Market news

-

23:28

Commodities. Daily history for Jan 16’2017:

(raw materials / closing price /% change)

Oil 52.52 +0.29%

Gold 1,197.30 +0.09%

-

23:27

Stocks. Daily history for Jan 16’2017:

(index / closing price / change items /% change)

Nikkei -192.04 19095.24 -1.00%

TOPIX -14.25 1530.64 -0.92%

Hang Seng -219.23 22718.15 -0.96%

CSI 300 -0.46 3319.45 -0.01%

Euro Stoxx 50 -29.81 3294.53 -0.90%

FTSE 100 -10.68 7327.13 -0.15%

DAX -74.47 11554.71 -0.64%

CAC 40 -40.31 4882.18 -0.82%

DJIA -5.27 19885.73 -0.03%

S&P 500 +4.20 2274.64 +0.18%

NASDAQ +26.63 5574.12 +0.48%

S&P/TSX -17.99 15479.29 -0.12%

-

23:26

Currencies. Daily history for Jan 16’2017:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0601 -0,33%

GBP/USD $1,2045 -1,17%

USD/CHF Chf1,0117 +0,27%

USD/JPY Y114,19 -0,33%

EUR/JPY Y121,04 -0,68%

GBP/JPY Y137,53 -1,51%

AUD/USD $0,7475 -0,31%

NZD/USD $0,7101 -0,28%

USD/CAD C$1,3174 +0,36%

-

21:16

New Zealand: NZIER Business Confidence, Quarter IV 28%

-

17:00

European stocks closed: FTSE 100 -10.68 7327.13 -0.15% DAX -74.47 11554.71 -0.64% CAC 40 -40.31 4882.18 -0.82%

-

16:38

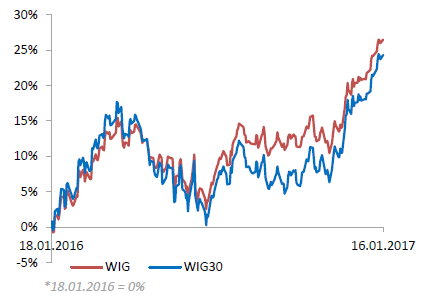

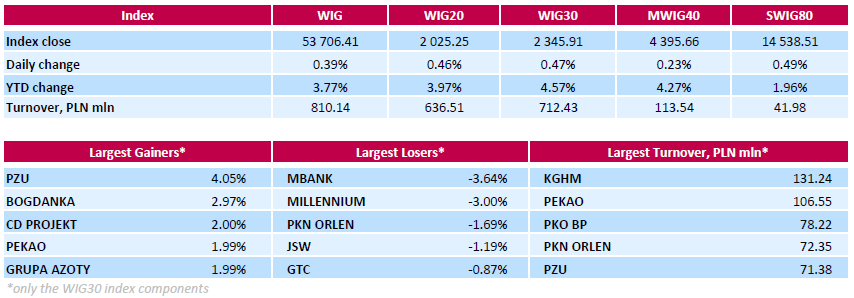

WSE: Session Results

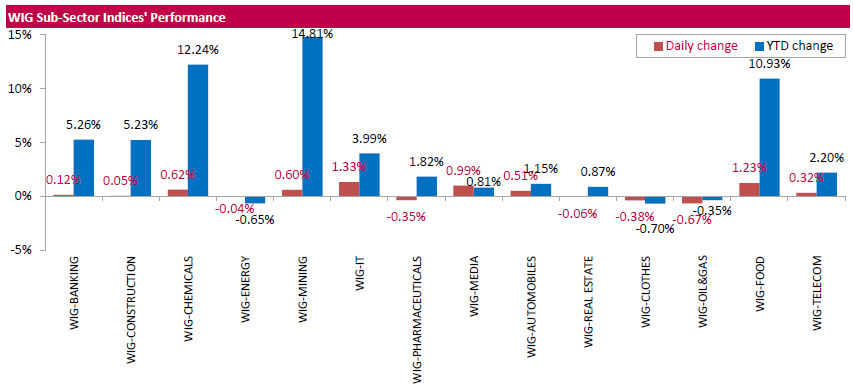

Polish equity market closed higher on Monday. The broad measure, the WIG index, added 0.39%. Sector-wise, informational technology stocks (+2.30%) outperformed, while oil and gas names (-0.67%) recorded the worst result.

