Market news

-

20:00

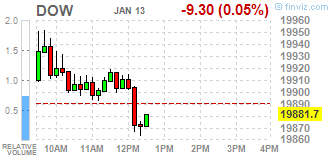

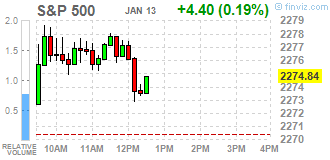

DJIA 19881.47 -9.53 -0.05%, NASDAQ 5574.12 26.63 0.48%, S&P 500 2274.51 4.07 0.18%

-

17:39

Wall Street. Major U.S. stock-indexes mixed

Major U.S. stock-indexes mixed on Friday as strong earnings from large U.S. lenders bode well for the rest of the earnings season. The Dow's gains were comparatively lesser, held back by a drop in consumer stocks after a report showed U.S. retail sales and core retail sales increased less than expected in December. Trading volumes were light ahead of a three-day weekend.

Most of Dow stocks in negative area (18 of 30). Top gainer - Merck & Co., Inc. (MRK, +0.48%). Top loser - E. I. du Pont de Nemours and Company (DD, -0.92%).

Most of S&P sectors in positive area. Top loser - Healthcare (+0.6%). Top gainer - Conglomerates (-0.7%).

At the moment:

Dow 19791.00 -12.00 -0.06%

S&P 500 2268.50 +5.00 +0.22%

Nasdaq 100 5054.25 +19.50 +0.39%

Oil 52.59 -0.42 -0.79%

Gold 1196.70 -3.10 -0.26%

U.S. 10yr 2.41 +0.04

-

17:00

European stocks closed: FTSE 7337.81 45.44 0.62%, DAX 11629.18 108.14 0.94%, CAC 4922.49 58.52 1.20%

-

16:43

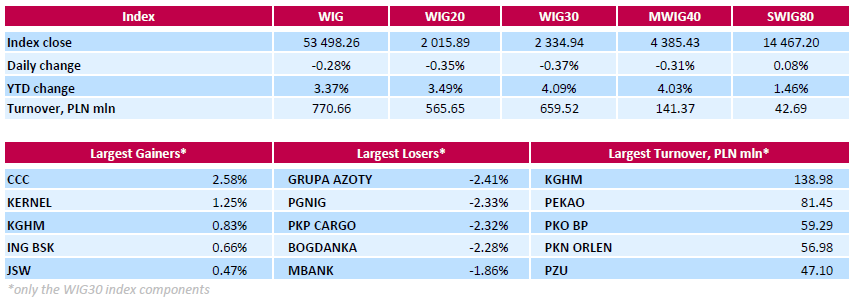

WSE: Session Results

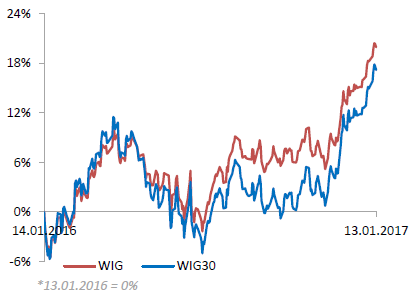

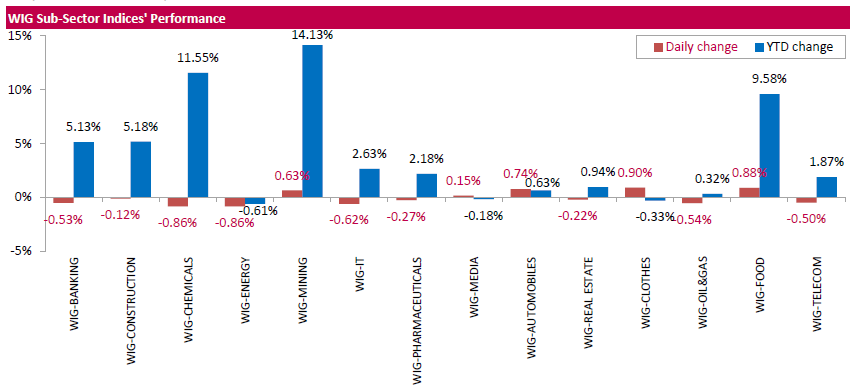

Polish equity market closed lower on Friday. The broad market measure, the WIG index, fell by 0.28%. Most sectors dropped, with chemicals (-0.86%) and energy (-0.86%) underperforming.

