Notícias do Mercado

-

20:00

Dow 15,031.48 -101.66 -0.67%, Nasdaq 3,778.50 -36.52 -0.96%, S&P 500 1,681.88 -11.99 -0.71%

-

18:19

European stocks close

European stocks declined for a second day, as a shutdown of the U.S. government continued and a gauge of service-industry activity in the world’s biggest economy fell more than forecast.

U.S. President Barack Obama and congressional leaders yesterday failed to break a budget impasse in their first face-to-face negotiations since the government began its first partial shutdown in 17 years on Oct. 1. The standoff raises concern the budget dispute may affect talks to increase the $16.7 trillion debt ceiling by Oct. 17 so as to avoid a default.

The Institute for Supply Management’s U.S. non-manufacturing index fell to 54.4 in September from 58.6 the prior month, the Tempe, Arizona-based group said today. The median forecast in a Bloomberg survey called for a drop to 57. Estimates of the 75 economists ranged from 55 to 59.

National benchmark indexes retreated in 14 of the 18 western European markets. The U.K’s FTSE 100 added 0.2 percent, while France’s CAC 40 fell 0.7 percent. Germany’s DAX fell 0.4 percent, with the volume of shares traded 46 percent lower than the 30-day average as many businesses closed for the Unity Day holiday.

Gerresheimer declined 2 percent to 44.68 euros. Credit Suisse downgraded the producer of pharmaceutical and health-care equipment to neutral from outperform, similar to buy, saying the shares are nearing the brokerage’s 12-month price estimate of 46 euros. Gerresheimer closed at 45.60 euros yesterday.

Aviva climbed 1.4 percent to 413.1 pence after saying the sale of its U.S. life-insurance and annuities business to Apollo Global Management LLC’s Athene Holding Ltd. generated proceeds of $2.6 billion, higher than the $1.8 billion purchase price disclosed in December. Earnings and other improvements in the U.S. company’s surplus increased the value, Aviva said.

BP advanced 1.1 percent to 437.15 pence as the U.S. Court of Appeals asked District Judge Carl Barbier to review his interpretation of some of the terms of a settlement reached with spill victims’ lawyers in 2012.

-

17:00

European stocks closed in different ways: FTSE 100 6,449.04 +11.54 +0.18%, CAC 40 4,127.98 -30.18 -0.73%, DAX 8,597.91 -31.51 -0.37%

-

16:40

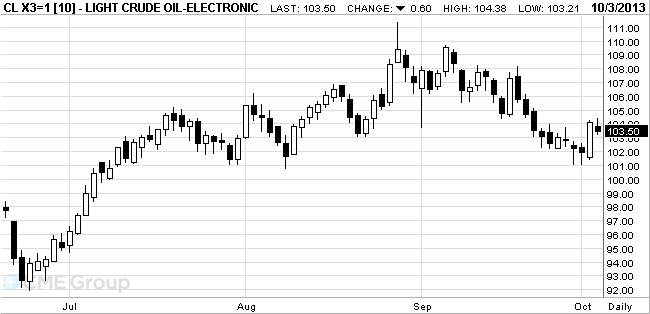

Oil fell

West Texas Intermediate fell from its highest settlement in almost two weeks as the

Futures slid as much as 0.6 percent in

WTI for November delivery dropped as much as 65 cents to $103.45 a barrel in electronic trading on the New York Mercantile Exchange. It was at $103.69 as of 1:22 p.m.

Brent for November settlement fell as much as 49 cents, or 0.5 percent, to $108.70 a barrel on the London-based ICE Futures Europe exchange. The European benchmark was at a premium of $5.82 to WTI, up from $5.09 yesterday, the least since Sept. 23.

-

16:20

Gold fell

Gold prices decline on weak economic performance and closing the U.S. Government .

From the beginning, gold fell by almost 25 percent due to concerns that the Fed this year will decline in buying bonds. Before you start reducing the incentives , the Fed need to get the October economic data , said the president of the Federal Reserve Bank of Boston , Eric Rosengren . But many federal agencies have suspended the collection and publication of data due to the termination of funding .

Markets are worried about the outcome of the upcoming negotiations in mid-October to raise the upper limit of borrowing dollars. According to analysts, if the politicians fail to agree on raising the debt ceiling , the world 's largest economy could default that will hurt global growth .

