Noticias del mercado

-

22:06

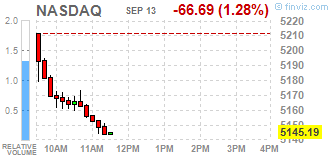

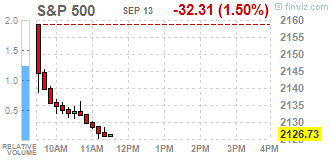

Major US stock indexes finished trading in the red zone

Major stock indexes in Wall Street fell more than a percent on the background of the collapse of the energy sector stocks due to lower oil prices.

On the trading dynamics also affect underestimated prospects of higher interest rates in the near future. Recall, on the eve of comments voiced by the Federal Reserve Board of Governors member Lyell Breynar strengthened the confidence of market participants that at the September meeting of the regulator of any change in monetary policy will not be amended. The chances of a rate hike at the meeting in September were down after the publication of a number of macroeconomic reports, unrealistic expectations. These include, first of all, data on employment, as well as statistics on the ISM index and some other indicators. But despite published at the beginning of the month data, uncertainty about further Fed action was sufficiently high, the chances of a rate hike, according to the dynamics of futures on the federal funds, equal to about 30%. Statements Brainard substantially clarified the Fed's intentions, is now the probability of a rate hike next week is estimated at only 15%.

Oil prices have fallen by about 3% after the report of the International Energy Agency, which added to concerns about global oversupply. In addition, yesterday in its monthly report, OPEC reported that in 2016, production in the United States, Russia, Norway and several other countries will be approximately 190,000 barrels per day higher than expected. This factor may indicate that oil production outside OPEC was stable, despite low oil prices.

Most DOW components of the index closed in negative territory (29 of 30). More rest rose stocks Apple Inc. (AAPL, + 2.55%). Outsider were shares of Chevron Corporation (CVX, -2.75%).

All business sectors S & P index showed a decline. Most of the basic materials sector fell (-3.4%).

At the close:

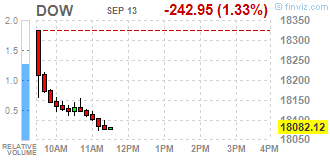

Dow -1.41% 18,066.89 -258.18

Nasdaq -1.09% 5,155.26 -56.63

S & P -1.48% 2,127.04 -32.00

-

21:00

Dow -1.34% 18,080.41 -244.66 Nasdaq -1.15% 5,152.01 -59.88 S&P -1.53% 2,125.95 -33.09

-

20:00

U.S.: Federal budget , August -107 (forecast -108)

-

18:00

European stocks closed: FTSE 100 -35.27 6665.63 -0.53% DAX -45.17 10386.60 -0.43% CAC 40 -52.62 4387.18 -1.19%

-

17:50

The price of oil has fallen more than 2.5 percent

Oil futures fell on updated forecasts from the International Energy Agency (IEA) and the US dollar rate growth.

The IEA reported that in the 3 rd quarter oil demand growth has slowed sharply - up to 800 thousand barrels per day vs the 3rd quarter of 2015 when demand growth was higher at 1.5 million barrels per day. In addition, the forecast for growth of world oil demand in 2016 was reduced by 100 thousand barrels to 1.3 million barrels per day. The IEA estimates that global oil demand growth rate in 2017 would be another 100 thousand barrels per day lower than in 201t and amount to 1.2 million barrels per day. The IEA added that demand growth in developed countries has practically stopped, while consumption in Asia, in countries such as China and India, has been growing much more slowly.

IEA comments followed unexpectedly pessimistic forecast of OPEC. Yesterday, OPEC reported that in 2016, production in the United States, Russia, Norway and several other countries will be approximately 190,000 barrels per day higher than expected. This factor may indicate that oil production outside OPEC was stable, despite low oil prices. As expected by the cartel in 2017 oil supply will exceed demand by about 760,000 barrels a day, which is more than three times higher than the previous forecast.

"It seems the situation is much worse in the eyes of the OPEC and the IEA, - said Commerzbank strategist Eugen Weinberg -. Given the recent forecasts, I would not be surprised if the fall in oil prices will continue for some time."

The cost of the October futures for US light crude oil WTI (Light Sweet Crude Oil) fell to 44.92 dollars per barrel on the New York Mercantile Exchange.

October futures price for North Sea petroleum mix of mark Brent fell to 47.13 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

17:35

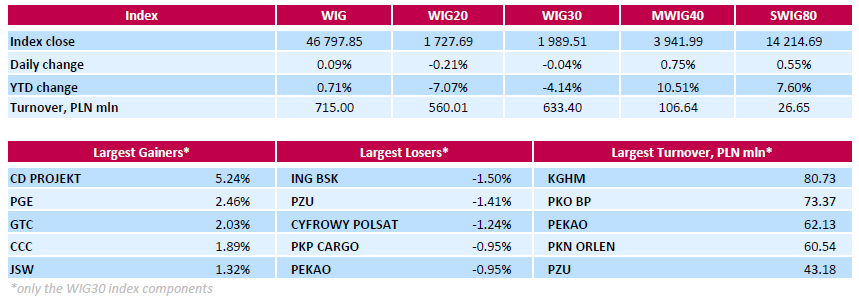

WSE: Session Results

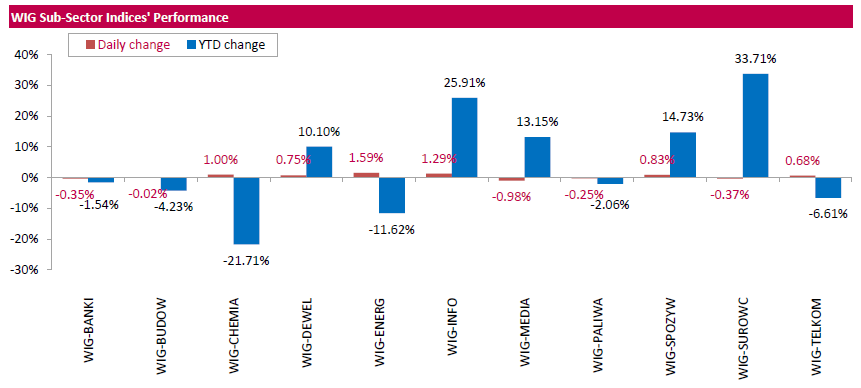

Polish equity market closed flat on Tuesday. The broad market measure, the WIG Index edged up 0.09%. Sector performance within the WIG Index was mixed. Utilities (+1.59%) outperformed, while media (-0.98%) lagged behind.

