Noticias del mercado

-

23:58

Schedule for today, Thursday, Mar 17’2016:

(time / country / index / period / previous value / forecast)

00:30 Australia RBA Bulletin

00:30 Australia Changing the number of employed February -7.9 10

00:30 Australia Unemployment rate February 6.0% 6%

06:30 Japan BOJ Governor Haruhiko Kuroda Speaks

08:15 Switzerland Producer & Import Prices, m/m February -0.4% 0.2%

08:15 Switzerland Producer & Import Prices, y/y February -5.3% -5.1%

08:30 Switzerland SNB Interest Rate Decision -0.75% -0.75%

10:00 Eurozone Trade balance unadjusted January 24.3 9.0

10:00 Eurozone Harmonized CPI February -1.4% 0.1%

10:00 Eurozone Harmonized CPI, Y/Y (Finally) February 0.3% -0.2%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Finally) February 1% 0.7%

12:00 United Kingdom BoE Interest Rate Decision 0.5% 0.5%

12:00 United Kingdom Bank of England Minutes

12:00 United Kingdom Asset Purchase Facility 375 375

12:30 Canada Wholesale Sales, m/m January 2.0% 0.2%

12:30 U.S. Current account, bln Quarter IV -124.1 -118

12:30 U.S. Continuing Jobless Claims March 2225 2229

12:30 U.S. Philadelphia Fed Manufacturing Survey March -2.8 -1.5

12:30 U.S. Initial Jobless Claims March 259 266

14:00 U.S. Leading Indicators February -0.2% 0.2%

14:00 U.S. JOLTs Job Openings January 5.607 5.566

23:50 Japan Monetary Policy Meeting Minutes

-

22:45

New Zealand: GDP y/y, Quarter IV 2.3% (forecast 2%)

-

22:45

New Zealand: GDP q/q, Quarter IV 0.9% (forecast 0.6%)

-

21:09

US stocks closed

The Standard & Poor's 500 Index closed at its highest level this year as the Federal Reserve signaled a slower pace of interest-rate increases amid the potential impact from weaker global growth and financial-market turmoil.

Commodity shares led the advance as crude rallied with metals prices after the Fed decision sent the dollar tumbling against major peers. Oracle Corp. rose to a four-month high, boosting technology shares after its quarterly profits topped estimates. Banks slid on the outlook for a slower climb in rates.

The S&P 500 added 0.6 percent to 2,027.42 at 4 p.m. in New York, halting a two-day slide to close at its highest since Dec. 31.

The Federal Open Market Committee kept the target range for the benchmark federal funds rate at 0.25 percent to 0.5 percent. The median of policy makers' updated quarterly projections saw the rate at 0.875 percent at the end of 2016, implying two quarter-point increases this year, down from four forecast in December.

"The committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen," the FOMC said. "However, global economic and financial developments continue to pose risks."

It is the third major central-bank policy event since Thursday, following an unprecedented stimulus package unleashed by the European Central Bank, and after the Bank of Japan held off from adding more to its record stimulus as officials gauge the impact of a negative interest-rate strategy adopted in January.

-

20:00

DJIA 17343.47 91.94 0.53%, NASDAQ 4758.42 29.75 0.63%, S&P 500 2026.37 10.44 0.52%

-

19:00

U.S.: Fed Interest Rate Decision , 0.5% (forecast 0.5%)

-

18:49

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Wednesday afternoon, awaiting the outcome of the U.S. Federal Reserve's meeting on monetary policy. While interest rates are expected to remain unchanged, investors will parse the Fed's commentary for clues on the path of future hikes as the economy begins to show signs of recovery. Data on Wednesday showed underlying U.S. inflation rose more than expected in February, while the housing market continued to strengthen, bolstering the Fed's case that the economy was strong enough to withstand a gradual increase in rates.

Most of Dow stocks in negative area (19 of 30). Top looser - Pfizer Inc. (PFE, -1,83%). Top gainer - Caterpillar Inc. (CAT, +0,64%).

Most of S&P sectors in negative area. Top looser - Healthcare (-1,0%). Top gainer - Basic Materials (+1,5%).

At the moment:

Dow 17126.00 -22.00 -0.13%

S&P 500 2001.25 -5.25 -0.26%

Nasdaq 100 4353.75 -2.50 -0.06%

Oil 37.81 +1.47 +4.05%

Gold 1229.70 -1.30 -0.11%

U.S. 10yr 1.99 +0.03

-

18:00

European stocks close: stocks closed mixed ahead the Fed’s interest rate decision

Stock indices closed mixed ahead of the release of the Fed's interest rate decision later in the day. Analysts expect the Fed to keep its monetary policy unchanged.

A rise in oil prices supported stocks. Oil prices increased on news that OPEC and non-OPEC members will meet on April 17 in Doha to discuss the stabilisation of the oil market. The U.S. crude oil inventories data also supported oil prices.

Market participants eyed the Eurozone's economic data. The Eurostat released its construction production data for the Eurozone on Wednesday. Construction production in the Eurozone climbed 3.6% in January, after a 0.7% decline in December.

Civil engineering output rose 1.7% in January, while production in the building sector was up 4.1%.

On a yearly basis, construction output jumped 6.0% in January, after a 0.4% gain in December. December's figure was revised up from a 0.4% drop.

Civil engineering output increased 1.4% year-on-year in January, while production in the building sector climbed 7.1% year-on-year.

Britain's Chancellor George Osborne presented the budget 2016 on Wednesday. Growth and inflation forecasts were lowered. According to the U.K. Office for Budget Responsibility (OBR), the U.K. economy is expected to expand 2.0% in 2016, down from the previous forecast of 2.4%, and 2.2% in 2017, down from the previous forecast of 2.5%.

