Noticias del mercado

-

22:45

New Zealand: GDP y/y, Quarter III 2.3% (forecast 2.3%)

-

22:45

New Zealand: GDP q/q, Quarter III 0.9% (forecast 0.8%)

-

21:00

Dow +0.93% 17,688.26 +163.35 Nasdaq +1.15% 5,052.56 +57.20 S&P +4.86% 2,067.20 +95.80

-

20:00

U.S.: Fed Interest Rate Decision , 0.5% (forecast 0.5%)

-

18:52

WSE: Session Results

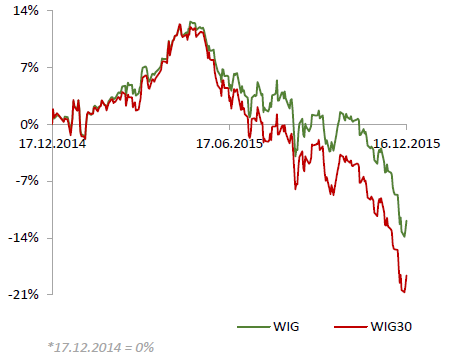

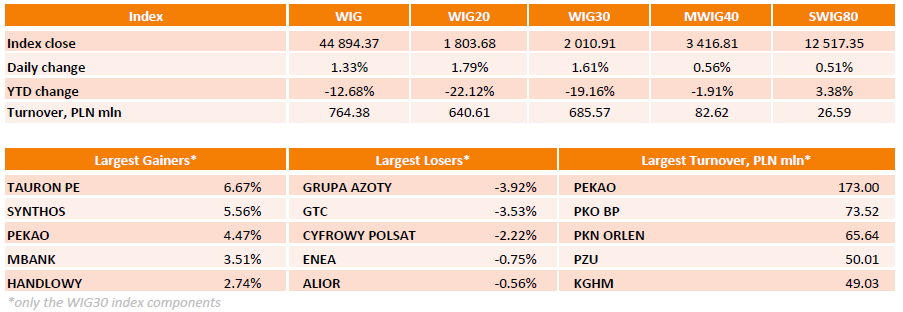

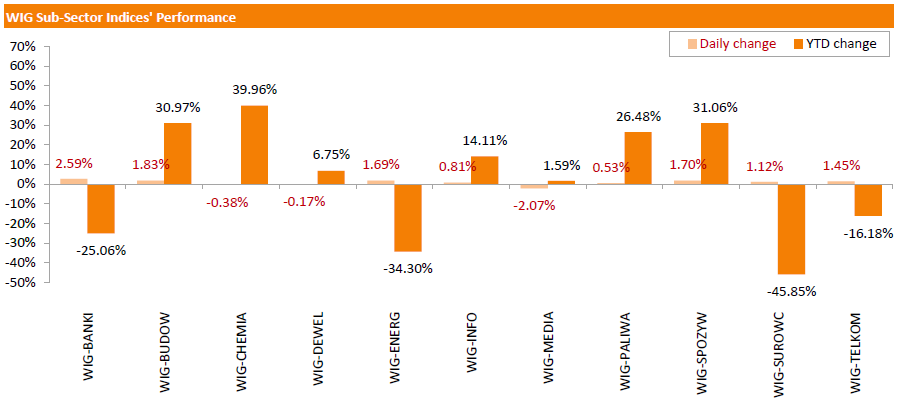

Polish equities advanced on Wednesday. The broad market measure, the WIG Index, added 1.33%. Sector-wise, media sector (-2.07%) was the day's biggest laggard, while banking sector (+2.59%) benefited the most.

The large-cap stocks' measure, the WIG30 Index, advanced by 1.61%. In the index basket, utilities name TAURON PE (WSE: TPE) and chemicals name SYNTHOS (WSE: SNS) were the strongest performers, jumping by 6.67% and 5.56%. Other major outperformers were stocks from banking sector, namely stocks PEKAO (WSE: PEO), MBANK (WSE: MBK) and HANDLOWY (WSE: BHW), which added 4.47%, 3.51% and 2.74% respectively. On the other side of the ledger, chemicals name GRUPA AZOTY (WSE: ATT) and developing sector name GTC (WSE: GTC) fared the worst, retreating 3.92% and 3.53% respectively. They were followed by media name CYFROWY POLSAT (WSE: CPS), which fell by 2.22%, following report that Poland might impose a fee on private TV and radio broadcasters to finance public media.

-

18:10

Wall Street. Major U.S. stock-indexes sligtly rose

Major U.S. stock-indexes slightly rose for the third straight day on Wednesday as investors prepare for a widely anticipated interest rate hike by the Federal Reserve later in the day. An increase in the Fed's benchmark rate from near zero would be the first since June 29, 2006. After more than a year of posturing and a couple of false starts, the U.S. central bank is seen raising rates by a token 25 basis points.

Most of Dow stocks in positive area (22 of 30). Top looser - E. I. du Pont de Nemours and Company (DD, -3.96%). Top gainer - Verizon Communications Inc. (VZ, +1.32%).

Almost all S&P index sectors also in positive area. Top looser - Basic Materials (-0.6%). Top gainer - Utilities (+1,5%).

At the moment:

Dow 17474.00 +4.00 +0.02%

S&P 500 2041.00 +4.00 +0.20%

Nasdaq 100 4599.25 -1.75 -0.04%

Oil 35.80 -1.55 -4.15%

Gold 1075.30 +13.70 +1.29%

U.S. 10yr 2.30 +0.03

-

18:00

European stocks close: stocks closed higher as market participants are awaiting the release of the Fed's monetary policy meeting results later in the day

Stock indices closed higher as market participants are awaiting the release of the Fed's monetary policy meeting results later in the day. Analysts expect the Fed to raise its interest rate by 25 basis points to 0.50% or to the range 0.25% - 0.50% from 0.00% - 0.25%.

Meanwhile, the economic data from Eurozone was mixed. Eurostat released its final consumer price inflation data for the Eurozone on Wednesday. Eurozone's harmonized consumer price index fell 0.1% in November, beating expectations for a 0.2% drop, after a 0.1% increase in October.

On a yearly basis, Eurozone's final consumer price inflation increased to 0.2% in November from 0.1% in October, exceeding the preliminary reading of a 0.1% rise.

Eurozone's final consumer price inflation excluding food, energy, alcohol and tobacco fell to an annual rate of 0.9% in November from 1.1% in October, in line with the preliminary reading.

Eurozone's unadjusted trade surplus rose to €24.1 billion in October from €20.5 billion in September, exceeding expectations for a rise €21.5 billion.

Exports rose at an annual rate of 1.0% in October, while imports were flat.

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for the Eurozone on Wednesday. Eurozone's preliminary manufacturing PMI rose to 53.1 in December from 52.8 in November. Analysts had expected the index to remain unchanged at 52.8.

Eurozone's preliminary services PMI fell to 53.9 in December from 54.2 in November, missing expectations for a fall to 54.1.

Growth of new business supported both indexes.

"The Eurozone economy enjoyed a comfortably solid end to 2015, though policymakers are likely to remain disappointed by the relatively modest pace of expansion and lack of inflationary pressures, given the stage of the recovery and the amount of stimulus already in place", Markit's Chief Economist Chris Williamson said.

He noted that data was signalling the Eurozone's economy could expand 0.4% in the fourth quarter, meaning that the economy grew 1.5% in 2015.

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate fell to 5.2% in the August to October quarter from 5.3% in the July to September quarter. It was the lowest reading since three months to January 2006.