The large-cap stocks' gauge, the WIG30 Index, sank by 0.37%. 2/3 of the index components recorded declines. Chemical company GRUPA AZOTY (WSE: ATT) suffered the biggest daily drop, tumbling by 2.41% after significant gains earlier this week. Other largest losers were oil and gas producer PGNIG (WSE: PGN), railway freight transport operator PKP CARGO (WSE: PKP) and thermal coal miner BOGDANKA (WSE: LWB), falling 2.33%, 2.32% and 2.28% respectively. At the same time, footwear retailer CCC (WSE: CCC) and agricultural producer KERNEL (WSE: KER) led a handful of gainers, adding 2.58% and 1.25% respectively. The latter published Q2 operational update, which reviled that the company increased its grain sales by 15% y/y, sunflower oil sales in bulk by 13% y/y and bottled oil sales by almost 17% y/y.

-

15:35

-

15:06

US consumer confidence remained unchanged in January

Consumer confidence remained unchanged at the cyclical peak levels recorded in December. The Current Conditions Index rose 0.6 points to reach its highest level since 2004, and the Expectations Index fell 0.6 points which was lower than only the 2015 peak during the past dozen years. The post-election surge in optimism was accompanied by an unprecedented degree of both positive and negative concerns about the incoming administration spontaneously mentioned when asked about economic news. The importance of government policies and partisanship has sharply risen over the past half century.

-

15:05

US business inventories rose more than expected

The combined value of distributive trade sales and manufacturers' shipments for November, adjusted for seasonal and trading-day differences but not for price changes, was estimated at $1,326.7 billion, up 0.1 percent from October 2016 and was up 2.3 percent from November 2015.

Inventories Manufacturers' and trade inventories, adjusted for seasonal variations but not for price changes, were estimated at an end-of-month level of $1,827.5 billion, up 0.7 percent from October 2016 and were up 1.5 percent (±0.4 percent) from November 2015

-

15:00

U.S.: Business inventories , November 0.7% (forecast 0.5%)

-

15:00

U.S.: Reuters/Michigan Consumer Sentiment Index, January 98.1 (forecast 98.5)

-

14:54

WSE: After start on Wall Street

The market on Wall Street took off with optimism, the first transactions surprise positively and the S&P500 index is rising by more than 0.3 percent. This favorable situation has been noticed in Europe. However on the Warsaw Stock Exchange any reaction is not seen. Clearly weaker today the WIG20 seems to be sentenced for decline at the end of the day. But we have to keep in mind the low turnover, which reduces the credibility of discounts.

An hour before the close of trading the WIG20 index was at the level of 2,014 points (-0,43%).

-

14:38

The dollar strengthened against other major currencies, supported by strong data on producer prices, which offset the negative impact of the retail sales report. Currently EUR / USD traded at $ 1.0623. Strong support - $ 1.0545 (MA 200 H1)

The dynamics of the US bond market also contributes to the strengthening of the dollar. At present, the yield of 10-year US bonds is 2.39%. Earlier today, the yield dropped to 2.34%.

-

14:34

U.S. Stocks open: Dow +0.17%, Nasdaq +0.24%, S&P +0.19%

-

14:27

Before the bell: S&P futures +0.11%, NASDAQ futures +0.13%

U.S. stock-index futures edged up as investors assessed Q4 earnings reports released by the U.S. largest banks and data on retail sales and PPI for December.

Global Stocks:

Nikkei 19,287.28 +152.58 +0.80%

Hang Seng 22,937.38 +108.36 +0.47%

Shanghai 3,112.33 -6.96 -0.22%

FTSE 7,324.27 +31.90 +0.44%

CAC 4,909.77 +45.80 +0.94%

DAX 11,592.21 +71.17 +0.62%

Crude $52.67 (-0.64%)

Gold $1,198.30 (-0.13%)

-

13:57

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

32.99

-0.05(-0.1513%)

6895

Amazon.com Inc., NASDAQ

AMZN

814.24

0.60(0.0737%)

19174

American Express Co

AXP

77

0.12(0.1561%)

500

Apple Inc.