Activity in the U.S. non-manufacturing sector grew in September , but at a much slower pace than expected . Employment growth also slowed. This is according to data released on Thursday by the Institute for Supply Management (ISM). Reported Purchasing Managers Index (PMI) for the non-production sphere of the United States in September fell to 54.4 from 58.6 in August. The August index was the highest since January 2008 , when the index was introduced . Economists expected the index to decline only in September to 57.2 . A reading above 50 indicates expanding activity .

Stocks of the world's largest exchange-traded fund backed by gold (ETF) SPDR Gold Trust on Wednesday declined by 4.2 tons to 901.79 tons, which was the sharpest decline in nearly three weeks .

Physical demand remains depressed due to a national holiday in China. Chinese markets will resume work on October 8.

The cost of the December gold futures on COMEX today dropped to $ 1302.00 per ounce.

-

15:00

U.S.: ISM Non-Manufacturing, September 54.4 (forecast 57.2)

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.3475, $1.3500, $1.3530, $1.3550, $1.3600, $1.3660

GBP/USD $1.6170, $1.6175, $1.6200, $1.6350

USD/JPY Y97.25, Y97.50, Y98.20, Y98.25, Y98.80, Y99.00, Y99.10, Y99.15, Y99.25, Y99.50, Y99.70, Y100.00

AUD/USD $0.9280, $0.9350, $0.9365, $0.9400, $0.9450, $0.9465

EUR/CHF Chf1.2225, Chf1.2280, Chf1.2300

EUR/GBP stg0.8290, stg0.8350

EUR/AUD A$1.4490

-

13:30

U.S.: Initial Jobless Claims, September 308 (forecast 315)

-

13:16

European session: The yen fell against the dollar

Data

00:00 China Bank holiday

01:00 China Non-Manufacturing PMI September 53.9 55.4

06:00 Germany Bank holiday

07:00 United Kingdom Halifax house price index September +0.4% +0.6% +0.3%

07:00 United Kingdom Halifax house price index 3m Y/Y September +5.4% +6.2%

07:48 France Services PMI (Finally) September 50.7 50.7 50.5

07:53 Germany Services PMI (Finally) September 54.4 54.4 53.7

07:58 Eurozone Services PMI (Finally) September 52.1 52.1 52.2

08:30 United Kingdom Purchasing Manager Index Services September 60.5 60.4 60.3

09:00 Eurozone Retail Sales (YoY) August -0.7% Revised From -1.3% -1.5% -0.3%

09:00 Eurozone Retail Sales (MoM) August +0.5% Revised From +0.1% +0.3% +0.7%

The euro rose to eight-month high against the dollar , where it continues to trade in a consolidation mode . Note that this dynamics associated with discussions on the extension of stopping the U.S. government. This fact will lead to slower economic growth in the country and can serve as a signal for a possible expansion of quantitative easing program , which will undoubtedly have a negative impact on the U.S. currency . Yesterday, after a meeting of congressional leaders with President Barack Obama, House Speaker John Boehner said that the progress in the negotiations to address the financial impasse has been reached . U.S. lawmakers also need to negotiate with the White House to raise the debt limit . Otherwise, the 17 October, the U.S. will default .

Earlier in the European session the pair hardly reacted to the positive data on the services PMI eurozone and the strong performance in retail sales in the region.

Add that to the course of trade is also affected by expectations of American publishing data on the number of applications for unemployment benefits . It is expected that this indicator will rise to the level of 315 thousand to 305 thousand additional impact on the dollar can have today's publication of data on the manufacturing index from the Institute for Supply Management (ISM). According to the median forecast of economists , the index for September is likely to fall to 57 from 58.6 a month earlier. Recall that the value is above the 50 level punknogo points to economic growth.

The pound fell against the dollar , dropping at the same session to a minimum , due to the expectations of the publication of data on the U.S..

Note that a significant , though not long support the pound had data on activity in the service sector. As it became known , the activity in a key sector of the British economy - the service sector - in September remained near record highs , although it declined to 60.3 from 60.5 in August. Economists expected a decline to 60.4 . Readings above 50.0 indicates expanding activity , while below 50 - the reduction .