The large-cap stocks' measure, the WIG30 Index inched down 0.04%. Within the Index components, videogame developer CD PROJEKT (WSE: CDR) was the best-performing name, climbing by 5.24% and fully erasing its yesterday's losses. It was followed by genco PGE (WSE: PGE), property developer GTC (WSE: GTC) and footwear retailer CCC (WSE: CCC), advancing 2.46%, 2.03% and 1.89% respectively. On the other side of the ledger, bank ING BSK (WSE: ING), insurer PZU (WSE: PZU) and media group CYFROWY POLSAT (WSE: CPS) were the biggest decliners, dropping by 1.5%, 1.41% and 1.24% respectively.

-

17:33

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes lower on Tuesday, with energy stocks falling on lower oil prices and financials hit by diminished prospects of an interest rate hike in the near term. Oil prices were down more than 2,5% after a report from the International Energy Agency added to concerns about global oversupply. U.S. stocks had racked up their strongest gain in two months on Monday after Federal Reserve Board Governor Lael Brainard stuck to her dovish stance on interest rates and urged caution about removing monetary stimulus too quickly.

Most of Dow stocks in negative area (29 of 30). Top gainer - Apple Inc (AAPL, +2.62%). Top loser - Verizon Communications Inc. (VZ, -2.46%).

All S&P sectors also in negative area. Top gainer - Basic Materials (-3.2%).

At the moment:

Dow 18008.00 -238.00 -1.30%

S&P 500 2120.00 -32.00 -1.49%

Nasdaq 100 4710.25 -53.50 -1.12%

Oil 44.95 -1.34 -2.89%

Gold 1328.10 +2.50 +0.19%

U.S. 10yr 1.69 +0.02

-

17:31

Gold price moderately lower

Gold prices fell slightly, being under pressure from a strengthening US dollar and uncertainty about a Fed hike next week. At the same time, a further fall in prices restrained the negative dynamics of stock markets.

The US Dollar Index, showing the US dollar against a basket of six major currencies, was up 0.25%. Since gold prices are tied to the dollar, a stronger dollar makes the precious metal more expensive for holders of foreign currencies.

The main theme in the markets continues to be yesterday's comments by the Fed Brainard that seem less convincing for a hike and reinforced the view of those investors who believe the Fed in the coming months will keep rates unchanged.

"The focus of is still directed to the possible hike and the dynamics of the market will be completely determined by this expectations.", - Said David Gavett of Marex Spectron.

Gold may continue to trade near $ 1330 resistance before resuming a downward trend, says Reuters technical analyst Wang Tao.

"The probability of Fed rate increase in the short term is reduced, and if the oil quotes stabilize the gold price should find a bottom, at least, before the meeting of the FOMC", - HSBC analyst James Steel said.

The cost of the October futures for gold on the COMEX fell to $ 1324.5 per ounce.

-

16:31

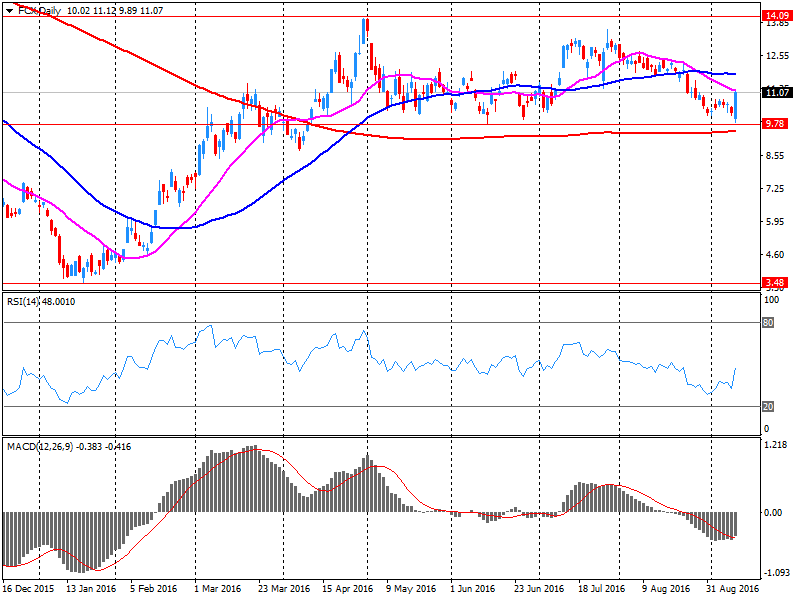

Company News: Freeport-McMoRan (FCX) is selling its deep-water assets in the Gulf of Mexico for $ 2 billion.

Freeport-McMoRan reported that its oil and gas subsidiary is selling deep-water assets in the Gulf of Mexico to Anadarko Petroleum for $ 2 billion.

At the end of the 12-month period ending June 30, 2016, these assets provided an average of 73 thousand barrels of oil per day. During this period, revenues reached $ 1.0 billion., Operating costs (before deducting administrative expenses) amounted to $ 0.3 billion., While capital expenditures totaled $ 1.6 billion. Freeport-McMoRan does not expect that the transaction will bring significant damages or losses.

FCX shares fell in premarket trading to $ 10.78 (-2.71%).

-

15:54

WSE: After start on Wall Street

The market in the US began with a discount of 0.6%, which increased slightly after the first transactions.

It's weak start, but generally in line with expectations. There is the interesting information, that the Bank of England has included Apple on the lists of companies qualified for its new economic stimulus bond-buying scheme.

An hour before the end of trading, the WIG20 index reached the level of 1,735 points (+ 0.25%).

-

15:50

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.1150 (EUR 265m) 1.1200 (297m) 1.1220 (721m) 1.1225 (380m) 1.1230 (1.2bln) 1.1250 (570m) 1.1270 (222m) 1.1300 (301m) 1.1350 (444m) 1.1360 (653m)

USD/JPY: 100.00-05 (315m) 101.02( 240m) 101.47-50 (560m) 102.00 (541m) 104.00-05 (1.16bln)

AUD/USD: 0.7370-75( AUD 300m)

USD/CAD 1.3100 (USD 590m) 1.3275 (400m)

NZD/USD 0.7450 (262m)

AUD/JPY 77.50 (AUD 445m) 77.95-0.7600 (619m)

-

15:34

U.S. Stocks open: Dow -0.81%, Nasdaq -0.53%, S&P -0.79%

-

15:28

The International Energy Agency (IEA): The growth of world oil demand is slowing faster than previously thought

- IEA lowers forecast for world oil demand in 2016 to 100,000 barrels / day, and in 2017 to 200 000 barrels / day.

