Market news

-

21:05

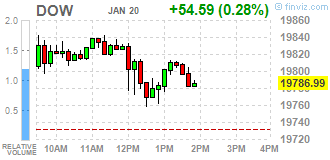

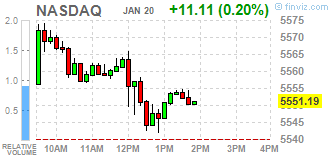

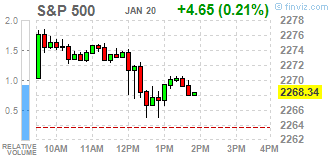

Major US stock indexes finished trading slightly above zero

Major stock indexes Wall Street rose slightly on Friday after the inaugural speech of Donald Trump as the 45th President of the United States of America. After the oath Trump said that US policy will be aimed at the purchase of US and hiring Americans. Trump Election promises about tax and regulatory reforms, as well as the increase in infrastructure spending drove Wall Street to new highs after the elections. Nevertheless, trade in recent weeks have calmed down, as investors awaited more clarity to stimulate the economy. Important statistics that could have an impact on market sentiment, was not published.

Oil prices rose by more than 2%, continuing yesterday's trend, helped by expectations that the coming weekend the world's leading manufacturers to demonstrate their commitment to the terms of the deal to reduce oil production.

The objective planned for this weekend's meeting in Vienna, which will be attended by members of the Organization of Petroleum Exporting Countries, and some producers outside the group is to create a mechanism to verify compliance with the conditions of the transaction by reducing production.

DOW index components ended the day mostly in positive territory (20 of 30). Most remaining shares fell General Electric Company (GE, -2.40%). Leaders of growth were shares of Merck & Co., Inc. (MRK, + 3.91%).

Sector S & P index closed mostly in positive territory. The leader turned out to be the sector of consumer goods (+ 0.5%). The health sector fell the most (-0.4%).

-

20:00

DJIA +0.32% 19,795.33 +62.93 Nasdaq +0.16% 5,549.04 +8.96 S$P +0.18% 2,267.72 +4.03

-

18:53

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes gains sharply on Friday after Donald Trump made his inaugural speech as the 45th president of the United States. "From this day forward it is going to be only America first," Trump said after being sworn in, adding that the U.S. policy will be to buy American and hire American. Trump's campaign promises of tax and regulatory reforms and higher infrastructure spending had driven Wall Street to new highs in a post-election rally. However, the Trump trade had been unraveling in recent weeks as investors waited for more clarity on his plans to boost the economy.

Most of Dow stocks in positive area (21 of 30). Top gainer - General Electric Company (GE, -1.87%). Top loser - Merck & Co., Inc. (MRK, +3.58%).

Most of S&P sectors in positive area. Top loser - Basic Materials (+0.5%). Top loser - Healthcare (-0.3%).

At the moment:

Dow 19732.00 +38.00 +0.19%

S&P 500 2264.75 +3.25 +0.14%

Nasdaq 100 5056.25 +2.75 +0.05%

Oil 53.30 +1.18 +2.26%

Gold 1205.20 +3.70 +0.31%

U.S. 10yr 2.48 +0.02

-

17:00

European stocks closed: FTSE 100 -10.00 7198.44 -0.14% DAX +33.24 11630.13 +0.29% CAC 40 +9.53 4850.67 +0.20%

