Noticias del mercado

-

21:00

Dow -49.61 17,377.48 -0.28% Nasdaq -49.64 4,589.68 -1.07% S&P -10.9 2,000.37 -0.54%

-

18:00

European stocks close: stocks closed higher on speculation the ECB will add further stimulus measures

Stock indices closed higher on speculation the ECB will add further stimulus measures as the Swiss National Bank (SNB) announced today that it will discontinue the 1.20 per euro exchange rate floor.

The Swiss National Bank (SNB) President Thomas Jordan said at a press conference on Thursday that the SNB will intervene in the foreign exchange markets if required.

Investors speculate that the European Central Bank could decide on its policy meeting on January 22 to purchase government bonds.

Eurozone's trade surplus widened to €20.0 billion in November from €19.6 billion in October, missing expectations for a rise to €21.3 billion. October's figure was revised up from a surplus of €19.4 billion.

The increase was driven by a weaker euro and falling oil prices.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,498.78 +110.32 +1.73%

DAX 10,032.61 +215.53 +2.20%

CAC 40 4,323.2 +99.96 +2.37%

-

18:00

European stocks closed: FTSE 100 6,498.78 +110.32 +1.73% CAC 40 4,323.2 +99.96 +2.37% DAX 10,032.61 +215.53 +2.20%

-

15:35

U.S Stocks open: Dow +0.25%, Nasdaq +0.37%, S&P +0.29%

-

15:27

Before the bell: S&P futures +0.30%, Nasdaq futures +0.08%

U.S. stock-index futures rose as data showed wholesale prices fell and New York-area manufacturing expanded. Futures fluctuated earlier after Switzerland's central bank unexpectedly gave up its minimum exchange rate.

Global markets:

Nikkei 17,108.7 +312.74 +1.86%

Hang Seng 24,350.91 +238.31 +0.99%

Shanghai Composite 3,335.88 +113.44 +3.52%

FTSE 6,457.9 +69.44 +1.09%

CAC 4,294.21 +70.97 +1.68%

DAX 9,956.74 +139.66 +1.42%

Crude oil $50.27 (+3.75%)

Gold $1255.20 (+1.67%)

-

15:07

DOW components before the bell

(company / ticker / price / change, % / volume)

Caterpillar Inc

CAT

86.14

+0.08%

52.1K

Home Depot Inc

HD

102.79

+0.15%

0.8K

Goldman Sachs

GS

180.72

+0.27%

2.8K

Cisco Systems Inc

CSCO

28.00

+0.29%

2.6K

Nike

NKE

94.00

+0.31%

5.3K

McDonald's Corp

MCD

91.82

+0.31%

0.3K

Verizon Communications Inc

VZ

47.13

+0.34%

11.7K

AT&T Inc

T

33.45

+0.36%

3.1K

American Express Co

AXP

87.50

+0.49%

0.2K

JPMorgan Chase and Co

JPM

57.10

+0.51%

8.5K

Visa

V

257.00

+0.56%

0.1K

General Electric Co

GE

23.93

+0.63%

15.8K

Intel Corp

INTC

36.60

+0.69%

10.3K

Walt Disney Co

DIS

94.88

+0.69%

0.3K

Boeing Co

BA

131.34

+0.74%

4.8K

Wal-Mart Stores Inc

WMT

87.44

+0.96%

0.2K

Chevron Corp

CVX

105.51

+1.55%

7.4K

Exxon Mobil Corp

XOM

91.17

+1.59%

44.6K

Pfizer Inc

PFE

32.48

0.00%

4.2K

Microsoft Corp

MSFT

45.95

-0.01%

8.0K

Travelers Companies Inc

TRV

103.76

-0.01%

1.3K

International Business Machines Co...

IBM

155.65

-0.10%

2.2K

The Coca-Cola Co

KO

42.39

-0.40%

0.5K

Merck & Co Inc

MRK

62.24

-0.64%

0.2K

Johnson & Johnson

JNJ

103.30

-0.67%

48.0K

-

15:03

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Apple (AAPL) downgrade to Neutral from Buy at Mizuho, target $115

Johnson&Johnson (JNJ) downgraded to Sell from Neutral at Goldman

Other:

Hewlett-Packard (HPQ) removed from Short-Term Buy List at Deutsche Bank

JPMorgan Chase (JPM) target lowered to $65 from $68 at Jefferies

-

14:47

Company News: Bank of America (BAC) reported weaker than expected fourth quarter profits

Bank of America (BAC) earned $0.32 per share in the fourth quarter, missing analysts' estimate of $0.31. Revenue in the fourth quarter dropped 12.7% year-over-year to $20.15 billion, missing analysts' estimate of $21.01 billion.