AAPL

119.18

-0.07(-0.0587%)

43520

AT&T Inc

T

40.97

-0.04(-0.0975%)

6141

Barrick Gold Corporation, NYSE

ABX

16.97

0.08(0.4736%)

24751

Boeing Co

BA

159

0.71(0.4485%)

7473

Caterpillar Inc

CAT

94

0.01(0.0106%)

623

Chevron Corp

CVX

116.01

-0.15(-0.1291%)

425

Cisco Systems Inc

CSCO

30.13

0.09(0.2996%)

513

Citigroup Inc., NYSE

C

59.05

-0.18(-0.3039%)

52505

E. I. du Pont de Nemours and Co

DD

73.95

-0.16(-0.2159%)

100

Exxon Mobil Corp

XOM

86.35

0.01(0.0116%)

10998

Facebook, Inc.

FB

127.49

0.87(0.6871%)

211181

Ford Motor Co.

F

12.61

0.02(0.1589%)

18588

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

15.3

0.03(0.1965%)

64513

General Electric Co

GE

31.36

-0.03(-0.0956%)

3760

Goldman Sachs

GS

242.88

-0.96(-0.3937%)

20395

Google Inc.

GOOG

808

1.64(0.2034%)

1554

International Business Machines Co...

IBM

167.5

-0.45(-0.2679%)

1714

JPMorgan Chase and Co

JPM

86.3

0.06(0.0696%)

618492

Merck & Co Inc

MRK

62.36

0.15(0.2411%)

2660

Microsoft Corp

MSFT

62.7

0.09(0.1437%)

10499

Procter & Gamble Co

PG

84

0.16(0.1908%)

1856

Tesla Motors, Inc., NASDAQ

TSLA

230.14

0.55(0.2396%)

6428

The Coca-Cola Co

KO

41

0.05(0.1221%)

299

Twitter, Inc., NYSE

TWTR

17.4

0.02(0.1151%)

4461

Verizon Communications Inc

VZ

52.96

0.28(0.5315%)

154

Walt Disney Co

DIS

107.35

-0.18(-0.1674%)

1056

Yahoo! Inc., NASDAQ

YHOO

42.18

0.07(0.1662%)

1602

-

13:55

Upgrades and downgrades before the market open

Upgrades:

Facebook (FB) upgraded to Strong Buy from Outperform at Raymond James; target $160

Downgrades:

Credit Suisse (CS) downgraded to Underperform from Neutral at Macquarie

Other:

Merck (MRK) initiated with a Buy at Bryan Garnier

-

13:47

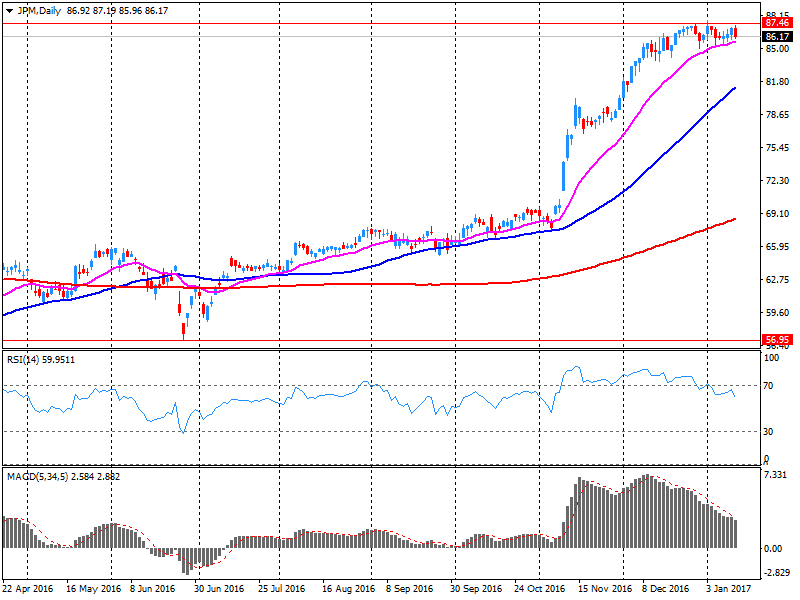

Company News: JPMorgan Chase (JPM) Q4 EPS beat analysts’ estimate

JPMorgan Chase reported Q4 FY 2016 earnings of $1.71 per share (versus $1.32 in Q4 FY 2015), beating analysts' consensus estimate of $1.43.

