Notícias do Mercado

-

20:00

DJIA 14,957.00 26.12 0.17%, S&P 500 1,656.74 3.66 0.22%, NASDAQ 3,663.95 14.91 0.41%

-

18:23

European stocks close

European stocks climbed as European Central Bank President Mario Draghi reiterated that interest rates will stay low for an extended period, while the Federal Reserve said it saw a modest to moderate U.S. economic recovery.

The ECB today kept its benchmark interest rate unchanged at a record low after the 17-nation euro area returned to growth in the second quarter.

The euro-area economy expanded 0.3 percent in the three months through June. Recent economic indicators point to a further recovery in the second half as an index of services and factory output climbed to the highest level since June 2011 and economic confidence soared to a two-year high.

Bank of England officials left their bond-buying program unchanged today at 375 billion pounds ($586 billion), as forecast by all 38 economists in a survey. They also kept the key interest rate at a record low 0.5 percent.

National benchmark indexes advanced in 16 of the 18 western European markets today. France’s CAC 40 gained 0.7 percent, while Germany’s DAX added 0.5 percent. The U.K.’s FTSE 100 climbed 0.9 percent.

Peugeot, Europe’s second-biggest automaker, rose 5.4 percent to 11.24 euros. CEO Philippe Varin forecast an increase in market share in the third quarter, according to an interview with Le Parisien.

A gauge of auto-related companies posted the largest gain of the 19 industry groups on the Stoxx 600. Bayerische Motoren Werke AG, the biggest maker of luxury cars, added 6 percent to 76.97 euros, its highest price since at least 1992. Volkswagen AG, Europe’s largest automaker, climbed 1.2 percent to 172 euros. Renault SA advanced 5.8 percent to 56.50 euros.

Telecom Italia jumped 8.4 percent to 60.7 euro cents. La Repubblica reported that Sawiris may buy a stake in the phone company. The newspaper didn’t cite anyone.

TeliaSonera slid 1.9 percent to 47.56 Swedish kronor. Solidium Oy, Finland’s equity-asset manager, sold 1.6 percent of shares in the Stockholm-based company in an accelerated book building to institutional investors, it said in a statement.

Aker Solutions ASA slipped 1.6 percent to 91.50 Norwegian kroner. Nomura Holdings Inc. downgraded the oil services group controlled by billionaire Kjell Inge Roekke to reduce, similar to a sell rating, from buy.

-

17:20

U.S. factory orders fall 2.4% in July, less than expected

After reporting three consecutive monthly increases, the Commerce Department released a report on Thursday showing a drop in new orders for U.S. manufactured goods in the month of July.

The Commerce Department said factory orders fell by 2.4 percent in July following a revised 1.6 percent increase in June.

Economists had expected orders to decrease by about 3.4 percent compared to the 1.5 percent increase originally reported for the previous month.

The drop in factory orders in July largely reflected a 19.4 percent decrease in orders for transportation equipment, which came on the heels of an 11.7 percent increase in June.

Excluding the drop in orders for transportation equipment, factory orders actually rose by 1.2 percent in July compared to a 0.3 percent drop in the previous month.

The report said orders for manufactured durable goods tumbled by 7.4 percent in July, while orders for manufactured non-durable goods jumped by 2.4 percent.

The Commerce Department also said shipments of manufactured goods rose by 1.1 percent in July following a 0.3 percent decrease in June.

Inventories of manufactured goods edged up by 0.2 percent in July after dipping by 0.2 percent in the previous month.

With shipments rising at a faster rate than inventories, the inventories-to-shipments ratio fell to 1.29 in July from 1.30 in June.

-

17:01

European stocks closed in plus: FTSE 100 6,532.44 +57.70 +0.89%, CAC 40 4,006.8 +26.38 +0.66%, DAX 8,234.98 +39.06 +0.48%

-

16:41

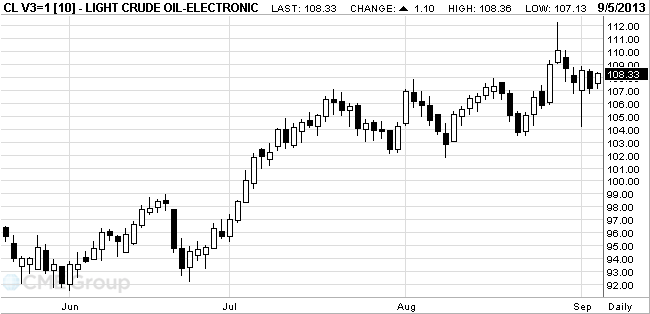

Oil rose

West Texas Intermediate crude climbed from the lowest price in more than a week as a U.S. Senate committee approved military strikes on

