Noticias del mercado

-

16:38

RBA Governor Stevens: It's hard to wave away demand for the Australian dollar

-

Aussie housing is not in a risky category

-

Housing debt is significant

-

Housing slump would not lead to systemic risk and would not trigger bank failures

-

Stronger GDP growth rates would be welcomed

-

-

15:43

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.1100 (EUR 324m) 1.1200 (351m) 1.1250 (515m) 1.1300 (210m)

USD/JPY 103.00 (USD 246m)

GBP/USD 1.2600 (GBP 849m) 1.2950 (532m) 1.2995 (340m)

AUD/USD 0.7400 (AUD 200m) 0.7625 (279m) 0.7690 (210m) 0.7715 (311m)

USD/CAD 1.3150 (USD 250m)

NZD/USD 0.7180 (NZD 451m) 0.7200-01 (417m)

AUD/NZD 1.0600 (AUD 809m)

-

15:22

US Industrial production rose 0.7% in July

Industrial production rose 0.7 percent in July after moving up 0.4 percent in June. The advance in July was the largest for the index since November 2014. Manufacturing output increased 0.5 percent in July for its largest gain since July 2015. The index for utilities rose 2.1 percent as a result of warmer-than-usual weather in July boosting demand for air conditioning. The output of mining moved up 0.7 percent; the index has increased modestly, on net, over the past three months after having fallen about 17 percent between December 2014 and April 2016. At 104.9 percent of its 2012 average, total industrial production in July was 0.5 percent lower than its year-earlier level. Capacity utilization for the industrial sector increased 0.5 percentage point in July to 75.9 percent, a rate that is 4.1 percentage points below its long-run (1972-2015) average.

-

15:15

U.S.: Industrial Production (MoM), July 0.7% (forecast 0.3%)

-

15:15

U.S.: Industrial Production YoY , July -0.5%

-

15:15

U.S.: Capacity Utilization, July 75.9% (forecast 75.6%)

-

14:42

Dollar change course after Fed’s Dudley said: approaching Time For Rate Hikes

-

September hike is possible

-

Headline inflation is drifting up a bit

-

We seem to be on a trajectory for 2% inflation

-

Core inflation has been flat

-

Economy will be generally better in H2

-

If we raise rates this year it will be good news

-

Still expects more than one hike before the end of 2017

-

US Treasury yields are pretty low given the economic environment

-

Election won't weigh on Fed rate decisions

-

It's premature to talk about raising the Fed's inflation target

*via forexlive -

-

14:39

Canadian manufacturing sales rose 0.8%

Manufacturing sales rose 0.8% to $50.2 billion in June, following a 1.0% decline in May.

Higher sales of machinery and transportation equipment products were largely responsible for the gain. Nearly three-quarters of the increase in June was attributable to these two industries.

Overall, sales were up in 15 of 21 industries, representing 62% of the manufacturing sector. Durable goods rose 1.6% to $27.0 billion, while non-durable goods decreased 0.1% to $23.2 billion. Constant dollar sales increased 0.5%, indicating a higher volume of goods sold.

-

14:37

US CPI lower than forecasts. USD initially sold

The Consumer Price Index was unchanged in July on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index rose 0.8 percent before seasonal adjustment.

The energy index declined in July and the food index was unchanged. The index for all items less food and energy rose, but posted its smallest increase since March. As a result, the all items index was unchanged after rising in each of the 4 previous months.

The energy index fell 1.6 percent after rising in each of the last four months. The decline was due to a sharp decrease in the gasoline index; other energy indexes were mixed. The food at home index declined 0.2 percent as four of the six major grocery store food group indexes decreased, while the index for food away from home rose 0.2 percent.

The all items index rose 0.8 percent for the 12 months ending July, a smaller increase than the 1.0 percent rise for the 12 months ending June. Similarly, the index for all items less food and energy rose 2.2 percent for the 12 months ending July, a smaller increase than the 2.3 percent rise for the 12 months ending June.

