Market news

-

23:28

Stocks. Daily history for Jan 18’2017:

(index / closing price / change items /% change)

Nikkei +80.84 18894.37 +0.43%

TOPIX +4.76 1513.86 +0.32%

Hang Seng +257.29 23098.26 +1.13%

CSI 300 +13.01 3339.37 +0.39%

Euro Stoxx 50 +8.96 3294.00 +0.27%

FTSE 100 +27.23 7247.61 +0.38%

DAX +59.39 11599.39 +0.51%

CAC 40 -6.29 4853.40 -0.13%

DJIA -22.05 19804.72 -0.11%

S&P 500 +4.00 2271.89 +0.18%

NASDAQ +16.93 5555.66 +0.31%

S&P/TSX -43.51 15397.85 -0.28%

-

21:07

Major US stock indexes finished trading in different directions

Major US stock indexes closed mostly in positive territory, as the growth of technology companies companies fall leveled retailers. At the same time the Dow fell below zero under the pressure of the basic materials sector shares.

Investors assessed makrostatisticheskie publishing quarterly reports and a number of US companies, as well as preparing for the speech of Fed Chairman Janet Yellen.

As it became known, the consumer prices in the US rose in December as households increased spending on gasoline and rental housing, which led, a sign that inflationary pressures may be growing to the largest growth at an annual rate of 2.5 per year. According to the report, the consumer price index rose 0.3% last month, after rising 0.2% in November. In the 12 months to October, the consumer price index increased by 2.1% - the largest increase year on year in June, 2014. The consumer price index rose by 1.7% in the year to November. The increase was in line with economists' expectations.

The volume of industrial production rose in December for the biggest jump of utilities since 1989, as the temperature dropped throughout the country. The Fed reported that industrial production increased by 0.8% after a downwardly revised decline of 0.7% in November. Economists had forecast an increase of 0.6%.

sentiment index from the National Association of Home Builders fell by 2 points to 67 in January. Even with the reduction, the December reading was still the highest point of the index with the peak of the housing boom time in 2005, and in January was the second largest. Economists had forecast a reading of 69 in January.

However, the Fed's Beige Book showed that the economy continued to grow at a moderate pace in most regions at the end of 2016 and beginning of this year. In addition, the company is optimistic with regards to future growth in 2017. "In many regions they noted that they expect the continuation of labor market recovery in 2017, while the pressure on wages is likely to grow, and job growth will remain at the same level or accelerate", - the report says.

As for the performances Yellen, she said that the US economy is close to maximum employment, and inflation "is moving toward the goal." "The December rate hike reflects confidence that the economic situation will continue to improve. The scale of the next rate increase depends on how the economy will develop. But too long a delay in raising rates is fraught with "unpleasant surprises" in the form of high inflation, instability. Now Fed officials expect rate hikes, "a few times a year" until 2019 "- said Yellen. - Perhaps there is still potential for progress in the labor market. Wage growth is still quite low, and only began to accelerate in recent years. Broader indicators of unemployment is still above doretsessionnyh levels. "

DOW index components closed mostly in the red (16 of 30). Most remaining shares fell UnitedHealth Group, Inc. (UNH, -2.00%). The leader of growth were the shares of American Express Company (AXP, + 1.16%).

Sector S & P index finished the session mixed. Most of the basic materials sector fell (-0.4%). The leader turned out to be the industrial goods sector (+ 0.4%).

At the close:

Dow -0.11% 19,804.68 -22.09

Nasdaq + 0.31% 5,555.66 +16.93

S & P + 0.17% 2,271.85 +3.96

-

20:00

DJIA -0.17% 19,793.08 -33.69 Nasdaq +0.05% 5,541.60 +2.87 S&P +0.04% 2,268.73 +0.84

-

18:45

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes were flat in choppy trading on Wednesday as gains in tech stocks offset a weakness in retail sector, while the Dow was dragged down by healthcare shares. Investors assessed a raft of corporate earnings and economic data, while awaiting Federal Reserve Chair Janet Yellen's speech (at 20:00 GMT).

Almost all of Dow stocks in negative area (20 of 30). Top loser - UnitedHealth Group, Inc. (UNH, -2.58%). Top gainer - 3M Company (MMM, +1.04%).

A majority of S&P sectors in negative area. Top loser - Services (-0.3%). Top gainer - Industrial Goods (+0.4%).

