USD pair gained modestly on Tuesday, inching up to approximately 0.5600 following a prolonged slump to levels unseen since October 2022. Although this slight uptick provides temporary relief from the recent selling streak, the overarching bias remains tilted to the downside.

From a technical perspective, the Relative Strength Index (RSI) has climbed to 43, an indication of some stabilizing momentum while still embedded in negative territory. Meanwhile, the Moving Average Convergence Divergence (MACD) histogram is printing fewer green bars, suggesting that any ongoing recovery could be fragile without additional bullish impetus.

On the downside, should the pair fail to hold above 0.5570, sellers may seize control once more, potentially targeting the 0.5530 mark. Conversely, a rally beyond the 0.5620 region could set the stage for a test of 0.5650, though any extended move higher would likely hinge on a more decisive shift in market sentiment.

NZD/USD daily chart

-

22:38

United States API Weekly Crude Oil Stock came in at -2.6M, above expectations (-3.5M) in January 10

-

22:21

Gold price climb on investors renewed Fed easing hopes

- Gold rebounds from weekly low, fueled by hopes for looser Fed policy after weak PPI.

- Focus on upcoming CPI; cooler report could boost chances for rate cuts.

- Potential Trump tariffs pose a risk to inflation, impacting Gold and market sentiment.

Gold prices edged higher on Tuesday after data from the United States (US) showed that prices paid by producers cooled off. This kept traders hopeful for additional monetary policy easing by the US Federal Reserve (Fed). At the time of writing, the XAU/USD trades at $2,675, up 0.46%.

The yellow metal recovered after beginning the week on the back foot, down over 1%. The US Bureau of Labor Statistics (BLS) revealed that the Producer Price Index (PPI) increased but missed estimates for a higher print. This exacerbated Gold’s jump as traders grew optimistic that if the Consumer Price Index (CPI) report on Wednesday comes cooler than foreseen, it could increase the Fed’s chances of easing policy during the year.

Market participants are eyeing the CPI release on Wednesday. If December prints are below the prior month’s 2.7% number, it could indicate that the disinflation process continues. Inflation has risen since October to 2.6%, following September’s 2.4% YoY increase.

Traders had priced in 29.4 basis points of easing by the Federal Reserve in 2025. But a cool CPI report could bolster bullion prices.

Earlier, Kansas City Fed President Jeffrey Schmid stated that the Fed would act if Trump’s tariffs threw inflation or jobs off course.

In six days, US President-elect Donald Trump will take office. He has threatened to impose universal tariffs, though focused mainly on China, Canada and Mexico. If he goes ahead with this, analysts have mentioned that a trade war could reignite inflation.

Bullion prices are also taking a hit amid good news of a possible deal that could end Gaza's war, according to Reuters, which cited an official briefed on the matter.

In the US, key data releases include consumer inflation figures, Retail Sales and jobless claims for the week ending January 11.

Daily digest market movers: Gold price advances on steady US yields

- Gold price shrugs off higher US real yields, which remain at around 2.34%.

- The US Dollar retreated after the data, with the US Dollar Index (DXY) hitting 109.21, down 0.26%.

- The US 10-year Treasury bond yield remains unchanged at 4.794%.

- The US PPI in December rose 3.3% YoY, below forecasts of 3.4%. Excluding volatile items, the so-called Core PPI expanded by 3.5% YoY, up from November’s figures but beneath 3.8% expectations.

XAU/USD technical outlook: Gold price soars above $2,650 as bulls stepped in

Gold price uptrend resumed after a ‘bearish engulfing’ chart pattern formed, inviting buyers to step in and increase prices. If Bullion clears $2,700, the next resistance would be the December 12 peak of $2,726, followed by the record high at $2,790.

Conversely, if XAU/USD drops below $2,650, the next support would be the 50-day Simple Moving Average (SMA) at $2,643, followed by the 100-day SMA at $2,633.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

-

22:00

South Korea Import Price Growth (YoY) up to 7% in December from previous 3%

-

22:00

New Zealand NZIER Business Confidence (QoQ) up to 16% in 4Q from previous -1%

-

21:28

Australian Dollar rebounds from multi-year lows but upside remains limited

- AUD edges up to 0.6180 on Tuesday, off multi-year lows.

- Fed rate-hold expectations in January underpin the US Dollar.

- Soft Australian fundamentals, China slowdown cap Aussie recovery.

The Australian Dollar (AUD) rebounded from 0.6130, its lowest level since April 2020, to reach 0.6180 on Tuesday, buoyed by firm commodity prices and a slight improvement in market sentiment. Despite this partial comeback, the pair still remains vulnerable amid a dovish Reserve Bank of Australia (RBA) and an uncertain local economic outlook.

Daily digest market movers: Aussie sees some light after soft PPI data from the US

- The US Dollar Index (DXY) retreats after Monday’s gains but keeps an overall firm tone, supported by the Fed’s likely rate hold in January.

- Producer Price Index (PPI) data in the US rose 3.3% year-over-year for December, missing the 3.4% forecast; core PPI reached 3.5%, also below estimates.

- Following the data, US Treasury yields dropped, favouring the pair’s upside, but the USD’s outlook remains favourable.

- Consumer Price Index data on Wednesday will be key for the pair’s trajectory.

AUD/USD technical outlook: Bulls eye 20-day SMA as pair hovers near oversold territory

The Relative Strength Index (RSI) stands at 42, rising sharply but still in negative territory, while the Moving Average Convergence Divergence (MACD) histogram prints flat red bars, indicating only modest relief for bulls. While the Aussie has managed to halt its latest losing streak, the pair remains near April 2020 lows. Any sustained recovery may require a clear break above the 20-day Simple Moving Average (SMA), which is currently acting as a barrier to further upside.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

-

20:59

Canadian Dollar catches some relief as Greenback eases

- The Canadian Dollar gained a slim 0.3%, but remains mired in congestion.