Inflation is expected to be 0.7% in 2016, down from the previous forecast of 1.0%, and 1.6% in 2017, down from the previous forecast of 1.8%.

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate remained unchanged at 5.1% in the November to January quarter, in line with expectations.

The claimant count slid by 18,000 people in February, beating expectations for a fall by 9,100, after a decrease of 28,400 people in January. January's figure was revised down from a 14,800 decrease.

Average weekly earnings, excluding bonuses, climbed by 2.2% in the November to January quarter, after a 2.0% gain in the October to December quarter.

Average weekly earnings, including bonuses, rose by 2.1% in the November to January quarter, in exceeding expectations for a 2.0% gain, after a 1.9% increase in the October to December quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,175.49 +35.52 +0.58 %

DAX 9,983.41 +49.56 +0.50 %

CAC 40 4,463 -9.63 -0.22 %

-

18:00

European stocks closed: FTSE 6175.49 35.52 0.58%, DAX 9983.41 49.56 0.50%, CAC 40 4463.00 -9.63 -0.22%

-

17:46

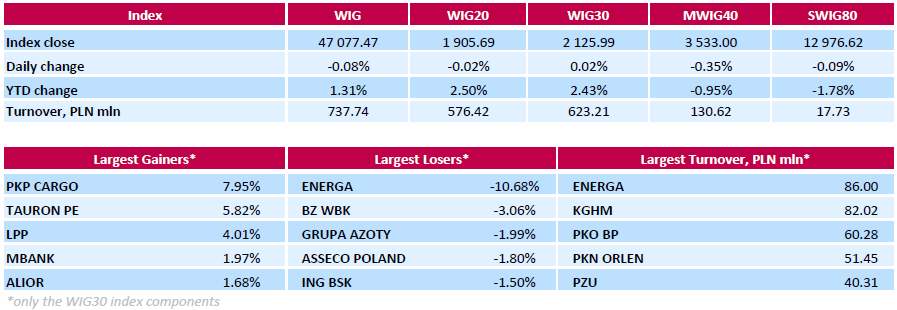

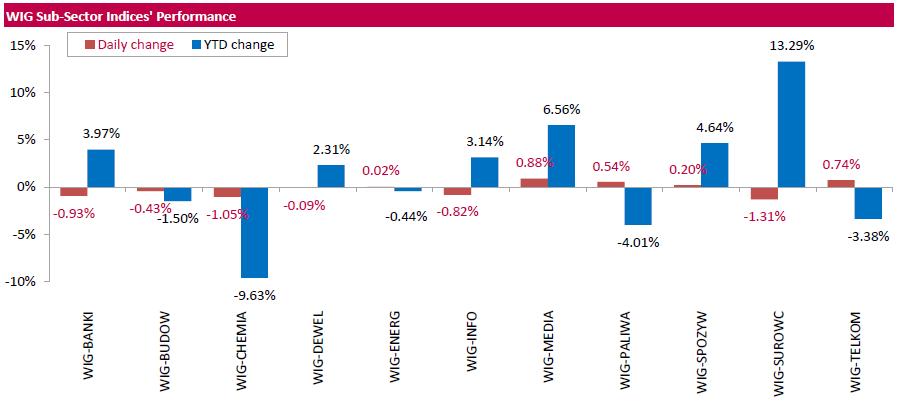

WSE: Session Results

Polish equity market closed flat Wednesday. Volatility stopped, the market calmed down ahead of Fed rate decision. The broad market measure, the WIG Index, slid down 0.08%. Sector performance within the WIG Index was mixed. Media sector (+0.88%) outperformed, while materials (-1.31%) lagged behind.

The large-cap stocks inched up by 0.02%. Within the index components, railway freight transport operator PKP CARGO (WSE: PKP) became the session's best performer, gaining 7.95% on the announcement the company had reached agreement with labor unions. It was followed by genco TAURON PE (WSE: TPE) and clothing retailer LPP (WSE: LPP), which advanced 5.82% and 4.01% respectively. On the other side of the ledger, genco ENERGA (WSE: ENG) recorded the biggest drop, down 10.68%, after news the company had submitted preliminary offers to buy shares in a state-controlled coal group PGG for up to PLN 600 mln. Other major decliners were bank BZ WBK (WSE: BZW), chemical producer GRUPA AZOTY (WSE: ATT) and IT-company ASSECO POLAND (WSE: ACP), losing 3.06%, 1.99% and 1.8% respectively.

-

17:28

Australian leading economic index declines 0.2% in February

Westpac Bank released the Westpac-Melbourne Institute leading economic index for Australia on late Tuesday evening. The leading economic index declined 0.2% in February, after a 0.1% rise in January. January's figure was revised up from a flat reading.

"Despite some improvement over the last two months, the Leading Index continues to point to below trend growth through much of 2016, implying a slowdown from 2015's slightly above trend pace," Westpac's Chief Economist, Matthew Hassan, said.

-

17:15

U.K. leading economic index increases 0.2% in January

The Conference Board (CB) released its leading economic index for the U.K. on Wednesday. The leading economic index (LEI) increased 0.2% in January, after a 0.3% rise in December. December's figure was revised down from a 0.4% gain.

The coincident index rose 0.3% in January, after a 0.1% decline in December. December's figure was revised down from a flat reading.

-

17:04

Britain’s government cuts growth and inflation forecasts

Britain's Chancellor George Osborne presented the budget 2016 on Wednesday. Growth and inflation forecasts were lowered. According to the U.K. Office for Budget Responsibility (OBR), the U.K. economy is expected to expand 2.0% in 2016, down from the previous forecast of 2.4%, and 2.2% in 2017, down from the previous forecast of 2.5%.

Inflation is expected to be 0.7% in 2016, down from the previous forecast of 1.0%, and 1.6% in 2017, down from the previous forecast of 1.8%.

