Notícias do Mercado

-

22:30

Australia: AiG Performance of Construction Index, March 37.9

-

20:50

Schedule for tomorrow, Friday, April 3, 2020

Time Country Event Period Previous value Forecast 00:30 Australia Retail Sales, M/M February -0.3% 0.4% 01:45 China Markit/Caixin Services PMI March 26.5 07:50 France Services PMI March 52.5 29.0 07:55 Germany Services PMI March 52.5 34.3 08:00 Eurozone Services PMI March 52.6 28.4 08:30 United Kingdom Purchasing Manager Index Services March 53.2 35.7 09:00 Eurozone Retail Sales (MoM) February 0.6% 0.1% 09:00 Eurozone Retail Sales (YoY) February 1.7% 1.7% 12:30 U.S. Manufacturing Payrolls March 15 -20 12:30 U.S. Average workweek March 34.4 34.1 12:30 U.S. Government Payrolls March 45 12:30 U.S. Average hourly earnings March 0.3% 0.2% 12:30 U.S. Labor Force Participation Rate March 63.4% 63.3% 12:30 U.S. Private Nonfarm Payrolls March 228 -163 12:30 U.S. Unemployment Rate March 3.5% 3.8% 12:30 U.S. Nonfarm Payrolls March 273 -100 13:45 U.S. Services PMI March 49.4 39.1 14:00 U.S. ISM Non-Manufacturing March 57.3 44 17:00 U.S. Baker Hughes Oil Rig Count April 624 -

20:01

DJIA +0.84% 21,119.29 +175.78 Nasdaq +0.45% 7,393.63 +33.05 S&P +0.98% 2,494.80 +24.30

-

17:01

European stocks closed: FTSE 100 5,480.22 +25.65 +0.47% DAX 9,570.82 +26.07 +0.27% CAC 40 4,220.96 +13.72 +0.33%

-

16:00

U.S.: Astronomical Initial Jobless Claims – BMO

FXStreet reports that Jennifer Lee, a Senior Economist at BMO Capital Markets Economics, notes that U.S. Initial Jobless Claims soared to an astronomical 6,648,000 in the week of March 28th.

“The number of Americans filing for unemployment hit a record 6.6 mln in the last week of March, which nearly doubled already high estimates. That's an increase of 3.341 mln from the prior week, the second week in a row of 3 mln-plus gains.”

“Note that this is a seasonally adjusted figure; without that adjustment, claims are at 5.82 mln. Regardless, this is ridiculously and absurdly high.”

“This is a brutal report and sets the tone for how ugly the employment picture is going to be. Double-digit jobless rates are here.”

-

15:50

Saudi Arabia calls for urgent OPEC+ meeting to stabilize oil market - state-run Saudi Press Agency (SPA)

-

15:38

-

15:34

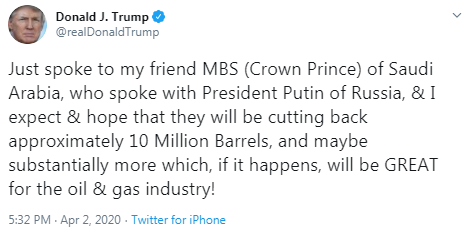

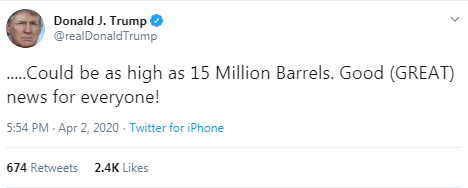

U.S. President Trump told CNBC he expected oil production cut in Saudi Arabia, Russia of 10-15 mbpd

-

15:24

U.S. factory orders unexpectedly unchanged in February

The U.S. Commerce Department reported on Thursday that the value of new factory orders was unchanged m-o-m in February, following an unrevised 0.5 percent m-o-m drop in January.

Economists had forecast a 0.2 percent m-o-m gain.

According to the report, orders for transportation equipment rose 4.6 percent m-o-m in February after a 1.0 percent m-o-m drop in January, while orders for electrical equipment, appliances and components increased 1.3 percent m-o-m in February after a 1.1 drop in the previous month. However, these gains were offset by drops in orders for fabricated metal products (-1.1 percent m-o-m), primary metals (-1.0 percent m-o-m), computers and electronic products (-0.7 percent m-o-m), and machinery (-0.6 percent m-o-m).

Total factory orders excluding transportation, a volatile part of the overall reading, declined 0.9 percent m-o-m in February (compared to a revised 0.4 percent m-o-m growth in January), while orders for nondefense capital goods excluding aircraft, a measure of business spending plans, also dropped 0.9 percent m-o-m, instead of declining 0.8 percent m-o-m as reported last month. The report also showed that shipments of core capital goods decreased 0.8 percent m-o-m in February, rather than dropping 0.7 percent m-o-m as previously reported.

