Market news

-

15:38

Trump administration considers mobilizing as many as 100,000 National Guard troops to round up unauthorized immigrants - AP

-

15:14

US Conference Board leading index rose more than expected in January

The Conference Board Leading Economic Index for theU.S. increased 0.6 percent in January to 125.5 (2010 = 100), following a 0.5 percent increase in December, and a 0.2 percent increase in November.

"The U.S. Leading Economic Index increased sharply again in January, pointing to a positive economic outlook in the first half of this year," said Ataman Ozyildirim, Director of Business Cycles and Growth Research at The Conference Board. "The January gain was broad based among the leading indicators. If this trend continues, the U.S. economy may even accelerate in the near term."

-

15:00

U.S.: Leading Indicators , January 0.6% (forecast 0.5%)

-

14:37

Morgan Stanley recommends selling EUR/GBP, entering the trade at 0.8650, with a target of 0.800 and a stop at 0.8800

-

13:49

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.0600-05 (EUR 693m) 1.0650 (955m) 1.0700 (887m) 1.0780 (1.33bln) 1.0950 (880m)

USD/JPY: 112.00 (USD 607m) 112.50 (350m) 114.00 (670m) 115.00 (465m)

GBP/USD: 1.2565-70 (GBP 437m) 1.2600 (469m)

AUD/USD: 0.7400 (AUD 571m)

USD/CAD 1.2975 (USD 485m)

-

13:33

Foreign investment in Canadian securities reached $10.2 billion in December

Foreign investment in Canadian securities reached $10.2 billion in December, largely through acquisitions of shares. At the same time, Canadian investors increased their holdings of foreign securities by $6.7 billion, led by purchases of non-US foreign shares.

As a result, international transactions in securities generated a net inflow of funds of $3.6 billion into the Canadian economy in December and a record $147.5 billion for 2016 as a whole. Moreover, foreign investment in Canadian securities has exceeded Canadian investment in foreign securities by $634.4 billion since 2009, following the global financial crisis.

-

13:30

Canada: Foreign Securities Purchases, December 10.23

-

13:01

Orders

EUR/USD

Offers: 1.0680 1.0700-05 1.0730 1.0750 1.0780 1.0800

Bids: 1.0630 1.0600 1.0585 1.0550 1.0520 1.0500

GBP/USD

Offers: 1.2500 1.2520 1.2550 1.2580 1.2600 1.2630 1.2350 1.2680 1.2700

Bids: 1.2475 1.2460 1.2450 1.2430 1.2400 1.2380 1.2345-50 1.2300

EUR/GBP

Offers: 0.8550-55 0.8585 0.8600 0.8620 0.8650

Bids: 0.8500 0.8480-85 0.8450 0.8430 0.8400

EUR/JPY

Offers: 120.80 121.00 121.35 121.50 121.80 122.00

Bids: 102.30 120.00 119.75 119.50 119.00

USD/JPY

Offers: 113.50 113.80-85 114.00-05 114.20 114.35 114.50

Bids: 113.15 113.00 112.80 112.50 112.30 112.00

AUD/USD

Offers: 0.7720 0.7735 0.7750 0.7780 0.7800 0.7820 0.7850

Bids: 0.7680 0.7660 0.7620 0.7600 0.7580 0.7550

-

11:14

ECB, Lane: taper decision is data dependent, not calendar dependent

-

See Firms Scattering Staff Due to Brexit

-

Monetary Policy Will Return Inflation to Target

-

No Reason Now to Turn Off Policy Accommodation

-

Don't Expect 'Steady Surge' in Inflation

-

QE Program Is 'Open Ended'

-

Don't Expect to Have to Cut Deposit Rate Again

-

-

10:36

Despite the long delays by the Democrats in finally approving Dr. Tom Price, the repeal and replacement of ObamaCare is moving fast! @realDonaldTrump

-

10:05

Danske Bank expect AUD/USD to back down from overbought levels over the next one-three months

"AUD/USD has reversed the move after US elections, which pushed the pair as low as below 0.72 around year end. The lack of details of the US administration's economic plans has weighed on USD and supported AUD in January-February. Furthermore, improvement in Australian economic data together with a more optimistic tone from the central bank has helped AUD to return to pre-Trump levels. We recognise the support for AUD from improved global economic conditions and rising commodity prices. However, we still think the RBA wants to limit the upside in AUD and is ready to soften its tone in case the exchange rate appreciates excessively. Moreover, as the market could well price in more aggressive action by the Fed, we see relative monetary policies supporting USD versus AUD in coming months.

We expect AUD/USD to back down from overbought levels over the next one-three months.

We make a level shift to our forecast reflecting the latest moves but keep the profile unchanged, expecting short-term weakness and longer-term stabilisation in AUD.

Our 1M forecast is 0.75, 3M forecast 0.73 and 6-12M forecasts 0.74 and 0.75, respectively".

Copyright © 2017 Danske, eFXnews™

-

09:33

UK retail sales down 0.3% in January. GBP/USD dropped 50 pips instantly

In January 2017, the quantity bought in the retail industry is estimated to have increased by 1.5% compared with January 2016, the lowest growth since November 2013.

Month-on-month the quantity bought is estimated to have fallen by 0.3%.

The underlying pattern as suggested by the 3 month on 3 month movement decreased by 0.4%; the first fall since December 2013.

Average store prices (including fuel) increased by 1.9% on the year, the largest contribution to this increase came from petrol stations, where year-on-year average prices were estimated to have risen by 16.1%.

