Notícias do Mercado

-

20:00

Dow 16,431.72 +9.83 +0.06%, Nasdaq 4,329.55 -22.58 -0.52%, S&P 500 1,876.37 -0.66 -0.04%

-

18:21

European stocks close

European stocks slid, completing their first weekly decline since January, as Russia said it may cut off Ukraine’s gas, outweighing a report that showed the U.S. economy created more jobs last month than forecast.

The Stoxx Europe 600 Index dropped 1.3 percent to 333.06 at the close of trading. The benchmark has fallen 1.5 percent this week amid concern that Russia would intervene in Ukraine, resulting in sanctions and disrupted trade. European equities slid 2.3 percent on March 3 after Russia’s parliament authorized President Vladimir Putin to send troops into Ukraine.

Russia said Ukraine must pay off almost $2 billion owed for natural gas today and signaled supplies may otherwise be cut. The two countries have clashed over control of Ukraine’s Crimea region, where a majority of people speak Russian. Lawmakers in Moscow said they would accept the results of a March 16 referendum on Crimea joining Russia, while Ukrainian Prime Minister Arseniy Yatsenyuk reiterated that his cabinet deems the vote illegal.

A Labor Department report showed that employers in the U.S. added 175,000 jobs in February. That exceeded the median estimate of 149,000 net hires in a Bloomberg News survey of economists. The government revised its figure for January to 129,000 from 113,000.

A release yesterday showed claims for unemployment benefits fell to a three-month low last week, indicating that companies are holding on to staff because they anticipate economic growth will rebound following the harsh winter weather.

Benchmark indexes retreated in every western-European market except Greece. Germany’s DAX fell 2 percent, while France’s CAC 40 dropped 1.2 percent. The U.K.’s FTSE 100 slipped 1.1 percent.

Getinge slumped 21 percent to 182.80 kronor. The Swedish maker of sterilization systems forecast first-quarter pretax profit of 160 million kronor ($25 million), roughly a quarter of the average analyst estimate of 629 million kronor. A gauge of health-care companies on the Stoxx 600 fell 1.4 percent.

Fugro declined 2.1 percent to 40.83 euros. The Dutch company posted revenue of 2.42 billion euros ($3.4 billion) for last year, less than the 2.63 billion euros that analysts had estimated. Its net income of 428 million euros fell short of the 444 million-euro average in a Bloomberg survey.

Air France-KLM climbed 4.4 percent to 10.40 euros, rising for the fourth day to its highest price since July 2011. Europe’s largest airline said it flew 5.34 million passengers in February, a 1.8 percent increase from a year earlier.

FLSmidth & Co. added 2.5 percent to 295.60 kroner. The Danish mining-equipment supplier named Lars Vestergaard as its new chief financial officer, saying Ben Guren will leave the company for personal reasons.

-

17:00

European stocks closed in minus: FTSE 100 6,712.67 -75.82 -1.12%, CAC 40 4,366.42 -50.62 -1.15%, DAX 9,350.75 -192.12 -2.01%

-

16:42

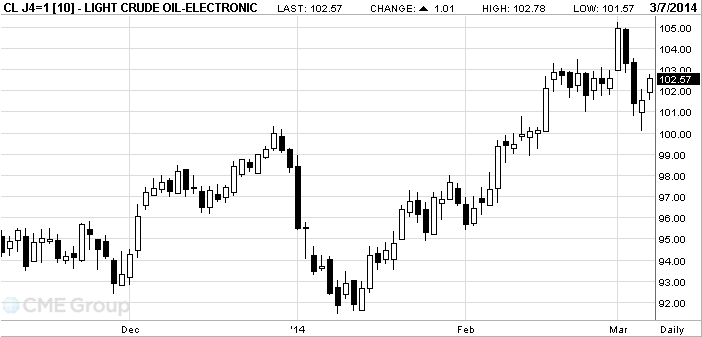

Oil rose

West Texas Intermediate crude rose for a second day after

Futures increased as much as 1.1 percent in

Bloomberg survey estimates of 92 economists for February payrolls ranged from gains of 100,000 to 220,000.

