Noticias del mercado

-

22:07

Major US stock indexes finished trading with a decrease

Major US stock indexes fell moderately Tuesday amid mixed economic data and comments of a number of Fed officials.

According to the Ministry of Labor, consumer prices in the US remained unchanged in July, after rising 0.2% in June and May, as the cost of gasoline has fallen for the first time in five months. At the same time, core inflation has been moderate, which can further reduce prospects for increasing interest rates the Fed this year. During the 12 months to July, the consumer price index rose by 0.8% after rising 1.0 percent in June. Economists forecast that the consumer price index will be unchanged last month and will increase by 0.9% compared to last year. The so-called core CPI, which excludes food and energy, rose by 0.1% in July. The base consumer price index increased by 2.2% after rising by 2.3% year on year.

At the same time, the establishment of new homes in July rose to 1211 thousand. Against 1189 thousand. And June, and analysts forecast at the level of 1180 thousand. At the same time, the number of building permits dropped to 1152 thousand. To 1153 thousand. Analysts expected 1160 thousand.

In addition, the industrial production growth rate in the US in July accelerated to 0.7% after rising 0.6% in June. Analysts expected an increase of 0.3%. Compared to July of the previous year, industrial production fell by 0.5% after declining by 0.7% y / y in the previous month.

With regard to the statements made by the Fed, Dudley noted that allows increase in the interest rate the Federal Reserve is already September. "We are approaching the moment when it is appropriate to re-raise the rate, - said Dudley -. In US employment in the last 3 months is growing at an average rate at the level of 190 thousand per month, and economic growth should accelerate in the 2nd half of the year we started.. see the signals accelerating wage growth. overall, the US economy is in good condition. "

Meanwhile, the head of the Federal Reserve Bank of Atlanta, Lockhart said that optimistic about the economic outlook, and therefore feel justified in raising rates. He added that the weak data on US GDP for the 2nd quarter should be viewed in the context of other factors. "Most of the fundamental factors right now a positive effect on consumer spending in the United States," - he said, adding that he remains confident in the prospects for the economy in the 2nd half of 2016 and 2017.

Gradually, investors' attention shifted to the protocols of the July meeting of the Fed, which could shed light on the Central Bank plans for the timing of rate hikes.

Most DOW components of the index closed in negative territory (21 of 30). Most remaining shares rose Intel Corporation (INTC, + 0.40%). Outsider were shares of Johnson & Johnson (JNJ, -1.44%).

Almost all sectors of the S & P index fell. The leader turned out to be the basic materials sector (+ 0.4%). Most utilities sector fell (-1.0%).

At the close:

Dow -0.45% 18,552.19 -83.86

Nasdaq -0.66% 5,227.11 -34.91

S & P -0.55% 2,178.18 -11.97

-

21:00

Dow -0.30% 18,580.59 -55.46 Nasdaq -0.46% 5,237.97 -24.05 S&P -0.37% 2,182.02 -8.13

-

18:00

European stocks closed: FTSE 100 -47.27 6893.92 -0.68% DAX -62.56 10676.65 -0.58% CAC 40 -37.42 4460.44 -0.83%

-

17:36

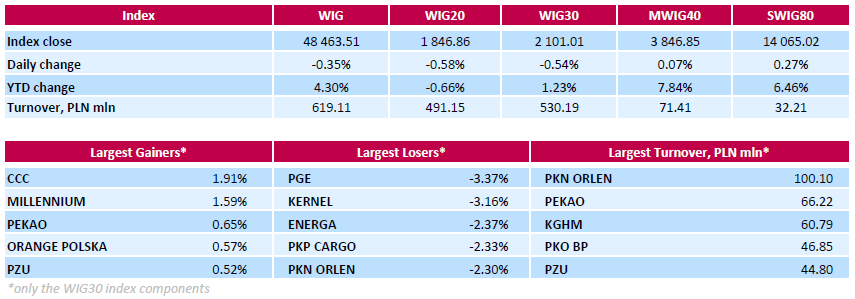

WSE: Session Results

Polish equity market closed lower on Tuesday. The broad market benchmark, the WIG Index, dropped by 0.35%. Sector-wise, utilities names (-2.31%) were the worst-performing group, while telecommunication sector stocks (+0.47%) outpaced.