Osborne said that the global economic outlook was weak, due to the slowdown in emerging economies and a weak growth in the developed economies.

The chancellor warned that Britain's exit from the European Union ('Brexit') would have a negative impact on the economy.

"Brexit could have negative implications for activity via business and consumer confidence and might result in greater volatility in financial and other asset markets," Osborne said.

The government will miss its public debt target. Debt forecasts as a share of GDP were upgraded.

-

16:27

U.S. crude inventories rise by 1.37 million barrels to 523.2 million in the week to March 11

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories rose by 1.32 million barrels to 523.2 million in the week to March 11.

Analysts had expected U.S. crude oil inventories to rise by 3.5 million barrels.

Gasoline inventories decreased by 747,000 barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, climbed by 545,000 barrels.

U.S. crude oil imports decreased by 355,000 barrels per day.

Refineries in the U.S. were running at 89.0% of capacity, down from 89.1% the previous week.

-

15:31

U.S.: Crude Oil Inventories, March 1.317

-

15:02

U.S. weekly earnings decline 0.5% in February

The U.S. Labor Department released its real earnings data on Wednesday. Average weekly earnings declined 0.5% in February, after a 0.7% increase in January.

Average hourly earnings were flat in February, after a 0.5% rise in January.

On a yearly basis, real average weekly earnings increased 0.6% in February, while hourly earnings rose 1.2%.

-

14:53

Foreign exchange market. European session: the U.S. dollar traded higher against the most major currencies after the release of the mixed U.S. economic data

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

09:30 United Kingdom Average Earnings, 3m/y January 1.9% 2% 2.1%

09:30 United Kingdom ILO Unemployment Rate January 5.1% 5.1% 5.1%

09:30 United Kingdom Claimant count February -28.4 Revised From -14.8 -9.1 -18

10:00 Eurozone Construction Output, y/y January 0.4% Revised From -0.4% 6%

11:00 U.S. MBA Mortgage Applications March 0.2% -3.3%

12:30 United Kingdom Annual Budget Release

12:30 Canada Foreign Securities Purchases January -1.40 Revised From -1.41 13.51

12:30 Canada Manufacturing Shipments (MoM) January 1.4% Revised From 1.2% 0.5% 2.3%

12:30 U.S. Housing Starts February 1120 Revised From 1099 1150 1178

12:30 U.S. Building Permits February 1204 Revised From 1202 1200 1167

12:30 U.S. CPI, m/m February 0.0% -0.2% -0.2%

12:30 U.S. CPI, Y/Y February 1.4% 0.9% 1.0%

12:30 U.S. CPI excluding food and energy, m/m February 0.3% 0.2% 0.3%

12:30 U.S. CPI excluding food and energy, Y/Y February 2.2% 2.2% 2.3%

13:15 U.S. Capacity Utilization February 77.1% 76.9% 76.7%

13:15 U.S. Industrial Production (MoM) February 0.8% Revised From 0.9% -0.3% -0.5%

13:15 U.S. Industrial Production YoY February -0.7% -1%

The U.S. dollar traded higher against the most major currencies after the release of the mixed U.S. economic data. The U.S. Commerce Department released the housing market data on Wednesday. Housing starts in the U.S. jumped 5.2% to 1.178 million annualized rate in February from a 1.120 million pace in January, exceeding expectations for an increase to 1.150 million. The increase was mainly driven by rise in starts of single-family homes.

The U.S. Labor Department released consumer price inflation data on Wednesday. The U.S. consumer price inflation fell 0.2% in February, in line with expectations, after a flat reading in January.

The index was mainly driven by lower gasoline prices, which slid 13% in February.

On a yearly basis, the U.S. consumer price index decreased to 1.0% in February from 1.4% in January, beating expectations for a fall to 0.9%.

The U.S. consumer price inflation excluding food and energy gained 0.3% in February, exceeding expectations for a 0.2% rise, after a 0.3% increase in January. It was the largest rise since May 2012.

The increase was driven by rents and medical costs.

On a yearly basis, the U.S. consumer price index excluding food and energy increased to 2.3% in February from 2.2% in January, beating expectations for a 2.2% rise.

The Federal Reserve released its industrial production report on Wednesday. The U.S. industrial production slid 0.5% in February, missing expectations for a 0.3% decrease, after a 0.8% rise in January. The decline was mainly driven by a drop in utilities.

Market participants are awaiting the release of the Fed's interest rate decision later in the day. Analysts expect the Fed to keep its monetary policy unchanged.

The euro traded lower against the U.S. dollar despite the strong construction data from the Eurozone. The Eurostat released its construction production data for the Eurozone on Wednesday. Construction production in the Eurozone climbed 3.6% in January, after a 0.7% decline in December.

Civil engineering output rose 1.7% in January, while production in the building sector was up 4.1%.

On a yearly basis, construction output jumped 6.0% in January, after a 0.4% gain in December. December's figure was revised up from a 0.4% drop.

Civil engineering output increased 1.4% year-on-year in January, while production in the building sector climbed 7.1% year-on-year.

The British pound traded lower against the U.S. dollar as the U.K. Office for Budget Responsibility (OBR) downgrades its growth and inflation forecasts. The U.K. economy is expected to expand 2.0% in 2016, down from the previous forecast of 2.4%, and 2.2% in 2017, down from the previous forecast of 2.5%.

Inflation is expected to be 0.7% in 2016, down from the previous forecast of 1.0%, and 1.6% in 2017, down from the previous forecast of 1.8%.

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate remained unchanged at 5.1% in the November to January quarter, in line with expectations.

The claimant count slid by 18,000 people in February, beating expectations for a fall by 9,100, after a decrease of 28,400 people in January. January's figure was revised down from a 14,800 decrease.

Average weekly earnings, excluding bonuses, climbed by 2.2% in the November to January quarter, after a 2.0% gain in the October to December quarter.

