Notícias do Mercado

-

20:00

Dow +150.9 15,073.40 +1.01% Nasdaq +44.81 3,704.82 +1.22% S&P +16.00 1,671.17 +0.95%

-

20:00

U.S.: Consumer Credit , July 10.4 (forecast 12.7)

-

19:20

American focus : the U.S. dollar significantly weakened against major currencies

The dollar declined significantly against the euro, because of the uncertainty around the reduction of quantitative easing in the U.S. . We also add that the markets are still analyzing the data on non-farm payrolls , which were released on Friday . Investors expect the Fed will begin reducing incentives in September , despite the negative statistics

Meanwhile , we note that the growth of the euro was supported by news from the Bank of France. The Bank of France said Monday that the revised upward its growth estimate for the French economy in the third quarter and now expects gross domestic product expanded by 0.2 % q / q.

In the previous forecast of the central bank of France was expecting growth of 0.1 % in the third quarter compared with the previous quarter . The French economy grew by 0.2 % in the second quarter, after two consecutive quarters of reductions .

The Bank of France reported that business sentiment in August showed a slight improvement in most industries , with higher supplies and lower stocks, and business leaders are expected to accelerate activity in September.

The yen rose against the dollar, which , in the first place , helped publish a report on the GDP . As shown by the final data from the Cabinet of Ministers , which were published yesterday in the second quarter , Japan's economy grew more than initially thought , but still not enough to confirm the predictions of experts.

According to the report . Japan's gross domestic product grew by 0.9 % in the second quarter of 2013 compared with the previous three months. We add that the final figure was higher than the preliminary estimate at 0.6 % , which was published on August 12. It should also be noted that according to the average forecasts of experts the economy were to expand by 1.0 %.

In the Cabinet of Ministers also reported that the annual rate of gross domestic product was revised to 3.8 % from 2.6 % in the preliminary reading, which was slightly below economists' forecast of 3.9 percent growth . We also recall that in the first quarter economic growth rate was 4.1%.

Nominal GDP , meanwhile, grew by 0.9 % in the quarter , which was slightly more than the initial assessment at the level of 0.7% , but still below the expectations of experts at the level of 1.0 %, which was followed after increasing 0.6 % in the previous quarter.

The pound has appreciated strongly against the dollar as risk appetite and , as a consequence, the British currency is still prevalent among traders. It should be noted that today the pair rose sharply, leaving behind a mark of $ 1.5700 and tested the multi-week peak around $ 1.5730 . Risk sentiment continued to dominate the currency markets at the beginning of this week, but volatility may be somewhat exaggerated view of an empty economic calendar in the euro area and the United States . Experts point out that it is still the balance of risks indicates a weakening of the pound by the end of the year, as there is no confidence in the stability of the British economy recovery . According to estimates , the rate of growth are exaggerated , but the rise in consumer spending may not correspond to the declared rate of economic growth , given the sluggish increase in wages.

-

18:20

European stock close

European stocks were little changed after their biggest weekly advance since April, as Chinese exports rose more than expected and investors awaited a U.S. decision this week on possible air strikes against Syria.

The Stoxx Europe 600 Index lost 0.1 percent to 305.75 at 4:30 p.m. in London. The gauge advanced 0.5 percent on Sept. 6 as investors assessed whether the Federal Reserve will reduce its monthly bond purchases after data showed the U.S. economy added fewer jobs last month than expected.

China’s exports increased more in August than forecast and inflation stayed below a government target. Overseas shipments rose 7.2 percent from a year earlier, the General Administration of Customs said in Beijing yesterday. That beat the 5.5 percent median estimate of analysts. Consumer prices rose 2.6 percent, the statistics bureau said today.

Obama this week will seek to persuade a skeptical Congress and a reluctant American public to support air strikes against Syria. He failed to win backing from foreign leaders at last week’s Group of 20 summit for military action in response to a chemical weapons attack that his administration said killed more than 1,400 people.

National benchmark indexes fell in 11 of the 18 western European markets today.