-

15:00

U.S.: Factory Orders , February 0% (forecast 0.2%)

-

14:57

U.S. Initial Jobless Claims: Devastating report – RBC

FXStreet reports that Josh Nye from the Royal Bank of Canada notes that new unemployment insurance claims skyrocketed to 6.65 million last week while current unemployment rate nearing 10%, 2009's high.

“Jobless claims came in well above expectations with another 6.65 million Americans filing for unemployment insurance last week, building on what was already a record 3.31 million claims in the prior week.”

“Those 10 million people represent about 6% of the US labour force, suggesting the current unemployment rate is near the last recession's high water mark of 10%. And layoffs are likely to continue in the coming weeks.”

-

14:44

Canada’s trade deficit narrows in February

Statistics Canada announced on Thursday that Canada's merchandise trade deficit stood at CAD0.98 billion in February, narrowing from a revised CAD1.66 billion gap in January (originally a CAD1.47-billion gap).

Economists had expected a deficit of CAD1.87 billion.

According to the report, the country's exports rose 0.5 percent m-o-m in February, driven by higher exports of aircraft and other transportation equipment and parts (+18.5 percent m-o-m) and motor vehicles and parts (+3.1 percent m-o-m), which more than offset a plunged in exports of energy products (-7.0 percent m-o-m). Meanwhile, imports decreased 0.8 percent m-o-m in February, led by a slump in imports of energy products (-16.0 percent m-o-m), mainly crude oil. However, higher imports of aircraft and other transportation equipment and parts (+27.3 percent m-o-m) moderated the drop in overall imports.

-

14:33

U.S. Stocks open: Dow +0.02%, Nasdaq -0.03%, S&P +0.11%

-

14:27

Before the bell: S&P futures +0.56%, NASDAQ futures +0.28%

U.S. stock-index futures rose modestly on Thursday, giving up early gains, after the release of grim jobless claims data.

Global Stocks:

Index/commodity

Last

Today's Change, points

Today's Change, %

Nikkei

17,818.72

-246.69

-1.37%

Hang Seng

23,280.06

+194.27

+0.84%

Shanghai

2,780.64

+46.12

+1.69%

S&P/ASX

5,154.30

-104.30

-1.98%

FTSE

5,464.97

+10.40

+0.19%

CAC

4,200.89

-6.35

-0.15%

DAX

9,478.39

-66.36

-0.70%

Crude oil

$22.18

+9.21%

Gold

$1,617.40

+1.63%

-

14:02

U.S. trade deficit narrows more than expected in February

The U.S. Commerce Department reported on Thursday that U.S. the goods and services trade deficit narrowed to $39.9 billion in February from a revised $45.5 billion in the previous month (originally a gap of $45.3 billion). This represented the lowest trade gap since September 2016.

Economists had expected a deficit of $40.0 billion.

According to the report, the February decline in the goods and services deficit reflected a decrease in the goods deficit of $5.9 billion to $61.2 billion and a decrease in the services surplus of $0.4 billion to $21.3 billion.

Exports of goods and services from the U.S. fell 0.4 percent m-o-m to $207.5 billion in February, while imports dropped 2.5 percent m-o-m to $247.5 billion.

Year-to-date, the goods and services deficit tumbled 18.7 percent from the same period in 2019. Exports rose 1.1 percent, while imports decreased 3.6 percent.

-

13:58

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

6.32

0.07(1.12%)

47364

3M Co

MMM

133.11

-0.03(-0.02%)

5059

ALTRIA GROUP INC.

MO

37.4

-0.21(-0.56%)

15695

Amazon.com Inc., NASDAQ

AMZN

1,910.12

2.42(0.13%)

39177

American Express Co

AXP

78.01

0.60(0.78%)

33659

AMERICAN INTERNATIONAL GROUP

AIG

21.9

0.29(1.34%)

10879

Apple Inc.

AAPL

241.53

0.62(0.26%)

488925

AT&T Inc

T

28.2

0.15(0.53%)

99537

Boeing Co

BA

131.47

0.77(0.59%)

703293

Caterpillar Inc

CAT

112.88

1.53(1.37%)

6339

Chevron Corp

CVX

72.9

4.34(6.33%)

146468

Cisco Systems Inc

CSCO

38

0.03(0.08%)

118021

Citigroup Inc., NYSE

C

38.45

-0.06(-0.16%)

124682

E. I. du Pont de Nemours and Co

DD

34.4

1.88(5.78%)

1301

Exxon Mobil Corp

XOM

39.3

1.77(4.72%)

488627

Facebook, Inc.