The data also showed that the index of activity in all sectors of the economy grew in the 3rd quarter to a 15- year high , which gives reason to expect GDP growth for the quarter of 1.2% , which would be the highest since the start of the global financial crisis.

" Services reported continued growth in September - said Markit chief economist Chris Williamson . - There are encouraging signs that in the coming months will show strong growth . In September was marked by record high increase in new orders. Business confidence about the prospects increased . " . After GDP growth in the first two quarters , we should expect increases in the 3rd quarter .

EUR / USD: during the European session, the pair rose to $ 1.3615

GBP / USD: during the European session, the pair fell to $ 1.6181

USD / JPY: during the European session, the pair rose to Y97.88, then fell to Y97.65

At 12:30 GMT the U.S. will report on changes in initial claims for unemployment insurance . At 14:00 GMT the U.S. will release the ISM composite index of non-manufacturing activity in September , and will report on changes in the volume of industrial orders in August.

-

13:00

Orders

EUR/USD

Offers $1.3720, $1.3700, $1.3660/80, $1.3650

Bids $1.3580, $1.3550, $1.3520, $1.3500

GBP/USD

Offers $1.6320, $1.6300, $1.6280, $1.6270, $1.6250

Bids $1.6185/80, $1.6150, $1.6120, $1.6100

AUD/USD

Offers $0.9500, $0.9480, $0.9457, $0.9450, $0.9425/30

Bids $0.9350, $0.9320, $0.9300, $0.9280, $0.9250

EUR/JPY

Offers Y134.50, Y134.20, Y134.00, Y133.80, Y133.45/50

Bids Y132.50, Y132.20, Y132.00, Y131.50

USD/JPY

Offers Y98.80, Y98.45/50, Y98.20, Y98.06/07

Bids Y97.40, Y97.00, Y96.55/50, Y96.20, Y96.00

EUR/GBP

Offers stg0.8500, stg0.8480, stg0.8450, stg0.8420

Bids stg0.8350, stg0.8335/30, stg0.8320, stg0.8300, stg0.8280

-

11:30

Major stock indexes in Europe traded almost unchanged

European stocks were little changed , after yesterday showed the largest decline over the month , due to the shutdown of the U.S. government , as well as the publication of data on China's non-manufacturing sector .

According to the report, the Purchasing Managers Index for non-manufacturing areas of China, which includes the service sector and construction industry , rose in September to the level of 55.4 points, compared with 53.9 in August , which was the highest since March this year. Recall that the value of this index above 50 indicates expansion of the sector , while a reading below 50 suggests contraction activity.

Meanwhile, it became known that the sub- index of new orders index rose to 53.4 in September from 50.9 in August. We add that the volume of new export orders also rose , against which the relevant sub-index has advanced to the level of 50.5 points from 49.6 in August.

In addition, the data showed that the sub-index of business expectations fell to 60.1 from 62.9 a month earlier. The component that tracks the employment rate , meanwhile , fell to 51.3 from 52.5 in August. Input prices continued to rise , but inflation fell in August , against which the relevant sub-index fell in September to a level of 56.7 to 57.1 points.

Recall that the official data from China showed that in the month of September, the business activity in the manufacturing sector has grown, but was less than predicted by many experts .

Stoxx Europe 600 Index fell 0.1 percent to 310.64 . Note that from the beginning of the year , the index rose by 11 percent, as the central banks around the world have pledged to keep interest rates low for an extended period.

As for shatdauna the U.S. government , President Barack Obama said he was " annoyed " by the stalemate on the budget and the national debt ceiling , and accused his opponents in Congress (ie, Republicans ) in the unwillingness to compromise.

"I " caved in "and try to work with the Republican Party " - Obama said in an interview with CNBC. - " Why should not I be angry ? Of course I'm angry. Because it is completely unnecessary . "

The president says he is ready to negotiate, but added that he " will not move from his seat about demand in Congress for funding the government and raising the debt ceiling without addressing minor issues." Republicans insist that the new health care law has been deprived of funding or postponed.

