Noticias del mercado

-

21:00

DJIA 18559.38 29.96 0.16%, NASDAQ 5264.20 19.59 0.37%, S&P 500 2188.58 5.94 0.27%

-

18:01

European stocks closed: FTSE 6868.51 39.97 0.59%, DAX 10592.88 98.53 0.94%, CAC 4421.45 31.51 0.72%

-

17:52

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes rose on Tuesday, with the Nasdaq hitting a record intraday high, led by technology companies and robust housing market data. With the U.S. earnings season winding down, investors are also weighing up the prospect of an interest rate hike in the coming months. Federal Reserve Chair Janet Yellen's speech on Friday at Jackson Hole will be scrutinized for clues on the timing of a rate hike, especially after some Fed policymakers have in recent days hinted at the possibility of a hike in the coming months.

Most of Dow stocks in positive area (23 of 30). Top gainer - American Express Company (AXP, +1.10%). Top loser - The Boeing Company (BA, -0.89%).

All S&P sectors in positive area. Top gainer - Basic Materials (+0.9%).

At the moment:

Dow 18551.00 +32.00 +0.17%

S&P 500 2188.75 +7.25 +0.33%

Nasdaq 100 4827.75 +16.00 +0.33%

Oil 47.97 +0.56 +1.18%

Gold 1342.70 -0.70 -0.05%

U.S. 10yr 1.55 +0.01

-

17:41

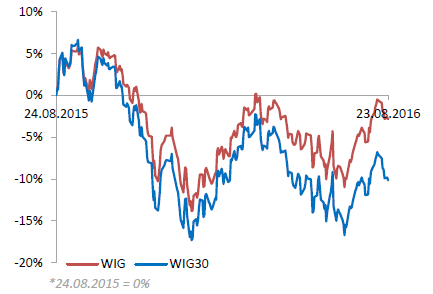

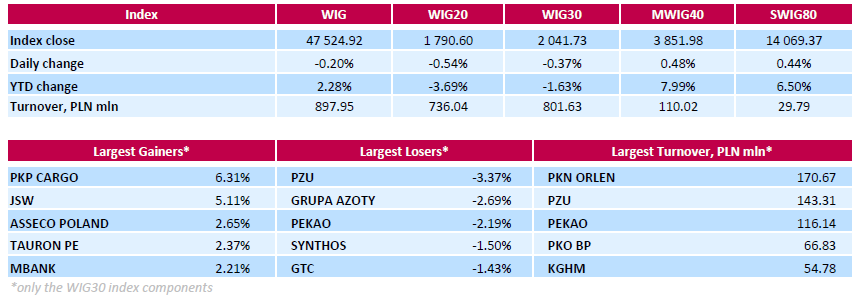

WSE: Session Results

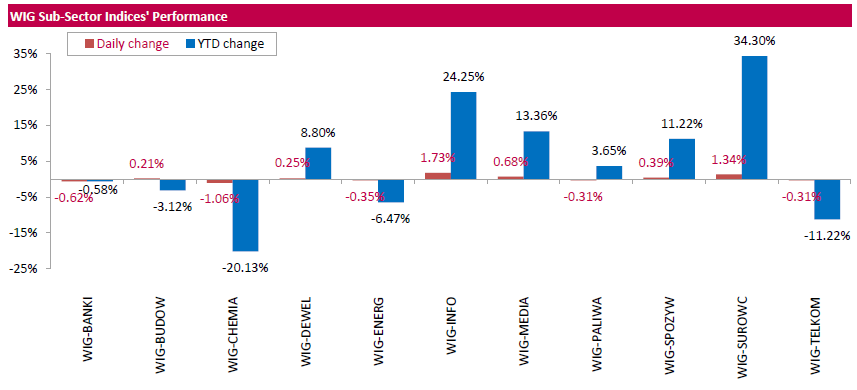

Polish equity market closed lower on Tuesday. The broad market benchmark, the WIG Index, lost 0.20%. Sector performance in the WIG Index was mixed. Chemicals (-1.06%) recorded the biggest decline, while information technology (+1.73%) fared the best.

