Notícias do Mercado

-

20:00

DJIA 15,033.30 123.18 0.83%, S&P 500 1,615.23 11.97 0.75%, NASDAQ 3,401.09 24.87 0.74%

-

19:33

American focus: the dollar strengthened against the yen and the pound

The U.S. dollar rose against the yen after a series of statistics and comments President Federal Reserve Bank of New York Uilliyama Dudley. The labor market is the number of initial claims for unemployment benefits fell last week to 346 thousand, and personal income and spending showed an increase in May. So, Americans are spending more in the past month by 0.3% m / m, and their incomes rose by 0.5% m / m with average expectations of +0.2% m / m It is also worth noting the growth of the index of pending home sales in May by 6.7% m / m to 112.3 points and the drop in the index of business activity in the Federal Reserve Bank of Kansas industry in June to -17 points with 5 points in May. The President of the Federal Reserve Bank of New York Willie Dudley, in turn, said that the central bank may extend bond purchases if the economy does not justify the hopes regulators.

The euro rose against the dollar after a report from the European Commission showed that in June, the index of sentiment in the economy increased markedly, thereby exceeded the forecasts of experts, and reaching the highest level since May 2012. According to a report in the current month index of sentiment in the economy, which integrates research businesses and consumers across the euro zone, rose to 91.3, up from 89.5 in May. Economists say the index, as well as recent surveys of purchasing managers suggest that the recession in the euro zone may slow down in the second quarter. If this trend will continue, it will help to increase consumer spending and companies, as well as be able to contribute to a return to growth at the end of this year. However, it is worth noting that the index of sentiment in the economy remains below the average of 100.00 since 1990. The European Commission also reported that the increase in confidence has been allocated for the five largest economies of the eurozone - the largest increase was recorded in Spain and Italy. However, confidence fell in Greece, Austria and Slovakia.

Value of the pound fell sharply against the U.S. dollar in the background that the final data, which were presented by the Office for National Statistics (ONS) showed that the British economy could avoid a recession in the first quarter, while confirming the initial estimates. According to the report, in the first three months of this year, gross domestic product grew by 0.3%, while changing the 0.2% decline that was recorded in the fourth quarter of last year. It should be noted that the last value found in accordance with the forecasts of experts. Meanwhile, it was revealed that, compared with the first quarter of 2012 the economy grew by 0.3%, after zero growth in the previous quarter, which was a surprise to many experts, as they were waiting for confirmation of the initial assessment - at the level of 0.6 %. The Office for National Statistics also reported that first-quarter GDP is estimated to have been 3.9% lower than before the peak of the financial crisis peak in the first quarter of 2008. In addition, it was noted that a review of past GDP figures showed that the economy has not recorded double-dip recession in 2012. In the ONS today announced that in the first quarter of 2012, the economy showed zero increase, instead of the earlier estimate of 0.1% contraction, so that there were no two consecutive quarterly declines that define a recession.

-

18:30

European stocks close

European stocks climbed for a third day, the longest winning streak for the Stoxx Europe 600 Index in five weeks, as a report showed that U.S. consumer spending rebounded last month.

National benchmark indexes advanced in 15 of the 18 western-European markets. France's CAC 40 climbed 1 percent, Germany's DAX added 0.6 percent and the U.K.'s FTSE 100 jumped 1.3 percent.

Alcatel-Lucent rose 6.4 percent to 1.40 euros. Morgan Stanley reiterated its overweight recommendation, which is similar to a buy rating, after Alcatel yesterday started a 550 million-euro ($716 million) convertible bond issue and bought back debt as part of its strategy to reduce financing costs. The brokerage said the plan would benefit shareholders.

Alcatel said as markets closed that it raised the amount of the sale to 629 million euros.

Drax surged 7.3 percent to 573 pence, after the U.K. Department of Energy and Climate Change set the subsidy rates for power from renewable energy plants. The government said it will pay pay biomass-conversion plants 105 pounds per megawatts per hour.