Analysts had expected the unemployment rate to remain unchanged at 5.3%.

The claimant count rose by 3,900 people in November, beating expectations for a rise by 1,500, after an increase of 200 people in October. October's figure was revised down from a 3,300 increase.

U.K. unemployment in the July to September period dropped by 110,000 to 1.71 million from the previous quarter.

Average weekly earnings, excluding bonuses, climbed by 2.0% in the August to October quarter, missing expectations for a 2.0% rise, after a 2.4% gain in the July to September quarter. The previous quarter's figure was revised down from a 2.5% increase.

Average weekly earnings, including bonuses, rose by 2.4% in the August to October quarter, missing expectations for a gain of 2.5%, after a 3.0% increase in the July to September quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,061.19 +43.40 +0.72 %

DAX 10,469.26 +18.88 +0.18 %

CAC 40 4,624.67 +10.27 +0.22 %

-

18:00

European stocks closed: FTSE 100 6,061.19 +43.40 +0.72% CAC 40 4,624.67 +10.27 +0.22% DAX 10,469.26 +18.88 +0.18%

-

17:47

Oil prices decline more than 2%

Oil prices fell on the U.S. crude oil inventories data. The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories increased by 4.80 million barrels to 490.7 million in the week to December 11.

Analysts had expected U.S. crude oil inventories to decline by 1.4 million barrels.

Gasoline inventories increased by 1.7 million barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, climbed by 607,000 barrels.

U.S. crude oil imports increased by 291,000 barrels per day.

Refineries in the U.S. were running at 91.9% of capacity, down from 93.1% the previous week.

Market participants are awaiting the release of the Fed's monetary policy meeting results later in the day. Analysts expect the Fed to raise its interest rate.

News that congressional leaders in the U.S. reached a deal which would lift the ban on U.S. crude oil exports supported oil prices.

WTI crude oil for January delivery declined to $35.78 a barrel on the New York Mercantile Exchange.

Brent crude oil for January decreased to $37.46 a barrel on ICE Futures Europe.

-

17:25

Gold climbs ahead the release of the Fed's monetary policy meeting results

Gold price showed a correction ahead the release of the Fed's monetary policy meeting results. Analysts expect the Fed to raise its interest rate by 25 basis points to 0.50% or to the range 0.25% - 0.50% from 0.00% - 0.25%.

Market participants will closely monitor the Fed's statement and a speech by the Fed Chairwoman Janet Yellen for hints for the pace of further interest rate hikes. Yellen and Fed officials said several times that it will raise its interest rate gradually.

Gold is traded in U.S. dollars. It suffers when the U.S. dollar strengthens, becoming more expensive for holders of other currencies.

January futures for gold on the COMEX today traded at 1074.70 dollars per ounce.

-

17:06

The People's Bank of China’s working paper: the Chinese economy is expected to expand 6.9% this year and 6.8% next year

The People's Bank of China (PBoC) said in a working paper on Wednesday that it expects the Chinese economy to expand 6.9% this year and 6.8% next year.

The central bank noted that industrial overcapacity, weak demand for Chinese goods and rising non-performing loans from banks weigh on the Chinese economy.

Inflation is expected to be 1.5% year-on-year in 2015, exports are expected to drop 2.9% this year from a year earlier, while imports are expected to slide 14.8%.

According to the working paper, the governments' stimulus measures should take effect from the fourth quarter of 2015 to the first half of 2016.

-

16:55

The Greek parliament approves a bill to receive bailout funds

The Greek parliament on Tuesday approved a bill to receive next €1 billion of bailout funds. All 153 lawmakers of the government coalition voted in favour of the bill.

-

16:48

U.S. crude inventories climb by 4.80 million barrels to 490.7 million in the week to December 11

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories increased by 4.80 million barrels to 490.7 million in the week to December 11.

Analysts had expected U.S. crude oil inventories to decline by 1.4 million barrels.

Gasoline inventories increased by 1.7 million barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, climbed by 607,000 barrels.

U.S. crude oil imports increased by 291,000 barrels per day.

Refineries in the U.S. were running at 91.9% of capacity, down from 93.1% the previous week.

-

16:32

U.K. household finance index rises to 45.0 in December

Markit Economics and financial information provider Ipsos Mori released its household finance index (HFI) for the U.K. on Wednesday. The household finance index increased to 45.0 in December from 44.1 in November.

The increase was partly driven by a rise in workplace activity and income from employment.

The index measuring the outlook for financial well-being over the coming twelve months decreased to 49.4 in December from 50.4 in November.

The current inflation perceptions index declined to 61.7 in December.

The index measuring expected living costs over the twelve months was down to 78.4 in December from 80.0 in November.

61% of respondents expects the Bank of England's monetary policy to tighten in 2015.

"Markit's HFI survey painted a mixed picture in December. On the one hand, the strain on current finances eased to one of the weakest in the series history, helped by relatively low inflation perceptions and further improvements in the labour market. In particular, growth of workplace activity quickened, while worries about job security abated," economist at Markit, Philip Leake, said.

-

16:30

U.S.: Crude Oil Inventories, December 4.801 (forecast -1.4)

-

15:52

U.S. preliminary manufacturing purchasing managers' index drops to 51.3 in December, the lowest level since October 2012

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for the U.S. on Wednesday. The U.S. preliminary manufacturing purchasing managers' index (PMI) dropped to 51.3 in December from 52.8 in November, missing expectations for a decline to 52.6. It was the lowest level since October 2012.

A reading above 50 indicates expansion in economic activity.

The decline was partly driven by a slower pace of expansion in new orders and production volumes. New orders grew at weakest pace weakest since September 2009, while production volumes rose at softest pace since October 2013.

"Just as the Fed looks set to hike interest rates for the first time since 2006, the manufacturing sector shows signs of stalling. The flash PMI results show factories ending the year with the weakest inflow of new orders since the global financial crisis," Markit Chief Economist Chris Williamson.

"Low oil prices are hurting the energy sector, feeding through to reduced investment demand for plant and machinery, while the stronger dollar is hitting exports and encouraging import substitution. These are major headwinds that show no sign of easing any time soon," he added.

-

15:45

U.S.: Manufacturing PMI, December 51.3 (forecast 52.6)

-

15:36

U.S. Stocks open: Dow +0.90%, Nasdaq +0.82%, S&P +0.78%

-

15:32

U.S. industrial production declines 0.6% in November, the fastest drop since March 2012

The Federal Reserve released its industrial production report on Wednesday. The U.S. industrial production fell 0.6% in November, missing expectations for a 0.1% decrease, after a 0.4% decline in October. It was the fastest drop since March 2012.

October's figure was revised down from a 0.2% fall.

The drop was mainly driven by a fall in the mining output and utilities. Mining output plunged by 1.1% in November, while utilities production slid 4.3%.

Manufacturing output was flat in November, after a 0.3% rise in October. October's figure was revised down from a 0.4% increase.

Capacity utilisation rate decreased to 77.0% in November from 77.5% in October, missing expectations for a decline to 77.4%.

-

15:28

Before the bell: S&P futures +0.58%, NASDAQ futures +0.55%

U.S. stock-index futures rose.