- Canada remains absent from the data docket on Tuesday.

- Cooler-than-expected US PPI inflation figures calm market tensions.

The Canadian Dollar (CAD) caught a thin bid on Tuesday, bostlered by a general easing in US Dollar flows after US Producer Price Index (PPI) inflation accelerated at a slower pace than markets expected in December. Traders’ hopes that this week’s US Consumer Price Index (CPI) print will also come in below expectations have been reignited following the PPI print, although the figure is ultimately expected to rise over previous periods.

Canada remains almost entirely absent from the economic data release schedule this week, with only low-tier data on the offering. The Bank of Canada (BoC) is broadly expected to continue trimming rates while the Federal Reserve (Fed) is slated to hold off on any further rates cuts through the first half of 2025, which will widen the CAD’s rate differential against the Greenback.

Daily digest market movers: CAD gets a step up thanks to US data

- The Canadian Dollar is up, forcing the USD/CAD pair back down below the 1.400 handle, but market flows remain one-sided as the Loonie lacks intrinsic momentum.

- PPI inflation figures eased broadly below expectations in December, with headline PPI printing at just 0.2% MoM.

- Investors were expecting a downtick to 0.3% from the previous 0.4%.

- Core PPI, excluding price increases in volatile food and energy prices, was flat in December versus the forecast of 0.3% and 0.2% last.

- headline PPI inflation rose to 3.3% YoY versus the previous figure of 3.0%, while core PPI accelerated to 3.5% YoY compared to the previous 3.4%.

Canadian Dollar price forecast: CAD set to continue rising as long as market holds off on USD bidding

The Canadian Dollar’s gain on Tuesday amounted to one-third of one percent, a scant percentage with the Loonie parked near multi-year lows against the Greenback. Loonie bidders are struggling to push USD/CAD back into the latest swing low into the 1.4300 handle, but USD bulls continue to get wrapped up in a congestion zone around 1.4400, stamping in a tight consolidation range.

A lack of momentum is bleeding clear signals out of momentum oscillators, and long-run moving averages are beginning to catch up to bids, leaving candlesticks exposed to a difficult chart space looking forward.

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

-

20:48

Forex Today: Investors shift their focus to US CPI data

The Greenback traded on the defensive once again on Tuesday, testing two-day lows and weighed down by another tariff story as well as disappointing US Producer Prices, while market participants got ready for the release of the more relevant CPI on Wednesday.

Here is what you need to know on Wednesday, January 15:

The US Dollar Index (DXY) retreated to the low-109.00 amid weaker yields and the generalised recovery in the risk-associated assets. The release of the CPI will take centre stage, seconded by usual MBA Mortgage Applications, the NY Empire State Manufacturing Index, and the Fed Beige Book. In addition, the Fed’s Barkin, Kashkari, Williams, and Goolsbee are all due to speak.

EUR/USD rebounded further from Monday’s fresh cycle lows near 1.0180 and traded at shouting distance from the 1.0300 hurdle. Wholesale Prices in Germany and the Full Year GDP Growth are expected along with the speech by the ECB’s Lane and De Guindos.

Following a brief drop to the sub-1.2100 region, GBP/USD regained some composure and revisited the 1.2250 zone. Key UK Inflation Rate will be at the centre of the debate, seconded by a 10-year Gilt auction.

USD/JPY reversed three consecutive daily pullbacks and advanced to two-day highs just above the 158.00 barrier. The Reuters Tankan Index and Machine Tool Orders are due.

Renewed selling pressure in the Greenback allowed AUD/USD to briefly trespass the 0.6200 hurdle and print three-day peaks on Tuesday. Next of relevance in Oz will be the publication of the jobs report on January 16.

WTI prices gave away part of the recent three-day strong climb and slipped back below the $78.00 mark per barrel.

Gold prices resumed their ascent and retested the vicinity of the $2,680 mark per troy ounce encouraged by the weaker Dollar and lower yields. Silver prices traded with decent gains although another move above the key $30.00 mark per ounce remained elusive.

-

20:06

Argentina Consumer Price Index (MoM): 2.7% (December) vs 2.4%

-

20:00

United States Monthly Budget Statement registered at $-87B, below expectations ($-75B) in November

-

19:39

Mexican Peso rallies as US PPI shows moderate rise

- Mexican Peso strengthens as December US PPI data suggests easing inflation, lessening Fed pressure.

- Gross Fixed Investment data and President Sheinbaum's nearshoring incentives may further Peso influence.

- US focus on CPI; upcoming retail sales and jobless claims to guide Fed decisions.

The Mexican Peso recovered some ground against the US Dollar on Tuesday after US inflation data suggested that prices paid by producers rose moderately but below economists’ estimates. Although it didn’t change traders' views that the US Federal Reserve (Fed) could lower rates just once in 2025, the Greenback remained on the back foot, a headwind for USD/MXN, which trades at 20.45, down 0.95%.

Mexico’s economic docket remains scarce, but Gross Fixed Investment for October will be released on January 15. Meanwhile, President Claudia Sheinbaum presented a plan to boost nearshoring incentives and reduce the country’s imports from China.

In the US, the December Producer Price Index (PPI) dipped less than estimates, indicating that inflation has resumed its downward trend. Nevertheless, traders are eyeing the release of the latest Consumer Price Index (CPI) for the same period, which is expected to remain around familiar levels.