Drax brought the first converted biomass unit at its coal-burning plant into service in April.

DS Smith Plc climbed 5.4 percent to 252.7 pence. The paper company increased its dividend by 36 percent to 8 pence apiece, more than analysts had estimated. DS Smith also reported full-year revenue and earnings that beat analysts' estimates. The company added that the current year has started well, matching its expectations.

Subsea 7 tumbled 13 percent to 106 kroner after the oil-field services provider said it no longer expects full-year earnings to grow from 2012. The Norwegian company increased its estimate for the full-life loss on the Guara-Lula NE project off the coast of Brazil.

-

17:24

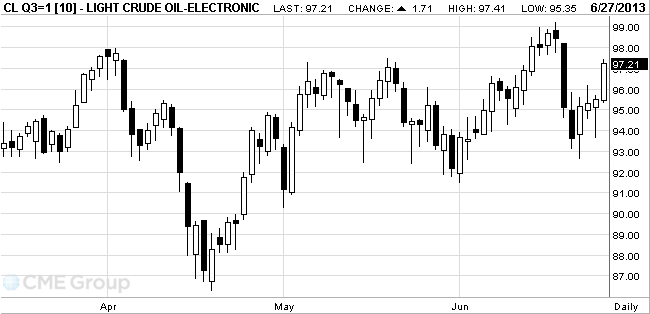

Oil climbed to a one-week high

West Texas Intermediate climbed to a one-week high as fewer Americans filed claims for unemployment benefits last week and consumer spending rebounded in May.

Prices gained for a fourth day as jobless claims decreased to 346,000 from a revised 355,000 the prior period, the Labor Department reported. Household purchases, which account for about 70 percent of the economy, rose 0.3 percent last month, the Commerce Department said.

The four-week moving average of jobless claims, a less-volatile measure than the weekly figures, dropped to 345,750 last week from 348,500, according to the Labor Department.

The gains in consumer spending followed a 0.3 percent decline the prior month that was the biggest since September 2009, according to the Commerce Department.

More Americans signed contracts in May to buy previously owned homes than at any time in more than six years, a sign of bigger progress in the industry, figures from the National Association of Realtors showed.

WTI for August delivery rose 99 cents, or 1 percent, to $96.49 a barrel at 11:16 a.m. on the New York Mercantile Exchange. The price reached $96.54, the highest since June 20. The volume of all futures traded was 16 percent lower than the 100-day average for the time of day. Futures have declined 0.8 percent in the second quarter.

Brent for August settlement increased 90 cents, or 0.9 percent, to $102.56 a barrel on the London-based ICE Futures Europe exchange. The volume traded was 39 percent below the 100-day average.

-

17:00

European stocks closed in plus: FTSE 100 6,243.4 +77.92 +1.26%, CAC 40 3,762.19 +36.15 +0.97%, DAX 7,990.75 +49.76 +0.63%

-

16:27

Gold stabilized after 3-day fall

The value of gold is kept in a range after three consecutive sessions of decline, as weak U.S. GDP returned to investors hope for continuation of the Fed's incentive program.

U.S. GDP in the first quarter rose, according to the final estimate of 1.8 percent compared to the same period of 2012, with growth forecast at 2.4 percent, reported Wednesday the Commerce Department. Markets expect that these data will influence the Fed's decision to reduce the volume of buying up bonds this year.

From the beginning, gold fell by more than 26 percent, and the second quarter could be the worst for the market since 1968, due to growth in stock price and the value of the dollar. ABN Amro Bank after other banks lowered the forecast of the price of gold at the end of 2013 to $ 1,100 an ounce from $ 1,300, and the forecast for the end of 2014 - up to $ 900 to $ 1,000.

Stocks of the world's largest exchange-traded fund backed by gold (ETF) SPDR Gold Trust fell on Tuesday to its lowest level in more than four years.

The demand in the physical markets in China and Asia, though improved from the fall in prices, but not as much as in April, when prices showed the sharpest drop in 30 years. Growth in demand in India to restrain the import duty, while in China - the fear of the credit crisis.