The large-cap benchmark, the WIG30 Index, surged by 0.47%. Within the index components, insurer PZU (WSE: PZU) led the advancers, climbing by 4.05%. It was followed by thermal coal miner BOGDANKA (WSE: LWB), videogame developer CD PROJEKT (WSE: CDR), chemical producer GRUPA AZOTY (WSE: ATT) and bank PEKAO (WSE: PEO), which gained between 1.99% and 2.97%. On the other side of the ledger, banking names MBANK (WSE: MBK) and MILLENNIUM (WSE: MIL) were the weakest performers, tumbling by 3.64% and 3% respectively.

-

15:51

Allianz Chief Economist El-Erian: stronger US dollar - the biggest risk in 2017

"In 2017, world economic growth may be better than expected, although there remains a lot of uncertainty factors that may affect the expansion, and the most significant of which is the strengthening of the US dollar", - said the chief economist of Allianz, Mohamed El-Erian.

"Prospects for the world economy in 2017 will be the same as last year, but the risks are reversed. The world economy will expand at a rate lower than 3 percent, and the US economy will outperform it, with growth of 2.5-3 percent, pointed El-Erian.

"The dynamics of the US economy is expected to support the US dollar, but the currency can be strengthened further if the US Federal Reserve will raise interest rates at least three times in accordance with the baseline scenario for 2017, rather than twice, as priced in".

-

15:29

Raiffeisen Bank expects EUR/HUF to return to levels around and above 310, saying higher-than-expected CPI doesn't underpin an earlier-than-seen rise in the country's key policy rate

-

14:49

Average Canadian Home Sales Price Climbed 3.5% in December from Year Ago

-

14:30

The IMF expects global economic growth to accelerate to 3.4% in 2017 and to 3.1% in 2016

-

The IMF lowered its forecast for Mexico, Brazil, and India, but raised for China

-

The IMF raised its forecast for US GDP growth for 2017 to 2.3% from 2.2% in view of the stimulus plan proposed by Trump

-

Trump policy may harm economic growth in the case of growing protectionism in the US

-

The forecast for GDP growth in the UK in 2017 has been improved to 1.5% from 1.1%

-

The forecast for Eurozone GDP in 2017 was revised to 1.6% from 1.5%

-

The forecast for GDP growth in Italy in 2017 was downgraded to 0.7% from 0.9%

-

The forecast for the growth of Japan's GDP for 2017 was revised to 0.8% from 0.6%

-

The forecast for GDP growth in Canada for 2017 was confirmed at 1.9%.

-

The forecast for China's GDP growth for 2017 was revised to 6.5% from 6.2%

-

-

14:02

OECD unemployment rate remained stable in November

The data published by the Organisation for Economic Cooperation and Development, showed that the unemployment rate among the OECD countries remained unchanged in November.

The unemployment rate was 6.2 percent, in line with the figure for the previous month. Across the OECD area, 38.5 million people were unemployed.

In the euro area unemployment rate also remained stable, at around 9.8 percent. Meanwhile, the unemployment rate decreased by 0.2 percentage points to 6.8 per cent in Canada and 4.6 percent in the United States. The report also showed that the unemployment rate in Japan rose in November by 0.1 percentage points to 3.1 percent.

The OECD reported that the unemployment rate among young people aged 15 to 24 years remained high, especially in Southern Europe. In total, 9.3 million young people were unemployed in the OECD countries. The youth unemployment rate was 12.8 percent.

