Noticias del mercado

-

23:59

Schedule for today, Friday, Sep 18’2015:

(time / country / index / period / previous value / forecast)

08:00 Eurozone Current account, unadjusted, bln July 31.1

11:05 United Kingdom MPC Member Andy Haldane Speaks

12:30 Canada Consumer Price Index m / m August 0.1% 0%

12:30 Canada Consumer price index, y/y August 1.3% 1.3%

12:30 Canada Bank of Canada Consumer Price Index Core, y/y August 2.4% 2.1%

14:00 U.S. Leading Indicators August -0.2% 0.2%

-

22:16

U.S. stocks ended lower

U.S. stocks ended lower, after swinging between gains and losses, as the Federal Reserve's decision to keep interest rates near zero percent raised questions about the strength of the global economy.

The Fed kept its policy interest rate unchanged, showing reluctance to end an era of record monetary stimulus in a time of market turmoil, rising international risks and slow inflation at home. Stocks erased an advance after Chair Janet Yellen indicated that risks in the global economy overshadowed signs of strength in America while inflation remained stubbornly low.

The decision to stand pat on rates keeps a pillar of the bull market in place, as record-low borrowing costs have helped propel stocks higher by nearly 200 percent in the past 6 1/2 years.

It also amplifies uncertainty about the strength of the American economy at a time financial markets have been roiled by concern that a slowdown in China will spread. The S&P 500 had fallen 3.1 percent this year through Wednesday after three years of double-digit gains.

At 5.1 percent, U.S. unemployment is the lowest in seven years and housing sales are rebounding, giving ample evidence that the economy is finding firmer footing. But inflation has remained below the objective of Fed policy makers amid a 51 percent plunge in energy costs over the past 12 months and a rising dollar.

The argument against tightening got a boost from concern that, with central banks from Asia to Europe considering adding stimulus, any Fed move would have fueled a rally in the greenback. A stronger dollar may crimp profits at exporters at a time when analysts forecast earnings at S&P 500 companies will fall in the final two quarters of 2015.

The decision to keep rates near zero wasn't a surprise given the weakness on U.S. equity markets. In four tightenings since 1990, including the tapering of bond purchases announced in 2013, the S&P 500 had posted positive returns over the prior three and six month periods, and was within 3 percent of the gauge's 52-week high, according to a Bank of America Corp. report.

By comparison, the benchmark index was down 4.8 percent over the last three months through yesterday and 6.4 percent below its high of 2,130.82 reached in May. The S&P 500 has alternated between gains and losses for the past nine weeks, a streak of indecision that's happened only three times in 20 years, according to data compiled by Bloomberg.

Thursday's rate decision is being received in a market where the role of computers has grown drastically since the last time the Fed raised rates. With high-frequency firms accounting for about half of trading in the U.S., daily volume has tripled since the early 2000s and now regularly tops 6 billion shares.

The market has whipsawed since China's shock devaluation of its currency on Aug. 11, a move that sent the S&P 500 to its first 10 percent decline since 2011. The Fed has never started tightening within a month of a correction.

Market anxiety has been elevated amid concern that higher U.S. rates could rattle emerging markets and threaten global growth. Price swings on the S&P 500 have widened to 1.5 percent a day in the past month, compared with 0.6 percent this year through July.

-

21:00

DJIA 16889.57 149.62 0.89%, NASDAQ 4949.90 60.67 1.24%, S&P 500 2014.81 19.50 0.98%

-

20:00

U.S.: Fed Interest Rate Decision , 0.25% (forecast 0.25%)

-

18:14

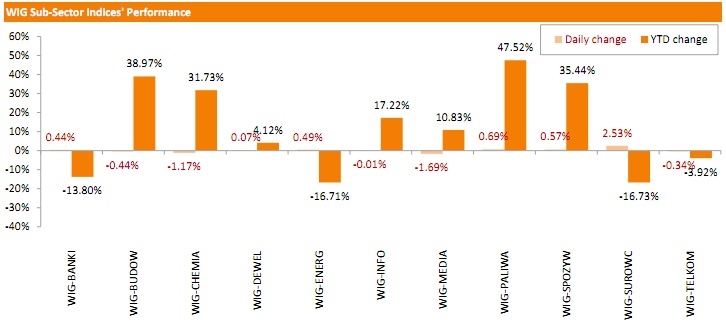

WSE: Session Results

Polish equity market advanced on Thursday. The broad market benchmark, the WIG index, surged by 0.52%. Sector performance within the WIG was mixed. Materials (+2.53%) held up best, while media sector (-1.69%) dropped the most.