Online sales (excluding fuel) increased by 10.1% year-on-year, but fell on the month by 7.2%; accounting for approximately 14.6% of all retail spending.

-

09:30

United Kingdom: Retail Sales (MoM), January -0.3% (forecast 0.9%)

-

09:30

United Kingdom: Retail Sales (YoY) , January 1.5% (forecast 3.4%)

-

09:04

The current account of the euro area recorded a surplus of €31.0 billion in December 2016.

This reflected surpluses for goods (€31.7 billion), primary income (€5.3 billion) and services (€4.6 billion), which were partly offset by a deficit for secondary income (€10.6 billion).

According to the preliminary results for 2016 as a whole, the current account recorded a surplus of €364.7 billion (3.4% of euro area GDP), compared with one of €319.3 billion (3.1% of euro area GDP) in 2015. All the components of the current account increased. There were increases in the surpluses for goods (from €348.2 billion to €372.2 billion), services (from €58.9 billion to €69.1 billion) and primary income (from €42.1 billion to €52.4 billion), as well as a slight decrease in the deficit for secondary income (from €129.9 billion to €129.0 billion).

-

09:00

Eurozone: Current account, unadjusted, bln , December 47

-

08:15

Japan PM Abe: Trump's FX Comments Are Related To China, Not To Japan - Livesquawk

-

07:55

Chinese Banks sold net $19.2 bln of foreign exchange in Jannuary vs $46.3 bln in December

-

07:30

Options levels on friday, February 17, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0819 (4868)

$1.0753 (3360)

$1.0705 (3070)

Price at time of writing this review: $1.0663

Support levels (open interest**, contracts):

$1.0632 (3336)

$1.0570 (5202)

$1.0488 (5792)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 70453 contracts, with the maximum number of contracts with strike price $1,0800 (4868);

- Overall open interest on the PUT options with the expiration date March, 13 is 83728 contracts, with the maximum number of contracts with strike price $1,0500 (5792);

- The ratio of PUT/CALL was 1.19 versus 1.19 from the previous trading day according to data from February, 16

GBP/USD

Resistance levels (open interest**, contracts)

$1.2702 (2337)

$1.2604 (2338)

$1.2509 (3529)

Price at time of writing this review: $1.2485

Support levels (open interest**, contracts):

$1.2395 (1921)

$1.2298 (3759)

$1.2199 (1620)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 33984 contracts, with the maximum number of contracts with strike price $1,2500 (3529);

- Overall open interest on the PUT options with the expiration date March, 13 is 37582 contracts, with the maximum number of contracts with strike price $1,2300 (3759);

- The ratio of PUT/CALL was 1.11 versus 1.12 from the previous trading day according to data from February, 16

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:06

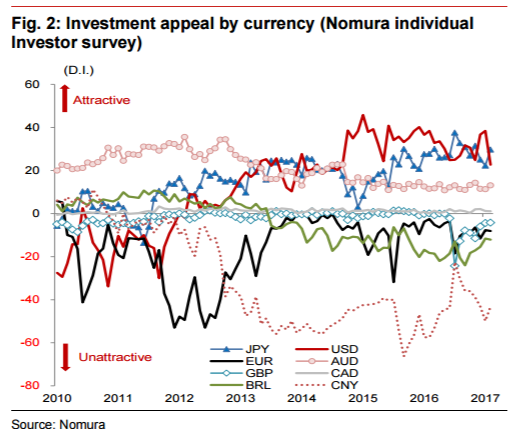

Retail investors’ views on the Japanese equity market have weakened slightly - Nomura. USD/JPY dip demand weak

"Retail investors' views on the Japanese equity market have weakened slightly, according to the latest Nomura Individual Investor Survey (6-7 February).

.....More investors see downside risks for USD/JPY than last month too. 63.9% of investors expect USD/JPY to fall over the next three months, while 53.0% expected a fall the previous month.

They do not necessarily expect a significant decline in USD/JPY, while most retail investors expected around 5 point fall in USD/JPY.

The reference level was lower at 112.45 than the 115.60 in the previous month, but the survey result showed weaker demand for dip-buying for now".

Copyright © 2017 Nomura, eFXnews™

-

07:00

Japanese Finance Minister Taro Aso to start economic dialogue with the US

During his speech today the Minister of Finance of Japan, Taro Aso announced its readiness to launch an economic dialogue with the US in April. "We will focus on economic policy, infrastructure, energy projects and trade".

-

06:58

UK Prime Minister May said to plan Brexit trigger close to March 9-10 EU Summit

-

06:57

Eleven of the 15 New Zeeland industries had higher sales volumes this quarter

Car sales continued to push the volume of total retail trade sales up, with sales rising 1.9 percent in the December 2016 quarter, Statistics NZ said today.

Motor-vehicles sales led most of the quarterly industry movements over 2016.

"More expensive cars and SUV vehicles are selling well, especially in Auckland, according to comments from car dealers and industry experts," business indicators manager Tehseen Islam said.

"Some of the increase in car sales may reflect a growing population, with net migration at record levels in 2016."

After adjusting for seasonal effects, total retail sales volumes rose 0.8 percent in the latest quarter. This follows a similar 0.8 percent rise in September, and a stronger 2.2 percent rise in the June 2016 quarter.

Eleven of the 15 industries had higher sales volumes this quarter, with the largest increases in:

-

motor-vehicle and parts retailing - up 1.9 percent

-

pharmaceutical and other store-based retailing - up 2.5 percent

-

accommodation - up 3.5 percent

-

electrical and electronic goods - up 2.0 percent.

-

-