The company's quarterly revenues amounted to $23.376 bln (+2.1% y/y), generally in-line with analysts' consensus estimate of $23.476 bln.

JPM rose to $86.55 (+0.36%) in pre-market trading.

-

13:45

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0500 (EUR 2,790 M) 1.0550 (EUR 1,473 M) 1.0570-1.0575 (EUR 434 M) 1.0600 (EUR 3,755 M) 1.0615-1.0620 (EUR 198 M) 1.0630-1.0635 (EUR 738 M) 1.0650-1.0665 (EUR 686 M) 1.0695-1.0705 (EUR 1,357 M) 1.0750-1.0765 (EUR 1,206 M)

GBP/USD 1.2000 (GBP 619 M) 1.2180 (GBP 482 M) 1.2200 (GBP 496 M) 1.2295-1.2305 (GBP 905 M)

USD/JPY 113.50 (USD 1,220 M) 113.75 (USD 320 M) 114.00-114.10 (USD 342 M) 114.50 (USD 856 M) 114.75-114.90 (USD 398 M) 115.00 (USD 1,830 M) 115.10-115.17 (USD 270 M) 115.35-115.50 (USD 1,093 M) 116.00 (USD 1,762 M) 116.10-116.25 (USD 2,020 M)

EUR/JPY 122.00 (EUR 221 M) 122.42-122.55 (EUR 517 M)

USD/CHF 1.0115-1.0120 (USD 255 M)

AUD/USD 0.7300 (AUD 1,199 M) 0.7340-0.7350 (AUD 390 M) 0.7375-0.7380 (AUD 192 M) 0.7400-0.7415 (AUD 250 M) 0.7420-0.7425 (AUD 369 M) 0.7480-0.7495 (AUD 301 M) 0.7500-0.7505 (AUD 265 M) 0.7535-0.7550 (AUD 399 M) 0.7600-0.7610 (AUD 1,119 M)

USD/CAD 1.3095-1.3105 (USD 766 M) 1.3150-1.3155 (USD 626 M) 1.3230 (USD 213 M) 1.3300 (USD 2,302 M)

NZD/USD 0.7040-0.7050 (NZD 196 M)

-

13:39

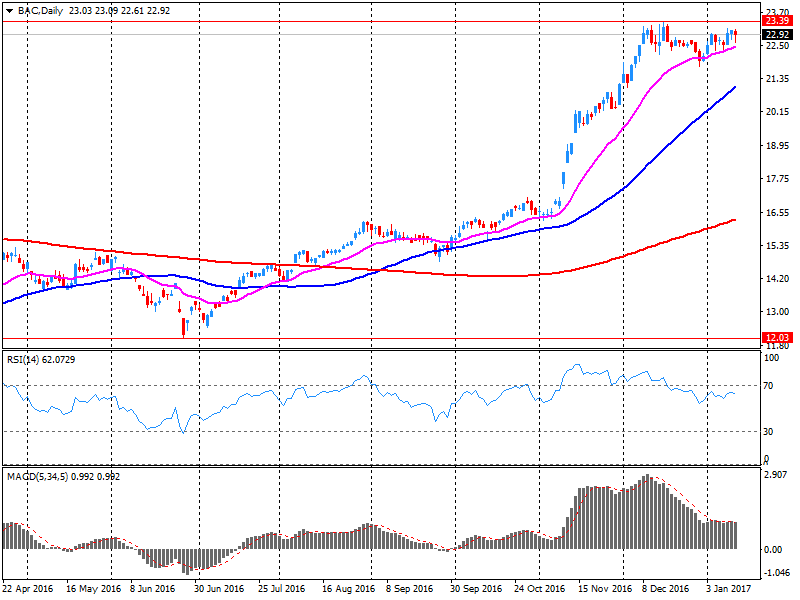

Company News: Bank of America (BAC) posts mixed quarterly results

Bank of America reported Q4 FY 2016 earnings of $0.40 per share (versus $0.28 in Q4 FY 2015), beating analysts' consensus estimate of $0.38.

