Notícias do Mercado

-

20:00

DJIA 15,010.20 7.18 0.05%, S&P 500 1,652.87 0.52 0.03%, NASDAQ 3,627.36 13.77 0.38%

-

18:48

American focus: dollar moderately rising in anticipation of the Fed's protocols

During the U.S. session, the greenback shows moderate gains against major currencies. Market participants expect the publication of the minutes of the last meeting of the Federal Open Market Committee Federal Reserve, hoping to get more information about the prospects for monetary policy the Fed.

Support for the U.S. dollar has also had a strong statistics on the housing market in the U.S.. The report showed that sales in the secondary market in July rose to the highest level in nearly four years. This may reflect a jump in activity of buyers who want to complete the transaction before the mortgage rates will rise even higher. It reported sales of existing homes in July rose by 6.5% compared with the previous month to 5.39 million homes a year. July was the best month for sales since November 2009, when the tax credit for home buyers spurred activity in the market. Economists had forecast that sales will reach 5.15 million homes a year.

Quite volatile trading pound. Influence on its dynamics have provided the publication of macroeconomic reports. Sterling was able to update the session high against the dollar due to the released data on the balance of industrial orders from the Confederation of British Industry (CBI). The survey recorded 400 manufacturers that balance index of industrial orders in August reached the zero mark against -12 points in July and expectations of improvement to -8 points. The August figure was the highest value in the last 2 years and was another signal that the British economy is gaining momentum.

-

18:21

European stocks close

European stocks posted their longest losing streak in eight weeks amid speculation that the minutes of the Federal Reserve’s July meeting will give further details of when the central bank will slow its monthly bond purchases.

Investors will scrutinize the minutes of the Federal Open Market Committee’s July 30-31 meeting for signs of when the Fed will begin to reduce the $85 billion pace of monthly bond purchases. The U.S. central bank will start to scale back bond buying next month, according to 65 percent of economists surveyed by Bloomberg from Aug. 9-13. The median estimate called for purchases to drop to $75 billion a month. The Fed publishes the minutes after the close of European trading today.

National benchmark indexes declined in 14 of the 18 western-European markets today. Germany’s DAX dropped 0.2 percent, while the U.K.’s FTSE 100 fell 1 percent. France’s CAC 40 slipped 0.3 percent.

Heineken dropped 4 percent to 53.29 euros. The Amsterdam-based company reported adjusted earnings before interest and taxes of 1.33 billion euros ($1.8 billion) for the first half, missing the average analyst estimate of 1.34 billion euros. The brewer of the eponymous lager also said that the poor weather in Europe in the spring will affect its full-year earnings.

HSBC, Europe’s largest lender, fell 2.3 percent to 682 pence as bank stocks contributed the most to the Stoxx 600’s retreat. BHP Billiton lost 2.6 percent to 1,873 pence.

Vestas rallied 5.4 percent to 109 kroner after naming Anders Runevad as CEO. Runevad will succeed Ditlev Engel on Sept. 1 following two successive years of losses. The company also increased its forecast for free cash flow in 2013 to 200 million euros. It had projected positive cash flow this year.

Veolia Environnement SA jumped 8.3 percent to 11.46 euros, its highest price in 16 months. Morgan Stanley added Europe’s biggest water company to its best-ideas list.

-

17:00

European stocks closed in minus: FTSE 100 6,390.84 -62.62 -0.97%, CAC 40 4,015.09 -13.84 -0.34%, DAX 8,285.41 -14.62 -0.18%

-

16:44

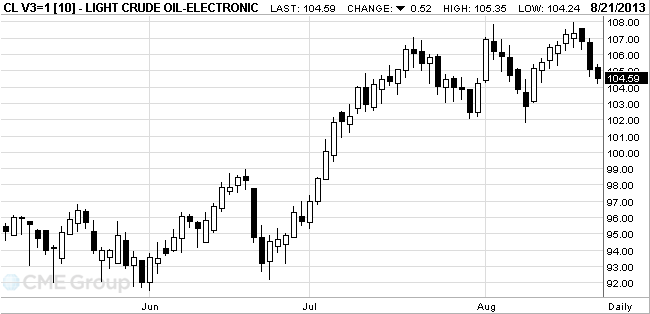

Oil fell

West Texas Intermediate crude dropped to the lowest level in more than a week amid speculation that the Federal Reserve will reduce economic stimulus.