- World oil supply in August -300,000 barrels / day due to lower non-OPEC production.

- OPEC crude oil in August, 20 000 barrels / day to 33.47 million barrels / day.

- Oil production in Saudi Arabia in August, 10.60 million barrels / day against 10.65 million barrels / day in July

- Oil stocks in the OECD countries increased by 32.5 million barrels to a new record level of 3.111 billion barrels.

- The global demand for oil under pressure due to the sharp slowdown in oil consumption in China and India.

- European demand for oil showed the first annual decline in six years.

- The scale of a slowdown in demand growth in the 3rd quarter is amazing.

-

15:28

Before the bell: S&P futures -0.79%, NASDAQ futures -0.62%

U.S. stock-index futures retreated amid renewed weakness in crude oil, and as investors remained on edge over central banks' ability to bolster growth.

Global Stocks:

Nikkei 16,729.04 +56.12 +0.34%

Hang Seng 23,215.76 -74.84 -0.32%

Shanghai 3,023.79 +1.81 +0.06%

FTSE 6,705.37 +4.47 +0.07%

CAC 4,434.39 -5.41 -0.12%

DAX 10,464.86 +33.09 +0.32%

Crude $45.18 (-2.40%)

Gold $1327.10 (+0.11%)

-

14:55

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Chevron (CVX) initiated with an Outperform at BMO Capital; target $120

Altria (MO) initiated with a Buy at Citigroup; target $72

-

14:36

Time To Sell JPY: Looking To Go Short Vs USD & EUR - Nomura

"Trading G3 currencies in the second half of this year has been treacherous so far. The euro has traded in a 1.095 to 1.137 range, which itself lies in the rough range of 1.08 to 1.15 that has been in place since early 2015. Meanwhile, USD/JPY has traded choppily in a 100 to 107 range. This has been in sharp contrast to its almost straight line decline from 120 to 100 in the first half of this year. EUR/JPY has broadly followed USD/JPY but with a smaller range.

While the recent price action of G3 FX may be off-putting, it could be signalling a change in trend - at least over the coming months. Indeed, the yen rally earlier this year was a two-standard-deviation move, which typically subsequently reverse. This could therefore be a good starting point to consider short yen trades.

Looking at the correlations among EUR/USD, USD/JPY and EUR/JPY, we find that in recent months, the yen pairs have been the most correlated suggesting that the yen is indeed the currency to focus on rather than the dollar or euro. Focusing on the yen against both the dollar and the euro also allows one not to become too dependent on to Fed hike expectations. That leaves Japanese factors to spur yen weakness. On that front the picture is promising. The Bank of Japan is likely to engage in further easing, whether a cut deeper into negative territory, the introduction of negative rates to its loan support programmes or an extension of easing guidance or some combination of this. This could happen at the 21 September meeting or the October/November meeting.

After the big disappointment of the 29 July meeting which saw little action and so resulted in rates selling off and the yen rallying, investors are much more cautious around upcoming BOJ meetings. For example, 2yr yields have essentially moved sideways in recent weeks, rather than falling at the same stage as they did ahead of the July meeting. FX positioning, meanwhile, shows leveraged funds increasing long yen positions and asset managers scaling back short yen positions into the upcoming BOJ meeting.

Finally, the behaviour of domestic Japanese investors appears to be shifting in favour of yen weakness. Japanese purchases of foreign equities, a barometer of tolerance to currency risk (and so sell yen), have increased sharply of late. The sharp widening on a cross-currency basis caused by forthcoming US money market reform and Fed hike expectations should lead to less currency hedging, which in turn implies more net selling of yen.

Therefore, we would look to sell the yen against both the dollar and the euro".

Copyright © 2016 Nomura, eFXnews™

-

14:27

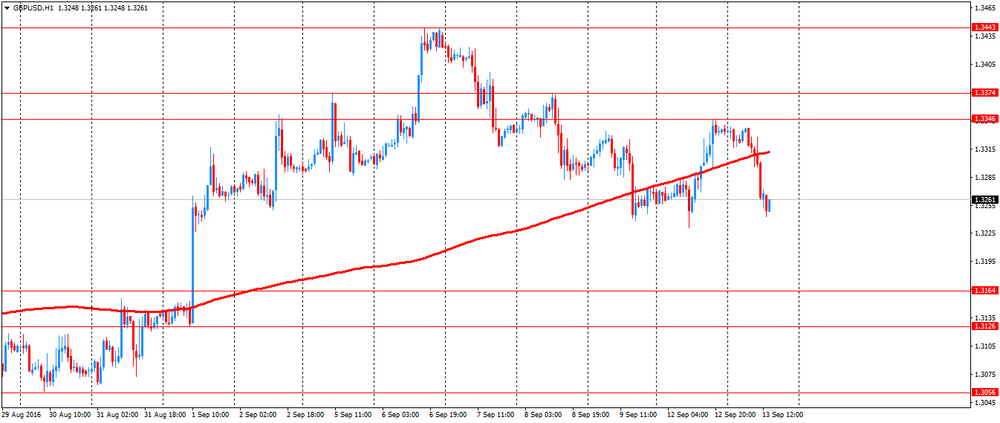

European session review: the pound traded lower vs the US dollar

The following data was published:

(Time / country / index / period / previous value / forecast)

6:00 Germany Consumer Price Index m / m (final data) August 0.3% 0.0% 0.0%

6:00 Germany CPI, y / y (final data) August 0.4% 0.4% 0.4%

Switzerland 7:15 producers and import price index m / m in August -0.1% -0.3%

Switzerland 7:15 producers and import price index y / y in August -0.8% -0.4%

8:30 UK Producer Price Index (m / m) in August 0.3% 0.2% 0.1%

8:30 UK producers selling prices index, y / y in August 0.3% 0.8% 1%

8:30 UK producers purchase prices index m / m in August 3.1% Revised to 3.3% 0.5% 0.2%

8:30 UK purchasing producer prices index, y / y in August to 4.1% from 4.3 Revised% 8.1% 7.6%

8:30 UK Retail Price Index m / m in August 0.1% 0.4% 0.4%

8:30 UK Retail Price Index y / y in August 1.9% 1.8% 1.8%

8:30 UK Consumer Price Index m / m in August -0.1% 0.4% 0.3%

8:30 UK Consumer Price Index y / y in August 0.6% 0.7% 0.6%

08:30 UK Consumer Price Index, the base value, y / y August 1.3% 1.4% 1.3%

9:00 Eurozone index of sentiment in the business environment from the ZEW Institute in September 4.6 5.4

9:00 Eurozone Employment Change, q / q to 0.4% q II Revised to 0.3% 0.4%

9:00 Germany Sentiment Index in the business environment of the institute ZEW September 0.5 2.5 0.5

The pound fell after data on inflation in the UK pointed to the acceleration of price growth in August, but not as strong as expected by the market.

