Notícias do Mercado

-

19:00

Dow 16,353.98 +22.93 +0.14%, Nasdaq 4,281.10 -38.19 -0.88%, S&P 500 1,869.53 -2.48 -0.13%

-

18:20

American focus : the Canadian dollar strengthened

The Canadian dollar has risen considerably after strong economic data on retail sales and inflation. The data presented by Statistics Canada showed that in January retail sales rose by 1.3 % - to $ 40.7 billion , almost offsetting the decline in December by 1.9% ( revised from -1.8 %). Experts predicted that sales will rise by 0.8%. Meanwhile, it became known that an increase was reported in 7 of 11 subsectors , representing 83% of total retail sales. Sales in dollar terms increased by 1.4% , indicating that higher volumes of goods sold.

Statistics Canada reported last month that the consumer price index increased by 1.1 % per annum, after increasing by 1.5%. According to estimates , the index should rise by 0.9%. Lower gasoline prices have led to slower growth in the consumer price index . Compared with February last year, gasoline prices have fallen by 1.3% , after rising in January by 4.6%. On a monthly basis , gasoline prices rose 2.3 % in February , compared with an increase of 8.4% in the same month last year. Of the eight major components , six recorded growth in annual terms . Higher housing costs and food prices have led to an increase in the CPI. At the same time , the indices for transportation and for clothes and shoes made the greatest contribution to the slowdown in the CPI.

The euro exchange rate against the dollar rose moderately against the background data , which showed that the positive balance of payments euro zone increased significantly in the month of January , which was caused by an increase in the trade surplus in goods and services . According to the report , the seasonally adjusted current account surplus rose in January to a level of 25.3 billion euros, compared with a surplus of 20 billion euros a month earlier , which was revised down from 21.0 billion euros. Meanwhile , we add that the surplus in trade in goods amounted to 15.9 billion in January, compared with EUR 14.5 billion in the previous month . In addition, the services account surplus rose to 11.8 billion euros from 9.6 billion euros in December. The European Central Bank reported that the growth of the surplus in merchandise trade deficit was partially offset by a current account transfers - at 9.3 billion, however , the deficit fell from 11.2 billion euros in December. Revenue fell to 6.8 billion euros from 7.1 billion euros.

The pound fell slightly against the dollar , reaching a minimum at the same time yesterday . Possible driver of this decline was the dynamics of GBP / JPY, due to the increasing demand for the yen. Repatriation flows bound for Japan in anticipation of the end of the financial year are probably now the only catalyst for the exchange . Little influenced by data that showed that the UK 's budget deficit in February widened more than expected . Note that net borrowing in the public sector , excluding the intervention has increased to 9.3 billion pounds in February , while in the same period last year borrowing was 6.5 billion pounds. In January 2014 net borrowing in the public sector showed a negative balance of 4.99 billion pounds. It was expected that the budget deficit will rise to 8.6 billion pounds. Over the 2013/14 financial year net borrowing in the public sector excluding temporary effects of financial interventions was 87.2 billion pounds. It turned out to be 17.9 billion pounds higher than for the same period of 2012 /13 , while borrowing was 69.3 billion pounds. In addition, according to official figures , net debt in the public sector excluding temporary effects was 1.2468 trillion pounds by the end of February , which is equivalent to 74.7 % of GDP.

-

18:01

European stocks close

European stocks were little changed, with the Stoxx Europe 600 Index posting its biggest weekly gain in five weeks, as consumer confidence increased more than forecast, while derivatives contracts expired.

The Stoxx 600 gained 0.1 percent to 327.91 at the close of trading. The index has advanced 1.8 percent this week, paring its loss this year to 0.1 percent, as President Vladimir Putin said he wasn’t seeking to split up Ukraine after Crimea voted to join Russia.

Consumer confidence in the euro area improved this month more than projected, according to data from the European Commission. An advance reading showed an index of household confidence increased in March to minus 9.3 from minus 12.7 in February. The median economist estimate compiled by Bloomberg had predicted a reading of minus 12.3.

National benchmark indexes rose in 10 of the 18 western-European markets today. Germany’s DAX gained 0.5 percent, France’s CAC added 0.2 percent, and the U.K.’s FTSE 100 also rose 0.2 percent.

Commerzbank climbed 2.5 percent to 13.33 euros. Morgan Stanley raised Germany’s second-largest lender to overweight, similar to buy, from equal weight. Analysts Hubert Lam and Francesca Tondi said non-core assets are undervalued and the likelihood of another capital increase has decreased. Separately, Commerzbank said today that it has already attained its capital requirement target for 2014.