The cost of the August gold futures on COMEX today is trading in the range of 1223.40 - 1244.20 per ounce.

-

15:00

U.S.: Pending Home Sales (MoM) , May +6.7% (forecast +1.1%)

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.2700, $1.2980, $1.3015, $1.3050, $1.3100, $1.3140

USD/JPY Y96.50, Y97.00, Y97.50, Y98.00, Y98.50

GBP/USD $1.5370, $1.5600

AUD/USD $0.9200, $0.9300, $0.9350

-

14:34

U.S. Stocks open: Dow 15,003.37 +93.23 +0.63%, Nasdaq 3,397.51 +21.29 +0.63%, S&P 1,612.96 +9.70 +0.61%

-

14:30

Before the bell: S&P futures +0.63%, Nasdaq futures +0.50%

U.S. stock futures rose as reports showed consumer spending rebounded in May and fewer Americans filed claims for unemployment last week.

Global Stocks:

Nikkei 13,213.55 +379.54 +2.96%

Hang Seng 20,440.08 +101.53 +0.50%

Shanghai Composite 1,950.01 -1.48 -0.08%

FTSE 6,212.74 +47.26 +0.77%

CAC 3,737.86 +11.82 +0.32%

DAX 7,956.66 +15.67 +0.20%

Crude oil $95.77 +0.28%

Gold $1231.10 +0.11%

-

13:51

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Other:

Cisco Systems (CSCO) target raised to $28 from $25 at Stifel

Apple (AAPL) target lowered to $440 from $480 at Susquehanna

-

13:31

U.S.: PCE price index ex food, energy, Y/Y, May +1.1% (forecast +1.1%)

-

13:31

U.S.: Personal Income, m/m, May +0.5% (forecast +0.2%)

-

13:31

U.S.: Personal spending , May +0.3% (forecast +0.4%)

-

13:30

U.S.: Initial Jobless Claims, June 346 (forecast 351)

-

13:30

U.S.: PCE price index ex food, energy, m/m, May +0.1% (forecast +0.1%)

-

13:15

European session: the British Pound declined significantly

Data

01:00 New Zealand ANZ Business Confidence June 41.8 50.1

04:30 Japan All Industry Activity Index, m/m April -0.3% +0.5% +0.4%

06:45 France Consumer confidence June 79 80 78

07:55 Germany Unemployment Change June 21 6 -12

07:55 Germany Unemployment Rate s.a. June 6.9% 6.9% 6.8%

08:00 Eurozone M3 money supply, adjusted y/y May +3.2% +2.9% +2.9%

08:30 United Kingdom Current account, bln Quarter I -14.0 -11.8 -14.5

08:30 United Kingdom GDP, q/q (Finally) Quarter I +0.3% +0.3% +0.3%

08:30 United Kingdom GDP, y/y Quarter I +0.6% +0.6% +0.3%

09:00 Eurozone Business climate indicator June -0.76 -0.65 -0.68

09:00 Eurozone Economic sentiment index June 89.4 90.4 91.3

09:00 Eurozone Industrial confidence June -13.0 -12.3 -18.8

10:00 Eurozone EU Economic Summit June

The euro exchange rate recovered previously lost ground against the dollar, which has been associated with the publication of data that supported the single currency, as well as expectations of U.S. output reports. Expected to publish data on the state personal income and spending and the number of U.S. citizens reported new claims for unemployment benefits. According to the median forecast of economists amount of personal spending in the U.S. will grow up in May by 0.3%, the fastest pace in the last three months. A number of requests for unemployment benefits fall by 9,000 to 345,000 in the week ended June 22.

It should be noted that the report from the European Commission showed that in June, the index of sentiment in the economy increased markedly, thereby exceeded the forecasts of experts, and reaching the highest level since May 2012.