FTSE 100 6,530.74 -16.59 -0.25% CAC 40 4,040.33 -8.86 -0.22% DAX 8,276.32 +0.65 +0.01%

BG (BG/) fell 5.6 percent to 1,210.5 pence, its biggest drop since October 2012. Turmoil in Egypt has delayed the West Delta Deep Marine project and first production from the Knarr project in Norway has been pushed back four months to the second half of next year. The combined impact will shave 30,000 barrels a day off next year’s production. BG will also operate fewer rigs in the U.S., reducing next year’s volumes by 17,000 barrels a day, the Reading-based company said.

EON SE and RWE AG, Germany’s two biggest utilities, fell 1.9 percent to 12.46 euros and 1.8 percent to 22.85 euros, respectively. Bank of America Corp. downgraded EON’s shares to underperform, similar to a sell rating, from neutral, citing “misplaced optimism” and the likelihood of lower power prices.

HSBC Holdings Plc cut its projected price targets on EON and RWE’s shares to 10 euros and 18 euros, respectively, saying the harsh trading environment will continue.

Munich Re jumped 3.3 percent to 139.45 euros. Bank of America upgraded the world’s biggest reinsurer from neutral to buy, citing the recent overdone share-price weakness, its strong capital position and lower exposure to catastrophe reinsurance relative with its peers. Shares have lost 12 percent since reaching their highest price in more than 10 years on April 25.

Vallourec rose 3.4 percent to 47.70 euros after Kepler Cheuvreux upgraded the shares to buy from hold, citing significant price hikes by its U.S. competitors.

Christian Dior SA (CDI) advanced 3.2 percent to 136.35 euros as the French luxury goods maker announced that it has entered into a forward purchase agreement with an authorized financial intermediary to buy a maximum 550,000 of its own shares.

-

17:00

European stock close: FTSE 100 6,530.74 -16.59 -0.25% CAC 40 4,040.33 -8.86 -0.22% DAX 8,276.32 +0.65 +0.01%

-

16:40

Oil: an overview of the market situation

The cost of oil futures declined markedly today , departing from the two-year high against the background of the fact that President Barack Obama is struggling to convince Congress of the need for a military strike on Syria . Negative dynamics of oil prices is also due to profit-taking , which was formed in the previous two sessions .

It should be noted that today the U.S. Congress returns to work after the summer break , which lasted more than a month . Also on this day, the U.S. president is scheduled interviews with five television channels regarding Syria , and on Tuesday Barack Obama will make a televised address to the nation on the same topic. The administration , according to the latest data , while not gained enough votes in the Senate. But the most difficult for the White House situation in the House of Representatives, where , according to media reports , the opponents of the resolution may constitute a majority.

However, the decrease in the price of oil futures contribute on the decline in August, China's oil imports . According to the report , in August, China's oil imports fell relative to July by 18 % (from 6.15 million bbl. / Day to 5.07 million barrels. / Day ), which has raised fears of weakening global demand for energy.

Meanwhile, we note that the data published by the General Administration of Customs of China showed that export growth accelerated in August to 7.2 percent from 5.1 percent in July . Imports, meanwhile, grew at a slower pace - by 7 per cent, which was followed after an increase of 10.9 percent in July , contributing to the growth of the trade surplus to $ 28.6 billion from $ 17.8 billion add that surplus was higher than forecasts of experts at $ 20 billion.

The cost of the October futures on U.S. light crude oil WTI (Light Sweet Crude Oil) fell to $ 109.82 a barrel on the New York Mercantile Exchange.

October futures price for North Sea Brent crude oil mixture fell $ 1.46 to $ 114.25 a barrel on the London exchange ICE Futures Europe.

-

16:21

Gold: an overview of the market situation

Gold prices fell slightly today , but still reduced their early losses , as many market participants continue to analyze Friday's U.S. employment data . In addition, the course of trade affect the expectations that the Fed may still insist on some reduction of monetary stimulus . Note that the assumptions on the fact that the U.S. central bank may cut back on their monthly purchases of bonds in the amount of $ 85 billion , which is a key factor in price increases, contributed to the fall in gold prices this year by 17 % after more than a decade of growth.

Also today it was announced that hedge funds and other speculators increased bullish positions in gold , amid concerns that the conflict in the Middle East will drive the price of crude oil will slow down economic growth and ignite inflation.

