Market news

-

15:07

US wholesale inventories in line with expectations in October

The U.S. Census Bureau announced today that October 2016 sales of merchant wholesalers were $452.2 billion, up 1.4 percent from the revised September level and were up 2.2 percent from the October 2015 level.

The August 2016 to September 2016 percent change was revised from the preliminary estimate of up 0.2 percent to up 0.4 percent. October sales of durable goods were up 1.1 percent from last month and were up 2.5 percent from a year ago.

-

15:03

US consumer confidence surged in early December - UoM survey

Consumer confidence surged in early December to just one-tenth of an Index point below the 2015 peak-which was the highest level since the start of 2004. The surge was largely due to consumers' initial reactions to Trump's surprise victory. When asked what news they had heard of recent economic developments, more consumers spontaneously mentioned the expected positive impact of new economic policies than ever before recorded in the long history of the surveys. To be sure, an equal number volunteered negative judgments about prospective economic policies, but the frequency of those negative references was less than half its prior peak levels whereas positive references were about twice its prior peak says surveys of consumers chief economist, Richard Curtin.

-

15:01

U.S.: Reuters/Michigan Consumer Sentiment Index, December 98 (forecast 94.5)

-

15:00

U.S.: Wholesale Inventories, October -0.4% (forecast -0.4%)

-

14:56

ECB contemplated bolder stimulus before compromise - Reuters

-

14:47

Bundesbank raised forecasts for the German economy

The German economy continues its steady rise, supported by a flexible internal demand which reinforce the labor market and incomes of the population, according to the Bundesbank.

Gross domestic product will grow by 1.8 percent this year, which is slightly faster than the expansion of 1.7 percent projected in June, the bank said in its semi-annual economic outlook.

Growth will continue at 1.8 percent next year, which was stronger than +1.4 percent expected in June. The Bank maintained a forecast for 2018 at 1.6 percent and predicted a 1.5 percent expansion in 2019.

The inflation forecast for 2018 was maintained at 1.7 per cent, while a higher figure of 1.9 percent was forecast for 2019. Inflation is expected to accelerate since labor costs are projected to increase strongly, the bank said. The bank added that consumer prices may rise further than expected, in particular in 2017.

-

14:22

ECB rejected Banca Monte dei Paschi di Siena for more time to raise capital. Shares suspended briefly from trading in Milan for excessive losses

The European Central Bank has rejected a request from Italian lender Banca Monte dei Paschi di Siena SpA for more time to raise capital, a person familiar with the matter said, paving the way for the government to step in and rescue the bank.

-

13:58

EUR/USD set to close the week in important bid area

-

13:40

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0500 (EUR 2,03bln) 1.0575 (715m) 1.0600 (3.42bln) 1.0625 (1.36bln) 1.0650 (2.61bln) 1.0700 (1.7bln) 1.0750 (2.46bln) 1.0800 (2.89bln) 1.0850 (1.24bln)

USD/JPY 112.25 (USD 800m) 113,75 (505m) 114,.00 (407m) 114.50 (786m)

GBP/USD 1.2300 (USD 398m) 1.2500 (453m)

AUD/USD 0.7300 (2.02bln) 0.7325 (669m) 0.7400 (419m) 0,7500 (952m)

USD/CAD 1.3200 (USD 1.37bln)

-

13:27

Riksbank will have to stay relatively dovish given the European Central Bank's dovish line - Danske

Danske Bank thinks the Riksbank will have to stay relatively dovish given the European Central Bank's dovish line Thursday. It will definitely have to do more QE and, in Danske's view, also a 10bp repo rate cut, although the latter is a close call, it says. "We see near-term upside risk for the EUR/SEK, as the market is not priced for a rate-cut scenario. However, in 2017, we expect the EUR/SEK to move lower on valuation, global reflation and relatively strong growth in the Swedish economy." EUR/SEK is flat on the day at 9.6906, having dropped sharply on Thursday following the ECB decision - Dow Jones.