Bank of America (BAC) shares decreased to $15.54 (-3.12%) prior to the opening bell.

-

14:38

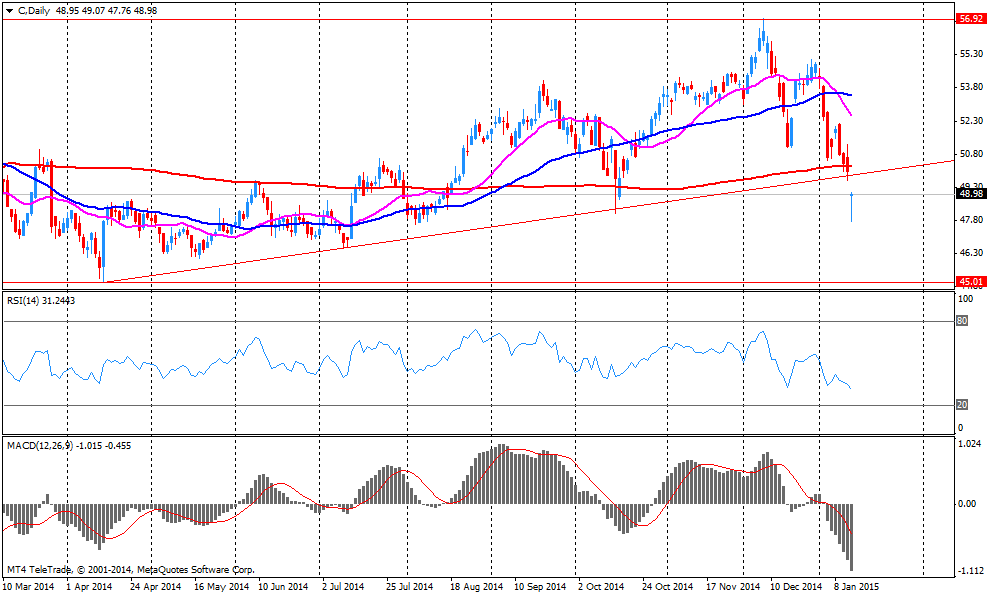

Company News: Citigroup (C) reported weaker than expected fourth quarter profits

Citigroup (C) earned $0.06 per share in the fourth quarter, missing analysts' estimate of $0.10. Revenue in the fourth quarter increased 0.2% year-over-year to $17.81 billion, missing analysts' estimate of $18.53 billion.

Citigroup (C) shares decreased to $48.55 (-1.02%) prior to the opening bell.

-

13:00

European stock markets mid-session: SNB sends European indices south in volatile trading after early gains

European indices sharply declined after the SNB decided to discontinue the minimum exchange rate of 1.20 per euro and lowered interest rates more into negative territory to -0.75. The surprise move erased early gains driven by a recovery in commodities. The Swiss franc rallied against its major peers and Swiss stocks plunged.

Earlier in the session markets were driven by expectations that the ECB will implement quantitative easing after its policy meeting on January 22nd after the interim ruling by the European Court of Justice. Yesterday Advocate General Pedro Cruz Villalon of the EU Court of justice in Luxembourg said the ECB's Outright Monetary Transactions program is "in principle" in line with European law and advised the judges to approve the measures.

Investors are looking forward to the European Central Bank policy meeting taking place on January 22nd and the Greek elections on January 25th where the anti-austerity party Syriza, that wants to renegotiate debt, is leading polls. According to Moody the "Grexit" seems a relatively unlikely scenario, even if the anti-austerity party Syriza will win in the upcoming Greek elections.

Eurozone's Trade Balance rose less-than-expected in the last quarter. Analysts forecasted the balance to rise to 21.3 billion, 1.3 billion more than the actual reading reported by Eurostat. In the previous quarter the Trade Balance had a reading of 19.4 billion.

In today's session the FTSE 100 index lost declining -0.61% quoted at 6,349.27. France's CAC 40 lost -0.66% trading at 4,195.46. Germany's DAX 30 is currently trading -0.30% at 9,787.87.

-

10:00

European Stocks. First hour: Indices recover after yesterday’s commodity rout and World Bank outlook on growth

European indices rebound from yesterday's drop tracking gains in commodities with mining and energy stocks adding the most as copper rose from 5-year lows and oil recovered. Yesterday commodities fell as the World Bank cut its forecast for 2015 despite continuously falling oil prices. The bank cited disappointing growth prospects in the Eurozone and Japan as main reasons. Strong company quarterly results further lend support.

