Market news

-

19:00

U.S.: Consumer Credit , August 25.87 (forecast 16.5)

-

19:00

DJIA 18268.84 0.34 0%, NASDAQ 5295.00 -11.85 -0.22%, S&P 500 2156.75 -4.02 -0.19%

-

16:01

European stocks closed: FTSE 7044.39 44.43 0.63%, DAX 10490.86 -77.94 -0.74%, CAC 4449.91 -30.19 -0.67%

-

15:46

Oil traded in the red zone today. Potential reversal

Oil prices fell after the statement of the Russian Minister of Petroleum weakened hopes for a production cut agreement.

Earlier Friday, oil prices briefly rose after the US Labor Department report that showed an increase in the number of jobs to 156,000, while economists had expected 175 000. The dollar index was down by 0.12%, while the earlier on Friday it was in positive territory.

In recent months, oil prices are highly dependent on the US currency. A weaker dollar typically makes oil more attractive in price to holders of other currencies.

Recently, however, traders in the oil market are increasingly watching OPEC and its plans to reduce production. Despite doubts about some of the particulars of the agreement and skepticism about the readiness of the cartel to implement it, oil has risen to the highest levels since June.

The cost of the November futures for US light crude oil WTI fell to 49.96 dollars per barrel on the New York Mercantile Exchange.

November futures price for North Sea petroleum mix of Brent crude rose to 51.89 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

15:39

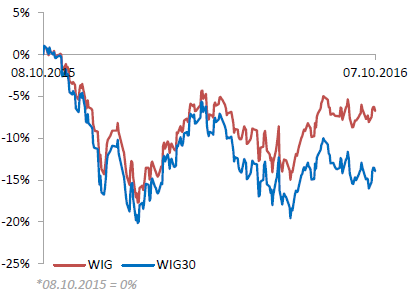

WSE: Session Results

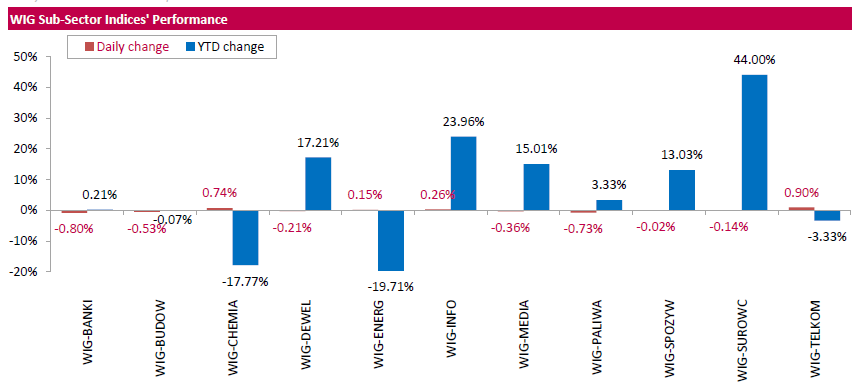

Polish equity market closed lower on Friday. The broad market measure, the WIG index, fell by 0.52%. Most sectors dropped, with financials (-0.80%) underperforming.

The large-cap stocks' benchmark, the WIG30 Index, plunged by 0.44%. In the index basket, coking coal producer JSW (WSE: JSW) topped the list of decliners with a 2.81% drop. Other major laggards were genco TAURON PE (WSE: TPE), bank BZ WBK (WSE: BZW), railway freight transport operator PKP CARGO (WSE: PKP) and oil and gas producer PGNIG (WSE: PGN), slipping by 1.9%-1.98%. On the other side of the ledger, bank ALIOR (WSE: ALR) led the gainers with a 3.57% advance, followed by two chemical producers GRUPA AZOTY (WSE: ATT) and SYNTHOS (WSE: SNS), each growing by 1.36%.

-

15:31

Wall Street. Major U.S. stock-indexes slightly fell

Major U.S. stock-indexes lower on Friday after a weaker-than-expected September jobs report indicated that the U.S. Federal Reserve would be cautious about raising interest rates. U.S. employment growth slowed for the third straight month in September, with employers adding 156,000 jobs, a report by the Labor Department showed. Economists polled by Reuters had expected 175,000. The rate of unemployment climbed to 5% from 4.9% in August, though the increase was driven by Americans rejoining the labor force.

Most of Dow stocks in negative area (21 of 30). Top gainer - The Travelers Companies, Inc. (TRV, +1.20%). Top loser - United Technologies Corporation (UTX, -1.80%).

Most of S&P sectors also in negative area. Top gainer - Conglomerates (+0.1%). Top loser - Industrial Goods (-1.3%).