Global Stocks:

Nikkei 19,049.91 +484.01 +2.61%

Hang Seng 21,701.21 +426.84 +2.01%

Shanghai Composite 3,517.05 +6.70 +0.19%

FTSE 6,083.86 +66.07 +1.10%

CAC 4,652.67 +38.27 +0.83%

DAX 10,554.64 +104.26 +1.00%

Crude oil $37.19 (-0.43%)

Gold $1070.30 (+0.82%)

-

15:15

U.S.: Industrial Production (MoM), November -0.6% (forecast -0.1%)

-

15:15

U.S.: Capacity Utilization, November 77% (forecast 77.4%)

-

15:15

U.S.: Industrial Production YoY , November -1.2%

-

15:05

Australia’s leading index declines 0.2% in November

Westpac Bank and the Melbourne Institute released its leading index for Australia on late Tuesday. The index declined 0.2% in November, after a 0.1% in October.

"This result is a little disappointing. In the two previous months we had seen some modest improvement in the growth rate raising hopes that growth in the Leading Index might exceed trend by year's end," Westpac Bank said in its statement.

Westpac expects the Australian economy to expand 2.8% in 2015-16 and 2.7% in 2016-17.

-

14:58

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.74

3.37%

26.3K

Walt Disney Co

DIS

115.25

2.75%

18.0K

HONEYWELL INTERNATIONAL INC.

HON

101.00

2.57%

0.7K

Merck & Co Inc

MRK

53.82

1.74%

15.8K

Barrick Gold Corporation, NYSE

ABX

7.21

1.55%

4.4K

JPMorgan Chase and Co

JPM

66.89

1.20%

14.8K

Citigroup Inc., NYSE

C

53.14

1.18%

4.0K

Visa

V

79.49

1.11%

8.6K

Goldman Sachs

GS

183.98

1.08%

2.0K

McDonald's Corp

MCD

118.14

1.03%

4.1K

Boeing Co

BA

147.99

1.00%

18.8K

International Business Machines Co...

IBM

139.00

0.88%

0.6K

ALCOA INC.

AA

9.20

0.88%

6.4K

Chevron Corp

CVX

93.54

0.84%

0.6K

Amazon.com Inc., NASDAQ

AMZN

664.00

0.81%

19.1K

Hewlett-Packard Co.

HPQ

12.30

0.74%

2.4K

General Motors Company, NYSE

GM

34.42

0.70%

0.1K

Verizon Communications Inc

VZ

45.86

0.68%

20.5K

Microsoft Corp

MSFT

55.56

0.65%

11.5K

Tesla Motors, Inc., NASDAQ

TSLA

222.50

0.64%

0.9K

Nike

NKE

129.41

0.62%

0.1K

Google Inc.

GOOG

747.95

0.61%

1.1K

Pfizer Inc

PFE

32.45

0.59%

1.7K

United Technologies Corp

UTX

93.80

0.58%

3.7K

Ford Motor Co.

F

13.95

0.58%

18.1K

Facebook, Inc.

FB

105.15

0.57%

67.5K

Cisco Systems Inc

CSCO

27.00

0.56%

1.0K

Starbucks Corporation, NASDAQ

SBUX

60.31

0.55%

0.3K

Twitter, Inc., NYSE

TWTR

24.08

0.54%

12.4K

Home Depot Inc

HD

131.99

0.53%

5.9K

The Coca-Cola Co

KO

43.30

0.53%

0.3K

AMERICAN INTERNATIONAL GROUP

AIG

60.25

0.52%

7.7K

3M Co

MMM

148.87

0.50%

403.2K

AT&T Inc

T

33.98

0.50%

4.0K

Johnson & Johnson

JNJ

104.64

0.49%

0.2K

Intel Corp

INTC

35.35

0.48%

3.1K

Exxon Mobil Corp

XOM

79.80

0.47%

22.7K

Apple Inc.

AAPL

111.00

0.46%

182.9K

Procter & Gamble Co

PG

79.99

0.39%

2.2K

ALTRIA GROUP INC.

MO

57.56

0.38%

0.5K

General Electric Co

GE

30.43

0.36%

10.5K

Yahoo! Inc., NASDAQ

YHOO

33.01

-0.06%

0.3K

Wal-Mart Stores Inc

WMT

59.46

-0.30%

13.6K

Caterpillar Inc

CAT

65.95

-1.20%

1.5K

-

14:53

Upgrades and downgrades before the market open

Upgrades:

Chevron (CVX) upgraded to Buy from Hold at Argus; target $100

Downgrades:

Caterpillar (CAT) downgraded to Hold from Buy at Deutsche Bank

Other:

Apple (AAPL) target lowered to $130 from $140 at UBS

3M (MMM) target lowered to $136 from $140 at RBC Capital Mkts

UnitedHealth (UNH) initiated with a Outperform at Credit Suisse

MasterCard (MA) initiated with a Buy at UBS

Visa (V) initiated with a Buy at UBS

-

14:52

Housing starts in the U.S. jump 10.5% in November

The U.S. Commerce Department released the housing market data on Wednesday. Housing starts in the U.S. soared 10.5% to 1.173 million annualized rate in November from a 1,062 million pace in October, exceeding expectations for an increase to 1.135 million.

October's figure was revised up from 1.160 million units.

The increase was driven by rises in starts of single-family and multifamily homes.

Housing market benefits from the strengthening of the labour market. But there is a shortage of houses available for sale.

Building permits in the U.S. climbed 11.0% to 1.289 million annualized rate in November from a 1.161 million pace in October, beating expectations for a 1,150 pace.

Starts of single-family homes increased 7.6% in November. Building permits for single-family homes were up 1.1%.

Starts of multifamily buildings climbed 16.4% in November. Permits for multi-family housing rose 26.9%.

-

14:46

Option expiries for today's 10:00 ET NY cut

USD/JPY:120.00-10 (USD 2bln) 121.00 (720m) 121.30-35 (350m)

EUR/USD:1.0900 (EUR 919m) 1.0945-50 (575m) 1.1000 (622m) 1.1100 (664m) 1.1200 (1.5bln)

EUR/GBP:0.7170 (EUR 350m)

AUD/USD:0.7245 (AUD 273m) 0.7350 (628m)

AUD/NZD:1.0950 (AUD 901m)

-

14:43

Foreign investors add C$22.1 billion of Canadian securities in October

Statistics Canada released foreign investment figures on Wednesday. Foreign investors added C$22.1 billion of Canadian securities in October, after an investment of C$3.35 billion in September.

Canadian investors added C$3.2 billion of foreign securities in October, led by non-US foreign bonds.

-

14:37

Preliminary Markit/Nikkei manufacturing purchasing managers' index for Japan declines to 52.5 in December

The preliminary Markit/Nikkei manufacturing Purchasing Managers' Index (PMI) for Japan declined to 52.5 in December from 52.6 in November.

A reading below 50 indicates contraction of activity.

The index was partly driven by a rise in new orders and backlogs of work.

"Operating conditions at Japanese manufacturers continued to improve at a solid rate in the final month of 2015. Despite easing, the rate of expansion in production was robust overall," economist at Markit, Amy Brownbill, said.