Inflation has remained stable, while there was a marked rise in producer prices in August, the Office for National Statistics said on Tuesday.

Consumer prices advanced 0.6 percent year on year in August, showing the same growth rate as in July. Prices were expected to rise by 0.7 percent.

Core inflation, which excludes energy, food, alcoholic beverages and tobacco, remained stable at 1.3 percent in August. Economists had forecasted core inflation at +1.4 percent in August.

On a monthly basis, consumer prices rose by 0.3 percent, slightly slower than the growth of 0.4 percent, which economists had expected.

The US dollar rose against other major currencies, as the official comments of the Fed, voiced on Monday, caused fresh uncertainty about the timing of interest rates hike.

The dollar came under pressure after Fed's Lael Brainard warned about the risks of a premature increase in interest rates.

In his speech on Monday, Brainard said that it would be wise not to rush to tight policy.

The euro briefly came under pressure after the economic sentiment in Germany remained stable in September, according to data of the Center for European Economic Research / ZEW.

The index of sentiment in the business environment was 0.5 points in September, remained unchanged from August vs +2.5 forecast.

At the same time, the current conditions index fell by 2.5 points to 55.1 in September. The reading was below the expected level of 56.

"The current uncertainty of economic impuls from Germany and abroad means that the forecasts for the next few months is difficult to do," said the president of the ZEW, Professor Achim Wambach. "German exports, especially in countries that are not EU members, as well as industrial production figures disappointed."

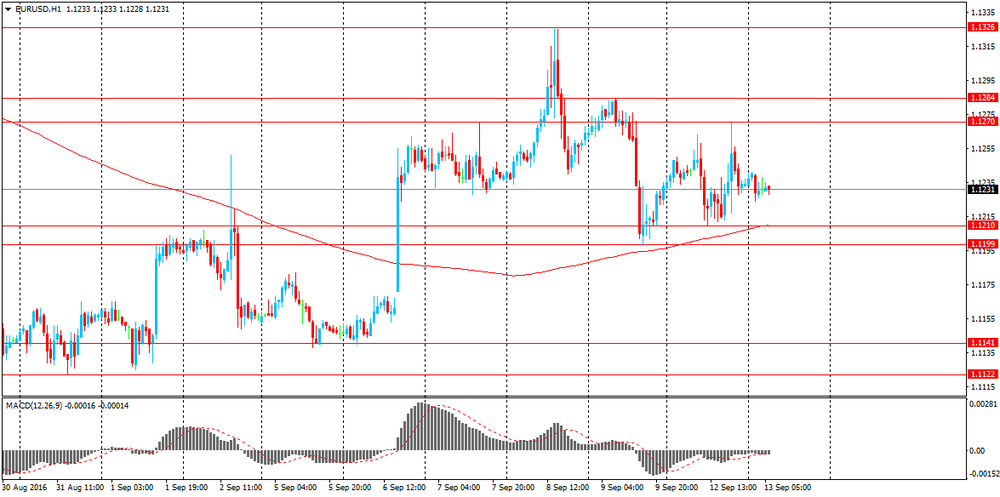

EUR / USD: during the European session, the pair fell to $ 1.1216, and then rose to $ 1.1243

GBP / USD: during the European session, the pair fell to $ 1.3243

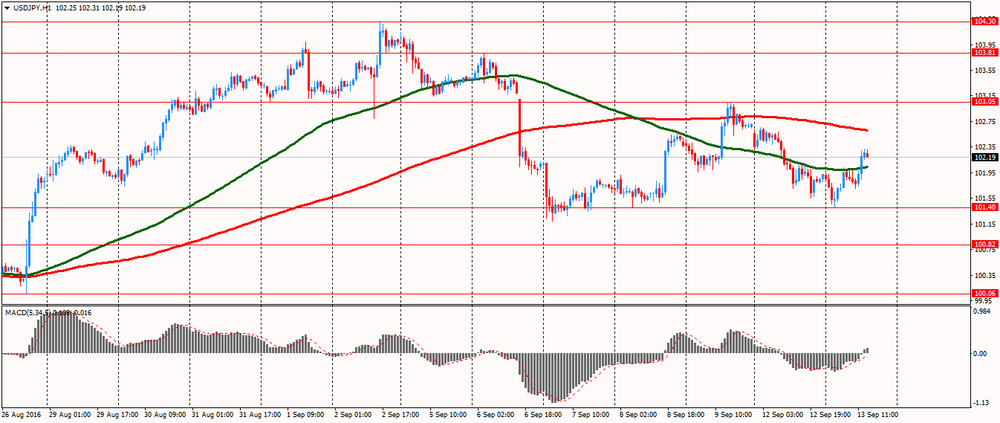

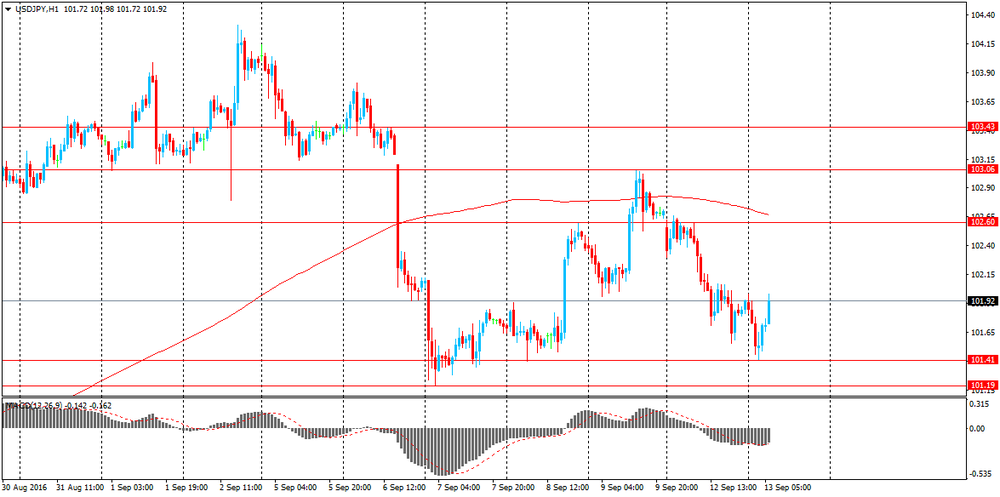

USD / JPY: during the European session, the pair rose to Y102.32

-

13:11

WSE: Mid session comment

German ZEW index was slightly worse than forecast, but did not change its value compared to the previous month. The ZEW Institute indicates that the economic picture in the EU is improving, however it was not groundbreaking news for investors. Major indexes in France and Germany gaining cosmetically today's and session looks very calm with low volatility. At the same time it does not appear any will to quick make up for Friday's losses.