The large-cap stocks fell by 0.37%, as measured by the WIG30 Index. Within the index components, insurer PZU (WSE: PZU) and bank PEKAO (WSE: PEO) were among the weakest performers, tumbling by 3.37% and 2.19% respectively, weighted down by the rumors that PZU's chief executive, Michal Krupinski, is to go to Milan this week to discuss a possible purchase of PEKAO from its owner, the Italian bank UniCredit. Other major laggards were property developer GTC (WSE: GTC), two chemicals names SYNTHOS (WSE: SNS) and GRUPA AZOTY (WSE: ATT) as well as two utilities names ENEA (WSE: ENA) and PGE (WSE: PGE), losing between 1.06% and 2.69%. On the plus side, railway freight transport operator PKP CARGO (WSE: PKP) and coking coal miner JSW (WSE: JSW) topped the list of gainers, climbing by 6.31% and 5.11% respectively.

-

15:47

WSE: After start on Wall Street

The situation on the parquets did not change much since noon. Gains of the German DAX still reach 1% and especially not increased. After several hours of extremely poor atmosphere on the Warsaw Stock Exchange, before the start of Wall Street was a chance to improve trading in the first line of companies, mainly due to the slight improvement seen in two of today's outsiders, Bank Pekao and PZU. These values have much place to rebound.

The market on Wall Street opens with expected growth, which reaches 0.35%. That's a pretty big shift as recently presented variability and already missing little to historical records. As we may see the market rather does not believe in the possibility of a rate hike in September.

-

15:33

U.S. Stocks open: Dow +0.45%, Nasdaq +0.42%, S&P +0.40%

-

15:27

Before the bell: S&P futures +0.26%, NASDAQ futures +0.28%

U.S. stock-index futures climbed as investors await housing data and a speech Friday from Federal Reserve Chair Janet Yellen.

Global Stocks:

Nikkei 16,497.36 -100.83 -0.61%

Hang Seng 22,998.93 +1.02 0.00%

Shanghai 3,090.63 +5.83 +0.19%

FTSE 6,874.93 +46.39 +0.68%

CAC 4,425.13 +35.19 +0.80%

DAX 10,594.38 +100.03 +0.95%

Crude $46.91 (-1.05%)

Gold $1347.70 (+0.32%)

-

15:01

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

179.07

0.00(0.00%)

28555

ALCOA INC.

AA

10.37

0.05(0.4845%)

41101

ALTRIA GROUP INC.

MO

66.37

0.03(0.0452%)

365

Amazon.com Inc., NASDAQ

AMZN

762.74

3.26(0.4292%)

8472

American Express Co

AXP

65.36

0.00(0.00%)

181429

AMERICAN INTERNATIONAL GROUP

AIG

58.99

0.00(0.00%)

10140

Apple Inc.

AAPL

108.57

0.06(0.0553%)

48609

AT&T Inc

T

40.92

0.01(0.0244%)

660

Barrick Gold Corporation, NYSE

ABX

20.61

0.22(1.079%)

54249

Boeing Co

BA

134.99

0.00(0.00%)

3609

Caterpillar Inc

CAT

83.59

0.00(0.00%)

12237

Chevron Corp

CVX

101.69

-0.25(-0.2452%)

3057

Cisco Systems Inc

CSCO

30.8

0.17(0.555%)

14344

Citigroup Inc., NYSE

C

46.95

0.29(0.6215%)

17265

Deere & Company, NYSE

DE

88.1

0.14(0.1592%)

5828

E. I. du Pont de Nemours and Co

DD

70.1

0.15(0.2144%)

300

Exxon Mobil Corp

XOM

88.1

0.11(0.125%)

2050

Facebook, Inc.

FB

124.56

0.41(0.3302%)

33378

FedEx Corporation, NYSE

FDX

167.89

0.00(0.00%)

704

Ford Motor Co.

F

12.4

0.04(0.3236%)

4600

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.89

0.06(0.5072%)

29703

General Electric Co

GE

31.37

0.05(0.1596%)

2632

General Motors Company, NYSE

GM

31.81

-0.06(-0.1883%)

455

Goldman Sachs

GS

166.26

0.00(0.00%)

3587

Google Inc.

GOOG

774

1.85(0.2396%)

1636

Hewlett-Packard Co.