-

14:30

U.S.: Building Permits, July 1152 (forecast 1160)

-

14:30

U.S.: CPI excluding food and energy, Y/Y, July 2.2% (forecast 2.3%)

-

14:30

U.S.: CPI, Y/Y, July 0.8% (forecast 0.9%)

-

14:30

U.S.: CPI, m/m , July 0% (forecast 0%)

-

14:30

U.S.: CPI excluding food and energy, m/m, July 0.1% (forecast 0.2%)

-

14:30

Canada: Manufacturing Shipments (MoM), June 0.8% (forecast 0.7%)

-

14:30

U.S.: Housing Starts, July 1211 (forecast 1180)

-

14:17

European session review: Euro and the pound rose against the US dollar

The following data was published:

(Time / country / index / period / previous value / forecast)

8:30 UK Producer Price Index (m / m) July 0.3% Revised to 0.2% 0.2% 0.3%

8:30 UK producers selling prices index, y / y in July -0.2% Revised to -0.4% 0% 0.3%

8:30 UK producers purchase prices index m / m in July 1.7% Revised to 1.8% 1% 3.3%

8:30 UK purchasing producer prices index, y / y in July -0.5% 4.3% 2%

8:30 UK Retail Price Index m / m in July to 0.4% -0.1% 0.1%

08:30 UK retail price index y / y in July 1.6% 1.7% 1.9%

8:30 UK Consumer Price Index m / m in July 0.2% -0.1% -0.1%

8:30 UK Consumer Price Index y / y in July 0.5% 0.5% 0.6%

8:30 UK consumer price index base value, y / y in July 1.4% 1.3% 1.3%

9:00 Eurozone index of sentiment in the business environment from the ZEW Institute in August -14.7 -6.3 4.6

9:00 The Eurozone trade balance, without seasonal adjustments in June 24.6 25.8 29.2

9:00 Germany Sentiment Index in the business environment of the institute ZEW August -6.8 2 0.5

The euro rose against the US dollar, supported by strong data on the index of sentiment in the business environment of the ZEW Institute in Germany and the euro zone.

The index of sentiment in the business environment from the ZEW Institute in Germany rose less than expected to 0.5 in August from -6.8 in July. The index was expected to rise to 2 in August.

Similarly, the current conditions rose to 57.6 compared to 49.8 in July. Economists had forecast that the indicator improved to 50.2.

"The indicator of economic sentiment from the ZEW partially recovered from Brexit shock," said ZEW President Achim Wambach.

"Political risks within and outside the European Union, however, continues to hamper a more optimistic economic outlook in Germany. In addition, uncertainty about the stability of the EU banking sector is maintained," said Wambach.

Economic confidence index in the euro zone rose by 19.3 points to 4.6 points in August. Increased by 2.1 points, the current economic situation indicator reached a value of minus 10.3 points in August.

The pound rose against the US dollar after the release of positive inflation data while the demand for the US currency remained under pressure.

In the UK, inflation increased slightly in July to its highest level since November 2014, showed the Office for National Statistics on Tuesday.

Consumer prices rose 0.6 percent year on year in July, after rising 0.5 percent in June. Economists had forecast that inflation will remain at 0.5 percent.

On a monthly basis, consumer prices fell by 0.1 percent, as expected, which was the first drop in six months. In June, prices rose by 0.2 percent.

Core inflation, which excludes energy, food, alcoholic beverages and tobacco, slowed slightly to 1.3 percent in July compared with 1.4 percent in June.

Another ONS report shows that manufacturers selling prices increased for the first time since June, 2014. Prices for finished goods advanced by 0.3 percent year on year, after a decline by 0.2 percent in June. Prices were expected to remain unchanged in July.

On a monthly basis, producer prices rose 0.3 percent in July, showing the same growth rate as in June and slightly faster than expected growth of 0.2 percent.

At the same time, the purchase prices have increased markedly by 4.3 percent per year after easing 0.5 percent a month ago, and also faster than the expected 2 percent rise.

The monthly increase in purchase prices accelerated to 3.3 percent from 1.7 percent. Economists had forecast an increase of 1 percent.

Comments by president of the Federal Reserve of San Francisco John Williams led to a large-scale reduction in the US dollar on Tuesday.

On Monday he said that the central bank executives should either increase the target level of inflation, which currently stands at 2%, and start using any new reference-based pricing levels or on the economic growth.

A higher target for inflation rate may give the Fed more room to keep the interest rates at current levels.

