Notícias do Mercado

-

20:00

DJIA 15,043.20 -38.26 -0.25%, S&P 500 1,650.59 -5.24 -0.32%, NASDAQ 3,606.13 3.35 0.09%

-

19:19

American focus: the euro and the pound stabilized

Against the background of the empty economic calendar in the U.S. session, the euro and the pound stabilized.

Earlier, the euro managed to show modest gains against the dollar, thus responding to the comments Bundesbank. The German central bank said it expected normalization of economic growth in the second half of this year. There were also marked reduction in expectations of inflationary pressures in the coming months and added that "the ECB's low interest rates continue to support the recovery in the years 2013-2014."

The limiting factor for the single currency was data from the Bank of Spain, which recorded a growth in the share of problem loans of Spanish banks to a new historical high of 11.6% in June from May's value at the level of 11.2%.

Pound was able to update the August highs against the U.S. dollar, but to develop a pair of upward movement failed and retreated somewhat. Positive impact on the dynamics of the pound rise projections for the growth of the British economy by the Confederation of British Industry (CBI). CBI, which represents the interests of about 240,000 businesses expect growth in the current year the British economy will be 1.2% versus 1.0% previously expected. Forecast for 2014 also increased: from 2.0% to 2.3%.

-

18:21

European stocks close

European stocks fell, following three weeks of gains for the Stoxx Europe 600 Index, as this week’s release of minutes from the Federal Reserve’s last meeting fueled speculation policy makers will trim bond buying.

Investors will scrutinize minutes of the FOMC’s July 30-31 meeting for indications of when the Fed will begin to reduce the $85 billion pace of monthly bond purchases. The minutes may also describe the risks from inflation staying below the central bank’s 2 percent goal. The FOMC holds its next two-day meeting on Sept. 17-18.

Treasuries fell, pushing the yield on the 10-year securities up as much as 5 basis points to 2.87 percent, the highest since July 2011.

Central bankers and policy makers meet in Jackson Hole, Wyoming, from Aug. 22 to Aug. 24 to discuss the global economy and monetary policy.

Glencore lost 2.1 percent to 301.95 pence after Reuters reported the mining company created three months ago may write down as much as $7 billion of inherited Xstrata assets when it reports its first-half earnings tomorrow.

A gauge of lenders contributed the most to the Stoxx 600’s decline. Santander, Spain’s largest bank, retreated 2.9 percent to 5.65 euros as the spread on 10-year Spanish bonds over German securities widened four basis points to 252 basis points. Bankinter SA slid 5.2 percent to 3.65 euros.

UniCredit fell 5.2 percent to 4.53 euros and Banco Popolare SC lost 4.5 percent to 1.12 euros. The spread on benchmark 10-year Italian debt over bunds with the same maturity widened eight basis points to 238 basis points.

Kentz jumped 24 percent to 591 pence, the biggest rally since its initial public offering in February 2008, after rejecting potential takeover approaches from companies including Amec Plc and M&W Group GmbH. Amec said in a statement that Kentz’s board of directors turned down its offer of 565 pence to 580 pence a share, saying it undervalued the company. Kentz also rejected M&W’s possible offer, which it said was lower than Amec’s.

Atlas Copco AB advanced 1.4 percent to 180 kronor. The world’s largest maker of air compressors agreed to buy Edwards Group Ltd. for $1.2 billion in cash to expand in vacuum pumps. Shareholders of the British company will receive as much as $10.50 a share depending on this year’s financial results, Stockholm-based Atlas Copco said in a statement.

National benchmark indexes retreated in 15 of the 18 western European markets today. France’s CAC 40 slipped 1 percent and Germany’s DAX fell 0.3 percent. The U.K.’s FTSE 100 declined 0.5 percent.

-

17:00

European stocks closed in minus: FTSE 100 6,465.52 -34.47 -0.53%, CAC 40 4,084.06 -39.83 -0.97%, DAX 8,367.21 -24.73 -0.29%

-

16:41

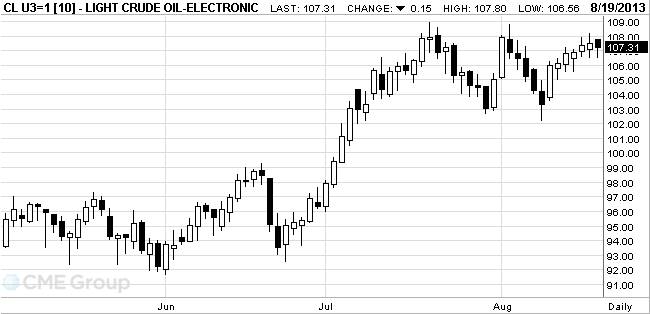

Oil fell

West

WTI crude for September delivery, which expires tomorrow, fell 5 cents to $107.41 a barrel at 10:06 a.m. on the New York Mercantile Exchange. It settled at $107.46 on Aug. 16, the highest close since Aug. 1. The October contract slipped 18 cents to $107.11. The volume of all futures traded was about 9.7 percent below the 100-day average.

