Notícias do Mercado

-

18:21

European stocks close

European stocks declined as comments from Federal Reserve policy makers fueled speculation the central bank will begin tapering stimulus next month, and as companies from Salzgitter AG to Lanxess AG cut profit forecasts.

The Stoxx Europe 600 Index lost 0.4 percent to 303.5 at the close of trading. The benchmark gauge erased earlier gains of as much as 0.4 percent as Fed Bank of Atlanta President Dennis Lockhart said in an interview with Market News International that if economic growth and job creation pick up as expected, the central bank should proceed with the “removal” of its asset purchases, and as investors awaited remarks from Fed Bank of Chicago President Charles Evans.

Fed Bank of Dallas President Richard Fisher, one of the most vocal critics of quantitative easing, yesterday warned investors not to rely on stimulus.

National benchmark indexes retreated in 14 of the 18 western-European markets today. The U.K.’s FTSE 100 dropped 0.2 percent, Germany’s DAX fell 1.2 percent and France’s CAC 40 slipped 0.4 percent.

Salzgitter tumbled 12 percent to 25.27 euros, its biggest decline since March 2009. The steelmaker expects a pretax loss of about 400 million euros this year amid a slump in demand due to the deterioration of the European economy. “The ongoing recession in many European countries has put pressure on the European steel industry in the form of a structural crisis,” it said yesterday after the close of regular trading.

Lanxess retreated 4.3 percent to 44.48 euros after it cut its profit forecast for 2014 and predicted no recovery in second-half demand. The Cologne, Germany-based company said it won’t achieve its Ebitda target for next year of 1.4 billion euros. It forecast earnings for this year of 700 million euros to 800 million euros.

Munich Re, the world’s biggest reinsurer, dropped 4.9 percent to 145.25 euros after it said second-quarter profit fell 35 percent, missing analysts’ estimates, as claims arising from natural disasters rose. Net income dropped to 529 million euros from 808 million euros a year earlier, trailing the 557.1 million-euro average estimate of analysts.

InterContinental Hotels rose 6.4 percent to 2,030 pence after the world’s largest provider of hotel rooms reported first-half net income of $340 million, compared with $271 million a year earlier.

UniCredit SpA added 2.2 percent to 4.26 euros. Italy’s biggest bank said second-quarter net income climbed to 361 million euros from 169 million euros a year earlier. That was in line with the 360 million-euro average estimate of eight analysts surveyed by Bloomberg. The Milan-based bank posted a 254 million-euro return from the buyback of 4.2 billion euros of senior securities in April, according to a statement today.

Royal DSM NV gained 6.4 percent to 56.02 euros. The Dutch chemical company posted second-quarter profit that beat analyst estimates after a $3.1 billion-acquisition spree and as it cut costs. Earnings before interest, taxes, depreciation and amortization jumped 19 percent to 345 million euros. That exceeded the 333 million-euro average estimate of 11 analysts.

-

16:43

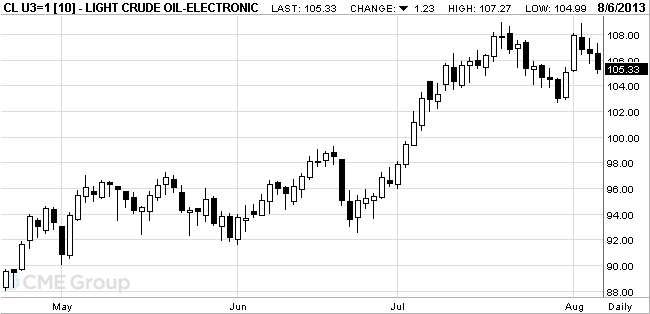

Oil fell for a third day

West Texas Intermediate crude fell for a third day amid speculation that the Federal Reserve may reduce stimulus and after Bank of America’s Francisco Blanch said it will be difficult for WTI to rally much more.

