Notícias do Mercado

-

20:01

-

19:33

American focus: the euro fluctuates

The yen fell against most major currencies against the measures taken to mitigate the monetary policies adopted by the Bank of Japan, which continue to put pressure on the Japanese yen. Today begins a meeting of finance ministers and central bank governors G20. This is the first meeting since then, such as Japan, the third largest economy in the world, has activated a program to combat deflation. Japan is preparing to respond to criticism from foreign colleagues. Also today, the data released in Japan on the deficit of the trade balance. In March, 2013. the figure was $ 3.7 billion, which is almost two times less than in February of this year. However, the March trade deficit means that the level of imports in Japan than exports ninth month in a row, which is the longest period since 1980. For the year exports to the U.S. increased by 7%, while in China, by contrast, fell by 2.5%. It is worth noting that experts suggest that the level of Japanese exports will increase in the coming months due to the devaluation of the yen against the background of large-scale injections into the economy by the Bank of Japan.

The euro exchange rate fluctuates against the dollar on the ambiguous statistics and numerous comments by officials. Rumors that Societe Generale has suffered heavy losses, caused panic in the financial markets. After the denial of problems SocGen, the euro / dollar has formed a wedge, stopping at 1.3096 and extending the maximum daily range.

According to the report, which was published by the Federal Reserve Bank of Philadelphia, business activity among manufacturers Philadelphia region declined this month, but still remained in expansion. The data showed that the value of the Philadelphia Fed manufacturing index fell in April to the level of 1.3, compared with the February index at the level of 2.0. Note that this drop was a big surprise to many economists, since according to them the average forecast the figure would rise to the level of 3.1.

As the results of recent studies that have been presented today Conference Board, the index of leading economic indicators fell unexpectedly last month as the economic outlook worsened among consumers. According to the report, in March the index of leading indicators fell 0.1%, compared with unedited growth of 0.5% in February. Note that the last time the index of leading indicators showed a decline in August 2012.

Meanwhile, the meeting of the G20 continues, and the head of the Bank of Canada's Carney (soon to become head of the Bank of England) agreed with the head of the IMF's Lagarde on the fact that the U.S. is no longer part of the group of crisis economies. He also talked about the program with Cyprus, noting that in principle not against the participation of investors.

On Friday, investors will focus on producer prices in Germany and the euro area current account balance. Next will come industrial sales / orders of Italy and Spain's trade balance. G20 summit ends tomorrow, and the weekend will be a meeting IMF.

The pound fell to a one-month low against the euro after the data from the Office for National Statistics showed that by the end of last month, the volume of retail sales in the UK fell markedly, which is evidence of pressure on the finances of consumers, which jeopardizes the prospects for sustainable, long-term economic recovery. In addition, it was reported that the volume of sales, however, increased in the first quarter of this year, thanks to strong performance in February and no increase store sales. Economists point out that these data support the tentative signs that the UK can avoid a return to recession for the third time in five years. According to the report, in March retail sales fell by 0.7% compared to February and were up 0.5% compared with the same month a year earlier. Note that according to the average estimate of experts, the value of this index was reduced by 0.3% and 0.4%, respectively. Meanwhile, it was reported that the annual sales for the previous month was revised down to 2.5% growth, compared to the initial estimate of 2.6% increase.

-

18:38

European stocks close

European stocks closed unchanged from yesterday’s level, erasing intraday gains, as companies from Debenhams Plc to Syngenta AG and Nokia Oyj reported financial results.

Stocks erased gains after U.S. economic data missed estimates. A release showed the Conference Board’s index of leading indicators unexpectedly dropped 0.1 percent in March. Economists had forecast a 0.1 percent gain.

The Federal Reserve Bank of Philadelphia’s general economic index fell to 1.3 in April from 2 in March. Readings greater than zero mean manufacturing expanded in eastern Pennsylvania, southern New Jersey and Delaware. The median forecast in a survey had called for a reading of 3.

National benchmark indexes fell in 12 of the 18 western European markets. The U.K.’s FTSE 100 Index and France’s CAC 40 Index were little changed and Germany’s DAX Index slid 0.4 percent.

Syngenta climbed 3 percent to 389.60 Swiss francs after the world’s largest maker of crop chemicals reported a 6 percent increase in first-quarter sales to to $4.60 billion, buoyed by Brazilian operations that helped offset weaker demand for seeds and crop chemicals in parts of Europe. That met the $4.57 billion average analyst estimate in a survey.