Havas declined 1.8 percent to 5.70 euros. The French advertising agency partly-owned by billionaire Vincent Bollore said net income rose to 128 million euros ($177 million). That missed the 133 million-euro average analyst estimate compiled by Bloomberg.

Remy fell 3.9 percent to 59.07 euros. The company will find it harder to recover from a slump in Chinese sales because it lacks the global distribution channels of its rivals, according to UBS. Cognac sales may drop as much as 25 percent in the fourth quarter, UBS said.

Vivendi SA lost 1.4 percent to 19.67 euros. Altice SA, which is in talks to buy Vivendi’s SFR phone unit, has no plan to revise its bid even after Bouygues SA sweetened its rival offer yesterday, according to a person familiar with the matter. Altice can change its bid during the three-week exclusivity period ending April 4, the person said.

-

17:00

European stocks closed in plus: FTSE 100 6,557.17 +14.73 +0.23%, CAC 40 4,335.28 +7.37 +0.17%, DAX 9,342.94 +46.82 +0.50%

-

15:41

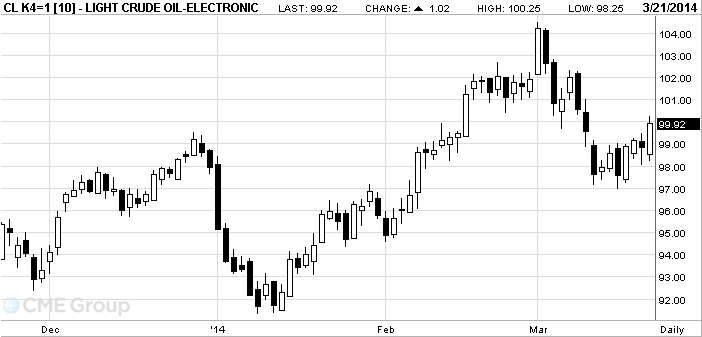

Oil rose

Brent crude rose after

Brent futures climbed as much as 0.9 percent and WTI 0.8 percent. Russian President Vladimir Putin signed legislation needed to absorb the Black Sea peninsula and its

“Crude is rising because Putin’s actions are getting more provocative,” said Dan Flynn, an energy market analyst at Price Futures Group in

Brent for May settlement rose 94 cents, or 0.9 percent, to $107.39 a barrel on the London-based ICE Futures Europe exchange as of 11:30 a.m.

WTI for May delivery advanced 83 cents, or 0.8 percent, to $99.73 on the New York Mercantile Exchange. The April contract expired yesterday after dropping 0.9 percent to $99.43. Trading volume was 19 percent lower than the 100-day average.

-

15:20

Gold rose

Gold rose on Friday in anticipation of statements by the U.S. central bank , but the week promises to be the worst since November due to market reaction to the Fed's promise to head Janet Yellen to raise rates in the first half of 2015 .

The Fed is likely to complete its bond-buying program this fall and begin to raise interest rates after about 6 months after that , Yellen said . Although she carefully introduced this forecast , making numerous reservations , this was still enough to bother investors. Some market participants are buying gold and other precious metals as a tool for protection against low interest rates, inflation and uncertainty in the economy.

" Coming rising interest rates , a stronger dollar , and inflation is not observed , - said James Cordier , director of Liberty Trading Group. - All the factors to reduce the price of gold ."

Bond buying program , the volume of which is now $ 55 billion a month, helped keep rates low at the same time putting pressure on the dollar.

Gold prices jumped to a 6 - month high of 1,392.60 dollars on March 17 as a result of growth , partly provoked instability in Ukraine and Russian military intervention in the Republic of Crimea.

However, prices fell this week, as it became apparent that the West is almost inclined to interfere with Russia to join the Crimea. Russian President Vladimir Putin on Tuesday signed an agreement on accession of the Ukrainian region of the territory of Russia . He said that his country is not seeking to " separation of Ukraine" and will protect the interests of the Russian-speaking population in the country " diplomatic and legal means ."

The cost of the April gold futures on the COMEX today rose to $ 1343.00 per ounce.