-

14:30

U.S.: Building Permits, November 1289 (forecast 1150)

-

14:30

U.S.: Housing Starts, November 1173 (forecast 1135)

-

14:30

Canada: Foreign Securities Purchases, October 22.08

-

14:23

Foreign exchange market. European session: the British pound traded lower against the U.S. dollar after the release of the U.K. labour market data

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

01:35 Japan Manufacturing PMI (Preliminary) December 52.6 52.5

08:00 France Manufacturing PMI (Preliminary) December 50.6 50.5 51.6

08:00 France Services PMI (Preliminary) December 51 50.8 50

08:30 Germany Manufacturing PMI (Preliminary) December 52.9 53 53

08:30 Germany Services PMI (Preliminary) December 55.6 55.5 55.4

09:00 Eurozone Manufacturing PMI (Preliminary) December 52.8 52.8 53.1

09:00 Eurozone Services PMI (Preliminary) December 54.2 54.1 53.9

09:30 United Kingdom Average earnings ex bonuses, 3 m/y October 2.4% Revised From 2.5% 2.3% 2.0%

09:30 United Kingdom Average Earnings, 3m/y October 3% 2.5% 2.4%

09:30 United Kingdom Claimant count November 0.2 Revised From 3.3 1.5 3.9

09:30 United Kingdom ILO Unemployment Rate October 5.3% 5.3% 5.2%

10:00 Eurozone Trade balance unadjusted October 20.5 21.5 24.1

10:00 Eurozone Harmonized CPI November 0.1% -0.2% -0.1%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Finally) November 1.1% 0.9% 0.9%

10:00 Eurozone Harmonized CPI, Y/Y (Finally) November 0.1% 0.1% 0.2%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) December 0.0 16.6

12:00 U.S. MBA Mortgage Applications December 1.2% -1.1%

The U.S. dollar traded mixed to higher against the most major currencies ahead of the release of the U.S. economic data. Housing starts in the U.S. are expected to rise to 1.135 million units in November from 1.060 million units in October.

The number of building permits is expected to decrease to 1.150 million units in November from 1.161 million units in October.

The U.S. industrial production is expected to fall 0.1% in November, after a 0.2% decline in October.

The U.S. preliminary manufacturing PMI is expected to decline to 52.6 in December from 52.8 in November.

The Fed will release its latest monetary policy decision at 19:00 GMT.

The euro traded lower against the U.S. dollar after the release of the mixed economic data from the Eurozone. Eurostat released its final consumer price inflation data for the Eurozone on Wednesday. Eurozone's harmonized consumer price index fell 0.1% in November, beating expectations for a 0.2% drop, after a 0.1% increase in October.

On a yearly basis, Eurozone's final consumer price inflation increased to 0.2% in November from 0.1% in October, exceeding the preliminary reading of a 0.1% rise.

Eurozone's final consumer price inflation excluding food, energy, alcohol and tobacco fell to an annual rate of 0.9% in November from 1.1% in October, in line with the preliminary reading.

Eurozone's unadjusted trade surplus rose to €24.1 billion in October from €20.5 billion in September, exceeding expectations for a rise €21.5 billion.

Exports rose at an annual rate of 1.0% in October, while imports were flat.

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for the Eurozone on Wednesday. Eurozone's preliminary manufacturing PMI rose to 53.1 in December from 52.8 in November. Analysts had expected the index to remain unchanged at 52.8.

Eurozone's preliminary services PMI fell to 53.9 in December from 54.2 in November, missing expectations for a fall to 54.1.

Growth of new business supported both indexes.

"The Eurozone economy enjoyed a comfortably solid end to 2015, though policymakers are likely to remain disappointed by the relatively modest pace of expansion and lack of inflationary pressures, given the stage of the recovery and the amount of stimulus already in place", Markit's Chief Economist Chris Williamson said.

He noted that data was signalling the Eurozone's economy could expand 0.4% in the fourth quarter, meaning that the economy grew 1.5% in 2015.

The British pound traded lower against the U.S. dollar after the release of the U.K. labour market data. The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate fell to 5.2% in the August to October quarter from 5.3% in the July to September quarter. It was the lowest reading since three months to January 2006.

Analysts had expected the unemployment rate to remain unchanged at 5.3%.

The claimant count rose by 3,900 people in November, beating expectations for a rise by 1,500, after an increase of 200 people in October. October's figure was revised down from a 3,300 increase.

U.K. unemployment in the July to September period dropped by 110,000 to 1.71 million from the previous quarter.

Average weekly earnings, excluding bonuses, climbed by 2.0% in the August to October quarter, missing expectations for a 2.0% rise, after a 2.4% gain in the July to September quarter. The previous quarter's figure was revised down from a 2.5% increase.

Average weekly earnings, including bonuses, rose by 2.4% in the August to October quarter, missing expectations for a gain of 2.5%, after a 3.0% increase in the July to September quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

The Canadian dollar traded lower against the U.S. dollar ahead of the release of the Canadian economic data.

The Swiss franc traded lower against the U.S. dollar. A survey by the ZEW Institute and Credit Suisse Group showed on Wednesday that Switzerland's economic sentiment index jumped to 16.6 in December from 0.0 in November.

"As in the previous months, the clear majority of survey respondents regard the present state of Switzerland's economy as being "normal". The group of analysts sharing this assessment has increased slightly and now amounts to 86.1 per cent of respondents," the ZEW said.

The current conditions climbed to -2.7 in December from -12.2 points in November.

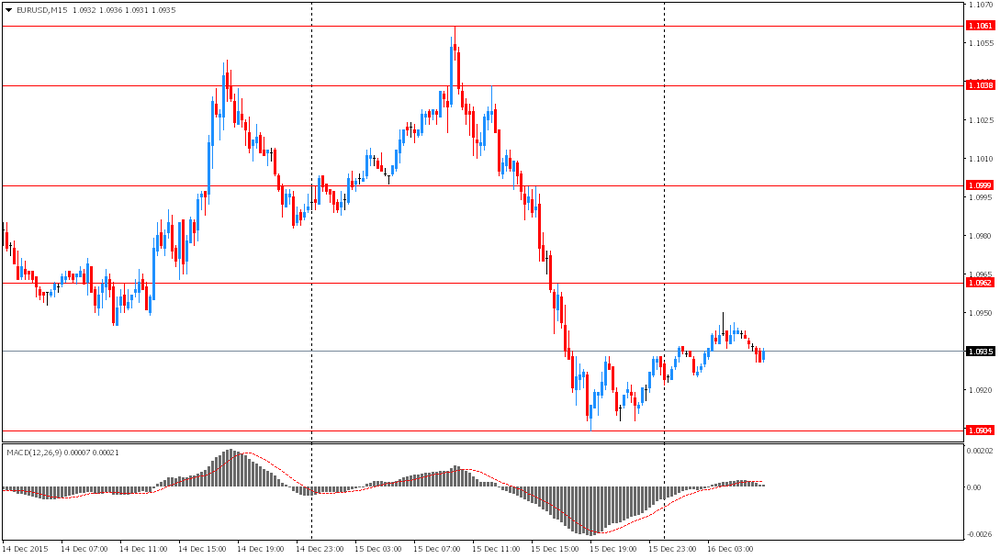

EUR/USD: the currency pair declined to $1.0912

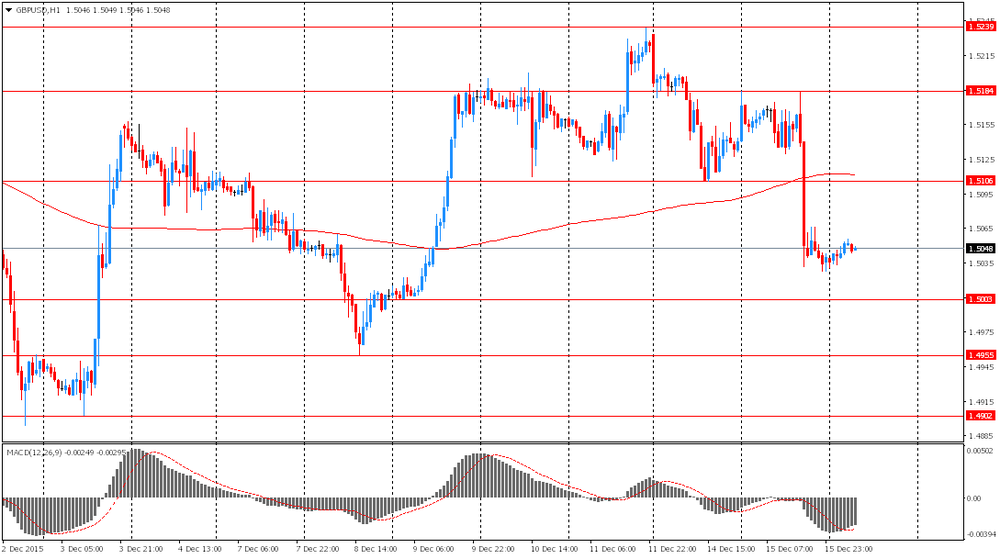

GBP/USD: the currency pair fell to $1.4988

USD/JPY: the currency pair traded mixed

The most important news that are expected (GMT0):

