Notícias do Mercado

-

20:00

-

19:20

American focus: the euro exchange rate fell

Euro fell against the dollar, reaching in this two-week low, helped by a weak presented a report on the euro area, which added speculation that the European Central Bank will cut interest rates to stimulate economic growth. It should be noted that the sharp drop in business activity in Germany has overshadowed the data output to ease the recession in France in April. As it became known, the PMI index for the services sector in the euro area rose to the level of April of 46.6, compared with 46.4 in March, below the 50 level that separates growth from contraction. Add that bad index for the euro area as a whole has coincided with a decrease in the index for German companies that make up the backbone of the economy in the eurozone. Meanwhile, studies have shown that the euro-zone companies are cutting jobs at a faster pace this month, after the March survey found that companies are firing employees at a slower pace. Economists note that at the moment clarity about the outlook completely absent, and as long as this situation remains, it will slow economic growth, and the decline will continue.

Sterling fell to a two-week low against the dollar, but later still managed to recover most of the losses after a report from the Confederation of British Industry showed that the balance of industrial orders declined significantly in April, reaching with its lowest level in half a year, in spite of Economists forecast a modest improvement, which was mainly due to the fall in domestic demand. According to the report, the balance of industrial orders fell in April to a level of -25, compared to -15 in March. Note that according to the average forecast of most economists, the value of this index would grow to -14. We add that the latest reading was the lowest since October 2010. In addition, the data presented today show that in the three months ended April, the number of new orders fell slightly, while the index, which measures expectations for the next quarter orders grew. Note also that the number of producers who expect to increase the total volume of new orders was 22%, while 28% expected a decrease of orders, against which the balance amounted to 6%. Note that the balance was much lower than the expected 14%, but remained above the long term average level to 3%.

The Canadian dollar traded at almost a six-week low against the U.S. dollar on the data from Europe and China, which indicate a slowdown in global economic growth, undermining demand for Canadian exports. Meanwhile, we observe the dynamics of trading was influenced by a report from Statistics Canada, which showed that retail sales in February rose at a faster pace than expected. In real terms, however, sales remained at the same level, which means that the February increase was driven mainly by higher prices, particularly for gasoline. Agency data showed that retail sales rose 0.8% to 39.55 billion Canadian dollars ($ 38.54 billion), which exceeded the expected 0.3%. Excluding the auto sector index rose by 0.7% m / m vs. 0.5% expected and revised January figure of 0.4%.

-

18:20

European stock close:

European stocks jumped the most in eight months as ARM (ARM) Holdings Plc and Cie. Financiere Richemont SA reported results that topped estimates and speculation grew that the region's central bank will cut interest rates.

The Stoxx Europe 600 Index (SXXP) soared 2.4 percent to 292.63 at the close of trading, the biggest jump since Aug. 3.

Stocks extended gains even after a report showed euro-area services and manufacturing output shrank for a 15th month in April. The reading of 46.5 in the Markit Economics purchasing- managers index boosted speculation the European Central Bank will trim interest rates when it meets next week.

A separate report showed Chinese manufacturing expanded at a slower pace than forecasts this month. The preliminary PMI for April released by HSBC Holdings Plc and Markit stood at 50.5, compared with a final 51.6 in March. That was below the median economist estimate of 51.5.

National benchmark indexes climbed in all 18 western European markets, except Greece.

FTSE 100 6,406.12 +125.50 +2.00% CAC 40 3,783.05 +130.92 +3.58% DAX 7,658.21 +180.10 +2.41%

ARM surged 12 percent to 972 pence, the highest price since March 2000. Revenue in the quarter ending in March rose 29 percent to 170.3 million pounds ($260 million) amid demand for it graphics and processing technology, the company said. Analysts had predicted 160 million pounds.

Richemont (CFR) rallied 8.3 percent to 73.80 Swiss francs, the biggest gain since December 2008. The Swiss company said full- year net income climbed about 30 percent as the dollar's strength against the euro boosted sales growth. Analysts had expected a 25 percent gain in profit.