-

15:00

Eurozone: Consumer Confidence, March -9.3 (forecast -12.3)

-

13:45

Option expiries for today's 1400GMT cut

USD/JPY Y101.00, Y101.50, Y101.80, Y102.00, Y102.25, Y102.50, Y103.60, Y104.00

EUR/JPY Y142.80

EUR/USD $1.3850, $1.3900, $1.4000

GBP/USD $1.6470, $1.6535, $1.6645, $1.6750

EUR/GBP stg0.8335, stg0.8445, stg0.8450

USD/CHF Chf0.8700, Chf0.8810

EUR/CHF Chf1.2200, Chf1.2225

AUD/USD $0.9050, $0.9100, $0.9125, $0.9140, $0.9150

AUD/JPY Y90.50, Y91.50

NZD/USD $0.8600

USD/CAD C$1.1225, C$1.1250, C$1.1300

-

13:37

U.S. Stocks open: Dow 16,359.99 +0.18%, Nasdaq 4,340.49 +0.49%, S&P 1,881.63 +0.51%

-

13:29

Before the bell: S&P futures +0.23%, Nasdaq futures +0.26%

U.S. stock-index futures advanced. With no major data releases on tap, corporate news and Fed speakers are likely to claim most of investors’ attention.

Global markets:

FTSE

6,549.6

+7.16

+0.11%

CAC

4,335.57

+7.66

+0.18%

DAX

9,316.29

+20.17

+0.22%

Hang Seng

21,436.7

+254.54

+1.20%

Shanghai Composite

2,047.62

+54.14

+2.72%

Crude oil $99.22 (+0.32%)

Gold $1337.80 (+0.55%).

-

13:15

European session: the pound fell moderately against the U.S. dollar

Data

00:00 Japan Bank holiday

09:00 Eurozone European Council Meeting

09:00 Eurozone EU Economic Summit

09:00 Eurozone Current account, adjusted, bln January 20.0 Revised From 21.3 18.4 25.3

09:30 United Kingdom PSNB, bln February -6.4 7.8 7.47

12:30 Canada Retail Sales, m/m January -1.9% Revised From -1.8% +0.8% +1.3%

12:30 Canada Retail Sales ex Autos, m/m January -1.5% Revised From -1.4% +0.9% +1.0%

12:30 Canada Consumer Price Index m / m February +0.3% +0.6% +0.8%

12:30 Canada Consumer price index, y/y February +1.5% +0.9% +1.1%

12:30 Canada Bank of Canada Consumer Price Index Core, m/m February +0.2% +0.5% +0.7%

12:30 Canada Bank of Canada Consumer Price Index Core, y/y February +1.4% +1.1% +1.2%

Rate of the euro retreated from highs against the dollar , while returning to the opening level of the current session . Partly influenced by the dynamics of the data , which showed that the positive balance of payments euro zone increased significantly in the month of January , which was caused by an increase in the trade surplus in goods and services . According to the report , the seasonally adjusted current account surplus rose in January to a level of 25.3 billion euros, compared with a surplus of 20 billion euros a month earlier, which was revised down from 21.0 billion euros. Meanwhile , we add that the surplus in trade in goods amounted to 15.9 billion in January, compared with EUR 14.5 billion in the previous month . In addition, the services account surplus rose to 11.8 billion euros from 9.6 billion euros in December. The European Central Bank reported that the growth of the surplus in merchandise trade deficit was partially offset by a current account transfers - at 9.3 billion, however , the deficit fell from 11.2 billion euros in December. Revenue fell to 6.8 billion euros from 7.1 billion euros.

Also note that investors are waiting for evidence of improvement in consumer confidence in the euro-zone economy . A preliminary report will be released in 15:00 GMT. Economists estimate that the index potrebdoveriya rose in March to minus 12.3 points from minus 12.7 points a month earlier .

The course of trading may also affect the word Fed : 17:45 GMT to perform a member of the Committee on the Federal Open Market R. Fisher in 20:30 GMT - member of the Federal Open Market N. Kocherlakota , and 22:30 GMT - Member FOMC Fed Jerome Stein .

The pound fell slightly against the dollar , reaching thus minmiuma yesterday . Possible driver of this decline was the dynamics of GBP / JPY, due to the increasing demand for the yen. Repatriation flows bound for Japan in anticipation of the end of the financial year are probably now the only catalyst for the exchange . Little influenced by data that showed that the UK 's budget deficit in February widened more than expected . Note that net borrowing in the public sector , excluding the intervention has increased to 9.3 billion pounds in February , while in the same period last year borrowing was 6.5 billion pounds. In January 2014 net borrowing in the public sector showed a negative balance of 4.99 billion pounds. It was expected that the budget deficit will rise to 8.6 billion pounds. Over the 2013/14 financial year net borrowing in the public sector excluding temporary effects of financial interventions was 87.2 billion pounds. It turned out to be 17.9 billion pounds higher than for the same period of 2012 /13 , while borrowing was 69.3 billion pounds. In addition, according to official figures , net debt in the public sector excluding temporary effects was 1.2468 trillion pounds by the end of February , which is equivalent to 74.7 % of GDP.