-

12:50

USD/JPY rises to 10-month high above 115

-

11:29

ECB announcements on Thursday support a steeper yield curve - PIMCO

The European Central Bank's announcements on Thursday support a steeper yield curve, says Andrew Bosomworth, Pimco managing director and head of German portfolio management, cited by Dow Jones. He points to the increase in the number of bonds at the front end of the yield curve which are eligible for the asset purchase program, coupled with some national central banks' revealed preference to buy shorter-maturity bonds. The ECB altered its program so that it can buy bonds down to one year of residual maturity, reducing the previous lower bound of two years.

-

11:15

UBS Expects ECB to Start Tapering in Jan 2018

-

10:03

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0500 (EUR 2,03bln) 1.0575 (715m) 1.0600 (3.42bln) 1.0625 (1.36bln) 1.0650 (2.61bln) 1.0700 (1.7bln) 1.0750 (2.46bln) 1.0800 (2.89bln) 1.0850 (1.24bln)

USD/JPY 112.25 (USD 800m) 113,75 (505m) 114,.00 (407m) 114.50 (786m)

GBP/USD 1.2300 (USD 398m) 1.2500 (453m)

AUD/USD 0.7300 (2.02bln) 0.7325 (669m) 0.7400 (419m) 0,7500 (952m)

USD/CAD 1.3200 (USD 1.37bln)

Информационно-аналитический отдел TeleTrade

-

09:41

Bank of England inflation survey: respondents estimate inflation at 2.3%, compared to 1.8% in August

-

Median expectations of the rate of inflation over the coming year were 2.8%, compared with 2.2% in August.

-

Asked about expected inflation in the twelve months after that, respondents gave a median answer of 2.5%, compared with 2.2% in August.

-

Asked about expectations of inflation in the longer term, say in five years' time, respondents gave a median answer of 3.1%, compared to 3.0% in August.

-

By a margin of 50% to 10%, survey respondents believed that the economy would end up weaker rather than stronger if prices started to rise faster, compared with 44% to 10% in August.

-

-

09:39

UK construction output decreased by 0.6%

In October 2016, construction output was estimated to have decreased by 0.6% compared with September 2016. All new work decreased by 0.9%, with the largest downward contribution coming from infrastructure, while all repair and maintenance showed no growth.

Compared with October 2015, construction output increased by 0.7%. All new work increased by 2.9% with repair and maintenance falling by 3.2%. Within all new work total new housing was the biggest upwards contribution with an increase of 12.6%.

New orders for the construction industry in Quarter 3 2016 were estimated to have decreased by 2.4% compared with Quarter 2 (Apr to June) 2016. Public other new work fell by 24.8% while infrastructure increased by 22.4%.

-

09:37

UK trade deficit declined in October

The UK's deficit on trade in goods and services was estimated to have been £2.0 billion in October 2016, a narrowing of £3.8 billion from September 2016. Exports increased by £2.0 billion and imports decreased by £1.8 billion.

The deficit on trade in goods was £9.7 billion in October 2016, narrowing by £4.1 billion from September 2016. This narrowing reflected a £2.1 billion increase in exports to £26.8 billion and a £2.0 billion decrease in imports to £36.5 billion.

Between the 3 months to July 2016 and the 3 months to October 2016, the total trade deficit for goods and services widened by £4.7 billion to £13.2 billion.

Between the 3 months to July 2016 and the 3 months to October 2016, the deficit on trade in goods widened by £6.2 billion to £37.0 billion. Exports increased by £1.6 billion (2.0%) and imports increased by £7.7 billion (7.3%).

-

09:31

United Kingdom: Total Trade Balance, October -1.97

-

09:12

Where to target AUD? - Credit Suisse

"We noted in a previous update that although the post-Trumpian world of a stronger USD, bond yields and inflation expectations were taking AUDUSD to our forecast levels, the local picture looked mixed. In Australia, the balance of domestic risks since then has tilted decidedly to the downside.

Given prospects of further deterioration in the data, relatively sanguine pricing of RBA expectations, and a constrained fiscal policy, we downgrade our AUD forecasts vs. both the USD and NZD accordingly.

We revise our AUDUSD forecast lower to 0.72 in 3m and 0.70 in 12m.