GlaxoSmithKline Plc rallied 3.2 percent to 1,658 pence, the highest price since April 2002, after advisers to the U.S. Food and Drug Administration recommended that experimental treatment Breo Ellipta be approved to treat a lung disorder.

Sodexo tumbled 9.6 percent to 64.03 euros, the largest drop since November 2007. The second-biggest provider of catering services cut its annual profit-growth forecast after first-half results missed projections. The company expects “stable” earnings before interest and taxes compared with last year, after saying in January it expected “modest” profit growth.

-

17:53

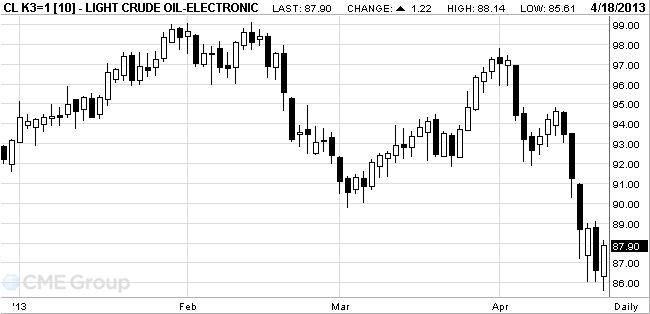

Oil rose

West Texas Intermediate rose from a four-month low after

Futures in

WTI crude oil for May delivery rose to $88.14 a barrel on the New York Mercantile Exchange. The contract fell to $85.61 earlier, the least since Dec. 11. The volume of all futures traded was 47 percent above the 100-day average for the time of day.

Brent oil for June settlement advanced $1.41, or 1.4 percent, to $99.10 a barrel on the London-based ICE Futures Europe exchange. Brent touched $96.75, the lowest level since July 2. The volume of all futures traded today was 45 percent higher than the 100-day average.

-

17:01

European stocks closed in different ways: FTSE 100 6,243.67 -0.54 -0.01%, CAC 40 3,599.36 +0.13 0.00%, DAX 7,473.73 -29.30 -0.39%

-

15:00

U.S.: Philadelphia Fed Manufacturing Survey, April 1.3 (forecast 3.1)

-

15:00

U.S.: Leading Indicators , March -0.1% (forecast +0.1%)

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.2900, $1.$1.2905, $1.2910, $1.2925, $1.2930, $1.2950, $1.2960, $1.3000, $1.3015, $1.3145

USD/JPY Y97.00, Y97.50, Y98.00, Y98.50, Y99.90, Y100.00

GBP/USD $1.5050, $1.5200

GBP/CAD C$1.5675

USD/CHF Chf0.9330, Chf0.9450

EUR/CHF Chf1.2230

AUD/USD $1.0490, $1.0550

NZD/USD $0.8500

-

14:34

U.S. Stocks open: Dow 14,623.00 +4.41 +0.03%, Nasdaq 3,208.12 +3.45 +0.11%, S&P 1,552.85 +0.84 +0.05%

-

14:29

Before the bell: S&P futures +0.29%, Nasdaq futures +0.33%

U.S. stock futures advanced as earnings from Verizon Communications Inc. (VZ) to PepsiCo Inc. (PEP) exceeded estimates.

Global Stocks:

Nikkei 13,220.07 -162.82 -1.22%

Hang Seng 21,512.52 -57.15 -0.26%

Shanghai Composite 2,197.6 +3.81 +0.17%

FTSE 6,270.09 +25.88 +0.41%

CAC 3,623.27 +24.04 +0.67%

DAX 7,526.47 +23.44 +0.31%

Crude oil $87.18 +0.58%

Gold $1387.20 +0.33%

-

13:30

U.S.: Initial Jobless Claims, April 352 (forecast 347)

-

13:13

European session: the euro is recovering after yesterday's fall

Data

01:30 Australia NAB Quarterly Business Confidence Quarter I -5 +2

08:30 United Kingdom Retail Sales (MoM) March +2.1% -0.3% -0.7%

08:30 United Kingdom Retail Sales (YoY) March +2.6% -0.4% -0.5%

09:00 Switzerland Gov Board Member Fritz Zurbrugg Speaks

The dollar fell after the data that the yield on 5-year bonds of France noted a record low 0.73%. We also note that today Spain held an auction for 3 -, 5 - and 10-year government bonds and was able to draw on its results E4.71 billion, exceeding the target range of 3.5-3.5 billion were sold during the auction of 3-year bonds worth E1.38 billion, and the average yield was 2.792% against 3.019% in the previous auction. 5-year bonds were sold at E2.043 billion, with an average yield of 3.257% vs. prev. 3.598%. Finally, the yield of securities maturing in January 2033 amounted to 4.612% against prev. 4.898%.