The yen fell against the dollar , while losing all positions earned in the first half of the day . Liquidity during the Asian session was low , as financial markets in Japan closed for a public holiday. Support also has a pair of growth yield of U.S. Treasury bonds , a weakened yen appeal as safe-haven currency . In addition, the decline of the pair will be constrained by the loose monetary policy of the Bank of Japan and the orders to buy the yen by Japanese importers. American calendar of events is almost empty - only planned for the evening performances of several representatives of the Federal Reserve, which can cause sharp fluctuations .

EUR / USD: during the European session, the pair fell to $ 1.3764 , but then rose to $ 1.3805

GBP / USD: during the European session, the pair fell to $ 1.6473

USD / JPY: during the European session, the pair traded dropped to Y102.00, then returned to Y102.40

At 15:00 GMT the euro area indicator of consumer confidence will be released in March . At 17:45 GMT we planned a member of the Committee on the Federal Open Market R. Fisher. At 20:30 GMT will make the Bank of England Chief Economist Spencer Dale . At 20:30 GMT - we are a member of the Committee on the Federal Open Market N. Kocherlakoty . At 22:30 GMT member of the Committee on the Federal Open Market Jerome Stein .

-

13:03

Upgrades and downgrades before the market open:

Upgrades:

Goldman upgraded United Tech (UTX) from Neutral to Buy, target raised from $123 to $138

Downgrades:

Goldman downgraded Boeing (BA) from Buy to Neutral

Other:

-

13:00

Orders

EUR/USD

Offers $1.4000, $1.3967/75, $1.3945/50, $1.3890/00, $1.3845

Bids $1.3740, $1.3700/05, $1.3640, $1.3600

GBP/USD

Offers $1.6720/25, $1.6665/70, $1.6605/15, $1.6570, $1.6520

Bids $1.6420/30, $1.6400, $1.6380

AUD/USD

Offers $0.9200, $0.9165, $0.9150, $0.9140, $0.9100

Bids $0.9030, $0.8990/00, $0.8950, $0.8910/00

EUR/JPY

Offers Y142.90/00, Y142.50, Y142.00, Y141.70/75, Y141,20

Bids Y140.30, Y140.00, Y139.80, Y139.50

USD/JPY

Offers Y103.75, Y103.45, Y103.00, Y102.85

Bids Y101.90, Y101.70, Y101.20, Y101.00, Y100.50

EUR/GBP

Offers stg0.8470, stg0.8415/20, stg0.8405, stg0.8370/75

Bids stg0.8335/40, stg0.8320/25, stg0.8280/75

-

12:32

Canada: Consumer price index, y/y, February +1.1% (forecast +0.9%)

-

12:32

Canada: Bank of Canada Consumer Price Index Core, y/y, February +1.2% (forecast +1.1%)

-

12:31

Canada: Bank of Canada Consumer Price Index Core, m/m, February +0.7% (forecast +0.5%)

-

12:30

Canada: Retail Sales, m/m, January +1.3% (forecast +0.8%)

-

12:30

Canada: Retail Sales ex Autos, m/m, January +1.0% (forecast +0.9%)

-

12:30

Canada: Consumer Price Index m / m, February +0.8% (forecast +0.6%)

-

11:30

European stock rose

European stocks gained, with the Stoxx Europe 600 Index heading for its biggest weekly advance in five weeks, as investors watched the expiry of derivative contracts. U.S. stock-index futures and Asian shares also rose.

The Stoxx 600 rose 0.4 percent to 328.92 at 10:26 a.m. in London. The index has added 2.1 percent this week, for a 0.2 percent gain this year, as President Vladimir Putin said he wasn’t seeking to split up Ukraine after Crimea voted to join Russia.

“The market has proven to be very resilient and we think it will trade within this range in the next few months,” Supriya Menon, a strategist at Pictet Asset Management, said by phone from London. “We did turn more cautious on Europe at the end of February because so much is already priced into valuations. You have to be much more tactical now with your entry points to take advantage of any dips in the market.”

Trading may be more volatile today and volumes might be greater as futures and options contracts expire in a process known as witching. The VStoxx Index, which measures expected Euro Stoxx 50 Index volatility using options prices, has fallen 24 percent this week, for its largest weekly drop in 14 months.

Consumer confidence in the euro area improved this month, economists predicted before a report at 3 p.m. GMT. An advance reading will probably show the European Commission’s index of household confidence increased in March to minus 12.3 from minus 12.7 in February, according to the median of estimates.