-

13:45

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0440 (EUR 1,221 M) 1.0450 (EUR 234 M) 1.0500-1.0515 (EUR 530 M) 1.0575-1.0580 (EUR 528 M) 1.0600 (EUR 182 M) 1.0625 (EUR 301 M) 1.0640-1.0650 (EUR 204 M) 1.0700-1.0710 (EUR 335 M) 1.0745-1.0760 (EUR 591 M)

GBP/USD 1.2180 (GBP 188 M) 1.2200 (GBP 952 M) 1.2225 (GBP 479 M)

USD/JPY 112.00 (USD 1,285 M) 114.00 (USD 575 M) 115.00 (USD 3,626 M) 116.00-116.05 (USD 340 M)

AUD/USD 0.7470-0.7485 (AUD 1,215 M)

NZD/USD 0.7300 (NZD 603 M)

-

13:12

Tomorrow afternoon UK Prime Minister May speaks about Brexit, in London. GBP volatility expected to continue. "Hard" Brexit rumors hit the pound

-

13:07

Capital Economics expects central banks in Romania and the Czech Republic to "rein in extremely loose monetary policy," in the short run on strengthening core inflation and as higher oil prices boosting headline CPI

-

12:04

WSE: Mid session comment

The first half of today's trading was relatively peacefully, although held under the sign of discounts. Moving away from Friday's closing was seen quite wide. The turnover in the amount of PLN 210 million in the segment of blue chips and PLN 300 million for the entire market is slightly smaller than usual, but not so low as usual in the absence of the Americans. South phase of the session brought the chart of the WIG20 index on the green side.

At the halfway point of today's quotations the WIG20 index was at the level of 2,016 points (+ 0.01%).

-

11:44

Major stock indices in Europe little changed

Market's attention this week is aimed at the European Central Bank meeting. Also, market participants expect British Prime Minister Theresa May's speech on Tuesday devoted to the position of London in the Brexit negotiations.

The surplus of the trade balance of the euro zone rose in November as export growth outpaced import growth showed Eurostat data. The surplus of the trade balance rose to a seasonally adjusted 22.7 billion euros in November, compared with 19.9 billion euros in October. Exports rose by 3.3 percent, while imports grew by 1.8 percent from October.

In unadjusted basis, the trade surplus amounted to 25.9 billion euros compared to 22.9 billion euros in the previous year. Exports showed an annual growth of 6 per cent, while imports posted a 5 percent increase. Exports to the 28 EU countries increased by 3.1 percent and imports by 3 per cent. As a result, the trade surplus increased to EUR 4.1 billion from EUR 3.9 billion in October.

The composite index of the largest companies in the region Stoxx Europe 600 fell 0,5%, to 364.01 points.

Some support for the UK market had a weakening of the pound sterling against the US dollar, down 1.6%.

The structure of the UK FTSE 100 index includes companies primarily focused on foreign markets, for which the weakening of the pound is a favorable factor.

Thus, the value of Unilever shares rose 0,4%, Reckitt Benckiser +0.8%.

Meanwhile, shares of British banks are getting cheaper: Barclays - 2%, HSBC Holdings - 0,1%, Royal Bank Of Scotland - 3%.

The value of shares of the French manufacturer of eyeglass lenses and optical equipment Essilor International jumped 12.4% on the information of the merger with the Italian company Luxottica Group SpA, which owns such well-known brands of glasses as Ray-Ban and Oakley. The amount of the transaction, which will be held in the form of an exchange of shares, will be about 22.8 billion euros. Luxottica Shares rose 8%.

At the moment:

FTSE 7340.82 3.01 0.04%

DAX 11559.43 -69.75 -0.60%

CAC 4897.66 -24.83 -0.50%

-

11:13

Allianz Chief Executive Oliver Baete expects Donald Trump's presidency to have a positive effect on the insurer

-

10:27

The sterling exchange rate moves every time May puts continued access to the single market into question by insisting on immigration controls - Citigroup

-

10:21

The euro area recorded a €25.9 bn surplus in trade in November, higher than expected

The first estimate for euro area (EA19) exports of goods to the rest of the world in November 2016 was €184.2 billion, an increase of 6% compared with November 2015 (€173.8 bn). Imports from the rest of the world stood at €158.3 bn, a rise of 5% compared with November 2015 (€150.9 bn).