In the last hours the Polish zloty strengthened all along the line. This can be justified by an optimistic statement of the Minister of Finance regarding the implementation of the budget.

In the mid-session the WIG20 index was at the level of 1,729 points and the turnover in index of the largest companies was amounted to PLN 245 mln.

-

12:47

Major stock indices in Europe in the green zone

Stock indices in Western Europe recovered after declining for three sessions to the lowest in almost three weeks.

Various statements by members of the Federal Reserve in recent days have forced some investors to believe that the US seriously intends to increase the Central Bank base interest rate in September.

However, Leil Brainard, member of the Board of Governors of the Federal Reserve said that the central bank should be cautious in raising interest rates, the markets have calmed somewhat and reduced the likelihood of a rate hike at the next meeting.

Meanwhile, market sentiment improved after data showed that China's industrial output grew in August at an annualized rate of 6.3%, exceeding the expectations of +6.1%, after rising 6.0% in the previous month.

In addition, consumer prices in Germany, calculated by the standards of the European Union increased in August 2016 by 0.3%. The indicator has coincided with the expectations.

Meanwhile, prices in Spain fell by 0.3% in annual terms, after falling 0.7% in July. Deflation continues in the country since May, 2014.

In Sweden, inflation stood at 1.1%, the highest since 2012, although it was slightly worse than forecasts.

In the UK, inflation has remained stable, while there was a marked acceleration in producer prices in August, the Office for National Statistics said.

Consumer prices advanced 0.6 percent year on year in August, showing the same growth rate as in July. Prices were expected to rise by 0.7 percent.

Core inflation, which excludes energy, food, alcoholic beverages and tobacco, remained stable at 1.3 percent in August. Economists had forecasted core inflation at +1.4 percent in August.

On a monthly basis, consumer prices rose by 0.3 percent, slightly slower than the growth of 0.4 percent, which economists had expected.

The composite index of the largest companies in the region Stoxx Europe 600 rose 0,1% - to 342.63 points.

The capitalization of the Swiss Foundation Partners Group Holding increased by 10% after the company reported an increase in profit in the first half of the year by 64%.

The cost of British sportswear retailer JD Sports Fashion has increased by 4.1% on profit growth in the first half of the year and the optimistic outlook for the second half of the year.

Meanwhile, the price of the UK online store Ocado Group Plc fell by 12%. The company said it does not expect any easing of pressure on margins in the near future.

RWE AG's shares fell 1% after analysts at DZ Bank confirmed its rating to "sell."

Shire Plc jumped 1.7% after Jefferies Group analysts confirmed their rating to "buy."

At the moment:

FTSE 6707.12 6.22 0.09%

DAX 10470.35 38.58 0.37%

CAC 4446.68 6.88 0.15%

-

12:37

ECB President Draghi: EU single market must be completed to be protected

- EU discussion on tax fairness support integration.

- EU unemployment insurance fund would support union.

- EU action on migration and security/defence is essential.

*via forexlive

-

11:32

The ZEW Indicator of Economic Sentiment for Germany remains unchanged in September

The ZEW Indicator of Economic Sentiment for Germany remains unchanged in September 2016. The index stands at a level of 0.5 points (long-term average: 24.1 points). "The current ambiguity of economic impulses from Germany and abroad means that forecasts for the next few months are difficult. German exports, particularly to non-EU countries, as well as industrial production figures have disappointed. By contrast, the economic environment in the European Union is improving. Overall, the ZEW Indicator of Economic Sentiment suggests that the economic situation in Germany will remain favourable in the coming six months," comments ZEW-President Professor Achim Wambach.

-

11:06

Employment up by 0.4% in euro area and by 0.3% in EU28

Employment up by 0.4% in euro area and by 0.3% in EU28, +1.4% and +1.5% respectively compared with the second quarter of 2015.

The number of persons employed increased by 0.4% in the euro area (EA19) and by 0.3% in the EU28 in the second quarter of 2016 compared with the previous quarter, according to national accounts estimates published by

Eurostat, the statistical office of the European Union. In the first quarter of 2016, employment increased by 0.4% in both zones. These figures are seasonally adjusted.

Compared with the same quarter of the previous year, employment increased by 1.4% in the euro area and by 1.5% in the EU28 in the second quarter of 2016 (after +1.4% in both zones in the first quarter of 2016).

Eurostat estimates that, in the second quarter of 2016, 232.1 million men and women were employed in the EU28 (highest level ever recorded); of which 153.3 million were in the euro area (highest level since the fourth quarter of 2008). These figures are seasonally adjusted.

-

11:01

Germany: ZEW Survey - Economic Sentiment, September 0.5 (forecast 2.5)

-

11:01

Eurozone: Employment Change, Quarter II 0.4%

-

11:01

Eurozone: ZEW Economic Sentiment, September 5.4

-

10:37

UK house price pressures continued to grow in July

- the average price of a property in the UK was £216,750

- the annual price change for a property in the UK was 8.3%

- the monthly price change for a property in the UK was 0.4%

- the monthly index figure for the UK was 113.7 (January 2015 = 100)

According to gov.uk, house price pressures continued to grow in July, reflecting the strength of demand relative to supply in the housing market. However, there were indications that some of the heat had been taken out of the market, with several indicators pointing towards weaker housing demand and supply in recent months.

On the demand side, the volume of lending approvals for house purchases fell by 5.1% in July 2016 compared to the previous month, continuing a downward trend since the beginning of the year. As such, monthly approvals remain below the levels seen in the 10 months prior to stamp duty changes in April 2016. UK home sales fell by 0.9% in July 2016 compared to the previous month, which means that home sales on a monthly basis remain below levels seen in 2014 and 2015 and before the stamp duty changes in early 2016.). Furthermore, the Royal Institution of Chartered Surveyors (RICS) market survey for July reported a fourth consecutive month of falling new buyer enquiries, affecting all regions of the UK.