Futures advanced as much as 0.8 percent in

WTI for October delivery increased as much as 81 cents to $108.04 a barrel in electronic trading on the New York Mercantile Exchange, and was at $107.86 at 1:29 p.m. London time. The contract dropped 1.2 percent to $107.23 yesterday, the biggest decline since Aug. 20 and the lowest settlement since Aug. 26. The volume of all futures traded was about 50 percent below the 100-day average.

Brent for October settlement was 40 cents higher at $115.31 a barrel on the London-based ICE Futures Europe exchange. The European benchmark crude was at a premium of $7.39 to WTI, compared with $7.68 yesterday.

-

16:20

Gold becomes cheaper on stronger dollar

Gold prices are falling for the fourth time in five sessions because of the dollar after data on unemployment and activity in the U.S. service sector .

According to recent reports, which were submitted to the Department of Labor , at the end of last week, the number of those who applied for a first time unemployment benefits fell moderately , reaching with levels seen before the recession .

The report showed that for the week ended Aug. 31 , the number of initial claims for unemployment benefits fell to a seasonally adjusted at 9000 , down to the level of 323 thousand Many economists predicted that this figure will drop to 330 thousand from 332 thousand , of which initially reported last week. We add that the number of complaints varies near five-year low since the end of July.

Meanwhile, it was reported that the average number of claims for the past four weeks was 328.5 thousand, which is 3,000 less than was recorded in the previous week. Note that the latter figure was the lowest since October 2007 , which was several months before the start of the last recession .

Economic activity in the non-manufacturing sector in the U.S. rose in August, the growth continues the 44th month in a row - according to national survey of managers conducted by ISM. The index of non-manufacturing sector rose to 56.0 % in July to 58.6 % in August. This shows that the growth in the non-manufacturing sector accelerated. The August with the maximum value of the index in January 2008

The cost of the October gold futures on COMEX today dropped to $ 1364.50 per ounce.

-

16:00

U.S.: Crude Oil Inventories, August -1.8

-

15:00

U.S.: ISM Non-Manufacturing, August 58.6 (forecast 55.2)

-

15:00

U.S.: Factory Orders , July -2.4% (forecast -3.2%)

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.3060/65, $1.3100, $1.3110, $1.3150, $1.3175, $1.3200, $1.3250

USD/JPY Y98.85, Y98.90, Y99.00, Y99.40, Y99.50, Y99.65, Y100.00

EUR/JPY Y130.20, Y131.00

GBP/USD $1.5500, $1.5700

EUR/GBP stg0.8475

EUR/CHF Chf1.2320, Chf1.2360, Chf1.2425

AUD/USD $0.9100

NZD/USD $0.7750, $0.7770

USD/CAD C$1.1.0545, C$1.0570, C$1.0600

-

14:33

U.S. Stocks open: Dow 14,927.88 -2.99 -0.02%, Nasdaq 3,651.64 +2.60 +0.07%, S&P 1,653.11 +0.03 +0.00%

-

14:29

Before the bell: S&P futures +0.06%, Nasdaq futures +0.06%

U.S. stock futures were little changed as investors weighed reports showing jobless claims fell more than forecast and disappointing growth in private payrolls.

Global Stocks:

Nikkei 14,064.82 +10.95 +0.08%

Hang Seng 22,597.97 +271.75 +1.22%

Shanghai Composite 2,122.43 -5.19 -0.24%

FTSE 6,515.16 +40.42 +0.62%

CAC 4,005 +24.58 +0.62%

DAX 8,224.22 +28.30 +0.35%

Crude oil $107.56 +0.31%

Gold $1390.20 +0.01%

-

13:48

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Other:

Caterpillar (CAT) initiated at Equal-Weight at Morgan Stanley.