Unemployment rose to 6.7 percent from 6.6 percent as more people entered the labor force and couldn’t find work, the data released today in

U.S. President Barack Obama signed an order authorizing financial sanctions against

The flow of Russian crude through Ukraine to Europe in the southern branch of the Druzhba oil pipeline is uninterrupted, Natalya Kutsik, a spokeswoman for Russia’s oil pipeline operator OAO Transneft, said by text message. The link carried about 300,000 barrels a day last year, according to data from

WTI for April delivery increased 89 cents, or 0.9 percent, to $102.45 a barrel at 10:40 a.m. on the New York Mercantile Exchange. Prices are down 0.1 percent this week. The volume of all futures traded was 2.4 percent above the 100-day average.

Brent for April settlement rose 36 cents, or 0.3 percent, to $108.46 a barrel on the London-based ICE Futures Europe exchange. Trading volume was near the 100-day average. The European benchmark was at a $6.01 premium to WTI, down from $6.54 at yesterday’s close.

-

16:20

Gold fell on a report on employment

Gold pullback from 4 -month high after the release of surprisingly strong data on the U.S. labor market .

U.S. labor market in February showed a marked improvement in February , beating estimates of experts. However, growth remains subdued and unemployment is consistently high.

The Labor Department said that the number of non-farm payrolls increased seasonally adjusted 175 million in February , compared with a rise of 129 million in January , which was revised up from 113 thousand also added that the increase in December also been revised - to 84 thousand 75 thousand

But despite the marked improvement , the unemployment rate also rose - to 6.7 % from 6.6 % in January. The labor force grew, but also allow the number of unemployed . Economists forecast that the number of employees will be at the level of 151 thousand and the unemployment rate - 6.6%.

Gold rose this year by 12% in terms of demand for safe assets due to concern growth of the U.S. economy , as well as Ukrainian crisis erupted . However, the results of the report on the U.S. labor market helped ease tensions.

Demand for gold in the physical market fell after the price exceeded $ 1,300 . Margins on the spot market of China on Friday below $ 1 per ounce , compared with more than $ 20 early this year.

The cost of the April gold futures on the COMEX today dropped to $ 1326.60 per ounce.

-

14:34

U.S. Stocks open: Dow 16,470.44 +48.55 +0.30%, Nasdaq 4,367.77 +15.64 +0.36%, S&P 1,883.09 +6.06 +0.32%

-

14:18

Before the bell: S&P futures +0.50%, Nasdaq futures +0.39%

U.S. stock futures rose as a faster-than-estimated jump in payrolls indicated the economy is starting to bounce back from a weather-induced setback.

Global markets:

Nikkei 15,274.07 +139.32 +0.92%

Hang Seng 22,660.49 -42.48 -0.19%

Shanghai Composite 2,057.91 -1.67 -0.08%

FTSE 6,791.24 +2.75 +0.04 %

CAC 4,424.28 +7.24 +0.16 %

DAX 9,517.78 -25.09 -0.26 %

Crude oil $102.04 (+0.47%)

Gold $1337.00 (-1.09%).

-

13:47

Option expiries for today's 1400GMT cut

USD/JPY Y101.00, Y101.25, Y101.50, Y102.00, Y102.50, Y102.80-90, Y103.00-05, Y103.30, Y103.50

EUR/USD $1.3600, $1.3605, $1.3650, $1.3700, $1.3750, $1.3800

GBP/USD $1.6550, $1.6580, $1.6600, $1.6750, $1.6800, $1.6850

EUR/GBP stg0.8125-35, stg0.8150, stg0.8200, stg0.8300

GBP/JPY Y172.00, Y173.00

AUD/USD $0.8900, $0.8910, $0.8945, $0.8995, $0.9000, $0.9025, $0.9060, $0.9130

USD/CAD C$1.0950, C$1.1000, C$1.1025, C$1.1050, C$1.1100, C$1.1150, C$1.1175, C$1.1200

-

13:32

U.S.: Average workweek, February 34.2 (forecast 34.4)

-

13:31

Canada: Unemployment rate, February 7.0% (forecast 7.0%)

-

13:31

Canada: Employment , February -7.0 (forecast 16.9)

-

13:31

U.S.: Average hourly earnings , February +0.4% (forecast +0.2%)

-

13:31

U.S.: International Trade, bln, January -39.1 (forecast -39.1)

-

13:31

Canada: Trade balance, billions, January -0.2 (forecast -1.6)

-

13:30

U.S.: Nonfarm Payrolls, February 175 (forecast 151)

-

13:30

U.S.: Unemployment Rate, February 6.7% (forecast 6.6%)