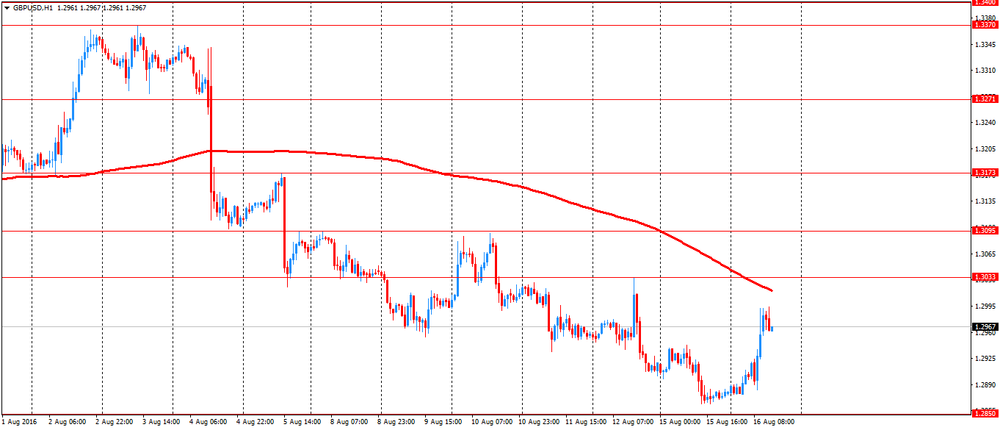

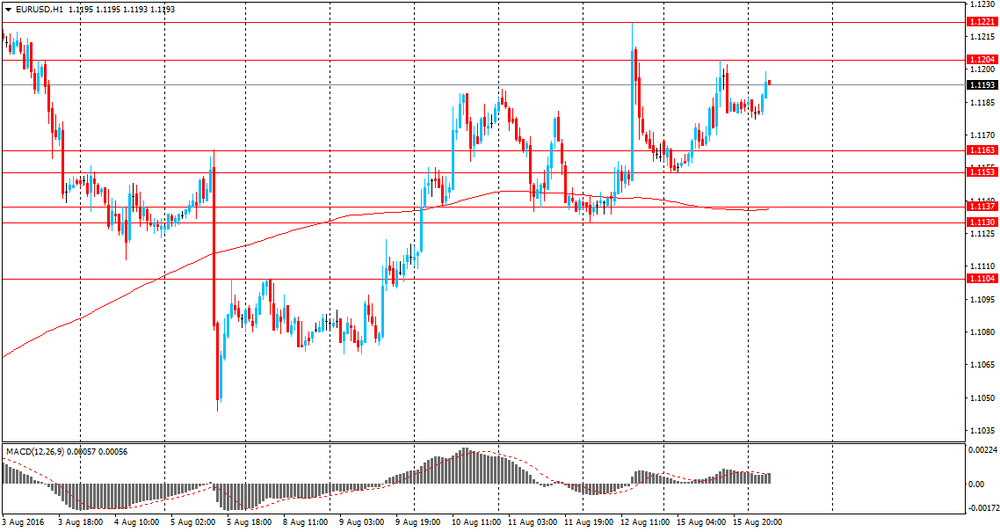

EUR / USD: during the European session, the pair rose to $ 1.1303

GBP / USD: during the European session, the pair rose to $ 1.2994

USD / JPY: during the European session, the pair fell to Y99.79

-

13:48

Orders

EUR/USD

Offers : 1.1250-60 1.1280 1.1300-05 1.1325-30 1.1350 1.1365 1.1380 1.1400

Bids : 1.1200 1.1200 1.1185 1.1150 1.1130 1.1115 1.1100 1.1070 1.1050-55

GBP/USD

Offers : 1.2920-25 1.2950 1.2980 1.3000 1.3020-25 1.3065 1.3080 1.3095-05

Bids : 1.2880 1.1265 1.2850 1.2830 1.2800 1.2780 1.2750 1.2730 1.2700

EUR/GBP

Offers : 0.8725-30 0.8750 0.8765 0.8785 0.8800 0.8830 0.8860

Bids : 0.8700 0.8680 0.8650 0.8620 0.8600 0.8585 0.8570 0.8550

EUR/JPY

Offers : 113.00 113.25 113.50 113.80 114.00 114.50

Bids : 112.50 112.30 112.00-10 111.85 111.50 111.00

USD/JPY

Offers : 100.50-60 100.80 101.00 101.25-30 101.50 101.80 102.00

Bids : 100.00 99.85 99.50 99.30 99.00 98.80 98.50 98.00

AUD/USD

Offers : 0.7720 0.7750-55 0.7785 0.7800

Bids : 0.7700 0.7685 0.7660 0.7635-40 0.7620 0.7600 0.7585 0.7565

-

12:24

USD/JPY: Around Post-BoJ Lows: What's Next? - Barclays

USDJPY remained largely range-bound around the post-BoJ lows of 101-102 in a quiet summer week with a Japanese public holiday last Thursday. Although the BoJ disappointment against some excessive easing expectations is weighing on USDJPY, the BoJ did double up its annual ETF purchases to JPY6trn from JPY3.3trn. This is likely supporting Nikkei and USDJPY, given their correlations; furthermore, expectations of further easing at September's BoJ meeting will likely persist as the BoJ conducts comprehensive reviews.

A notable move this week was in 3m USDJPY basis, which has now completely reversed the post-BoJ tightening. However, as we noted in No breakthrough from BoJ, 29 July, the BoJ's USD Funds-Supplying Operations under central bank FX swap lines are an emergency liquidity backstop rather than a pool of USD liquidity for Japanese investors to tap to fund foreign bond investments. Indeed, the outstanding balance of the CB swap line as of 10 August declined to zero from a very small positive in previous weeks.

We believe solid portfolio rebalancing outflows and upcoming MMF reform will likely to continue to exert widening pressure on short-end USDJPY basis.

Target: USD/JPY at 92 by end of Q3 and at 87 by end of the year".

Copyright © 2016 Barclays Capital, eFXnews™

-

11:10

Economic Sentiment for Germany gained 7.3 points in August