At the moment:

Dow 18153.00 -46.00 -0.25%

S&P 500 2149.00 -7.50 -0.35%

Nasdaq 100 4861.00 -11.00 -0.23%

Oil 50.33 -0.11 -0.22%

Gold 1255.70 +2.70 +0.22%

U.S. 10yr 1.75 +0.01

-

15:28

Gold moderately higher

Gold prices rose as more negative than expected data on the US labor market have reduced the likelihood of a Fed hike in the coming months.

The Labor Department reported that the US economy has shown a modest increase in the number of jobs in September, but wage increase has accelerated, which indicates a stable situation on the labor market.

According to the data, the seasonally adjusted number of people employed in non-agricultural sectors of the economy increased by 156 thousand, recording the smallest increase since May. The unemployment rate, obtained from a separate household survey, increased by 0.1 percentage points to 5.0%. Recent growth reflects encouraging signs: the total labor force grew rapidly, as Americans who previously were too discouraged to look for work again start to search. Economists had expected employment to increase by 175 thousand, while the unemployment rate to remain unchanged. The government also revised data for the previous months, although the overall outlook has not changed. According to the new estimates, the economy added 167 thousand jobs in August compared with the previously reported 151 thousand. Meanwhile, the change for July was revised downward to 252 thousand from 275 thousand..

In addition, the report showed that wages growth accelerated last month. Private sector workers earned on average $ 25.79 per hour in September, up 6 cents, or 0.2% more than a month earlier. In annual terms, the average wage increased by 2.6%.

"The data on the labor market should support the gold after a fairly uneven trading this week," - said Bob Haberkorn from RJO Futures.

Since last Friday, the price of gold fell by more than 4%, under pressure due to the strengthening of the dollar.

The cost of December futures for gold on COMEX rose to $ 1267.6 per ounce.

-

14:19

Canada: Ivey PMI has grown significantly in September

The research results presented by the Association of purchasing managers in Canada and the Richard Ivey School of Business, have shown that the index of business activity rose sharply, exceeding average forecasts.

According to the report, the September business activity index rose to 58.4 points from 52.3 points in the previous month. Analysts had expected the figure at 53.0 points. Recall, the indicator shows the level of business activity of the industrial sector. More than 150 managers from different regions and sectors are invited to assess the level of purchases compared to the previous month (above, below or at the same level). A reading above 50 indicates an increase in purchases, and a value below 50 indicates a decrease in their volume.

In addition:

-

employment sub-index rose to 54.0 in September from 46.9 in August

-

stocks fell in September to 46.7 against 61.2 in August

-

The index of price fell to 56.8 against 56.7 in August

-

delivery time index rose to 51.7 from 46.1 in August

The unadjusted index of business activity of purchasing managers in September amounted to 68.1 points compared to 53.8 points in August.

-

-

14:15

U.S. wholesale inventories in August fell more than previously reported

U.S. wholesale inventories in August fell more than previously reported as businesses ran down their stocks of farm goods and clothes, the Commerce Department reported on Friday.

Inventories dropped 0.2 percent during the month, the department said.

A drop in inventory investment weighed heavily on economic growth in the second quarter, and some economists believe the inventory correction is close to running its course.

But stocks have edged lower in the first two months of the third quarter, which could drag on economic growth during the period.

-

14:00

Canada: Ivey Purchasing Managers Index, September 58.4

-

14:00

U.S.: Wholesale Inventories, August -0.2% (forecast -0.1%)

-

13:50

WSE: After start on Wall Street

This week key data turned out to be very similar to the previous ones. The number of jobs passed the forecast. Wage increase was in line with expectations, but worse presented the unemployment rate. The report was worse than expected, and some players will be treated it as reducing the likelihood of interest rate hikes by the Fed. Looking at today's data is worth to remember that the market consensus says that the Fed may raise the price of the loan on December, so before the December FOMC meeting, there will be two more reports from the labor market, which can make a difference. For the stocks market data are neutral - neither too good nor too weak.

After weaker than expected data from the US labor market Wall Street started trading from small growths that are already at the beginning of the session led the S&P500 index to the highs of ending week. The scale of the increase, however, is so small that it is difficult to prejudge, not only the fate of the session, but even its first passage. One hour before the end today's trading the WIG20 index was at the level of 1,752 points (-0,54%).