Average weekly earnings, including bonuses, rose by 2.1% in the November to January quarter, in exceeding expectations for a 2.0% gain, after a 1.9% increase in the October to December quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

The Canadian dollar traded mixed against the U.S. dollar after the release of the positive Canadian economic data. Statistics Canada released manufacturing shipments on Wednesday. Canadian manufacturing shipments rose 2.3% in January, beating expectations for a 0.5% increase, after a 1.4% increase in December. December's figure was revised up from a 1.2% rise. The increase was mainly driven by higher motor vehicle products sales. Motor vehicle rose 9.6% in January, while sales of food climbed 4.6%.

Statistics Canada released foreign investment figures on Wednesday. Foreign investors purchased C$13.51 billion of Canadian securities in January, after a divestment of C$1.40 billion in December. December's figure was revised up from a divestment of C$1.41 billion. The investment was led by Canadian private corporate debt securities.

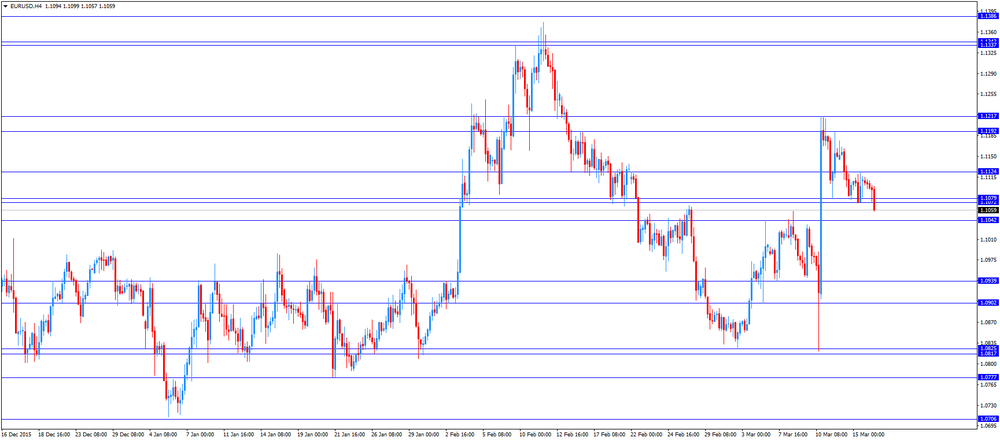

EUR/USD: the currency pair dropped to $1.1057

GBP/USD: the currency pair declined to $1.4051

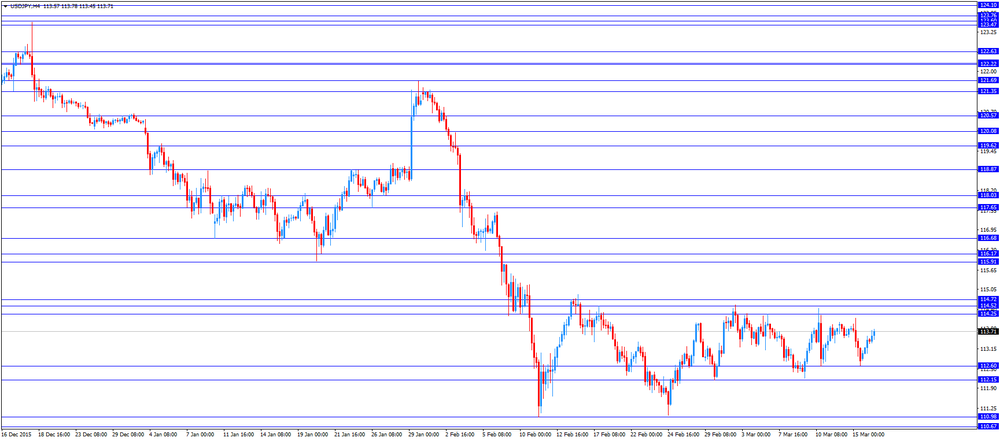

USD/JPY: the currency pair rose to Y113.78

The most important news that are expected (GMT0):

14:30 U.S. Crude Oil Inventories March 3.88

18:00 U.S. Fed Interest Rate Decision 0.5% 0.5%

18:00 U.S. FOMC Economic Projections

18:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter IV 0.9% 0.6%

21:45 New Zealand GDP y/y Quarter IV 2.3% 2%

22:05 Australia RBA Assist Gov Debelle Speaks

23:50 Japan Trade Balance Total, bln February -645.9 388.6

-

14:49

Option expiries for today's 10:00 ET NY cut

USDJPY: 110.55 (USD 250m) 113.00 (USD430m) 113.50 (453m) 114.00 (500m)

EURUSD: 1.0800 (EUR 1.13bln) 1.0860-65 (397m) 1.0900 (313m) 1.0955 (279m) 1.0975 (298m) 1.1050 (680m) 1.1200-05 (402m) 1.1250 (763m) 1.1300 (420m)

USDCHF 0.9800 (USD 180m) 1.0000 (201m)

AUDUSD 0.7350 (AUD 200m) 0.7450 (198m) 0..7500 (181m) 0.7550 (302m)

USDCAD 1.3400-10 (USD 430m) 1.3445 (206m)

AUDNZD 1.1100 ( AUD (238M)

EURJPY 127.90-95 (EUR 496m)

-

14:41

WSE: After start on Wall Street

The opening on Wall Street points to the beginning of another lackluster session. The main Wall Street indexes are in a light shade of red after opening. The WIG20 index decreased by 0.59%, and is five points below the level of 1900 points.

From the point of view of European markets, this means that starting a session on Wall Street should not bring major changes to the end of today's trading in Europe, however today should come to break the calm and the market probably will return to the previous variation.