The ZEW Indicator of Economic Sentiment for Germany increased in August 2016. The index gained 7.3 points compared to the previous month, now standing at 0.5 points (long-term average: 24.2 points). "The ZEW Indicator of Economic Sentiment has partly recovered from the Brexit shock. Political risks within and outside the European Union, however, continue to inhibit a more optimistic economic outlook for Germany. Furthermore, uncertainty about the resilience of the EU banking sector persists," comments ZEW-President Professor Achim Wambach.

-

11:04

Euro area trade balance surplus increased in June

The first estimate for euro area (EA19) exports of goods to the rest of the world in June 2016 was €178.8 billion, a decrease of 2% compared with June 2015 (€182.8 bn). Imports from the rest of the world stood at €149.5 bn, a fall of 5% compared with June 2015 (€157.4 bn). As a result, the euro area recorded a €29.2 bn surplus in trade in goods with the rest of the world in June 2016, compared with +€25.5 bn in June 2015. Intra-euro area trade fell to €150.2 bn in June 2016, down by 1% compared with June 2015. These data are released by Eurostat, the statistical office of the European Union.

-

11:01

Eurozone: ZEW Economic Sentiment, August 4.6 (forecast -6.3)

-

11:00

Germany: ZEW Survey - Economic Sentiment, August 0.5 (forecast 2)

-

11:00

Eurozone: Trade balance unadjusted, June 29.2 (forecast 25.8)

-

10:45

Producer prices in UK rose 3.3% in July

The price of goods bought and sold by UK manufacturers, as estimated by the Producer Price Index, rose in the year to July 2016 following 2 years of falls.

Factory gate prices (output prices) for goods produced by UK manufacturers rose 0.3% in the year to July 2016, compared with a fall of 0.2% in the year to June 2016.

This is the first time that factory gate prices have increased on the year since June 2014. The index has been following an upward trend since August 2015. The increase of 0.3% in the year to July 2016 is therefore a continuation of the trend over the past 11 months.

Core factory gate prices, which exclude the more volatile food, beverage, tobacco and petroleum products, rose 1.0% in the year to July 2016, compared with a rise of 0.7% in the year to June 2016.

The overall price of materials and fuels bought by UK manufacturers for processing (total input prices) rose 4.3% in the year to July 2016, compared with a fall of 0.5% in the year to June 2016.

Similar to factory gate prices, total input prices have also been following an upward trend in recent months. With the exception of April 2016, the annual rate has been trending upwards since November 2015.