Net long positions rose by 3.6 percent to 101,396 futures and options in the week ended Sept. 3 , - data showed US Commodity Futures Trading Commission. Long positions rose 0.6 percent, and short contracts fell by 8.6 percent . Net bullish stance on U.S. 18 tradable goods fell 0.3 percent, as investors have become less optimistic about copper.

Meanwhile, we add that many traders are closely watching the Indian demand for gold, which usually reaches its peak in the fourth quarter against the fact that officials of the largest consumption of gold country in the world have taken measures to curb imports in an attempt to reduce a record current account deficit .

The cost of the October gold futures on COMEX today rose to $ 1388.20 per ounce.

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.3050, $1.3100, $1.3110, $1.3120, $1.3200, $1.3245, $1.3250

USD/JPY Y98.50, Y98.60, Y99.00, Y99.25, Y99.50, Y100.00, Y100.75, Y100.90, Y101.00

EUR/JPY Y130.75

GBP/USD $1.5500, $1.5600

USD/CHF Chf0.9425, Chf0.9480

EUR/CHF Chf1.2345

AUD/USD $0.9000, $0.9020, $0.9100, $0.9160, $0.9200

AUD/NZD NZ$1.1450

AUD/JPY Y91.50

USD/CAD C$1.0400, C$1.0475

-

14:35

U.S. Stocks open: Dow 14,982.56 +60.06 +0.40%, Nasdaq 3,680.81 +20.80 +0.57%, S&P 1,662.15 +0.42%

-

14:29

Before the bell: S&P futures +0.27%, Nasdaq futures +0.49%

U.S. stock-index futures rose as exports from China topped forecasts.

Global Stocks:

Nikkei 14,205.23 +344.42 +2.48%

Hang Seng 22,750.65 +129.43 +0.57%

Shanghai Composite 2,212.52 +72.52 +3.39%

FTSE 6,513.2 -34.13 -0.52%

CAC 4,027.18 -22.01 -0.54%

DAX 8,268.95 -6.72 -0.08%

Crude oil $109.97 -0.51%

Gold $1388.40 +0.14%

-

13:45

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Other:

Apple (AAPL) target raised to $600 from $575 at FBN Securities

Wal-Mart (WMT) resumed with a Buy at Goldman

-

13:45

Eurozone investor confidence rises sharply in September: Sentix

Eurozone's investor confidence increased in September to the second-highest level on record, and to a significantly larger extent than economists had forecast, as the region emerged from its long-drawn recession in the second quarter, a closely watched survey revealed Monday.

Data from a survey conducted by think-tank Sentix showed that the headline investor confidence index for the Eurozone climbed to

Economists were looking for a score of -4. The September reading was the highest since May 2011. The headline index has returned to the positive territory for the first time since July 2011.

In September, Euro area investors were notably less downbeat about the current situation, with the corresponding sub-indicator rising sharply to a two-year high of -8.8 from

At the same time, the measure of respondents' expectations for investments over the next 6-month period advanced to 23 from

-

13:30

Canada: Building Permits (MoM) , July +20.7% (forecast +4.4%)

-

13:17

European session: the euro rose

05:45 Switzerland Unemployment Rate August 3.0% 3.0% 3.2%

06:00 Japan Eco Watchers Survey: Current August 52.3 53.8 51.2

06:00 Japan Eco Watchers Survey: Outlook August 53.6 51.2

07:15 Switzerland Retail Sales Y/Y July +2.3% +3.2% +0.8%

08:30 Eurozone Sentix Investor Confidence September -4.9 -4.0 +6.5

The euro strengthened against the U.S. dollar . After 26 months of negative performance index of confidence of European investors Sentix jumped in August to around 6.5 -4.9 against the July results . Analysts had expected growth to only -4.0 .

The yen rose against the dollar and the euro after a report by Japan's GDP for the second quarter of 2013, which increased by 3.8 % compared to the second quarter of 2012. Previously reported increase of GDP in the April-June by 2.6 %, after 4.1% in January- March. Analysts had expected a more significant revision - to 3.9 %. Evaluation of nominal GDP in the 2nd quarter compared to the 1st quarter without converting to an annual rate improved from 0.7 % to 0.9 %. The Cabinet expects economic growth of 2.8% in the current financial year ending 31 March 2014.