-

16:41

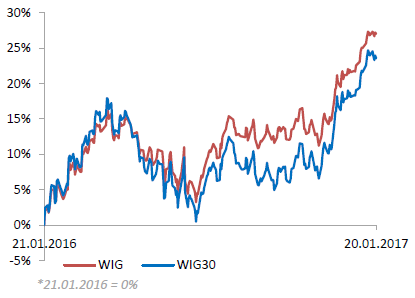

WSE: Session Results

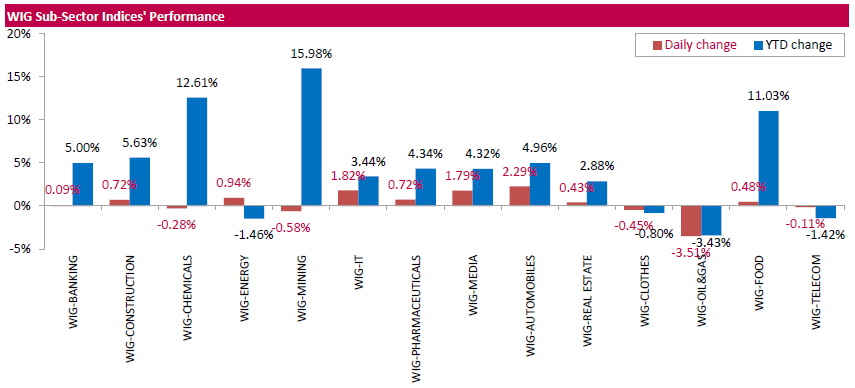

Polish equity market closed lower on Friday. The broad market measure, the WIG Index, fell by 0.15%. Sector-wise, oil and gas names (-3.51%) were the worst-performing group, while automobiles (+2.29%) outpaced.

The large-cap stocks' measure, the WIG30 Index, dropped by 0.31%. Oil refiner PKN ORLEN (WSE: PKN) was the biggest drag on the index, as the stock tumbled by 4.62% following announcement Poland increased its stake in the company. The Energy Ministry stated that Polish state pipeline operator PERN has bought a 4.9 percent stake in the company since August 2016 to date for about PLN1.5 bln ($365.37 mln). According to the statement, the stake acquisition will give Poland a lot more flexibility in terms of participation at the company's shareholder meetings. Recall, Poland's State Treasury is PKN ORLEN's largest shareholder with 27.52% of shares and votes. Among other biggest decliners were coking coal miner JSW (WSE: JSW), chemical producer GRUPA AZOTY (WSE: ATT) and bank MILLENNIUM (WSE: MIL), which fell by 3.7%, 2.6% and 2.14% respectively. At the same time, CD PROJEKT (WSE: CDR) recorded strongest advance among the WIG30 components, jumping by 3.93%. It was followed by IT-company ASSECO POLAND (WSE: ACP), bank ALIOR (WSE: ALR) and genco ENERGA (WSE: ENG), which gained 1.74%, 1.68% and 1.55% respectively.

-

15:35

Gold reversal on the US session

Gold edged lower on Friday as markets treaded water ahead of the inauguration of Donald Trump, whose plans for the U.S. economy have sapped demand for the metal since his election, says Dow Jones.

Gold was down 0.2% at $1,201.18 a troy ounce in midmorning trade in London, on course for a 0.1% gain for the week and 4.1% increase for the year so far.

The precious metal has also been hit recently by a strengthening dollar, a pattern which continued Friday. The WSJ Dollar Index was up 0.3% at 92.07.

Gold has fallen 6% since Mr. Trump's election as expectations of tax cuts, inflation and rising interest rates pulled money into riskier assets and sent the dollar soaring. Higher rates weigh on gold as it doesn't yield a return.

-

14:59

WSE: After start on Wall Street

The beginning of trading on Wall Street took place under the sign of a solid as for the last days gains. The Americans live today by sworn of 45 President of the United States and all the news are filled with information about the event. The Warsaw Stock Exchange still can not build a counterweight to nearly 5 percent drop in PKN and has had four hours of consolidation in the area of the daily minima.

An hour before the close of trading the WIG20 index was at the level of 2,010 points (-0.25%).

-

14:53

Fed's Harker: U.S. Likely to Achieve Fed 2% Inflation Target This Year or Next

-

Inflation Expectations Rallying to 2%

-

Concerned by Low Labor Force Participation Levels

-

Labor Market 'Strong,' Essentially at 'Full Health'

-

Rate Outlook Depends on Economy's Performance

-

Fed Likely to Raise Rates Three Times in 2017

-

-

14:35

U.S. Stocks open: Dow +0.36%, Nasdaq +0.44%, S&P +0.42%

-

14:28

Before the bell: S&P futures +0.24%, NASDAQ futures +0.26%

U.S. stock-index futures rose with investors counting down to Donald Trump's inauguration as the 45th president of the United States. Focus also is on quarterly earnings reports.

