Market news

-

23:29

Commodities. Daily history for Mar 20’02’2017:

(raw materials / closing price /% change)

Oil 48.29 +0.15%

Gold 1,234.00 0.00%

-

23:28

Stocks. Daily history for Mar 20’2017:

(index / closing price / change items /% change)

TOPIX -6.84 1565.85 -0.43%

Hang Seng +192.06 24501.99 +0.79%

CSI 300 +3.80 3449.61 +0.11%

Euro Stoxx 50 -10.93 3437.48 -0.32%

FTSE 100 +4.85 7429.81 +0.07%

DAX -42.34 12052.90 -0.35%

CAC 40 -17.08 5012.16 -0.34%

DJIA -8.76 20905.86 -0.04%

S&P 500 -4.78 2373.47 -0.20%

NASDAQ +0.53 5901.53 +0.01%

S&P/TSX -48.17 15442.32 -0.31%

-

23:27

Currencies. Daily history for Mar 20’2017:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0736 -0,01%

GBP/USD $1,2357 -0,30%

USD/CHF Chf0,9985 +0,02%

USD/JPY Y112,49 -0,16%

EUR/JPY Y120,77 -0,19%

GBP/JPY Y139 -0,46%

AUD/USD $0,7728 +0,31%

NZD/USD $0,7052 +0,51%

USD/CAD C$1,3353 +0,06%

-

22:59

Schedule for today,Tuesday, Mar 21’2017 (GMT0)

00:30 Australia House Price Index (QoQ) Quarter IV 1.5%

00:30 Australia RBA Meeting's Minutes

06:45 Switzerland SECO Economic Forecasts

07:00 Switzerland Trade Balance February 4.7

09:30 United Kingdom Producer Price Index - Input (MoM) February 1.7% 0%

09:30 United Kingdom Producer Price Index - Output (MoM) February 0.6% 0.3%

09:30 United Kingdom HICP ex EFAT, Y/Y February 1.6% 1.7%

09:30 United Kingdom Retail prices, Y/Y February 2.6% 2.9%

09:30 United Kingdom Producer Price Index - Input (YoY) February 20.5% 20%

09:30 United Kingdom Retail Price Index, m/m February -0.6% 0.8%

09:30 United Kingdom Producer Price Index - Output (YoY) February 3.5% 3.7%

09:30 United Kingdom PSNB, bln February 9.82 -2.5

09:30 United Kingdom HICP, m/m February -0.5% 0.5%

09:30 United Kingdom HICP, Y/Y February 1.8% 2.1%

10:00 United Kingdom BOE Gov Mark Carney Speaks

10:00 U.S. FOMC Member Dudley Speak

11:00 United Kingdom CBI industrial order books balance March 8 4

12:30 Canada Retail Sales, m/m January -0.5% 1.1%

12:30 Canada Retail Sales YoY January 4.3%

12:30 Canada Retail Sales ex Autos, m/m January -0.3% 1.2%

12:30 U.S. Current account, bln Quarter IV -113 -128.2

16:00 U.S. FOMC Member Esther George Speaks

20:00 Canada Annual Budget

22:00 U.S. FOMC Member Mester Speaks

23:30 Australia Leading Index February 0.0%

23:50 Japan Monetary Policy Meeting Minutes

23:50 Japan Trade Balance Total, bln February -1087 822

-

21:45

New Zealand: Visitor Arrivals, February 1.8%

-

20:06

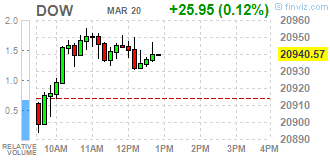

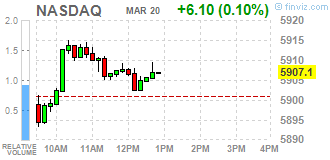

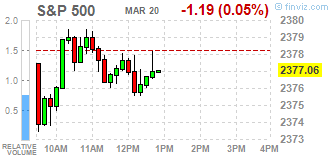

The main US stock indexes finished trading almost unchanged

Major US stock indexes finished the session near the zero mark, as growth in the consumer market was offset by a fall in the utility sector.

A certain impact on the mood of market participants had a fall in prices on the oil market, as well as the outcome of the meeting of the G20 countries, which ended at the weekend in Germany. Recall, the key point of the annual meeting of the G20 finance ministers was their inability to reach an agreement on protecting free trade and combating protectionism because of the US refusal to sign the document.