The US economic schedule will feature the CPI, Fed speakers, Retail Sales data and jobless claims data for the week ending January 11.

Daily digest market movers: Mexican Peso counterattacks ahead of US CPI report

- The Mexican currency advanced on news that the upcoming Trump team is considering gradual tariff hikes of 2% to 5% on a monthly basis.

- Sheinbaum’s “Plan Mexico” would offer incentives for nearshoring, including tax deductions, and develop plans for individual sectors. The decree, which will be published on January 17, offers incentives to domestic and foreign companies.

- Former Deputy Finance Minister Alejandro Werner said in an article by El Economista that the Mexican economy would enter a recession this year and could lose its investment-grade status before 2027.

- The US PPI rose by 3.3% YoY below estimates of 3.4%, up from 3%. Core PPI expanded 3.5% YoY, missed forecasts for a 3.8% increase, up a tenth from 3.4%.

- Last week, Banco de Mexico (Banxico) revealed December's meeting minutes. The minutes showed that inflation continues to trend lower, suggesting that the easing cycle might continue. Banxico's Governing board stated that "larger downward adjustments could be considered in some meetings."

- Kansas City Fed President Jeffrey Schmid said that the Fed will act if Trump’s tariffs throw inflation or jobs off course.

- The Fed's latest Meeting Minutes showed that despite reducing rates, some policymakers supported keeping the fed funds rate unchanged as worries had grown that inflation risks were skewed to the upside.

- Consequently, they adopted a more gradual approach as Fed officials opened the door to slowing the pace of interest rate cuts.

USD/MXN technical outlook: Mexican Peso recovers as USD/MXN falls below 20.50

The USD/MXN uptrend remains in place as long as buyers hold prices above the 50-day Simple Moving Average (SMA) of 20.32, but over the short-term momentum has shifted slightly bearish.

The Relative Strength Index (RSI) is bullish but aims down toward its neutral line, hinting that sellers are stepping in. Therefore, the USD/MXN first support will be the 50-day SMA, followed by the 20.00 figure. On further weakness, the 100-day SMA will be tested at 19.98.

Conversely, if USD/MXN rises past 20.50, the first resistance will be the year-to-date (YTD) peak of 20.90. If surpassed, the next stop would be the March 8, 2022 high of 21.46, ahead of 21.50 and the 22.00 psychological level.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

-

19:17

US Dollar dips as softer PPI data temper bullish momentum

- Traders exhibit caution following below-forecast US PPI figures that spark fresh inflation debates in global markets.

- President-elect Donald Trump’s potential remarks on tariffs and trade policies keep investors vigilant, unsure of the Dollar’s immediate trajectory.

- The Federal Reserve’s steady rate stance for January remains likely, but any inflation surprises could sway policy expectations again.

The US Dollar Index, which measures the value of the USD against a basket of currencies, is on the backfoot after the December Producer Price Index (PPI) was released. Traders are on edge over possible comments from President-elect Donald Trump on the above headline. The US Dollar Index (DXY) dips below 110.00 and looks for support to bounce back.

Daily digest market movers: USD eases on hot NFP report momentum as PPI disappoints

- December’s Producer Price Index (PPI) was softer than anticipated: core monthly PPI at 0.0% vs. 0.3% expected, headline at 0.2% vs. 0.3%, and yearly readings coming in below forecasts.

- The US Dollar weakened on this report, but analysts remain confident in the ongoing rally and view the tariff noise as short-lived.

- Inflation concerns persist, with sticky underlying price pressures suggesting the Federal Reserve (Fed) will retain its cautious easing pace into 2025.

- Yield softening sees the 10-year benchmark slip to around 4.80% from its 14-month high, reflecting market uncertainty post-PPI.

- CME FedWatch Tool shows that traders have already priced in the chance of unchanged rates at January’s meeting, underscoring the Fed’s data-dependent posture and potential Trump-driven volatility.

DXY technical outlook: Respite after softer data, but structure remains positive

The US Dollar Index witnessed a temporary dip below the 110.00 mark, pressured by profit-taking and underwhelming PPI numbers. Despite this pullback, the broader uptrend stays intact, hovering near multi-year highs. Indicators show a mild slowdown, hinting at a potential short-term consolidation phase. If profit-taking intensifies, the index may slip further, probably towards 107.00-108.00; however, strong fundamentals and robust Fed guidance suggest the Dollar could quickly find a bid, preserving its longer-term bullish bias.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

-

18:26

Dow Jones Industrial Average churns post-PPI print

- The Dow Jones tested higher ground after US producer inflation chilled in December.

- Despite an uptick in investor sentiment, markets are still apprehensive.

- Investors await Wednesday’s key CPI inflation print before making decisions.

The Dow Jones Industrial Average (DJIA) lurched around 150 points higher on Tuesday after Producer Price Index (PPI) inflation printed below median market forecasts. Treasury yields ticked down and equities explored the higher end after cooling inflation pressures gave investors a reason to look forward to key Consumer Price Index (CPI) inflation figures due on Wednesday. The bid in equities was short-lived, and the Dow Jones is now sinking back below Tuesday’s opening bids and exploring the 42,200 handle once again.

PPI inflation figures eased broadly below expectations in December, with headline PPI printing at just 0.2% MoM. Investors were expecting a downtick to 0.3% from the previous 0.4%. Core PPI, excluding price increases in volatile food and energy prices, was flat in December versus the forecast of 0.3% and 0.2% last.