Global Stocks:

Nikkei 19,137.91 +65.66 +0.34%

Hang Seng 22,885.91 -164.05 -0.71%

Shanghai 3,122.83 +21.53 +0.69%

FTSE 7,207.14 -1.30 -0.02%

CAC 4,852.10 +10.96 +0.23%

DAX 11,608.04 +11.15 +0.10%

Crude $53.02 (+1.73%)

Gold $1,203.50 (+0.17%)

-

14:05

Upgrades and downgrades before the market open

Upgrades:

Intl Paper (IP) upgraded to Buy from Hold at Jefferies

Visa (V) upgraded to Outperform at Wedbush; target raised to $96

Downgrades:

Other:

Apple (AAPL) target raised to $148 from $133 at Macquarie; maintain Outperform

Twitter (TWTR) resumed with a Sector Weight at Pacific Crest

Alphabet A (GOOGL) resumed with a Overweight at Pacific Crest

Facebook (FB) resumed with a Overweight at Pacific Crest

Wal-Mart (WMT) resumed with a Hold at Stifel; target $70

Amazon (AMZN) initiated with a Buy at Aegis Capital; target $953

-

13:56

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

35.6

0.18(0.5082%)

222

Amazon.com Inc., NASDAQ

AMZN

812.51

3.47(0.4289%)

10733

AMERICAN INTERNATIONAL GROUP

AIG

65.1

-1.19(-1.7951%)

23247

Boeing Co

BA

159.9

0.90(0.566%)

126

Caterpillar Inc

CAT

93.59

0.21(0.2249%)

3306

Cisco Systems Inc

CSCO

30.13

0.15(0.5003%)

1881

Citigroup Inc., NYSE

C

56.99

0.33(0.5824%)

17546

Exxon Mobil Corp

XOM

85.05

0.32(0.3777%)

8251

Facebook, Inc.

FB

127.8

0.25(0.196%)

57764

Ford Motor Co.

F

12.45

0.02(0.1609%)

15531

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

232.2

0.79(0.3414%)

14211

General Motors Company, NYSE

GM

232.2

0.79(0.3414%)

14211

Goldman Sachs

GS

232.2

0.79(0.3414%)

14211

Google Inc.

GOOG

804.89

2.715(0.3385%)

2556

Intel Corp

INTC

36.75

0.18(0.4922%)

363

International Paper Company

IP

53.13

0.45(0.8542%)

118

JPMorgan Chase and Co

JPM

83.64

0.34(0.4082%)

23452

Merck & Co Inc

MRK

62.35

2.02(3.3482%)

290071

Nike

NKE

53.27

0.34(0.6424%)

1344

Pfizer Inc

PFE

31.79

0.09(0.2839%)

13625

Twitter, Inc., NYSE

TWTR

16.85

0.06(0.3574%)

14461

Verizon Communications Inc

VZ

52.1

-0.26(-0.4966%)

346

Visa

V

82.39

0.66(0.8075%)

1975

Wal-Mart Stores Inc

WMT

67.78

0.16(0.2366%)

1300

Walt Disney Co

DIS

107.29

0.01(0.0093%)

1518

Yandex N.V., NASDAQ

YNDX

22.04

0.01(0.0454%)