13:30 Canada Foreign Securities Purchases October 3.35

13:30 U.S. Housing Starts November 1060 1135

13:30 U.S. Building Permits November 1161 1150

14:15 U.S. Capacity Utilization November 77.5% 77.4%

14:15 U.S. Industrial Production (MoM) November -0.2% -0.1%

14:15 U.S. Industrial Production YoY November 0.3%

14:45 U.S. Manufacturing PMI (Preliminary) December 52.8 52.6

15:30 U.S. Crude Oil Inventories December -3.568 -1.4

19:00 U.S. Fed Interest Rate Decision 0.25% 0.5%

19:00 U.S. FOMC Economic Projections

19:00 U.S. FOMC Statement

19:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter III 0.4% 0.8%

21:45 New Zealand GDP y/y Quarter III 2.4% 2.3%

23:50 Japan Trade Balance Total, bln November 111.5 -446.2

-

14:00

Orders

EUR/USD

Offers 1.0960 1.0985 1.1000 1.1025-30 1.1050 1.1065 1.1080-85 1.1100 1.1130 1.1150 1.1175 1.1200

Bids 1.0920-25 1.0900 1.0885 1.0865 1.0850 1.0830 1.0800 1.0785 1.0750 1.0730 1.0700

GBP/USD

Offers 1.5175-80 1.5200 1.5225 1.5240-50 1.5270 1.5285 1.5300

Bids 1.5125-30 1.5110 1.5100 1.5080 1.5065 1.5050 1.5030 1.5000

EUR/GBP

Offers 0.7300 0.7320 0.7350 0.7375 0.7400 0.7420 0.7450

Bids 0.7265 0.7250 0.7225-30 0.7200 0.7180 0.7165 0.7150

EUR/JPY

Offers 133.50 133.85 134.00 134.20-25 134.50 13475 135.00

Bids 133.00 132.80132.50 132.00 131.50 131.00 130.80 130.50

USD/JPY

Offers 122.20-25 122.50 122.80 123.00123.20 123.50 123.85 124.00

Bids 121.80 121.50 121.30 121.00 120.85 120.60-65 120.50 120.30 120.00 119.85 119.60 119.50

AUD/USD

Offers 0.7200 0.7220-25 0.7265 0.7285 0.7300 0.7320-25 0.7345-50 0.7375 0.7400

Bids 0.7180 0.7165 0.7150 0.7130 0.7100 0.7085 0.7065 0.7050 0.7020 0.7000

-

13:00

U.S.: MBA Mortgage Applications, December -1.1%

-

12:11

European stock markets mid session: stocks traded higher as market participants are awaiting the release of the Fed's monetary policy meeting results

Stock indices traded higher as market participants are awaiting the release of the Fed's monetary policy meeting results. Analysts expect the Fed to raise its interest rate.

Meanwhile, the economic data from Eurozone was mixed. Eurostat released its final consumer price inflation data for the Eurozone on Wednesday. Eurozone's harmonized consumer price index fell 0.1% in November, beating expectations for a 0.2% drop, after a 0.1% increase in October.

On a yearly basis, Eurozone's final consumer price inflation increased to 0.2% in November from 0.1% in October, exceeding the preliminary reading of a 0.1% rise.

Eurozone's final consumer price inflation excluding food, energy, alcohol and tobacco fell to an annual rate of 0.9% in November from 1.1% in October, in line with the preliminary reading.

Eurozone's unadjusted trade surplus rose to €24.1 billion in October from €20.5 billion in September, exceeding expectations for a rise €21.5 billion.

Exports rose at an annual rate of 1.0% in October, while imports were flat.

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for the Eurozone on Wednesday. Eurozone's preliminary manufacturing PMI rose to 53.1 in December from 52.8 in November. Analysts had expected the index to remain unchanged at 52.8.

Eurozone's preliminary services PMI fell to 53.9 in December from 54.2 in November, missing expectations for a fall to 54.1.

Growth of new business supported both indexes.

"The Eurozone economy enjoyed a comfortably solid end to 2015, though policymakers are likely to remain disappointed by the relatively modest pace of expansion and lack of inflationary pressures, given the stage of the recovery and the amount of stimulus already in place", Markit's Chief Economist Chris Williamson said.

He noted that data was signalling the Eurozone's economy could expand 0.4% in the fourth quarter, meaning that the economy grew 1.5% in 2015.

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate fell to 5.2% in the August to October quarter from 5.3% in the July to September quarter. It was the lowest reading since three months to January 2006.

Analysts had expected the unemployment rate to remain unchanged at 5.3%.

The claimant count rose by 3,900 people in November, beating expectations for a rise by 1,500, after an increase of 200 people in October. October's figure was revised down from a 3,300 increase.

U.K. unemployment in the July to September period dropped by 110,000 to 1.71 million from the previous quarter.

Average weekly earnings, excluding bonuses, climbed by 2.0% in the August to October quarter, missing expectations for a 2.0% rise, after a 2.4% gain in the July to September quarter. The previous quarter's figure was revised down from a 2.5% increase.

Average weekly earnings, including bonuses, rose by 2.4% in the August to October quarter, missing expectations for a gain of 2.5%, after a 3.0% increase in the July to September quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

Current figures:

Name Price Change Change %

FTSE 100 6,066.52 +48.73 +0.81 %

DAX 10,482.96 +32.58 +0.31 %

CAC 40 4,645.28 +30.88 +0.67 %

-

12:07

France's preliminary manufacturing PMI rises in December, while services PMI declines

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for France on Wednesday. France's preliminary manufacturing PMI rose to 51.6 in December from 50.6 in November, beating forecasts of a decline to 50.5.

France's preliminary services PMI decreased to 50.0 in December from 51.0 in November. Analysts had expected the index to fall to 50.8.

"French private sector output growth nearly ground to a halt at the end of 2015 amid faltering new business intakes. A slowdown in the dominant service sector was the driver, with some panellists indicating that their new business intakes had been impacted following the recent terrorist attacks," the Senior Economist at Markit Jack Kennedy said.

-

12:03

Germany's preliminary manufacturing PMI increases in December, while services PMI falls

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for Germany on Wednesday. Germany's preliminary manufacturing PMI climbed to 53.0 in December from 52.9 in November, in line with forecasts.

Germany's preliminary services PMI was down to 55.4 in December from 55.6 in November. Analysts had expected index to decline to 55.5.