The company's quarterly revenues amounted to $19.990 bln (+2.1% y/y), missing analysts' consensus estimate of $21.058 bln.

Bank of America also increased planned share repuchases for 1H17 by $1.8 bln to $4.3 bln.

BAC fell to $22.74 (-0.79%) in pre-market trading.

-

13:38

US Producer Price Index for final demand increased 0.3 percent in December

The Producer Price Index for final demand increased 0.3 percent in December, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices advanced 0.4 percent in November and were unchanged in October. On an unadjusted basis, the final demand index climbed 1.6 percent in 2016 after falling 1.1 percent in 2015.

In December, nearly 80 percent of the advance in the final demand index is attributable to a 0.7 percent increase in prices for final demand goods. The index for final demand services inched up 0.1 percent.

-

13:34

US retail sales in line with expectations in December

Advance estimates of U.S. retail and food services sales for December 2016, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $469.1 billion, an increase of 0.6 percent from the previous month, and 4.1 percent (±0.9 percent) above December 2015.

Total sales for the 12 months of 2016 were up 3.3 percent from 2015. Total sales for the October 2016 through December 2016 period were up 4.1 percent from the same period a year ago. The October 2016 to November 2016 percent change was revised from up 0.1 percent (±0.5 percent)* to up 0.2 percent.

Retail trade sales were up 0.8 percent (±0.5 percent) from November 2016, and up 4.3 percent (±0.7 percent) from last year. Nonstore retailers were up 13.2 percent (±1.8 percent) from December 2015, while Miscellaneous stores were up 7.1 percent (±4.6 percent) from last year.

-

13:30

U.S.: PPI excluding food and energy, Y/Y, December 1.6% (forecast 1.5%)

-

13:30

U.S.: Retail sales excluding auto, December 0.2% (forecast 0.5%)

-

13:30

U.S.: Retail sales, December 0.6% (forecast 0.7%)

-

13:30

U.S.: PPI excluding food and energy, m/m, December 0.2% (forecast 0.1%)

-

13:30

U.S.: Retail Sales YoY, December 4.1%

-

13:30

U.S.: PPI, m/m, December 0.3% (forecast 0.3%)

-

13:30

U.S.: PPI, y/y, December 1.6% (forecast 1.6%)

-

13:14

The pound depreciated significantly against the dollar, returning to the opening level, which was due to profit-taking in anticipation of the US data release and corrections before the weekend

Now the pair is trading at $ 1.2179. The nearest support - $ 1.2100.

-

13:00

Orders

EUR/USD

Offers 1.0650 1.0680 1.0700 1.0725-30 1.0750 1.0785 1.0800

Bids 1.0620 1.0600 1.0580 1.0550 1.0520 1.0500 1.0480 1.0450

GBP/USD

Offers 1.2200 1.2225-30 1.2250 1.2280 1.2300 1.2320-25 1.2360 1.2380 1.2400

Bids 1.2150 1.2125-30 1.2100 1.2080 1.20550 1.2030 1.2000

EUR/GBP

Offers 0.8750 0.8780 0.8800 0.8830 0.8850

Bids 0.8700 0.8685 0.8665 0.8650 0.8620 0.8600

EUR/JPY

Offers 122.30 122.50 122.85 123.00 123.30 123.60 123.85 124.00

Bids 121.50 121.20 121.00 120.80 120.50 120.00

USD/JPY

Offers 114.80 115.00 115.20 115.50 115.80 116.00 116.20-25 116.50

Bids 114.50 114.20 114.00 113.80 113.50 113.20-25 113.00 112.85 112.65 112.50

AUD/USD

Offers 0.7520 0.7550 0.7575 0.7600 0.7620 0.7650-60

Bids 0.7475-80 0.7450 0.7430 0.7400 0.7380 0.7350-55

-

12:05

WSE: Mid session comment

The morning part of the session on the Warsaw market was marked by growing correction's mood. The discount in the WIG20 index is limited be reduced level of turnover. Among major companies gain only shares of Pekao (WSE: PEO) and PKO. The fact that the Warsaw market falls the second day in a row should not be surprising after a strong approach up even only in January. Slowly investors begin to move in the direction of Wall Street and the banks' results.