-

13:44

Option expiries for today's 10:00 ET NY cut

EURUSD: 1.1000 (EUR 335m) 1.1100 (685m) 1.1120-25 (675m) 1.1135 (1.52bln)1.1150 (274m) 1.1175-80 (1.17bln) 1.1200 (446m) 1.1225 (686m) 1.1250 (690m) 1.1260 (316m) 1.1270 (373m) 1.1300 (333m) 1.1355 (224m) 1.1400 (1.12bln)

USDJPY: 101.00 (USD 811m) 101.50 (880m) 102.30-35 (730m) 102.75 (300m) 103.25(590m) 103.50 (634m) 103.75 (420m) 104.45-50 (483m) 105.00 (250m)

GBPUSD: 1.1730 (GBP 221m) 1.2290-1.2300 (GBP 623m) 1.2500 (1.18bln) 1.2700 (290m) 1.2900 (1.23bln) 1.3000 (582m)

EURGBP 0.8800 (EUR 200m) 0.8865 (236m)

USDCHF 0.9625 (USD 220m) 0.9705 (200m) 1.0000 (390m)

AUDUSD: 0.7300 (AUD 443m) 0.7390 (300m) 0.7400 (715m) 0.7475 (297m) 0.7560 (201m) 0.7595-0.7600 (670m) 0.7635 (318m)

USDCAD: 1.3025 ((USD 260m) 1.3100 (441m) 1.3120-25 (358m) 1.3170 (717m) 1.3200 (815m) 1.3245-50 (346m) 1.3275 (350m) 1.3300 (440m)

NZD/USD: 0.7100 (NZD 517m) 0.7150 (239m)

EURJPY 113.00 (EUR 300m)

-

13:35

United Kingdom: NIESR GDP Estimate, September 0.4%

-

13:34

-

13:33

U.S. Stocks open: Dow +0.07%, Nasdaq +0.03%, S&P +0.11%

-

13:31

UK GDP growth of 0.4 percent in 2016Q3 - NIESR

Our monthly estimates of GDP suggest that output grew by 0.4 per cent in the three months ending in September 2016 after growth of 0.5 per cent in the three months ending in August 2016. Our estimates suggest that economic growth slowed in 2016Q3 to 0.4 per cent, from 0.7 per cent in 2016Q2 .

James Warren, Research Fellow at NIESR, said "Our estimates suggest that economic growth slowed in 2016Q3 to 0.4 per cent, from 0.7 per cent in 2016Q2. While retail sales have been buoyant in recent months, the production sector has acted as a drag on economic growth. We estimate that output from the production sector declined by 0.2 per cent in the third quarter of this year."

-

13:27

Before the bell: S&P futures -0.26%, NASDAQ futures -0.22%

U.S. stock-index futures slipped as investors assessed jobs data.

Global Stocks:

Nikkei 16,860.09 -39.01 -0.23%

Hang Seng 23,851.82 -100.68 -0.42%

Shanghai Closed

FTSE 7,076.54 +76.58 +1.09%

CAC 4,475.49 -4.61 -0.10%

DAX 10,546.49 -22.31 -0.21%

Crude $50.41 (-0.06%)

Gold $1262.10 (+0.73%)

-

13:07

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

171.76

0.12(0.0699%)

428

ALCOA INC.

AA

31.94

0.16(0.5035%)

866

Amazon.com Inc., NASDAQ

AMZN

844.05

2.39(0.284%)

16398

American Express Co

AXP

62

0.06(0.0969%)

250

Apple Inc.

AAPL

114.11

0.22(0.1932%)

130869

AT&T Inc

T

39.19

0.08(0.2045%)

9314

Barrick Gold Corporation, NYSE

ABX

15.91

0.27(1.7263%)

226874

Chevron Corp

CVX

102

-0.18(-0.1762%)

4785

Cisco Systems Inc

CSCO

31.5

0.02(0.0635%)

721

Citigroup Inc., NYSE

C

48.92

-0.15(-0.3057%)

23896

Exxon Mobil Corp

XOM

86.99

-0.05(-0.0574%)

4486

Facebook, Inc.

FB

128.89

0.15(0.1165%)

44314

Ford Motor Co.

F

12.4

0.01(0.0807%)

2700

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

10.42

0.12(1.165%)

51127

General Electric Co

GE

29.12

-0.15(-0.5125%)

38802

General Motors Company, NYSE

GM

32.5

-0.03(-0.0922%)

1000

Goldman Sachs

GS

167

-0.15(-0.0897%)

560

Google Inc.

GOOG

779.85

2.99(0.3849%)

2464

Hewlett-Packard Co.

HPQ

15.52

-0.08(-0.5128%)

576

Home Depot Inc

HD

129.71

-0.48(-0.3687%)

26844

HONEYWELL INTERNATIONAL INC.

HON

108.9

-6.71(-5.804%)

81962

Intel Corp

INTC

38.05

-0.02(-0.0525%)

1813

International Business Machines Co...