FB

159.71

0.11(0.07%)

90439

FedEx Corporation, NYSE

FDX

114

0.52(0.46%)

4031

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.45

0.14(2.22%)

95957

Ford Motor Co.

F

4.45

0.05(1.14%)

598030

General Electric Co

GE

7.15

0.11(1.56%)

552849

General Motors Company, NYSE

GM

19.3

0.04(0.21%)

27409

Goldman Sachs

GS

145.01

-0.28(-0.19%)

8194

Google Inc.

GOOG

1,111.13

5.51(0.50%)

13027

Hewlett-Packard Co.

HPQ

14.98

0.14(0.94%)

8061

Home Depot Inc

HD

177.26

-1.37(-0.77%)

15940

Intel Corp

INTC

51.57

-0.31(-0.60%)

93176

International Business Machines Co...

IBM

105.24

0.10(0.10%)

15905

Johnson & Johnson

JNJ

129.6

0.79(0.61%)

15224

JPMorgan Chase and Co

JPM

84.81

0.45(0.53%)

152813

McDonald's Corp

MCD

158.83

0.66(0.42%)

15158

Merck & Co Inc

MRK

73.95

0.15(0.20%)

3415

Microsoft Corp

MSFT

152.55

0.44(0.29%)

472581

Nike

NKE

79.4

0.17(0.21%)

128316

Pfizer Inc

PFE

31.95

0.20(0.63%)

12856

Procter & Gamble Co

PG

109.79

0.46(0.42%)

4459

Starbucks Corporation, NASDAQ

SBUX

63.34

0.72(1.15%)

72598

Tesla Motors, Inc., NASDAQ

TSLA

482.96

1.40(0.29%)

294017

The Coca-Cola Co

KO

42.36

0.24(0.57%)

55824

Travelers Companies Inc

TRV

95.7

0.50(0.53%)

1226

Twitter, Inc., NYSE

TWTR

23.5

0.18(0.77%)

63417

United Technologies Corp

UTX

91.01

-0.36(-0.39%)

4289

UnitedHealth Group Inc

UNH

237

-0.32(-0.13%)

5242

Verizon Communications Inc

VZ

53.02

0.10(0.19%)

18887

Visa

V

153.7

0.59(0.39%)

30622

Wal-Mart Stores Inc

WMT

114.25

0.11(0.10%)

11099

Walt Disney Co

DIS

95.5

0.58(0.61%)

238313

Yandex N.V., NASDAQ

YNDX

32.99

0.56(1.73%)

1701

-

13:51

Downgrades before the market open

Lyft (LYFT) downgraded to Neutral from Outperform at Daiwa Securities; target lowered to $28

Walt Disney (DIS) downgraded to Neutral from Buy at Guggenheim

-

13:51

Upgrades before the market open

Travelers (TRV) upgraded to Mkt Perform from Underperform at Keefe Bruyette

Walt Disney (DIS) upgraded to Overweight from Neutral at Atlantic Equities; target lowered to $119

-

13:41

U.S. weekly jobless claims jump much more than forecast

The data from the Labor Department revealed on Thursday the number of applications for unemployment benefits soared much more than forecast last week as a sudden shutdown of businesses across the country as a part of social distancing policies aimed at keeping the coronavirus from spreading caused a cascade of joblessness.

According to the report, the initial claims for unemployment benefits climbed to a seasonally adjusted 6,648,000 for the week ended March 28. That was the highest reading on record.

Economists had expected 3,500,000 new claims last week.

Claims for the prior week remained unchanged at 3,283,000.

Meanwhile, the four-week moving average of claims climbed by 327,250 to 2,054,054.

-

13:30

U.S.: Continuing Jobless Claims, March 3029 (forecast 4882)

-

13:30

Canada: Trade balance, billions, February -0.98 (forecast -1.87)

-

13:30

U.S.: Initial Jobless Claims, March 6648 (forecast 3500)

-

13:30

U.S.: International Trade, bln, February -39.9 (forecast -40)

-

13:19

Fitch Ratings': Deep global recession in 2020 is now baseline forecast - Reuters reports

- Sees world economic activity to decline by 1.9% in 2020

- Sees world economic activity to decline by 1.9% in 2020

-

13:15

USD/JPY: Falling further going forward – MUFG

FXStreet notes that the global COVID crisis is set to keep the yen well supported. With yields in the US set to drop further, economists at MUFG Bank see USD/JPY falling further going forward.

“The main focus of the BoJ will likely remain upping purchases of ETFs. On four occasions in March, the BoJ purchased a record JPY 201.6bn worth of ETFs.”

“PM Abe indicated that he was going to act with another fiscal stimulus package to be announced in April. This would include cash handouts and protection for companies to help maintain employment.”