Also on this momentum trading has affected the annual report, which was presented today by international agency Moody 's Investors Service, and showed that Germany's sovereign rating unchanged - at' AAA ', facilitated by a highly competitive economy and a high level of investor confidence. In its annual credit report, Moody 's said that the sovereign rating at «AAA», albeit with a "negative" outlook is based on an advanced, diversified and highly competitive economy and a great track record of macroeconomic stability policy. In addition, it was noted that Germany enjoys a high level of investor confidence, which is reflected in the very low cost of debt financing.

Although Germany's debt remained high at around 80 per cent of the gross domestic product during the global financial crisis and the debt crisis in the eurozone, it was much lower than had been reported in many other major countries.

Meanwhile, the agency noted that the low cost of funding in Germany will ensure that its high level of debt and interest expense remains available.

We also note that today's leading economic institutes in Germany even more lowered their forecast for GDP in 2013 to Europe's largest economy. However, they stated that in 2014 the economic growth of more than double to 1.9% due to the revival of international trade and investment recovery company.

The pound fell to a one-month low against the euro after the data from the Office for National Statistics showed that by the end of last month, the volume of retail sales in the UK fell markedly, which is evidence of pressure on the finances of consumers, which jeopardizes the prospects for sustainable, long-term economic recovery. In addition, it was reported that the volume of sales, however, increased in the first quarter of this year, thanks to strong performance in February and no increase store sales. Economists point out that these data support the tentative signs that the UK can avoid a return to recession for the third time in five years.

According to the report, in March retail sales fell by 0.7% compared to February and were up 0.5% compared with the same month a year earlier. Note that according to the average estimates of experts, the value of this index was reduced by 0.3% and 0.4%, respectively. Meanwhile, it was reported that the annual sales for the previous month was revised down to 2.5% growth, compared to the initial estimate of 2.6% increase.

The yen fell against most major currencies against the measures taken to mitigate the monetary policies adopted by the Bank of Japan, which continue to put pressure on the Japanese yen. Today begins a meeting of finance ministers and central bank governors G20. This is the first meeting since then, such as Japan, the third largest economy in the world, has activated a program to combat deflation. Japan is preparing to respond to criticism from foreign colleagues. Also today, the data released in Japan on the deficit of the trade balance. In March, 2013. the figure was $ 3.7 billion, which is almost two times less than in February of this year. However, the March trade deficit means that the level of imports in Japan than exports ninth month in a row, which is the longest period since 1980. For the year exports to the U.S. increased by 7%, while in China, by contrast, fell by 2.5%. It is worth noting that experts suggest that the level of Japanese exports will increase in the coming months due to the devaluation of the yen against the background of large-scale injections into the economy by the Bank of Japan.

EUR / USD: during the European session, the pair rose to $ 1.3073, but later dropped to $ 1.3045

GBP / USD: during the European session, the pair dropped to $ 1.5217, after which rose to $ 1.5274

USD / JPY: during the European session, the pair rose to Y98.54

At 12:30 GMT the United States, there are data on initial claims for unemployment benefits last April. At 14:00 GMT the United States will be represented by the Philadelphia Fed manufacturing index for April. At 15:00 GMT will begin meeting G20, as well as the head of the Bank of Canada's Carney make a speech. At 16:00 GMT we planned a member of the Federal Open Market Committee Federal Reserve C. Raskin.

-

13:00

Orders

EUR/USD

Offers $1.3195/200, $1.3170/80, $1.3150/55, $1.3120/25, $1.3100/10, $1.3080, $1.3060/70