Prices dropped as much as 1.2 percent as investors awaited an address by Fed Bank of Chicago President Charles Evans for indications of the central bank’s policy. Dallas Fed President Richard Fisher said yesterday the bank is closer to slowing $85 billion in monthly bond buying. WTI could slide $8 to $10, Blanch, head of commodities research at Bank of America in

WTI for September delivery decreased $1.09, or 1 percent, to $105.47 a barrel at 10:23 a.m. on the New York Mercantile Exchange. Earlier, it gained as much as 0.7 percent. The volume of all futures traded was 7.2 percent below the 100-day average.

Brent for September settlement slid 94 cents, or 0.9 percent, to $107.76 a barrel on the London-based ICE Futures Europe exchange. Volume was 6.1 percent above 100-day average. The European benchmark grade was at a premium of $2.29 to WTI.

Crude surged 8.8 percent in July, the biggest monthly gain since August 2012, as

-

16:20

Gold is cheaper on strong data

Gold prices are falling, as strong economic data have made the metal less attractive as a low-risk assets, and the demand in the physical markets of India and China remains depressed.

Index PMI, reflecting activity in the services sector of the U.S. economy in July was 56.0 points compared to 52.2 points in June, shows an overview of the Institute of Supply Managers (ISM). Industrial production in the UK in June rose 1.1 percent from May and 1.2 percent - by June 2012.

Gold fell to a minimum of two weeks $ 1.282,69 Friday in the high rates of economic growth and industrial activity in the United States, but the prices have gone up after the publication of weak employment data.

Premiums in Hong Kong - the main supplier of gold in China - fell to $ 04.03 to the price in London from $ 5 two weeks ago, dealers said. Importers in India - the world's largest gold market - refrain from buying a third week in a row due to uncertain government policy on import.

Stocks of the world's largest exchange-traded fund backed by gold (ETF) SPDR Gold Trust on Monday, fell 0.2 percent to 917.14 tons.

The cost of the October gold futures on COMEX today dropped to $ 1278.40 per ounce.

-

15:02

U.S.: JOLTs Job Openings, June 3940 (forecast 3900)

-

15:00

United Kingdom: NIESR GDP Estimate, July +0.7%

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.3050, $1.3125, $1.3150, , $1.3285

USD/JPY Y99.00, Y99.10, Y99.60, Y100.00

EUR/JPY Y129.85

GBP/USD $1.5300

USD/CHF Chf0.9200

AUD/USD $0.8800, $0.9000, $0.9070

NZD/USD $0.7800

USD/CAD C$1.0370

AUD/CAD C$0.91, C$0.94

-

14:36

U.S. Stocks open: Dow 15,550.54 -61.59 -0.39%, Nasdaq 3,689.22 -3.73 -0.10%, S&P 1,704.12 -3.02 -0.18%

-

14:27

Before the bell: S&P futures -0.15%, Nasdaq futures -0.01%

U.S. stock-index futures fell as investors awaited an address by Federal Reserve Bank of Chicago President Charles Evans for indications of the central bank’s policy.

Global Stocks:

Nikkei 14,401.06 +143.02 +1.00%

Hang Seng 21,923.7 -298.31 -1.34%

Shanghai Composite 2,060.5 +10.02 +0.49%

FTSE 6,627.67 +8.09 +0.12%

CAC 4,059.79 +9.82 +0.24%

DAX 8,393.89 -4.49 -0.05%

Crude oil $106.93 +0.35%

Gold $1286.20 -1.01%

-

14:00

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

IBM (IBM) downgraded from Neutral to Underperform at Credit Suisse

Other: -

13:30

U.S.: International trade, bln, June -34.2 (forecast -43.1)

-

13:30

Canada: Trade balance, billions, June -0.5 (forecast -0.5)

-

13:19

European session: the euro currency has risen sharply

Data

01:30 Australia Trade Balance June 0.50 Revised From 0.67 0.81 0.60

01:30 Australia ANZ Job Advertisements (MoM) July -1.8% -6.8%

01:30 Australia House Price Index (QoQ) Quarter II +0.8% Revised From +0.1% +1.3% +2.4%

