Market news

-

20:08

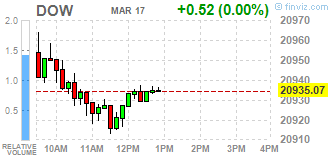

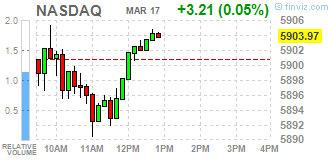

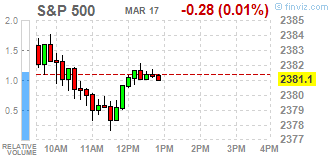

Major US stock indexes finished trading mostly in the red

The main US stock indexes mostly fell, as the continuing effects of the Fed's less aggressive position vis-à-vis the rates had a negative impact on the financial sector. As it became known today, manufacturing production in the US increased for the sixth consecutive month in February, which indicates that the recovery of production is gaining momentum, as rising commodity prices increase the demand for engineering products and other equipment. The Federal Reserve said manufacturing production in the manufacturing sector rose 0.5% last month.

In addition, preliminary research results submitted by Thomson-Reuters and the Michigan Institute showed that the mood sensor among US consumers increased in March, exceeding the average forecasts. According to the data, in March the consumer sentiment index rose to 97.6 points compared to the final reading for February at the level of 96.3 points. According to average estimates, the index had to grow to the level of 97 points.

At the same time, the index of leading economic indicators from the Conference Board (LEI) for the US increased by 0.6% in February, to 126.2 (2010 = 100) after a 0.6% increase in January, as well as an increase of 0, 6% in December. Analysts had expected the index to grow by 0.4%.

The components of the DOW index have mostly grown (17 out of 30). More shares fell The Goldman Sachs Group, Inc. (GS, -1.58%). The leader of growth was shares United Technologies Corporation (UTX, + 1.12%).

Most sectors of the S & P index recorded an increase. The leader of growth was the utilities sector (+ 0.9%). The financial sector fell most of all (-0.5%).

At closing:

Dow -0.10% 20,914.49 -20.06

Nasdaq + 0.00% 5,901.00 +0.24

S & P -0.14% 2,378.08 -3.30

-

19:00

DJIA +0.11% 20,957.19 +22.64 Nasdaq +0.14% 5,908.85 +8.09 S&P +0.08% 2,383.28 +1.90

-

17:01

European stocks closed: FTSE 100 +9.01 7424.96 +0.12% DAX +12.06 12095.24 +0.10% CAC 40 +15.86 5029.24 +0.32%

-

16:53

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Friday as the lingering effects of the Federal Reserve's less aggressive stance on the rates outlook hurt the financial sector.

Most of Dow stocks in positive area (17 of 30). Top loser - The Goldman Sachs Group, Inc. (GS, -1.41%). Top gainer - McDonald's Corporation (MCD, +1.12%).

Most of S&P sectors also in positive area. Top loser - Financials (-0.5%). Top gainer - Utilities (+0.5%).

At the moment:

Dow 20882.00 0.00 0.00%

S&P 500 2377.75 -1.25 -0.05%

Nasdaq 100 5418.00 +3.00 +0.06%

Oil 49.27 +0.03 +0.06%

Gold 1228.20 +1.10 +0.09%

U.S. 10yr 2.50 -0.02

-

15:31

U.S Tips inflation breakeven rates fall to session lows after U Michigan consumer sentiment data in early March

-

15:24

BoJ Kuroda: U.S administration's stance on trade not clear yet so shouldn't have any preconceptions at this stage

-

Hope to tell G20 BoJ will continue to pursue powerful monetary easing to achieve domestic mandate of 2 pct inflation

-

Don't think global consensus on importance of free trade will change suddenly, though unclear how debate at this G20 will unfold

-

There has been consensus among global institutions, including G20, on the need to promote free trade

-

-

15:15

Canadian manufacturing sales rose for the third consecutive month

Manufacturing sales rose for the third consecutive month, up 0.6% to $53.8 billion in January. The gain stemmed from a 2.3% increase in non-durable goods sales, led by the petroleum and coal, and chemical industries.

Sales were up in 14 of 21 industries, representing 75.4% of the total Canadian manufacturing sector.

In constant dollars, sales increased 0.7%, indicating that higher volumes of manufactured goods were sold in January.

-

15:14

Consumer sentiment in US remained quite favorable in early March - UoM

The overall level of consumer sentiment remained quite favorable in early March due to renewed strength in current economic conditions as well as the extraordinary influence of partisanship on economic prospects. The Current Economic Conditions component reached its highest level since 2000, largely due to improved personal finances.

While current economic conditions were not affected by partisanship, this was not true for the component about future economic prospects: among Democrats, the Expectations Index at 55.3 signaled that a deep recession was imminent, while among Republicans the Index at 122.4 indicated a new era of robust economic growth was ahead. Interestingly, those who self-identified as Independents had an Expectations Index of 88.3, which was nearly equal to the midpoint of the partisan difference.