The Australian dollar hit a three-week high after the trade surplus of China in August 2013 increased by 60.1 % to $ 28.5 billion from $ 17.8 billion in July. Index reached its highest level since January. China's export growth continues to gain momentum , the growth in August was 7.2 % compared to the same period last year. In July, exports rose by 5.1 %, while the rate in June fell by 3.1 %. The import of the previous month increased by 7 % in annual terms , while in July, an increase of 10.9%. The overall picture shows that the Chinese economy benefits from the gradual strengthening of demand in the U.S. and other major export markets. China also continues to stock raw materials for the industrial sector.

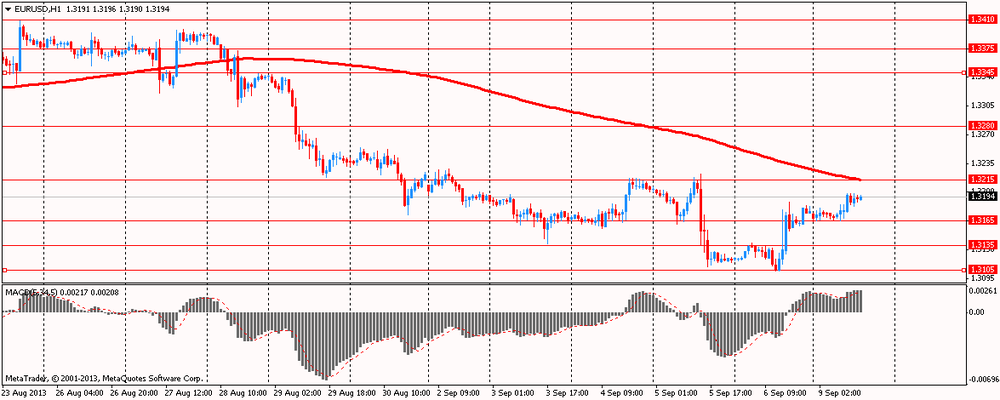

EUR / USD: during the European session, the pair rose to $ 1.3198

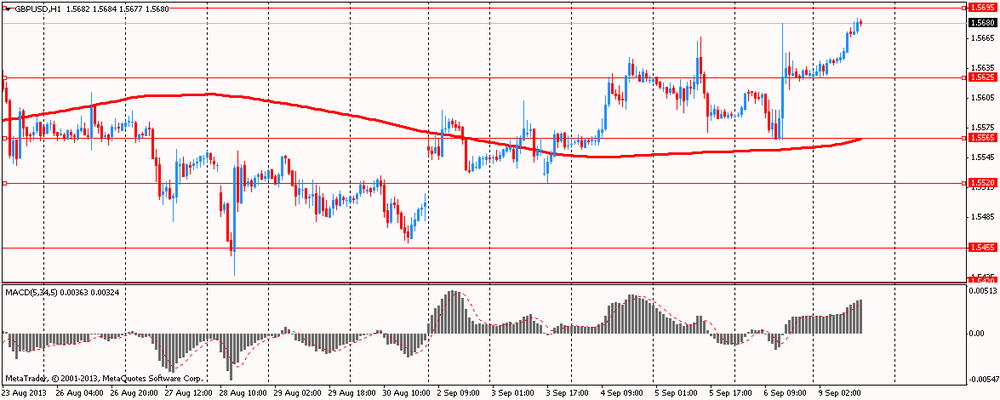

GBP / USD: during the European session, the pair rose to $ 1.5685

USD / JPY: during the European session, the pair fell to Y99.33

At 12:30 GMT Canada will report on changes in the volume of building permits issued in July. At 23:01 GMT Britain will publish house price balance of the RICS in August. At 23:50 GMT the meeting minutes will be published on the Bank of Japan's monetary policy , Japan will release the index of activity in the services sector in July.