Futures fell as much as 0.8 percent. The Federal Open Market Committee will publish minutes of a July meeting today, with 65 percent of economists surveyed by Bloomberg forecasting the Fed will taper bond purchases next month. A

WTI crude for October delivery slid 26 cents, or 0.2 percent, to $104.85 a barrel at 10:48 a.m. on the New York Mercantile Exchange. The contract traded at $104.75 before the release of the report at 10:30 a.m. in

Brent for October settlement dropped 5 cents to $110.10 a barrel on the London-based ICE Futures Europe exchange. Trading of futures was 9.2 percent below the 100-day average. The European benchmark crude traded at a $5.25 premium to WTI. The spread was $5.04 at yesterday’s settlement, the widest since June 28.

-

16:20

Gold stabilized

Gold prices stable ahead of today's publication of minutes of the last meeting of the Federal Reserve System.

Gold prices were under pressure for most of this year because of concerns about the fact that the U.S. central bank will begin to phase out its bond-buying program to a recovery in the U.S. economy. The belief that lasted for many years easing of monetary policy the Fed will lead to higher inflation, supported the price of gold.

Meanwhile, there are signs that, despite the recent rise in gold prices, the demand for gold coins and bars of the main consumers in Asia has been limited.

The spread between the cost of gold bullion in China and in London on Tuesday declined to $ 14 per ounce to $ 24 an ounce last week, traders said. Reducing the cost of gold in China, probably indicates a decline in demand in this country, which is the second-largest gold consumer after India.

In addition, the trading volume on the Shanghai Gold Exchange gradually declined since April, and this is "yet another signal that the demand for precious metals in Asia seems to be waning," - traders said.

As for India, which began on Tuesday, the Hindu festival of Raksha Bandhan is not provoked the traditional increase in demand for gold and silver, traders said. This festival offers a three-month season, when consumers tend to consider buying gold and silver right step.

The cost of the October gold futures on COMEX today dropped to $ 1359.60 per ounce.

-

15:30

U.S.: Crude Oil Inventories, August -4.0

-

15:00

U.S.: Existing Home Sales , July 5.39 (forecast 5.15)

-

14:49

Option expiries for today's 1400GMT cut:

EUR/USD $1.3250, $1.3300, $1.3325, $1.3350, $1.3400

USD/JPY Y97.00, Y97.50, Y97.60, Y98.00

EUr/JPY Y131.00

GBP/USD $1.5575, $1.5650

USD/CHF Chf0.9200, Chf0.9300, Chf0.9400

USD/SEK Sek6.5000

AUD/USD $0.9050, $0.9100, $0.9200

USD/CAD C$1.0315, C$1.0370, C$1.0380, C$1.0400

-

14:40

Moody's has lifted its collective outlook on U.S. states to stable from negative, citing increasing revenues following improvement in the labor and housing sectors, consumer confidence and the stock market.

-

14:34

U.S.Stocks open: Dow 14,974.30 -28.69 -0.19%, Nasdaq 3,605.90 -7.69 -0.21%, S&P 1,648.23 -4.12 -0.25%

-

14:21

Before the bell: S&P futures -0.24%, Nasdaq futures -0.28%

U.S. stock futures were lower as investors wait for the release of minutes from the U.S. Federal Reserve's latest monetary policy meeting.