“USD hedging costs are set to decline going forward as Fed monetary policy and liquidity injections drive US yields further lower, this will encourage greater hedged outflows from Japan that will remove one element of support for USD/JPY and help push the rate lower.”

-

13:13

Company News: Walgreens Boots Alliance (WBA) quarterly results beat analysts’ expectations

Walgreens Boots Alliance (WBA) reported Q2 FY 2020 earnings of $1.52 per share (versus $1.64 per share in Q2 FY 2019), beating analysts' consensus estimate of $1.46 per share.

The company's quarterly revenues amounted to $35.820 bln (+3.7% y/y), beating analysts' consensus estimate of $35.245 bln.

The company also said it would continue to closely assess the COVID-19 situation and would provide further updates in the next earnings report when both the potential positive and negative effects of the pandemic would be known in more detail.

WBA rose to $44.95 (+4.46%) in pre-market trading.

-

13:00

GBP/USD: A more stable global backdrop should allow a rebound – Westpac

FXStreet notes that the scale of the UK's support packages should offset the negative of the UK's trade balance pressures. A more stable global backdrop should also allow GBP/USD to rebound, in the opinion of economists at Westpac Institutional Bank.

“The UK Government raising its contingency funds to GBP266bn suggests that it is preparing for more.”

“Open-ended Fed QE, diminished USD yield support and a much less-compelling US growth advantage should weigh on USD prospects.”

“GBP/USD may be volatile but is likely to remain within a 1.20-1.25 range unless risk aversion causes another rush of USD demand.”

-

12:51

European session review: CAD strengthens against most major rivals as oil climbs 10%

Time Country Event Period Previous value Forecast Actual 06:00 United Kingdom Nationwide house price index March 0.3% -0.1% 0.8% 06:00 United Kingdom Nationwide house price index, y/y March 2.3% 2% 3% 06:30 Switzerland Consumer Price Index (MoM) March 0.1% 0.1% 0.1% 06:30 Switzerland Consumer Price Index (YoY) March -0.1% -0.5% -0.5% 09:00 Eurozone Producer Price Index, MoM February 0.2% -0.2% -0.6% 09:00 Eurozone Producer Price Index (YoY) February -0.7% -0.7% -1.3% CAD appreciated against most other major currencies in the European session on Thursday, supported by a 10% rebound in oil prices. The loonie rose against USD, EUR, JPY, and CHF, but it fell against GBP and AUD. The Canadian dollar is heavily dependent on the dynamics of the price of crude oil, one of Canada's key exports.

The U.S. West Texas Intermediate (WTI) crude futures climbed 10% on Thursday after the U.S. President Donald Trump said that he expected that Saudi Arabia and Russia could end their oil price war soon.

Speaking at a White House news conference on Wednesday, Trump said that he had talked recently with both countries' leaders and believed the nations would strike a deal to end their price war within a "few days".

"It's very bad for Russia, it's very bad for Saudi Arabia. I mean, it's very bad for both. I think they're going to make a deal", the U.S. president said.

Market participants also continued to assess the latest news on the coronavirus. According to data, compiled by Johns Hopkins University, the total number of global cases now stands at 951,901. With 9,731 confirmed coronavirus cases, Canada is ranked 15th in the list of the countries with confirmed COVID-19 cases.

-

12:21

USD/CNY: Expected to reach 7.15 on a three-month horizon – Nordea

FXStreet reports that Amy Yuan Zhuang from Nordea thinks that elevated uncertainty about COVID-19 as well as its impacts on the global economy will likely keep weakening pressure on the yuan against the dollar, as capital is flowing to safe-haven assets.

“In the near-term, the direction of USD/CNY will be dictated more by global risk sentiment than the domestic development in China.”

“We revise our USD/CNY forecasts and expect the pair to reach 7.15 on a three-month horizon. Nevertheless, our new USD/CNY forecasts do not match our new GDP forecasts in bearishness because we think the PBoC will continue to be the last line of defence for the CNY.”

“The PBoC has been intervening through verbal support and a stronger daily fixing rate, which we expect it to continue as long as weakening pressure persists.”

-

11:57

AUD/USD: Risking a return to 0.58-0.59 – Westpac

FXStreet reports that analysts at Westpac Institutional Bank suggest that AUD/USD is set to remain prey to global risk sentiment, occasionally probing 0.6150/70 but overall biased back towards 0.58 multi-week.

“Australia’s proposed JobKeeper Payment is a radical plan befitting an extraordinary hit to the economy. The government should save a large number of jobs and limit the contraction in GDP.”

“We expect a shocking -8.5% fall in output in Q2, even as the much-pledged return to surplus becomes a deficit of -5% of GDP in the year to June, blowing out to -10.5% in 2020/21, the largest deficit since WW2.”