-

14:37

U.S. industrial production slides 0.5% in February

The Federal Reserve released its industrial production report on Wednesday. The U.S. industrial production slid 0.5% in February, missing expectations for a 0.3% decrease, after a 0.8% rise in January. January's figure was revised down from a 0.9% increase.

The decline was mainly driven by a drop in utilities. Mining output fell 1.4% in February, while utilities production plunged 4.0%.

Manufacturing output rose 0.2% in February, after a 0.5% gain in January.

Capacity utilisation rate decreased to 76.7% in February from 77.1% in January, missing expectations for a decline to 76.9%.

-

14:35

U.S. Stocks open: Dow -0.17%, Nasdaq -0.20%, S&P -0.16%

-

14:27

Foreign investors purchase C$13.51 billion of Canadian securities in January

Statistics Canada released foreign investment figures on Wednesday. Foreign investors purchased C$13.51 billion of Canadian securities in January, after a divestment of C$1.40 billion in December. December's figure was revised up from a divestment of C$1.41 billion.

The investment was led by Canadian private corporate debt securities.

Canadian investors sold C$13.8 billion of foreign securities in January, mainly equities.

-

14:27

Before the bell: S&P futures -0.41%, NASDAQ futures -0.30%

U.S. stock-index slipped.

Global Stocks:

Nikkei 16,974.45 -142.62 -0.83%

Hang Seng 20,257.7 -31.07 -0.15%

Shanghai Composite 2,870.48 +6.11 +0.21%

FTSE 6,138.98 -0.99 -0.02%

CAC 4,458.5 -14.13 -0.32%

DAX 9,946.46 +12.61 +0.13 %

Crude oil $36.87 (+1.46%)

Gold $1228.90 (-0.17%)

-

14:22

Orders

EUR/USD

Offers 1.1100 1.1120 1.1150 1.1180 1.1200 1.1230 1.1250-60 1.1275 1.1300 1.1310-20

Bids 1.1075-80 1.1050 1.1030 1.1000 1.0985 1.0950 1.0925-30 1.0900

GBP/USD

Offers 1.4125-30 1.4150 1.4180 1.4200 1.4220 1.4250-55 1.4280 1.4300 1.4320 1.4350

Bids 1.4080-85 1.4065 1.4050 1.4030 1.4000 1.3985 1.3970 1.3950 1.3900

EUR/JPY

Offers 126.00 126.30 126.50 126.80 27.00 127.30 127.50

Bids 125.80 125.50 125.20 125.00 124.50 124.20 124.00

EUR/GBP

Offers 0.7880 0.7900 0.7925 0.7950 0.7985 0.8000

Bids 0.7840 0.7820 0.7800 0.7785 0.7770 0.7750

USD/JPY

Offers 113.80-85 114.00 114.25-30 114.50 114.76 115.00 115.50

Bids 113.30 113.00 112.80 112.40 112.20 112.00 111.85 111.50 111.30 111.00

AUD/USD

Offers 0.7500 0.7525-30 0.7550 0.7575-80 0.7600 0.7650

Bids 0.7450 0.7435 0.7420 0.7400 0.7385 0.7350

-

14:16

Canadian manufacturing shipments rise 2.3% in January

Statistics Canada released manufacturing shipments on Wednesday. Canadian manufacturing shipments rose 2.3% in January, beating expectations for a 0.5% increase, after a 1.4% increase in December. December's figure was revised up from a 1.2% rise.

The increase was mainly driven by higher motor vehicle products sales. Motor vehicle rose 9.6% in January, while sales of food climbed 4.6%.

Inventories increased 0.6% in January, driven by a rise in the transportation equipment industry.

-

14:15

U.S.: Industrial Production (MoM), February -0.5% (forecast -0.3%)

-

14:15

U.S.: Capacity Utilization, February 76.7% (forecast 76.9%)

-

14:15

U.S.: Industrial Production YoY , February -1%

-

14:10

U.S. consumer price inflation drops 0.2% in February

The U.S. Labor Department released consumer price inflation data on Wednesday. The U.S. consumer price inflation fell 0.2% in February, in line with expectations, after a flat reading in January.

The index was mainly driven by lower gasoline prices, which slid 13% in February.

Shelter costs climbed 0.3% in February, medical care costs were up 0.5%, while food prices increased 0.2%.

On a yearly basis, the U.S. consumer price index decreased to 1.0% in February from 1.4% in January, beating expectations for a fall to 0.9%.

The U.S. consumer price inflation excluding food and energy gained 0.3% in February, exceeding expectations for a 0.2% rise, after a 0.3% increase in January. It was the largest rise since May 2012.

The increase was driven by rents and medical costs.

On a yearly basis, the U.S. consumer price index excluding food and energy increased to 2.3% in February from 2.2% in January, beating expectations for a 2.2% rise.

The consumer price index is not preferred Fed's inflation measure.

-

13:59

Housing starts in the U.S. jump 5.2% in February

The U.S. Commerce Department released the housing market data on Wednesday. Housing starts in the U.S. jumped 5.2% to 1.178 million annualized rate in February from a 1.120 million pace in January, exceeding expectations for an increase to 1.150 million. January's figure was revised up from 1.099 million units.

The increase was mainly driven by rise in starts of single-family homes.

Housing market benefits from the strengthening of the labour market.

Building permits in the U.S. fell 3.1% to 1.1167 million annualized rate in February from a 1.204 million pace in January, missing expectations for a 1,200 million pace. January's figure was revised up from 1.202 million units.

Starts of single-family homes increased 7.2% in February. Building permits for single-family homes were up 0.4%.

Starts of multifamily buildings rose 0.8% in February. Permits for multi-family housing slid 8.4%.