STMicroelectronics NV, a maker of semiconductors, rallied 9.2 percent to 6.13 euros even after reporting a first-quarter net loss. Chief Executive Officer Carlo Bozotti told analysts on a conference call he expects "significant growth" in the second half of 2013, driven by new products and improved demand.

Telecom Italia SpA (TIT) increased 6.3 percent to 61.4 euro cents. The Italian phone company that's exploring a separation of its fixed-line assets is considering a sale of an initial 30 percent stake in the new company to state lender Cassa Depositi e Prestiti, two people familiar with the matter said.

Imtech tumbled 5.6 percent to 8.39 euros after the Dutch provider of stadium infrastructure for the London Olympics increased a writedown on projects in Germany by 70 million euros ($91 million) to about 220 million euros.

-

17:00

-

16:40

Oil: an overview of the market situation

The price of oil fell, dropping at the same time below $ 99, helped by a weaker-than-expected manufacturing data from China and Germany, which have worsened the prospects of demand for fuel.

As it became known, in the current month increase production sector in China has slowed. According to the report, a preliminary purchasing managers' index for the manufacturing sector from HSBC Holdings Plc and Markit Economics was 50.5, compared with a final figure for March, equal to 51.6. Published data fell short of analysts' forecasts, which suggested that the figure will be 51.5. Value is at the level above 50, indicating that the increase in production areas.

Note that a surprise to experts also found a reduction of business activity among German companies, but in the whole Eurozone services PMI rose slightly, being at the same time close to economists' forecasts.

We also add that prevented a sharper drop in oil prices helped the tense situation in the oil producing countries. As it became known, at least 23 people were killed in confrontations among the Iraqi forces and Sunni Muslims near Kirkuk. Later in the day, a bomb blast, at least seven people were killed and 17 were injured.

Meanwhile, we note that the dynamics of the trade is also affected by expectations about tomorrow's report on U.S. oil reserves, which will help to assess the demand of the largest oil consumer in the world. We add that, according to the predictions of many economists, crude oil inventories rose last week.

The cost of the June futures on U.S. light crude oil WTI (Light Sweet Crude Oil) fell to 88.93 dollars per barrel, the lowest intraday level since Dec. 19.

June futures price for North Sea Brent crude oil mixture fell $ 0.40 to $ 99.99 a barrel on the London exchange ICE Futures Europe.

-

16:20

Gold: an overview of the market situation

Gold prices fell today, losing more than one percent, which was associated with the acceleration of the outflow from the largest gold exchange-traded fund, as investors shifted their attention toward other assets such as stocks. In addition, experts point out that the strengthening of the dollar also put pressure on prices. Note also that the precious metal retreated from one-week high, which was fixed on the basis of the previous session, as investors were concerned with the state of their positions, which they held for a long time.

Meanwhile, we add that to the dynamics of trade have influenced U.S. data. After reporting a sharp drop in new home sales in the previous month, the Commerce Department released a report showed relatively modest sales growth in March.

The report showed that new home sales in March rose 1.5% year on year to 417,000 from the unrevised 411,000 in February. Economists had expected sales to rise to 419,000.

On a monthly measurement of sales in the primary housing market in the U.S. fell in February by 7.6% from 445 000 four-year high in January. The number of unsold homes in the U.S. in March corresponds to 4.4 months of sales.

At the same time, considering the current situation in the market of precious metals, traders point to the pressure with a shift in the distribution of assets, while Goldman Sachs said it expected further decline in gold prices, coupled with the ongoing flow of the ETF.

Note that the data showed that stocks in the SPDR Gold Trust fell by 1.6%, reaching thus the lowest level since November 2009, which followed the daily falls of less than 1% last week.

The cost of the June gold futures on COMEX today dropped to 1408.30 dollars per ounce.

-

15:20

U.S. new home sales show modest rebound in March

After reporting a sharp drop in new home sales in the previous month, the Commerce Department released a report on Tuesday showing a relatively modest rebound in sales in the month of March.

The report showed that new home sales rose 1.5 percent to an annual rate of

The monthly increase in new home sales in March came after sales tumbled 7.6 percent in February from a four-year high of

-

15:06

Canadian retail sales climbed at a faster-than-expected pace in February

Canadian retail sales climbed at a faster-than-expected pace in February, marking the best back-to-back monthly performance since the fall of 2011, Statistics Canada said Tuesday.