-

13:15

European session: the euro continued yesterday's rise against the U.S. dollar

Data

05:00 Japan Leading Economic Index January 111.7 112.4 112.2

05:00 Japan Coincident Index January 111.7 114.6 114.8

06:30 Switzerland Unemployment Rate February 3.2% 3.2% 3.2%

08:00 Switzerland Foreign Currency Reserves February 437.7 433.5

08:15 Switzerland Consumer Price Index (MoM) February -0.3% +0.4% +0.1%

08:15 Switzerland Consumer Price Index (YoY) February +0.1% +0.1% -0.1%

09:30 United Kingdom Consumer Inflation Expectations Quarter I +3.6% +2.8%

11:00 Germany Industrial Production s.a. (MoM) January +0.1% Revised From -0.6% +0.7% +0.8%

11:00 Germany Industrial Production (YoY) January +2.6% +5.0%

The euro exchange rate has risen considerably against the U.S. dollar , reaching at this level of $ 1.3915 . Positive attitude to the euro yesterday fueled refusal of additional ECB easing measures . Now the market is waiting for data on employment in the United States. According to the median forecast of economists , farm employment in February increased from 113 thousand to 151 thousand , while maintaining the level of unemployment at around 6.6 %, which would be welcomed by the markets. However, published earlier in the week ADP figure was worse than expected and so the official figures may also disappoint . Meanwhile, the positive signals are stored . Yesterday, the U.S. Labor Department reported that the number of initial claims for unemployment benefits in the U.S. last week fell by 26 thousand and reached 323 thousand Analysts believed that the number of jobless claims to fall by only 12 thousand

Positive impact on the dynamics of German data , which showed that the unusually warm winter has helped to raise industrial production. Industrial production rose 0.8% in January, exceeding economists' expectations of 0.7 %. Value in December was also revised upward - to 0.1 % from -0.6 %. Data follows the unexpectedly strong production orders in January , which suggest that the German economy was strong earlier this year. Overall increase in orders - a consequence of the growth of their domestic orders and orders outside the EU ( 7.2 %). On the other hand , the orders of the currency bloc fell by almost 9 % m / m Note that the German economy grew by 0.4 % in the fourth quarter of last year , is expected to add almost 2 % in 2014 as a whole.

Pound was able to compensate for their morning dip against the dollar, and even reached highs yesterday. Helped this data , which showed that the expectations of the British against rising interest rates over the next year are on the rise , even despite the fact that their inflation forecasts down . It became known from the quarterly survey , which was presented to the Bank of England . Add that this survey was conducted in the period from 6 to 18 February , and it was attended by 3949 people.

According to the data , 40 percent of Britons expect growth rates over the next 12 months , compared with 34 percent in November , the highest level since May 2012 . However , inflation expectations for the next year fell to 2.8 percent from 3.6 percent , and reached its lowest value in the last four years. Inflation expectations over the next two to five years also fell to its lowest level since August 2012 . Ratings inflation is likely to support the Bank of England's message that we should not rush to increase interest rates.

The Australian dollar gained new impetus and continued gains against the U.S. dollar, which has lasted for a fifth straight day . This allowed the peak for 3 months . Pair manages to break above the 0.9100 mark , despite comments RBA head Stevens , who said earlier that the rate at above 0.9000 is overpriced . Stevens also said that in anticipation of weakening labor market and a corresponding reduction in wages , as well as under the influence of the reduction of investment in the natural resources sector , the main task " very adaptive ," monetary policy is to stimulate the real estate market . " Projected inflation will meet the target level for the next two years , despite the fact that today it remains at a higher level than before. The overall economic situation in the country - regardless of the reduction in demand for labor , reducing wages , inflation - probably would not have a significant pressure on the national currency of Australia. Especially the demand from foreign central banks contributed to the strengthening of the Australian dollar , " - said Stevens.

Since the beginning of the week the Australian dollar rose more than two figures give support to such factors as rising risk appetite , the RBA decision to leave the rate unchanged monetary policy and strong national macro .

EUR / USD: during the European session, the pair rose to $ 1.3915

GBP / USD: during the European session, the pair fell to $ 1.6720 , but then rose to $ 1.6784

USD / JPY: during the European session, the pair dropped to Y102.82, then retreated to Y103.00

At 13:30 GMT Canada said the unemployment rate and the change in the number of employed in February , changing the level of productivity in the 4th quarter , and will report on its trade balance for January. At 13:30 GMT the U.S. will release data on its trade balance in January , the unemployment rate for February and to change the number of people employed in non-farm payrolls in February.