01:30 Australia House Price Index (YoY) Quarter II +2.6% +3.0% +5.1%

04:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50% 2.50%

04:30 Australia RBA Rate Statement

05:00 Japan Leading Economic Index June 110.7 108.0 107.0

05:00 Japan Coincident Index June 106.0 105.1 105.2

07:00 United Kingdom Halifax house price index July +0.6% +0.3% +0.9%

07:00 United Kingdom Halifax house price index 3m Y/Y July +3.7% +4.3% +4.6%

08:30 United Kingdom Industrial Production (MoM) June 0.0% +0.7% +1.1%

08:30 United Kingdom Industrial Production (YoY) June -2.3% +0.8% +1.2%

08:30 United Kingdom Manufacturing Production (MoM) June -0.8% +0.9% +1.9%

08:30 United Kingdom Manufacturing Production (YoY) June -2.9% +1.0% +2.0%

10:00 Germany Factory Orders s.a. (MoM) June -0.5% Revised From -1.3% +1.1% +3.8%

10:00 Germany Factory Orders n.s.a. (YoY) June -2.0% -0.3% +3.4%

Rate of the euro traded higher against the dollar, though retreated from earlier peak values. It should be noted that the Euro-currency support had submitted a report on Germany, which was much better than expected. As it became known, in June, the German promzakazy rose by 3.4% y / y vs. 2% y / y in May. Analysts had expected a contraction of 0.3%. In monthly terms, orders increased by 3.8% versus -0.5% previously forecast and +1%.

We also add that the cyclical improvement in the euro area data confirmed Italy's GDP in the second quarter, which showed a negative value. The Italian economy is still in recession, although the data on the dynamics of GDP for the II quarter are encouraging. Italian GDP for the period decreased by 0.2% qoq and 2% - in annualized, from the data of the national statistics institute ISTAT. At the same time, analysts expected a decline in GDP of 0.4% on the quarter and by 2.2% - year on year.

Italy's economy, "compressed" for the eighth consecutive quarter, although the decline in GDP was less than that predicted by experts, and less significant than in I quarter, when the economy shrank by 0.6% qoq.

Add that after the publication of the data market participants' attention shifted to the report on the U.S. trade balance for June and a voting member of the Fed's statement, Charles Evans.

Value of the pound has fallen significantly against the dollar, while offsetting the early growth. Note that the currency is reduced, even though the optimistic reports, which were released today. The Office for National Statistics reported on the results of June of the year, industrial output increased significantly, thereby exceeded the forecasts of experts, helped by recovery in the sector of mining and industrial production.

According to a report in the June monthly basis, the volume of industrial production increased by 1.1%, after three consecutive months of zero growth. It is worth noting that economists had forecast industrial production growth at only 0.7%. In addition, it was reported that production in the manufacturing industry increased 1.9% in June, fully offsetting the decline of 0.7% (revised from -0.8%), which was recorded in the previous month. This growth exceeded economists' forecast at 0.9%.

In annual terms, the volume of industrial production increased in June by 1.2%, which followed a 2.3% decline in the previous month. We also add that manufacturing output in June rose by 2%, partially offset by the decline of 2.9% recorded in May.

EUR / USD: during the European session, the pair rose to $ 1.3295

GBP / USD: during the European session, the pair rose to $ 1.5392, and then decreased slightly to $ 1.5332

USD / JPY: during the European session, the pair fell to Y98.00 from Y98.60

At 12:30 GMT, Canada and the U.S. will report on its trade balance for June. At 14:00 GMT Britain will release data on the change in GDP from NIESR for July. At 14:00 GMT the United States will present a report on the level of vacancies and labor turnover in June. At 22:45 GMT New Zealand will report on changes in the number of employees for the 2nd quarter, and the unemployment rate for the 2nd quarter.