-

15:12

US industrial production was unchanged in February following a 0.1 percent decrease in January

Industrial production was unchanged in February following a 0.1 percent decrease in January. In February, manufacturing output moved up 0.5 percent for its sixth consecutive monthly increase. Mining output jumped 2.7 percent, but the index for utilities fell 5.7 percent, as continued unseasonably warm weather further reduced demand for heating. At 104.7 percent of its 2012 average, total industrial production in February was 0.3 percent above its level of a year earlier. Capacity utilization for the industrial sector declined 0.1 percentage point in February to 75.4 percent, a rate that is 4.5 percentage points below its long-run (1972-2016) average.

-

14:00

U.S.: Leading Indicators , February 0.6% (forecast 0.4%)

-

14:00

U.S.: Reuters/Michigan Consumer Sentiment Index, March 97.6 (forecast 97)

-

13:34

U.S. Stocks open: Dow +0.14%, Nasdaq -0.04%, S&P +0.09%

-

13:25

Before the bell: S&P futures +0.03%, NASDAQ futures +0.14%

U.S. stock-index futures were flat, as investors looked for new catalyst for further movement.

Global Stocks:

Nikkei 19,521.59 -68.55 -0.35%

Hang Seng 24,309.93 +21.65 +0.09%

Shanghai 3,237.31 -31.62 -0.97%

FTSE 7,434.22 +18.27 +0.25%

CAC 5,029.75 +16.37 +0.33%

DAX 12,096.10 +12.92 +0.11%

Crude $48.98 (+0.47%)

Gold $1,228.90 (+0.15%)

-

13:15

U.S.: Industrial Production (MoM), February 0.0% (forecast 0.2%)

-

13:15

U.S.: Industrial Production YoY , February 0.3%

-

13:15

U.S.: Capacity Utilization, February 75.4% (forecast 75.5%)

-

13:00

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

190.62

0.31(0.16%)

500

Amazon.com Inc., NASDAQ

AMZN

850.49

-2.93(-0.34%)

13182

Apple Inc.

AAPL

140.89

0.20(0.14%)

51686

Barrick Gold Corporation, NYSE

ABX

19.05

0.14(0.74%)

32548

Boeing Co

BA

178.75

0.56(0.31%)

675

Caterpillar Inc

CAT

93

0.15(0.16%)

1160

Chevron Corp

CVX

107.8

-0.06(-0.06%)

661

Exxon Mobil Corp

XOM

82.3

0.23(0.28%)

5318

Facebook, Inc.

FB

140.08

0.09(0.06%)

30121

FedEx Corporation, NYSE

FDX

193.55

0.44(0.23%)

1720

Ford Motor Co.

F

12.68

-0.02(-0.16%)

19071

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

12.87

0.05(0.39%)

16531

General Electric Co

GE

29.74

-0.01(-0.03%)

9466

General Motors Company, NYSE

GM

36.99

-0.09(-0.24%)

3916

Intel Corp

INTC

35.27

0.13(0.37%)

12579

International Business Machines Co...

IBM

177.21

-0.03(-0.02%)

386

Johnson & Johnson

JNJ

128.44

-0.02(-0.02%)

492

McDonald's Corp

MCD

129

1.02(0.80%)

4608

Procter & Gamble Co

PG

91.64

0.20(0.22%)

2564

Starbucks Corporation, NASDAQ

SBUX

54.75

-0.05(-0.09%)

241

Tesla Motors, Inc., NASDAQ

TSLA

263.11

1.06(0.40%)

105871

Twitter, Inc., NYSE

TWTR

15.18

-0.01(-0.07%)

4771

Yandex N.V., NASDAQ

YNDX

23.99

0.25(1.05%)

300

-

12:45

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Tesla (TSLA) target raised to $187 from $185 at Goldman; maintain Sell

-

12:31

Romania IMF mission chief says estimates 2017 budget deficit will reach 3.7 pct/gdp

-

Pay inequities in public sector should be addressed

-

Successive tax cuts, wage hikes in excess of productivity and limited investment are threats to romanian economy

-

Sees no room for further tax cuts to preserve flexibility in the budget

-

Gains romania made to strengthen its economy are threatened

-

-

12:31

Canada: Manufacturing Shipments (MoM), January 0.6% (forecast -0.4%)

-

12:29

Latest French Opinionway poll: Le Pen 28%, +1

-

10:28

G20 financial leaders say monetary policy will continue to support economic growth and price stability, but cannot alone lead to balanced growth - Draft

-

Does not contain a reference to rejecting protectionism

-

To reiterate commitment to avoid competitive devaluations

-

To reiterate that exchange rate volatility is bad for economic growth

-

Will consult closely on exchange markets

-

Leaders agree on a set of principles to foster economic resilience

-

-

10:04

Euro area recorded a €0.6 bn deficit in trade in January 2017, compared with a surplus of €4.8 bn in January 2016

The first estimate for euro area (EA19) exports of goods to the rest of the world in January 2017 was €163.9 billion, an increase of 13% compared with January 2016 (€144.9 bn). Imports from the rest of the world stood at €164.5 bn, a rise of 17% compared with January 2016 (€140.1 bn).