As a result, the euro area recorded a €25.9 bn surplus in trade in goods with the rest of the world in November 2016, compared with +€22.9 bn in November 2015. Intra-euro area trade rose to €154.0 bn in November 2016, up by 5% compared with November 2015

-

10:00

Eurozone: Trade balance unadjusted, November 25.9 (forecast 22)

-

09:23

Oil is trading lower

This morning, the New York futures for Brent down 0.18% to $ 55.35 and WTI fell 0.17% to $ 52.28. Thus, the black gold prices trading with a small loss. Recall that last week, oil fell 3%. The US Department of Energy last week reported an increase in the production of 176,000 barrels a day. However, Baker Hughes data showed a decrease in the number of oil rigs in the United States over the last ten weeks. According to Baker Hughes, the number of drilling rigs decreased by seven in the past week, to 522 units.

-

09:05

Spokeswoman For British PM May says Talk of Hard Brexit is "Speculation" - Reuters

-

08:45

Major stock markets in Europe trading lower: FTSE 100 7,329.24 -8.57 -0.12%, DAX 11,629.18 108.14 0.94%, CAC 40 4,922.49 58.52 1.20%, IBEX 35 9,432.20 -79.40 -0.83%

-

08:17

WSE: After opening

WIG20 index opened at 2013.32 points (-0.13%)*

WIG 53421.67 -0.14%

WIG30 2331.07 -0.17%

mWIG40 4383.67 -0.04%

*/ - change to previous close

The Warsaw cash market started the new week with a light descent and with quite good turnover like for a Monday without the Americans. Weaker are banks with the portfolios of foreign currency loans, and they have the greatest impact on the decline in the index. The chart of the WIG20 index is slowly approaching the level of 2,000 points and broke the first line of the uptrend. The German DAX lost more than 0.6%, which means that today's departure from the risk applies to most markets.

After fifteen minutes of trading the WIG20 index was at the level of 2,007 points (-0.41%).

-

08:14

Deutsche Bank presents 5 stages of the Trump trade

"There are probably five defining stages for the "Trump trade": Trading i) 'the promise'; ii) the deal-making; iii) the enactment; iv) the economic impact, and, v) the payback.

i) The promise stage is done. It has been powerful, precisely because it has involved a possible paradigm shift in cyclical stimulus and because the expected US policy mix is seen as so differentiated from the rest of the world.

ii) The deal-making phase. will take shape over the next 100 days. Here we will start to get a better feel for the scale of fiscal stimulus, and therefore the spillover onto monetary policy. The complexity of far-reaching changes could stretch this phase, making for more frustrating trade conditions, especially since the Fed is not under too much pressure to front-load their actions, without more clarity on fiscal policy.

iii) For the enactment phase where deals are signed off on in H2, the market will be particularly responsive to issues that relate to timing of impact; multiplier effects; the breakdown not least as it relates to far reaching corporate tax reform that will impact trade patterns, FDI, equity and bond flows; and, protectionist elements where retaliation is a real threat. Not to be forgotten in this phase is the overlap with changes in key Fed personnel, including the Fed Chair appointment. The talk of a more rules based Fed, or at least having the Fed Chair explain departures in policy from a rules based system, is apt to be seen as hawkish, especially given how accommodative policy is now (fed funds is tracking 100 - 125bps below a Taylor Rule signal).

iv) The economic impact phase. The growth impulse will likely be felt mostly in 2018, with questions on how much the upturn is accelerated and elongated into say 2019. The inflation impulse could have even longer lags, unless there is a border adjustment tax that hits import prices quickly. This will be a phase where we better understand how much the Fed will tighten in this cycle and whether the peak in the USD is in 2018 or even beyond. If there is a genuine acceleration in growth, the market could make sizable adjustments in Fed expectations, and this may well prove another important period for trending markets.

v).The payback phase. Fiscal stimulus often brings growth forward, usually with a payback in the form of slower growth as the stimulus wears thin. Similarly, there is a reversal in financial prices. Think of this as the equivalent of what we saw for the USD in the 1982-84, where the rally gave way to 'the payback' of a much weaker USD in 1985-87. In current circumstances payback is more relevant for 2019 and beyond.