We also revise our AUDNZD forecast lower to 1.011 in both 3m and 12m, keeping our NZDUSD forecasts unchanged".

Copyright © 2016 Credit Suisse, eFXnews™

-

08:49

Today’s events

-

At 15:15 GMT the ECB board member Benoit Coeure will deliver a speech

-

At 18:00 GMT drilling rigs operating at Baker Hughes data

-

-

07:51

French industrial production down 0.2% in October

In October 2016, output diminished again in the manufacturing industry (−0.6% after −1.4%). It decreased slightly in the whole industry (−0.2% after −1.4%).

Manufacturing output increased over the past three months (+0.8%)

Over the past three months, output grew in the manufacturing industry (+0.8% q-o-q), as well as in the overall industry (+0.7% q-o-q).

Output increased in all branches. It rose markedly in the manufacture of machinery and equipment goods (+2.5%) and in the manufacture of food products and beverages (+1.5%), and rebounded in the manufacture of coke and refined petroleum products (+18.5%). It went up slightly in mining and quarrying; energy; water supply (+0.5%). Finally, it was virtually stable in "other manufacturing" (+0.1%) and stable in the manufacture of transport equipment.

Over the year, output decreased sharply in mining and quarrying; energy; water supply (−2.5%), in the manufacture of food products and beverages (−1.7%) and in the manufacture of machinery and equipment goods (−1.5%). It diminished slightly in "other manufacturing" (−0.2%). Conversely, it increased in the manufacture of transport equipment (+0.9%) and, more moderately, in the manufacture of coke and refined petroleum products (+0.3%).

-

07:45

France: Industrial Production, m/m, October -0.2% (forecast 0.6%)

-

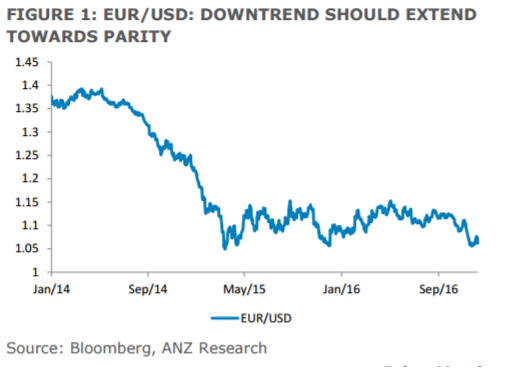

07:33

Stay short EUR/USD and sell rallies after ECB says ANZ

"The ECB delivered a bazooka. It extended QE (by €540bn), allowed the purchase of bonds with a minimum one year maturity and the purchase of bonds with yields below the deposit rate (-40bps).

The euro fell and the forthcoming political cycle suggests portfolio outflows from the euro area will continue. Further EUR underperformance vs. USD, AUD, NZD and Asia is expected.

Our forecasts assume that EUR/USD will move towards parity in coming months. If anything, the December ECB policy meeting reinforces that view. And whilst the ECB has mapped out its policy landscape for 2017, there are still material event risks facing the euro area. The elections in the Netherlands in March, elections in France -presidential election in April/May and Assembly election in June - and general election in Germany in September take place against a backdrop of rising support for populist parties. An election in Italy can't be completely discounted either. There is also the issue of bad debts in the banking system, in particular Italy, which needs to be addressed.

Against a backdrop where the FOMC will be raising interest rates we advise staying short EUR/USD and selling rallies".

Copyright © 2016 ANZ, eFXnews™

-

07:25

Options levels on friday, December 9, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.0752 (5985)

$1.0704 (4430)

$1.0663 (2346)

Price at time of writing this review: $1.0622

Support levels (open interest**, contracts):

$1.0580 (4500)

$1.0542 (2604)

$1.0500 (5913)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 92464 contracts, with the maximum number of contracts with strike price $1,1400 (6406);

- Overall open interest on the PUT options with the expiration date December, 9 is 74247 contracts, with the maximum number of contracts with strike price $1,0500 (5913);

- The ratio of PUT/CALL was 0.80 versus 0.84 from the previous trading day according to data from December, 8

GBP/USD

Resistance levels (open interest**, contracts)

$1.2900 (697)

$1.2800 (1756)