-

10:44

The big week for GBP started well as all indicators reported today show values above expectations. Will the markets start to reduce the stimulus expectations?

-

10:40

House prices in UK rose more than forecast

- the average price of a property in the UK was £213,927

- the annual price change for a property in the UK was 8.7%

- the monthly price change for a property in the UK was 1.0%

- the monthly index figure for the UK was 112.2 (January 2015 = 100)

Continuing price pressures in the housing market reflect stronger demand relative to supply in the housing market. However, there are also indications that the housing market pressure softened recently, with falls in both demand and supply.

-

10:38

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.1100 (EUR 324m) 1.1200 (351m) 1.1250 (515m) 1.1300 (210m)

USD/JPY 103.00 (USD 246m)

GBP/USD 1.2600 (GBP 849m) 1.2950 (532m) 1.2995 (340m)

AUD/USD 0.7400 (AUD 200m) 0.7625 (279m) 0.7690 (210m) 0.7715 (311m)

USD/CAD 1.3150 (USD 250m)

NZD/USD 0.7180 (NZD 451m) 0.7200-01 (417m)

AUD/NZD 1.0600 (AUD 809m)

-

10:36

UK’s inflation after Brexit was strong. GBP/USD on the rise

The reporting period for this release covers the calendar month of July 2016, therefore, the data refers to the period after the EU referendum.

The Consumer Prices Index (CPI) rose by 0.6% in the year to July 2016, compared with a 0.5% rise in the year to June.

Although the small increase in the rate between June 2016 and July 2016 takes it to the highest seen since November 2014, it is still relatively low in the historic context.

The main contributors to the increase in the rate were rising prices for motor fuels, alcoholic beverages and accommodation services, and a smaller fall in food prices than a year ago.

These upward pressures were partially offset by falls in social housing rent, and falling prices for certain games and toys.

CPIH (not a National Statistic) rose by 0.9% in the year to July 2016, up from 0.8% in June.

-

10:32

United Kingdom: Producer Price Index - Output (YoY) , July 0.3% (forecast 0%)

-

10:32

United Kingdom: Producer Price Index - Output (MoM), July 0.3% (forecast 0.2%)

-

10:32

United Kingdom: Producer Price Index - Input (MoM), July 3.3% (forecast 1%)

-

10:32

United Kingdom: Producer Price Index - Input (YoY) , July 4.3% (forecast 2%)

-

10:30

United Kingdom: Retail Price Index, m/m, July 0.1% (forecast -0.1%)

-

10:30

United Kingdom: HICP, Y/Y, July 0.6% (forecast 0.5%)

-

10:30

United Kingdom: Retail prices, Y/Y, July 1.9% (forecast 1.7%)

-

10:30

United Kingdom: HICP, m/m, July -0.1% (forecast -0.1%)

-

10:30

United Kingdom: HICP ex EFAT, Y/Y, July 1.3% (forecast 1.3%)

-

10:03

China’s State Administration of Foreign Exchange: Brexit and seasonal factors increased demand for FX in July

-

impact on FX supply and demand remains under control

-

pace of companies reduction of foreign debt continues to slow

-

cross border capital flows remain stable in the medium to long term

-

-

09:16

Today’s events:

At 15:30 GMT the United States will hold an auction of 4-week bills

At 16:30 GMT Statement by US Fed's Dennis Lockhart

At 20:30 GMT the report of the American Petroleum Institute (API) on oil stocks

-

09:13

Asian session review: the dollar weakened

During the Asian session, the yen strengthened against the dollar and other major currencies. According to some analysts the decline of USD / JPY to a one-month low could be due to low trading volumes and sales by exporters. During the session the pair reached the Y100,20 level.

Also the weakening dollar hit by the extremely weak data on US retail sales, which increased doubts about the fact that the economy is not so strong that the Fed will raise interest rates soon. According to the futures market, the probability of a Fed hike in September is 12%. Meanwhile and in December is estimated at 41.3% against 44.9% on Friday.

Now, investors' attention shifted to today's report on inflation in the US. In addition, on Wednesday are expected the protocols of the July FOMC meeting, which could also shed light on the central bank's plans for the timing of rate hikes.