2004

-

13:49

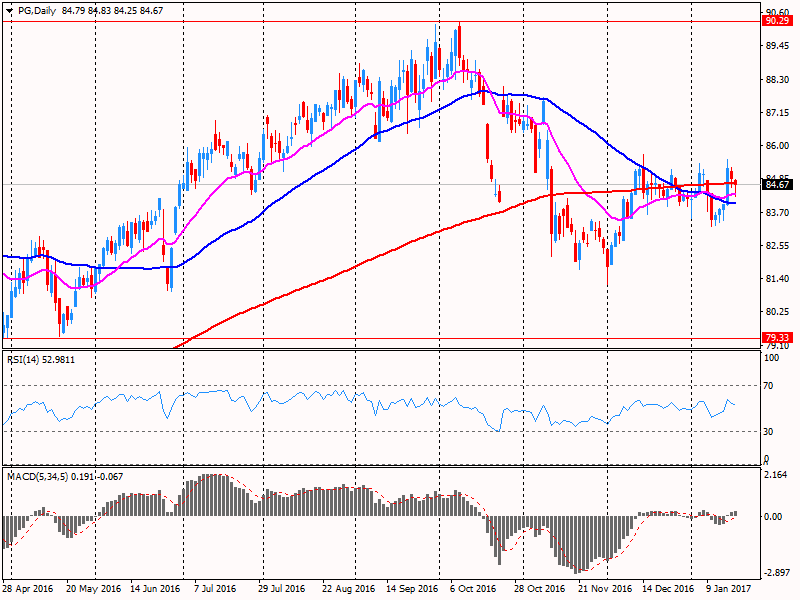

Company News: Procter & Gamble (PG) posts strong Q4 results

Procter & Gamble reported Q4 FY 2016 earnings of $1.08 per share (versus $1.04 in Q4 FY 2015), beating analysts' consensus estimate of $1.06.

The company's quarterly revenues amounted to $16.856 bln (-0.3% y/y), generally in-line with analysts' consensus estimate of $16.774 bln.

PG rose to $87.00 (+2.72%) in pre-market trading.

-

13:49

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0550 (EUR 1bln) 1.0640-55 (1.1bln) 1.0700 (751m)

USD/JPY 113.35 (USD 300m) 114.00 (893m) 114.10-15 (436m)

GBP/USD 1.2000 (GBP 410m)

EUR/GBP 0.8700 (EUR 300m)

EUR/JPY 120.95-121.00 (EUR 535m)

AUD/NZD 1.0500 (AUD 1bln)

-

13:40

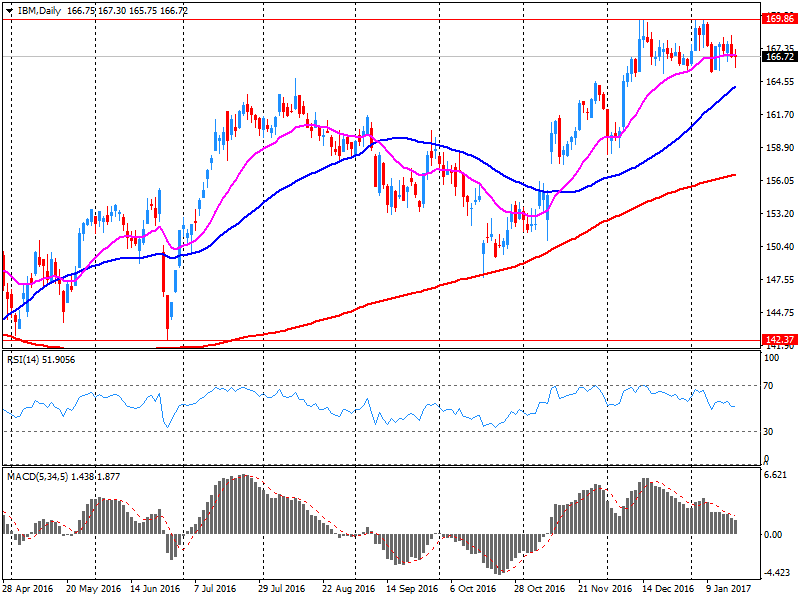

Company News: IBM (IBM) Q4 results beat analysts’ expectations

IBM reported Q4 FY 2016 earnings of $5.01 per share (versus $4.84 in Q4 FY 2015), beating analysts' consensus estimate of $4.88.

The company's quarterly revenues amounted to $21.770 bln (-1.3% y/y), beating analysts' consensus estimate of $21.632 bln.

The company also issued upside guidance for FY 2017, projecting EPS of at least $13.80 versus analysts' consensus estimate of $13.74.

IBM fell to $165.25 (-0.94%) in pre-market trading.

-

13:38

Canadian retail sales rose for the fourth consecutive month

Retail sales rose for the fourth consecutive month, edging up 0.2% to $45.2 billion in November. Higher sales at motor vehicle and parts dealers and building material and garden equipment and supplies dealers were the main contributors to the gain.

Sales were up in 5 of 11 subsectors, representing 45% of total retail trade.

After removing the effects of price changes, retail sales in volume terms increased

Sales were up for the third consecutive month at motor vehicle and parts dealers (+0.8%) in November. Higher sales at new car dealers (+1.9%) accounted for most of the gain at the subsector level. Sales at other motor vehicles dealers, which include retailers of recreational vehicles, motorcycles and boats, were up 1.8%. Lower sales were reported at automotive parts, accessories and tire stores (-11.0%) and used car dealers (-3.5%).0.7%.