IBM

157.45

0.57(0.3633%)

200

JPMorgan Chase and Co

JPM

67.71

-0.16(-0.2357%)

2275

Nike

NKE

52.26

0.23(0.442%)

2821

Starbucks Corporation, NASDAQ

SBUX

53.3

0.16(0.3011%)

632

The Coca-Cola Co

KO

41.77

0.06(0.1439%)

905

Twitter, Inc., NYSE

TWTR

19.8501

-0.0199(-0.1002%)

353036

United Technologies Corp

UTX

101.8

-0.28(-0.2743%)

2984

Wal-Mart Stores Inc

WMT

69.15

-0.21(-0.3028%)

1029

Walt Disney Co

DIS

93.05

0.22(0.237%)

2949

Yahoo! Inc., NASDAQ

YHOO

43.17

-0.51(-1.1676%)

39949

Yandex N.V., NASDAQ

YNDX

22.18

0.05(0.2259%)

100

-

12:52

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Alcoa (AA) target raised to $39 from $13 at Stifel

Wal-Mart (WMT) target lowered to $75 from $76 at RBC Capital Mkts

Wal-Mart (WMT) target lowered to $76 from $78 at Telsey Advisory Group

-

12:41

Canadian employment beats expectations. USD/CAD supported

Employment rose by 67,000 (+0.4%) in September, with most of the increase in part-time work. The unemployment rate was unchanged at 7.0%, as more people participated in the labour market.

In the third quarter of 2016, employment gains totalled 62,000 (+0.3%). This followed little change in employment in the second quarter and a slight increase of 33,000 (+0.2%) in the first quarter.

Compared with 12 months earlier, employment rose by 139,000 (+0.8%), with most of the gains in part-time work. Over the same period, the total number of hours worked edged up 0.2%.

In September, there were more employed people aged 55 and older. At the same time, there was little change in employment among both the 15-to-24 and 25-to-54 age groups.

Provincially, employment rose in Quebec, Alberta and New Brunswick. There was little change in the other provinces.

In September, more people worked in public administration, educational services, and transportation and warehousing. At the same time, employment declined in health care and social assistance.

Self-employment increased in September, while there was little change in the number of private and public sector employees.

-

12:38

-

12:36

US employment situation improves less than forecast

Total nonfarm payroll employment increased by 156,000 in September, and the unemployment rate was little changed at 5.0 percent, the U.S. Bureau of Labor Statistics reported today. Employment gains occurred in professional and business services and in health care.

The unemployment rate, at 5.0 percent, and the number of unemployed persons, at 7.9 million, changed little in September. Both measures have shown little movement, on net, since August of last year.

In September, both the labor force participation rate, at 62.9 percent, and the employment-population ratio, at 59.8 percent, changed little.The average workweek for all employees on private nonfarm payrolls increased by 0.1 hour to 34.4 hours in September. In manufacturing, the workweek increased by 0.1 hour to 40.7 hours, while overtime was unchanged at 3.3 hours. The average workweek for production and nonsupervisory

employees on private nonfarm payrolls was unchanged at 33.5 hours.In September, average hourly earnings for all employees on private nonfarm payrolls rose by 6 cents to $25.79. Over the year, average hourly earnings have risen by 2.6 percent. Average hourly earnings of private-sector production and nonsupervisory employees increased by 5 cents to $21.68

in September. -

12:30

Canada: Unemployment rate, September 7% (forecast 7%)

-

12:30

U.S.: Average hourly earnings , September 0.2% (forecast 0.2%)

-

12:30

U.S.: Unemployment Rate, September 5% (forecast 4.9%)

-

12:30

U.S.: Average workweek, September 34.4 (forecast 34.4)

-

12:30

U.S.: Nonfarm Payrolls, September 156 (forecast 175)

-

12:30

Canada: Employment , September 67.2% (forecast 10)

-

12:18

ECB's Draghi: We Will Act, if Warranted, by Using All Our Instruments

-

Our Policies Create Unique Window of Opportunity for

-

We'll go further than March 2017 if we need to

-

-

12:00

Orders

EUR/USD

Offers 1.1220 1.1235 1.1250 1.1280 1.1300 1.1320 1.1350

Bids 1.1100 1.1080 1.1050 1.1030 1.1000

GBP/USD

Offers 1.2480 1.2500 1.2550 1.2600 1.2630 1.2650 1.2700

Bids 1.2400-10 1.2350 1.2300 1.2250 1.2200

EUR/GBP

Offers 0.8930 0.8950 0.9000 0.9030 0.9050 0.9100

Bids 0.8900 0.8850-55 0.8835 0.8800 0.8785 0.8750

EUR/JPY

Offers 115.80 116.00 116.25-30 116.50 117.00 117.30 117.50

Bids 115.00 114.80 114.50 114.20 114.00

USD/JPY

Offers 104.00-05 104.20 104.30 104.50 104.80 105.00

Bids 103.50 103.25-30 103.00 102.85 102.70 102.50

AUD/USD

Offers 0.7585 0.7600 0.7630 0.7650 0.7685 0.7700 0.7720

Bids 0.7550 0.7530 0.7500 0.7485 0.7450

-

11:48

German finance minister, Gabriel: The government doesn't have a risk assessment for Deutsche Bank