The cost of oil slightly declined amid fears of investors that a growing volume of oil production in the US could hamper OPEC's efforts to reduce production. Pressure on quotes also provided the latest data from Baker Hughes on the number of drilling rigs in the US. On Friday, Baker Hughes reported that from March 11 to 17, the number of active oil drilling rigs in the US increased to 631 units from 617 units.

The focus was also the statements of representatives of the Fed, namely Evans, Kashkari and Harker. Head of the Federal Reserve Bank of Chicago, Evans, said that this year the Fed can start raising rates faster against the backdrop of positive economic outlook. In the meantime, the head of the Federal Reserve Bank of Minneapolis Kashkari noted that since inflation is now below 2% and there is still uncertainty about the weakness of the market, there are prerequisites for a more cautious increase in rates. Meanwhile, FRB President Philadelphia Harker said that, probably, the Central Bank will continue to raise rates gradually throughout 2017. Harker also noted that the rate increase last week was appropriate given all the data on the economy.

The components of the DOW index have mostly grown (19 out of 30). Caterpillar Inc. was the growth leader. (CAT, + 2.70%). More shares fell The Home Depot, Inc. (HD, -1.09%).

Most sectors of the S & P index recorded a decline. The utilities sector fell most of all (-0.5%). The leader of growth was the consumer goods sector (+ 0.3%).

At closing:

Dow -0.04% 20,907.12 -7.50

Nasdaq + 0.01% 5,901.53 +0.53

S & P -0.20% 2,373.46 -4.79

-

19:00

DJIA -0.09% 20,895.83 -18.79 Nasdaq -0.15% 5,892.39 -8.61 S&P -0.30% 2,371.09 -7.16

-

17:00

European stocks closed: FTSE 100 +4.85 7429.81 +0.07% DAX -42.34 12052.90 -0.35% CAC 40 -17.08 5012.16 -0.34%

-

16:52

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Monday. The U.S. stock market has been on record-setting spree since the election of Donald Trump as president, but the rally has faltered in recent weeks as investors fret over the lack of clarity on his proposals to reform taxes and cut regulation.

Most of Dow stocks in positive area (18 of 30). Top loser - Visa Inc. (V, -1.13%). Top gainer - Caterpillar Inc. (CAT, +2.41%).

Most of S&P sectors in negative area. Top loser - Utilities (-0.5%). Top gainer - Consumer goods (+0.4%).

At the moment:

Dow 20883.00 +20.00 +0.10%

S&P 500 2372.75 -2.50 -0.11%

Nasdaq 100 5418.00 +9.50 +0.18%

Oil 49.12 -0.19 -0.39%

Gold 1232.80 +2.60 +0.21%

U.S. 10yr 2.48 -0.03

-

15:30

Oil prices pare losses, brent crude turns positive after Reuters reports OPEC support increases for extending oil supply cut

-

15:08

OPEC support increases for extending oil supply cut into H2 2017, but non-OPEC participation needed – OPEC sources

-

14:38

CIBC targets USD/CAD at 1.36 by the end of Q2, 1.39 by the end of Q3

The Canadian dollar reversed its course following the Fed's interest rate decision, seeing its greatest daily appreciation in a year but such gains are likely to fade in the near-term, says CIBC World Markets Research.

"Look for Governor Poloz to retain a dovish tilt in April, especially given that Trump-related risks have yet to be resolved," CIBC argues.

As such, CIBC argues that a few months the stronger post-Fed loonie will likely look like just a 'flash in the pan' on the way to an even weaker exchange rate.

CIBC targets USD/CAD at 1.36 by the end of Q2, and at 1.39 by the end of Q3.

Source: CIBC Economics - CIBC Capital Markets, efxnews.

-

14:00

It's OK if inflation overshoots target a bit as the labor markets tighten, Fed's Harker says - CNBC

-

13:31

U.S. Stocks open: Dow -0.05%, Nasdaq -0.03%, S&P -0.11%

-

13:19

Before the bell: S&P futures -0.18%, NASDAQ futures -0.05%

U.S. stock-index futures were flat, as investors lacked a catalyst to decisively move the major averages in one direction or the other.