According to a report in the current month index of sentiment in the economy, which integrates research businesses and consumers across the euro zone, rose to 91.3, up from 89.5 in May. Economists say the index, as well as recent surveys of purchasing managers suggest that the recession in the euro zone may slow down in the second quarter. If this trend will continue, it will help to increase consumer spending and companies, as well as be able to contribute to a return to growth at the end of this year. However, it is worth noting that the index of sentiment in the economy remains below the average of 100.00 since 1990.

The European Commission also reported that the increase in confidence has been allocated for the five largest economies of the eurozone - the largest increase was recorded in Spain and Italy. However, confidence fell in Greece, Austria and Slovakia.

We add that the pressure on the dollar strengthened after the unexpected revision of estimates of U.S. GDP for the 1st Quarter in the direction of the sharp decline. Fell short of forecast data for the 1st quarter at least temporarily reassured investors that the Fed may consider delaying reductions in asset purchases under the program of QE.

Value of the pound fell sharply against the U.S. dollar, against the background of the fact that the final data, which were presented by the Office for National Statistics (ONS) showed that the British economy could avoid a recession in the first quarter, while confirming the initial estimates.

According to the report, in the first three months of this year, gross domestic product grew by 0.3%, while changing the 0.2% decline that was recorded in the fourth quarter of last year. It should be noted that the last value found in accordance with the forecasts of experts.

Meanwhile, it was revealed that, compared with the first quarter of 2012 the economy grew by 0.3%, after zero growth in the previous quarter, which was a surprise to many experts, as they were waiting for confirmation of the initial assessment - at the level of 0.6 %.

The Office for National Statistics also reported that first-quarter GDP is estimated to have been 3.9% lower than before the peak of the financial crisis peak in the first quarter of 2008.

In addition, it was noted that a review of past GDP figures showed that the economy has not recorded double-dip recession in 2012. In the ONS today announced that in the first quarter of 2012, the economy showed zero increase, instead of the earlier estimate of 0.1% contraction, so that there were no two consecutive quarterly declines that define a recession.

The Australian dollar is rising for the fifth consecutive day after Kevin Rudd won the election and became the new Prime Minister of Australia. As Prime Minister Rudd was replaced by Julia Gillard, who headed the government since 2010. Gillard has resigned after Wednesday, June 26, lost the election of a Labour party in power in Australia.

EUR / USD: during the European session, the pair rebounded from $ 1.3010 to $ 1.3044

GBP / USD: during the European session, the pair fell to $ 1.5261

USD / JPY: during the European session, the pair rose to Y98.36

At 12:30 GMT the U.S. will release the main index for personal consumption expenditures index-deflator of personal consumption expenditures, and also announced a change in the level of spending for May. At 14:00 GMT the U.S. will report on changes in the volume of pending home sales for May. At 22:45 GMT New Zealand will release data on changes in the volume of building permits issued in May. At 23:01 GMT Britain will present indicator of consumer confidence from the GfK in June. At 23:30 GMT Japan will announce to the change in the level of household spending in May, and will release the consumer price index, the preliminary data on industrial production, and changes in the volume of retail sales for May.

-

13:00

Orders

EUR/USD

Offers $1.3151, $1.3100/05, $1.3060/65, $1.3050

Bids $1.3005, $1.3005/00, $1.2985/80, $1.2960/50, $1.2920/10

GBP/USD

Offers $1.5420/30, $1.5395/400, $1.5370/80, $1.5350, $1.5335

Bids $1.5265/60, $1.5255/50, $1.5240, $1.5220/10, $1.5200/185

AUD/USD

Offers $0.9450, $0.9415/20, $0.9395/00, $0.9370/75, $0.9345/50

Bids $0.9275/70, $0.9250/45, $0.9220, $0.9200, $0.9180

EUR/GBP

Offers stg0.8595/600, stg0.8575/80, stg0.8540-42, stg0.853

Bids stg0.8492, stg0.8470, stg0.8465/60, stg0.8445/40, stg0.8420

EUR/JPY

Offers Y128.75/80, Y128.59/60 29, Y128.45/50, Y128.40, Y128.15/20

Bids Y127.30/20, Y127.05/00, Y126.80, Y126.50, Y126.20

USD/JPY

Offers Y99.00, Y98.70/75, Y98.68, Y98.45/50, Y98.35/40

Bids Y97.50, Y97.35, Y97.25/20, Y97.10, Y97.05/00

-

11:30

Major stock indexes in Europe have not changed

European stocks were little changed, following the Stoxx Europe 600 Index's largest two-day rally in 11 months, as investors awaited a report on U.S. personal spending. U.S. index futures were also little changed, while Asian shares rallied.