The large-cap stocks' measure, the WIG30 Index, fell by 0.54%. In the index basket, genco PGE (WSE: PGE) led the underperformers with a 3.37% drop, followed by agricultural producer KERNEL (WSE: KER) plunging by 3.16%. Other largest decliners were genco ENERGA (WSE: ENG), railway freight transport operator PKP CARGO (WSE: PKP) and oil refiner PKN ORLEN (WSE: PKN), losing between 2.3% and 2.37%. It should be noted that ENERGA, reportedly, may start negotiations with its bondholders in September over covenants requiring that net debt to EBITDA ratio does not exceed 3.5, as the plan to revive investment in the coal-fueled power plant in Ostroleka had triggered a risk that the covenants could be breached. On the other side of the ledger, footwear retailer CCC (WSE: CCC) and bank MILLENNIUM (WSE: MIL) were the session's best performers, jumping by 1.91% and 1.59% respectively.

-

17:14

Wall Street. Major U.S. stock-indexes slightly fell

Wall Street sharply lower on Tuesday, with indexes pulling away from record levels, after New York Federal Reserve President William Dudley said an interest rate in September was possible.

Most of all Dow stocks in negative area (26 of 30). Top gainer - The Home Depot, Inc. (HD, +0.56%). Top loser - Intel Corporation (INTC, -1.19%).

Most of S&P sectors also in negative area. Top gainer - Basic Materials (+0.2%). Top loser - Utilities (-0.7%).

At the moment:

Dow 18540.00 -42.00 -0.23%

S&P 500 2178.50 -7.50 -0.34%

Nasdaq 100 4802.75 -20.00 -0.41%

Oil 45.95 +0.21 +0.46%

Gold 1351.80 +4.30 +0.32%

U.S. 10yr 1.58 +0.03

-

15:44

WSE: After start on Wall Street

Today we have very interesting situation for the US dollar. In the first part of the day USD lost clearly against most major currencies, generally without much fundamental reason and sentiment towards USD was so clearly weak and was also supported by data from the US, which, especially for inflation, surprised slightly negative. After a few minutes after the data appeared words of important representative of the Federal Reserve, William Dudley, head of the New York Fed, which stated that approaching the time for a rate hike and it does not interfere with the presidential elections. This strengthened slightly the dollar. These types of statements are detrimental to the Warsaw Stock Exchange, because it may reduce the inflow of funds to the parquets of stock exchanges in emerging markets. The next set of US data concerning industrial production (+0,7% m/m) was more consistent with the vision of William Dudley about the possibility of rate hike in September. The market in the United States began from discount of 0.25%, what may be a result of fears about a rate hike in September, as previously was not expected.

-

15:33

U.S. Stocks open: Dow -0.30%, Nasdaq -0.26%, S&P -0.26%

-

15:29

Before the bell: S&P futures -0.24%, NASDAQ futures -0.22%

U.S. stock-index futures fell.

Global Stocks:

Nikkei 16,596.51 -273.05 -1.62%

Hang Seng 22,910.84 -21.67 -0.09%

Shanghai 3,110.48 -14.72 -0.47%

FTSE 6,922.63 -18.56 -0.27%

CAC 4,468.58 -29.28 -0.65%

DAX 4,468.58 -29.28 -0.65%

Crude $44.77 (+0.63%)

Gold $1345.50 (+0.17%)

-

14:53

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

180.56

-0.00(-0.00%)

6690

ALCOA INC.

AA

10.54

0.02(0.1901%)

76468

ALTRIA GROUP INC.

MO

66.1

-0.16(-0.2415%)

715

Amazon.com Inc., NASDAQ

AMZN

767.61

-0.88(-0.1145%)

13199

American Express Co

AXP

65.6

-0.03(-0.0457%)

373691

AMERICAN INTERNATIONAL GROUP

AIG

59.22

0.00(0.00%)

246421

Apple Inc.

AAPL

109.64

0.16(0.1461%)

209632

AT&T Inc

T

43.02

0.00(0.00%)

3520

Barrick Gold Corporation, NYSE

ABX

21.73

0.22(1.0228%)

81440

Boeing Co

BA

134.66

0.00(0.00%)

168001

Caterpillar Inc

CAT

84.1

-0.05(-0.0594%)

7287

Chevron Corp

CVX

102.73

-0.04(-0.0389%)

5021

Cisco Systems Inc

CSCO

31.2

0.01(0.0321%)

9263

Citigroup Inc., NYSE

C

46.25

-0.14(-0.3018%)

820

Deere & Company, NYSE

DE

78.28

0.00(0.00%)

29728

E. I. du Pont de Nemours and Co

DD

68.64

0.00(0.00%)

232952

Exxon Mobil Corp

XOM

88

0.19(0.2164%)

2119

Facebook, Inc.