Bids $1.3020, $1.3000, $1.2990, $1.2970, $1.2950/40

GBP/USD

Offers $1.5370/80, $1.5350, $1.5330/35, $1.5290/300, $1.5270/75

Bids $1.5200, $1.5180/70, $1.5150, $1.5130/20

AUD/USD

Offers $1.0420, $1.0395/00, $1.0380, $1.0350

Bids $1.0280, $1.0260/50, $1.0240/30, $1.0220

EUR/JPY

Offers Y130.50, Y130.20, Y130.00, Y129.70/80, Y129.50, Y129.00

Bids Y128.10/05, Y127.65/60, Y127.50, Y127.20/15, Y127.00, Y126.80

EUR/GBP

Offers stg0.8630/40, stg0.8610/15, stg0.8600

Bids stg0.8535/30, stg0.8500, stg0.8485/80, stg0.8460/50

USD/JPY

Offers Y99.50, Y99.20, Y99.00, Y98.65/70

Bids Y98.10/00, Y97.50

-

11:00

European stock indices rising

European (SXXP) stocks rose, snapping the biggest four-day selloff since July, as companies from Remy Cointreau SA (RCO) to Syngenta AG and Nestle SA (NESN) reported results. U.S. index futures also advanced, while Asian shares fell.

The Stoxx Europe 600 Index gained 0.5 percent to 285.08 at 10:26 a.m. in London.

Some 29 companies on the S&P 500 including Morgan Stanley, Google Inc. and Microsoft Corp. will report results today. In Europe, seven companies on the Stoxx 600 will also post earnings, according to data compiled by Bloomberg. Of those that have posted results so far, 64 percent have beaten estimates for profit.

Remy Cointreau added 1.5 percent to 87.20 euros after the maker of Mount Gay rum reported a 12 percent increase in fourth- quarter organic sales, aided by demand for pricier variants of its Remy Martin cognac during the Chinese New Year holiday. That exceeded the median 8.6 percent growth estimate of 10 analysts surveyed.

Syngenta climbed 4.3 percent to 394.60 euros after the world’s largest maker of crop chemicals reported a 6 percent increase in first-quarter sales to to $4.60 billion, buoyed by Brazilian operations that helped offset weaker demand for seeds and crop chemicals in parts of Europe. That met the $4.57 billion average analyst estimate.

Debenhams Plc climbed 7.5 percent to 86.55 pence, for the biggest advance on the Stoxx 600. The U.K.’s second-largest clothing retailer reported first-half pretax profit of 120.3 million pounds ($184 million), in line with analyst estimates.

Nestle slid 0.9 percent to 63.75 Swiss francs after the company posted a 4.3 percent increase in first-quarter sales, excluding acquisitions, divestments and currency swings. That fell short of the 4.7 percent average analyst estimate. Higher prices contributed 2 percent to sales growth, more than analysts’ estimates of 1.2 percent.

At that moment:

FTSE 100 6,274.33 +30.12 +0.48%

CAC 40 3,634.68 +35.45 +0.98%

DAX 7,551.27 +48.24 +0.64%

-

10:30

Option expiries for today's 1400GMT cut

EUR/USD $1.2900, $1.$1.2905, $1.2910, $1.2925, $1.2930, $1.2950, $1.2960, $1.3000, $1.3015, $1.3145

USD/JPY Y97.00, Y97.50, Y98.00, Y98.50, Y99.90, Y100.00

GBP/USD $1.5050, $1.5200

GBP/CAD C$1.5675

USD/CHF Chf0.9330, Chf0.9450

EUR/CHF Chf1.2230

AUD/USD $1.0490, $1.0550

NZD/USD $0.8500

-

10:14

Thursday: Asia Pacific stocks close

Asian stocks fell, with the regional benchmark index set for its biggest drop in a month, led by mining companies as commodities slumped on concern weaker global economic growth will crimp demand for raw materials.

Nikkei 225 13,220.07 -162.82 -1.22%

Hang Seng 21,490.56 -79.11 -0.37%

S&P/ASX 200 4,924.4 -80.15 -1.60%

Shanghai Composite 2,197.6 +3.81 +0.17%

BHP Billiton Ltd., the world’s biggest miner, sank 4.3 percent in Sydney.

LG Display Co., which supplies touch screens for Apple Inc., dropped 4.8 percent in Seoul after audio-chip maker Cirrus Logic Inc. reported an inventory glut that suggests iPhone sales may fall short of expectations.

Softbank Corp., Japan’s third-largest wireless carrier, lost 1.6 percent as a rival’s bid for Sprint Nextel Corp. gained shareholder support.

-

09:30

United Kingdom: Retail Sales (YoY) , March -0.5% (forecast -0.4%)

-

09:30

United Kingdom: Retail Sales (MoM), March -0.7% (forecast -0.3%)

-

09:11

FTSE 100 6,254.84 +10.63 +0.17%, CAC 40 3,619.3 +20.15 +0.56%, DAX 7,528.06 +25.03 +0.33%

-

07:42

European bourses are initially seen trading higher Thursday: the FTSE up 11, the DAX up 23 and the CAC up 11.