Annualized PPI inflation tells a slightly different story: headline PPI inflation rose to 3.3% YoY versus the previous figure of 3.0%, while core PPI accelerated to 3.5% YoY compared to the previous 3.4%. While both figures came in below expectations, the print wasn’t quite the boon to investor sentiment that many were hoping for as inflation pressures continue to simmer away in the background, albeit at a slightly lower boil than economists forecast. With inflation metrics still trending well above annualized Federal Reserve (Fed) targets, PPI figures printing below forecasts is a distinction without a difference when it comes to expectations of interest rate decreases.

Dow Jones news

Roughly half of the Dow Jones board is in the green on Tuesday, though steeper losses in key favorites are keeping the overall index slightly underwater for the day. Boeing (BA) backslid around 3%, falling to $165 per share after the aerospace manufacturer reported fewer customer deliveries than analysts expected. Boeing is slated to release its latest earnings report on January 28.

Salesforce (CRM) and Caterpillar (CAT) are two of the big winners on the Dow, rising around 1.5% apiece as investors continues to pivot out of tech favorites and bid up adjacent-industry familiars. CRM is knocking on $324 per share while CAT is trading into $368 per share.

Dow Jones price forecast

The Dow Jones is discovering some chart churn as bidders look to dig in some footholds above the 42,000 major price handle. The major equity index has backslid 7.4% top-to-bottom from record bids near 45,070 set in late November. Bulls are struggling to catch the backslide as the 200-day Exponential Moving Average (EMA) comes into view, and price action is poised to tap the key long-term average for the first time since November of 2023.

The immediate barrier to a technical recovery will be the 50-day EMA falling into 43,040. A near-term technical floor appears to be firming up at 42,000, but a fresh push into the low end could see supports snap.

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

-

16:42

EUR/USD Price Analysis: Pair attempts mild rebound but outlook remains negative

- EUR/USD slips marginally to 1.0270 on Tuesday, ending a five-day losing streak.

- RSI currently at 37, moving sharply higher despite remaining in negative territory.

The EUR/USD pair managed to eke out a modest recovery on Tuesday, edging down to 1.0270 yet avoiding a sixth consecutive day in the red. Despite this fragile bounce, the pair remains under pressure, underscoring the persistent headwinds that have characterized its performance over the past week.

Technical indicators offer a mixed perspective. While the Relative Strength Index (RSI) has ticked up to 37 and shows signs of life, it continues to reside in negative territory. Meanwhile, the Moving Average Convergence Divergence (MACD) histogram prints flat red bars, suggesting that the recent reprieve may lack the follow-through needed to spark a robust bullish reversal.

Looking ahead, immediate support stands near the 1.0250 handle, with any drop below that level potentially exposing the 1.0220 region. On the upside, overcoming resistance around 1.0300 would be essential to bolster the pair’s recovery attempt, opening the door for a possible retest of the 1.0350 zone if bullish momentum takes hold.

EUR/USD daily chart

-

16:09

United States RealClearMarkets/TIPP Economic Optimism (MoM) below forecasts (55.1) in January: Actual (51.9)

-

16:00

GBP/USD Price Forecast: Tumbles below 1.2200 after US PPI data

- GBP/USD extends downtrend, slipping below 1.2200 after US inflation release.

- Next GBP/USD support at 1.2136; potential drop to 1.2100 may hit a new year-to-date low.

- Recovery above 1.2200 needed to challenge the week’s high at 1.2249, further resistance up to 1.2351.

The GBP/USD plunged below 1.2200 during the North American session following the release of US producer price inflation data, which hinted that prices dipped slightly but close to Wall Street's estimates. At the time of writing, the pair trades at 1.2166, down by over 0.26%.

GBP/USD Price Forecast: Technical outlook

The downtrend remains intact even though buyers lifted the pair to an intraday high of 1.2249. However, sellers sold the rip driving the GBP/USD below 1.2200, extending its losses to current exchange rates.

If GBP/USD drops below 1.2150, the next support would be the day’s low of 1.2136. On further weakness, 1.2100 emerges as the next floor level, followed by the current year-to-date (YTD) low of 1.2099.

Meanwhile, GBP/USD must reclaim 1.2200 for a bullish resumption before testing the week’s peak of 1.2249. A breach of the latter will expose the April 2024 swing low of 1.2299, ahead of 1.2300. If surpassed, the next stop would be the January 2 daily low of 1.2351.