In volume terms, however, sales were flat, which means the February advance was largely due to higher prices, in particular for gasoline.

The data agency said retail sales rose 0.8% to 39.55 billion Canadian dollars ($38.54 billion), which beat expectations for a 0.3% gain among traders, according to economists at Royal Bank of

-

15:00

-

14:47

Option expiries for today's 1400GMT cut

EUR/USD $1.2900, $1.2950, $1.3000, $1.3030, $1.3050, $1.3065, $1.3100, $1.3135, $1.3200

USD/JPY Y98.00, Y99.00, Y99.50, Y100.00, Y100.50, Y101.00

EUR/JPY Y122.25

GBP/USD $1.5140, $1.5200, $1.5250, $1.5260

AUD/USD $1.0250, $1.0260, $1.0300, $1.0320

EUR/AUD A$1.2640

USD/CAD C$1.0260

-

14:35

-

14:29

Before the bell: S&P futures +0.32%, Nasdaq futures +0.54%

U.S. stock-index futures rose as Travelers Cos. and DuPont Co. beat estimates, outweighing a report that showed China's manufacturing is expanding at a slower pace this month.

Global Stocks:

Nikkei 13,529.65 -38.72 -0.29%

Hang Seng 21,806.61 -237.76 -1.08%

Shanghai Composite 2,184.54 -57.63 -2.57%

FTSE 6,372.44 +91.82 +1.46%

CAC 3,744.46 +92.33 +2.53%

DAX 7,605.12 +127.01 +1.70%

Crude oil $88.02 -0.74%

Gold $1415.60 -0.39%

-

14:00

-

13:31

-

13:31

-

13:27

European session: the euro declined

06:00 Switzerland Trade Balance March 2.10 1.73 1.9

07:00 France Manufacturing PMI (Preliminary) April 44.0 44.2 44.4

07:00 France Services PMI (Preliminary) April 41.3 42.3 44.1

07:30 Germany Manufacturing PMI (Preliminary) April 49.0 49.0 47.9

07:30 Germany Services PMI (Preliminary) April 50.9 51.1 49.2

08:00 Eurozone Manufacturing PMI (Preliminary) April 46.8 46.8 46.5

08:00 Eurozone Services PMI (Preliminary) April 46.4 46.7 46.6

08:30 United Kingdom PSNB, bln March 4.4 13.9 16.7

10:00 United Kingdom CBI industrial order books balance April -15 -14 -25

11:00 United Kingdom MPC Member McCafferty Speaks

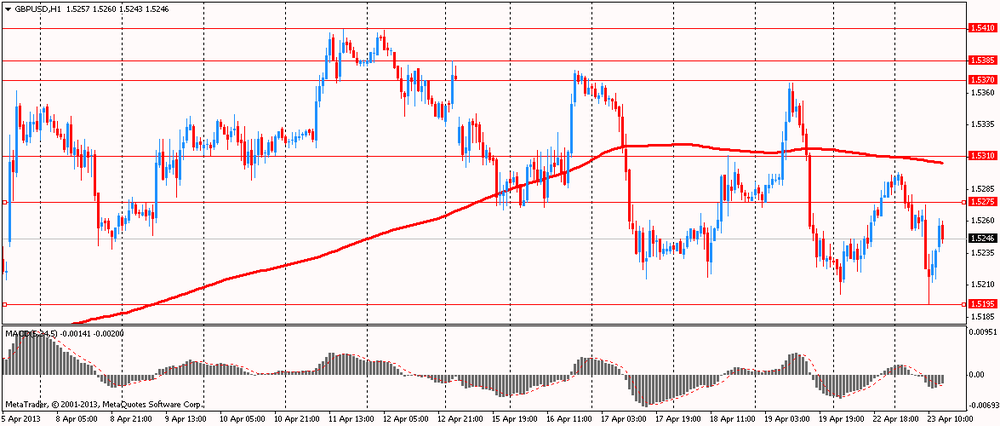

The British pound during the session updated intraday lows against the dollar on record PSNB, but then stabilized and recovered somewhat. According to the Confederation of British Industry, the April CBI industrial orders index fell to -25 from the March level of the value -15. Analysts had expected a slight improvement to -14. In March, public sector net borrowing of Britain (PSNB) increased to 16,747 billion pounds, although analysts expect growth to 14.000 billion pounds. February's result was also revised to increase - from 4.356 billion pounds to 7.196 billion pounds.