-

13:44

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Cisco Systems (CSCO) assumed with an Outperform at RBC Capital Mkts

-

13:31

U.S.: Building Permits, February 1167 (forecast 1200)

-

13:31

Canada: Manufacturing Shipments (MoM), January 2.3% (forecast 0.5%)

-

13:30

U.S.: Housing Starts, February 1178 (forecast 1150)

-

13:30

U.S.: CPI, Y/Y, February 1.0% (forecast 0.9%)

-

13:30

U.S.: CPI, m/m , February -0.2% (forecast -0.2%)

-

13:30

U.S.: CPI excluding food and energy, m/m, February 0.3% (forecast 0.2%)

-

13:30

Canada: Foreign Securities Purchases, January 13.51

-

13:30

U.S.: CPI excluding food and energy, Y/Y, February 2.3% (forecast 2.2%)

-

12:29

WSE: Mid session comment

The morning session phase came to an end. Despite the decline in the share price of Energy by 10 percent, Warsaw market stays in balance, although the index WIG20 lost approx. 0,36% and is below the level of 1900 points.

European markets also curbed their earlier optimism. Positive is to reduce earlier losses by the PLN, which weakened strongly this morning against the EUR and the USD.

-

12:00

U.S.: MBA Mortgage Applications, March -3.3%

-

12:00

European stock markets mid session: stocks traded higher, supported by higher oil prices

Stock indices traded higher on a rise in oil prices. Oil prices increase on news that OPEC and non-OPEC members will meet on April 17 in Doha to discuss the stabilisation of the oil market.

Market participants are awaiting the release of the Fed's interest rate decision today. Analysts expect the Fed to keep its monetary policy unchanged.

Market participants also eyed the Eurozone's economic data. The Eurostat released its construction production data for the Eurozone on Wednesday. Construction production in the Eurozone climbed 3.6% in January, after a 0.7% decline in December.

Civil engineering output rose 1.7% in January, while production in the building sector was up 4.1%.

On a yearly basis, construction output jumped 6.0% in January, after a 0.4% gain in December. December's figure was revised up from a 0.4% drop.

Civil engineering output increased 1.4% year-on-year in January, while production in the building sector climbed 7.1% year-on-year.

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate remained unchanged at 5.1% in the November to January quarter, in line with expectations.

The claimant count slid by 18,000 people in February, beating expectations for a fall by 9,100, after a decrease of 28,400 people in January. January's figure was revised down from a 14,800 decrease.

Average weekly earnings, excluding bonuses, climbed by 2.2% in the November to January quarter, after a 2.0% gain in the October to December quarter.

Average weekly earnings, including bonuses, rose by 2.1% in the November to January quarter, in exceeding expectations for a 2.0% gain, after a 1.9% increase in the October to December quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

Current figures:

Name Price Change Change %

FTSE 100 6,152.34 +12.37 +0.20 %

DAX 9,990.18 +56.33 +0.57 %

CAC 40 4,484 +11.37 +0.25 %

-

11:48

Qatar’s Energy Minister Mohammed al-Sada: OPEC and non-OPEC members will meet on April 17 in Doha

Qatar's Energy Minister Mohammed al-Sada said on Wednesday that OPEC and non-OPEC members will meet on April 17 in Doha to discuss the stabilisation of the oil market.

Russian Energy Minister Alexander Novak said on Monday that a deal on freezing oil output between OPEC and non-OPEC members could be signed in April. He added that this agreement could exclude Iran as it plans to boost its production.

-

11:42

European Central Bank Governing Council member Ardo Hansson warns about the side effects on the financial stability from the central bank’s stimulus measures

European Central Bank (ECB) Governing Council member Ardo Hansson on Wednesday warned about the side effects on the financial stability from the central bank's stimulus measures. He noted that the monetary policy could lead to asset price bubbles.

Hansson also said that governments would not implement reforms as they could get cheap money.

Hansson voted against further stimulus measures last Thursday.

-

11:25

Construction production in the Eurozone climbs 3.6% in January

The Eurostat released its construction production data for the Eurozone on Wednesday. Construction production in the Eurozone climbed 3.6% in January, after a 0.7% decline in December.

Civil engineering output rose 1.7% in January, while production in the building sector was up 4.1%.

On a yearly basis, construction output jumped 6.0% in January, after a 0.4% gain in December. December's figure was revised up from a 0.4% drop.

Civil engineering output increased 1.4% year-on-year in January, while production in the building sector climbed 7.1% year-on-year.

-

11:17

U.K. unemployment rate remains unchanged at 5.1% in the November to January quarter

The Office for National Statistics (ONS) released its labour market data on Wednesday. The U.K. unemployment rate remained unchanged at 5.1% in the November to January quarter, in line with expectations.

The claimant count slid by 18,000 people in February, beating expectations for a fall by 9,100, after a decrease of 28,400 people in January. January's figure was revised down from a 14,800 decrease.

U.K. unemployment in the November to January period dropped by 28,000 to 1.68 million from the previous quarter.

The employment rate was 74.1% in the November to January quarter. It was the highest reading since 1971.

Average weekly earnings, excluding bonuses, climbed by 2.2% in the November to January quarter, after a 2.0% gain in the October to December quarter.

Average weekly earnings, including bonuses, rose by 2.1% in the November to January quarter, in exceeding expectations for a 2.0% gain, after a 1.9% increase in the October to December quarter.

The Bank of England monitors closely the wages growth it considers when to start hiking its interest rate.

-

11:00

Eurozone: Construction Output, y/y, January 6%

-

10:50

China’s Premier Li Keqiang: China will achieve all economic growth targets

China's Premier Li Keqiang said on Wednesday that the country will achieve all economic growth targets, adding that there will be no "hard landing". He noted that the government should be able to stimulate the country's economy via structural reforms.

The government expect the economy to expand 6.5% - 7.0% this year and at least 6.5% until 2020.

