Market news

-

23:27

Stocks. Daily history for Jan 16’2017:

(index / closing price / change items /% change)

Nikkei -192.04 19095.24 -1.00%

TOPIX -14.25 1530.64 -0.92%

Hang Seng -219.23 22718.15 -0.96%

CSI 300 -0.46 3319.45 -0.01%

Euro Stoxx 50 -29.81 3294.53 -0.90%

FTSE 100 -10.68 7327.13 -0.15%

DAX -74.47 11554.71 -0.64%

CAC 40 -40.31 4882.18 -0.82%

DJIA -5.27 19885.73 -0.03%

S&P 500 +4.20 2274.64 +0.18%

NASDAQ +26.63 5574.12 +0.48%

S&P/TSX -17.99 15479.29 -0.12%

-

17:00

European stocks closed: FTSE 100 -10.68 7327.13 -0.15% DAX -74.47 11554.71 -0.64% CAC 40 -40.31 4882.18 -0.82%

-

16:38

WSE: Session Results

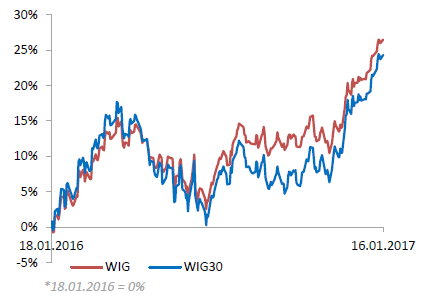

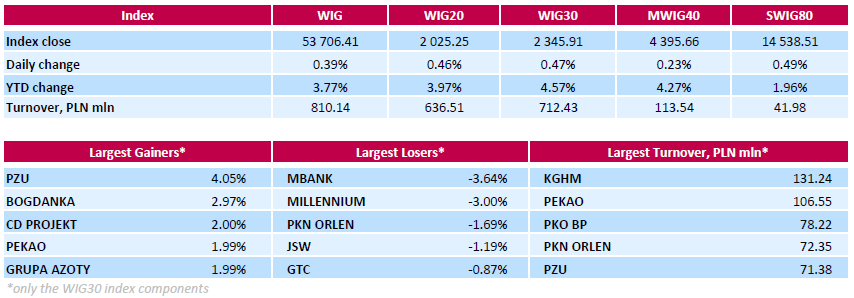

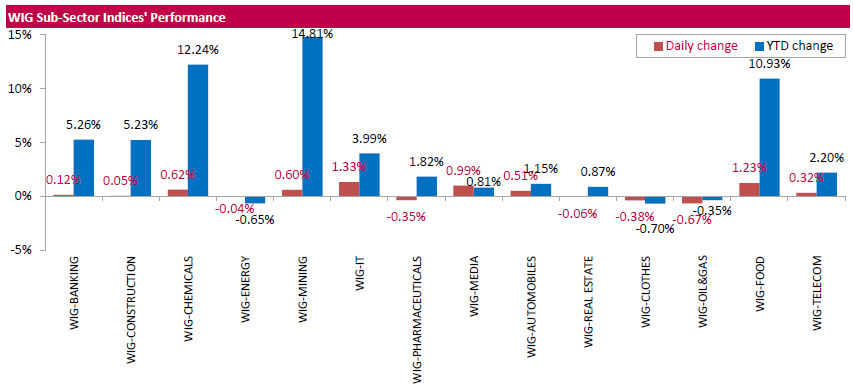

Polish equity market closed higher on Monday. The broad measure, the WIG index, added 0.39%. Sector-wise, informational technology stocks (+2.30%) outperformed, while oil and gas names (-0.67%) recorded the worst result.

The large-cap benchmark, the WIG30 Index, surged by 0.47%. Within the index components, insurer PZU (WSE: PZU) led the advancers, climbing by 4.05%. It was followed by thermal coal miner BOGDANKA (WSE: LWB), videogame developer CD PROJEKT (WSE: CDR), chemical producer GRUPA AZOTY (WSE: ATT) and bank PEKAO (WSE: PEO), which gained between 1.99% and 2.97%. On the other side of the ledger, banking names MBANK (WSE: MBK) and MILLENNIUM (WSE: MIL) were the weakest performers, tumbling by 3.64% and 3% respectively.

-

12:04

WSE: Mid session comment

The first half of today's trading was relatively peacefully, although held under the sign of discounts. Moving away from Friday's closing was seen quite wide. The turnover in the amount of PLN 210 million in the segment of blue chips and PLN 300 million for the entire market is slightly smaller than usual, but not so low as usual in the absence of the Americans. South phase of the session brought the chart of the WIG20 index on the green side.

At the halfway point of today's quotations the WIG20 index was at the level of 2,016 points (+ 0.01%).

-

11:44

Major stock indices in Europe little changed

Market's attention this week is aimed at the European Central Bank meeting. Also, market participants expect British Prime Minister Theresa May's speech on Tuesday devoted to the position of London in the Brexit negotiations.

The surplus of the trade balance of the euro zone rose in November as export growth outpaced import growth showed Eurostat data. The surplus of the trade balance rose to a seasonally adjusted 22.7 billion euros in November, compared with 19.9 billion euros in October. Exports rose by 3.3 percent, while imports grew by 1.8 percent from October.