Global Stocks:

Nikkei -

Hang Seng 24,501.99 +192.06 +0.79%

Shanghai 3,250.81 +13.36 +0.41%

FTSE 7,413.81 -11.15 -0.15%

CAC 5,013.10 -16.14 -0.32%

DAX 12,056.63 -38.61 -0.32%

Crude $48.05 (-1.50%)

Gold $1,230.80 (+0.05%)

-

12:58

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

192.65

0.29(0.15%)

550

ALTRIA GROUP INC.

MO

75.3

0.14(0.19%)

675

Amazon.com Inc., NASDAQ

AMZN

852.55

0.24(0.03%)

2494

AMERICAN INTERNATIONAL GROUP

AIG

62

-0.42(-0.67%)

1260

Apple Inc.

AAPL

140.31

0.32(0.23%)

97675

Barrick Gold Corporation, NYSE

ABX

18.97

0.12(0.64%)

14254

Caterpillar Inc

CAT

92.85

-0.06(-0.06%)

2674

Chevron Corp

CVX

107.81

0.13(0.12%)

924

Citigroup Inc., NYSE

C

60.05

-0.32(-0.53%)

17030

Exxon Mobil Corp

XOM

81.6

-0.40(-0.49%)

5800

Facebook, Inc.

FB

139.9

0.06(0.04%)

7809

Ford Motor Co.

F

12.49

0.01(0.08%)

11602

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

12.67

-0.09(-0.71%)

17358

General Electric Co

GE

29.9

0.02(0.07%)

558

General Motors Company, NYSE

GM

36.45

0.12(0.33%)

234

Goldman Sachs

GS

243

-0.94(-0.39%)

6089

Home Depot Inc

HD

149.3

-0.30(-0.20%)

5301

Intel Corp

INTC

35.36

0.09(0.26%)

12289

International Business Machines Co...

IBM

175.49

-0.16(-0.09%)

1537

Johnson & Johnson

JNJ

127.78

-0.28(-0.22%)

2729

JPMorgan Chase and Co

JPM

90.23

-0.45(-0.50%)

13568

Microsoft Corp

MSFT

65.01

0.14(0.22%)

1380

Nike

NKE

57.85

0.05(0.09%)

16215

Procter & Gamble Co

PG

91.04

0.04(0.04%)

1010

Starbucks Corporation, NASDAQ

SBUX

55.87

0.09(0.16%)

1042

Tesla Motors, Inc., NASDAQ

TSLA

261.35

-0.15(-0.06%)

14045

The Coca-Cola Co

KO

42.05

0.02(0.05%)

1837

Twitter, Inc., NYSE

TWTR

15.1

0.02(0.13%)

21949

Visa

V

90.48

0.24(0.27%)

1373

Wal-Mart Stores Inc

WMT

70.05

0.16(0.23%)

9099

Walt Disney Co

DIS

112.5

0.74(0.66%)

9910

Yahoo! Inc., NASDAQ

YHOO

46.71

0.12(0.26%)

192

Yandex N.V., NASDAQ

YNDX

23.43

-0.19(-0.80%)

601

-

12:58

Orders

EUR/USD

Offers: 1.0780 1.0800 1.0830 1.0850 1.0880 1.0900

Bids: 1.0750 1.0730 1.0700 1.0680 1.0650 1.0615-20 1.0600

GBP/USD

Offers: 1.2435 1.2445-50 1.2480 1.2500 1.2520 1.2550-55

Bids: 1.2400 1.2380 1.2365 1.2350 1.2330 1.2300 1.2285 1.2250 1.2200

EUR/JPY

Offers: 121.80 122.00 122.30 122.50 122.65 122.85 123.00

Bids: 121.00 120.75 120.50 120.30 120.00

EUR/GBP

Offers: 0.8720 0.8735 0.8750 0.8780-85 0.8800 0.8820 0.8850

Bids: 0.8665 0.8650 0.8630 0.8600 0.8580-85 0.8550 0.8520 0.8500

USD/JPY

Offers: 112.85 113.00 113.25-30 113.50 113.80 114.00 114.50

Bids: 112.45-50 112.30 112.00 111.85 111.65 111.50 111.00

AUD/USD

Offers: 0.7750 0.7780 0.7800 0.7830 0.785

Bids: 0.7700 0.7685 0.7665 0.7650 0.7600

Информационно-аналитический отдел TeleTrade

-

12:54

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Apple (AAPL) target raised to $155 from $135 at Cowen

-

12:40

Canadian wholesale sales rose 3.3% to a record high $59.1 billion in January

This was the largest monthly percentage gain since November 2009, when wholesale sales rose 3.8%. Sales were up in four of seven subsectors, representing 55% of total wholesale sales. The motor vehicle and parts subsector contributed the most to the gain.