Brent oil for October settlement increased 35 cents, or 0.3 percent, to $110.75 a barrel on the London-based ICE Futures Europe exchange. Trading of futures was 17 percent below the 100-day average. The European benchmark traded at a $3.64 premium to WTI.

-

16:20

Gold has updated two-month high and receded

Gold is the first time in two months exceeded $1,380 / Oz. Last above that mark gold price rose 18 June 2013

Golden quotes grew alongside evidence of recovery in investment demand for gold bullion. The assets of the world's largest holder of gold investment institutions exchange traded fund SPDR Gold Trust at the end of business day on August 16 increased by 2.4 tons and amounted to 915.32 tons - a maximum of 5 August this year

At the balance sheet date of August 8, 2013 assets of the fund SPDR Gold Trust, represented by gold bars, fell to its lowest level since February 2009 - up to 909.33 tons By this time, the fund's assets fell by 444.02 tons (-32 , 8%) after being on December 7, 2012 they reached a historic high - 1 353.35 thousand tons.

Later, gold fell to a two-month high as investors chose to take profits. This week's important to prices of precious metals will yield the minutes of the Fed meeting on Wednesday and the Fed in Jackson Hole at the end of the week, as the prospects for change in the quantitative easing program should be reflected in prices, as it is believed that quantitative easing has been an important factor in the rising cost of Gold previously.

The cost of the October gold futures on COMEX today rose to $ 1382.40 an ounce and then fell to $ 1363.50 an ounce.

-

14:33

U.S. Stocks open: Dow 15,060.31 -21.16 -0.14%, Nasdaq 3,602.38 -0.40 -0.01%, S&P 1,653.60 -2.23 -0.13%

-

14:20

Before the bell: S&P futures +0.06%, Nasdaq futures +0.20%

U.S. stock-index futures were little changed as investors awaited the release of Federal Reserve minutes.

Global Stocks:

Nikkei 13,758.13 +108.02 +0.79%

Hang Seng 22,463.7 -54.11 -0.24%

Shanghai Composite 2,085.6 +17.15 +0.83%

FTSE 6,473.68 -26.31 -0.40%

CAC 4,093.05 -30.84 -0.75%

DAX 8,374.42 -17.52 -0.21%

Crude oil $106.80 -0.61%

Gold $1372.30 +0.09%

-

12:40

Orders

EUR/USD

Offers $1.3440/50, $1.3415/20, $1.3390/400, $1.3380

Bids $1.3310/00, $1.3290/85, $1.3280

GBP/USD

Offers $1.5750/55, $1.5720/25, $1.5700, $1.5680

Bids $1.5610/00, $1.5585/80, $1.5555/50, $1.5505/00

AUD/USD

Offers $0.9315/20, $0.9300, $0.9265/70, $0.9250, $0.9230/40, $0.9195/00

Bids $0.9140/30, $0.9110/00, $0.9090, $0.9050

USD/JPY

Offers Y98.50, Y98.10/30

Bids Y97.55/50, Y97.20/00, Y96.80, Y96.60/50

EUR/JPY

Offers Y131.90/00, Y131.45/50, Y131.20, Y131.10

Bids Y130.40/35, Y130.00, Y129.50

EUR/GBP

Offers stg0.8620/30, stg0.8580/85, stg0.8565/70

Bids stg0.8505/00, stg0.8485/80, stg0.8565/60, stg0.8420

-

11:28

European stocks are in red zone

European stocks fell, investors awaited Wednesday’s release of minutes from last month’s Federal Open Market Committee meeting.

Shares of Glencore Xstrata lost 1.6% after Reuters reported the mining company may write down as much as $7 billion of inherited Xstrata assets when it reports results this week.

Lenders Drop after Bank of Spain data showed that Spanish banks' bad loans rose to a fresh high of 11.6% in June vs 11.2% in May. Shares of Banco Santander SA -1.4%, UBS -1.7%, UniCredit SpA -3.6%, Banco Popolare SC -3.9%.