GBP/USD Price Chart - Daily

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

-

14:55

United States Redbook Index (YoY) dipped from previous 6.8% to 4% in January 10

-

14:36

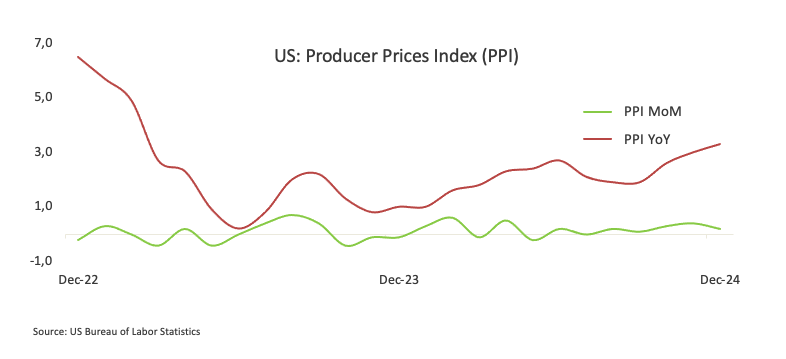

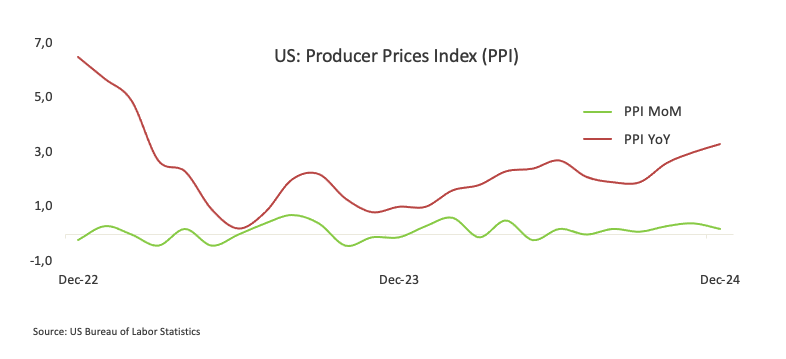

US: Headline Producer Prices rose below estimates 3.3% YoY in December

The latest data from the Bureau of Labor Statistics (BLS) shows that Producer Prices climbed 3.3% in December compared to a year earlier. This was below expectations of 3.4% and a decent uptick from November's 3.0% increase.

Excluding the often volatile food and energy categories, Producer Prices rose 3.5% over the last twelve months, again coming in short of the forecast of 3.8% and outpacing the 3.4% growth seen in the previous report.

On a monthly basis, the headline Producer Price Index (PPI) increased by 0.2%, while the core PPI (excluding food and energy) came in flat. Both figures disappointed market predictions.

Market reaction

The US Dollar treads water around 109.50 when tracked by the US Dollar Index (DXY) following Monday's knee-jerk and despite hitting a new cycle peak past the 110.00 barrier.

-

14:32

EUR/GBP Price Forecast: Aims to revisit four-month high of 0.8450

- EUR/GBP extends winning spree amid sheer weakness in the Pound Sterling.

- Surging borrowing costs for the UK government have weighed on their economic outlook.

- The Euro gains despite expectations for the ECB to reduce interest rates by 100 bps by the mid-summer.

The EUR/GBP pair extends its winning streak for the fifth trading day on Tuesday. The cross outperforms as the Pound Sterling (GBP) performs weakly across the board, given that the United Kingdom’s (UK) economic outlook has faltered due to rising yields on Britain’s gilt securities.

The 30-year yields on UK gilts have risen to 5.47%, the highest level seen in more than 26 years. The surge in the UK government’s borrowing cost is partly driven by the uncertainty over incoming trade policies by United States (US) President-elect Donald Trump and the nation’s heavy reliance on foreign financing.

Investors expect that higher borrowing costs could force Chancellor of the Exchequer Rachel Reeves to go against her fiscal rules as she vowed, in the autumn budget, to rely on foreign borrowing for funding investment and not on day-to-day spending.

Meanwhile, the Euro (EUR) performs strongly against its major peers on Tuesday even though the European Central Bank (ECB) is expected to continue reducing interest rates this year. The ECB cut its Deposit Facility rate by 100 basis points (bps) to 3% in 2024 and is expected to cut further by a similar size by the mid-summer.

Euro PRICE Today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the strongest against the British Pound.

USD EUR GBP JPY CAD AUD NZD CHF USD -0.26% 0.29% 0.16% -0.02% -0.10% -0.36% -0.11% EUR 0.26% 0.56% 0.39% 0.25% 0.16% -0.10% 0.15% GBP -0.29% -0.56% -0.13% -0.31% -0.37% -0.66% -0.40% JPY -0.16% -0.39% 0.13% -0.17% -0.24% -0.52% -0.26% CAD 0.02% -0.25% 0.31% 0.17% -0.08% -0.34% -0.08% AUD 0.10% -0.16% 0.37% 0.24% 0.08% -0.25% -0.01% NZD 0.36% 0.10% 0.66% 0.52% 0.34% 0.25% 0.25% CHF 0.11% -0.15% 0.40% 0.26% 0.08% 0.01% -0.25% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent EUR (base)/USD (quote).

EUR/GBP extends its weekly rally to near 0.8430. The cross strengthened after breaking above the December 27 high of 0.8329, which has become a support now. A fresh bull cross, suggested by the 20- and 50-day Exponential Moving Averages (EMAs) near 0.8330, indicates a strong uptrend.

The 14-day Relative Strength Index (RSI) rises sharply to near 70.00, suggesting a strong bullish momentum.

The cross would witness a fresh upside move to near the August 26 high of 0.8475 and the psychological resistance of 0.8500 after breaking above the October high of 0.8448.

Alternatively, a downside move below the January 14 low of 0.8384 would falter the upside move and drag the asset towards the October 24 high of 0.8350, followed by the December 27 high of 0.8329.

EUR/GBP daily chart

-

14:30

United States Producer Price Index ex Food & Energy (MoM) registered at 0%, below expectations (0.3%) in December

-

14:30

United States Producer Price Index (MoM) below forecasts (0.3%) in December: Actual (0.2%)

-

14:30

United States Producer Price Index (YoY) registered at 3.3%, below expectations (3.4%) in December

-

14:30

United States Producer Price Index ex Food & Energy (YoY) came in at 3.5%, below expectations (3.8%) in December

-

13:06

US Dollar softens after Trump administration tries to circumvent inflationary shock

- The US Dollar retraces after sources disclosed the Trump administration is considering a gradual tariff implementation.

- In early Tuesday trading, a knee-jerk reaction briefly pushed inflation and Fed policy concerns to the background.

- The US Dollar Index (DXY) dips below 110.00 and looks for support to bounce back.

The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, edges lower and dips below 110.00 on Tuesday, extending the previous day’s retracement from an over-two-year high of 110.18. The main driver comes after sources in the upcoming President-elect Donald Trump administration disclosed that they are considering a very slow month-to-month implementation of tariffs to avoid an inflationary shock, Bloomberg reported. A second driver comes from headlines of a ceasefire deal brokered by the US between Hamas and Israel, which is supported by both the current US President Joe Biden and President-elect Donald Trump.