In unadjusted basis, the trade surplus amounted to 25.9 billion euros compared to 22.9 billion euros in the previous year. Exports showed an annual growth of 6 per cent, while imports posted a 5 percent increase. Exports to the 28 EU countries increased by 3.1 percent and imports by 3 per cent. As a result, the trade surplus increased to EUR 4.1 billion from EUR 3.9 billion in October.

The composite index of the largest companies in the region Stoxx Europe 600 fell 0,5%, to 364.01 points.

Some support for the UK market had a weakening of the pound sterling against the US dollar, down 1.6%.

The structure of the UK FTSE 100 index includes companies primarily focused on foreign markets, for which the weakening of the pound is a favorable factor.

Thus, the value of Unilever shares rose 0,4%, Reckitt Benckiser +0.8%.

Meanwhile, shares of British banks are getting cheaper: Barclays - 2%, HSBC Holdings - 0,1%, Royal Bank Of Scotland - 3%.

The value of shares of the French manufacturer of eyeglass lenses and optical equipment Essilor International jumped 12.4% on the information of the merger with the Italian company Luxottica Group SpA, which owns such well-known brands of glasses as Ray-Ban and Oakley. The amount of the transaction, which will be held in the form of an exchange of shares, will be about 22.8 billion euros. Luxottica Shares rose 8%.

At the moment:

FTSE 7340.82 3.01 0.04%

DAX 11559.43 -69.75 -0.60%

CAC 4897.66 -24.83 -0.50%

-

08:45

Major stock markets in Europe trading lower: FTSE 100 7,329.24 -8.57 -0.12%, DAX 11,629.18 108.14 0.94%, CAC 40 4,922.49 58.52 1.20%, IBEX 35 9,432.20 -79.40 -0.83%

-

08:17

WSE: After opening

WIG20 index opened at 2013.32 points (-0.13%)*

WIG 53421.67 -0.14%

WIG30 2331.07 -0.17%

mWIG40 4383.67 -0.04%

*/ - change to previous close

The Warsaw cash market started the new week with a light descent and with quite good turnover like for a Monday without the Americans. Weaker are banks with the portfolios of foreign currency loans, and they have the greatest impact on the decline in the index. The chart of the WIG20 index is slowly approaching the level of 2,000 points and broke the first line of the uptrend. The German DAX lost more than 0.6%, which means that today's departure from the risk applies to most markets.

After fifteen minutes of trading the WIG20 index was at the level of 2,007 points (-0.41%).

-

07:48

Negative start of trading expected on the major stock exchanges in Europe: DAX -0.6%, CAC40 -0.4%, FTSE -0.3%

-

07:18

WSE: Before opening

On Friday, Fitch Ratings maintained the Polish rating of "A minus" with a stable outlook, which was fully in line with expectations. The agency expects that in 2017 the growth rate of the Polish economy will accelerate to 3.0 percent and in 2018 to 3.2 percent from 2.7 percent in 2016. More important was the verdict from Moody's Agency, which once again has not provided any statement, what should be read as a lack of updating rating and consequently to leave it unchanged.

Today in the US is the day off in relation with the Martin Luther King Day. No session on Wall Street traditionally should lead to lower volatility and activity.

In Asia, the morning is dominated by the color red, what may indicate some shift away from risk in Europe as well. The exception is London, where the next threat of the "hard" version of Brexit weakening the pound and will help for British shares.

-

06:32

Global Stocks

The British pound fell sharply against the dollar on Sunday ahead of a key speech by U.K. Prime Minister Theresa May in which many investors believe she could spell out an end to her country's participation in European Union's single market. The currency declined 1.6% against the dollar to $1.199. The pound dropped 1% last week after May repeated earlier indications that she was looking to push for a 'hard Brexit ' from the EU, which Britain voted to leave last June.

U.S. stocks have had an incredible run over the last two months and even at these record-breaking levels there are still profits to make - at least until March, when it will be time to run for the hills. That's a key message from Goldman Sachs chief U.S. equity strategist David Kostin, who says optimism over expected tax reforms from the Trump administration is likely to push the S&P 500 index SPX, +0.18% to 2,400 by the end of the first quarter.

Asian stocks indexes ended the week broadly lower after choppy trading Friday, as markets sought direction after largely trending higher in 2017. Market players have begun to adopt a wait-and-see approach following the great expectations a number of people had in the immediate aftermath of Donald Trump's election win.

-

01:31

Stocks. Daily history for Jan 13’2017:

(index / closing price / change items /% change)

Nikkei -90.51 19196.77 -0.47%

TOPIX -5.33 1539.56 -0.35%

Hang Seng +108.36 22937.38 +0.47%

Euro Stoxx 50 +37.64 3324.34 +1.15%

FTSE 100 +22.66 6954.21 +0.33%

DAX +108.14 11629.18 +0.94%

CAC 40 +28.59 4764.07 +0.60%

DJIA -5.27 19885.73 -0.03%

S&P 500 +4.20 2274.64 +0.18%

NASDAQ +26.63 5574.12 +0.48%

S&P/TSX +79.12 15497.28 +0.51%

-