The large-cap stocks' gauge, the WIG30 Index, rose by 0.54%. Stock-wise, JSW (WSE: JSW) continued its run-up, adding 7.32%. PZU (WSE: PZU) emerged as the second best-performing stock, returning 3.47%. It was followed by KGHM (WSE: KGH) and BORYSZEW (WSE: BRS), gaining 2.54% and 2.14% respectively. On the other side of the ledger, ALIOR (WSE: ALR) was the sharpest decliner, tumbling by 3.06%. HANDLOWY (WSE: BHW), CYFROWY POLSAT (WSE: CPS) and GRUPA AZOTY (WSE: ATT) also recorded notable losses, with each falling more than 2%.

-

18:00

European stocks close: stocks closed mixed ahead of the Fed's interest rate decision today

Stock indices closed mixed ahead of the Fed's interest rate decision today. The results are scheduled to be released at 18:00 GMT. According to analysts' forecasts, the Fed will not raise its interest rate in September due to concerns over a slowdown in the global economy and low inflationary expectations in the U.S.

The Office for National Statistics released its retail sales data for the U.K. on Thursday. Retail sales in the U.K. increased 0.2% in August, in line with expectations, after a 0.1% rise in July.

The higher growth was partly driven by higher sales of clothing and footwear, which climbed 2.3% in August.

Food sales fell 0.9% in August.

On a yearly basis, retail sales in the U.K. climbed 3.7% in August, missing forecasts of 3.8% increase, after a 4.1% rise in July. July's figure was revised down from a 4.2% gain.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,186.99 -42.22 -0.68 %

DAX 10,229.58 +2.37 +0.02 %

CAC 40 4,655.14 +9.30 +0.20 %

-

18:00

European stocks closed: FTSE 6200.63 -28.58 -0.46%, DAX 10246.55 19.34 0.19%, CAC 40 4663.49 17.65 0.38%

-

17:44

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock indexes were little changed in early trading on Thursday, with investors reluctant to trade aggressively ahead of the Federal Reserve's interest rate decision later in the day. The Fed will announce the outcome of its policy meeting and release its latest economic projections, followed by a news conference by Chair Janet Yellen. An increase in the Fed's benchmark rate, which has been near zero since the depths of the financial crisis in December 2008, would be the first since 2006.

Most of Dow stocks in positive area (18 of 30). Top looser - Verizon Communications Inc. (VZ, -2.81%). Top gainer - UnitedHealth Group Incorporated (UNH, +1.40).

S&P index sectors mixed. Top gainer - Conglomerates (-0.3%). Top gainer - Technology (+0,5%).

At the moment:

Dow 16652.00 -12.00 -0.07%

S&P 500 1986.50 -1.50 -0.08%

Nasdaq 100 4376.50 -4.50 -0.10%

10 Year yield 2,28% -0,02

Oil 47.00 -0.15 -0.32%

Gold 1117.80 -1.20 -0.11%

-

17:43

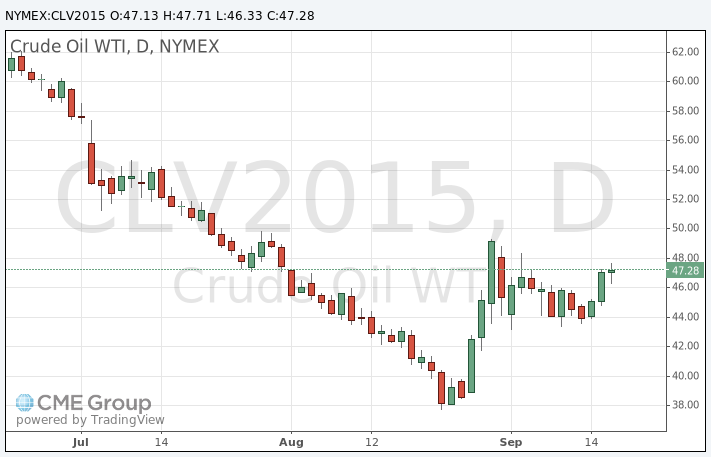

WTI crude rises ahead the Fed’s interest rate decision, while Brent crude oil declines