FB

123.6

-0.30(-0.2421%)

56398

FedEx Corporation, NYSE

FDX

166.4

0.00(0.00%)

6924

Ford Motor Co.

F

12.43

0.00(0.00%)

25382

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

12.35

0.18(1.479%)

131839

General Electric Co

GE

31.23

-0.01(-0.032%)

4735

General Motors Company, NYSE

GM

31.37

-0.49(-1.538%)

1700

Goldman Sachs

GS

164.9

-0.65(-0.3926%)

600

Google Inc.

GOOG

781

-1.44(-0.184%)

1109

Hewlett-Packard Co.

HPQ

14.52

0.00(0.00%)

52519

Home Depot Inc

HD

137.31

0.25(0.1824%)

135104

HONEYWELL INTERNATIONAL INC.

HON

116.84

0.00(0.00%)

44123

Intel Corp

INTC

34.91

0.00(0.00%)

586032

International Business Machines Co...

IBM

161.62

-0.26(-0.1606%)

2453

International Paper Company

IP

46.32

0.00(0.00%)

79595

Johnson & Johnson

JNJ

122.53

0.22(0.1799%)

624418

JPMorgan Chase and Co

JPM

65.4

-0.32(-0.4869%)

22053

McDonald's Corp

MCD

118.2

-0.32(-0.27%)

2048

Merck & Co Inc

MRK

63

-0.32(-0.5054%)

685

Microsoft Corp

MSFT

57.78

0.02(0.0346%)

6999

Nike

NKE

57.12

0.35(0.6165%)

3719

Pfizer Inc

PFE

35.02

-0.09(-0.2563%)

1132

Procter & Gamble Co

PG

86.71

-0.31(-0.3562%)

770

Starbucks Corporation, NASDAQ

SBUX

55.24

-0.01(-0.0181%)

2389

Tesla Motors, Inc., NASDAQ

TSLA

225.07

-0.52(-0.2305%)

11135

The Coca-Cola Co

KO

44.28

0.04(0.0904%)

248162

Travelers Companies Inc

TRV

118.35

0.00(0.00%)

16794

Twitter, Inc., NYSE

TWTR

20.67

-0.19(-0.9108%)

112743

United Technologies Corp

UTX

109.69

0.00(0.00%)

39165

UnitedHealth Group Inc

UNH

141.54

-0.08(-0.0565%)

79749

Verizon Communications Inc

VZ

53.73

0.12(0.2238%)

193

Visa

V

80.75

-0.16(-0.1978%)

203584

Wal-Mart Stores Inc

WMT

72.82

-0.50(-0.6819%)

11479

Walt Disney Co

DIS

97

-0.10(-0.103%)

1341

Yahoo! Inc., NASDAQ

YHOO

42.35

-0.32(-0.7499%)

28110

Yandex N.V., NASDAQ

YNDX

23.43

0.02(0.0854%)

1600

-

14:41

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

JPMorgan Chase (JPM) downgraded to Market Perform from Outperform at Bernstein

Other:

Home Depot (HD) reiterated with an Outperform at TAG; target $150

IBM (IBM) initiated with a Perform at Oppenheimer

-

13:51

Company News: Home Depot (HD) Q2 EPS beat analysts’ estimate

Home Depot reported Q2 FY 2017 earnings of $1.98 per share (versus $1.71 in Q2 FY 2016), beating analysts' consensus estimate of $1.97.

The company's quarterly revenues amounted to $26.472 bln (+6.6% y/y), generally in-line with analysts' consensus estimate of $26.489 bln.

HD rose to $137.89 (+0.61%) in pre-market trading.

-

13:17

Major stock indices in Europe fall moderately

European stocks fall on fears that the recent rally in stock price was excessive.

Last week, the European indices rose and completely leveled the drop since June 24, when the results of the referendum were announced in the UK, where the country's citizens voted for withdrawal from the EU.

Meanwhile, investors fears about a slowdown in the European economy and efficiency of the European Central Bank measures.