The Stoxx 600 was unchanged at 284.53 at 11 a.m. in London after falling as much as 0.3 percent and rising as much as 0.2 percent. The gauge has tumbled 5.5 percent in June, its first monthly retreat in a year. Standard & Poor's 500 Index futures increased 0.2 percent today, following a two-day rally for the U.S. equity benchmark. The Federal Reserve chairman indicated on June 19 that the central bank may start paring its bond-buying program if the economy strengthens. Stocks rebounded yesterday after a report showing slower-than-estimated U.S. economic growth fueled speculation that the central bank will maintain stimulus. The Stoxx 600 has lost 3.2 percent this quarter, its first drop in a year, paring its advance in 2013 to 1.7 percent.

The federal government releases economic data at 8:30 a.m. that may show U.S. personal spending rose in May at the fastest pace in three months. A separate report from the Labor Department at the same time may show jobless claims fell last week.

Subsea 7 tumbled 16 percent to 103.10 kroner after saying it no longer expects full-year earnings to grow from 2012. The Norwegian company increased its estimate for the full-life loss on the Guara-Lula NE project off the coast of Brazil.

Solvay retreated 4.9 percent to 97.70 euros, the biggest drop on a gauge of European chemical makers. Lanxess AG slid 4.7 percent to 45.95 euros and BASF SE lost 3 percent to 67.62 euros after JPMorgan downgraded all three companies to underweight, which is similar to a sell recommendation.

Bankia added 2.2 percent to 59.7 euro cents as the banking group bailed out by the Spanish government last year sold the holding in IAG (IAG) that it obtained in the 2011 merger of British Airways and Iberia.

The company's Bankia Bolsa SA brokerage arm, together with Bank of America Corp., sold the 224.3 million IAG shares at 256 pence apiece, according to a statement.

DS Smith Plc (SMDS) climbed 4.3 percent to 250 pence. The paper company increased its dividend 36 percent to 8 pence apiece, more than analysts had estimated. DS Smith also reported full-year revenue and earnings that beat analysts' estimates. The company added that the current year has started well, matching its expectations.

FTSE 100 6,189.45 +23.97 +0.39%

CAC 40 3,727.65 +1.61 +0.04%

DAX 7,948.31 +7.32 +0.09%

-

10:28

Option expiries for today's 1400GMT cut

EUR/USD $1.2700, $1.2980, $1.3015, $1.3050, $1.3100, $1.3140

USD/JPY Y96.50, Y97.00, Y97.50, Y98.00, Y98.50

GBP/USD $1.5370, $1.5600

AUD/USD $0.9200, $0.9300, $0.9350

-

10:02

Eurozone: Industrial confidence, June -18.8 (forecast -12.3)

-

10:01

Eurozone: Business climate indicator , June -0.68 (forecast -0.65)

-

10:01

Eurozone: Economic sentiment index , June 91.3 (forecast 90.4)

-

09:43

Asia Pacific stocks close

Asian stocks rose, with the regional benchmark index on course for its biggest gain since September, after slower-than-estimated U.S. economic growth stoked speculation the Federal Reserve may hold back from reducing stimulus.

Nikkei 225 13,213.55 +379.54 +2.96%

Hang Seng 20,513.42 +174.87 +0.86%

S&P/ASX 200 4,811.3 +79.59 +1.68%

Shanghai Composite 1,950.01 -1.48 -0.08%

Samsung Electronics Co., the world's largest maker of smartphones, climbed 6.2 percent in Seoul.