The US economic calendar picks up in importance on Tuesday, with the Producer Price Index (PPI) release as an appetizer for the more important Consumer Price Index (CPI) on Wednesday. Overall expectations are that the monthly gauges should soften or stay relatively stable while the year-on-year benchmarks will head higher compared to previous readings.

Daily digest market movers: Starting to thicken

- At 13:30 GMT, the Producer Price Index (PPI) for December is released:

- The monthly core PPI gauge is expected to increase 0.3% compared to 0.2% in November.

- The monthly headline PPI is expected to increase by 0.3%, coming from 0.4% in the previous month.

- The yearly headline PPI is expected to increase 3.4% from 3.0% in November, while the annual core PPI is expected to increase 3.8% from 3.4% in the previous month.

- At 15:00 GMT, Federal Reserve Bank of Kansas City President Jeff Schmid delivers a speech about the US economic and monetary policy outlook at an event organized by The Central Exchange.

- At 20:05 GMT, Federal Reserve Bank of New York President John Williams delivers open remarks at the "An Economy That Works for All: Housing Affordability" event organized by the New York Fed in New York.

- Chinese equities are rallying higher on the back of the rumors of gradual tariff implementation. European equities and US futures are taking over the positive sentiment, with all major indices in the green on the day.

- The CME FedWatch Tool projects a 97.3% chance that interest rates will be kept unchanged at current levels in the January meeting. Expectations are for the Federal Reserve (Fed) to remain data-dependent with uncertainties that could influence the inflation path once President-elect Donald Trump takes office on January 20.

- US yields are softening substantially. The 10-year benchmark trades around 4.753% at the time of writing on Tuesday, fading from its fresh 14-month high of 4.802% seen on Monday.

US Dollar Index Technical Analysis: This will be the new normal

The US Dollar Index (DXY) is set to see volatility pick up. The constant deliverance of statements from President-elect Donald Trump, followed by comments from sources inside his team, will deliver several knee-jerk moments and reactions. This means that sense of direction could get distorted and misty from now on.

On the upside, the 110.00 psychological level remains the key resistance to beat. Further up, the next big upside level to hit before advancing any further remains at 110.79. Once beyond there, it is quite a stretch to 113.91, the double top from October 2022.

Looking down, the DXY will look for a bounce off the green ascending trend line from December 2023, which currently comes in around 109.00 as nearby support. In case of more downside, the next support is 107.35. The next level that might halt any selling pressure is 106.52, with the 55-day Simple Moving Average (SMA) at 106.92 reinforcing ahead of this region of support.

US Dollar Index: Daily Chart

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

-

12:07

Germany 5-y Note Auction up to 2.42% from previous 2.04%

-

12:06

USD/CHF Price Forecast: Needs to break above 0.9250 for fresh upside

- USD/CHF recovers intraday losses as the outlook of the US Dollar remains firm.

- Investors await the US inflation data as it will influence the Fed’s interest rate outlook.

- The SNB is expected to cut interest rates further to fuel inflationary pressures.

The USD/CHF pair recovers its intraday losses and flattens to near 0.9160 in Tuesday’s European session. The Swiss Franc pair bounces back as investors turn cautious ahead of the United States (US) Consumer Price Index (CPI) data for December, which will be released on December.

Investors will pay close attention to US inflation data, which will influence market speculation about the Federal Reserve’s (Fed) interest rate outlook. Year-on-year headline inflation is expected to have accelerated to 2.8% from 2.7% in November, with core readings growing steadily by 3.3%.

According to the CME FedWatch tool, traders roughly price in a 69% chance that the central bank will reduce interest rates once this year.

Meanwhile, the Swiss Franc (CHF) has been underperforming against the US dollar for the past few months. The Swiss National Bank (SNB) is expected to continue reducing interest rates further to boost inflationary pressures. The SNB has already reduced its key borrowing rates to 0.5%.

USD/CHF trades close to its 15-month high around 0.9200. The outlook of the Swiss Franc pair remains firm as the 20-week Exponential Moving Average (EMA) near 0.8883 is sloping higher.

The 14-week Relative Strength Index (RSI) oscillates in the bullish range of 60.00-80.00, suggesting a strong upside momentum.

For a fresh upside toward the round-level resistance of 0.9300 and the 16 March 2023 high of 0.9342, the asset needs to break decisively above the October 2023 high of 0.9244.

On the flip side, a downside move below the psychological support of 0.9000 would drag the asset towards the November 22 high of 0.8958, followed by the December 16 low of 0.8900.

USD/CHF weekly chart

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

-

12:00

United States NFIB Business Optimism Index above forecasts (100.8) in December: Actual (105.1)

-

11:21

USD/JPY rises sharply to near 158.00 Yen’s safe-haven appeal falters

- USD/JPY gains to near 158.00 as the safe-haven demand of the Japanese Yen has eased.

- Investors await the US inflation data for fresh guidance on interest rates.

- Fed dovish bets have lately trimmed on upbeat US labor market data for December.

The USD/JPY pair moves sharply higher to near 158.00 in Tuesday’s European session. The asset gains firmly as the safe-haven appeal of the Japanese Yen (JPY) has faltered amid recovery in demand for risk-sensitive assets.

The Yen performed strongly in last three trading days against the US Dollar (USD) despite the latter rallied to a fresh more-than-two-year high. However, the Yen appears to be losing heat, with investors focusing on the United States (US) Consumer Price Index (CPI) data for December, which will be published on Wednesday.