Focus was also on the UK inflation data and indexes in the business environment sentiment from the ZEW Institute in Germany and the euro zone.

In the UK, inflation increased slightly in July to its highest level since November 2014, showed data of the Office for National Statistics on Tuesday. Consumer prices rose 0.6 percent year on year in July, after rising 0.5 percent in June. Economists had forecast that inflation will remain at 0.5 percent. On a monthly basis, consumer prices fell by 0.1 percent, as expected, which was the first drop in six months. In June, prices rose by 0.2 percent. Core inflation, which excludes energy, food, alcoholic beverages and tobacco, slowed slightly to 1.3 percent in July compared with 1.4 percent in June.

Economic sentiment in Germany improved in August, showed results of a survey by the Centre for European Economic Research (ZEW) on Tuesday. The index of sentiment in the business environment from the ZEW Institute in Germany rose less than expected to 0.5 in August from -6.8 in July. The index was expected to rise to 2 in August. Similarly, current conditions rose to 57.6 compared to 49.8 in July. Economists had forecast that the indicator improved to 50.2.

"The indicator of economic sentiment from the ZEW partially recovered from Brexit shock," said ZEW President Achim Wambach. "Political risks within and outside the European Union, however, continues to hamper a more optimistic economic outlook in Germany. In addition, uncertainty about the stability of the EU banking sector is maintained," said Wambach.

The composite index of Europe's largest enterprises Stoxx 600 fell by 0.2% - to 345.49 points.

Swedish Electrolux AB fell 2.2% on the majority of sales of household appliances in the US fell in July. The company gets more than a third of revenue in the US market.

The cost of Schindler Holding AG shares fell 3.7%. The Swiss company has given a negative outlook for the world market of elevator and escalator equipment.

The capitalization of Linde AG jumped 6% on rumors that Praxair Inc intends to acquire the German manufacturer of industrial gases.

Shares of mining company Antofagasta rose by 4%. The company reported an increase in profits in the first half.

Quotes of Svenska Handelsbanken AB securities dropped to 1.7% after one of the largest Swedish bank dismissed its CEO Frank Vang-Jensen.

Rotork Paper Industry slowed down 2.8%, the most among Stoxx 600 components, after HSBC downgraded the rating.

Swiss Geberit shares rose 4.8% to a record peak, as the quarterly results of the manufacturer of sanitary ware was better than expected.

Shares of St. James's Place PLC tumbled 1.2% after the asset management company reported a slight decline in profit for the last six months compared to the same period last year, but 15% increase in dividend payments.

At the moment:

FTSE 6934.00 -7.19 -0.10%

DAX 10709.85 -29.36 -0.27%

CAC 4494.94 -2.92 -0.06%

-

13:01

WSE: Mid session comment

The morning reading of the ZEW index for the German economy proved to be much better than expected and rose from 49.8 points up to 57.6 points in anticipation of slight twitch to 50.2 points. Thus, analysts and managers quite noticeably revised their earlier pessimistic visions of the immediate impact of Brexit on the condition of the German economy. The data become to be support for the earlier downward image in Europe and both the DAX and the CAC40 virtually erased earlier losses. Unfortunately the Warsaw Exchange did not react on these impulses and declines are sustained. In the halfway of today's trading the WIG20 index was at the level of 1,847 points (-0,55%) ant with the turnover of PLN 210 mln.

-

09:31

Major stock markets in Europe trading lower at the start: FTSE 100 6,911.00-5.02-0.07%, DAX 10,668.53-70.68-0.66%

-

09:18

WSE: After opening

The futures market (WSE: FW20U1620) started from decline by 0.32% to 1,857 points. In Germany contracts for the DAX fell a similar scale.

In this passage, we may see a small disappointment, because it is worth to remember that we return after 1-day absence from the market, and yesterday ended with a more or less such increases, which in theory would mean for us zero balance changes.

WIG20 index opened at 1856.22 points (-0.08%) *

WIG 48605.94 -0.05%

Wig30 2109.36 -0.15%

mWIG40 3855.46 0.29%

* / - Change to previous close

The cash market (the WIG20 index) opened with cosmetic exit down by 0.08% to 1,856 points at low turnover. The environment is weak and the DAX shortly after the opening went down by 0.6% pulling futures market in Frankfurt. After the first quarter of trading the WIG20 index drops by 0.37%

The Kredyt Inkaso (WSE: KRI) stands out of the market after it has been increased price in the tender offer for the shares.