-

13:00

Orders

EUR/USD

Offers $1.4000, $1.3950/60, $1.3937, $1.3920, $1.3900

Bids $1.3850, $1.3835/30, $1.3810/790, $1.3770, $1.3750, $1.3710/00

GBP/USD

Offers $1.6823, $1.6795/800, $1.6770/80

Bids $1.6702, $1.6700/695, $1.6662, $1.6650/40, $1.6617, $1.6605/00

AUD/USD

Offers $0.9200, $0.9165, $0.9150

Bids $0.9065, $0.9050, $0.9010/00, $0.8991, $0.8950, $0.8920, $0.8916/10

EUR/JPY

Offers Y144.50, Y144.00, Y143.80, Y143.50, Y143.20

Bids Y142.50, Y142.20, Y142.00, Y141.55/50, Y141.10/00

USD/JPY

Offers Y103.65, Y103.50, Y103.20

Bids Y102.50/60, Y102.20, Y102.00, Y101.80, Y101.50, Y101.20

EUR/GBP

Offers stg0.8333, stg0.8300/05, stg0.8295

Bids stg0.8270, stg0.8260, stg0.8204, stg0.8190-80, stg0.8160, stg0.8150

-

11:45

European stock fell

European stocks fell , heading for its first weekly decline since January , which is associated with a fall sensor healthcare companies, as well as expectations of U.S. employment data. U.S. index futures are mixed , while Asian stocks rose .

According to the median forecast of economists , farm employment in February increased from 113 thousand to 151 thousand , while maintaining the level of unemployment at around 6.6 %, which would be welcomed by the markets. However, published earlier in the week ADP figure was worse than expected and so the official figures may also disappoint. Meanwhile, the positive signals are stored . Yesterday, the U.S. Labor Department reported that the number of initial claims for unemployment benefits in the U.S. last week fell by 26 thousand and reached 323 thousand Analysts believed that the number of jobless claims to fall by only 12 thousand

The Stoxx Europe 600 Index fell 0.4 percent. Since the beginning of the week , the index fell by 0.6 percent. We add that the Stoxx 600 fell 2.3 percent on March 3 after the Russian parliament authorized the President Vladimir Putin to send troops to Ukraine. U.S. President Barack Obama signed an executive order authorizing financial sanctions , while EU leaders stopped trade and visa negotiations with Russia and threatened punitive economic measures .

Getinge shares fell 18 percent. The Swedish company said first-quarter profit before tax amounted to 160 million euros ( 25 million dollars), compared with the average estimate at 629 million kroons.

Fugro cost decreased by 6.6 percent . The Dutch company reported revenue in the amount of 2.42 billion euros last year , which was less than estimates - at the level of 2630 million euros.

Paper Air France-KLM rose 4.2 percent , recording the fourth -session increase in a row and reached the highest level since July 2011 . The largest airline in Europe, said that the number of passengers in February, increased in February by 1.8 percent compared with a year earlier.

At the current moment

FTSE 100 6,785.29 -3.20 -0.05 %

CAC 40 4,412.44 -4.60 -0.10%

DAX 9,505.98 -36.89 -0.39%

-

11:01

Germany: Industrial Production (YoY), January +5.0%

-

11:00

Germany: Industrial Production s.a. (MoM), January +0.8% (forecast +0.7%)

-

10:21

Option expiries for today's 1400GMT cut

USD/JPY Y101.00, Y101.25, Y101.50, Y102.00, Y102.50, Y102.80-90, Y103.00-05, Y103.30, Y103.50

EUR/USD $1.3600, $1.3605, $1.3650, $1.3700, $1.3750, $1.3800

GBP/USD $1.6550, $1.6580, $1.6600, $1.6750, $1.6800, $1.6850

EUR/GBP stg0.8125-35, stg0.8150, stg0.8200, stg0.8300

GBP/JPY Y172.00, Y173.00

AUD/USD $0.8900, $0.8910, $0.8945, $0.8995, $0.9000, $0.9025, $0.9060, $0.9130

USD/CAD C$1.0950, C$1.1000, C$1.1025, C$1.1050, C$1.1100, C$1.1150, C$1.1175, C$1.1200

-

10:02

Asia Pacific stocks close

Asia’s benchmark stock index headed for its fourth straight weekly advance as investors awaited U.S. jobs data. Energy and industrial shares led gains today.