In volume terms, wholesale sales increased 3.4%.

The motor vehicle and parts subsector recorded the largest gain in dollar terms in January, rising 17.1% to $11.9 billion, the first increase in three months. Excluding this subsector, wholesale sales increased 0.3% in January. Sales in the motor vehicle industry (+20.8%) rose to a record high, and accounted for most of the advance in the subsector. There were higher imports and exports of motor vehicles and parts in January, and motor vehicle manufacturing sales increased for a second consecutive month.

-

12:31

Sterling turns lower, falls almost half a cent to $1.2366

-

12:30

Canada: Wholesale Sales, m/m, January 3.3% (forecast 0.5%)

-

12:30

U.S.: Chicago Federal National Activity Index, February 0.34

-

12:11

European Commission says ready to begin Brexit negotiations

-

Tusk says will present EU 27 with draft Brexit negotiating guidelines within 48 hours from UK trigger

-

Everything is ready on this side", "we are waiting for notificaiton"

-

-

11:39

EU Told By Britain That It Will Announce On Monday It Will Trigger Art.50 Exit Clause On March 29 @LiveSquawk

-

10:50

German economy to grow by 1.6 pct in 2018 (1.6 pct workday adjusted) - Panel of Economic Advisers

-

2017 growth forecast by 0.1 pct point to 1.4 pct (1.7 pct workday adjusted)

-

Ecb should start winding down its bond-buying programme 'as soon as possible'

-

Expect german inflation to jump to 2.2 pct this year from 0.5 pct in 2016

-

German growth helped by robust labour market, positive outlook for global economy, higher state spending and ecb's 'still extremely' expansionary monetary policy

-

Trump's protectionist stance poses threat to international trade system, global economy

-

-

10:15

GBP/USD breaks major resistance at 1.2400. Retest expected

-

10:12

Wages and salaries per hour worked grew by 1.6% in the euro area

Hourly labour costs rose by 1.6% in the euro area (EA19) and by 1.7% in the EU28 in the fourth quarter of 2016, compared with the same quarter of the previous year. In the third quarter of 2016, hourly labour costs increased by 1.4% and 1.8% respectively. These figures are published by Eurostat, the statistical office of the European Union.

The two main components of labour costs are wages & salaries and non-wage costs. In the euro area, wages & salaries per hour worked grew by 1.6% and the non-wage component by 1.5%, in the fourth quarter of 2016 compared with the same quarter of the previous year. In the third quarter of 2016, the annual changes were +1.5% and +1.0% respectively. In the EU28, hourly wages & salaries rose by 1.8% and the non-wage component by 1.5% in the fourth quarter of 2016. In the third quarter of 2016, annual changes were +1.9% and +1.4% respectively.

-

09:36

Major stock exchanges in Europe started trading in the red zone: FTSE 7404.30 -20.66 -0.28%, DAX 12065.15 -30.09 -0.25%, CAC 5011.18 -18.06 -0.36%

-

09:35

Russia's finance minister says may buy up to $1 bln for current budget needs in 2017 - TASS

-

Good time to buy fx to fulfill ministry's commitments

-

Rouble overvalued

-

-

08:28

Gold long positions declined for second consecutive week. The net long position decreased by 27,647 contracts to +106K contracts - CFTC

-

08:13

Hungary's January gross wage growth 10 pct y/y vs 5.7 pct y/y in December - Stats

-

07:42

Barclays Capital FX Strategy now sees room for further near-term USD consolidation

Barclays Capital FX Strategy now sees room for further near-term USD consolidation in light of last week's 'unhurried' Fed which boosted risk assets and weakened the USD as the central bank seemed in no hurry to project a higher path of rate hikes next year.

In particular, Barclays expects further near-term USD weakness, concentrated primarily against high-yielding currencies.

"History suggests that this point in the Fed's tightening cycle is typically followed by further near-term USD weakness, stable equity prices and lower 10y UST yields," Barclays notes.