-

07:23

Asian session: The yen declined versus all 16 major peers

01:30 Australia NAB Quarterly Business Confidence Quarter I -5 +2

The yen declined against major counterparts amid bets Japan will escape censure for weakening its currency at a Group of 20 meeting starting today. BOJ Governor Haruhiko Kuroda unveiled a plan on April 4 to double the central bank’s holdings of government debt and stock funds in two years. Japan’s trade partners have expressed concern over the move, with the U.S. Treasury saying in its semi-annual currency report that Japan must “refrain from competitive devaluation.”

The currency earlier strengthened against most major peers after Japanese data showed domestic investors sold foreign bonds for a fifth week, casting doubt on whether monetary stimulus will continue to weaken the currency.

Domestic investors reduced their holdings of foreign debt by 331.9 billion yen ($3.4 billion) in the week ended April 12, according to data from the Asian nation’s Ministry of Finance. That followed a net sale of 1.14 trillion yen the prior week, the most in a year.

Australia’s dollar rebounded from a one-month low as Chinese stocks trimmed losses after data showed home prices in the South Pacific nation’s biggest trading partner increased. China’s new home prices rose in all but two cities. China’s new home prices in March climbed in 68 of the 70 cities the government tracks from a year earlier, the National Bureau of Statistics said in a statement today.

The New Zealand dollar rose. In New Zealand, job advertisements rose for a second month in March. The number of postings in newspapers and the Internet increased 0.7 percent last month from a revised 1.8 percent in February, ANZ Bank New Zealand Ltd. said in Wellington today.

EUR / USD: yesterday the pair rose to $ 1.3060

GBP / USD: yesterday the pair rose to $ 1.5250.

USD / JPY: yesterday the pair traded in the range of Y97.60-Y98.35.

UK data is expected at 0830GMT, with the release of the March Retail Sales numbers. The very cold March weather could well have provided yet more bad news for the U.K. High Street by persuading shoppers to stay at home. Analysts are looking for a fall of 0.6% on month. A fairly light data calendar in the Eurozone today, with main attention to befocussed on US weekly jobless claims at 1230GMT and Phila Fed at 1400GMT.

-

06:21

Commodities. Daily history for Apr 17’2013:

Change % Change Last

GOLD 1,382.70 -4.70 -0.30%

OIL 86.68 -2.04 -2.32%

-

06:21

Stocks. Daily history for Apr 17’2013:

Change % Change Last

Nikkei 225 13,221.44 -54.22 -0.41%

Hang Seng 21,763.94 -8.73 -0.04%

S&P/ASX 200 4,950.8 -17.11 -0.34%

Shanghai Composite 2,194.85 +12.90 +0.59%

FTSE 100 6,244.21 -60.37 -0.96%

CAC 40 3,599.23 -86.56 -2.35%

DAX 7,503.03 -179.55 -2.34%

DJIA 14,618.60 -138.19 -0.94%

S&P 500 1,552.01 -22.56 -1.43%

NASDAQ 3,204.67 -59.96 -1.84%

-

06:20

Currencies. Daily history for Apr 17'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3034 -1,28%

GBP/USD $1,5240 -0,91%

USD/CHF Chf0,9326 +1,13%

USD/JPY Y98,25 +0,48%

EUR/JPY Y128,08 -0,61%

GBP/JPY Y149,74 -0,32%

AUD/USD $1,0307 -0,74%

NZD/USD $0,8445 -0,54%

USD/CAD C$1,0260 +0,51%

-

06:01

Schedule for today, Thursday, Apr 18’2013:

01:30 Australia NAB Quarterly Business Confidence Quarter I -5 +2

08:30 United Kingdom Retail Sales (MoM) March +2.1% -0.3%

08:30 United Kingdom Retail Sales (YoY) March +2.6% -0.4%

09:00 Switzerland Gov Board Member Fritz Zurbrugg Speaks

12:30 U.S. Initial Jobless Claims April 346 347

14:00 U.S. Leading Indicators March +0.5% +0.1%

14:00 U.S. Philadelphia Fed Manufacturing Survey April 2.0 3.1

15:00 G20 G20 Meetings

15:00 Canada BOC Gov Carney Speaks

16:00 U.S. FOMC Member Raskin Speaks

-