-

13:30

U.S.: Nonfarm Productivity, q/q, Quarter II +2.3% (forecast +1.8%)

-

13:30

U.S.: Initial Jobless Claims, August 323 (forecast 330)

-

13:15

U.S.: ADP Employment Report, August 176 (forecast 181)

-

13:10

European session: the dollar has lost all previously earned positions against the euro

Data

00:00 G20 G20 Meetings

00:00 U.S. FOMC Member Narayana Kocherlakota

01:30 Australia Trade Balance July 0.60 0.11 -0.77

03:00 Japan BoJ Interest Rate Decision 0.10% 0.10% 0.10%

03:00 Japan Bank of Japan Monetary Base Target 270 270 270

03:00 Japan BoJ Monetary Policy Statement

07:30 Japan BOJ Press Conference

10:00 Germany Factory Orders s.a. (MoM) July +5.0% -0.7% -2.7%

10:00 Germany Factory Orders n.s.a. (YoY) July +4.3% +2.7% +5.0%

11:00 United Kingdom BoE Interest Rate Decision 0.50% 0.50% 0.50%

11:00 United Kingdom Asset Purchase Facility 375 375 375

11:00 United Kingdom MPC Rate Statement

11:45 Eurozone ECB Interest Rate Decision 0.50% 0.50% 0.50%

The euro rose against the dollar, thus restoring all the previously lost positions ahead of the ECB press conference and U.S. data .

In anticipation of the ECB meeting , experts note that most likely will repeat today Draghi pigeon abstracts of their policies transparent communication . Eurozone is still a long way out of the crisis and overcome the weakness of the economy, and in these circumstances, the ECB will try to put pressure on the recent rise in market rates . But if the spirit of pigeon ECB is not enough to lower the pair EUR / USD below $ 1.3139 (low of September) , it may make economic performance of the United States.

It is expected that, in general , the statistics on the U.S. would be positive. The continued economic growth favors the fast decline in stimulation of the Federal Reserve System . An estimated 65 % of the experts , the American Central Bank may decide to reduce the amount of monthly redemption of bonds at a meeting on September 17-18 . Impact on the dollar could have a publication of the report of the Employment Research Institute, ADP. According to the median forecast of economists , the number of new jobs created in the U.S. economy in the last month is likely to grow by 182 million value remains high as the July report , when the growth rate was fixed at 200 thousand

Meanwhile, we add that the course of trade partly influenced by the placement of bonds of Spain and France. Today, Spain's Treasury held an auction , the results of which failed through the sale of 10 - and 5- year bonds attract E4 billion , reaching the upper limit of the target range E3 -4 billion in the auction were sold at E2.412 billion of securities maturing in October 2023 ( average yield 4.526 % against 4.723 % at the previous auction ) . It was also sold bonds due in October 2018 to E1.596 billion ( average yield 3.504 % vs. prev. 3.561 %).

Recently it became known that the yield on Spanish debt fell for the most recent auction, while the yield on 10 -year securities of France noted a record high for Hollande stay in power.

The pound rose sharply against the dollar, against the decision of the Bank of England. Note that in the course of today's meeting of the Bank of England did not bring any surprises markets , leaving the key lending rate at a record low 0.5 %, where it has been since March 2009 . Acquisitions of assets of the Central Bank has kept the £ 375 billion Bank of England intends to maintain the rate at a low level, at least as long as the rate of unemployment in the country will not fall under the 7% mark , as it happens, is not expected before 2016. We add that the report of this meeting will be published on Wednesday, September 18.

The yen fell against the dollar, after not even looking at the fact that the Bank of Japan left its monetary policy unchanged and raised its forecast for growth. It should be noted that today, the Bank of Japan said that the country's economy is recovering. This strengthens the position of those who favor the increase of the sales tax next year. In addition , it was said that Japan's economy "moderately reduced " . This is the most optimistic statement from March 2008 , when the economy was rated as " expanding moderately " . In August assessment of the economy was a " moderate recovery " - the Bank of Japan announced almost a full recovery .

The government plans to raise the consumption tax from 5% to 8% in April next year, a decision about the strategy to be announced in early October.

The Bank of Japan unanimously decided to keep the key policy of increasing the money supply by 60-70 trillion . yen in the year through the purchase of government bonds in Japan. The bank plans to achieve the target level of 2% inflation over the current leniency policy. The government may take further measures to stimulate the economy in April in order to minimize the effect of increasing the sales tax on the growth of the economy.