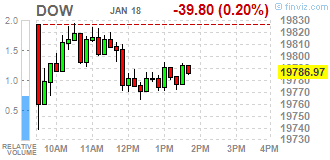

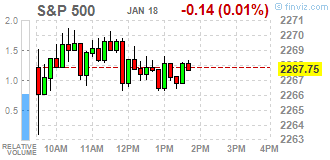

At the moment:

Dow 19786.97 -39.80 -0.20%

S&P 500 2,267.75 -0.14 -0.01%

Nasdaq 100 5,541.17 +2.45 +0.04%

Oil 51.32 -1.16 -2.21%

Gold 1211.50 -1.40 -0.12%

U.S. 10yr 2.39 +0.06

-

17:00

European stocks closed: FTSE 100 +27.23 7247.61 +0.38% DAX +59.39 11599.39 +0.51% CAC 40 -6.29 4853.40 -0.13%

-

16:39

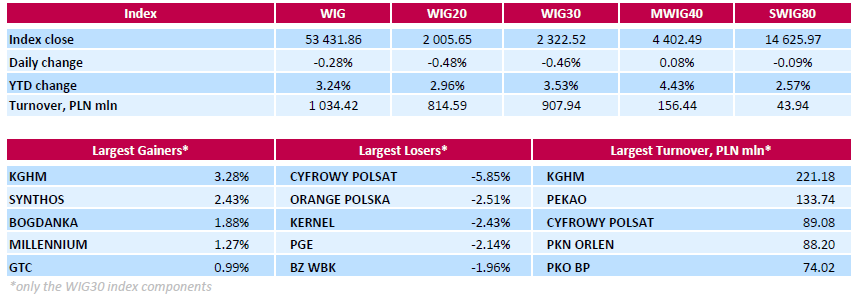

WSE: Session Results

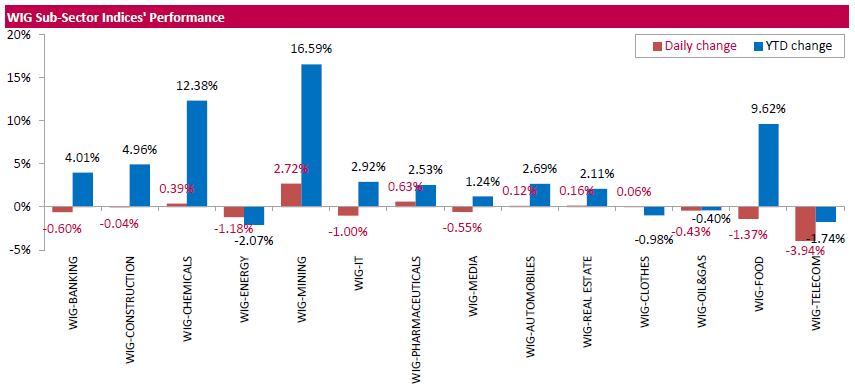

Polish equity market closed lower on Wednesday. The broad market measure, the WIG Index, fell by 0.28%. Sector performance within the WIG Index was mixed. Telecoms (-3.94%) underperformed, while mining (+2.72%) outpaced.

The large-cap stocks' measure, the WIG30 Index, dropped by 0.46%. Within the index components, media group CYFROWY POLSAT (WSE: CPS) was the session's biggest loser, tumbling by 5.85% on news the European Bank for Reconstruction and Development (EBRD) sold a 2.48 percent stake in the company at a small discount to Tuesday's closing price of PLN 25.65. Other largest decliners were telecommunication services provider ORANGE POLSKA (WSE: OPL), agricultural producer KERNEL (WSE: KER) and genco PGE (WSE: PGE), declining by 2.51%, 2.43% and 2.14% respectively. At the same time, property developer GTC (WSE: GTC) led a handful of gainers with a 0.99% advance, followed by clothing retailer LPP (WSE: LPP) and bank PKO BP (WSE: PKO), adding 0.36% and 0.2% respectively.

-

14:33

U.S. Stocks open: Dow -0.10%, Nasdaq +0.12%, S&P +0.04%

-

14:27

Before the bell: S&P futures +0.20%, NASDAQ futures +0.23%

U.S. stock-index futures rose as investors assessed a raft of corporate earnings and economic data, while awaiting Federal Reserve Chair Janet Yellen's speech (at 20:00 GMT).

Global Stocks:

Nikkei 18,894.37 +80.84 +0.43%

Hang Seng 23,098.26 +257.29 +1.13%

Shanghai 3,113.05 +4.28 +0.14%

FTSE 7,244.42 +24.04 +0.33%

CAC 4,842.80 -16.89 -0.35%

DAX 11,565.70 +25.70 +0.22%

Crude $51.70 (-1.49%)

Gold $1,211.90 (-0.08%)

-

13:56

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALTRIA GROUP INC.

MO

68.6

0.12(0.1752%)

470

Amazon.com Inc., NASDAQ

AMZN

806.81

-2.91(-0.3594%)

19447

American Express Co

AXP

76.95

0.35(0.4569%)

1775

AMERICAN INTERNATIONAL GROUP

AIG

66.09

0.03(0.0454%)

100

Apple Inc.