While each of these five stages is likely to have its own defined characteristics, there is apt to be plenty of overlap. Importantly for USD bulls, fiscal initiatives should be seen as the 'icing on the cake'. The Fed was lining up to be the only G10 Central Bank to tighten in 2017, whoever was elected. Even a moderate net fiscal stimulus of say 1% of GDP without far-reaching tax reform or border adjustment taxes can justify modest USD strength (~5% on the TWI). Border adjustment taxes with its impact on trade, inflation and Fed policy, would simply make the story overwhelming".

Copyright © 2017 DB, eFXnews™

-

07:48

Negative start of trading expected on the major stock exchanges in Europe: DAX -0.6%, CAC40 -0.4%, FTSE -0.3%

-

07:40

UK property prices increased 0.4 percent in January - Rightmove

U.K. house prices increased marginally in January, property website Rightmove, cited by rttnews.

Property prices increased 0.4 percent in January from prior month to hit GBP 300,245. On a yearly basis, house prices advanced 3.2 percent in January.

Those planning to buy their first home in 2017 have more choice of properties and less competition from other buyers than their counterparts a year ago. Miles Shipside, Rightmove director said.

Rightmove said its website traffic increased by 5 percent since Boxing Day.

-

07:38

Today’s events

-

At 12:30 GMT the ECB board member Yves Mersch will deliver a speech

-

At 15:45 GMT the ECB board member Peter Praet makes a speech

-

At 18:30 GMT Bank of England's Governor Mark Carney will deliver a speech

-

US celebrate Martin Luther King Day

-

-

07:20

Australian inflation gauge rose more than expected

In December, inflation data from TD Securities, published by the Faculty of Economics and Commerce at the University of Melbourne, have increased by 0.5% after rising 0.1% in November. In annual terms, the indicator rose to 1.8%, which is higher than the previous value of 1.5%.

Target inflation rate of the Reserve Bank of Australia is 2-3%, and judging by today's data, the central bank is likely to postpone an interest rate cut for some time

-

07:18

WSE: Before opening

On Friday, Fitch Ratings maintained the Polish rating of "A minus" with a stable outlook, which was fully in line with expectations. The agency expects that in 2017 the growth rate of the Polish economy will accelerate to 3.0 percent and in 2018 to 3.2 percent from 2.7 percent in 2016. More important was the verdict from Moody's Agency, which once again has not provided any statement, what should be read as a lack of updating rating and consequently to leave it unchanged.

Today in the US is the day off in relation with the Martin Luther King Day. No session on Wall Street traditionally should lead to lower volatility and activity.

In Asia, the morning is dominated by the color red, what may indicate some shift away from risk in Europe as well. The exception is London, where the next threat of the "hard" version of Brexit weakening the pound and will help for British shares.

-

07:17

Japan's index of business activity in the services sector rose 0.2% November

According to data released today by the Ministry of Economy, Trade and Industry of Japan, the index of business activity in the services sector grew by 0.2% in November on a monthly basis after flat in October.

It is worth noting that this was the first increase in the index for the last four months. Most activity has increased in sectors such as information and communication, trade, finance and insurance, related business services, health care services and social services (electricity, gas, heat and water). Meanwhile, there was a decline in the sectors of entertainment, transport and postal services, lease, rental, leasing, retail and real estate.