-

13:00

Orders

EUR/USD

Offers $1.3345/50, $1.3334, $1.3280/300, $1.3281

Bids $1.3235/30, $1.3220/10, $1.3205/190, $1.3180, $1.3165/50

GBP/USD

Offers $1.5480, $1.5450/60, $1.5430/35, $1.5420, $1.5400

Bids $1.5353, $1.5330/20, $1.5300, $1.5280, $1.5250/40

AUD/USD

Offers $0.9100, $0.9050, $0.9035/40

Bids $0.8950, $0.8900, $0.8880/75, $0.8820

EUR/JPY

Offers Y131.80, Y131.40/50, Y131.15/20, Y131.00, Y130.82/92

Bids Y130.10/00, Y129.55/50, Y129.20, Y129.00

USD/JPY

Offers Y99.50, Y99.02/15, Y98.90/00, Y98.55/63

Bids Y98.07, Y97.85/80, Y97.50, Y97.25/20, Y97.00

EUR/GBP

Offers stg0.8810/15, stg0.8790/00, stg0.8695-700, stg0.8670/75, stg0.8645/50

Bids stg0.8605/595, stg0.8585/80, stg0.8550, stg0.8540

-

11:33

European stock close

European stocks advanced for a seventh day as companies such as Credit Agricole SA posted better-than-expected earnings, outweighing cuts in profit forecasts from Salzgitter AG and Lanxess AG. U.S. index futures were little changed, while Asian shares rose.

The Stoxx Europe 600 Index added 0.2 percent to 305.29 at 11:03 a.m. in London. The benchmark gauge rose every day last week, adding 1.8 percent in the period, as European Central Bank President Mario Draghi said interest rates in the euro zone will remain low for an extended period.

Federal Reserve Bank of Dallas President Richard Fisher, one of the most vocal critics of quantitative easing, warned investors not to rely on stimulus.

“Financial markets may have become too accustomed to what some have depicted as a Fed put,” or the idea that the central bank will loosen credit after a market decline, Fisher said yesterday in a speech in Portland, Oregon.

Still, “markets continue to ponder the Federal Reserve’s next move, with some speculation that next month’s tapering of quantitative easing may slip back following the weaker than expected non-farms on Friday,” Hunter said, referring to a U.S. report that showed employers added fewer workers in July than economists had forecast.

Credit Agricole increased 1.1 percent to 7.92 euros. France’s third-largest bank by market value said profit surged in the second quarter after the sale of its unprofitable Greek unit. Net income jumped to 696 million euros from a restated 56 million euros a year earlier, the lender said in a spreadsheet posted today on its website. Earnings beat the 481.6 million-euro average estimate of analysts surveyed.

InterContinental Hotels rose 2.9 percent to 1,964 pence after the world’s largest provider of hotel rooms reported first-half net income of $340 million, compared with $271 million a year earlier.

Royal DSM NV (DSM) added 5.5 percent to 55.57 euros. The Dutch chemical company posted second-quarter profit that beat analyst estimates after a $3.1 billion-acquisition spree and as it cut costs. Earnings before interest, taxes, depreciation and amortization jumped 19 percent to 345 million euros. That exceeded the 333 million-euro average estimate of 11 analysts.

FTSE 100 6,615.14 -4.44 -0.07%

CAC 40 4,056.58 +6.61 +0.16%

DAX 8,420.02 +21.64 +0.26%

-

11:01

Germany: Factory Orders s.a. (MoM), June +3.8% (forecast +1.1%)

-

11:01

Germany: Factory Orders n.s.a. (YoY), June +3.4% (forecast -0.3%)

-

10:23

Option expiries for today's 1400GMT cut

EUR/USD $1.3050, $1.3125, $1.3150, , $1.3285

USD/JPY Y99.00, Y99.10, Y99.60, Y100.00

EUR/JPY Y129.85

GBP/USD $1.5300

USD/CHF Chf0.9200

AUD/USD $0.8800, $0.9000, $0.9070

NZD/USD $0.7800

USD/CAD C$1.0370

AUD/CAD C$0.91, C$0.94

-

09:31

United Kingdom: Industrial Production (YoY), June +1.2% (forecast +0.8%)

-

09:31

United Kingdom: Industrial Production (MoM), June +1.1% (forecast +0.7%)

-

09:30

United Kingdom: Manufacturing Production (MoM) , June +1.9% (forecast +0.9%)

-

09:30

United Kingdom: Manufacturing Production (YoY), June +2.0% (forecast +1.0%)

-

09:21

Asia Pacific stocks close

Asian stocks outside Japan fell as stronger growth in U.S. service industries fueled speculation the Federal Reserve will soon be able to reduce economic stimulus.