-

10:35

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.1150 (EUR 265m) 1.1200 (297m) 1.1220 (721m) 1.1225 (380m) 1.1230 (1.2bln) 1.1250 (570m) 1.1270 (222m) 1.1300 (301m) 1.1350 (444m) 1.1360 (653m)

USD/JPY: 100.00-05 (315m) 101.02( 240m) 101.47-50 (560m) 102.00 (541m) 104.00-05 (1.16bln)

AUD/USD: 0.7370-75( AUD 300m)

USD/CAD 1.3100 (USD 590m) 1.3275 (400m)

NZD/USD 0.7450 (262m)

AUD/JPY 77.50 (AUD 445m) 77.95-0.7600 (619m)

-

10:34

UK CPI up 0.6% y/y on rising food prices and air fares

The Consumer Prices Index (CPI) rose by 0.6% in the year to August 2016, unchanged from July. The rate is still relatively low in the historic context although it is above the rates experienced in 2015 and early 2016.

The main upward contributors to change in the rate were rising food prices and air fares, and a smaller fall in the price of motor fuels than a year ago. These upward pressures were offset by falls in hotel accommodation prices, in addition to smaller rises in the prices of alcohol, and clothing and footwear than a year ago.

CPIH (not a National Statistic) rose by 0.9% in the year to August 2016, unchanged from July.

-

10:31

United Kingdom: Producer Price Index - Output (MoM), August 0.1% (forecast 0.2%)

-

10:31

United Kingdom: Producer Price Index - Output (YoY) , August 0.8% (forecast 1%)

-

10:30

United Kingdom: HICP, Y/Y, August 0.6% (forecast 0.7%)

-

10:30

United Kingdom: Retail prices, Y/Y, August 1.8% (forecast 1.8%)

-

10:30

United Kingdom: HICP, m/m, August 0.3% (forecast 0.4%)

-

10:30

United Kingdom: Retail Price Index, m/m, August 0.4% (forecast 0.4%)

-

10:30

United Kingdom: HICP ex EFAT, Y/Y, August 1.3% (forecast 1.4%)

-

10:30

United Kingdom: Producer Price Index - Input (MoM), August 0.2% (forecast 0.5%)

-

10:30

United Kingdom: Producer Price Index - Input (YoY) , August 7.6% (forecast 8.1%)

-

10:25

Italian industrial production up 0.4% in July

The index measures the monthly evolution of the volume of industrial production (excluding construction). With effect from January 2013 the indices are calculated with reference to the base year 2010 using the Ateco 2007 classification (Italian edition of Nace Rev. 2).

In July 2016 the seasonally adjusted industrial production index increased by 0.4% compared with the previous month. The percentage change of the average of the last three months with respect to the previous three months was -0.5.

The calendar adjusted industrial production index decreased by 0.3% compared with July 2015 (calendar working days being 21 versus 23 days in July 2015); in the period January-July 2016 the percentage change was +0.6 compared with the same period of 2015.

The unadjusted industrial production index decreased by 6.3% compared with July 2015.

-

10:05

Oil is traded lower

This morning New York WTI crude oil futures fell 1.58% to $ 45.57 and Brent oil futures fell 1.22% to $ 47.73 per barrel. Thus, the black gold is traded lower on the background of concerns about the increase in drilling activity in the US, as well as profit taking. According to experts, the fall in prices shows that the increasing drilling activity in the US still remains a cause for concern, despite the fact that oil quotes finished the Monday session in positive territory on the background of dollar weakness.

-

10:02

Major stock exchanges trading in the green zone: FTSE + 0.2%, DAX + 0.5%, CAC40 + 0.5%, FTMIB + 0.6%, IBEX + 0.6%

-

09:32

Swiss producer prices decline in August

The Producer and Import Price Index fell in August 2016 by 0.3% compared with the previous month, reaching 99.5 points (base December 2015 = 100). This decline is due in particular to lower prices for petroleum products and pharmaceutical products. Compared with August 2015, the price level of the whole range of domestic and imported products fell by 0.4%. These are the findings of the Federal Statistical Office (FSO).

-

09:16

WSE: After opening

WIG20 index opened at 1736.54 points (+0.30%)*

WIG 46951.94 0.42%

WIG30 2000.27 0.50%

mWIG40 3925.33 0.32%

*/ - change to previous close

The futures market began trading from increase by 0.17% to 1,735 points.

The cash market opens with an increase of 0.3% to 1,736 points. It is a reaction to yesterday's successful session in the United States, although the scale of growth is not spectacular. Investors' attention is still focused on the level of 1,750 points., which remains unconquered. So it appears that, although the situation has been stabilized after three days of declines, a smooth transition to growth will not be easy.

The decrease in the valuation of contracts on the S & P500 by approx. 0.5%. somewhat dampens possible earlier appetites, and on the Warsaw Stock Exchange may lead to a well-known stop.

-

09:15

Switzerland: Producer & Import Prices, y/y, August -0.4%

-

09:15

Switzerland: Producer & Import Prices, m/m, August -0.3%

-

09:00

Huge week for the pound as today’s CPI will set the tone. Employment and Bank of England up next. Volatility expected

-

08:57

Expected positive start of trading on the major stock exchanges in Europe: DAX futures + 0.9%, CAC40 + 0.7%, FTSE + 0.5%

-

08:41

Gold Remains An Attractive Medium-Term Buy - Credit Agricole

"We remain of the view that precious metals such as gold should prove an attractive medium-term buy in the current environment. This is not only due to rising uncertainty about global central banks' ability to stimulate their respective economies; political developments in Europe and elsewhere may unsettle markets somewhat, at least from a broader angle. It may be true that global risk sentiment remains broadly stable. However, a large part of that stability was due to rising liquidity expectations rather than better global growth prospects.

From the current levels, we see limited room for major central banks such as the Fed or ECB turning more aggressive, and that may cause more unstable market conditions ahead.

In terms of trade recommendations, we stay long XAU/CHF. In that respect, it must still be noted that the SNB's aggressive monetary policy stance is keeping the franc's safe haven appeal low. The central bank meets this week and we expect them to reaffirm that a policy mix consisting of negative interest rates and FX intervention stays intact".

Copyright © 2016 Credit Agricole CIB, eFXnews™

-

08:39

Asian session review The dollar reversals on Brainard's comments

The Australian dollar fell slightly, despite the more positive-than-expected economic data from China and Australia. Today was published the monthly report on the index of business sentiment from Australian National Australia Bank. It is based on a survey of top managers of more than 500 green companies on the continent. It turned out that in August, the index fell 2 points to 7.0. However, the index of business sentiment rose to six, after a decline of one point in July. Also, increased sales and profits of companies and the employment index showed growth above the average by 4 points.