At the halfway point of today's trading the WIG20 index was at the level of 2,013 points (-0,47%) and the turnover in the segment of blue chips was amounted to PLN 260 million.

-

11:52

Major European stock indices trading in the green zone

European stock indices show a moderately positive trend, aided by rise in price of shares of the automotive sector. In addition, investors analyze the latest statistical data from China and the start in the US corporate reporting season.

The data showed that exports from China fell sharply in December due to weak demand, which increased investors' anxiety about the state's second-largest economy in the world. General Customs Administration of China reported that the total volume of foreign trade in December fell by 6.8% per year, amounting to 3,684 billion dollars. The volume of China's exports in December alone totaled 209.4 billion dollars, down 6.1% compared to the same period last year. China's import volume in December was 168.6 billion dollars, a decline of 3.1% per annum. In addition, it was reported on the results of China's exports in 2016 decreased by 7.7%, imports decreased by 5.5% per annum. The volume of China's exports in 2016 amounted to 2.097 billion dollars, and imports US $ 1.587 trillion. The trade surplus for the end of 2016 amounted to 509.9 billion.

Investors are also preparing for the US report season, which starts today.

The composite index of the largest companies in the region Stoxx Europe 600 rose 0.6%, to the level of 364.68. Most sectors and stock exchanges are trading in positive territory.

Automotive segment rose by 0.59 percent despite news that US Environmental Protection Agency accused Fiat Chrysler Automobiles of installing software on cars, underestimating the figures on emissions of harmful substances. However, the automaker rejected these accusations. Currently, shares of Fiat Chrysler Automobiles show an increase of 3.6%.

Renault's capitalization fell by 2.4 percent after reports that the French authorities have launched an investigation against the company, suspecting of manipulation of car exhaust data.

Shares of the health sector are growing, recovering from the comments made earlier this week by US President that pharmaceutical companies "go with murder."

At the moment:

FTSE 100 +20.27 7312.64 + 0.28%

DAX +67.03 11588.07 + 0.58%

CAC 40 +43.61 4907.58 + 0.90%

-

10:33

Oil is trading moderately lower

This morning, the New York futures for Brent are down a modest 0.18% to $ 55.9 and WTI fell 0.13% to $ 52.94. Saudi Oil Minister said yesterday that they have reduced oil production by more than 486,000 barrels per day. Moreover, the minister said that the Saudis production is now less than 10 million barrels per day. Also, Iraq has cut production by 170,000 barrels per day and will soon cut another 210 thousand.

-

10:30

Greece's Cash Reserves Can Last Up To May, Says Eurobank

-

09:47

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0500 (EUR 2.42bln) 1.0600 (505m) 1.0700 (2.41bln) 1.0800 (281m) 1.0850 (690m)

USD/JPY 115.00 (USD 1.3bln) 116.00 (700m) 117.00 (420m) 117.25 (380m) 118.00 (839m)

USD/CAD 1.3245 (USD 300m) 1.3300 (1.26bln)

NZD/USD 0.7005 (NZD 173m)

Информационно-аналитический отдел TeleTrade

-

09:30

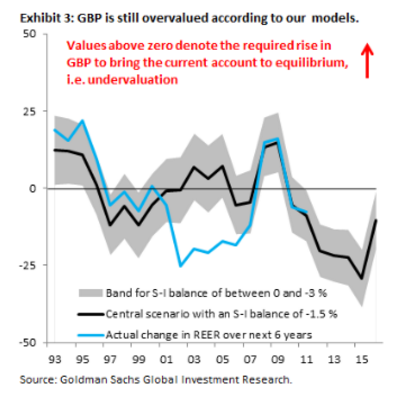

Goldman Sachs staying short GBP, more downside expected on Article 50

"We see the path for the British Pound as a function of two things.

First, there is the question of where GBP/$ would trade in the event of a "hard Brexit." We have used several approaches to show that Sterling could fall between 20-40 percent relative to pre-referendum levels, with a low of 1.10 for GBP/$ quite possible.