$1.2700 (1873)

Price at time of writing this review: $1.2583

Support levels (open interest**, contracts):

$1.2500 (2566)

$1.2400 (1550)

$1.2300 (2186)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 35981 contracts, with the maximum number of contracts with strike price $1,3400 (2561);

- Overall open interest on the PUT options with the expiration date December, 9 is 36577 contracts, with the maximum number of contracts with strike price $1,2500 (2566);

- The ratio of PUT/CALL was 1.02 versus 1.00 from the previous trading day according to data from December, 8

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:22

China's inflation rose more than expected. AUD/USD traded higher

China's factory gate inflation increased to a more than five-year high in November on higher commodity prices and consumer price inflation exceeded expectations due to rising food costs.

Producer price inflation accelerated notably to 3.3 percent in November from 1.2 percent in the previous month, the National Bureau of Statistics showed Friday. Inflation was expected to rise to 2.3 percent.

Consumer price inflation rose to 2.3 percent in November from 2.1 percent in October. A similar high rate was last seen in April. The pace also exceeded the expected 2.2 percent.

Nonetheless, the figure continues to remain below the government's full-year target of 3 percent, says rttnews.

-

07:16

Australian housing market improves

The trend estimate for the total value of dwelling finance commitments excluding alterations and additions rose 0.3%. Investment housing commitments rose 1.5%, while owner occupied housing commitments fell 0.5%.

In seasonally adjusted terms, the total value of dwelling finance commitments, excluding alterations and additions fell 0.2%.

In trend terms, the number of commitments for owner occupied housing finance fell 0.9% in October 2016.

In trend terms, the number of commitments for the purchase of established dwellings fell 1.0%, the number of commitments for the construction of dwellings fell 0.7%, and the number of commitments for the purchase of new dwellings fell 0.3%.

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 13.7% in October 2016, from 13.1% in September 2016. This rise was driven by a fall in the number of non-first home buyer commitments; the number of first home buyer commitments fell slightly.

-

07:10

Swiss unemplyment rate rose in November

According to the State Secretariat of Economic Affairs (SECO) surveys, 149,228 unemployed were registered at the Regional Employment Services Centers (RAV) at the end of November 2016, 4,697 more than in the previous month.

The unemployment rate thus rose from 3.2% in October 2016 to 3.3% in the reporting month. Compared to the previous month, unemployment increased by 1,085 persons (+ 0.7%). Youth unemployment in November 2016 Youth unemployment (15 to 24 year olds) decreased by 174 persons (-0.9%) to 18'921. Compared to the previous year, this corresponds to a decrease of 1,133 persons.

-

07:04

German trade balance surplus declined slightly

Germany exported goods to the value of 101.5 billion euros and imported goods to the value of 82.2 billion euros in October 2016. Based on provisional data, the Federal Statistical Office (Destatis) also reports that German exports decreased by 4.1% in October 2016 year on year while imports were down by 2.2%. After calendar and seasonal adjustment, exports increased by 0.5% and imports by 1.3% compared with September 2016.

The foreign trade balance showed a surplus of 19.3 billion euros in October 2016. In October 2015, the surplus amounted to 21.7 billion euros. In calendar and seasonally adjusted terms, the foreign trade balance recorded a surplus of 20.5 billion euros in October 2016.

According to provisional results of the Deutsche Bundesbank, the current account of the balance of payments showed a surplus of 18.4 billion euros in October 2016, which takes into account the balances of trade in goods including supplementary trade items (+20.2 billion euros), services (-3.5 billion euros), primary income (+5.5 billion euros) and secondary income (-3.8 billion euros). In October 2015, the German current account showed a surplus of 21.7 billion euros.

-

07:01

Germany: Trade Balance (non s.a.), bln, October 19.3

-

07:01

Germany: Current Account , October 18.4

-

06:45

Switzerland: Unemployment Rate (non s.a.), November 3.3%

-

01:31

China: PPI y/y, November 3.3% (forecast 2.2%)

-

01:30

China: CPI y/y, November 2.3% (forecast 2.2%)

-

00:30

Australia: Home Loans , October -0.8% (forecast -1%)

-