The euro fell against the dollar on weak results PMI Germany. Activity in the private sector of the eurozone declined again in April. Such developments are likely to trigger the growth of appeals to the rejection of austerity measures in favor of the policy instruments that promote growth.

According to a survey of purchasing managers, active in German business confidence fell for the first time since November. Together with a similar report testifying to the slowdown in manufacturing activity in China, it has raised concern about the likely decline in global growth.

In April, a preliminary PMI index of manufacturing activity in the country has decreased to around 47.9 to 49 pips. in March. The result was weaker than the market forecast of 49. A similar index in the services sector also dropped from 50.9 pts. in March to 49.2, contrary to expectations of growth to 51. France reported that preliminary index of manufacturing activity PMI Markit rose to 44.4 in April, surpassing the forecast of 44.3 and 44.0 March result, while the same index in the service sector rose from 41.3 to 44.1, compared with an expected 42.0.

The disappointing news came today from China, where preliminary index of manufacturing activity in China HSBC PMI in March amounted to 50.5 (vs. 51.5). According to experts, these results have reinforced voiced over the weekend words of the head of the Central Bank of China that the country is going now to the "slower pace of sustainable growth." Market and leading institutions such as the IMF still predicts China's GDP growth this year at 8 +%.

EUR / USD: during the European session, the pair fell to $ 1.2971

GBP / USD: during the European session, the pair fell to $ 1.5195

USD / JPY: during the European session, the pair fell to Y98.47

At 12:30 GMT Canada will release the change in the volume of retail sales, the change in retail sales excluding auto sales for February. In the U.S., will be released at 13:00 GMT the index of business activity in the manufacturing sector in April, the 14:00 GMT - sales in the primary market in March, at 20:30 GMT - the change in volume of crude oil, according to API. At 21:00 GMT we will know the decision of the Reserve Bank of New Zealand's main interest rate and the accompanying statement will be made of the Reserve Bank of New Zealand.

-

13:10

Orders

EUR/USD

Offers $1.3150/55, $1.3130, $1.3100, $1.3050, $1.3015/20

Bids $1.2970, $1.2950/40, $1.2920

GBP/USD

Offers $1.5330, $1.5300/10, $1.5250

Bids $1.5160/50, $1.5130/20, $1.5100/090

AUD/USD

Offers $1.0345/50, $1.0320, $1.0300, $1.0275/80

Bids $1.0220, $1.0200, $1.0185/80, $1.0155/50, $1.0120/15, $1.0100

EUR/GBP

Offers stg0.8630/40, stg0.8610/15, stg0.8600

Bids stg0.8500, stg0.8485/80, stg0.8460/50

EUR/JPY

Offers Y129.90/00, Y129.80/85, Y129.40/50, Y128.90/00, Y128.55/60

Bids Y127.55/50, Y127.10/00, Y126.80, Y126.55/50

USD/JPY

Offers Y99.70, Y99.30, Y99.10/20

Bids Y98.50, Y98.30, Y98.00

-

11:30

European stocks advanced for a third day

European stocks advanced for a third day as companies from ARM Holdings Plc to Cie. Financiere Richemont SA reported better-than-estimated results. Asian shares declined and U.S. index futures fluctuated.

A Chinese purchasing managers' index for April released by HSBC Holdings Plc and Markit Economics today had a preliminary reading of 50.5, compared with a final 51.6 in March. That was below the median 51.5 estimate in a survey. A reading above 50 indicates expansion.

Euro-area services and manufacturing output contracted for a 15th month in April, with a composite index based on a survey of purchasing managers holding at 46.5, according to Markit.