The pound fell against the US dollar. Later this week, economists will monitor the British inflation data, the number of applications for unemployment benefits, and retail sales for July to assess the initial effects of Brexit. Recall before the referendum GDP growth in the UK expected to be close to 0.6%, but now economists surveyed by Reuters forecast that the economy will shrink by 0.1%. If the estimates are confirmed, the UK economy will be in a technical recession. Reuters surveys also showed that, on average, analysts expect the Central Bank of England to cut rates by only 0.1% at the meeting in November.

The Australian dollar fell on negative data on vehicle sales in Australia. According to the report by the Australian Bureau of Statistics, in July, sales of new vehicles fell by 1.3%, after rising 3.5% in June. The value in June was revised from 3.1%. The annual sales on year increased by 1.6%, but the rate was lower than the previous value of 2.6%. The report on sales of new vehicles reflects the number of sales of new vehicles and is an indicator of consumer confidence.

During the session, the Australian currency gained after the publication RBA minutes as well as the weakening of the US dollar.

As stated in the minutes of the July meeting of the RBA, there is potential for faster growth in the Australian economy. Also in the minutes was noted that credit growth and housing prices slowed and recent inflation data confirm the weakening of inflation. RBA forecast GDP growth to be higher than the potential in the mid-2017

EUR / USD: during the Asian session, the pair was trading in $ 1.1180-1.1230 range

GBP / USD: during the Asian session, the pair was trading in $ 1.2880-1.2915 range

USD / JPY: the pair fell to Y100.20

-

08:30

Options levels on tuesday, August 16, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1339 (4543)

$1.1306 (4988)

$1.1255 (3344)

Price at time of writing this review: $1.1214

Support levels (open interest**, contracts):

$1.1141 (1825)

$1.1091 (3291)

$1.1021 (5378)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 50303 contracts, with the maximum number of contracts with strike price $1,1250 (4988);

- Overall open interest on the PUT options with the expiration date September, 9 is 56185 contracts, with the maximum number of contracts with strike price $1,1000 (5811);

- The ratio of PUT/CALL was 1.12 versus 1.11 from the previous trading day according to data from August, 15

GBP/USD

Resistance levels (open interest**, contracts)

$1.3203 (2253)

$1.3105 (1278)

$1.3008 (979)

Price at time of writing this review: $1.2899

Support levels (open interest**, contracts):

$1.2791 (2439)

$1.2694 (1153)

$1.2597 (728)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 31944 contracts, with the maximum number of contracts with strike price $1,3300 (2500);

- Overall open interest on the PUT options with the expiration date September, 9 is 25903 contracts, with the maximum number of contracts with strike price $1,2800 (2439);

- The ratio of PUT/CALL was 0.81 versus 0.81 from the previous trading day according to data from August, 15

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:20

GBPUSD has to break the 1.2798 Brexit low to gather downside momentum - Morgan Stanley

"GBPUSD has to break the 1.2798 Brexit low to gather downside momentum taking its closer towards our 1.24 target.

The July RICS house price index fell 1.2% which should not surprise. The 'Sunday Times' suggested the British government may be not anywhere near in its logistical efforts to draw Article 50 as the government's 'Brexit department' run by Davis is not yet functional. Sources close to the British government also cite French and German General Elections, due in May and October respectively as stumbling blocks.

All in all, there seems to be no desire to draw Article 50 early. Hence Brexit negotiations will be delayed. When Theresa May speaks at the Conservative Party Conference next month she may address her plans and time table for the start of the Brexit negotiations. BoE's chief economist Haldane laid down the reasoning for the BoE's drastic monetary policy response suggesting that 'hundreds of thousands' of jobs were at risk

Therefore we will put little attention towards the July retail sales report due on Thursday. Within the post Brexit world it is the supply side of the economy what matters. Due to the delayed labour market response, retail sales could hold up for longer, but this would come at the prices of a further widening of the British 7% current account deficit.

*Morgan Stanley maintains a short GBP/USD position from around 1.3107 targeting a move to 1.24".

-

08:09

Car sales in Australia stable

The July 2016 trend estimate an increased by 0.1% when compared with June 2016. When comparing national trend estimates for July 2016 with June 2016, sales for passenger vehicles increased by 0.4% and sales for Other vehicles decreased by 0.4%. There was no movement in sales for sports utility vehicles. The largest upward movement across all states and territories, on a trend basis, was in Victoria (0.5%), continuing an upward trend which commenced in March 2016.