Global Stocks:

Nikkei 13,424.33 +27.95 +0.21%

Hang Seng 21,817.73 -152.56 -0.69%

Shanghai Composite 2,072.96 +0.37 +0.02%

FTSE 6,416.31 -37.15 -0.58%

CAC 4,024.01 -4.92 -0.12%

DAX 8,283.47 -16.56 -0.20%

Crude oil $104.57 -0.51%

Gold $1365.30 -0.53%

-

13:57

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Caterpillar (CAT) downgraded to Neutral from Outperform at Daiwa Securities

Other:

Apple (AAPL) target raised to $560 from $500 at UBS

Hewlett-Packard (HPQ) target raised to $30 from $24 at BMO Capital Mkts

-

12:53

Orders

EUR/USD

Offers $1.3520, $1.3500, $1.3475/85, $1.3450, $1.3420, $1.3400

Bids $1.3385/80, $1.3375/70, $1.3360/50

GBP/USD

Offers $1.5750/55, $1.5720/25, $1.5700, $1.5695

Bids $1.5655/50, $1.5630/25, $1.5610/00, $1.5580/70, $1.5555/50, $1.5505/00

USD/JPY

Offers Y98.50, Y98.00, Y97.85/90, Y97.75/80

Bids Y97.20/10, Y96.95/90, Y96.80, Y96.60/50, Y96.00

AUD/USD

Offers $0.9180, $0.9150, $0.9120, $0.9090/00, $0.9070/75, $0.9035/40

Bids $0.9005/00, $0.8980, $0.8950, $0.8920, $0.8900, $0.8880/75

EUR/JPY

Offers Y131.95/00, Y131.80, Y131.45/50, Y131.10/20

Bids Y130.00, Y129.80/75, Y129.50

EUR/GBP

Offers stg0.8620/30, stg0.8600/10, stg0.8580/85

Bids stg0.8510/00, stg0.8485/80, stg0.8565/60

-

11:00

United Kingdom: CBI industrial order books balance, August 0 (forecast -8)

-

10:24

Option expiries for today's 1400GMT cut

EUR/USD $1.3250, $1.3300, $1.3325, $1.3350, $1.3400

USD/JPY Y97.00, Y97.50, Y97.60, Y98.00

EUr/JPY Y131.00

GBP/USD $1.5575, $1.5650

USD/CHF Chf0.9200, Chf0.9300, Chf0.9400

USD/SEK Sek6.5000

AUD/USD $0.9050, $0.9100, $0.9200

USD/CAD C$1.0315, C$1.0370, C$1.0380, C$1.0400

-

10:03

Asia Pacific stocks close

Asia’s benchmark stock index fell for a fifth day to trade at the lowest level in six weeks before the release of minutes of the Federal Reserve’s July meeting.

Nikkei 225 13,424.33 +27.95 +0.21%

Hang Seng 21,817.73 -152.56 -0.69%

S&P/ASX 200 5,099.99 +21.81 +0.43%

Shanghai Composite 2,072.96 +0.37 +0.02%

BHP Billiton Ltd. sank 2.2 percent in Sydney after the world’s biggest mining company reported a drop in second-half profit amid slowing growth in emerging economies.

Tokyo Electric Power Co. tumbled 9.3 percent after Japan’s Nuclear Regulation Authority said it plans to increase the severity level of a radiated water leak at its Fukushima plant.

Cnooc Ltd. surged 4.9 percent in Hong Kong after China’s largest offshore oil and gas explorer posted a better-than-estimated increase in first-half profit.

-

09:31

United Kingdom: PSNB, bln, July -1.6% (forecast -4.8)

-

08:40

FTSE 100 6,438.48 -14.98 -0.23%, CAC 40 4,042.44 +13.51 +0.34%, Xetra DAX 8,295.71 -4.32 -0.05%

-

07:21

European bourses are initially seen trading lower Wednesday: the FTSE down 19, the DAX down 18 and the CAC down 7.