Li pointed out the government had tools to stimulate the economy if there will be risks that targets could not be reached.

He also said that the government planned to launch a link connecting the Hong Kong and Shenzhen stock exchanges this year.

-

10:48

WSE: Energa SA

Listed power groups PGE (WSE: PGE) and Energa (WSE: ENG), as well as PGNiG Termika, a unit of natural gas group PGNiG (WSE: PGN), filed preliminary non-binding offers to invest in total up to PLN 1.5 bln in Polska Grupa Gornicza (Polish Mining Group), the latter having a mandate to restructure heavily indebted coal miner Kompania Węglowa.

The amount of the contemplated investment by Energa, which can reach up to PLN 600 mln, is expected to be frowned upon by investors, and we can see impressive sell-side build up of Energa SA, whose shares lost up to 10%.

-

10:40

Bank of Japan Governor Haruhiko Kuroda: it is possible to cut interest rate to around -0.5%.

Bank of Japan (BoJ) Governor Haruhiko Kuroda said on Wednesday that it was possible to cut interest rate to around -0.5%.

Kuroda also said that negative interest rates led to lower currency but it was not the central bank's target.

He pointed out that the BoJ was ready to add further stimulus measures if needed to boost inflation toward 2% target.

-

10:30

United Kingdom: Average Earnings, 3m/y , January 2.1% (forecast 2%)

-

10:30

United Kingdom: Claimant count , February -18 (forecast -9.1)

-

10:30

United Kingdom: ILO Unemployment Rate, January 5.1% (forecast 5.1%)

-

10:22

New Zealand’s seasonally adjusted current account deficit widens to NZ$1.95 billion in the fourth quarter

Statistics New Zealand released its current account data on late Tuesday evening. New Zealand's seasonally adjusted current account deficit widened to NZ$1.95 billion in the fourth quarter from NZ$1.72 billion from the third quarter.

The rise in deficit was driven by a drop in earnings from both goods and services exports.

The services surplus fell by NZ$14 million to NZ$977 million in the fourth quarter from the previous quarter, while the goods deficit climbed by NZ$277 million to NZ$810 million.

"While lower petrol prices caused the value of imports to decrease, the fall in dairy prices in the latest quarter had a bigger impact on our exports, resulting in a larger deficit," international statistics manager Stuart Jones said.

-

10:09

Saud Arabian government launches new austerity measures

Reuters reported on Monday that Saud Arabian government launched new austerity measures. The government ordered to lower contract spending by at least 5% as the government faced a budget deficit due to low oil prices. The ministry of economy said that new measures aimed to "rationalize spending and increase its efficiency".

-

09:17

WSE: After opening

Trading on the WIG20 futures contracts began with a cosmetic increase, at the level of +0.2% (FW20H16 opened at 1911 points). This fits into the expected pattern of quiet, neutral behavior of European contracts after a very calm session in the US.

Wig20 index opened at level of 1909.60 points (+0.18% to previous close)

WIG 47212.18 +0.21%

WIG20 1909.60 +0.18%

WIG30 2131.16 +0.26%

mWIG40 3545.07 -0.01%

European stock exchanges started the day with no surprises and indices gaining in value. WSE fits in the environment with the increase in the WIG20, and increasing turnover, with PKO and PGE being most noticeable gainers.

-

09:04

Option expiries for today's 10:00 ET NY cut

USD/JPY: 110.55 (USD 250m) 113.00 (USD430m) 113.50 (453m) 114.00 (500m)

EUR/USD: 1.0800 (EUR 1.13bln) 1.0860-65 (397m) 1.0900 (313m) 1.0955 (279m) 1.0975 (298m) 1.1050 (680m) 1.1200-05 (402m) 1.1250 (763m) 1.1300 (420m)

USD/CHF 0.9800 (USD 180m) 1.0000 (201m)

AUD/USD 0.7350 (AUD 200m) 0.7450 (198m) 0..7500 (181m) 0.7550 (302m)

USD/CAD 1.3400-10 (USD 430m) 1.3445 (206m)

AUD/NZD 1.1100 ( AUD (238M)

EUR/JPY 127.90-95 (EUR 496m)

-

08:30

WSE: Before opening

Sessions on Wall Street ended with modest movements of the major indexes. Shadow over the market was cast by the oil prices and concerns about the condition of the economy, but overall, there is no doubt that Tuesday has been another day after Monday waiting for today's announcement of the Federal Open Market Committee.

Quotations of index futures in Europe indicate, however, that in the morning we can expect European indices rebound in values similar to yesterday's losses. In other words, maintaining the current atmosphere till 9:00 would give a slightly positive plus openings, which should quickly turn into waiting for US data. Expectations seem to be clear - no interest rate hike and signal that a hike would take place at the June meeting of the FOMC. Any deviation from such a scenario will be considered more or less surprising.

Locally looking it is hard to expect that the Warsaw Stock Exchange will managed to break away from dependence on core markets.

-

08:23

Asian session: Yen fell

Yen fell as Bank of Japan Gov. Haruhiko Kuroda said Wednesday it is theoretically possible to cut a short-term interest rate to around minus 0.5%, a comment that could add to uneasiness among the public over the policy experiment aimed at beating deflation. Kuroda said it is theoretically possible to bring the rate down to about minus 0.5%, and that he may take such measures if a major global economic crisis potentially threatens Japan's economy.

The New Zealand dollar fell as banks could face billions in write-offs, and may have to go to their owners for extra cash, under a grim scenario for the dairy sector. On Wednesday the Reserve Bank revealed its stress tests for New Zealand's major rural lenders about the impact of dairy prices staying low for years to come.