AAPL

120.11

0.11(0.0917%)

64607

Barrick Gold Corporation, NYSE

ABX

17.2

-0.04(-0.232%)

53504

Caterpillar Inc

CAT

92.96

0.16(0.1724%)

1800

Chevron Corp

CVX

116.24

-0.04(-0.0344%)

1153

Cisco Systems Inc

CSCO

30.03

0.04(0.1334%)

60942

Citigroup Inc., NYSE

C

58.19

-0.19(-0.3255%)

444282

Deere & Company, NYSE

DE

104.87

0.53(0.508%)

1112

Exxon Mobil Corp

XOM

87.13

-0.23(-0.2633%)

3457

Facebook, Inc.

FB

128.2

0.33(0.2581%)

79572

Ford Motor Co.

F

12.51

0.10(0.8058%)

82554

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

14.93

-0.13(-0.8632%)

13240

General Electric Co

GE

31.3

0.03(0.0959%)

3529

General Motors Company, NYSE

GM

37.45

0.14(0.3752%)

300

Goldman Sachs

GS

236.65

0.91(0.386%)

130621

Intel Corp

INTC

36.89

0.09(0.2446%)

3195

Johnson & Johnson

JNJ

115

0.13(0.1132%)

32767

JPMorgan Chase and Co

JPM

83.95

0.40(0.4788%)

50044

McDonald's Corp

MCD

122.56

-0.19(-0.1548%)

1652

Microsoft Corp

MSFT

62.65

0.12(0.1919%)

2667

Pfizer Inc

PFE

32.2

0.14(0.4367%)

74840

Procter & Gamble Co

PG

84.61

0.0695(0.0822%)

700

Starbucks Corporation, NASDAQ

SBUX

58.47

0.47(0.8103%)

12459

Tesla Motors, Inc., NASDAQ

TSLA

237

1.42(0.6028%)

4709

The Coca-Cola Co

KO

41.3

0.08(0.1941%)

348

Twitter, Inc., NYSE

TWTR

17.01

0.05(0.2948%)

10862

UnitedHealth Group Inc

UNH

161.48

0.82(0.5104%)

405

Wal-Mart Stores Inc

WMT

67.51

-0.91(-1.33%)

42493

Walt Disney Co

DIS

106.95

-1.02(-0.9447%)

14895

Yahoo! Inc., NASDAQ

YHOO

42.08

0.09(0.2143%)

125500

Yandex N.V., NASDAQ

YNDX

22

0.08(0.365%)

2300

-

13:47

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Walt Disney (DIS) downgraded to Underperform from Market Perform at BMO Capital

Other:

-

13:21

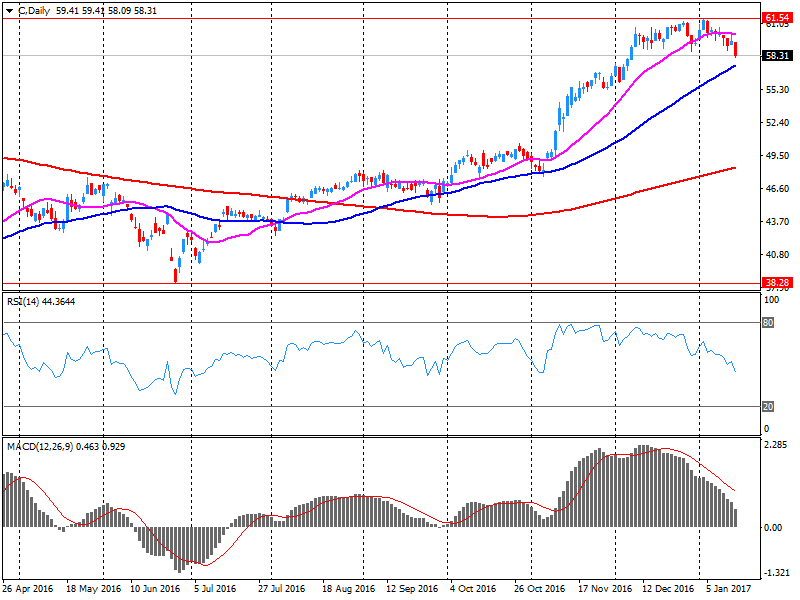

Company News: Citigroup (C) posts mixed quarterly results

Citigroup reported Q4 FY 2016 earnings of $1.14 per share (versus $1.06 in Q4 FY 2015), beating analysts' consensus estimate of $1.12.

The company's quarterly revenues amounted to $17.012 bln (-7.8% y/y), slightly missing analysts' consensus estimate of $17.260 bln.

C fell to $58.20 (-0.31%) in pre-market trading.