HPQ

14.37

0.00(0.00%)

18878

Home Depot Inc

HD

135.75

0.41(0.3029%)

385

HONEYWELL INTERNATIONAL INC.

HON

116.58

0.00(0.00%)

12947

Intel Corp

INTC

35.36

0.00(0.00%)

1294

International Business Machines Co...

IBM

159.81

-0.19(-0.1188%)

305

International Paper Company

IP

46.56

0.00(0.00%)

66947

Johnson & Johnson

JNJ

119.7

0.57(0.4785%)

100

JPMorgan Chase and Co

JPM

66.03

0.23(0.3495%)

8323

McDonald's Corp

MCD

115.95

0.53(0.4592%)

2035

Merck & Co Inc

MRK

63.55

0.00(0.00%)

57633

Microsoft Corp

MSFT

57.8

0.13(0.2254%)

1766

Nike

NKE

58.55

-0.11(-0.1875%)

2200

Pfizer Inc

PFE

35.04

0.20(0.5741%)

3242

Procter & Gamble Co

PG

87.1

0.25(0.2879%)

900

Starbucks Corporation, NASDAQ

SBUX

55.93

0.08(0.1432%)

2685

Tesla Motors, Inc., NASDAQ

TSLA

223.9

0.97(0.4351%)

7336

The Coca-Cola Co

KO

43.85

0.11(0.2515%)

853

Travelers Companies Inc

TRV

116.95

0.00(0.00%)

3632

Twitter, Inc., NYSE

TWTR

18.68

0.13(0.7008%)

110489

United Technologies Corp

UTX

109.19

0.69(0.6359%)

685

UnitedHealth Group Inc

UNH

142.09

0.00(0.00%)

11760

Verizon Communications Inc

VZ

52.4

-0.15(-0.2854%)

108898

Visa

V

80.97

-0.09(-0.111%)

10325

Wal-Mart Stores Inc

WMT

72.99

0.29(0.3989%)

1340

Walt Disney Co

DIS

95.99

0.12(0.1252%)

1833

Yahoo! Inc., NASDAQ

YHOO

42.64

0.12(0.2822%)

15800

Yandex N.V., NASDAQ

YNDX

22.3

0.17(0.7682%)

335

-

14:58

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Yahoo! (YHOO) target raised to $53 from $50 at BofA/Merrill

McDonald's (MCD) initiated with Hold rating at Canaccord Genuity

-

13:09

WSE: Mid session comment

The morning readings of PMI indices for the European market were not much different from the expectations and have been welcomed. It looks that the whole economic area copes well with Brexit, which seems to have no impact on economic growth. The data result in new peaks in Paris and Frankfurt, where increases reach 0.8%.

Unfortunately, this noticeable improvement in sentiment in the world went unnoticed on the Warsaw market and the southern phase of trade coincides with plotting new session lows and further remoteness from the level of 1,800 points. To strongly falling valuation of PZU and Pekao shares joined another critical for the WIG20 index components such as PKO, PKN or PGE.

At a time when the Warsaw Stock Exchange recorded minimums with a fall of about 1 per cent, the Frankfurt DAX improves the session peak rising to the level of 10,600 points, an increase of nearly 1 percent.

Thus it remains firmly established downward trend in the spectrum of blue chips, and in opposition to still better small and medium-sized companies that are trying to take advantage of better global sentiment.

At the halfway point of the session the index WIG20 was at the level of 1,780 points (-1,13%) and with the turnover of PLN 318 mln.

-

09:28

Major stock exchanges trading mixed: FTSE 100 6,863.10 + 4.15 + 0.06%, DAX 10,557.37 + 63.02 + 60%

-

09:16

WSE: After opening

WIG20 index opened at 1793.48 points (-0.38%)*

WIG 47501.33 -0.25%

WIG30 2043.25 -0.29%

mWIG40 3838.17 0.12%

*/ - change to previous close

The WIG20 futures took off 2 points above yesterday's closing and extending the lateral movement that operated during yesterday's trading. This is part of a cosmetic change in the morning, fits the climate in other markets, particularly in Europe, where contracts for major European indices grow at a similar size.