EUR / USD: during the European session, the pair rose from $ 1.3161 to $ 1.3218

GBP / USD: during the European session, the pair rose to $ 1.5662

USD / JPY: during the European session, the pair reached the level of Y100.12

At 12:15 GMT the United States will announce the change in the number of employees from ADP in August. At 12:30 GMT will be the monthly press conference of the ECB . Also at this time, the U.S. announced a change in the level of labor productivity in the non-manufacturing sector for the 2nd quarter . At 14:00 GMT the U.S. will report on changes in the volume of industrial orders in July , and will also release a composite index of ISM non-manufacturing activity in August. In Russia will meet G20.

-

13:00

Orders

EUR/USD

Offers $1.3290/300, $1.3250/60, $1.3235/40, $1.3220/25, $1.3218

Bids $1.3160/55, $1.3150, $1.3130/15, $1.3100, $1.3090

GBP/USD

Offers $1.5720/25, $1.5680/85, $1.5650, $1.5625/35

Bids $1.5585/80, $1.5570, $1.5555/50, $1.5525/20, $1.5510/00

AUD/USD

Offers $0.9300, $0.9250, $0.9220, $0.9200, $0.9185/90

Bids $0.9120, $0.9100, $0.9080, $0.9050

EUR/GBP

Offers stg0.8550/55, stg0.8520, stg0.8465, stg0.8465

Bids stg0.8425/20, stg0.8400, stg0.8380, stg0.8350

EUR/JPY

Offers Y132.50, Y132.20, Y131.95/00

Bids Y131.45/40, Y131.00, Y130.85/80, Y130.50, Y130.47/45

USD/JPY

Offers Y101.00, Y100.80, Y100.50, Y100.30, Y100.15/20

Bids Y99.36/33, Y99.20/15, Y99.00, Y98.76/74/73

-

12:46

Eurozone: ECB Interest Rate Decision, 0.50% (forecast 0.50%)

-

12:00

United Kingdom: BoE Interest Rate Decision, 0.50% (forecast 0.50%)

-

12:00

United Kingdom: Asset Purchase Facility, 375 (forecast 375)

-

11:30

European stock indices rose

European stocks were little changed as investors awaited central-bank meetings, and as the Federal Reserve said it saw a modest to moderate recovery in the world’s biggest economy. U.S. stock futures and Asian shares were also little changed.

The Stoxx Europe 600 Index fell 0.1 percent to 301.93 at 10:51 a.m. in London. The gauge lost 2.4 percent last week on concern the U.S. and its allies would take military action against Syria after chemical-weapon attacks that President Barack Obama’s administration said killed more than 1,400 people.

The euro-area economy expanded 0.3 percent in the three months through June. Recent economic indicators point to a further recovery in the second half as an index of services and factory output climbed to the highest level since June 2011 and economic confidence soared to a two-year high.

Rate Decisions

Policy makers meeting in Frankfurt today will keep the European Central Bank’s benchmark interest rate unchanged at a record low of 0.5 percent, according to economists in survey. The central bank will announce its interest-rate decision at 1:45 p.m. and President Mario Draghi will hold a press conference 45 minutes later.

The Bank of England will keep its quantitative-easing program at 375 billion pounds ($585 billion) and hold the benchmark rate at a low of 0.5 percent, according to separate surveys of economists. That decision is due at noon in London.

The Senate Foreign Relations Committee voted to authorize Obama to conduct a limited U.S. military operation in Syria, the first step toward congressional endorsement of the effort. The full Senate is expected to consider the resolution on Sept. 9.

Aker slid 2.8 percent to 90.40 kroner. Nomura cut its rating on the oil services group controlled by billionaire Kjell Inge Roekke to reduce from buy.

Altran Technologies (ALT) slid 5.5 percent to 5.48 euros as it reported net income for the first half of this year of 15.1 million euros ($19.9 million), compared with 30.3 million euros a year earlier. The engineering and technology consulting company forecast a “much brighter” second half and said that it is confident of reaching its 2015 targets.

Schweizerische National-Versicherungs-Gesellschaft AG (NATN), a provider of insurance products, lost 2.1 percent to 42.45 Swiss francs after it reported first-half net income fell to 53 million francs ($56 million) from 56.6 million francs last year.