“AUD/USD’s bounce extended further than we expected, touching 0.62. Yet our bias is unchanged, looking for rallies to the 0.61 handle to fail, risking a return to 0.58-0.59 initially.”

-

11:55

ECB extends review of its monetary policy strategy until mid-2021

"The Governing Council of the European Central Bank (ECB) has decided to extend the timeline for the review of its monetary policy strategy. In the current situation, the decision-making bodies and staff of the ECB and the national central banks of the Eurosystem are focusing all their efforts on addressing the challenges posed by the coronavirus pandemic. The conclusion of the strategy review will therefore be postponed from the end of 2020 to mid-2021", the ECB said in its press release.

-

11:37

U.S.: Initial jobless claims to remain historically high – TDS

FXStreet notes that U.S. initial jobless claims will offer another update on the US labour market after last week's record-breaking print. Analysts at TD Securities expect a higher number for this week.

“We caution against extrapolating indefinitely but jobless claims are likely to remain historically high for at least a few weeks as the impact of COVID-19 shutdowns is reflected in the data.”

“Last week's 3.283mn figure was more than four times the previous all-time high, 695K in 1982. The high in the 2008-09 recession was 665K.”

“We are projecting an even higher number for this week at 4.3mn but caution it could be even higher. The consensus is looking for a lower number at 3.6mn.”

-

11:23

U.S. Initial Jobless Claims: A reading well above 3 million seems unavoidable – Nordea

FXStreet reports that analysts at Nordea provide an overview of what to expect from upcoming US initial jobless claims.

“In terms of today’s initial claims number, consensus is at 3.5 million which is even higher than last week.”

“A reading well above 3 million seems unavoidable and we see a highly asymmetric risk picture that leans towards a much higher number than consensus.”

“Looking further ahead, we expect initial claims to drop materially, although remain at historically high levels. A drop by 25-50% in each of the coming few weeks could be on the cards, leaving the total number of claims until the April Establishment Survey around 7.5-11 million with much depending on today’s number.”

-

11:20

Japan finance ministry: Market participants reaffirm they can absorb JPY16 trillion extra Japanese government bonds to fund stimulus package

-

11:15

Spain: Confirmed coronavirus cases rose by 8,102, or 7.9%, to 110,238 on Thursday from 102,136 on Wednesday

The total number of virus-related deaths climbed by 950, or 10.5%, to 10,003 from 9,053 on Wednesdy. That set a new daily record in coronavirus-related fatalities in Spain.

-

10:58

Canada: Overwhelmingly focused on income support for workers – RBC

FXStreet reports that Ottawa pledges $71 billion to pay 75% of wages up to $847 per week for workers in hard-hit industries. Canadian Minister Morneau confirmed details of the proposed subsidy, Colin Guldimann from the Royal Bank of Canada reports.

"The Government pledged $71 billion (3.1% of GDP) to help businesses of all sizes who suffer revenue drops of 30% or more relative to this time last year. The subsidy will cover 75% of a worker's pre-COVID earnings for up to 12 weeks, up to a maximum of about $10,000 per worker."

"These measures bring the federal government's direct support for the economy to about $105 billion (4.6% of GDP), overwhelmingly focused on income support for workers (totaling $95 billion)."

"Our overall view of the deficit for the 2020/2021 fiscal year now tracks at a whopping $170 billion (7.4% of GDP)."

-

10:39

China says to ease car buying curbs to boost sales

Reuters reports that China's commerce ministry will relax or remove restrictions on car purchases in some regions to help sales of new vehicles, while accelerating plans to boost the scrapping of old ones.

Wang Bin, the deputy head of the ministry's consumption promotion division, said the ministry will continue to help "realize the consumption potential" in the world's largest auto market, during a weekly briefing held online on Thursday.

China's auto industry suffered a 79% drop in sales in February and expects a fall of around 10% in the first half of this year.

While the coronavirus outbreak has been mostly contained at home, Liu Changyu, another senior commerce ministry official, said, its spread overseas will inevitably impact China's auto trade and its supply chain.

The ministry will therefore guide Chinese automakers to expand orders from overseas suppliers, stock up on inventory and make alternative plans, Liu said.

-

10:19

Eurozone industrial producer prices fell more than expected in February

According to the report from Eurostat, in February 2020, - the month before COVID-19 containment measures began to be widely introduced by Member States -, industrial producer prices decreased by 0.6% in both the euro area and the EU, compared with January 2020. Economists had expected a 0.2% decrease. In January 2020, prices increased by 0.2% in both the euro area and the EU.

In February 2020, compared with February 2019, industrial producer prices decreased by 1.3% in the euro area and by 1.0% in the EU. Economists had expected a 0.7% decrease.