-

13:35

Canadian CPI inflation declined 0.2% in December

The Consumer Price Index (CPI) rose 1.5% on a year-over-year basis in December, following a 1.2% gain in November.

Prices were up in seven of the eight major components in the 12 months to December, with the transportation and shelter indexes contributing the most to the year-over-year rise in the CPI. The food index declined on a year-over-year basis for the third consecutive month.

The transportation index rose on a year-over-year basis for the fifth consecutive month, up 3.0% in December, after a 1.4% gain in November. This increase was led by gasoline prices, which increased 5.5% in the 12 months to December, following a 1.7% decline in November. At the same time, the purchase of passenger vehicles index rose less year over year in December (+2.6%) than in November (+3.0%), and the air transportation index registered its largest year-over-year gain since August 2013.

-

13:30

Canada: Retail Sales, m/m, November 0.2% (forecast 0.5%)

-

13:30

Canada: Consumer price index, y/y, December 1.5% (forecast 1.7%)

-

13:30

Canada: Bank of Canada Consumer Price Index Core, y/y, December 1.6% (forecast 1.7%)

-

13:30

Canada: Consumer Price Index m / m, December -0.2% (forecast -0.1%)

-

13:30

Canada: Retail Sales ex Autos, m/m, November 0.1% (forecast 0.1%)

-

13:30

Canada: Retail Sales YoY, November 3%

-

13:29

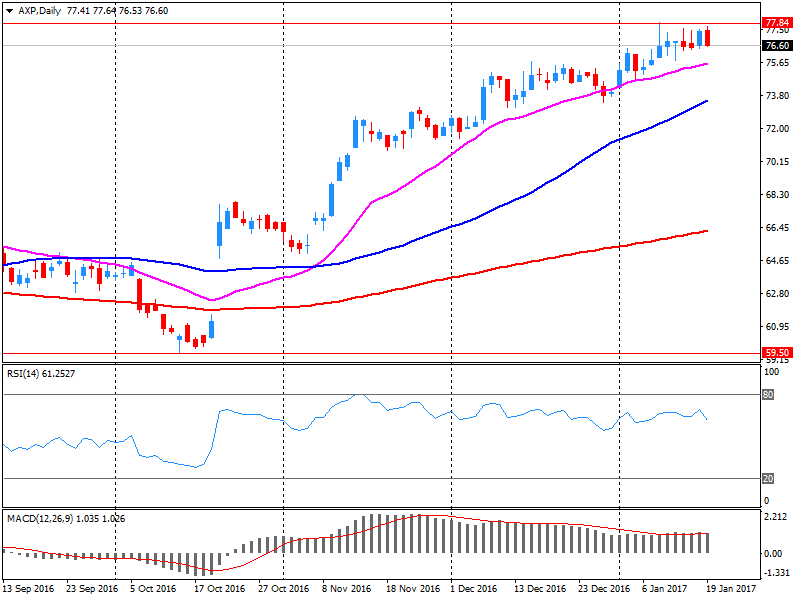

Company News: American Express (AXP) Q4 EPS miss analysts’ estimate

American Express reported Q4 FY 2016 earnings of $0.91 per share (versus $1.23 in Q4 FY 2015), missing analysts' consensus estimate of $0.99.

The company's quarterly revenues amounted to $8.022 bln (-4.4% y/y), generally in-line with analysts' consensus estimate of $7.986 bln.

AXP fell to $75.10 (-2.07%) in pre-market trading.