Second, what probability should markets assign to "hard Brexit." In our minds, it has been this probability that has been moving the Pound around since June of last year. In particular, the political vacuum following the referendum meant that there was some probability that Article 50 might never be triggered. In the presence of large speculative shorts, this kept the Pound supported after its initial referendum fall. But the Conservative party conference changed that, with Prime Minster May committing to trigger Article 50 by March. We thought the market would price a greater probability of "hard Brexit" as a result, reiterating our near-term target of 1.20 for Cable in the days ahead of the 'flash crash'. The November High Court decision was a move back in the opposite direction, reducing in the market's eyes the odds that Article 50 could be triggered by March and, more fundamentally, limiting how aggressive the government could be in its negotiating position. This buoyed Cable, pushing it back up towards 1.28 and pre-'flash crash' levels in mid-December (Exhibit 1). However, our underlying conviction is that Sterling needs to weaken quite a bit more, given that the trade-weighted decline is only 13 percent so far (Exhibit 2), well shy of our 20-40 percent range.

We think the most recent decline, sparked by Prime Minister May's latest speech re-affirming her Brexit vision, is the start of that process, with the FX market only beginning to re-engage in the idiosyncratic Sterling down story.

Our 3-, 6- and 12-month forecasts for GBP/$ now stand at 1.20, 1.18 and 1.14, respectively, with risks tilted in the direction of a sharper, more front-loaded decline. Our conviction for this forecast rests on the fact that the fall in GBP is still relatively small in trade-weighted terms, something that has been overlooked, while we also think the market continues to under-price Prime Minister May's commitment to trigger Article 50 by March. Taking into account that the Pound has fallen 13 percent from pre-Brexit vote levels, this is still well short of the upper bound of our range between 20-40 percent that we derive using various approaches (Exhibit 3).

We continue to think that - even with the decline since June - the Pound is not yet cheap and that more declines are coming. We remain short Sterling also in our Top Trade for 2017, where we are short GBP and EUR equally weighted against the Dollar".

Copyright © 2017 Goldman Sachs, eFXnews™

-

09:07

Major stock markets in Europe trading in the green zone: FTSE + 0.5%, DAX + 0.5%, CAC 40 + 0.6%, IBEX + 0.4%

-

08:30

Today’s events

-

At 09:30 GMT the Bank of England Member of the Commission Michael Saunders will make a speech

-

At 14:30 GMT FOMC member Patrick T. Harker will deliver a speech

-

-

08:28

Australian Dollar consolidates after strong weekly rally

-

08:18

WSE: After opening

WIG20 index opened at 2023.01 points (+0.00%)*

WIG 53707.82 0.11%

WIG30 2346.16 0.11%

mWIG40 4402.28 0.07%

*/ - change to previous close

The cash market started the day on a neutral levels and with moderate level of turnover. At the beginning of the session in European markets, as expected, it was considered better yesterday's ending in the US. The session - at least until the entrance Wall Street to the game - promises to be an extension of the two-day suspension. The theme for today is waiting for revisions of Polish rating by Moody's and Fitch agencies.

After fifteen minutes of trading the WIG20 index was at the level of 2,022 points (-0,04%).

-

07:21

Options levels on friday, January 13, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0739 (2214)

$1.0712 (442)

$1.0693 (254)

Price at time of writing this review: $1.0635

Support levels (open interest**, contracts):

$1.0566 (1201)

$1.0526 (1145)

$1.0475 (2385)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 53089 contracts, with the maximum number of contracts with strike price $1,1500 (3331);

- Overall open interest on the PUT options with the expiration date March, 13 is 62478 contracts, with the maximum number of contracts with strike price $1,0000 (5389);

- The ratio of PUT/CALL was 1.18 versus 1.19 from the previous trading day according to data from January, 12

GBP/USD

Resistance levels (open interest**, contracts)

$1.2411 (330)

$1.2315 (437)

$1.2220 (222)

Price at time of writing this review: $1.2166

Support levels (open interest**, contracts):

$1.2082 (467)

$1.1986 (2161)

$1.1889 (3022)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 16654 contracts, with the maximum number of contracts with strike price $1,2800 (3018);

- Overall open interest on the PUT options with the expiration date March, 13 is 20859 contracts, with the maximum number of contracts with strike price $1,1500 (3218);

- The ratio of PUT/CALL was 1.25 versus 1.24 from the previous trading day according to data from January, 12

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:21

WSE: Before opening

Thursday's sessions on the New York stock markets ended with slight declines in the major indexes. At the close the Dow Jones Industrial fell 0.32 percent, Nasdaq Composite went down by 0.29 percent and the S&P 500 lost 0.21 percent. Markets still remain under the influence of Wednesday's Donald Trump press conference, which has not met the expectations of investors.