Also, today's report, published by China's National Bureau of Statistics showed that the volume of industrial production in August, year on year increased by 6.3%. Analysts had expected an increase of 6.1%. During the period from January to August of last year this indicator increased by 6.0%. Production growth was recorded in 33 of 41 industries. The highest growth rates showed the automotive and electronics industry.

Also today was reported that retail sales in China increased in August by 10.6%, after rising by 10.2% previously. Analysts had expected an increase of 10.3%. The volume of investments in fixed assets in China, with the exception of agriculture, grew by 6.1%, lower than the previous value of 8.1%, and experts forecast of 8.0% in January-August 2016.

At the end of eight months of this year the volume of investments in the Chinese mining industry grew by 21.5%. The inflow of investments in the manufacturing sector increased by 3%.

The US dollar traded in a narrow range against the major currencies, as investors continue to analyze the comments from the Fed before the meeting of the US central bank, which is scheduled for September 20-21.

Fed official Lael Brainard said yesterday that the grounds for preventive rate hikes seem less convincing, and improvement in the labor market has not had the desired impact on inflation. "Right now, the impact of external negative shocks stronger than before, focusing on downside risks than pre-emptively raise rates". According to the futures market, the likelihood of a hike in September is 12% against 24% before Brainard's speech. Meanwhile, the probability of rate increase during the December meeting of the Fed declined to 56.8% from 59.3% the previous day.

EUR / USD: during the Asian session, the pair was trading in the $ 1.1225-40 range

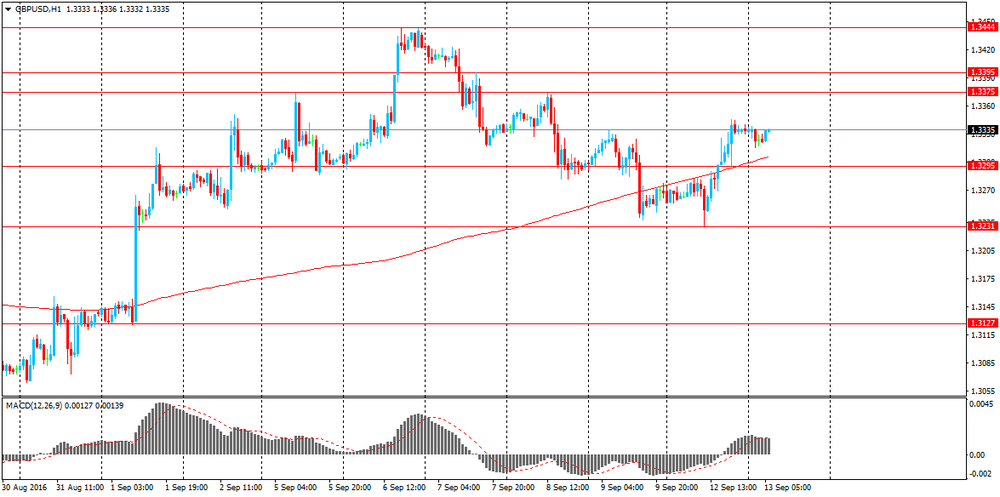

GBP / USD: during the Asian session, the pair was trading in the $ 1.3315-40 range

USD / JPY: during the Asian session, the pair was trading in the Y101.40-00 range

-

08:27

WSE: Before opening

During yesterday's session on Wall Street, the S&P500 gained almost 1.5% in the move limiting most of the losses from Friday. However in the morning derivative market slightly adjusted, but so successful yesterday's session should find their impact on market performance in Europe. Seems that the risk of continuing price reductions on the present moment was averted.

Yesterday's comments of Lael Brainard, a significant member of the Fed, did not indicate imminent desire to raise the cost of money, what was positively received by investors and the likelihood of the next week rate hike decreased from 24% on Friday to 15% today.

The positive data came from China. Readings on industrial production, retail sales and investment slightly positively surprised, although it seems that investors passed them by indifferently. Modest gains in Asian parquets are interspersed with equally modest declines.

Today's macro calendar will not be rich. The most interesting issue will be the ZEW index in Germany. On the Warsaw market, we may expect attempts to rebound, especially in the range of small and medium-sized companies. In the case of blue-chips the main challenge is to return above the level of 1,750 points., which already was lost yesterday's opening.

-

08:27

Options levels on tuesday, September 13, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1384 (2133)

$1.1342 (2106)

$1.1302 (425)

Price at time of writing this review: $1.1229

Support levels (open interest**, contracts):

$1.1176 (3045)

$1.1144 (3580)

$1.1108 (3602)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 35940 contracts, with the maximum number of contracts with strike price $1,1500 (5361);

- Overall open interest on the PUT options with the expiration date October, 7 is 37891 contracts, with the maximum number of contracts with strike price $1,1100 (5582);

- The ratio of PUT/CALL was 1.05 versus 1.01 from the previous trading day according to data from September, 12

GBP/USD

Resistance levels (open interest**, contracts)

$1.3604 (1529)

$1.3507 (1421)

$1.3411 (1931)

Price at time of writing this review: $1.3320

Support levels (open interest**, contracts):

$1.3193 (1834)

$1.3096 (768)

$1.2998 (3071)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 20300 contracts, with the maximum number of contracts with strike price $1,3450 (2699);

- Overall open interest on the PUT options with the expiration date October, 7 is 19872 contracts, with the maximum number of contracts with strike price $1,3000 (3071);

- The ratio of PUT/CALL was 0.98 versus 1.04 from the previous trading day according to data from September, 12

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:27

The Wall Street Journal: New Zealand's GDP in the 2nd quarter likely rose 1.1%

According to the median estimate of economists surveyed by The Wall Street Journal, the gross domestic product of New Zealand in the second quarter probably rose by 1.1% compared with the previous quarter. Recall that in the first quarter the economy rose 0.7%. On an annualized basis, economists forecast the growth rate at 3.6%. 9 experts surveyed said that the positive dynamics of GDP set by the construction sector, manufacturing and retail. Recall, the official data will be published on Wednesday at 21.45 GMT.

-

08:21

Industrial production in China climbed 6.3 percent on year

According to rttnews, industrial production in China climbed 6.3 percent on year in August, the National Bureau of Statistics said on Tuesday - beating forecasts for a gain of 6.2 percent and up from 6.0 percent in July.

On a monthly basis, output expanded 0.5 percent.

The bureau also said that retail sales advanced an annual 10.6 percent - again exceeding expectations for 10.2 percent, which would have been unchanged from the previous month.

Fixed asset investment gained 8.1 percent on year, beating forecasts for 7/9 percent and unchanged from the July reading.