Industrial producer prices in the euro area in February 2020, compared with January 2020, decreased by 2.3% in the energy sector and by 0.2% for intermediate goods, while prices rose by 0.1% for capital goods and by 0.2% for durable consumer goods and for non durable consumer goods. Prices in total industry excluding energy remained stable.

In the EU, industrial producer prices decreased by 2.4% in the energy sector and by 0.2% for intermediate goods, while prices rose by 0.1% for capital goods and for non-durable consumer goods and by 0.3% for durable consumer goods. Prices in total industry excluding energy remained stable.

-

10:07

European commissioner for the economy Gentiloni: Each month of lockdown causes 3% annual GDP slump

-

There's no discussion about an Italian bailout

-

-

10:00

Eurozone: Producer Price Index (YoY), February -1.3% (forecast -0.7%)

-

10:00

Eurozone: Producer Price Index, MoM , February -0.6% (forecast -0.2%)

-

09:40

China: Economy remains challenging despite signs of recovery – HSBC

FXStreet reports that against the backdrop of a sharp near-term slowdown in economic activity in January-February, investor focus is now on the pace at which China's economy can return to normal, economists at HSBC brief.

"Chinese policymakers have responded to the COVID-19 through mostly short-term, emergency and targeted fiscal and credit (relief) policies, as well as monetary easing. More policy support is expected to boost demand as supply-side disruptions may gradually ease."

"Faster work resumption coupled with relaxation in containment measures and intensified macro policy support should allow for a sequential activity recovery in March vs. February, though the overall growth likely remains subdued in March and Q1 is on track to show contraction."

"Even after assuming growth normalisation in April/Q2 and a further rebound in the second half of the year, the recovery is likely to be insufficient to fully offset the large negative shock in Q1. This coupled with increased risk of a global recession could result in significantly lower annual growth than 2019's 6.2%."

-

09:21

EUR/JPY: Attention has reverted to the 115.87 key September low – Commerzbank

FXStreet reports that EUR/JPY's outlook stays negative, in the opinion of Karen Jones, Team Head FICC Technical Analysis Research at Commerzbank.

"EUR/JPY has again recently failed ahead of the 121.38/47 October and February highs."

"It has eroded the 118.10 2nd March low and attention has reverted to the 115.87 key September low."

"The 61.8% retracement of the move from 2012 lies at 115.38 and only below here does the chart picture really start to deteriorate further and target the 109.30 2016 low."

-

08:59

Coronavirus epicenter could "possibly" shift back to Asia - public health expert

CNBC reports that the epicenter of the coronavirus outbreak is at risk of shifting constantly, posing challenges to public health systems, a health expert said.

"The epicenters will shift constantly," said Teo Yik Ying, dean at the Saw Swee Hock School of Public Health at the National University of Singapore.

Although the U.S. is now seen as the epicenter of the outbreak with cases surpassing 200,000 - "in a month's time, the epicenter will shift," Teo told CNBC.

"Would it shift to South Asia? Would it shift to Africa or Latin America? We don't know at the moment, but there is that real risk that the epicenters will continue to shift, and it could possibly even shift back to East Asia," Teo said.

China has seen more and more cases being imported from overseas, prompting the government there to close its border to foreigners.

A similar trend is also being observed in Singapore, which is witnessing another wave of infections brought in by sick residents returning from overseas.

"This is really the fear for what will be seeding the second wave, that countries that are still suffering the brunt of the coronavirus infection will be exporting people with the virus," said Teo, who emphasized international coordination in managing the pandemic.

The epicenter could continue shifting until people develop herd immunity, said Teo.

Until there is a viable vaccine, it is important to spread out the epidemic to allow time for the healthcare system to recover, said Teo.

-

08:40

Coronavirus: US deaths surpass 5,000 as global infections top 930,000

-

CNBC reports that as many as 937,783 cases of coronavirus infection have been recorded around the world and at least 47,261 people have died, according to the latest information compiled by Johns Hopkins University.

-

Singapore now has 1,000 recorded instances of COVID-19 infection due to an influx of "imported" cases as more residents returned from abroad.

-

Total deaths in the U.S. related to the coronavirus reached 5,138, according to data compiled by Johns Hopkins University. New York City recorded the highest number of fatalities at 1,374, the data showed.

-

China's National Health Commission (NHC) said there were 35 new cases as of April 1, all of which were "imported" from other countries.

-

Global cases: More than 937,783

-

Global deaths: At least 47,261

-

Top 5 countries: United States (216,721), Italy (110,574), Spain (104,118), China (82,394), and Germany (77,981)

-

-

08:40

USD/CNH: A test of 7.1700 loses momentum – UOB

FXStreet reports that in opinion of FX Strategists at UOB Group, prospects for USD/CNH to visit the 7.1700 region appear to have lost traction as of late.