From the point of view of the European markets this small changes in the indices are positive surprise. When Europe closed the day the S&P 500 lost nearly 1 percent, and close the day giving barely 0.2 percent. We may therefore expect an alignment in Europe, which supports the positive position of the contract for the S&P500.

On the Warsaw market overcome by the WIG20 level of 2,000 points built potential for growth in the region of 2,350 pts., but there were also attempts to profit taking. Market defends itself against a decline under 2,000 pts., however, has not enough power to overcome the region of 2,040 pts.

The impetus for further play likely will flow from the US, where investors will meet today with the first quarterly results. In the plans are among other reports of three major banks. Positive reactions from US investors surely will be noticed in other markets.

-

07:03

German index of selling prices in wholesale trade was down 1.0% on an annual average

The index of selling prices in wholesale trade was down 1.0% on an annual average in 2016 from the preceding year, as reported by the Federal Statistical Office (Destatis).

Compared with December 2015, the index increased by 2.8% in December 2016. In November 2016 the annual rate of change was +0.8% and in October 2016 it was +0.5%, respectively.

Compared with November 2016 the index of wholesale prices rose by 1.2% in December 2016.

-

07:01

UAE oil minister, Suhail Al-Mazrui: the price of $ 50 a barrel is too low for most of the producer countries

Analysts of the IMF stated that the price of $ 60 per barrel is the minimum cost-effective for the United Arab Emirates.

-

07:00

Yellen: Fed Working on Behalf of Main Street, Not Wall Street

-

Fed Not Trying to Give Advantage to One Group Over Another With Policy Decisions

-

Made No Comments on Monetary Policy, Interest Rates

-

Fed Committed to Promoting Diversity in Fed Ranks, Economics Profession

-

Consumers Skilled in Financial Management Better Able to Weather Hard Times

-

Improving Education Can Help Spur Economic Growth, Raise Living Standards

-

Without Fed Emergency Lending, 2008 Crisis Outcomes Would Have Been 'Far Worse'

-

Important for Students to Understand Fed's Unconventional Monetary Policies

-

Women Hugely Underrepresented in Economics Jobs, College Majors, PhD Programs

-

-

06:55

China's trade surplus declined in December

As reported today by the General Customs Administration of China, China's trade surplus of the foreign trade balance in December was $ 40.81 billion. Analysts had expected an increase of $ 46.5 billion

The trade balance - the indicator assesses the overall ratio of exports and imports of goods and services. A positive balance indicates a surplus, while a negative a deficit. As China's economy has a major impact on the global economy, this indicator has a specific meaning for the Forex market.

As the volume of exports from China fell by 6.1% year on year, lower than the previous value of -1.9% and -3.5% forecast. Imports to China increased by 3.1%, after rising 4.7% in October.

-

06:26

Global Stocks

European stocks broke a two-day winning run on Thursday, yanked lower by drug makers as U.S. President-elect Donald Trump's comments on the pharma industry continued to bite. Auto stocks also slumped following accusations that Fiat Chrysler doctored its diesel-emissions test.

U.S. stocks rebounded from a sharp morning selloff, but still closed lower Thursday, with the Nasdaq snapping a seven-day winning streak as investors paused before the start of earnings season and a lack of policy detail in President-elect Donald Trump's first formal news conference a day ago. Equity markets have been trading mostly sideways as investors begin to question the run-up in stock prices following the election on Trump's promises of fiscal stimulus.

Many major Asian stocks indexes started lower Friday after modest overnight declines in the U.S., but the Nikkei bucked the trend as the dollar has regained some footing versus the yen. Following broad gains last week, regional equity markets have been choppy this week as liquidity steadily returned following a slowdown during the Christmas season.

-

03:01

China: Trade Balance, bln, December 40.82 (forecast 46.5)

-