-

08:28

WSE: Before opening

Yesterday Wall Street indices gained 0.3% to 0.6% and established new record levels. In Europe also dominated rise, albeit at a smaller scale. During our absence nothing special had happened, and investors are waiting for Wednesday, when are going to be published the minutes of the last FOMC meeting.

Today's macro calendar includes data on inflation in the UK for July and in Europe will be published the ZEW index, which earlier surprised negatively and now is expected to be reflected. In the afternoon, from the US the most important information will be industrial production data, which may cause the biggest reaction, although Friday's weaker retail sales data did not lead to larger perturbations, and may be considered more important than production, which already generates less than 20% of the US GDP.

The US futures quotations in the morning went down approx. 0,10% and with declines on the Nikkei (-1,7%) may mean an offset of yesterday's light increases.

From the point of view of the Warsaw Stock Exchange, this means that a larger gap at the opening should not be expected. The WIG20 index on Friday admittedly fell, but remained above the level of 1850 points and a broad market still prevailed good mood.

-

08:21

Expected negative start of trading on the major stock exchanges in Europe: DAX-0.5%, CAC40 -0.5%, FTSE -0.4%

-

07:13

Global Stocks

European stocks ended a choppy session in the red on Friday after weaker-than-expected U.S. retail sales cast doubt on the health of the world's largest economy.

The Stoxx Europe 600 SXXP, -0.01% dropped 0.2% to close at 346.09, partly erasing a 0.8% gain from Thursday, which was fueled by higher oil prices. For the week, it ended 1.4% higher.

U.K. stocks rose Monday, with gains in energy shares helping to lift the FTSE 100 to a new high for the year, as the benchmark extended its run of winning sessions.

The FTSE 100 UKX, +0.36% finished up 0.4% at 6,941.19, its best close since early June 2015, according to FactSet data. The index has risen for eight straight sessions, matching the longest string of wins since October 2015.

The Dow Jones Industrial Average, the S&P 500 index, and the Nasdaq Composite Index all closed at record highs on Monday for the second time since 1999, thanks in part to a sharp uptick in oil prices, which boosted energy and materials shares.

The S&P 500 SPX, +0.28% rose 6.10 points, or 0.3%, to close at 2,190.15, with seven of the 10 main sectors trading higher. The materials, industrial, and energy sectors led the gains, while so-called defensive sectors, such as utilities, consumer staples and telecom were in negative territory. On Thursday, the index closed at a high of 2,185.79.

The Dow Jones Industrial Average DJIA, +0.32% gained 59.58 points, or 0.3%, to 18,636.05, with shares of DuPont DD, +1.45% and Goldman Sachs Group Inc. GS, +1.41% leading the gains. Back on Thursday, the Dow closed at a high of 18,613.52.

The Nasdaq Composite COMP, +0.56% logged its third record closing high in a row, advancing 29.12 points, or 0.6%, to finish at 5,262.02, topping Friday's previous closing high of 5,232.89.

Aug 16 Japan's Nikkei share average edged down on Tuesday morning as weakness in domestic demand-driven stocks offset gains in cyclicals such as exporters in a relatively quiet holiday-thinned market.

The Nikkei dropped 0.2 percent to 16,837.98 in midmorning trade.

Traders said that with many investors away for Japan's 'bon' holidays, activity will likely be subdued again. On Monday, trading volume stood at only 1.24 billion shares on the broader market, the lowest level since April 2014.

The downside for the broader market, however, will likely be limited thanks to strong performances in overseas stocks, they said.

-

00:30

Stocks. Daily history for Aug 15’2016:

(index / closing price / change items /% change)

Nikkei 225 16,869.56 -50.36 -0.30%

Shanghai Composite 3,125.40 +74.73 +2.45%

S&P/ASX 200 5,539.96 +9.05 +0.16%

FTSE 100 6,941.19 +25.17 +0.36%

CAC 40 4,497.86 -2.33 -0.05%

Xetra DAX 10,739.21 +25.78 +0.24%

S&P 500 2,190.15 +6.10 +0.28%

Dow Jones Industrial Average 18,636.05 +59.58 +0.32%

S&P/TSX Composite 14,777.02 +29.57 +0.20%

-