Market news

-

23:29

Stocks. Daily history for Mar 13’2017:

(index / closing price / change items /% change)

Nikkei +29.14 19633.75 +0.15%

TOPIX +3.39 1577.40 +0.22%

Hang Seng +261.00 23829.67 +1.11%

CSI 300 +30.21 3458.10 +0.88%

Euro Stoxx 50 -0.78 3415.49 -0.02%

FTSE 100 +24.00 7367.08 +0.33%

DAX +26.85 11990.03 +0.22%

CAC 40 +6.28 4999.60 +0.13%

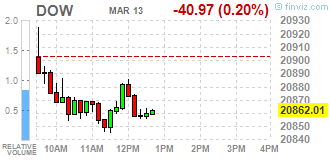

DJIA -21.50 20881.48 -0.10%

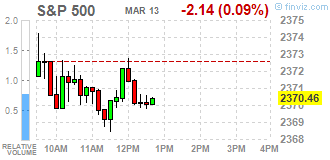

S&P 500 +0.87 2373.47 +0.04%

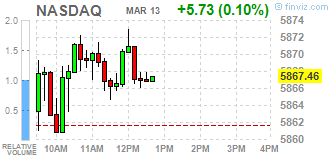

NASDAQ +14.06 5875.79 +0.24%

S&P/TSX +38.14 15544.82 +0.25%

-

20:08

The main US stock indexes finished trading mostly in positive territory

Major US stock indexes mostly rose on Monday, as the rise in the price of financial sector shares before the expected increase in interest rates the Federal Reserve compensated for the loss of shares in the health sector.

It is expected that the Federal Open Market Committee, which is the central bank's policy council, will raise interest rates by 0.25 percent, to 0.75-1.00 percent after a two-day meeting that will begin on Tuesday.

In addition, according to the report presented by the Conference Board, the US employment trends index, which is a combination of labor market indicators, improved significantly in February, continuing the trend of the previous month. According to the data, the February index of employment trends increased to 131.39 points compared to 129.91 points in January (revised from 130.04 points). In annual terms, the index increased by 3.1 percent.

Quotes of oil fluctuated within 3-month lows, as the growth of oil reserves in the US and further strengthening of drilling activity in the United States compensates optimism about OPEC's efforts to limit oil production and reduce global overabundance.

Components of the DOW index finished trading mixed (15 in positive territory, 15 in negative territory). The shares of Intel Corporation fell more than others (INTC, -2.30%). The leader of growth was the shares of The Walt Disney Company (DIS, + 0.57%).

Almost all sectors of the S & P index recorded an increase. The leader of growth was the sector of basic materials (+ 0.5%). The outsider was the health sector (0.0%).

At closing:

Dow -0.10% 20.881.48 -21.50

Nasdaq + 0.24% 5,875.78 +14.05

S & P + 0.04% 2.373.47 + 0.87

-

19:00

DJIA -0.12% 20,878.39 -24.59 Nasdaq +0.21% 5,873.87 +12.14 S&P -0.02% 2,372.11 -0.49

-

17:00

European stocks closed: FTSE 100 +24.00 7367.08 +0.33% DAX +26.85 11990.03 +0.22% CAC 40 +6.28 4999.60 +0.13%

-

16:44

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Monday as gains in financials shares - ahead of a widely expected interest rate hike - were weighed down by losses in drug stocks. The Federal Open Market Committee, the central bank's policy-setting board, is expected to lift interest rates by a 0.25 to 0.75 percent-1.00 percent after a two-day meeting that starts on Tuesday.

Most of Dow stocks in negative area (20 of 30). Top loser - Intel Corporation (INTC, -2.27%). Top gainer - Caterpillar Inc. (CAT, +0.37%).

Almost all of S&P sectors in positive area. Top loser - Healthcare (-0.2%). Top gainer - Basic Materials (+0.4%).

At the moment:

Dow 20824.00 -24.00 -0.12%

S&P 500 2367.75 -0.75 -0.03%

Nasdaq 100 5390.50 +4.25 +0.08%

Oil 48.39 -0.10 -0.21%

Gold 1205.80 +4.40 +0.37%

U.S. 10yr 2.61 +0.02

-

06:30

Global Stocks

European stocks pared gains in afternoon trade on Friday, closing only slightly higher after a report the European Central Bank has discussed whether it could raise interest rates before ending its program of monthly asset purchases. "Stock markets spent most of Friday in positive territory with investors still unwilling to bet against higher prices despite strong odds of a rate increase in the U.S. next week. Data showing solid U.S. job growth makes a rate hike at next week's meeting of the Federal Reserve a near certainty," said Jasper Lawler, senior market analyst, at London Capital Group, in a note.

U.S. stocks closed higher Friday on a stronger-than-expected February jobs report, but major benchmarks snapped multiweek winning streaks as oil prices weighed on markets over the past five sessions. The U.S. economy added 235,000 jobs in February, while the January number was revised to show payrolls rose 238,000, pushing the unemployment rate to 4.7%. Hourly pay increased 2.8% from February 2016 to February 2017, up from 2.6% in the prior month.

Global stocks lacked direction at the beginning of the week, with some markets in Asia ignoring a positive lead from the U.S. as local drivers took precedence. Trading was subdued at the start of what stands to be an action-packed week, with the Federal Reserve and the Bank of Japan set to make interest rate decisions. According to CME Group data, there is an 88.6% probability of the Fed raising rates.

-