Currently:

FTSE 6,489.5

11:01Bank of Spain data showed That Spanish banks' bad loans rose to a fresh high of 11.6% in June vs 11.2% in May

10:27Option expiries for today's 1400GMT cut

EUR/USD $1.3200, $1.3285, $1.3310, $1.3400, $1.3405

USD/JPY Y97.00, Y97.50, Y97.75, Y98.00(large), Y98.25, Y99.25, Y99.75

GBP/USD $1.5455, $1.5460, $1.5485, $1.5600, $1.5615, $1.5620, $1.5650, $1.5655, $1.5700

EUR/GBP stg0.8550

USD/CHF Chf0.9200, Chf0.9220, Chf0.9250, Chf0.9260

AUD/USD $0.9100

AUD/NZD NZ$1.1455

USD/CAD C$1.0350, C$1.0400

EUR/NOK Nok7.8000, Nok7.8020

10:01Asia Pacific stocks close

Asian stocks outside Japan fell for a third day as a retreat in emerging markets dragged the regional equities gauge to its lowest level in a week. Japan’s Topix index gained amid low trading volumes.

Nikkei 225 13,758.13 +108.02 +0.79%

Hang Seng 22,442.34 -75.47 -0.34%

S&P/ASX 200 5,112.53 -1.33 -0.03%

Shanghai Composite 2,085.6 +17.15 +0.83%

Tokyo Electric Power Co. fell 3.6 percent after saying an alarm went off at its Fukushima Dai-Ichi nuclear reactor, indicating high radioactive concentration.

BlueScope Steel Ltd. fell 14 percent as sales missed analyst estimates and Australia’s No. 1 steel producer forecast a weaker first half of the financial year.

JX Holdings Inc. gained 4 percent after Mitsubishi UFJ Morgan Stanley Securities Co. advised buying the Japanese refiner’s shares.

08:39FTSE 100 6,500.92 +0.93 +0.01%, CAC 40 4,122.38 -1.51 -0.04%, Xetra DAX 8,376.08 -15.86 -0.19%

07:19European bourses are initially seen trading flat to modestly lower Monday: the FTSE down 2, the DAX down 4 and the CAC unchanged.

07:02Asian session: The euro was 0.4 percent from a one-week high

01:30 Australia New Motor Vehicle Sales (MoM) July +3.6% Revised From +4.0% -4.0% -3.5%

01:30 Australia New Motor Vehicle Sales (YoY) July +6.9% Revised From +7.1% +3.0%

The euro was 0.4 percent from a one-week high against its U.S. peer before German data this week that analysts predict may show the currency bloc’s largest economy is gaining momentum. Germany’s producer prices probably rose in July, while surveys of purchasing managers in manufacturing and services industries showed activity picked up this month in the nation and in the euro region, according to economists polled by Bloomberg News. A gauge of German manufacturing gained to 51.1 this month from 50.7 in July and the services index rose to 51.7 from 51.3, an Aug. 22 report from London-based Markit Economics may show according to a separate Bloomberg poll of economists. An index of activity for both industries in the euro zone rose to 50.9 from 50.5, another Bloomberg survey predicts. A reading above 50 indicates expansion.

The yen fell earlier on data showing Japan’s trade deficit widened in July. Japan’s imports outpaced exports by 1.02 trillion yen ($10.5 billion) in July, compared with the median estimate for a 773.5 billion yen gap, data showed today. It was the worst since January, when the deficit was a record 1.63 trillion yen.

Australia’s dollar rose amid speculation minutes tomorrow of the Reserve Bank’s last meeting will signal no hurry to reduce interest rates further. The Reserve Bank of Australia cut its benchmark rate to a record 2.5 percent on Aug. 6. In the statement announcing the move, policy makers changed the wording when discussing whether the inflation outlook provided scope for further easing, damping expectations for additional cuts.

EUR / USD: during the Asian session the pair traded in the range of $ 1.3320-40

GBP / USD: during the Asian session the pair traded in a range of $ 1.5615-40

USD / JPY: during the Asian session the pair traded in the range of Y97.35-85

As the summer holiday season continues, Monday sees a very light data calendar that is light on volume on both sides of the Atlantic. Flash euro zone PMIs on Thursday will provide the main data focus for the markets in an otherwise ho-hum August week. The release will provide the first indication on whether the return to growth seen in Q2 GDP data will be sustained through Q3. Another relatively strong number will likely quash utterly any lingering speculation that the European Central Bank will move to cut rates again in coming months - something which had already been very much on the cards following Mario Draghi's guidance commitment in July. The only release set for Monday is the German Bundesbank's August monthly report at 1000GMT.

06:23Schedule for today, Monday, Aug 19’2013:

01:30 Australia New Motor Vehicle Sales (MoM) July +3.6% Revised From +4.0% -4.0% -3.5%

01:30 Australia New Motor Vehicle Sales (YoY) July +6.9% Revised From +7.1% +3.0%