-

DB faces enormous challenges with fines from US

-

the fact that the DB head wants to change the business model is a sign that they are reacting to risks

-

declines to comment on speculation that listed German companies want to help DB

-

Germany has an interest in ensuring DB has a successful future

*via forexlive -

-

11:05

French Prime Minister said that Hollande was right, calling for a tougher approach to Brexit

-

The country can not be both in and outside the EU

-

France and Germany has a special responsibility for the future of Europe

-

-

11:04

Major stock indices in Europe trading mixed

European stocks traded mostly in the red zone, as investors await US labor market data, which may affect the likelihood and timing of the Fed interest rates hike. Meanwhile, the British markets approaching all-time highs, receiving support from a renewed collapse of the pound.

According to analysts, today's NFP may provide additional arguments in favor of raising rates. According to the futures market, the likelihood of a Fed hike in December is 63.4% versus 59.8% the previous day. The median forecast for payrolls report is 175 thousand vs 151 thousand prior .. add the average value of the index over the past 12 months amounted to 204 ths.,

If the Fed will take such a step, the ECB may find itself in an even more precarious position. Earlier it was reported that the ECB may begin to gradually reduce the amount QE as the end date draws nearer (March 2017).

"There is a limit to what central banks can do to help the economy and the markets should start to take into account the growth in prices" - said Guillermo Samper expert at MPPM EK.

Little impact on markets had data for Germany and the UK. The Statistical Office Destatis reported that the volume of industrial production in Germany increased in August by 2.5 percent, after falling 1.5 percent in July (the index was not revised). Analysts, on average, had expected production to grow by only 0.8 percent. Last rate of increase was the fastest since January, when the volume of production increased by 2.8 percent. Excluding energy and construction, production increased by 3.3 percent compared to July.

Meanwhile, the Office for National Statistics reported that industrial production in the UK unexpectedly decreased in August, offsetting the previous two months of growth. The volume of industrial production fell by 0.4 percent on a monthly basis, which followed an increase of 0,1 percent in July and June. Economists had forecast that industrial production will increase again by 0.1 percent.

At the same time, the volume of production in the manufacturing industry rose by 0.2 percent after declined by 0.9 percent in July. Nevertheless, the pace of recent growth has been significantly lower than expected (+0.5 percent). The decline was seen in two of the four major sectors, led by mining and quarrying, where output fell by 3.7 per cent.

The composite index of the largest companies in the region Stoxx Europe 600 fell by 0.8 percent.

Creditors shares rises fot the fourth day, moving counter to the common market dynamics. Cost of Deutsche Bank AG rose 1.3 percent after people familiar with the matter, said that the bank holds informal talks with firms involved in securities, to explore various options, including raising capital.

Shares of mining companies rose after Bank of America analysts recommended buying shares of the sector.

Capitalization of Delta Lloyd NV increased by 2.1 per cent following the rejection of an unsolicited offer from the NN Group NV, referring to the very low valuation. It is worth emphasizing, NN Group NV offered 2.4 bln. Euro.

The cost of EON rose 2.4 percent after reports that Cevian Capital AB is considering the purchase of 10 percent stake in the German company.

At the moment:

FTSE 100 +75.06 7075.02 + 1.07%

DAX -59.93 10508.87 -0.57%

CAC 40 4457.85 -22.25 -0.50%

-

11:03

WSE: Mid session comment

After the morning market activity and the subsequent stabilization, everything pointed to the fact that for trade with a more dynamic we will have to wait until the publication of data in the US. This did not happen and two hours prior to the publication of mentioned data atmosphere in the markets deteriorated, in theory in a quietest phase of the trade and the Warsaw market in the wake of the DAX went down below the minimum of the morning. It is difficult to find a direct cause of such weakness. Looking for a bit of force to explain the observed weakness should be mentioned concerns before too strong data which will have impact for further increase the likelihood of the December interest rate hikes in the US.

At the halfway point of the session the WIG20 index was at the level of 1,751 points (-0,60%).

-

10:14

Extreme volatility continue on GBP pairs

-

10:04

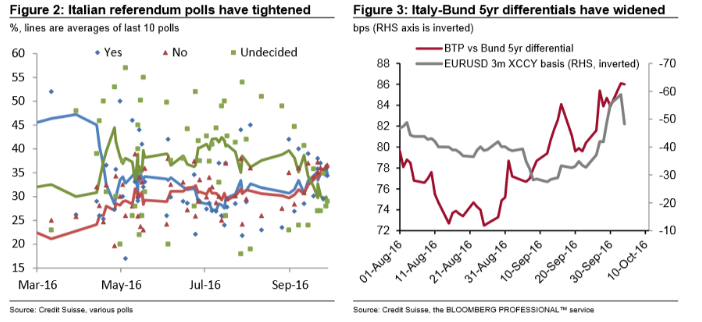

After GBP, 5 Scenarios For A Sudden Big Drop In EUR/USD - Credit Suisse

"We take the opportunity this week to cut our 3m EURUSD forecast to 1.10 from 1.15, leaving the 12m target unchanged at 1.05.