-

13:22

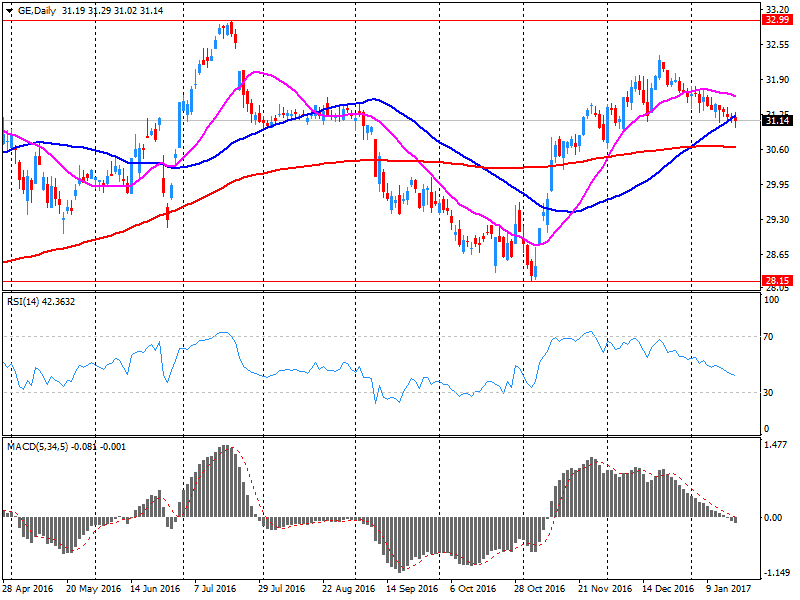

Company News: General Electric (GE) posts mixed quarterly results

General Electric reported Q4 FY 2016 earnings of $0.46 per share (versus $0.52 in Q4 FY 2015), in-line with analysts' consensus estimate of $0.46.

The company's quarterly revenues amounted to $33.088 bln (-2.4% y/y), missing analysts' consensus estimate of $33.669 bln.

GE fell to $30.73 (-1.54%) in pre-market trading.

-

13:01

Orders

EUR/USD

Offers: 1.0685 1.0700 1.0720-25 1.0750 1.0785 1.0800

Bids: 1.0650 1.0625-30 1.0600 1.05801.0565 1.0550 1.0520 1.0500

GBP/USD

Offers: 1.2380 1.2400 1.2420 1.2450 1.2475-80 1.2500 1.2520 1.2550

Bids: 1.2320-25 1.2300 1.2280 1.2250 1.2230 1.2200 1.2185 1.2150 1.2100

EUR/GBP

Offers: 0.8660 0.8680 0.8700 0.8730 0.8750 0.8780 0.8800

Bids: 0.8625-30 0.8600 0.8585 0.8550 0.8530 0.8500

EUR/JPY

Offers: 122.80 123.00 123.50 124.00 124.50 124.80 125.00

Bids: 122.30 122.00 121.80 121.50 121.00 120.80 120.50 120.00

USD/JPY

Offers: 115.00 115.20 115.35 115.55-60 115.80 116.00 116.30 116.50 116.80 117.00

Bids: 114.50 114.20 114.00 113.85 113.55-60 113.20 113.00 112.80 112.65 112.50

AUD/USD

Offers: 0.7565 0.7585 0.7600 0.7630 0.7650 0.7675 0.7700

Bids: 0.7525-30 0.7500 0.7480-850.7450 0.7430 0.7400

Информационно-аналитический отдел TeleTrade

-

12:04

Hungary's central bank is widely expected to leave interest rates unchanged next week at a record low, despite a pickup in inflation, to help boost growth ahead of the spring 2018 parliamentary elections - Dow Jones

-

12:02

WSE: Mid session comment

The first half of today's session is the search for growth and the correlation with the environment, where the German DAX recorded slight increases. And that has happened to publication of the information given by the Ministry of Energy that in the shareholding of PKN Orlen (WSE: PKN) appeared PERN Company, with the participation of 4.9 percent in the PKN shares. PERN SA is the sole shareholder of the Treasury, thereby PKN Orlen has become less private. Investors reacted to that info by sell-off of PKN shares which affected the quotations of the WIG20 index.

At the halfway point of the session WIG20 index was at the level of 2,008 points (-0.33%).

-

10:44

A weekly close above 0.7330 on NZD/USD would imply a retest of the 2016 highs says NAB

"Price is in the process of completing its fourth consecutive up week. This aggressive bounce has negated the downtrend that began in September 2016 at 0.7486 (downtrend break confirmed by the recent close above 0.7095 - 61.8% retrace). This downtrend was material in magnitude but fell some 150-200 points short of our aggressive downside target at 0.6650/0.6700.

The upswing to date is yet to retest the broken uptrend channel at 0.7310/30. This is a likely interim target and level that must be broken if a more sustainable uptrend is to be maintained.