"Germany's private sector companies ended the fourth quarter on a solid footing, with all key barometers of corporate health showing further improvements. While output and new orders increased at slightly weaker rates, growth remained above their respective long-term trends," Markit's economist Oliver Kolodseike noted.

-

11:54

Eurozone's preliminary manufacturing PMI rise in December, while services PMI declines

Markit Economics released its preliminary manufacturing purchasing managers' index (PMI) for the Eurozone on Wednesday. Eurozone's preliminary manufacturing PMI rose to 53.1 in December from 52.8 in November. Analysts had expected the index to remain unchanged at 52.8.

Eurozone's preliminary services PMI fell to 53.9 in December from 54.2 in November, missing expectations for a fall to 54.1.

Growth of new business supported both indexes.

"The Eurozone economy enjoyed a comfortably solid end to 2015, though policymakers are likely to remain disappointed by the relatively modest pace of expansion and lack of inflationary pressures, given the stage of the recovery and the amount of stimulus already in place", Markit's Chief Economist Chris Williamson said.

He noted that data was signalling the Eurozone's economy could expand 0.4% in the fourth quarter, meaning that the economy grew 1.5% in 2015.

-

11:46

Eurozone's harmonized consumer price index declines 0.1% in November

Eurostat released its final consumer price inflation data for the Eurozone on Wednesday. Eurozone's harmonized consumer price index fell 0.1% in November, beating expectations for a 0.2% drop, after a 0.1% increase in October.

On a yearly basis, Eurozone's final consumer price inflation increased to 0.2% in November from 0.1% in October, exceeding the preliminary reading of a 0.1% rise.

Restaurants and cafés prices were up 0.10% year-on-year in November, vegetables prices rose by 0.10%, fruit gained 0.08%, fuel prices for transport declined by 0.54%, heating oil prices decreased by 0.21%, while gas prices were down by 0.10%.

Eurozone's final consumer price inflation excluding food, energy, alcohol and tobacco fell to an annual rate of 0.9% in November from 1.1% in October, in line with the preliminary reading.

-

11:38

Eurozone's unadjusted trade surplus rises to €24.1 billion in October

Eurostat released its trade data for the Eurozone on Wednesday. Eurozone's unadjusted trade surplus rose to €24.1 billion in October from €20.5 billion in September, exceeding expectations for a rise €21.5 billion.

Exports rose at an annual rate of 1.0% in October, while imports were flat.

-

11:35

U.K. unemployment rate declines to 5.2% in the August to October quarter

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate fell to 5.2% in the August to October quarter from 5.3% in the July to September quarter. It was the lowest reading since three months to January 2006.

Analysts had expected the unemployment rate to remain unchanged at 5.3%.

The claimant count rose by 3,900 people in November, beating expectations for a rise by 1,500, after an increase of 200 people in October. October's figure was revised down from a 3,300 increase.

U.K. unemployment in the July to September period dropped by 110,000 to 1.71 million from the previous quarter.

Average weekly earnings, excluding bonuses, climbed by 2.0% in the August to October quarter, missing expectations for a 2.0% rise, after a 2.4% gain in the July to September quarter. The previous quarter's figure was revised down from a 2.5% increase.

Average weekly earnings, including bonuses, rose by 2.4% in the August to October quarter, missing expectations for a gain of 2.5%, after a 3.0% increase in the July to September quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

-

11:23

ZEW Institute and Credit Suisse Group’s survey: Switzerland's economic sentiment index jumps to 16.6 in December

A survey by the ZEW Institute and Credit Suisse Group showed on Wednesday that Switzerland's economic sentiment index jumped to 16.6 in December from 0.0 in November.

"As in the previous months, the clear majority of survey respondents regard the present state of Switzerland's economy as being "normal". The group of analysts sharing this assessment has increased slightly and now amounts to 86.1 per cent of respondents," the ZEW said.

The current conditions climbed to -2.7 in December from -12.2 points in November.

-

11:07

Reserve Bank of Australia Governor Glenn Stevens: the central bank could cut its interest rate further

The Reserve Bank of Australia Governor Glenn Stevens said in an interview with the Financial Review published Wednesday that the central bank could cut its interest rate further.

"The stated position of the board is that inflation is sufficiently low that, if it makes sense to ease a bit further to help the economy, then we can," he said.

He added that interest rate "can fall further if that's helpful".

-

11:01

Eurozone: Harmonized CPI ex EFAT, Y/Y, November 0.9% (forecast 0.9%)

-

11:00

Eurozone: Trade balance unadjusted, October 24.1 (forecast 21.5)

-

11:00

Eurozone: Harmonized CPI, Y/Y, November 0.2% (forecast 0.1%)

-

11:00

Eurozone: Harmonized CPI, November -0.1% (forecast -0.2%)

-

11:00

Switzerland: Credit Suisse ZEW Survey (Expectations), December 16.6

-

10:57

New Zealand’s seasonally adjusted current account deficit is NZ$1.8 billion in the third quarter

Statistics New Zealand released its current account data on late Tuesday evening. New Zealand's seasonally adjusted current account deficit was NZ$1.8 billion in the third quarter, down NZ$322 million from the second quarter.

An increase in export earnings offset the rise in the overseas expenditure.

"Overseas visitor spending is driving our services surplus, which has grown each quarter since December 2013. On average, visitors spent more per person this quarter than last, which was the key driver for the increase in total expenditure," international statistics manager Jason Attewell said.

"The falling New Zealand dollar may also have been a factor in attracting visitors to New Zealand as the better exchange rate meant visitors could get more for their money," he added.

-

10:44

Bank of Canada Governor Stephen Poloz: the recovery of the Canadian economy was on track

The Bank of Canada Governor Stephen Poloz said on Tuesday that the recovery of the Canadian economy was on track.

"Although Q3 was quite good, it was not necessarily the new trend line. We expected Q4 to be a little softer than Q3. So far, things have been more or less in line with the dynamic that we predicted," he said.

"We do think that the positives will be dominant in 2016," Poloz added.

-

10:35

Moody's cuts its oil forecasts

Moody's Investors Service lowered its oil forecasts on Tuesday. The agency expects Brent price of $43 a barrel in 2016, down from an earlier forecast of $53, and WTI price of $40 per barrel in 2016, down from an earlier forecast of $48. Brent and WTI prices are expected to increase $5 per barrel in 2017 and 2018.

"Moody's Investors Service has significantly lowered its price assumptions for Brent crude and West Texas Intermediate crude as continued high levels of production by global oil producers has significantly exceeded growth in oil consumption. The potential lifting of Iranian sanctions could add significant supply to the market in 2016, offsetting or even exceeding expected declines in US production. The rating agency says this will lead to a prolonged period of oversupply that will continue to keep oil prices low," the agency said in its statement.

-

10:30

United Kingdom: ILO Unemployment Rate, October 5.2% (forecast 5.3%)

-

10:30

United Kingdom: Claimant count , November 3.9 (forecast 1.5)

-

10:30

United Kingdom: Average Earnings, 3m/y , October 2.4% (forecast 2.5%)

-

10:30

United Kingdom: Average earnings ex bonuses, 3 m/y, October 2.0% (forecast 2.3%)

-

10:22

OPEC Secretary-General Abdullah Al-Badri: oil prices will not continue to drop

OPEC Secretary-General Abdullah Al-Badri said on Tuesday that oil prices will not continue to drop as some oil producer will lower its output.

"I saw very high price, I saw low price, and this is one of them. This will not continue. In a few months or a year or so this will change," he said.

Al-Badri noted that OPEC does not target a certain price but is looking for a fair value.