China Gas Holdings Ltd. gained 5.4 percent in Hong Kong after the supplier of natural gas to 172 Chinese cities posted earnings that beat estimates.

Newcrest Mining Ltd., Australia's biggest gold producer, jumped 6.3 percent as the bullion headed for its first advance in four days.

-

09:32

United Kingdom: GDP, y/y, Quarter I +0.3% (forecast +0.6%)

-

09:32

United Kingdom: Current account, bln , Quarter I -14.5 (forecast -11.8)

-

09:31

United Kingdom: GDP, q/q, Quarter I +0.3% (forecast +0.3%)

-

09:20

FTSE 100 6,186.29 +20.81 +0.34%, CAC 40 3,715.14 -10.90 -0.29%, Xetra DAX 7,935.1 -5.89 -0.07%

-

09:01

Eurozone: M3 money supply, adjusted y/y, May +2.9% (forecast +2.9%)

-

08:56

Germany: Unemployment Change, June -12 (forecast 6)

-

08:56

Germany: Unemployment Rate s.a. , June 6.8% (forecast 6.9%)

-

07:45

France: Consumer confidence , June 78 (forecast 80)

-

07:45

France: Consumer confidence , June 78 (forecast 80)

-

07:26

European bourses are initially seen trading highest Thursday, after US indices closed near their highs and Asian stocks bounce: the FTSE up 30, the DAX up 32 and the CAC up 11.

-

07:23

Asian session: The Dollar Index held a six-day gain

01:00 New Zealand ANZ Business Confidence June 41.8 50.1

04:30 Japan All Industry Activity Index, m/m April -0.3% +0.5% +0.4%

The Dollar Index held a six-day gain, its longest winning streak in more than a year, before U.S. reports forecast to show spending rose at the fastest pace in three months and jobless claims declined. U.S. consumer spending probably increased 0.3 percent in May, after falling 0.2 percent the previous month, according to the median forecast in a Bloomberg News survey before today's report. Commerce Department data will also show incomes grew 0.2 percent last month after being unchanged in April, according to the Bloomberg poll.

Jobless claims fell by 9,000 to 345,000 in the week ended June 22, the Labor Department is projected to say according to a separate survey.

Euro demand was dented yesterday after European Central Bank President Mario Draghi said policy will remain stimulative.

Australia's dollar rallied for a fifth day as Kevin Rudd took over as prime minister, after winning leadership of the Labor party from Julia Gillard.

EUR / USD: during the Asian session the pair rose to $ 1.3035

GBP / USD: during the Asian session the pair rose to $ 1.5340

USD / JPY: during the Asian session the pair traded in the range of Y97.35/85

The European calendar gets underway at 0700GMT, when ECB'S Ewald Nowotny delivers a speech at the International Arab Banking Summit, in Vienna. AT the same time, German Chancellor Angela Merkel statement on the upcoming EU summit, results of G8 summit, in Berlin. Early data also due at 0700GMT, sees the release of Spanish May retail sales and the June flash HICP numbers. At 0755GMT, the German June unemployment data is due, to be followed at 0800GMT by the release of the German May VDMA machine orders data. ECB Governing Council member Jens Weidmann is set to deliver a speech to the Federation of European Securities Exchanges, in Berlin at 0815GMT. At 0900GMT, German Labour Minister Ursula von der Leyen delivers a press conference in Berlin following the earlier jobs data. At 0900GMT, the EMU Jun business climate indicator is set for publication, along with the June consumer confidence numbers. ECB Governing Council member Christian Noyer will deliver a press conference in Paris, also at 0900GMT. German Finance Minister Wolfgang Schaeuble delivers a speech to the Federation of European Securities Exchanges at 0930GMT.

UK data set for release at 0830GMT includes the Q1 Current Account numbers and the final estimate of the Q1 GDP numbers. There is no reason to expect GDP revision to the 0.3% figure published in previous estimates. The latest monthly data on construction output and industrial production are in line with the numbers pencilled in by National Statistics in the first two estimates of Q1 GDP.