-

08:05

RBA minutes: additional stimulus likely would aid the prospects for the country's economic

Members of the Reserve Bank of Australia's monetary policy board said that additional stimulus likely would aid the prospects for the country's economic, minutes from the central bank's August 2 revealed on Tuesday.

Inflation was below the target range and was expected to remain there for the foreseeable future, giving the bank the means to cut rates.

Inflation was just 1 percent in the June quarter, well below the RBA's target band of 2-3 percent.

"Underlying inflation was expected to remain low for a time before picking up gradually as spare capacity in labor and many product markets diminished," the minutes said.

In particular, it was weakness in the housing market that convinced the board to take action.

At the meeting, the board trimmed its benchmark lending rate by 25 basis points, to a fresh record low 1.50 percent from 1.75 percent following two months of no action.

The bank last reduced its rate by 25 basis points in May, which was the first reduction in a year.

The RBA noted the possibility that it may not be the only bank to provide stimulus.

"Monetary policy had continued to be highly accommodative in most economies and there was a reasonable likelihood of further stimulus by a number of the major central banks," the minutes said. - RTT

-

03:31

Australia: New Motor Vehicle Sales (MoM) , July -1.3%

-

03:31

Australia: New Motor Vehicle Sales (YoY) , July 1.6%

-

00:28

Currencies. Daily history for Aug 15’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1183 +0,21%

GBP/USD $1,2880 -0,30%

USD/CHF Chf0,9729 -0,16%

USD/JPY Y101,26 +0,02%

EUR/JPY Y113,24 +0,17%

GBP/JPY Y130,41 -0,33%

AUD/USD $0,7673 +0,31%

NZD/USD $0,7215 +0,28%

USD/CAD C$1,2926 -0,22%

-

00:02

Schedule for today,Tuesday, Aug 16’2016

(time / country / index / period / previous value / forecast)

01:30 Australia New Motor Vehicle Sales (MoM) July 3.1%

01:30 Australia New Motor Vehicle Sales (YoY) July 2.1%

01:30 Australia RBA Meeting's Minutes

08:30 United Kingdom Producer Price Index - Output (MoM) July 0.2% 0.2%

08:30 United Kingdom Producer Price Index - Output (YoY) July -0.4% 0%

08:30 United Kingdom Producer Price Index - Input (MoM) July 1.8% 1%

08:30 United Kingdom Producer Price Index - Input (YoY) July -0.5% 2%

08:30 United Kingdom Retail Price Index, m/m July 0.4% -0.1%

08:30 United Kingdom Retail prices, Y/Y July 1.6% 1.7%

08:30 United Kingdom HICP, m/m July 0.2% -0.1%

08:30 United Kingdom HICP, Y/Y July 0.5% 0.5%

08:30 United Kingdom HICP ex EFAT, Y/Y July 1.4% 1.3%

09:00 Eurozone ZEW Economic Sentiment August -14.7

09:00 Eurozone Trade balance unadjusted June 24.6

09:00 Germany ZEW Survey - Economic Sentiment August -6.8 2

12:30 Canada Manufacturing Shipments (MoM) June -1% 0.9%

12:30 U.S. Building Permits July 1153 1160

12:30 U.S. Housing Starts July 1189 1180

12:30 U.S. CPI, m/m July 0.2% 0.1%

12:30 U.S. CPI, Y/Y July 1% 1%

12:30 U.S. CPI excluding food and energy, m/m July 0.2% 0.2%

12:30 U.S. CPI excluding food and energy, Y/Y July 2.3% 2.3%

13:15 U.S. Capacity Utilization July 75.4% 75.6%

13:15 U.S. Industrial Production (MoM) July 0.6% 0.2%

13:15 U.S. Industrial Production YoY July -0.7%

22:45 New Zealand PPI Input (QoQ) Quarter II -1%

22:45 New Zealand PPI Output (QoQ) Quarter II -0.2%

22:45 New Zealand Employment Change, q/q Quarter II 1.2% 0.7%

22:45 New Zealand Unemployment Rate Quarter II 5.2% 5.2%

-