Nikkei 225 14,401.06 +143.02 +1.00%

Hang Seng 21,952.78 -269.23 -1.21%

S&P/ASX 200 5,105.6 -5.65 -0.11%

Shanghai Composite 2,060.5 +10.02 +0.49%

HSBC Holdings Plc slumped 4.6 percent in Hong Kong after earnings at Europe’s biggest bank missed analysts’ estimates.

Sony Corp. sank 4.6 percent in Tokyo after its board rejected billionaire Daniel Loeb’s call to sell part of its entertainment business.

Fonterra Shareholders Fund climbed 1.3 percent in New Zealand, recouping some of yesterday’s record decline after Russia and China halted imports of milk powder from Fonterra Cooperative Group Ltd., the world’s largest dairy exporter.

-

09:02

FTSE 100 6,606.66 -12.92 -0.20%, CAC 40 4,053.98 +4.01 +0.10%, Xetra DAX 8,389.24 -9.14 -0.11%

-

08:02

United Kingdom: Halifax house price index, July +0.9% (forecast +0.3%)

-

08:02

United Kingdom: Halifax house price index 3m Y/Y, July +4.6% (forecast +4.3%)

-

07:21

European bourses are initially seen trading lower Tuesday: the FTSE down 27, the DAX down 18 and the CAC down 8.

-

07:03

Asian session: The yen rose

01:30 Australia Trade Balance June 0.50 Revised From 0.67 0.81 0.60

01:30 Australia ANZ Job Advertisements (MoM) July -1.8% -6.8%

01:30 Australia House Price Index (QoQ) Quarter II +0.8% Revised From +0.1% +1.3% +2.4%

01:30 Australia House Price Index (YoY) Quarter II +2.6% +3.0% +5.1%

04:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50% 2.50%

04:30 Australia RBA Rate Statement

05:00 Japan Leading Economic Index June 110.7 108.0 107.0

05:00 Japan Coincident Index June 106.0 105.1 105.2

The yen rose against most major peers amid speculation the Bank of Japan will refrain from adding to stimulus at a meeting starting tomorrow, with Prime Minister Shinzo Abe still to detail fresh policies to boost growth.

The dollar fell for a third day versus the yen before Federal Reserve Bank of Chicago President Charles Evans speaks after jobs data last week missed estimates. Cleveland Fed President Sandra Pianalto is due to speak on monetary policy and the economic outlook at the Center for Community Solutions Annual Human Services Institute on tomorrow.

The euro was near a seven-week high ahead of a report forecast to show German factory orders rebounded and the Italian economy contracted at a slower pace. German factory orders, adjusted for seasonal swings and inflation, rose 1 percent from May, when they fell 1.3 percent, economists forecast in a Bloomberg News survey before the Economy Ministry releases the data today.

New Zealand’s currency rose after Fonterra Cooperative Group Ltd. said milk products it offers at auction today will meet any additional standards set by China.

Australia’s dollar rose as the central bank cut borrowing costs to a record low and said the currency remains strong. Australian government bonds slid after the Reserve Bank reduced the overnight cash rate by a quarter percentage point to 2.5 percent, the highest benchmark borrowing costs among developed central banks along with New Zealand’s. The Australian dollar sank 11 percent in 2013 through yesterday, the sharpest drop among 10 developed market currencies tracked by Bloomberg Correlation Weighted Indexes. The reduction was the second this year, and extends an easing cycle that began in November 2011, when the benchmark rate was lowered from 4.75 percent.