24-hour view: "Our expectation for USD to 'dip towards 7.0650' was wrong as it rose to 7.1333 before ending the day on a firm note at 7.1227 (+0.41%). Upward momentum has picked up and from here, USD is expected to extend its advance but last month's peak at 7.1652 is likely out of reach. Support is at 7.1000 followed by 7.0800."

Next 1-3 weeks: "As highlighted, the chance for USD to break above 7.1700 has diminished. However, only a breach of 7.0450 ('strong support' level previously at 7.0350) would indicate that the current upward pressure has eased. Looking ahead, a break of 7.0450 would suggest USD could spend trade in a broad range for a period."

-

08:39

China commerce ministry says production of auto, auto parts has fully resumed

-

08:19

USD: Why the March jobs report is already outdated before it is released - Danske

eFXdata reports that Danske Research discusses why this Friday's jobs report might not be of that significance for market direction given that it's inputs are already outdated.

"Normally, the US jobs report is considered perhaps the most important economic indicator, but the jobs report for March due out on Friday is already outdated before it is released. We know from initial jobless claims that there was a record spike of 3.3m in the number of jobless claims two weeks ago but this will not be reflected in the March jobs report. To understand this, one should look into the technical notes on how the jobs report is made. The jobs report is based on the pay period covering the 12 th of the month, which is before the US really started to lock down. In this week, initial jobless claims 'only' rose by 60-70,000 more than a 'normal' week before the coronacrisis. If you had a paid job in this week, you are counted as having a job, regardless of what happened later in the month," Danske notes.

We are likely to continue to see layoffs in coming weeks, as long as the US economy remains locked down, and hence the jobs report for April will be extremely negative. If claims have risen by another 3.5m, the April jobs report will show a decline in employment of at least 7m but, unfortunately, probably more. As the jobs report is already outdated, we do not expect it to be a major market mover this week. As mentioned, the focus is instead on the initial jobless claims due out tomorrow, Thursday"

-

07:59

Asian session review: the US dollar rose against the euro and yen

During today's Asian trading, the US dollar strengthened against the euro and the yen. Waves of uncertainty in various markets, including stocks and oil, increase demand for safe haven assets, which continues to support the US currency, experts say.

A drop in the US equity market on Wednesday, a decline in manufacturing activity indices in the US and several other countries, as well as a continuing increase in the number of deaths from coronavirus in the US, support demand for the dollar and other assets considered the most reliable.

US President Donald Trump said earlier this week that the States will have to overcome "an agonizing two weeks" in the fight against the COVID-19 coronavirus infection before a trend of improvement can be seen. "I would like to hope that, as experts predict and as many of US predict, we will see the real light at the end of the tunnel, but this is preceded by a very, very painful two weeks," Trump said at a briefing on the coronavirus at the White house.

He noted that to improve the situation with coronavirus, it is necessary to adhere to the guidelines for combating COVID-19, calling compliance with these measures "a matter of life and death".

Meanwhile, according to the Institute for supply management (ISM), the index of business activity in the US manufacturing sector in March fell to 49.1 points from 50.1 points a month earlier. A drop in the index below 50 points indicates a decline in activity in the American industry in the context of the coronavirus pandemic.

-

07:45

Swiss consumer price Index increased by 0.1% in March

According to the report from Federal Statistical Office, the consumer price index (CPI) increased by 0.1% in March 2020 compared with the previous month, reaching 101.7 points (December 2015 = 100). Inflation was -0.5% compared with the same month of the previous year.

The 0.1% increase compared with the previous month can be explained by several factors including rising prices for clothing and footwear due to the end of the seasonal sales. New cars also recorded a price increase, as did beef. In contrast, prices for heating oil and fuels decreased.

In March 2020, the Swiss Harmonised Index of Consumer Prices (HICP) stood at 100.78 points (base 2015=100). This corresponds to a rate of change of +0.1% compared with the previous month and of -0.4% compared with the same month the previous year.

The HICP is a supplementary indicator for inflation based on a harmonised method across EU member countries. It enables inflation in Switzerland to be compared with that of European countries.

-

07:30

Switzerland: Consumer Price Index (YoY), March -0.5% (forecast -0.5%)

-

07:30

Switzerland: Consumer Price Index (MoM) , March 0.1% (forecast 0.1%)

-

07:16

UK annual house price growth edged higher in March - Nationwide

According to the report from Nationwide Building Society, prices rose 0.8% in March, after taking account of seasonal factors. The sample period excludes recent COVID-19 related disruption.