-

13:00

Orders

EUR/USD

Offers $1.3290/300, $1.3250/60, $1.3220/25, $1.3200

Bids $1.3150/40, $1.3110/00, $1.3090/85, $1.3080-50, $1.3025/20

GBP/USD

Offers $1.5780/85, $1.5750/55, $1.5720/25, $1.5700/10, $1.5680/85

Bids $1.5630, $1.5600, $1.5565/60, $1.5555/50, $1.5525/20

AUD/USD

Offers $0.9400, $0.9335-50, $0.9300, $0.9270/75, $0.9250, $0.9230/35, $0.9225

Bids $0.9155/50, $0.9100, $0.9080

EUR/GBP

Offers stg0.8550/55, stg0.8520, stg0.8450/65, stg0.8430/35

Bids stg0.8400, stg0.8390, stg0.8380, stg0.8350

EUR/JPY

Offers Y133.00, Y132.50, Y132.20, Y131.80\5/00

Bids Y130.00/9.80, Y129.50, Y129.20, Y129.00, Y128.50

USD/JPY

Offers Y101.00, Y100.80, Y100.50, Y100.20/30

Bids Y99.35/30, Y99.20-00, Y98.50, Y98.25/20, Y98.00

-

11:30

European stocks declined

European stocks declined, after their biggest weekly gain since April, as investor uncertainty about this week’s U.S. vote on possible air strikes against Syria outweighed better-than-expected Chinese export data. U.S futures and Asian shares advanced.

China’s exports increased more in August than forecast and inflation stayed below a government target. Overseas shipments rose 7.2 percent from a year earlier, the General Administration of Customs said in Beijing yesterday. That beat the 5.5 percent median estimate of analysts surveyed by News. Consumer prices rose 2.6 percent, the statistics bureau said today.

Obama this week will seek to persuade a skeptical Congress and a reluctant American public to support air strikes against Syria. He failed to win backing from foreign leaders at last week’s Group of 20 summit for military action in response to a chemical weapons attack that his administration said killed more than 1,400 people.

EON SE and RWE AG, Germany’s two biggest utilities, fell 2.2 percent to 12.42 euros and 2.7 percent to 22.64 euros, respectively. Bank of America Corp. downgraded EON’s shares to underperform, similar to a sell rating, from neutral, citing “misplaced optimism” and the likelihood of lower power prices.

Munich Re jumped 3.2 percent to 139.35 euros. Bank of America upgraded the world’s biggest reinsurer from neutral to buy, citing the recent overdone share-price weakness, its strong capital position and lower exposure to catastrophe reinsurance relative with its peers. Shares have lost 12 percent since reaching their highest price in more than 10 years on April 25.

Vallourec rose 3.8 percent to 47.87 euros after Kepler Cheuvreux upgraded the shares to buy from hold, citing significant price hikes by its U.S. competitors.

Christian Dior SA advanced 3.4 percent to 136.55 euros as the French luxury goods maker announced that it has entered into a forward purchase agreement with an authorized financial intermediary to buy a maximum 550,000 of its own shares.

FTSE 100 6,520.38 -26.95 -0.41 %

CAC 40 4,033.37 -15.82 -0.39 %

DAX 8,274.91 -0.76 -0.01 %

-

10:25

Option expiries for today's 1400GMT cut

EUR/USD $1.3050, $1.3100, $1.3110, $1.3120, $1.3200, $1.3245, $1.3250

USD/JPY Y98.50, Y98.60, Y99.00, Y99.25, Y99.50, Y100.00, Y100.75, Y100.90, Y101.00

EUR/JPY Y130.75

GBP/USD $1.5500, $1.5600

USD/CHF Chf0.9425

EUR/CHF Chf1.2345

AUD/USD $0.9000, $0.9020, $0.9100, $0.9160, $0.9200

AUD/NZD NZ$1.1450

USD/CAD C$1.0475

-

10:02

Asia Pacific stocks close

Asian stocks rose, with the regional benchmark index extending its longest rally in nine months, after Tokyo won the rights to host the 2020 Olympics, China’s exports beat estimates and Australia elected a new government.

Nikkei 225 14,205.23 +344.42 +2.48%

Hang Seng 22,697.74 +76.52 +0.34%

S&P/ASX 200 5,181.47 +36.48 +0.71%

Shanghai Composite 2,212.52 +72.52 +3.39%

Agricultural Bank of China Ltd. advanced 4.3 percent, pacing gains among Chinese lenders.