-

08:19

Food prices in New Zealand added 1.3% in August

Food prices rose 1.3 percent in August 2016, partly influenced by record high banana prices, Statistics New Zealand said today.

Banana prices spiked 22 percent from July, to $3.51 per kilo. The previous peak was $3.23, in March this year.

"Banana prices were at their highest since the series began in 1949, reflecting a supply shortage from Ecuador. Over the last three years, Ecuador has overtaken the Philippines as the main supplier of bananas to New Zealand," consumer prices manager Matt Haigh said today. "Kiwi households spend an average of $88 a year on bananas, making them the most popular fruit."

Seasonally adjusted fruit prices rose 3.2 percent, as the rise in banana prices was partly offset by lower prices for avocados (down 25 percent).

-

08:16

Consumer prices in Germany were 0.4% higher in August

Consumer prices in Germany were 0.4% higher in August 2016 than in August 2015. The consumer price index in August 2016 remained unchanged compared with July 2016. This means that the inflation rate as measured by the consumer price index persists at a low level. A slightly higher rate had last been recorded in January 2016 (+0.5%). The Federal Statistical Office (Destatis) thus confirms its provisional overall results of 30 August 2016.

As in the preceding months, the low inflation rate in August 2016 was mainly due to the decrease in energy prices (-5.9%). Compared with the previous month, the decrease of energy prices slowed down year on year; it had stood at -7.0% in July 2016. Consumers benefited especially from the prices of mineral oil products, which were down in August 2016 on a year earlier (-10.4%, of which heating oil: -15.0%, and motor fuels: -9.1%). The prices of other energy products, too, were below the level of a year earlier (for example, charges for central and district heating: -8.6%; gas: -3.1%). Only electricity prices rose compared with the previous year (+0.7%). Excluding energy prices, the inflation rate in August 2016 would have been +1.1%.

-

08:00

Germany: CPI, y/y , August 0.4% (forecast 0.4%)

-

08:00

Germany: CPI, m/m, August 0.0% (forecast 0.0%)

-

06:41

Global Stocks

Global Stocks

European stocks slid Monday, with investors fleeing risky assets as the markets confronted the prospect that interest rates will be raised in the U.S. this month. Monday's selloff followed Friday's slide of 1.1% for the pan-European index. That drop came after Boston Federal Reserve President Eric Rosengren said a "reasonable case can be made" for raising interest rates in the U.S. A rate hike could hurt appetite for European assets as investors search for higher-yielding investments in the U.S.

U.S. stocks rallied Monday, finishing near session highs and taking back a chunk of Friday's losses, after Federal Reserve Gov. Lael Brainard called for prudence in raising interest rates. Investors were grappling with the prospect of the Federal Reserve tightening monetary policy following a series of hawkish comments from central-bank officials last week.

Asian shares rebounded Tuesday as fears of a rate increase by the U.S. Federal Reserve that had built up in recent days eased following dovish comments overnight from Fed Gov. Lael Brainard. She said that caution by the central bank concerning a rate rise "has served us well in recent months, helping to support continued gains in employment and progress on inflation."

-

04:01

China: Retail Sales y/y, August 10.6% (forecast 10.3%)

-

04:01

China: Fixed Asset Investment, August 8.1% (forecast 8%)

-

04:01

China: Industrial Production y/y, August 6.3% (forecast 6.1%)

-

03:30

Australia: National Australia Bank's Business Confidence, August 6

-

01:51

Japan: BSI Manufacturing Index, Quarter III 2.9

-

00:30

Commodities. Daily history for Sep 12’2016:

(raw materials / closing price /% change)

Oil 46.06 -0.50%

Gold 1,331.10 +0.41%

-

00:30

Stocks. Daily history for Sep 12’2016:

(index / closing price / change items /% change)

Nikkei 225 16,672.92 -292.84 -1.73%

Shanghai Composite 3,020.94 -57.92 -1.88%

S&P/ASX 200 5,219.61 -119.57 -2.24%

FTSE 100 6,700.90 -76.05 -1.12%

CAC 40 4,439.80 -51.60 -1.15%

Xetra DAX 10,431.77 -141.67 -1.34%

S&P 500 2,159.04 +31.23 +1.47%

Dow Jones Industrial Average 18,325.07 +239.62 +1.32%

S&P/TSX Composite 14,597.14 +57.14 +0.39%

-

00:29

Currencies. Daily history for Sep 12’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1234 +0,01%

GBP/USD $1,3334 +0,50%

USD/CHF Chf0,9718 -0,37%

USD/JPY Y101,92 -0,77%

EUR/JPY Y114,50 -0,72%

GBP/JPY Y135,89 -0,27%

AUD/USD $0,7562 +0,33%

NZD/USD $0,7350 +0,39%

USD/CAD C$1,3039 -0,04%

-

00:00

Schedule for today,Tuesday, Sep 13’2016

(time / country / index / period / previous value / forecast)

01:30 Australia National Australia Bank's Business Confidence August 4

02:00 China Retail Sales y/y August 10.2% 10.3%

02:00 China Fixed Asset Investment August 8.1% 8%

02:00 China Industrial Production y/y August 6.0% 6.1%

06:00 Germany CPI, m/m (Finally) August 0.3% 0.0%

06:00 Germany CPI, y/y (Finally) August 0.4% 0.4%

07:15 Switzerland Producer & Import Prices, m/m August -0.1%

07:15 Switzerland Producer & Import Prices, y/y August -0.8%

08:30 United Kingdom Producer Price Index - Output (MoM) August 0.3% 0.2%

08:30 United Kingdom Producer Price Index - Output (YoY) August 0.3% 1%

08:30 United Kingdom Producer Price Index - Input (MoM) August 3.3% 0.5%

08:30 United Kingdom Producer Price Index - Input (YoY) August 4.3% 8.1%

08:30 United Kingdom Retail Price Index, m/m August 0.1% 0.4%

08:30 United Kingdom Retail prices, Y/Y August 1.9% 1.8%

08:30 United Kingdom HICP, m/m August -0.1% 0.4%

08:30 United Kingdom HICP, Y/Y August 0.6% 0.7%

08:30 United Kingdom HICP ex EFAT, Y/Y August 1.3% 1.4%

09:00 Eurozone ZEW Economic Sentiment September 4.6

09:00 Eurozone Employment Change Quarter II 0.3%

09:00 Germany ZEW Survey - Economic Sentiment September 0.5 2.5

18:00 U.S. Federal budget August -113

22:45 New Zealand Current Account Quarter II 1.31

-