EUR/USD: during the Asian session the pair traded in the range of $1.1095-10

GBP/USD: during the Asian session the pair fell to $1.4120

USD/JPY: during the Asian session the pair rose to Y113.55

Based on ForexLive materials

-

08:18

Options levels on wednesday, March 16, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1254 (1112)

$1.1210 (2032)

$1.1170 (3150)

Price at time of writing this review: $1.1093

Support levels (open interest**, contracts):

$1.1035 (1399)

$1.0979 (2124)

$1.0945 (4398)

Comments:

- Overall open interest on the CALL options with the expiration date April, 8 is 38289 contracts, with the maximum number of contracts with strike price $1,0900 (3150);

- Overall open interest on the PUT options with the expiration date April, 8 is 62993 contracts, with the maximum number of contracts with strike price $1,0900 (5994);

- The ratio of PUT/CALL was 1.65 versus 1.65 from the previous trading day according to data from March, 15

GBP/USD

Resistance levels (open interest**, contracts)

$1.4506 (1429)

$1.4410 (2464)

$1.4314 (890)

Price at time of writing this review: $1.4255

Support levels (open interest**, contracts):

$1.4190 (613)

$1.4093 (610)

$1.3995 (1529)

Comments:

- Overall open interest on the CALL options with the expiration date April, 8 is 20925 contracts, with the maximum number of contracts with strike price $1,4400 (2464);

- Overall open interest on the PUT options with the expiration date April, 8 is 19291 contracts, with the maximum number of contracts with strike price $1,3850 (3266);

- The ratio of PUT/CALL was 0.92 versus 0.92 from the previous trading day according to data from March, 15

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:19

Global Stocks: markets await news from U.S.

U.K. stocks dropped Tuesday, suffering their first loss in three sessions, as mining shares were swept lower after Antofagasta PLC canceled its final dividend. The axed dividend "acted as a sharp reminder of the industry's suffering after the hefty drop in metals prices," wrote Jasper Lawler, market analyst at CMC Markets, in a note.

U.S. stocks finished lower Tuesday, but off session lows, as weak oil prices drove a selloff in energy and materials shares. Weak U.S. economic data also weighed on sentiment a day before the Federal Reserve is expected to release an updated policy statement and economic projections.

Asian shares were mixed Wednesday ahead of Chinese Premier Li Keqiang's address to government officials in Beijing. While investors don't expect the Federal Reserve to change monetary policy, they will be closely watching the bank's policy statement and economic projections, as well as Chairwoman Janet Yellen's news conference. Most expect the Fed will raise rates later in the year, with a vast majority of fund managers expecting no more than two hikes in the next 12 months, according to a fund manager survey published Wednesday by Bank of America Merrill Lynch.

Based on MarketWatch materials

-

03:06

Nikkei 225 17,037.82 -79.25 -0.46 %, Hang Seng 20,312.33 +23.56 +0.12 %, Shanghai Composite 2,866.7 +2.33 +0.08 %

-

00:33

Commodities. Daily history for Mar 15’2016:

(raw materials / closing price /% change)

Oil 36.79 +1.24%

Gold 1,232.70 +0.14%

-

00:32

Stocks. Daily history for Sep Mar 15’2016:

(index / closing price / change items /% change)

Nikkei 225 17,117.07 -116.68 -0.7 %

Hang Seng 20,288.77 -146.57 -0.7 %

Shanghai Composite 2,864.26 +4.76 +0.2 %

FTSE 100 6,139.97 -34.60 -0.6 %

CAC 40 4,472.63 -33.96 -0.8 %

Xetra DAX 9,933.85 -56.41 -0.6 %

S&P 500 2,015.93 -3.71 -0.2 %

NASDAQ Composite 4,728.67 -21.61 -0.5 %

Dow Jones 17,251.53 +22.40 +0.1 %

-

00:31

Currencies. Daily history for Mar 15’2016:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1105 +0,04%

GBP/USD $1,4151 -1,05%

USD/CHF Chf0,9869 -0,02%

USD/JPY Y113,19 -0,53%

EUR/JPY Y125,68 -0,51%

GBP/JPY Y160,17 -1,59%

AUD/USD $0,7458 -0,66%

NZD/USD $0,6606 -0,95%

USD/CAD C$1,3349 +0,63%

-

00:02

Schedule for today, Wednesday, Mar 16’2016:

(time / country / index / period / previous value / forecast)

09:30 United Kingdom Average Earnings, 3m/y January 1.9% 2%

09:30 United Kingdom ILO Unemployment Rate January 5.1% 5.1%

09:30 United Kingdom Claimant count February -14.8 -9.1

10:00 Eurozone Construction Output, y/y January -0.4%

11:00 U.S. MBA Mortgage Applications March 0.2%

12:30 United Kingdom Annual Budget Release

12:30 Canada Foreign Securities Purchases January -1.41

12:30 Canada Manufacturing Shipments (MoM) January 1.2% 0.5%

12:30 U.S. Housing Starts February 1099 1150

12:30 U.S. Building Permits February 1202 1200

12:30 U.S. CPI, m/m February 0.0% -0.2%

12:30 U.S. CPI, Y/Y February 1.4% 0.9%

12:30 U.S. CPI excluding food and energy, m/m February 0.3% 0.2%

12:30 U.S. CPI excluding food and energy, Y/Y February 2.2% 2.2%

13:15 U.S. Capacity Utilization February 77.1% 76.9%

13:15 U.S. Industrial Production (MoM) February 0.9% -0.3%

13:15 U.S. Industrial Production YoY February -0.7%

14:30 U.S. Crude Oil Inventories March 3.88

18:00 U.S. Fed Interest Rate Decision 0.5% 0.5%

18:00 U.S. FOMC Economic Projections

18:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter IV 0.9% 0.6%

21:45 New Zealand GDP y/y Quarter IV 2.3% 2%

22:05 Australia RBA Assist Gov Debelle Speaks

23:50 Japan Trade Balance Total, bln February -645.9 388.6

-