Analysts at Bank of America (BofA) expect, "If US CPI surprises to the upside this week, upward pressure for USDJPY spot is likely to resume, due to the pair's high sensitivity to CPI surprises."

According to market expectations, annual headline inflation is estimated to have grown by 2.8%, faster than 2.7% in November. In the same period, the core CPI – which excludes volatile food and energy prices – rose steadily by 3.3%.

Signs of price pressures remaining stubborn would further weigh on Federal Reserve (Fed) dovish bets. Lately, Fed dovish prospects trimmed significantly after the release of the surprisingly stronger US Nonfarm Payrolls (NFP) data for December.

On the domestic front, the Japanese Yen will be influenced by the market speculation for the Bank of Japan’s (BoJ) likely interest rate action in the policy meeting on January 24. BoJ Deputy Governor Ryozo Himino said on Tuesday that the board will discuss whether to “raise interest rates next week and reach a decision”, based on the economic and price projections laid out in our quarterly outlook report."

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The BoJ ultra-loose monetary policy between 2013 and 2024 caused the Yen to depreciate against its main currency peers due to an increasing policy divergence between the Bank of Japan and other main central banks. More recently, the gradually unwinding of this ultra-loose policy has given some support to the Yen.

Over the last decade, the BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supported a widening of the differential between the 10-year US and Japanese bonds, which favored the US Dollar against the Japanese Yen. The BoJ decision in 2024 to gradually abandon the ultra-loose policy, coupled with interest-rate cuts in other major central banks, is narrowing this differential.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

-

11:14

Spain 9-Month Letras Auction: 2.485% vs 2.366%

-

11:14

Spain 3-Month Letras Auction declined to 2.493% from previous 2.567%

-

11:08

EUR/USD rebounds as US Dollar ticks lower ahead of US inflation data

- EUR/USD recovers to near 1.0270 as the US Dollar performs subduedly as investors focus on the US PPI data for December.

- President-elect Donald Trump’s policies are expected to boost US inflation and growth.

- ECB’s Rehn sees monetary policy restrictions concluding by mid-summer.

EUR/USD extends its recovery from Monday’s over-two-year low of 1.0175 and trades near 1.0270 in Tuesday’s European session. The major currency pair rebounds as the US Dollar (USD) witnesses a marginal correction, with the US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, trading subduedly around 109.50.

However, the strong near-term trend in the US Dollar remains intact. According to the CME FedWatch tool, the 30-Day Fed Funds futures prices signal higher probabilities for only one interest rate cut from the Federal Reserve (Fed) this year, compared to two rate cuts shown by the dot plot at the latest Fed Summary of Economic Projections (SEP).

Traders have trimmed Fed dovish bets on the back of robust labor demand, as shown by the latest United States (US) Nonfarm Payrolls (NFP) data released on Friday, which signifies a strong economic outlook. Also, market participants expect inflationary pressures to remain stubborn under President-elect Donald Trump’s administration as incoming policies, such as immigration controls, tariff hikes, and lower taxes, will boost aggregate demand and growth.

For fresh cues on the current status of inflation, investors will focus on the US Consumer Price Index (CPI) data for December, which will be released on Wednesday.

In Tuesday’s session, investors will focus on the US Producer Price Index (PPI) data for December, which will be published at 13:30 GMT. Annual headline PPI is estimated to have accelerated to 3.4% from 3% in November. In the same period, the core PPI – which excludes volatile food and energy items – is expected to have grown by 3.7%, faster than the previous release of 3.4%.

Daily digest market movers: EUR/USD gains at US Dollar’s expense

- EUR/USD rebounds at the expense of the US Dollar. The outlook of the Euro (EUR) remains weak as European Central Bank (ECB) officials continue to support market expectations of further policy-easing, which have stemmed from a weak Eurozone economic outlook amid fears that US President-elect Donald Trump could slap hefty tariff hikes on the old continent, a scenario that could weaken the export sector.

- ECB policymaker and Bank of Finland Governor Olli Rehn said in a conference on Monday that he expects the monetary policy to leave the restrictive territory in the coming months, at the latest by “midsummer”. However, Rehn’s comments indicated he is not worried about the Trump trade. Rehn argued that firms would find ways to “circumvent” them and even a recent decline in direct trade between China and the US was masking such a trend, Reuters reported.

- Market participants expect the ECB to cut interest rates in each of their next four policy meetings, suggesting that the Deposit Facility rate will come down to 2%. Analysts at Barclays expect the Eurozone to start 2025 on a weak note, notably due to a “significant sluggishness“ in Germany’s manufacturing sector.

Technical Analysis: EUR/USD rebounds from a two-year low of 1.0175

EUR/USD bounces to near 1.0270 in Tuesday’s European session after refreshing its more-than-two-year low around 1.0175 on Monday. However, the outlook for the major currency pair is broadly bearish as the 20-week Exponential Moving Average (EMA) at 1.0585 is declining.

The 14-week Relative Strength Index (RSI) slides below 30.00, indicating a strong downside momentum.

Looking down, the pair could find support near the October 2022 high near 1.0100. Conversely, the January 6 high of 1.0437 will be the key barrier for the Euro bulls.

Euro FAQs

The Euro is the currency for the 19 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day. EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy. The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control. Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency. A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall. Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

-

11:01

Gold slightly recovers after gradual tariff plans leaked

- Gold price halts Monday’s decline and ties up again with gains on Tuesday.

- Sources in the Trump administration disclosed that a gradual tariff introduction is being considered to avoid an inflation shock.

- Gold is testing the upside barrier in a broader-term pennant formation.