Mitsubishi Estate Co. jumped 4.7 percent as Japan’s biggest developer by market value may benefit from projects such as the Olympic Village complex that will house athletes.

BHP Billiton Ltd., the world’s largest mining company, added 1.4 percent in Sydney on optimism the new Australian government will abolish a mining tax.

-

09:30

Eurozone: Sentix Investor Confidence, September +6.5 (forecast -4.0)

-

08:40

FTSE 100 6,545.95 -1.38 -0.02%, CAC 40 4,034.5 -14.69 -0.36%, Xetra DAX 8,257.63 -18.04 -0.22%

-

08:18

Switzerland: Retail Sales Y/Y, July +0.8% (forecast +3.2%)

-

07:40

European bourses are initially seen trading a touch lower Monday: the FTSE down 5, the DAX down 1 and the CAC down 4.

-

07:22

Asian session: The yen fell

01:30 Australia ANZ Job Advertisements (MoM) August -1.1% -2.0%

01:30 Australia Home Loans July +2.6% Revised From 2.7% +2.2% +2.4

01:30 China PPI y/y August -2.3% -1.7% -1.6%

01:30 China CPI y/y August +2.7% +2.6% +2.6%

02:00 China Trade Balance, bln August 17.8 20.3 19.6

05:00 Japan Consumer Confidence August 43.6 44.3 43.0

The yen fell as Tokyo’s winning bid to host the 2020 Olympics boosted optimism in Japanese Prime Minister Shinzo Abe’s package of fiscal and monetary policies that have helped weaken the currency 13 percent this year. Japan’s capital, which staged the 1964 Summer Games, beat Madrid and Istanbul to win the 2020 host role, the International Olympic Committee said Sept. 7 in Buenos Aires. Abe said yesterday at a televised press conference that the games would have “good effects on a wide range of areas such as infrastructure and tourism.

The yen was lower against all of its major peers after a report showed the nation’s economy expanded faster than initially estimated. Japan’s gross domestic product rose an annualized 3.8 percent in the second quarter from three months before, compared with a preliminary estimate of 2.6 percent, the Cabinet Office said in Tokyo today. First quarter growth was revised to 4.1 percent, the fastest in a year, from 3.8 percent.

The U.S. currency held gains from last week versus the euro amid expectations the Federal Reserve will reduce its $85 billion in monthly bond purchases this month.

Australia’s dollar touched a three-week high after data showed China’s exports increased, boosting trade prospects. In China, overseas shipments rose 7.2 percent in August from a year earlier, the General Administration of Customs said in Beijing yesterday. That compares with the 5.5 percent median estimate of economists surveyed by Bloomberg and July’s 5.1 percent gain. Imports rose a less-than-estimated 7 percent, leaving a trade surplus of more than $28 billion.

Consumer prices in China rose 2.6 percent last month from a year earlier, the Beijing-based National Bureau of Statistics said today, matching the median economist estimate in a Bloomberg poll. Prices gained 2.7 percent in both July and June, the fastest pace since February.

EUR / USD: during the Asian session the pair traded in the range of $ 1.3160-80

GBP / USD: during the Asian session, the pair rose to $ 1.5645

USD / JPY: during the Asian session the pair is trading around the level to Y99.80

The first half of the week is fairly data light on both sides of the Atlantic, with much investor attention on the address to the nation by President Obama on Tuesday evening, laying out the case for strikes against Syria. Then there will be the votes in Congress later in the week. Today's data gets underway with the release of the Swiss August unemployment numbers at 0545GMT. There is further Swiss data expected at 0715GMT, with the release of the July retail sales numbers. The main euro area release comes at 1000GMT, when the OECD leading indicator will be released.

-

07:00

Japan: Eco Watchers Survey: Current , August 51.2 (forecast 53.8)

-

06:45

Switzerland: Unemployment Rate, August 3.2% (forecast 3.0%)

-

06:01

Japan: Consumer Confidence, August 43.0 (forecast 44.3)

-