We have long feared that the UK vs EU tensions could become a problem in 2017, not least if they highlight divisions within the rest of the EU going into key elections in France and Germany next year. As GBP is suffering through its divorce, EUR cannot deny its own failings that helped end the marriage.

Italy's December 4 constitutional referendum is another key factor consider, with latest polls showing the "No" note in the lead. As Figure 3 shows, Italy - Germany yield differentials are widening again despite the ever-present ECB balance sheet support for European bond markets. And while European banking problems have taken a back seat this week, they are not off the agenda to the degree needed to tighten up the EUR basis again.

In light of and in addition to the discussion above, we see a number of scenarios that could lead to a sudden shift lower in EURUSD:

1. Article 50 being triggered before end-March 2017 in an acrimonious environment.

2. A related or separate pickup in euro area political and / or financial risk.

3. A rise in US inflation expectations / resumption of Fed rate hike cycle (not one and done).

4. The ECB introducing new easing measures even as the market now focuses on tapering.

5. The passage of USD political risk leads to a renewed bid for USD as the global currency of choice".

Copyright © 2016 Credit Suisse, eFXnews™

-

08:41

UK's trade balance deficit increased sharply

The UK's deficit on trade in goods and services was estimated to have been £4.7 billion in August 2016, a widening of £2.5 billion from July 2016. Exports increased by £0.1 billion and imports increased by £2.6 billion.

The deficit on trade in goods was £12.1 billion in August 2016, widening by £2.6 billion from July 2016. This widening reflected an increase in exports of £0.1 billion to £25.8 billion and an increase in imports of £2.7 billion to £37.9 billion.

Between the 3 months to May 2016 and the 3 months to August 2016, the total trade deficit for goods and services widened by £3.6 billion to £12.6 billion.

Between the 3 months to May 2016 and the 3 months to August 2016, the deficit on trade in goods widened by £3.3 billion to £34.5 billion. Exports increased by £0.9 billion (1.2%) and imports increased by £4.2 billion (4.0%).

-

08:40

UK manufacuring production growth slows down in August

This is the second release of Index of Production covering data post EU referendum. This release shows production decreased month-on-month in August 2016, with a fall in mining and quarrying partially offset by a rise in manufacturing. Users should note that ONS always warns against overly interpreting one month's figures.

In August 2016, total production output was estimated to have increased by 0.7% compared with August 2015. There were increases in 2 of the 4 main sectors, with the largest contribution coming from water supply, sewerage and waste management output, which increased by 7.0%.

Manufacturing was estimated to have increased by 0.5% on a year ago. Other manufacturing and repair provided the largest contribution to growth, increasing by 5.9%.

-

08:31

United Kingdom: Total Trade Balance, August -4.7

-

08:30

United Kingdom: Manufacturing Production (MoM) , August 0.2% (forecast 0.5%)

-

08:30

United Kingdom: Manufacturing Production (YoY), August 0.5% (forecast 0.9%)

-

08:30

United Kingdom: Industrial Production (YoY), August 0.7% (forecast 1.3%)

-

08:30

United Kingdom: Industrial Production (MoM), August -0.4% (forecast 0.1%)

-

08:10

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.1000 (EUR 335m) 1.1100 (685m) 1.1120-25 (675m) 1.1135 (1.52bln) 1.1150 (274m) 1.1175-80 (1.17bln) 1.1200 (446m) 1.1225 (686m) 1.1250 (690m) 1.1260 (316m) 1.1270 (373m) 1.1300 (333m) 1.1355 (224m) 1.1400 (1.12bln)

USD/JPY: 101.00 (USD 811m) 101.50 (880m) 102.30-35 (730m) 102.75 (300m) 103.25(590m) 103.50 (634m) 103.75 (420m) 104.45-50 (483m) 105.00 (250m)

GBP/USD: 1.1730 (GBP 221m) 1.2290-1.2300 (GBP 623m) 1.2500 (1.18bln) 1.2700 (290m) 1.2900 (1.23bln) 1.3000 (582m)

EUR/GBP 0.8800 (EUR 200m) 0.8865 (236m)

USD/CHF 0.9625 (USD 220m) 0.9705 (200m) 1.0000 (390m)

AUD/USD: 0.7300 (AUD 443m) 0.7390 (300m) 0.7400 (715m) 0.7475 (297m) 0.7560 (201m) 0.7595-0.7600 (670m) 0.7635 (318m)