Markets were also driven by expectations that the ECB will implement quantitative easing at its policy meeting on January 22nd after the interim ruling by the European Court of Justice. Yesterday Advocate General Pedro Cruz Villalon of the EU Court of justice in Luxembourg said the ECB's Outright Monetary Transactions program is "in principle" in line with European law and advised the judges to approve the measures.

The FTSE 100 index, the most commodity-and energy heavy index out of the three, is currently trading +1.14% quoted at 6,461.19 points, Germany's DAX 30 added +1.24% trading at 9,938.53. France's CAC 40 rose +1.31%, currently trading at 4,278.64 points.

Market participants are looking forward to the publication of the Eurozone's Trade Balance and later in the day the NY Fed Empire State manufacturing index, Initial Jobless claims and the Producer Price Index as well as the Philadelphia Fed Manufacturing Survey in the U.S.

-

09:00

Global Stocks: U.S. indices decline, Nikkei, Hang Seng and Shanghai Composite add gains

U.S. markets closed lower on Wednesday after disappointing retail sales data showig the steepest drop in almost a year, with losses in the Basic Materials, Consumer Services and Financials losing the most. The DOW JONES index lost -1.06%, 186 points, closing at 17,427.09. The S&P 500 declined by -0.58% with a final quote of 2,011.27, dropping intraday below the level of 2,000 points.

Chinese stock markets rose on Thursday. Hong Kong's Hang Seng added +0.86% with a final quote of 24,319.17 points. China's Shanghai Composite closed at 3,335.88 points, adding 3.52%. China was reported to have broadened lending rules amid surging loan growth.

Japan's Nikkei advanced +1.86% posting the biggest gains in 4 weeks closing at 17,108.70 points after yesterday's sharp decline. A rebound in oil eased worries about global growth and lifted energy shares and a weaker Japanese yen helped exporters. Bank of Japan Governor Haruhiko Kuroda said that the bank will maintain stimulus measures until inflation is stable at 2 percent as monetary easing has its intended effects. Core Machinery Orders in November grew less-than expected +1.3%, analysts predicted +4.8%. Year on year Orders declined -14.6%, far more than the forecasted -5.8%.

-

09:00

Global Stocks: U.S. indices decline on disappointing results and mixed data

U.S. markets closed lower on Wednesday for a fifth day as bank results disappointed and energy shares extended losses on falling oil prices. According to Reuters expectations for U.S. fourth-quarter earnings have been scaled back sharply. The SNB's decision to scrap its cap to the franc further added to volatility. A mixed set of economic data added to the negative sentiment. The Philadelphia Federal Reserve Bank released its manufacturing index on Thursday. The index dropped to 6.3 in January from 24.5 in December. That was the lowest level since February 2014. Analysts had expected the index to decline to 20.3. The DOW JONES index lost -0.61%, declining by 106 points, closing at 17,320.71. The S&P 500 declined by -0.92% with a final quote of 1,992.67, falling below the level of 2,000 points for the first time in a month.

Chinese stock markets were mixed on Friday amid speculation the government will increase stimulus to boost economic growth. Hong Kong's Hang Seng trading -0.80% at 24,156.92 points. China's Shanghai Composite closed at 3,377.43 points, adding +1.23% extending its longest weekly winning streak in 8 years.

Japan's Nikkei fell to a 2-½ moth low during trade. The index closed -1.43 at 16,864.16 points falling for a third week. A strong yen as a result of flight to safety weighed Japanese stocks down. At markets close speculations on pension funds and the BOJ buying stocks trimmed losses and investors saw the sharp decline in prices as buying opportunity.

-

03:01

Nikkei 225 17,001.64 +205.68 +1.22%, Hang Seng 24,110.96 -1.64 -0.01%, Shanghai Composite 3,209.08 -13.36 -0.41%

-

00:31

Stocks. Daily history for Jan 14’2015:

(index / closing price / change items /% change)

Nikkei 225 16,795.96 -291.75 -1.71%

Hang Seng 24,112.6 -103.37 -0.43%

Shanghai Composite 3,223.25 -12.05 -0.37%

FTSE 100 6,388.46 -153.74 -2.35%

CAC 40 4,223.24 -67.04 -1.56%

Xetra DAX 9,817.08 -123.92 -1.25%

S&P 500 2,011.27 -11.76 -0.58%

NASDAQ Composite 4,639.32 -22.18 -0.48%

Dow Jones 17,427.09 -186.59 -1.06%

-