Nikkei 225 15,274.07 +139.32 +0.92%

S&P/ASX 200 5,462.31 +16.42 +0.30%

Shanghai Composite 2,057.91 -1.67 -0.08%

China Petroleum & Chemical Corp., the refiner better known as Sinopec, climbed 3.4 percent in Hong Kong after Premier Li Keqiang reiterated this week that China would allow private investment in oil and power projects.

Fanuc Corp., a factory-robotics maker that get 78 percent of sales overseas, gained 1.8 percent in Tokyo as exporters advanced with the yen trading near a five-week low against the dollar.

Great Wall Motor Co. dropped 2.5 percent in Hong Kong after reporting slower sales.

-

09:30

United Kingdom: Consumer Inflation Expectations, Quarter I +2.8%

-

09:02

FTSE 100 6,765.97 -22.52 -0.33%, CAC 40 4,407.97 -9.07 -0.21%, Xetra DAX 9,474.89 -67.98 -0.71%

-

08:15

Switzerland: Consumer Price Index (MoM) , February +0.1% (forecast +0.4%)

-

08:15

Switzerland: Consumer Price Index (YoY), February -0.1% (forecast +0.1%)

-

08:01

Switzerland: Foreign Currency Reserves, February 433.5

-

06:42

European bourses are initially seen opening higher Friday: the FTSE is seen opening 0.2% higher, with both the CAC and DAX seen higher by 0.3%

-

06:21

Asian session: The dollar was set for its biggest weekly gain in three months versus the yen

05:00 Japan Leading Economic Index January 111.7 112.4 112.2

05:00 Japan Coincident Index January 111.7 114.6 114.8

The dollar was set for its biggest weekly gain in three months versus the yen before the release of U.S. payrolls data, with Federal Reserve officials reiterating the threshold for changing its stimulus tapering is high. The U.S. probably added 149,000 jobs in February, after a 113,000 increase a month earlier, according to the median estimate in a Bloomberg News survey of economists taken before the Labor Department report today. Payroll gains averaged almost 200,000 a month in 2013.

The U.S. currency yesterday touched its strongest versus the yen since January as reports showed fewer Americans filed claims for jobless benefits. Jobless claims fell by 26,000 to 323,000 in the week ended March 1, the least since the end of November and fewer than the lowest forecast in a Bloomberg poll, data showed yesterday.

The euro headed for a fifth weekly gain as European Central Bank President Mario Draghi damped speculation of further monetary easing. The ECB left its benchmark interest rate at 0.25 percent at a meeting in Frankfurt yesterday as forecast by 40 out of 54 economists surveyed by Bloomberg News. The other 14 were predicting a rate cut.

Australia’s dollar held near its highest in almost three months as central bank Governor Glenn Stevens said he doesn’t see a need to cut interest rates. He said he doesn’t see the need to loosen already “very accommodative” monetary policy “at this point in time.”

EUR / USD: during the Asian session, the pair traded in the range of $ 1.3855-65

GBP / USD: during the Asian session the pair traded in the range of $ 1.6725-45

USD / JPY: on Asian session the pair fell to Y102.85

With the policy decisions from both the ECB and BOE behind us, the markets now focus their attention across the Atlantic on the US employment report. Ahead of the jobs data, there is a full calendar in Europe, starting with the release of the Swiss National Bank's annual results, due at 0630GMT. Other Swiss data set for an early release includes the February unemployment data at 0645GMT. At 0700GMT, the German January wholesale prices data will be published. French data due at 0745GMT includes the January foreign trade data and the January budget balance. At 0800GMT, Spain's January industrial output numbers will cross the wires. There is further Swiss data set for release at 0815GMT, when the February CPI numbers cross the wires. The last German release of the day comes at 1100GMT, when the January industrial orders data is published. German Chancellor Angela Merkel and Irish Prime Minister Enda Kenny will hold a joint press conference, in Dublin at 1200GMT.

-

05:06

Japan: Coincident Index, January 114.8 (forecast 114.6)

-

05:05

Japan: Leading Economic Index , January 112.2 (forecast 112.4)

-