Peugeot (UG), Europe’s second-biggest automaker, rose 2.4 percent to 10.93 euros. CEO Philippe Varin forecast an increase in market share in the third quarter, according to an interview with Le Parisien.

FTSE 100 6,484.59 +9.85 +0.15%

CAC 40 3,983.89 +3.47 +0.09%

DAX 8,191.3 -4.62 -0.06%

-

11:00

Germany: Factory Orders s.a. (MoM), July -2.7% (forecast -0.7%)

-

11:00

Germany: Factory Orders n.s.a. (YoY), July +5.0% (forecast +2.7%)

-

10:25

Option expiries for today's 1400GMT cut

EUR/USD $1.3060/65, $1.3100, $1.3110, $1.3150, $1.3175, $1.3200, $1.3250

USD/JPY Y98.85, Y98.90, Y99.00, Y99.40, Y99.50, Y99.65, Y100.00

EUR/JPY Y130.20, Y131.00

GBP/USD $1.5500, $1.5700

EUR/GBP stg0.8475

EUR/CHF Chf1.2320, Chf1.2360, Chf1.2425

AUD/USD $0.9100

NZD/USD $0.7750, $0.7770

USD/CAD C$1.1.0545, C$1.0570, C$1.0600

-

09:41

Asia Pacific stocks close

Asian stocks rose for a sixth day, the longest streak of gains in nine months, as shipping lines surged and the Federal Reserve said it saw a moderate recovery in the world’s biggest economy.

Nikkei 225 14,064.82 +10.95 +0.08%

Hang Seng Closed 22,596.63 +270.41 +1.21%

S&P/ASX 200 5,142.51 -19.12 -0.37%

Shanghai Composite 2,122.43 -5.19 -0.24%

Honda Motor Co. led Japanese carmakers higher, advancing 2.3 percent after Asia-based auto manufacturers recorded their best-ever month for U.S. sales.

Shippers gained from Hong Kong to Tokyo as a measure of freight prices reached its highest in 21 months.

BHP Billiton Ltd., the world’s largest mining company, sank 0.7 percent after metals fell yesterday in London for the sixth time in seven days.

-

08:40

FTSE 100 6,509.23 +34.49 +0.53%, CAC 40 3,987.48 +7.06 +0.18%, Xetra DAХ 8,229.46 +33.54 +0.41%

-

07:40

European bourses are initially seen trading higher Thursday: the FTSE up 17, the DAX up 35 and the CAC up 6.

-

07:20

Asian session: The Dollar Index rose

00:00 G20 G20 Meetings

00:00 U.S. FOMC Member Narayana Kocherlakota

01:30 Australia Trade Balance July 0.60 0.11 -0.77

03:00 Japan BoJ Interest Rate Decision 0.10% 0.10% 0.10%

03:00 Japan Bank of Japan Monetary Base Target 270 270 270

03:00 Japan BoJ Monetary Policy Statement

The Dollar Index rose before private U.S. reports projected to show employment increased and the service industry expanded, adding to the case for the Fed to reduce debt purchases at a policy meeting on Sept. 17-18. The ADP Research Institute will probably say today U.S. companies added 182,000 jobs last month, according to the median economist estimate compiled by Bloomberg. That would follow a 200,000 increase in July, the most since December.

The Labor Department may say tomorrow U.S. payrolls rose by 180,000 in August while the jobless rate held at 7.4 percent, the lowest since December 2008, a separate poll showed.

The Institute for Supply Management’s gauge of non-manufacturing industries was probably at 55 in August from 56 the previous month, another survey showed before the figures today. Readings above 50 signify expansion.

The yen strengthened against 13 of its 16 major counterparts after the Bank of Japan raised its assessment of the nation’s economy as it left its easing program unchanged.

The Bank of England and the European Central Bank will also announce interest-rate decisions today. U.K. central bank Governor Mark Carney introduced forward guidance on the path of interest rates last month, saying the Monetary Policy Committee won’t consider raising its key rate until unemployment falls to 7 percent, while MPC member Martin Weale voted against it.