-

13:06

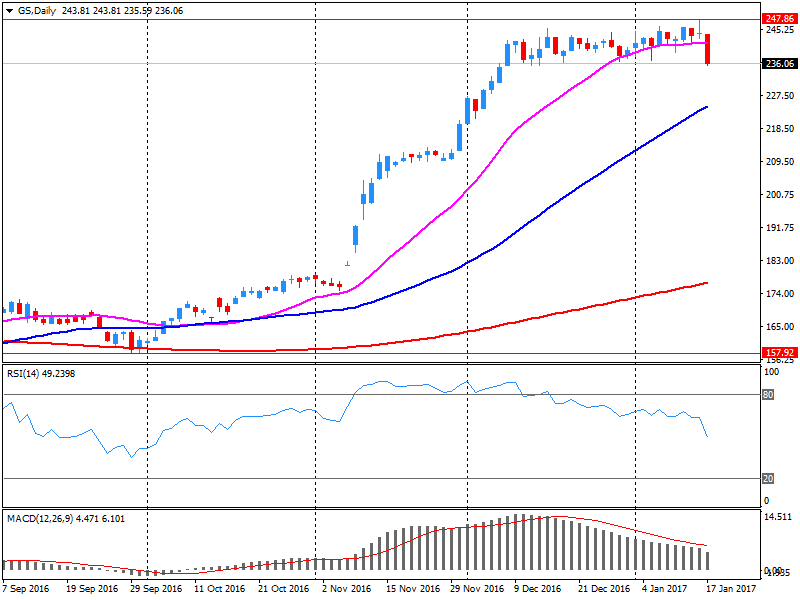

Company News: Goldman Sachs (GS) quarterly results beat expectations

Goldman Sachs reported Q4 FY 2016 earnings of $5.08 per share (versus $4.68 in Q4 FY 2015), beating analysts' consensus estimate of $4.80.

The company's quarterly revenues amounted to $8.170 bln (+12.3% y/y), beating analysts' consensus estimate of $7.803 bln.

GS rose to $237.25 (+0.64%) in pre-market trading.

-

12:04

WSE: Mid session comment

The morning phase of the session on the Warsaw Stock Exchange did not bring any spectacular decisions and volatility in case of the WIG20 index is practically imperceptible. The only good looks the level of turnover. The market apparently waiting for the solstice.

At the halfway point of the session WIG20 index was at 2015 points (0.00%), the turnover in the segment of the largest companies was amounted to PLN 412 million.

-

08:34

Major stock markets in Europe trading in the green zone: FTSE + 0.5%, DAX + 0.4%, CAC40 + 0.3%, FTMIB + 0.2%, IBEX + 0.4%

-

08:21

WSE: After opening

WIG20 index opened at 2018.57 points (+0.16%)

WIG 53737.19 0.29%

WIG30 2341.54 0.36%

mWIG40 4413.70 0.33%

*/ - change to previous close

The Warsaw market started trading from with a slight increase, although fast retraction in the first minutes tool all upward move. Nevertheless, the start may be considered as neutral. For several days the market is in consolidation and investors are waiting for a clear signal as to the further direction, which perhaps will flow from Wall Street.

After fifteen minutes of trading, the WIG index level of 2,012 points (-0.14%).

-

07:50

-

06:36

WSE: before opening

Tuesday's session on Wall Street ended with a slight discount and the S&P500 index at the end of the day lost 0.3 percent. The causes of this situation can be traced in the currency market, where the pound strengthened against the dollar and also the president-elect commented the strength of the US currency as harmful to the US economy.

In today's calendar will be important macro readings from the US (CPI and industrial production) and the quarterly earnings season, with reports of Goldman Sachs and Citigroup.

On the Warsaw market the WIG20 index is consolidating above the level of 2,000 points and despite yesterday's descent down is still stronger than the underlying market indexes. -

06:30

Global Stocks

European stocks pared losses Tuesday after U.K.'s Prime Minister Theresa May said Britain will break away from the European Union's single market and British lawmakers will be able to vote on Brexit's terms. May, in a highly anticipated speech in London, said Britain does "not seek membership of the single market but the greatest possible access to it," signaling a so-called hard Brexit from the other 27 members of the EU.

U.S. stocks retreated on Tuesday as investors remained cautious in the wake of President-elect Donald Trump's charge that a strong dollar is hurting the economy. "There is a lot going on this week, making investors slightly cautious. For example, the Davos meeting is where a confrontation between globalization and populism is on full display," said Jack Ablin, chief investment officer at BMO Private Bank, referring to the World Economic Forum's annual meeting in the Swiss Alps.

Asian markets were broadly lower Wednesday, following drops overnight in U.S. stocks on worries about the economic impact of the policies of President-elect Donald Trump, who will be inaugurated on Friday.

-