Gold’s price (XAU/USD) halts its poor Monday performance when Federal Reserve (Fed) policy rate concerns took over sentiment, recovering slightly and trading near $2,670 at the time of writing on Tuesday. That sentiment is now changing again into a sigh of relief on headlines that the President-elect Donald Trump administration is considering a very gradual implementation of its tariff plans. Sources close to the matter disclosed that the Trump administration is very much concerned about an inflation shock and wants to avoid it at all costs.

On the economic data front, some cautionary warnings need to be issued. In the runup to the US Consumer Price Index (CPI) on Wednesday, the Producer Price Index (PPI) will be released this Tuesday. Traders will need to watch out for some knee-jerk reactions in yields, as a surprise upside beat in PPI numbers could spill over into expectations for a hot CPI release.

A hot PPI and CPI print would cause US yields to surge again and offset the reaction seen this Tuesday on the gradual tariff implementation news. For the Fed policy rate projections, this would mean the chances of any rate cut in 2025 would diminish further and might even head to nil.

Daily digest market movers: Trump administration is worried

- Sources at President-elect Donald Trump’s administration are discussing slowly ramping up tariffs in a gradual approach trying to avoid a spike in inflation, according to people familiar with the matter, Bloomberg reports.

- The US 10-year benchmark rate falls to 4.753% at the time of writing on Tuesday, fading from its fresh 14-month high of 4.802% seen on Monday.

- The CME (Chicago Mercantile Exchange) Fedwatch tool currently shows that the Federal Reserve will keep rate expectations steady until its meeting on June 18, when odds of keeping rates unchanged at current levels stand at 47.2%, compared to 52.8% for lower rates.

- The Commodity Futures Trading Commission (CFTC) released the Gold NC Net Positions on Monday. The current position came in positive at $254,900, compared to the previous at $247,300. This means a surge in long-positioning from speculative traders. The report provides information on the size and direction of the positions taken across all maturities, participants primarily based in Chicago and New York futures markets. Forex traders focus on "non-commercial" or speculative positions to determine whether a trend remains healthy or not, as well as market sentiment towards a certain asset.

Technical Analysis: Risk of slipping away

Gold has slipped back into the broader pennant chart formation in which it has been trading since November. The risk now is that the upside pennant border becomes a resistance again. A firm rejection from here could set off another downward move, towards $2,650 and lower.

On the downside, the 55-day Simple Moving Average (SMA) at $2,650 is the first support. Further down, the 100-day SMA at $2,635 is the next in line. Ultimately, the ascending trend line at the lower boundary of the pennant should contain the price action from falling, standing at $2,615 for now.

On the upside, the October 23 low at $2,708 is the next pivotal level to look out for. Once that level is cleared, though still quite far off, the all-time high of $2,790 is the key upside level.

XAU/USD: Daily Chart

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

-

10:30

Silver price today: Silver rises, according to FXStreet data

Silver prices (XAG/USD) rose on Tuesday, according to FXStreet data. Silver trades at $29.74 per troy ounce, up 0.45% from the $29.61 it cost on Monday.

Silver prices have increased by 2.92% since the beginning of the year.

Unit measure Silver Price Today in USD Troy Ounce 29.74 1 Gram 0.96

The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, stood at 89.80 on Tuesday, down from 89.93 on Monday.

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.

Silver is widely used in industry, particularly in sectors such as electronics or solar energy, as it has one of the highest electric conductivity of all metals – more than Copper and Gold. A surge in demand can increase prices, while a decline tends to lower them. Dynamics in the US, Chinese and Indian economies can also contribute to price swings: for the US and particularly China, their big industrial sectors use Silver in various processes; in India, consumers’ demand for the precious metal for jewellery also plays a key role in setting prices.

Silver prices tend to follow Gold's moves. When Gold prices rise, Silver typically follows suit, as their status as safe-haven assets is similar. The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, may help to determine the relative valuation between both metals. Some investors may consider a high ratio as an indicator that Silver is undervalued, or Gold is overvalued. On the contrary, a low ratio might suggest that Gold is undervalued relative to Silver.

(An automation tool was used in creating this post.)

-

10:04

Silver Price Forecast: XAG/USD tests 14-day EMA near $30.00

- Silver price tests immediate resistance at the 14-day EMA of $29.83 level.

- The 14-day RSI consolidates around the 50 level, indicating a neutral market outlook.

- The pair may test initial support at the four-month low of $28.74, recorded on December 19.

Silver price (XAG/USD) recovers some of their recent losses from the previous session, trading near $29.80 per troy ounce during European trading hours on Tuesday. Analyzing the daily chart suggests that short-term price momentum appears neutral, with the XAG/USD pair positioned around the nine-day and 14-day Exponential Moving Averages (EMAs). A breakout in either direction could signal a clearer trend.

Moreover, the 14-day Relative Strength Index (RSI) hovers near the 50 level, suggesting a neutral outlook. This suggests the market is evenly balanced, with no clear indication of overbought or oversold conditions, reflecting equilibrium between bullish and bearish momentum.

Silver price currently tests resistance at the immediate 14-day EMA of $29.83, followed closely by the nine-day EMA at $29.84. A breakout above these levels could boost market sentiment and drive the XAG/USD pair toward the key psychological level of $30.00. A sustained move beyond this threshold may strengthen bullish momentum, potentially setting the stage for the grey metal to target its two-month high of $32.28, last achieved on December 9.

On the downside, initial support is located at the four-month low of $28.74, recorded on December 19, followed by the critical psychological level of $28.00. A break below these levels could intensify bearish momentum and signal further downside potential for Silver price.

XAG/USD: Daily Chart

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.