-

06:22

Commodities. Daily history for Jun 26’2013:

Change % Change Last

GOLD 1,229.60 -45.20 -3.55%

OIL (WTI) 95.45 0.13 0.14%

-

06:22

Stocks. Daily history for Jun 26’2013:

Nikkei 225 12,834.01 -135,33 -1,04%

Hang Seng 20,194.33 338,61 1,71%

S & P / ASX 200 4,731.7 75,74 1,63%

Shanghai Composite -9,02 -0,46 1,950.49%

FTSE 100 6,165.48 +63.57 +1.04%

CAC 40 3,726.04 +76.22 +2.09%

DAX 7,940.99 +129.69 +1.66%

DJIA 14,910.10 149.83 1.02%

S&P 500 1,603.26 15.23 0.96%

NASDAQ 3,376.22 28.34 0.85%

-

06:21

Currencies. Daily history for Jun 26'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3006 -0,45%

GBP/USD $1,5312 -0,72%

USD/CHF Chf0,9428 +0,52%

USD/JPY Y97,79 -0,16%

EUR/JPY Y127,16 -0,76%

GBP/JPY Y140,71 -6,65%

AUD/USD $0,9279 +0,23%

NZD/USD $0,7781 +0,49%

USD/CAD C$1,0475 -0,35%

-

06:00

Schedule for today, Thursday, June 27’2013:

1:00 New Zealand ANZ Business Confidence June 41.8 50.1

04:30 Japan All Industry Activity Index, m/m April -0.3% +0.5%

06:45 France Consumer confidence June 79 80

07:55 Germany Unemployment Change June 21 6

07:55 Germany Unemployment Rate s.a. June 6.9% 6.9%

08:00 Eurozone M3 money supply, adjusted y/y May +3.2% +2.9%

08:30 United Kingdom Current account, bln Quarter I -14.0 -11.8

08:30 United Kingdom GDP, q/q Quarter I +0.3% +0.3%

08:30 United Kingdom GDP, y/y Quarter I +0.6% +0.6%

09:00 Eurozone Business climate indicator June -0.76 -0.65

09:00 Eurozone Economic sentiment index June 89.4 90.4

09:00 Eurozone Industrial confidence June -13.0 -12.3

10:00 Eurozone EU Economic Summit June

12:30 U.S. Initial Jobless Claims June 354 351

12:30 U.S. Personal Income, m/m May 0.0% +0.2%

12:30 U.S. Personal spending May -0.2% +0.4%

12:30 U.S. PCE price index ex food, energy, m/m May 0.0% +0.1%

12:30 U.S. PCE price index ex food, energy, Y/Y May +1.1% +1.1%

14:00 U.S. Pending Home Sales (MoM) May +0.3% +1.1%

14:00 U.S. FOMC Member Dudley Speak

14:30 U.S. FOMC Member Jerome Powell Speaks

15:00 Switzerland SNB Quarterly Bulletin Quarter II

22:45 New Zealand Building Permits, m/m May +18.5% -3.9%

23:01 United Kingdom Gfk Consumer Confidence June -22 -21

23:15 Japan Manufacturing PMI June 51.5

23:30 Japan Household spending Y/Y May +1.5% +1.5%

23:30 Japan Tokyo Consumer Price Index, y/y June -0.2% +0.1%

23:30 Japan Tokyo CPI ex Fresh Food, y/y June +0.1% +0.2%

23:30 Japan Unemployment Rate May 4.1% 4.0%

23:30 Japan National Consumer Price Index, y/y May -0.7% -0.4%

23:30 Japan National CPI Ex-Fresh Food, y/y May -0.4% 0.0%

23:50 Japan Industrial Production (MoM) May +0.9% +0.2%

23:50 Japan Industrial Production (YoY) May -3.4% -2.3%

23:50 Japan Retail sales, y/y May -0.1% +0.1%

-

05:32

Japan: All Industry Activity Index, m/m, April +0.4% (forecast +0.5%)

-