As a result, the euro area recorded a €0.6 bn deficit in trade in goods with the rest of the world in January 2017, compared with a surplus of €4.8 bn in January 2016. Intra-euro area trade rose to €145.7 bn in January 2017, up by 10% compared with January 2016.

-

10:00

Eurozone: Trade balance unadjusted, January -0.6

-

09:34

Major stock markets in Europe trading mixed: DAX 12035.78 -47.40-0.39%, FTSE 7419.14 + 3.19 + 0.04%, CAC 5008.21 -5.17-0.10%

-

09:28

Italian trade balance declined significantly in January

In January 2017 seasonally-adjusted data, compared to December 2016, increased by 0.5% for outgoing flows and decreased by 0.2 for incoming flows. Exports increased for non EU countries (+2.8%) while decreased for EU countries (-1.3%).

The decrease of imports is the result of an increase for non EU countries (+1.7%) and a drop for EU countries (-1.5%). Over the last three months, seasonally-adjusted data, in comparison with the previous three months, showed a growth of 3.8% for exports and of 4.3% for imports.

-

08:09

Markets price in 46 percent probability that rates will be at 0.75-1.00 percent, 51 percent probability that rates will be at 1.00-1.25 percent, and 3 percent probability that rates will be at 1.25-1.50 percent at the June 14th FOMC meeting

-

07:33

Options levels on friday, March 17, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0876 (989)

$1.0856 (116)

$1.0828 (47)

Price at time of writing this review: $1.0767

Support levels (open interest**, contracts):

$1.0672 (296)

$1.0622 (590)

$1.0562 (665)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 39673 contracts, with the maximum number of contracts with strike price $1,1450 (4228);

- Overall open interest on the PUT options with the expiration date June, 9 is 41789 contracts, with the maximum number of contracts with strike price $1,0350 (3869);

- The ratio of PUT/CALL was 1.05 versus 1.02 from the previous trading day according to data from March, 16

GBP/USD

Resistance levels (open interest**, contracts)

$1.2612 (315)

$1.2516 (758)

$1.2420 (291)

Price at time of writing this review: $1.2327

Support levels (open interest**, contracts):

$1.2283 (223)

$1.2187 (348)

$1.2090 (561)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 13832 contracts, with the maximum number of contracts with strike price $1,3000 (1223);

- Overall open interest on the PUT options with the expiration date June, 9 is 16411 contracts, with the maximum number of contracts with strike price $1,1500 (3142);

- The ratio of PUT/CALL was 1.19 versus 1.21 from the previous trading day according to data from March, 16

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:22

Negative start of trading expected in major European stock markets: DAX -0.3%, CAC -0.1%, FTSE -0.1%

-

07:21

ANB AMRO says weakness in the gold price is over for now and a move back towards USD 1,250 is on the cards in the coming weeks

Markets were positioned for a more hawkish Fed in both of its tone and its dot plot but the Fed did not meet these expectations as instead signalled a gradual approach for rate tightening with only two more rate hikes this year, notes ANB AMRO Research.

On the FX front, ABN AMRO projects that the broad USD weakness post-FOMC is likely to persist over the coming days.

"It is likely that the US dollar rally has come to an end and that more downward pressure is building in the near-term," ABN AMRO adds.

ANB AMRO also thinks that weakness in the gold price is over for now and a move back towards USD 1,250 is on the cards in the coming weeks.

USD Index is trading at 100.41 and Gold is trading circa 1229.59 as of writing.

Source: ABN AMRO Research, efxnews.

-

07:14

Euro zone 10-year govt bond yields broadly higher, traders cite ECB's Nowotny comments

-

07:13

New Zealand's manufacturing sector saw activity increase in February

New Zealand's manufacturing sector saw activity increase in February after a dip in expansion during January, according to the BNZ - BusinessNZ Performance of Manufacturing Index (PMI).

The seasonally adjusted PMI for February was 55.2 (a PMI reading above 50.0 indicates that manufacturing is generally expanding; below 50.0 that it is declining). This was 3.0 points higher than January, and the highest level of expansion since September 2016. Overall, the sector has remained in expansion in almost all months since October 2012.

-

07:11

ECB Council member Nowotny told Handelsblatt that a "rate increase may be on the way"

-

06:32

Global Stocks

European stocks leapt to their strongest levels in more than a year Thursday, buoyed by a rally in mining shares, and after Dutch voters rebuffed Geert Wilders's far-right party in a general election.

U.S. stocks retreated Thursday to close lower, giving back some of the previous day's Federal Reserve-inspired gains as a fall for health-care and utilities stocks pushed the market into negative territory.

Investors in Asia turned cautious Friday ahead of a meeting of finance chiefs from the Group of 20 industrialized and emerging economies, where U.S. Treasury Secretary Steven Mnuchin is widely expected to pressure countries to boost the value of their currencies.

-