-

07:01

Asian session: The dollar rose versus its Asia-Pacific counterparts

00:30 Australia Leading Index June +0.2% 0.0%

02:00 China Leading Index July +1.0% +1.4%

03:00 New Zealand Credit Card Spending July +5.4% +4.7%

The dollar rose versus its Asia-Pacific counterparts as investors await the release today of minutes from the Federal Reserve’s last meeting for signals on when it may curtail monetary stimulus. The Fed will publish today its July meeting minutes that may offer clues on whether policy makers will start reducing their $85 billion of monthly bond purchases known as quantitative easing or QE. The Federal Open Market Committee next gathers on Sept. 17-18 and will probably to reduce the program at that meeting, according to 65 percent of economists surveyed by Bloomberg News Aug. 9-13. The central bank has said it will keep benchmark rates near zero at least as long as unemployment is above 6.5 percent and inflation is no more than 2.5 percent.

The greenback extended gains against the Australian and New Zealand dollars into a third day.

The yen erased earlier losses as Asian stocks fell and Japanese regulators raised the severity of a radioactive water leak in Fukushima.

The euro was near a six-month high before manufacturing and services data tomorrow that may add to evidence of a recovery in the region.

EUR / USD: during the Asian session the pair traded in the range of $ 1.3415-35

GBP / USD: during the Asian session the pair traded in the range of $ 1.5645-70

USD / JPY: during the Asian session the pair rose to Y97.60

Across the Atlantic, the US data gets underway from 1100GMT, when the MBA Mortgage Index for the August 16 week will be released. At 1400GMT, the July Existing Home Sales data will be released. The pace of existing home sales is expected to rebound to a 5.20 million annual rate in July after slowing in June. Sales are still well above their year ago levels and should continue to move higher. In contrast, home supply remains well below its year ago level despite an upward trend over the last five months. The relatively low supply appears to be holding back sales, but lifting sales prices. The EIA Crude Oil Stocks data for the August 16 week will be published at 1430GMT. Perhaps the session's main release will be the FOMC minutes for the July 30/31 meeting at 1800GMT. Once again, the markets will be on "tapering" alert and any further positioning from Fed voters.

-

06:22

Commodities. Daily history for Aug 20’2013:

Change % Change Last

GOLD 1,372.00 5.80 0.42%

OIL (WTI) 104.96 -2.14 -2.00%

-

06:21

Stocks. Daily history for Aug 20’2013:

Nikkei 225 13,396.38 -361,75 -2,63%

Hang Seng 21,955.68 -508,02 -2,26%

S & P / ASX 200 5,078.18 -34,35 -0,67%

Shanghai Composite -0,62 -13,01 2,072.59%

FTSE 100 6,453.46 -12.27 -0.19%

CAC 40 4,028.93 -55.05 -1.35%

DAX 8,300.03 -66.26 -0.79%

DJIA 15,003.00 -7.75 -0.05%

S&P 500 1,652.35 6.29 0.38%

NASDAQ 3,613.59 24.50 0.68%

-

06:20

Currencies. Daily history for Aug 20'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3417 +0,60%

GBP/USD $1,5662 +0,10%

USD/CHF Chf0,9172 -0,75%

USD/JPY Y97,31 -0,33%

EUR/JPY Y130,56 +0,27%

GBP/JPY Y152,39 -0,22%

AUD/USD $0,9067 -0,55%

NZD/USD $0,7960 -1,34%

USD/CAD C$1,0394 +0,48%

-

06:00

Schedule for today, Wednesday, Aug 21’2013:

00:30 Australia Leading Index June +0.2% 0.0%

02:00 China Leading Index July +1.0% +1.4%

03:00 New Zealand Credit Card Spending July +5.4% +4.7%

08:30 United Kingdom PSNB, bln July 10.2 -4.8

10:00 United Kingdom CBI industrial order books balance August -12 -8

14:00 U.S. Existing Home Sales July 5.08 5.15

14:30 U.S. Crude Oil Inventories August -2.8

18:00 U.S. FOMC meeting minutes

-