Aviva shares rose 2.6 percent to 418.1 pence after the announcement of the sale of its U.S. life insurance business Apollo Global Management LLC's Athene Holding Ltd, which will provide an income of $ 2.6 billion should be noted that originally reported that the amount income from this transaction will be around $ 1.8 billion

Cost of BP rose 0.9 percent to 436.1 pence , as the U.S. Court of Appeals asked the District Judge Carl Barbier to reconsider its interpretation of certain terms of the agreement reached with the lawyers of the victims of flood in 2012.

Gerresheimer shares fell 1.9 percent to 44.73 euros after Credit Suisse downgraded shares of pharmaceutical products and medical equipment to "neutral " from " buy," saying the shares are close to a 12- month target value at 46 euros . Gerresheimer shares closed yesterday at 45.60 euros yesterday.

At the moment :

FTSE 100 6,450.41 +12.91 +0.20 %

CAC 40 4,158.16 -38.44 -0.92 %

DAX 8,621.8 -7.62 -0.09%

-

10:20

Option expiries for today's 1400GMT cut

EUR/USD $1.3475, $1.3500, $1.3530, $1.3550, $1.3600, $1.3660

GBP/USD $1.6170, $1.6175, $1.6200, $1.6350

USD/JPY Y97.25, Y97.50, Y98.20, Y98.25, Y98.80, Y99.00, Y99.10, Y99.15, Y99.25, Y99.50, Y99.70, Y100.00

AUD/USD $0.9280, $0.9350, $0.9365, $0.9400, $0.9450, $0.9465

EUR/CHF Chf1.2225, Chf1.2280, Chf1.2300

EUR/GBP stg0.8290, stg0.8350

EUR/AUD A$1.4490

-

10:02

Eurozone: Producer Price Index, MoM , August (forecast +0.1%)

-

10:02

Eurozone: Producer Price Index (YoY) , August (forecast -0.5%)

-

10:01

Eurozone: Retail Sales (MoM), August +0.7% (forecast +0.3%)

-

10:01

Eurozone: Retail Sales (YoY), August -0.3% (forecast -1.5%)

-

09:51

Asia Pacific stocks close

Asian stocks rose after a gauge of China’s services industries jumped to a six-month high and as investors watched for progress on ending a budget impasse that has shut down the U.S. government.

Nikkei 225 14,157.25 -13.24 -0.09%

Hang Seng 23,199.73 +215.25 +0.94%

S&P/ASX 200 5,234.9 +19.34 +0.37%

Shanghai Composite 2,174.66 +14.64 +0.68%

Sands China Ltd., a unit of billionaire Sheldon Adelson’s Las Vegas casino company, advanced 3.1 percent after its equity rating was raised at DBS Vickers Hong Kong Ltd. China Huishan Dairy Holdings Co. jumped 9.1 percent, pacing gains among Chinese dairy producers.

Leighton Holdings Ltd., Australia’s biggest builder, slumped 10 percent after saying it’s unaware of any new allegations or ethics breaches in a statement responding to newspaper reports.

-

09:30

United Kingdom: Purchasing Manager Index Services, September 60.3 (forecast 60.4)

-

09:30

United Kingdom: Purchasing Manager Index Services, September 60.3 (forecast 60.4)

-

08:58

Eurozone: Services PMI, September 52.2 (forecast 52.1)

-

08:56

Germany: Services PMI, September 53.7 (forecast 54.4)

-

08:49

France: Services PMI, September 50.5 (forecast 50.7)

-

08:34

FTSE 100 6,457.49 +19.99 +0.31%, CAC 40 4,158.93 +0.77 +0.02%, Xetra DAX 8,646.53 +17.11 +0.20%

-

08:04

United Kingdom: Halifax house price index 3m Y/Y, September +6.2%

-

08:02

United Kingdom: Halifax house price index, September +0.3% (forecast +0.6%)

-

07:21

European bourses are initially seen trading mixed on Thursday: the FTSE up 6, the CAC down 5 and the DAX down 10.

-

07:00

Asian session: The dollar slid to an eight-month low

00:00 China Bank holiday

01:00 China Non-Manufacturing PMI September 53.9 55.4

The dollar slid to an eight-month low versus the euro as the U.S. government’s partial shutdown continued, adding to concern it will slow economic growth and postpone a tapering of monetary stimulus. The Bloomberg U.S. Dollar Index fell to the lowest in two weeks as House Speaker John Boehner signaled a lack of progress on resolving the fiscal impasse after congressional leaders met President Barack Obama. U.S. lawmakers still need to agree on raising the debt limit to avoid a default after Oct. 17.