Commerzbank climbed 3 percent to 13.40 euros. Morgan Stanley raised Germany’s second-largest lender to overweight, similar to buy, from equal weight. Analysts Hubert Lam and Francesca Tondi said non-core assets are undervalued and the likelihood of another capital increase has decreased.

Meggitt increased 1.7 percent to 477.6 pence. UBS upgraded its rating to buy from neutral, with analyst Charles Armitage citing the stock’s value relative to the FTSE 100 Index. The aerospace and defense engineering company lost 11 percent this year through yesterday, compared with a 3.1 percent retreat for the U.K. equity benchmark in the same period. Meggitt traded at 12.4 times projected earnings as of yesterday’s close, below the average of 13.1 for the gauge.

Havas slipped 1.6 percent to 5.71 euros. The French advertising agency partly-owned by billionaire Vincent Bollore said net income rose to 128 million euros ($176 million). That missed the 133 million-euro average analyst estimate.

Crest Nicholson Holdings Plc (CRST) declined 4.5 percent to 382 pence. Deutsche Bank AG is selling as many as 16.5 million shares in the U.K. housebuilder, according to a term sheet. The German lender is its largest publicly disclosed shareholder, holding a 10 percent stake.

At the current moment

FTSE 100 6,567.86 +25.42 +0.39%

CAC 40 4,342.01 +14.10 +0.33%

DAX 9,338.95 +42.83 +0.46%

-

10:10

Option expiries for today's 1400GMT cut

USD/JPY Y101.00, Y101.50, Y101.80, Y102.00, Y102.25, Y102.50, Y103.60, Y104.00

EUR/JPY Y142.80

EUR/USD $1.3850, $1.3900, $1.4000

GBP/USD $1.6470, $1.6535, $1.6645, $1.6750

EUR/GBP stg0.8335, stg0.8445, stg0.8450

USD/CHF Chf0.8700, Chf0.8810

EUR/CHF Chf1.2200, Chf1.2225

AUD/USD $0.9050, $0.9100, $0.9125, $0.9140, $0.9150

AUD/JPY Y90.50, Y91.50

NZD/USD $0.8600

USD/CAD C$1.1225, C$1.1250, C$!.1300

-

09:39

Asia Pacific stocks close

Asian stocks rose, with a regional index of shares outside Japan rebounding from the biggest loss yesterday since August.

Nikkei 225 Closed

S&P/ASX 200 5,338.08 +44.08 +0.83%

Shanghai Composite 2,047.62 +54.14 +2.72%

Li & Fung Ltd. surged 18 percent in Hong Kong after the world’s largest supplier of clothes and toys to retailers reported profit that beat analyst estimates and proposed to spin off its branding and licensing business.

Gome Electrical Appliances Holding Ltd. gained 8.3 percent in the city as earnings exceeded forecasts.

Metcash Ltd. slumped 9.5 percent in Sydney after the consumer goods marketing firm missed profit projections and said it will cut its dividend.

-

09:31

United Kingdom: PSNB, bln, February 7.47 (forecast 7.8)

-

09:00

Eurozone: Current account, adjusted, bln , January 25.3 (forecast 18.4)

-

08:42

FTSE 100 6,551.44 +9.00 +0.14%, CAC 40 4,333.93 +6.02 +0.14%, Xetra DAX 9,313.85 +17.73 +0.19%

-

06:41

European bourses are seen higher Friday: the FTSE nad DAX are seen 0.4% higher, with the CAC up 0.3%.

-

06:26

Asian session: The dollar was set for its biggest weekly advance in two months

00:00 Japan Bank holiday

The dollar was set for its biggest weekly advance in two months versus major peers before Dallas Federal Reserve President Richard Fisher speaks today amid prospects the central bank will pare stimulus. Fisher, who votes on policy this year, said this month that the Fed’s asset purchases are “distorting” financial markets. Fisher will speak about forward guidance in London today.

The greenback reached a two-week high against the euro yesterday, the day after Fed Chair Janet Yellen said borrowing costs could start rising “around six months” following an end to the U.S. central bank’s bond buying.

Australia’s dollar was set for a weekly advance after a gauge of economic surprises rose to a 10-month high. Citigroup Inc.’s Economic Surprise Index for the nation was at 50.10 yesterday after reaching 50.60 on March 13, the highest since May 23. A positive reading signals data releases exceed economist estimates.

Japan’s markets are shut today for a national holiday.

EUR / USD: during the Asian session, the pair traded in the range of $ 1.3775-90

GBP / USD: during the Asian session, the pair traded in the range of $ 1.6500-20

USD / JPY: on Asian session the pair traded in the range of Y102.30-40

UK borrowing data is set for release at 0930GMT in an otherwise data light calendar. -