USD/CAD: 1.3025 ((USD 260m) 1.3100 (441m) 1.3120-25 (358m) 1.3170 (717m) 1.3200 (815m) 1.3245-50 (346m) 1.3275 (350m) 1.3300 (440m)

NZD/USD: 0.7100 (NZD 517m) 0.7150 (239m)

EUR/JPY 113.00 (EUR 300m)

-

07:49

Major stock exchanges began trading mixed: FTSE + 0.6%, DAX -0.2%, CAC40 flat, FTMIB + 0.1%, IBEX flat

-

07:40

UK: The reduction in annual house price growth in line with forecasts

-

House prices in the three months to September were 5.8% higher than in the same three months of 2015

-

Prices in the last three months (JulySeptember) were 0.1% lower than in the preceding quarter

Martin Ellis, Halifax housing economist, said: "House prices in the three months to September were largely unchanged compared with the previous quarter. The annual rate of growth eased from 6.9% in August to 5.8%.

"The housing market has followed a steady downward trend over the past six months with clear evidence of both a softening in activity levels and an easing in house price inflation.

"The reduction in annual house price growth from a peak of 10.0% in March to 5.8% six months later remains in line with our forecast at the end of 2015. A lengthy period where house prices have risen more rapidly than earnings has put pressure on affordability, therefore constraining demand. Very low mortgage rates and a shortage of properties available for sale should, however, help support price levels over the coming months."

-

-

07:31

United Kingdom: Halifax house price index 3m Y/Y, September 5.8% (forecast 5.8%)

-

07:31

United Kingdom: Halifax house price index, September 0.1% (forecast 0%)

-

07:20

Output rebounded sharply in the French manufacturing industry

In August 2016, output rebounded sharply in the manufacturing industry (+2.2% after -0.2% in July). It also bounced back in the whole industry (+2.1% after -0.5%).

Manufacturing output diminished slightly over the past three months (-0.2%)

Over the past three months, output decreased slightly in the manufacturing industry (-0.2% q-o-q). It diminished in the overall industry (-0.5% q-o-q).

Output shrank strongly in mining and quarrying; energy; water supply (-1.9%) and in the manufacture of transport equipment (-1.8%), and more moderately in the manufacture of food products and beverages (-0.6%). It dropped sharply in the manufacture of coke and refined petroleum products (-4.3%). Conversely, output grew in the manufacture of machinery and equipment goods (+0.5%). It was stable in "other manufacturing".

-

07:17

WSE: After opening

WIG20 index opened at 1762.35 points (+0.03%)*

WIG 48046.12 0.07%

WIG30 2034.51 0.01%

mWIG40 4047.59 0.18%

*/ - change to previous close

Unexpectedly, the beginning of the session brings departure down both in our market as well as on the main floors of Euroland. Yesterday's session in Europe and in the United States clearly indicated that investors are waiting for today's publication of data from the US labor market. So it should be now and we may assume that the initial fall will soon be stopped, and move on to a more peaceful trade. After fifteen minutes of the session WIG20 index was at the level of 1,756 points (-028%).

-

06:45

France: Trade Balance, bln, August -4.3 (forecast -4.3)

-

06:45

France: Industrial Production, m/m, August 2.1% (forecast 0.7%)

-

06:30

"This is a price move you would expect from an emerging-market currency, not from the third most-heavily traded pair in the world"

The sharp fall in the British pound against the U.S. dollar that rattled markets earlier Friday is a worrying sign for the sterling, says Sean Callow, a senior currency strategist at Westpac Banking in Sydney. "This is a price move you would expect from an emerging-market currency, not from the third most-heavily traded pair in the world," says Callow. He says the move is reminiscent of a flash crash in April 2013 that sent the gold price down by about $200 in just moments. The metal price never fully rebounded, signaling a similar scenario might transpire for the pound. "It's not going to recover, there's no bottom, just air below," he says.

-

06:28

Options levels on friday, October 7, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1302 (3373)

$1.1256 (2382)

$1.1194 (1186)

Price at time of writing this review: $1.1120

Support levels (open interest**, contracts):

$1.1091 (5824)

$1.1046 (4358)

$1.0998 (4344)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 39308 contracts, with the maximum number of contracts with strike price $1,1500 (6100);

- Overall open interest on the PUT options with the expiration date October, 7 is 42032 contracts, with the maximum number of contracts with strike price $1,1150 (6497);

- The ratio of PUT/CALL was 1.07 versus 1.05 from the previous trading day according to data from October, 6

GBP/USD

Resistance levels (open interest**, contracts)

$1.2712 (828)

$1.2675 (313)

$1.2632 (70)

Price at time of writing this review: $1.2467

Support levels (open interest**, contracts):

$1.2400 (221)