EUR / USD: during the Asian session the pair is trading around the $ 1.3260

GBP / USD: during the Asian session the pair is trading around the $ 1.5355

USD / JPY: during the Asian session the pair fell to Y97.85

There is another full calendar on both sides of the Atlantic Tuesday. Up first is the Italian June industrial output data. Economists are looking for a rise of 0.3% on month and a fall of 3.5% on year. Italian second quarter GDP is expected at 0900GMT. Economists are looking for a 0.4% fall on the quarter, down 2.2% on year. Germany June manufacturing orders are expected at 1000GMT. The UK July SMMT Car Registrations data is also expected at 0800GMT. That will be followed by the June Industrial Production data at 0830GMT.

-

06:21

Commodities. Daily history for Aug 5’2013:

Change % Change Last

GOLD 1,300.90 -9.70 -0.74%

OIL (WTI) 106.49 -0.45 -0.42%

-

06:20

Stocks. Daily history for Aug 5’2013:

Nikkei 225 14,258.04 -208,12 -1,44%

Hang Seng 22,224.82 33,85 0,15%

S & P / ASX 200 5,111.25 -5.51 -0.11%

Shanghai Composite 2,050.48 21,06 1,04%

FTSE 100 6,619.58 -28.29 -0.43%

CAC 40 4,049.97 +4.32 +0.11%

DAX 8,398.38 -8.56 -0.10%

DJIA 15,612.10 -46.23 -0.30%

S&P 500 1,707.14 -2.53 -0.15%

NASDAQ 3,692.95 3.36 0.09%

-

06:20

Currencies. Daily history for Aug 5'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3261 +0,39%

GBP/USD $1,5356 +1,56%

USD/CHF Chf0,9275 -0,96%

USD/JPY Y98,24 -1,27%

EUR/JPY Y130,29 -0,87%

GBP/JPY Y150,84 +0,29%

AUD/USD $0,8932 -0,03%

NZD/USD $0,7850 -0,60%

USD/CAD C$1,0358 +0,08%

-

06:06

Schedule for today, Tuesday Aug 6’2013:

01:30 Australia Trade Balance June 0.50 Revised From 0.67 0.81 0.60

01:30 Australia ANZ Job Advertisements (MoM) July -1.8% -6.8%

01:30 Australia House Price Index (QoQ) Quarter II +0.8% Revised From +0.1% +1.3% +2.4%

01:30 Australia House Price Index (YoY) Quarter II +2.6% +3.0% +5.1%

04:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50%

04:30 Australia RBA Rate Statement

05:00 Japan Leading Economic Index June 110.7 108.0

05:00 Japan Coincident Index June 106.0 105.1

07:00 United Kingdom Halifax house price index July +0.6% +0.3%

07:00 United Kingdom Halifax house price index 3m Y/Y July +3.7% +4.3%

08:30 United Kingdom Industrial Production (MoM) June 0.0% +0.7%

08:30 United Kingdom Industrial Production (YoY) June -2.3% +0.8%

08:30 United Kingdom Manufacturing Production (MoM) June -0.8% +0.9%

08:30 United Kingdom Manufacturing Production (YoY) June -2.9% +1.0%

10:00 Germany Factory Orders s.a. (MoM) June -1.3% +1.1%

10:00 Germany Factory Orders n.s.a. (YoY) June -2.0% -0.3%

12:30 Canada Trade balance, billions June -0.3 -0.5

12:30 U.S. International trade, bln June -45.0 -43.1

14:00 United Kingdom NIESR GDP Estimate July +0.6%

14:00 U.S. JOLTs Job Openings June 3828 3900

17:00 U.S. FOMC Member Charles Evans Speaks

20:30 U.S. API Crude Oil Inventories July -0.7

22:45 New Zealand Employment Change, q/q Quarter II +1.7% +0.4%

22:45 New Zealand Unemployment Rate Quarter II 6.2% 6.3%

-

06:01

Japan: Coincident Index, June 105.2 (forecast 105.1)

-

06:01

Japan: Leading Economic Index , June 107.0 (forecast 108.0)

-

05:30

Australia: Announcement of the RBA decision on the discount rate, 2.50% (forecast 2.50%)

-