-

07:11

Theresa May to say UK is 'prepared to accept hard Brexit'. GBP/USD gaps down 150 pips

-

06:32

Global Stocks

The British pound fell sharply against the dollar on Sunday ahead of a key speech by U.K. Prime Minister Theresa May in which many investors believe she could spell out an end to her country's participation in European Union's single market. The currency declined 1.6% against the dollar to $1.199. The pound dropped 1% last week after May repeated earlier indications that she was looking to push for a 'hard Brexit ' from the EU, which Britain voted to leave last June.

U.S. stocks have had an incredible run over the last two months and even at these record-breaking levels there are still profits to make - at least until March, when it will be time to run for the hills. That's a key message from Goldman Sachs chief U.S. equity strategist David Kostin, who says optimism over expected tax reforms from the Trump administration is likely to push the S&P 500 index SPX, +0.18% to 2,400 by the end of the first quarter.

Asian stocks indexes ended the week broadly lower after choppy trading Friday, as markets sought direction after largely trending higher in 2017. Market players have begun to adopt a wait-and-see approach following the great expectations a number of people had in the immediate aftermath of Donald Trump's election win.

-

06:09

Options levels on monday, January 16, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0780 (2217)

$1.0745 (2213)

$1.0703 (254)

Price at time of writing this review: $1.0618

Support levels (open interest**, contracts):

$1.0541 (1263)

$1.0488 (2433)

$1.0422 (3270)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 53315 contracts, with the maximum number of contracts with strike price $1,1500 (3335);

- Overall open interest on the PUT options with the expiration date March, 13 is 62630 contracts, with the maximum number of contracts with strike price $1,0000 (4911);

- The ratio of PUT/CALL was 1.17 versus 1.18 from the previous trading day according to data from January, 13

GBP/USD

Resistance levels (open interest**, contracts)

$1.2316 (528)

$1.2221 (222)

$1.2126 (162)

Price at time of writing this review: $1.2032

Support levels (open interest**, contracts):

$1.1987 (2202)

$1.1890 (3233)

$1.1792 (1011)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 17747 contracts, with the maximum number of contracts with strike price $1,2800 (3018);

- Overall open interest on the PUT options with the expiration date March, 13 is 21484 contracts, with the maximum number of contracts with strike price $1,1500 (3223);

- The ratio of PUT/CALL was 1.21 versus 1.25 from the previous trading day according to data from January, 13

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

04:32

Japan: Tertiary Industry Index , November 0.2%

-

01:32

Commodities. Daily history for Jan 13’2017:

(raw materials / closing price /% change)

Oil 52.52 +0.29%

Gold 1,197.30 +0.09%

-

01:31

Stocks. Daily history for Jan 13’2017:

(index / closing price / change items /% change)

Nikkei -90.51 19196.77 -0.47%

TOPIX -5.33 1539.56 -0.35%

Hang Seng +108.36 22937.38 +0.47%

Euro Stoxx 50 +37.64 3324.34 +1.15%

FTSE 100 +22.66 6954.21 +0.33%

DAX +108.14 11629.18 +0.94%

CAC 40 +28.59 4764.07 +0.60%

DJIA -5.27 19885.73 -0.03%

S&P 500 +4.20 2274.64 +0.18%

NASDAQ +26.63 5574.12 +0.48%

S&P/TSX +79.12 15497.28 +0.51%

-

01:30

Currencies. Daily history for Jan 13’2017:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0636 +0,24%

GBP/USD $1,2186 +0,22%

USD/CHF Chf1,009 -0,18%

USD/JPY Y114,57 -0,11%

EUR/JPY Y121,86 +0,11%

GBP/JPY Y139,6 +0,09%

AUD/USD $0,7498 +0,21%

NZD/USD $0,7121 +0,38%

USD/CAD C$1,3126 -0,13%

-

01:01

Schedule for today, Monday, Jan 16’2017 (GMT0)

04:30 Japan Tertiary Industry Index November 0.2%

10:00 Eurozone Trade balance unadjusted November 20.1 22

12:00 U.S. Bank holiday

21:00 New Zealand NZIER Business Confidence Quarter IV 26%

-