Annual house price growth increased to 3% in March, up from 2.3% the previous month - - the fastest pace since January 2018 (when annual growth was 3.2%). The last six months have all seen month on-month increases, after taking account of seasonal effects.

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said: "Annual house price growth increased to 3% in March. In the opening months of 2020, before the pandemic struck the UK, the housing market had been steadily gathering momentum. Activity levels and price growth were edging up thanks to continued robust labour market conditions, low borrowing costs and a more stable political backdrop following the general election. But housing market activity is now grinding to a halt as a result of the measures implemented to control the spread of the virus, and where the government has recommended not entering into housing transactions during this period"

-

07:01

United Kingdom: Nationwide house price index , March 0.8% (forecast -0.1%)

-

07:01

United Kingdom: Nationwide house price index, y/y, March 3% (forecast 2%)

-

06:57

Options levels on thursday, April 2, 2020

EUR/USD

Resistance levels (open interest**, contracts)

$1.1105 (2602)

$1.1061 (1481)

$1.1023 (4149)

Price at time of writing this review: $1.0943

Support levels (open interest**, contracts):

$1.0912 (3075)

$1.0880 (2035)

$1.0840 (1793)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date April, 3 is 87181 contracts (according to data from April, 1) with the maximum number of contracts with strike price $1,1000 (4149);

GBP/USD

Resistance levels (open interest**, contracts)

$1.2656 (373)

$1.2565 (367)

$1.2487 (605)

Price at time of writing this review: $1.2402

Support levels (open interest**, contracts):

$1.2327 (398)

$1.2300 (203)

$1.2217 (195)

Comments:

- Overall open interest on the CALL options with the expiration date April, 3 is 19411 contracts, with the maximum number of contracts with strike price $1,3200 (2376);

- Overall open interest on the PUT options with the expiration date April, 3 is 21936 contracts, with the maximum number of contracts with strike price $1,2900 (2837);

- The ratio of PUT/CALL was 1.13 versus 1.19 from the previous trading day according to data from April, 1

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

03:30

Commodities. Daily history for Wednesday, April 1, 2020

Raw materials Closed Change, % Brent 23.18 0.61 WTI 19.91 8.03 Silver 13.93 0.07 Gold 1591.84 1.06 Palladium 2217.17 -4.71 -

01:30

Stocks. Daily history for Wednesday, April 1, 2020

Index Change, points Closed Change, % NIKKEI 225 -851.6 18065.41 -4.5 Hang Seng -517.69 23085.79 -2.19 KOSPI -69.18 1685.46 -3.94 ASX 200 181.8 5258.6 3.58 FTSE 100 -217.39 5454.57 -3.83 DAX -391.09 9544.75 -3.94 CAC 40 -188.88 4207.24 -4.3 Dow Jones -973.65 20943.51 -4.44 S&P 500 -114.09 2470.5 -4.41 NASDAQ Composite -339.52 7360.58 -4.41 -

01:30

Schedule for today, Friday, April 3, 2020

Time Country Event Period Previous value Forecast 00:30 Australia Retail Sales, M/M February -0.3% 0.4% 01:45 China Markit/Caixin Services PMI March 26.5 07:50 France Services PMI March 52.5 29.0 07:55 Germany Services PMI March 52.5 34.3 08:00 Eurozone Services PMI March 52.6 28.4 08:30 United Kingdom Purchasing Manager Index Services March 53.2 35.7 09:00 Eurozone Retail Sales (MoM) February 0.6% 0.1% 09:00 Eurozone Retail Sales (YoY) February 1.7% 1.7% 12:30 U.S. Manufacturing Payrolls March 15 -20 12:30 U.S. Average workweek March 34.4 34.1 12:30 U.S. Government Payrolls March 45 12:30 U.S. Average hourly earnings March 0.3% 0.2% 12:30 U.S. Labor Force Participation Rate March 63.4% 63.3% 12:30 U.S. Private Nonfarm Payrolls March 228 -163 12:30 U.S. Unemployment Rate March 3.5% 3.8% 12:30 U.S. Nonfarm Payrolls March 273 -100 13:45 U.S. Services PMI March 49.4 39.1 14:00 U.S. ISM Non-Manufacturing March 57.3 44 17:00 U.S. Baker Hughes Oil Rig Count April 624 -

01:15

Currencies. Daily history for Wednesday, April 1, 2020

Pare Closed Change, % AUDUSD 0.60667 -1.45 EURJPY 117.189 -1.12 EURUSD 1.09435 -0.76 GBPJPY 132.669 -0.64 GBPUSD 1.23857 -0.27 NZDUSD 0.59087 -1.04 USDCAD 1.41823 0.82 USDCHF 0.96536 0.55 USDJPY 107.093 -0.35 -