ARM surged 7.5 percent to 934 pence, the biggest jump since Feb. 5. Revenue in the quarter ending in March rose 29 percent to 170.3 million pounds ($260 million), the Cambridge, England- based company said. Analysts had predicted 160 million pounds, according to the average of a survey.

Richemont rallied 5.7 percent to 72 Swiss francs, the biggest gain since Jan. 9. The Swiss company said full-year net income climbed about 30 percent as the dollar's strength against the euro boosted sales growth. Analysts had expected a 25 percent gain in profit, according to the average of 17 estimates.

STMicroelectronics NV, a maker of semiconductors, advanced 6.1 percent to 5.96 euros even after reporting a first-quarter net loss. Chief Executive Officer Carlo Bozotti told analysts on a conference call he expects "significant growth" in the second half of 2013, driven by new products and improved demand.

FTSE 100 6,328.19 +47.57 +0.76%

CAC 40 3,708.19 +56.06 +1.53%

DAX 7,516.61 +38.50 +0.51%

-

11:00

-

10:32

Tuesday: Asia Pacific stocks close

Asian stocks fell, with the regional benchmark index heading for its first decline in three days, after a preliminary report showed Chinese manufacturing expanded less than economists estimated.

Nikkei 225 13,568.37 +251.89 +1.89%

S&P/ASX 200 4,966.55 +34.64 +0.70%

Shanghai Composite 2,242.17 -2.47 -0.11%

Agricultural Bank of China Ltd., the nation's third-largest lender, slid 3.1 percent, the most in two months, in Hong Kong.

Yamada Denki Co. sank 4.8 percent in Tokyo after the consumer electronics retailer missed its full-year profit forecast.

Woodside Petroleum Ltd., Australia's second-biggest oil producer, jumped 9.7 percent after announcing plans to return cash to shareholders. -

10:16

Option expiries for today's 1400GMT cut

EUR/USD $1.2900, $1.2950, $1.3000, $1.3030, $1.3065, $1.3100, $1.3135, $1.3200

USD/JPY Y98.00, Y99.00, Y99.50, Y100.00, Y100.50, Y101.00

EUR/JPY Y122.25

GBP/USD $1.5140, $1.5200, $1.5250, $1.5260

AUD/USD $1.0250, $1.0260, $1.0300, $1.0320

EUR/CHF A$1.2640

USD/CAD C$1.0260

-

09:43

FTSE 100 6,280.62 -5.97 -0.09%, CAC 40 3,680.9 +28.77 +0.79%, DAX 7,478.11 +18.15 +0.24%

-

09:31

-

08:59

Eurozone: Services PMI, April 46.6 (forecast 46.7)

-

08:58

-

08:33

Germany: Services PMI, April 49.2 (forecast 51.1)

-

08:32

Germany: Manufacturing PMI, April 47.9 (forecast 49.0)

-

07:59

France: Manufacturing PMI, April 44.4 (forecast 44.2)

-

07:59

France: Services PMI, April 44.1 (forecast 42.3)

-

07:40

European bourses are seen opening narrowly mixed Tuesday: the FTSE up 3, the DAX down 2 and the CAC up 7.

-

07:25

Asian session: The euro slid

00:00 Australia Conference Board Australia Leading Index February +0.2% +0.3%

01:45 China HSBC Manufacturing PMI (Preliminary) April 51.6 51.4 50.5

The euro slid before data projected to show services and manufacturing output in Europe shrank. A composite PMI for services and manufacturing industries was unchanged at 46.5 in April, London-based Markit Economics is predicted to say according to the median estimate of economists surveyed by Bloomberg before today's report. Readings below 50 indicates contraction.

The Ifo institute's business climate index for Germany, based on a survey of 7,000 executives, probably fell to 106.2 this month from 106.7, a separate poll showed before tomorrow's release.

The Australian and New Zealand currencies led losses versus the yen and dollar after the Purchasing Managers' Index for China by HSBC Holdings Plc and Markit Economics missed economists' forecasts. The preliminary PMI for China was 50.5 this month compared with a final 51.6 reading for March. The number was below the median 51.5 estimate in a Bloomberg News survey of analysts. A reading above 50 indicates expansion.