At this time we are comfortable targeting 0.7310/30 but prefer to take a wait and see approach to further gains depending upon the price response to this key resistance levels.

A weekly close above 0.7330 would imply a retest of the 2016 highs at 0.7403/0.7486".

Copyright © 2017 NAB, eFXnews™

-

10:24

ECB forecasts

Inflation expectations have been revised upwards for 2017 and 2018, largely because of higher oil prices. Longer-term inflation expectations remain unchanged at 1.8%.

Real GDP growth expectations have been revised upwards for 2017, but are unchanged for years further ahead further out.

Unemployment rate expectations have been revised downwards.

-

09:34

UK retail sales declined more than expected in December

Estimates of the quantity bought in retail sales increased by 4.3% compared with December 2015 and fell by 1.9% compared with November 2016.

The largest contribution to the month-on-month fall came from non-food stores.

The underlying trend remains one of growth with the 3 month on 3 month movement in the quantity bought increasing by 1.2%.

Average store prices increased by 0.9% on the year and for all retailing excluding fuel prices increased by 0.1%; the first increase since June 2014.

Online sales (excluding automotive fuel) increased year-on-year by 21.3%, but fell on the month by 5.3%; accounting for approximately 15% of all retail spending.

-

09:30

United Kingdom: Retail Sales (MoM), December -1.9% (forecast -0.1%)

-

09:30

United Kingdom: Retail Sales (YoY) , December 4.3% (forecast 7.2%)

-

09:20

UK Chancellor Hammond: UK Economy Effectively At Full Employment, Will Continue To Need Migrants - Livesquawk

-

09:19

Major stock markets in Europe trading mixed: FTSE flat, DAX -0.2%, CAC40-0.2%, FTMIB + 0.3%, IBEX-0.1%

-

08:17

WSE: After opening

WIG20 index opened at 2015.31 points (-0.01%)*

WIG 53591.25 -0.12%

WIG30 2330.58 -0.17%

mWIG40 4420.82 -0.11%

*/ - change to previous close

At the beginning of trading on the Warsaw spot market (WIG20), we may see a slight withdrawal which is the result of yesterday's draw up at the final fixing. The German DAX began the session slightly worse than expected and losing 0.3 percent, which also does not help for the demand side in Warsaw. The level of turnover is not high and confirms the consolidation nature of this morning.

After fifteen minutes of trading the WIG20 index was at the level of 2,014 points (-0,07%).

-

07:44

Mixed start of trading expected on the major stock exchanges in Europe: DAX -0.1%, CAC40 -0.1%, FTSE + 0.1%

-

07:43

ECB's Coeure: Risk That Euro Group Ministers Won’t Act Together To Address Any Problem In Eurozone - CNBC

-

07:33

Japan's Minister of Economy, Nobuteru Ishihara convinced that the Bank of Japan will touch 2% inflation target

During his speech today the minister of the Japanese economy, Nobuteru Ishihara stressed his confidence once again that the Bank of Japan will achieve 2% inflation. "The Ministry of Economy believes that the Central Bank will be able to accelerate inflation to the target level of 2%, while taking into account economic trends. Now the country's GDP recovered moderately together with the labor market and wage growth. Nevertheless, it is necessary to closely monitor the financial markets and the uncertainty in the external economy "- said Nobuteru Ishihara.

-

07:21

WSE: Before opening

Thursday's session on the New York stock markets ended with slight declines in the major indexes. The Dow Jones Industrial dropped at the closing of about 0.34 percent, the S&P500 went down by 0.36 percent and the Nasdaq Comp. lost 0.28 percent. Markets are waiting for Friday's speech by Donald Trump after being sworn as President of the United States.

In the macro calendar there is not particularly important data today, except quarterly results published by the company General Electric. So the whole attention of investors should be focused on events in the US and Wall Street reaction to the swearing-in of the new president.

On the WSE the situation seems to be clear. The WIG20 index consolidates above the level of 2,000 pts., but supply more boldly pushing for support in the area of 2,000 points and the line of upward trend.