EUR / USD: during the Asian session the pair fell below $ 1.3170

GBP / USD: during the Asian session, the pair fell to $ 1.5600

USD / JPY: during the Asian session the pair rose to Y99.95

The data calendar is set to kick off at 0530GMT, with the release of the French second quarter ILO unemployment data. Analysts are looking for a number of 10.6%, up from 10.4% in Q1. At 0700GMT, Eurogroup President Jeroen Dijsselbloem will speak at the European Parliament's Committee on Economic and Monetary Affairs, in Belgium. At 1000GMT, the German July manufacturing orders data will be released. The latest ECB policy decision is expected at 1145GMT, to be followed by President Mario Draghi's press conference at 1230GMT. As well as the policy decision, we will get the release of key "Staff Forecasts" - the figures on growth and inflation from the Banks' economic experts. Given the recent slowdown in headline consumer prices, not to mention the recent exit from the Eurozone's longest recession, investors will be keen to hear what both President Mario Draghi has to say about the Bank's new forward guidance policy as well as the Bank's strategy for dealing with the market implications of the US Federal Reserve's anticipated tapering.

There is another full calendar on both sides of the Atlantic Thursday, with the policy decisions from both the ECB and the BOE set to dominate. There is only limited UK data, with the release of the August SMMT Car Registrations data at 0800GMT. The first central bank decision comes at 1100GMT, when the Bank of England releases the outcome of the September MPC meeting. The meet is the third under the stewardship of Mark Carney. However, analysts expect no change in either Bank Rate of the stg375 billion quantitative easing program, despite the solid upturn in recent economic data.

-

06:21

Commodities. Daily history for Sep 4’2013:

GOLD 1,393.90 -17.80 -1.26%

OIL (WTI) 107.34 -1.20 -1.11%

-

06:20

Currencies. Daily history for Sep 4'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3202 +0,27%

GBP/USD $1,5622 +0,42%

USD/CHF Chf0,9355 -0,13%

USD/JPY Y99,77 +0,22%

EUR/JPY Y131,70 +0,46%

GBP/JPY Y155,83 +0,62%

AUD/USD $0,9162 +1,16%

NZD/USD $0,7893 +1,20%

USD/CAD C$1,0495 -0,38%

-

06:20

Stocks. Daily history for Sep 4’2013:

Nikkei 225 14,053.87 75,43 0,54%

Hang Seng 22,324.22 -70,36 -0,31%

S & P / ASX 200 5,161.64 -34,93 -0,67%

Shanghai Composite 2,127.62 4,51 0,21%

FTSE 100 6,474.74 +6.33 +0.10%

CAC 40 3,980.42 +6.35 +0.16%

DAX 8,195.92 +15.21 +0.19%

DJIA 14,930.90 96.91 0.65%

S&P 500 1,652.45 12.68 0.77%

NASDAQ 3,649.04 36.43 1.01%

-

06:00

Schedule for today, Thursday, Sep 5’2013:

00:00 G20 G20 Meetings

00:00 U.S. FOMC Member Narayana Kocherlakota

01:30 Australia Trade Balance July 0.60 0.11 -0.77

03:00 Japan BoJ Interest Rate Decision 0.10% 0.10% 0.10%

03:00 Japan Bank of Japan Monetary Base Target 270 270 270

03:00 Japan BoJ Monetary Policy Statement

07:00 United Kingdom Halifax house price index August +0.9% +0.7%

07:00 United Kingdom Halifax house price index 3m Y/Y August +4.6% +5.6%

07:30 Japan BOJ Press Conference

10:00 Germany Factory Orders s.a. (MoM) July +3.8% -0.7%

10:00 Germany Factory Orders n.s.a. (YoY) July +4.3% +2.7%

11:00 United Kingdom BoE Interest Rate Decision 0.50% 0.50%

11:00 United Kingdom Asset Purchase Facility 375 375

11:00 United Kingdom MPC Rate Statement

11:45 Eurozone ECB Interest Rate Decision 0.50% 0.50%

12:15 U.S. ADP Employment Report August 200 181

12:30 Eurozone ECB Press Conference

12:30 U.S. Initial Jobless Claims August 331 330

12:30 U.S. Nonfarm Productivity, q/q (Finally) Quarter II +0.9% +1.8%

13:00 U.S. FOMC Member Narayana Kocherlakota

14:00 U.S. ISM Non-Manufacturing August 56.0 55.2

14:00 U.S. Factory Orders July +1.5% -3.2%

15:00 U.S. Crude Oil Inventories August +3.0

23:30 Australia AiG Performance of Construction Index August 44.1

-