Barclays also continues to forecast two more rate hikes this year and three hikes in 2018 and expect to hear more from the committee about its balance sheet policies at the June FOMC.

Source: Barclays Research, efxnews.

-

07:38

Negative start of trading on the main European stock markets expected: DAX -0.3%, CAC -0.2%, FTSE -0.1%

-

07:32

Danish Central Bank says that for the first time in at least 183 years the Danish central government has no foreign currency loans

-

07:31

UK annual HPI rate of increase lowest since April 2013 at +2.3% - Rightmove

Annual rate of increase lowest since April 2013 at +2.3%, though overall demand remains strong:

-

Rightmove traffic at record January levels, with visits up 3% on January 2016's buy-to-let boosted period

-

Investor sectors understandably quieter than this time last year on number of properties coming to market and number of properties sold

-

Slower rate of price increases makes it riskier for sellers to over-price their property:

-

Analysis shows sellers are 40% more likely to sell if priced right when they first come to market

-

Three quarters of agents surveyed by Rightmove report price-sensitive markets with buyers reluctant to enquire if property is priced just a few percent too high

-

Price of property coming to market up 2.0% (+£5,986) this month, the smallest price rise at this time of year since February 2009

-

-

07:22

ECB Council member Visco: ECB could shorten break between of QE exit, rate hike

-

07:21

German producer prices for industrial products rose by 3.1%

In February 2017 the index of producer prices for industrial products rose by 3.1% compared with the corresponding month of the preceding year. This was the highest annual rate of change since December 2011 (+3.5%). In January 2017 the annual rate of change all over had been 2.4%.

Compared with the preceding month January 2017 the overall index rose by 0.2% in February 2017 (0.7% in January and 0.4% in December).

In February 2017 the price indices of all main industrial groups rose compared with February 2016: Energy prices increased by 5.4%, though prices of the different energy carriers diverged. Prices of petroleum products increased by 22.7%, whereas prices of natural gas (distribution) decreased by 7.5%. Prices of intermediate goods rose by 3.3%, prices of non-durable consumer goods by 2.3%. Prices of durable consumer goods increased by 1.1% and prices of capital goods by 0.9%.

-

07:00

Germany: Producer Price Index (YoY), February 3.1% (forecast 3.2%)

-

07:00

Germany: Producer Price Index (MoM), February 0.2% (forecast 0.3%)

-

06:30

Global Stocks

U.K. blue-chip stocks edged higher Friday, enough for the market to close at a second consecutive record high, as focus turned to the Group of 20 meeting of finance chiefs in Germany. Investors moved with caution Friday as the G-20 meeting of finance ministers and central bankers from the world's largest economies kicked off in the German spa town of Baden-Baden.

U.S. stocks edged lower on Friday but managed to post moderate weekly gains with investors awaiting further catalysts before jumping back into the market.

Equity markets kicked off the week lacking direction as investors digested news from the G-20 meeting over the weekend, while major U.S. indexes didn't provide much of a lead. As trading got underway, bearish sentiment reigned and volumes were lighter with Japan away on vacation; cautious investors stayed on the sidelines.

-

06:04

Options levels on monday, March 20, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0878 (989)

$1.0856 (116)

$1.0826 (47)

Price at time of writing this review: $1.0762

Support levels (open interest**, contracts):

$1.0659 (387)

$1.0610 (574)

$1.0582 (1096)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 39385 contracts, with the maximum number of contracts with strike price $1,1450 (3964);

- Overall open interest on the PUT options with the expiration date June, 9 is 43630 contracts, with the maximum number of contracts with strike price $1,0350 (4007);

- The ratio of PUT/CALL was 1.11 versus 1.05 from the previous trading day according to data from March, 17

GBP/USD

Resistance levels (open interest**, contracts)

$1.2710 (788)

$1.2613 (325)

$1.2517 (754)

Price at time of writing this review: $1.2390

Support levels (open interest**, contracts):

$1.2284 (223)

$1.2188 (358)

$1.2091 (541)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 13811 contracts, with the maximum number of contracts with strike price $1,3000 (1177);

- Overall open interest on the PUT options with the expiration date June, 9 is 16603 contracts, with the maximum number of contracts with strike price $1,1500 (3142);

- The ratio of PUT/CALL was 1.20 versus 1.19 from the previous trading day according to data from March, 17

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-