The Institute for Supply Management’s non-manufacturing index fell to 57 in September from 58.6 a month earlier, the Tempe, Arizona-based group’s report may show, according to the median estimate in a separate poll. Readings greater than 50 indicate growth.

The U.S. Labor department won’t release its monthly payrolls report tomorrow if the government remains closed, according to the Bureau of Labor Statistics.

Euro demand was bolstered before a report forecast to show retail sales in the currency bloc rose in August. Euro-area retail sales rose 0.2 percent in August following a 0.1 percent gain in the previous month, economists predicted before the data due today.

The yen retreated as Asian stocks rallied.

EUR / USD: during the Asian session the pair rose to $ 1.3625

GBP / USD: during the Asian session, the pair traded in the range of $1.6220-40

USD / JPY: during the Asian session the pair rose to Y97.80

There is a full calendar on both sides of the Atlantic Thursday, although some US data could be delayed due to the shutdown. Additionally, German markets are closed for the reunification holiday. The European data calendar kicks off at 0713GMT, with the release of the Spanish September final services PMI data. Italian services data comes at 0743GMT, French data at 0748GMT and German numbers at 0753GMT. Consolidated euro area services PMI will be released at 0758GMT. At 0900GMT, further Euro area data is expected, when the August retail sales numbers cross the wires. Back in Europe, late data sees the release of French October Insee economic outlook. There is limited UK data set for release, but the September CIPS/Markit Services PMI numbers will cross the wire and are likely to underline the nascent UK recovery.

-

06:20

Commodities. Daily history for Oct 2’2013:

GOLD 1,320.60 34.60 2.69%

OIL (WTI) 103.87 1.83 1.79%

-

06:20

Stocks. Daily history for Oct 2’2013:

Nikkei 225 14,170.49 -314,23 -2,17%

Hang Seng 22,999.22 139,36 0,61%

S & P / ASX 200 5,215.6 8,80 0,17%

Shanghai Composite 2,174.66 14,64 0,68%

FTSE 100 6,437.5 -22.51 -0.35%

CAC 40 4,158.16 -38.44 -0.92%

DAX 8,629.42 -59.72 -0.69%

Dow 15,133.14 -58.56 -0.39%

Nasdaq 3,815.02 -2.96 -0.08%

S&P 500 1,693.86 -1.14 -0.07%

-

06:20

Currencies. Daily history for Oct 2'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3581 +0,42%

GBP/USD $1,6228 +0,23%

USD/CHF Chf0,9025 -0,37%

USD/JPY Y97,38 -0,66%

EUR/JPY Y132,27 -0,23%

GBP/JPY Y158,04 -0,42%

AUD/USD $0,9385 -0,11%

NZD/USD $0,8313 +0,51%

USD/CAD C$1,0333 0,00%

-

05:59

Schedule for today, Thursday, Oct 3’2013:

00:00 China Bank holiday

01:00 China Non-Manufacturing PMI September 53.9 55.4

06:00 Germany Bank holiday

07:00 United Kingdom Halifax house price index September +0.4% +0.6%

07:00 United Kingdom Halifax house price index 3m Y/Y September +5.4%

07:48 France Services PMI (Finally) September 50.7 50.7

07:53 Germany Services PMI (Finally) September 54.4 54.4

07:58 Eurozone Services PMI (Finally) September 52.1 52.1

08:30 United Kingdom Purchasing Manager Index Services September 60.5 60.4

09:00 Eurozone Producer Price Index, MoM August +0.3% +0.1%

09:00 Eurozone Producer Price Index (YoY) August +0.2% -0.5%

09:00 Eurozone Retail Sales (YoY) August -1.3% -1.5%

09:00 Eurozone Retail Sales (MoM) August +0.1% +0.3%

12:30 U.S. Initial Jobless Claims September 305 315

14:00 U.S. ISM Manufacturing September 58.6 57.2

14:00 U.S. Factory Orders August -2.4% +0.2%

17:30 U.S. FOMC Member Jerome Powell Speaks

-