The cash market (the WIG20 index) began moving down by 0.38% to 1,793 points with activity focused on the shares of PZU and Pekao (WSE: PEO), which are expected to lose their values after media speculations about probable transaction. Further transactions resulted in a slight rebound, and after a quarter of an hour the WIG20 index stood at the level of 1,794 points (-0,32%).

-

08:26

Expected positive start of trading on the major stock exchanges in Europe: DAX + 0.4%, CAC40 + 0.3%, FTSE + 0.4%

-

08:25

WSE: Before opening

Yesterday's trading on Wall Street ended neutrally, the S&P500 index ended the session with a modest decline of 0.06%, roughly the same increase in value in the morning we may see on the US index futures. The Japanese Nikkei go down approx. 0.6 per cent due to the stronger yen. In the morning also strengthened euro, suggesting that investors still do not believe that the Federal Reserve will be able to raise interest rates before the presidential election.

This situation may mean a neutral start of trading in Europe and the Warsaw market should begin the session at the well-known level of 1,800 points. In the macro calendar will be announced today the publication of preliminary PMI for European economies. Their impact on the market depends on the possible differences in the levels expected or data from a month ago, although we do not expect in this case any significant reaction.

This morning appeared unofficial information about the sale of the bank Pekao (WSE: PEO). The Reuters agency reported that the president of the PZU Group intends this week to talk with representatives of the Italian UniCredit on the possible purchase of Bank Pekao. There is also information that the Italian UniCredit has already decided that the 40.1-percent stake in Pekao will be put up for sale. Certainly, investors will not be happy, because it means the risk of another supply of shares. Traditionally, any such speculation cause declines in stock prices of Pekao, PZU and Alior (WSE: ALR) - controlled by PZU.

-

07:42

Global Stocks

Europe's main stock benchmark closed slightly higher Monday, with Syngenta helping to lead the way up after clearing a regulatory hurdle in its takeover deal.

Exporters also got a lift from a lower euro, but a drop in oil prices weighed on commodity-related stocks.

The Stoxx Europe 600 SXXP, +0.09% inched up 0.1% to finish at 340.43, stabilizing a little after last week's loss of 1.7%.

U.S. stocks closed mostly lower Monday as oil futures snapped a seven-session win streak to finish sharply in negative territory. Losses in West Texas Intermediate oil trading on the New York Mercantile Exchange for September delivery CLU6, -3.52% pushed the contract down 3% at $47.05 a barrel. The October contract CLV6, -1.35% is now WTI's front-month contract. Energy shares on the S&P 500 followed oil's lead, falling 0.9%--suffering the worst drop among the S&P 500's 10 sectors. Overall, the large-cap benchmark SPX, -0.06% ended about a point lower at 2,182, the Dow Jones Industrial Average DJIA, -0.12% closed off 23 points, or 0.1% , at 18,529, while the Nasdaq Composite Index COMP, +0.12% edged 0.1% higher at 5,244. Thin trading and reluctance to make big bets ahead of a speech from Federal Reserve Chairwoman Janet Yellen in Jackson Hole, Wyo., on Friday, made for muted trading action. In merger news, Pfizer Inc. PFE, -0.40% confirmed plans to buy biotech firm Medivation Inc. MDVN, +19.74% in a deal valued at $14 billion.

Asia shares inched ahead while oil fell for a second session on Tuesday, as investors awaited guidance on whether the Federal Reserve will raise U.S. interest rates this year.

Japan's Nikkei .N225 went the other way and eased 0.2 percent as the yen held firm on the dollar.

A survey of Japanese manufacturing activity showed signs of steadying in August as output rose for the first time in six months, but had little impact on stocks.

-

00:31

Stocks. Daily history for Aug 22’2016:

(index / closing price / change items /% change)

Nikkei 225 16,598.19 +52.37 +0.32%

Shanghai Composite 3,084.76 -23.34 -0.75%

S&P/ASX 200 5,515.06 -11.63 -0.21%

FTSE 100 6,828.54 -30.41 -0.44%

CAC 40 4,389.94 -10.58 -0.24%

Xetra DAX 10,494.35 -50.01 -0.47%

S&P 500 2,182.64 -1.23 -0.06%

Dow Jones Industrial Average 18,529.42 -23.15 -0.12%

S&P/TSX Composite 14,748.19 +60.73 +0.41%

-