-

10:11

U.S. congressional leaders reach a deal, which would lift the ban on crude oil exports

U.S. congressional leaders on Tuesday reached a deal, which would lift the 40-year-old ban on crude oil exports. The deal could help U.S. oil producers to sell oil at a better price in the export market.

The deal would also lead to higher spending on defence and would avert a U.S. government shutdown.

-

10:00

Eurozone: Manufacturing PMI, December 53.1 (forecast 52.8)

-

10:00

Eurozone: Services PMI, December 53.9 (forecast 54.1)

-

09:30

Germany: Manufacturing PMI, December 53 (forecast 53)

-

09:30

Germany: Services PMI, December 55.4 (forecast 55.5)

-

09:22

Option expiries for today's 10:00 ET NY cut

USD/JPY:120.00-10 (USD 2bln) 121.00 (720m) 121.30-35 (350m)

EUR/USD:1.0900 (EUR 919m) 1.0945-50 (575m) 1.1000 (622m) 1.1100 (664m) 1.1200 (1.5bln)

EUR/GBP:0.7170 (EUR 350m)

AUD/USD:0.7245 (AUD 273m) 0.7350 (628m)

AUD/NZD:1.0950 (AUD 901m)

-

09:00

France: Manufacturing PMI, December 51.6 (forecast 50.5)

-

09:00

France: Services PMI, December 50 (forecast 50.8)

-

08:43

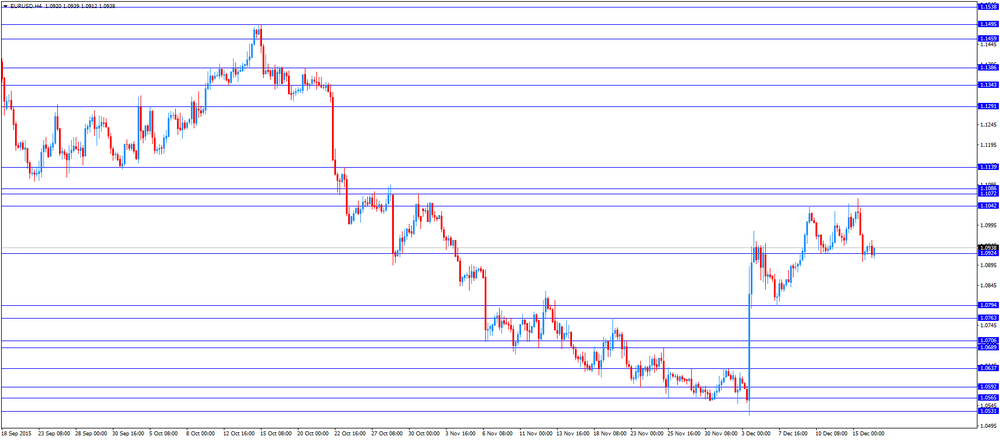

Options levels on wednesday, December 16, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1158 (7222)

$1.1093 (4396)

$1.1043 (4961)

Price at time of writing this review: $1.0953

Support levels (open interest**, contracts):

$1.0888 (549)

$1.0830 (1778)

$1.0773 (2216)

Comments:

- Overall open interest on the CALL options with the expiration date January, 8 is 55144 contracts, with the maximum number of contracts with strike price $1,1100 (7222);

- Overall open interest on the PUT options with the expiration date January, 8 is 66930 contracts, with the maximum number of contracts with strike price $1,0450 (8162);

- The ratio of PUT/CALL was 1.21 versus 1.23 from the previous trading day according to data from December, 15

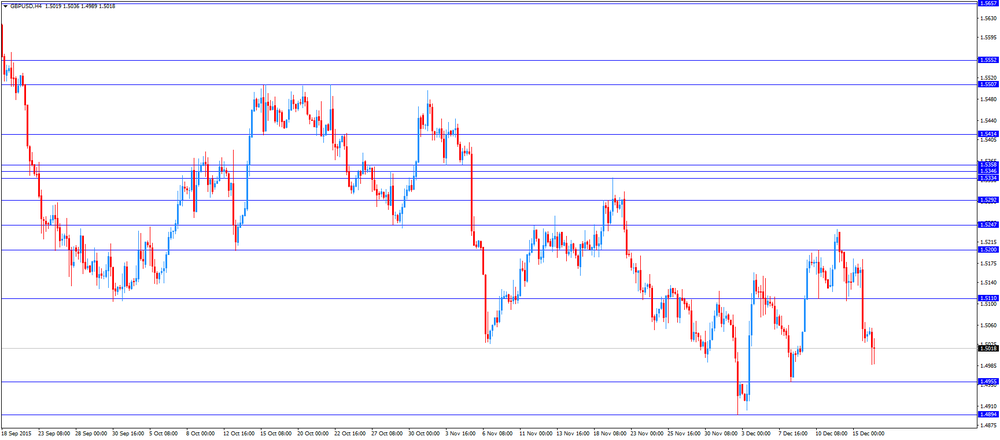

GBP/USD

Resistance levels (open interest**, contracts)

$1.5303 (1593)

$1.5205 (1225)

$1.5108 (2529)

Price at time of writing this review: $1.5049

Support levels (open interest**, contracts):

$1.4991 (1818)

$1.4894 (2212)

$1.4797 (1395)

Comments:

- Overall open interest on the CALL options with the expiration date January, 8 is 18193 contracts, with the maximum number of contracts with strike price $1,5100 (2529);

- Overall open interest on the PUT options with the expiration date January, 8 is 18306 contracts, with the maximum number of contracts with strike price $1,5100 (3087);

- The ratio of PUT/CALL was 1.00 versus 1.00 from the previous trading day according to data from December, 15

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:14

Foreign exchange market. Asian session: the U.S. dollar little changed

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

01:35 Japan Manufacturing PMI (Preliminary) December 52.6 52.5

The U.S. dollar traded range-bound ahead of the Fed's anticipated interest rate decision later today. Investors expect the central bank of the U.S. to raise its interest rates for the first time since 2006. Several times Fed Chair Janet Yellen pointed to a possibility of a liftoff in interest rates at December meeting in case of sustained economic growth and lower unemployment rate. Last week data showed that the unemployment rate remained at record-low 5% in November, while the number of employed outside the farming sector rose by 211,000. Higher rates would support the USD.

The Australian dollar edged up amid RBA Governor Glenn Stevens' speech. He made no comments on the recent strength of the Australian dollar. Usually Stevens tries to intervene verbally against the AUD in an interview with Australian Financial Review ahead of the holiday season, but not this year. Stevens made optimistic comments on the country's economy. "I think the economy is handling the shock remarkably well," he said.