-

07:19

Options levels on friday, January 20, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0778 (2450)

$1.0745 (2225)

$1.0723 (442)

Price at time of writing this review: $1.0686

Support levels (open interest**, contracts):

$1.0633 (2045)

$1.0603 (1380)

$1.0560 (1407)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 55224 contracts, with the maximum number of contracts with strike price $1,0750 (3475);

- Overall open interest on the PUT options with the expiration date March, 13 is 66105 contracts, with the maximum number of contracts with strike price $1,0000 (4926);

- The ratio of PUT/CALL was 1.20 versus 1.21 from the previous trading day according to data from January, 19

GBP/USD

Resistance levels (open interest**, contracts)

$1.2608 (1392)

$1.2511 (1349)

$1.2415 (464)

Price at time of writing this review: $1.2363

Support levels (open interest**, contracts):

$1.2284 (744)

$1.2188 (1033)

$1.2091 (541)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 18014 contracts, with the maximum number of contracts with strike price $1,2800 (1466);

- Overall open interest on the PUT options with the expiration date March, 13 is 21944 contracts, with the maximum number of contracts with strike price $1,1500 (3222);

- The ratio of PUT/CALL was 1.22 versus 1.23 from the previous trading day according to data from January, 19

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:09

China's economy expanded at a faster pace in the fourth quarter

China's economy expanded at a faster pace in the fourth quarter on spending, while the full-year growth hit the weakest in 26 years, data from the National Bureau of Statistics revealed Friday, cited by rttnews.

Gross domestic product grew 6.8 percent in the fourth quarter, while economists expected the rate to stabilize again at 6.7 percent.

In 2016 as a whole, the economy expanded 6.7 percent, which was within the government's target of 6.5 to 7 percent. However, this was the weakest growth in 26 years.

-

07:08

Chinese industrial production in line with expectations in December

Today's report on industrial production from China, published by the National Bureau of Statistics showed that industrial production, in December, year on year increased by 6.0%. However, the figure was a little lower than the previous value of 6.2% and economists' forecast of 6.1%.

This report shows the volume produced by the Chinese industrial enterprises, such as factories and production facilities. The decline in production volumes could have a negative impact on inflation, which may force the People's Bank of China to take measures aimed at easing monetary and fiscal policies.

-

07:03

German producer prices fell in December

In 2016 the index of producer prices for industrial products (domestic sales) for Germany fell by 1.7% on an annual average from the preceding year, as reported by the Federal Statistical Office (Destatis). A year before the index had fallen by 1.8%.

In December 2016 the index of producer prices for industrial products rose by 1.0% compared with the corresponding month of the preceding year. This was the highest positive annual rate of change since January 2013 (+1.5%). In November 2016 the annual rate of change all over had been +0.1%.

Compared with the preceding month November 2016 the overall index rose by 0.4% in December 2016 (0.3% in November and 0.7% in October).

-

07:02

Germany: Producer Price Index (MoM), December 0.4% (forecast 0.4%)

-

07:02

Germany: Producer Price Index (YoY), December 1.0% (forecast 1%)

-

06:31

Global Stocks

Europe's main stock gauge closed slightly lower, after gains sparked by European Central Bank President Mario Draghi's remarks failed to stick. The ECB chief struck a markedly dovish tone, emphasizing downside risks to the inflation outlook and reiterating that the bank's bond buying program can be extended or expanded, if needed.

The Dow Jones Industrial Average on Thursday suffered its worst losing streak since November as investors remained cautious a day ahead of Donald Trump's presidential inauguration.

Chinese stocks gained on stronger-than-expected economic growth to end 2016, but overall, Asian shares were again logging generally modest declines amid continued investor caution ahead of U.S. President-elect Donald Trump's inauguration. The world's No. 2 economy grew 6.8% last quarter from a year earlier after three straight increases of 6.7% - which economists polled by The Wall Street Journal expected to be repeated again. The full year's 6.7% growth was the least for China since 1990.

-

02:01

China: Fixed Asset Investment, December 8.1% (forecast 8.3%)

-

02:00

China: GDP y/y, Quarter IV 6.8% (forecast 6.7%)

-

02:00

China: Industrial Production y/y, December 6.0% (forecast 6.1%)

-

02:00

China: Retail Sales y/y, December 10.9% (forecast 10.7%)

-

00:00

Australia: HIA New Home Sales, m/m, November 6.1%

-