The yen rose versus all of its major peers after a private report signaled a slowdown in Chinese manufacturing, underscoring concern the largest Asian economy is faltering and boosting demand for refuge assets.

EUR / USD: during the Asian session the pair fell to $ 1.3030

GBP / USD: during the Asian session the pair fell to $ 1.5250.

USD / JPY: on Asian session the pair fell to Y98.55.

There is a full calendar Tuesday, including the release of the euro area flash manufacturing and service PMI numbers. The calendar gets underway with the release of the French April business climate indicator, including the April manufacturing and service sector sentiment indices, at 0645GMT. The release of the main flash PMI numbers starts at 0658GMT, with the release of the French flash numbers, followed at 0728GMT with the German numbers and the eurozone data at 0758GMT. That is followed at 0800GMT with the release of the Italian ISTAT April cоnsumer confidence numbers. Sovereign issuance in Europe sees Spain plan to tap 3-month Jul 19, 2013 Letra and tap 9-month Jan 24, 2014 Letra with indicative size to be announced on Monday, with expectations of between E3.5-E4.5bln.

-

07:00

Switzerland: Trade Balance, March 1.9 (forecast 1.73)

-

06:27

Commodities. Daily history for Apr 22’2013:

Change % Change Last

GOLD 1,424.90 29.30 2.10%

OIL (WTI) 88.76 0.75 0.85%

-

06:26

Stocks. Daily history for Apr 22’2013:

Change % Change Last

Nikkei 225 13,568.37 +251.89 +1.89%

Hang Seng 22,084.58 +71.01 +0.32%

S&P/ASX 200 4,966.6 +34.69 +0.70%

Shanghai Composite 2,242.17 -2.47 -0.11%

FTSE 100 6,280.62 -5.97 -0.09%

CAC 40 3,652.13 +0.17 0.00%

DAX 7,478.11 +18.15 +0.24%

Dow +19.58 14,567.09 +0.13%

Nasdaq +27.49 3,233.55 +0.86%

S&P +7.25 1,562.50 +0.47%

-

06:26

Currencies. Daily history for Apr 22'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3061 +0,08%

GBP/USD $1,5287 +0,37%

USD/CHF Chf0,9341 +0,05%

USD/JPY Y99,30 -0,20%

EUR/JPY Y129,70 -0,15%

GBP/JPY Y151,78 +0,15%

AUD/USD $1,0271 -0,04%

NZD/USD $0,8425 +0,15%

USD/CAD C$1,0260 -0,04%

-

06:07

Schedule for today, Tuesday, Apr 23’2013:

00:00 Australia Conference Board Australia Leading Index February +0.2%

01:45 China HSBC Manufacturing PMI (Preliminary) April 51.6 51.4

06:00 Switzerland Trade Balance March 2.10 1.73

07:00 France Manufacturing PMI (Preliminary) April 44.0 44.2

07:00 France Services PMI (Preliminary) April 41.3 42.3

07:30 Germany Manufacturing PMI (Preliminary) April 49.0 49.0

07:30 Germany Services PMI (Preliminary) April 50.9 51.1

08:00 Eurozone Manufacturing PMI (Preliminary) April 46.8 46.8

08:00 Eurozone Services PMI (Preliminary) April 46.4 46.7

08:30 United Kingdom PSNB, bln March 4.4 13.9

10:00 United Kingdom CBI industrial order books balance April -15 -14

11:00 United Kingdom MPC Member McCafferty Speaks

12:30 Canada Retail Sales, m/m February +1.0% +0.3%

12:30 Canada Retail Sales ex Autos, m/m February +0.5% +0.5%

12:45 Canada BOC Gov Carney Speaks

12:45 Canada Gov Council Member Macklem Speaks

13:00 U.S. Manufacturing PMI (Preliminary) April 54.6 54.3

14:00 U.S. New Home Sales March 411 419

20:30 U.S. API Crude Oil Inventories April -6.7

21:00 New Zealand RBNZ Interest Rate Decision 2.50% 2.50%

21:00 New Zealand RBNZ Rate Statement

-