$1.2300 (89)

$1.2200 (25)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 32962 contracts, with the maximum number of contracts with strike price $1,3500 (3374);

- Overall open interest on the PUT options with the expiration date October, 7 is 21817 contracts, with the maximum number of contracts with strike price $1,3000 (3210);

- The ratio of PUT/CALL was 0.66 versus 0.72 from the previous trading day according to data from October, 6

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

06:28

Expected negative start of trading on the major stock exchanges in Europe: DAX futures -0.2%, CAC40 -0.2%, FTSE -0.1%

-

06:28

WSE: Before opening

Thursday's session on Wall Street ended with a modest changes in the major indexes but much more interesting things happened in Asia, where was a displacement of sales of the British pound. The entire action lasted 3 minutes not giving anyone a chance to maintain a position on the Forex platforms either through killing SL orders or overload of margin. Unfortunately comes to mind a suspicion of price manipulation and the translations will be linked to alleged technical problems, which takes place in the first articles on the subject. The first comment from the Bloomberg Service as an excuse given the tile Asian market where the set algorithms joined to a sharp drop deepening it further. This event has more in common with the well-known phenomenon of the equity markets (ie. flash crash) than really serious sell-off but it could have an impact on equity markets in Europe.

Today's macro calendar contains a lot of data, but the key info for the markets will be "payrolls data", announced at 14:30 (Warsaw time). It will be the September data on employment change in the US and on the unemployment rate even the dynamics of the hourly rate. Investors bet the strong data on the currency market and it reinforce the dollar. Better than expected data will restore speculations about the December increase in the price of credit in the United States.

-

06:26

Comments about GBP flash crash

"I initially doubted what I saw on my screen," said Kenji Yoshii, a foreign exchange strategist at Mizuho Securities

Traders and strategists said the initial catalyst for the pound's drop came from remarks by French President François Hollande ... His comments came early in the Asian session, where light trading volumes likely exacerbated the move, they added

"There was a complete lack of two way interest in buying the pound on the way down," said Jeffrey Halley, a senior market strategist at Oanda.

Chris Weston, chief market strategist at IG, a broker. "This is the sort of time when the big U.S. traders are going home and Asian traders are getting back to the desk"

*via forexlive

-

06:22

Australian construction returns to growth in September

The Australian Industry Group/Housing Industry Association Australian Performance of Construction Index (Australian PCI®) lifted by 4.8 points to 51.4 points in the month (50 points is the threshold that separates expansion from contraction). This signalled a mild expansion across the construction industry led by stronger engineering construction activity.

Australian PCI® data for September revealed a marginal improvement in the activity subindex which remained in expansion (i.e. above 50 points) for a second consecutive month. In addition, businesses lifted their workforces, with employment increasing at its highest pace in two years. New orders continued to contract in September, although the rate of decline was slight, and slower than in August.

-

06:17

German industrial production up 2.5% in August

In August 2016, production in industry was up by 2.5% from the previous month on a price, seasonally and working day adjusted basis according to provisional data of the Federal Statistical Office (Destatis). In July 2016, the corrected figure shows a decrease of 1.5% from June 2016, thus confirming the provisional result published in the previous month.

In August 2016, production in industry excluding energy and construction was up by 3.3%. Within industry, the production of capital goods increased by 4.7% and the production of consumer goods by 3.3%.The production of intermediate goods showed an increase by 1.6%. Energy production was up by 1.1% in August 2016 and the production in construction decreased by 1.2%.

-

06:16

GBP/USD meltdown. The pound drops around 600 pips in the low volumes of the asian session. Moves in such low volumes almost always recover completely

-

06:00

Germany: Industrial Production s.a. (MoM), August 2.5% (forecast 0.8%)

-

05:21

Global Stocks

European stocks closed in negative territory Thursday, as airline shares were punished after a profit warning from EasyJet PLC, but bank shares rebounded.

U.S. stocks flatlined on Thursday as investors abstained from making big bets ahead of Friday's much-anticipated September jobs report. Stocks sold off in early trade, but the market recouped much of its losses after a high-ranking European Central Bank official repudiated reports that the central bank had discussed tapering its bond-buying program.

Market worries sent Asian equities broadly lower early Friday, as increasingly heated discussions over the U.K.'s exit from the European Union saw the pound plunging against the U.S. dollar. The selloff began after French President François Hollande called for tough negotiations with the U.K. as it leaves the EU. Britain wanted to leave the bloc "but doesn't want to pay," which was "not possible," Mr. Hollande said in comments cited by Sky News.

-

05:02

Japan: Leading Economic Index , August 101.2 (forecast 101.7)

-

05:01

Japan: Coincident Index, August 112

-

00:00

Japan: Labor Cash Earnings, YoY, August 1.4% (forecast 0.5%)

-