EUR/USD: the pair fluctuated within $1.0925-50 in Asian trade

USD/JPY: the pair traded within Y121.60-95

GBP/USD: the pair traded within $1.5035-55

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

08:00 France Manufacturing PMI (Preliminary) December 50.6 50.5

08:00 France Services PMI (Preliminary) December 51 50.8

08:30 Germany Manufacturing PMI (Preliminary) December 52.9 53

08:30 Germany Services PMI (Preliminary) December 55.6 55.5

09:00 Eurozone Manufacturing PMI (Preliminary) December 52.8 52.8

09:00 Eurozone Services PMI (Preliminary) December 54.2 54.1

09:30 United Kingdom Average earnings ex bonuses, 3 m/y October 2.5% 2.3%

09:30 United Kingdom Average Earnings, 3m/y October 3% 2.5%

09:30 United Kingdom Claimant count November 3.3 1.5

09:30 United Kingdom ILO Unemployment Rate October 5.3% 5.3%

10:00 Eurozone Trade balance unadjusted October 20.5 21.5

10:00 Eurozone Harmonized CPI November 0.1% -0.2%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Finally) November 1.1% 0.9%

10:00 Eurozone Harmonized CPI, Y/Y (Finally) November 0.1% 0.1%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) December 0.0

12:00 U.S. MBA Mortgage Applications December 1.2%

13:30 Canada Foreign Securities Purchases October 3.35

13:30 U.S. Housing Starts November 1060 1135

13:30 U.S. Building Permits November 1161 1150

14:15 U.S. Capacity Utilization November 77.5% 77.4%

14:15 U.S. Industrial Production (MoM) November -0.2% -0.1%

14:15 U.S. Industrial Production YoY November 0.3%

14:45 U.S. Manufacturing PMI (Preliminary) December 52.8 52.6

15:30 U.S. Crude Oil Inventories December -3.568 -1.4

19:00 U.S. Fed Interest Rate Decision 0.25% 0.5%

19:00 U.S. FOMC Economic Projections

19:00 U.S. FOMC Statement

19:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter III 0.4% 0.8%

21:45 New Zealand GDP y/y Quarter III 2.4% 2.3%

23:50 Japan Trade Balance Total, bln November 111.5 -446.2

-

07:50

Oil prices mixed ahead of Fed's interest rate decision

West Texas Intermediate futures for January delivery is currently at $37.11 (-0.64%), while Brent crude is at $38.59 (+0.36%) after gains generated late Tuesday when sources reported that congressional leaders agreed to lift the oil exports ban, which lasted for 40 years. The House and Senate need to pass this bill and U.S. President Barack Obama must sign it. This deal could help the U.S. reduce its crude oil inventories.

Investors await the Fed's interest rate decision and crude inventories data from the Energy Information Administration.

-

07:17

Gold climbed ahead of Fed rates decision

Gold climbed to $1,064.60 (+0.28%) ahead of the end of the Fed's two-day policy meeting. The central bank of the U.S. is widely expected to raise rates to a range of 0.25%-0.50% from 0%-0.25%. Higher rates increase the opportunity cost of holding the non-interest paying precious metal and reduce demand for it. Bullion has already lost 9% of its price this year.

Analysts say that gold might plunge after the rate hike, but rebound this loss in the short-term period as the hike is expected.

-

07:04

Global Stocks: U.S. stock indices rose

U.S. stock indices rose on Tuesday supported by gains in oil prices.

The Dow Jones Industrial Average added 156.41 points, or 0.9%, to 17,524.91. The S&P 500 climbed 21.47 points, or 1.1%, to 2,043.4 (all of its 10 sectors closed higher; the energy sector gained 2.9%). The Nasdaq Composite rose 43.13 points, or 0.9% to 4,995.36.

Data showed that U.S. consumer prices were unchanged in November due to declines in gas prices. Nevertheless the core inflation showed some strengthening amid rising services prices. The CPI was unchanged in November on a seasonally adjusted basis after a 0.2% increase in October. The so-called core index rose by 0.2% just like in the two previous months. Both readings were in line with expectations.

This morning in Asia Hong Kong Hang Seng rose 2.07%, or 439.65, to 21,714.02. China Shanghai Composite Index climbed 0.38%, or 13.32, to 3.523.67. The Nikkei jumped 2.52%, or 467.88, to 19,033.78.

Asian indices advanced following gains in U.S. stocks. Analysts say that rising stock prices ahead of the Fed's interest rate decision signal that market participants are convinced that the rate hike will take place.

Japanese stocks rose with financial companies leading the gains. Shares of exporters also climbed.

-

03:05

Nikkei 225 18,879.03 +313.13 +1.69 %, Hang Seng 21,628.98 +354.61 +1.67 %, Shanghai Composite 3,522.99 +12.63 +0.36 %

-

02:35

Japan: Manufacturing PMI, December 52.5

-

01:07

Commodities. Daily history for Dec 15’2015:

(raw materials / closing price /% change)

Oil 36.74 -1.63%

Gold 1,060.40 -0.11%

-

01:07

Stocks. Daily history for Sep Dec 15’2015:

(index / closing price / change items /% change)

Nikkei 225 18,565.9 -317.52 -1.68 %

Hang Seng 21,274.37 -35.48 -0.17 %

Shanghai Composite 3,510.9 -9.76 -0.28 %

FTSE 100 6,017.79 +143.73 +2.45 %

CAC 40 4,614.4 +141.33 +3.16 %

Xetra DAX 10,450.38 +311.04 +3.07 %

S&P 500 2,043.41 +21.47 +1.06 %

NASDAQ Composite 4,995.36 +43.13 +0.87 %

Dow Jones 17,524.91 +156.41 +0.90 %

-

01:05

Currencies. Daily history for Dec 15’2015:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0929 -0,57%

GBP/USD $1,5040 -0,66%

USD/CHF Chf0,9913 +0,67%

USD/JPY Y121,67 +0,53%

EUR/JPY Y132,99 -0,02%

GBP/JPY Y182,94 -0,16%

AUD/USD $0,7199 -0,60%

NZD/USD $0,6765 +0,13%

USD/CAD C$1,3731 -0,01%

-

00:31

Australia: Leading Index, November -0.2%

-

00:04

Schedule for today, Wednesday, Dec 16’2015:

(time / country / index / period / previous value / forecast)

00:35 Japan Manufacturing PMI (Preliminary) December 52.6

08:00 France Manufacturing PMI (Preliminary) December 50.6 50.5

08:00 France Services PMI (Preliminary) December 51 50.8

08:30 Germany Manufacturing PMI (Preliminary) December 52.9 52.9

08:30 Germany Services PMI (Preliminary) December 55.6 55.5

09:00 Eurozone Manufacturing PMI (Preliminary) December 52.8 52.8

09:00 Eurozone Services PMI (Preliminary) December 54.2 54.1

09:30 United Kingdom Average earnings ex bonuses, 3 m/y October 2.5% 2.3%

09:30 United Kingdom Average Earnings, 3m/y October 3% 2.5%

09:30 United Kingdom Claimant count November 3.3 2

09:30 United Kingdom ILO Unemployment Rate October 5.3% 5.3%

10:00 Eurozone Trade balance unadjusted October 20.5 21.5

10:00 Eurozone Harmonized CPI November 0.1% -0.2%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Finally) November 1.1% 0.9%

10:00 Eurozone Harmonized CPI, Y/Y (Finally) November 0.1% 0.1%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) December 0.0

12:00 U.S. MBA Mortgage Applications December 1.2%

13:30 Canada Foreign Securities Purchases October 3.35

13:30 U.S. Housing Starts November 1060 1140

13:30 U.S. Building Permits November 1161 1150

14:15 U.S. Capacity Utilization November 77.5% 77.5%

14:15 U.S. Industrial Production (MoM) November -0.2% -0.1%

14:15 U.S. Industrial Production YoY November 0.3%

14:45 U.S. Manufacturing PMI (Preliminary) December 52.8 52.7

15:30 U.S. Crude Oil Inventories December -3.568

19:00 U.S. Fed Interest Rate Decision 0.25% 0.5%

19:00 U.S. FOMC Economic Projections

19:00 U.S. FOMC Statement

19:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter III 0.4% 0.8%

21:45 New Zealand GDP y/y Quarter III 2.4% 2.3%

23:50 Japan Trade Balance Total, bln November 111.5 -446.2

-