WTI crude oil rose ahead the Fed's interest rate decision, while Brent crude oil declined. The U.S. oil was supported by the initial jobless claims data. The number of initial jobless claims in the week ending September 12 in the U.S. declined by 11,000 to 264,000 from 275,000 in the previous week. Analysts had expected the initial jobless claims to remain unchanged at 275,000.

Yesterday's U.S. oil inventories data also supported WTI crude oil. U.S. crude inventories fell by 2.1 million barrels to 455.9 million in the week to September 11.

Concerns over the slowdown in the economy in Asia weighed on Brent crude. The Ministry of Finance released its trade data for Japan on the late Wednesday evening. Japan's trade deficit widened to ¥569.7 billion in August from a deficit of ¥268.1 billion in July. Analysts had expected a deficit of ¥541.3 billion.

Exports rose 3.1% year-on-year, while imports dropped 3.1%

WTI crude oil for October delivery rose to $47.71 a barrel on the New York Mercantile Exchange.

Brent crude oil for October decreased to $49.65 a barrel on ICE Futures Europe.

-

17:24

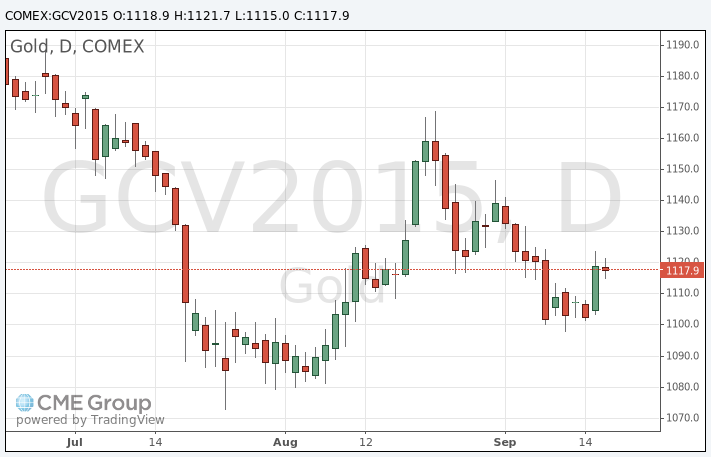

Gold price declines slightly ahead of the release of the Fed's interest rate decision

Gold price decreased slightly ahead of the release of the Fed's interest rate decision. The results are scheduled to be released tomorrow at 18:00 GMT. Market participants were cautious.

According to analysts' forecasts, the Fed will not raise its interest rate in September due to concerns over a slowdown in the global economy and low inflationary expectations in the U.S.

The interest rate hike by the Fed could weigh on gold price. Gold is traded in U.S. dollars. It suffers when the U.S. dollar strengthens, becoming more expensive for holders of other currencies.

October futures for gold on the COMEX today declined to 1114.90 dollars per ounce.

-

16:53

Italy’ trade surplus rises to €8.0 billion in July

The Italian statistical office Istat released its trade data for Italy on Thursday. Italy' trade surplus increased to a seasonally adjusted €8.0 billion in July from €6.9 billion in June.

Exports fell 0.4% in July, while imports decreased 3.7%.

On a yearly basis, exports climbed 6.3% in July, while imports rose 4.2%.

The trade surplus with the EU was €3 billion in July, while the trade surplus with non-EU countries was €5.0 billion.

-

16:28

Philadelphia Federal Reserve Bank’s manufacturing index drops to -6.0 in September

The Philadelphia Federal Reserve Bank released its manufacturing index on Thursday. The index slid to -6.0 in September from 8.3 in August, missing expectations for a decline to 6.0. It was the first negative reading since February 2014.

A reading above zero indicates expansion.

The shipments index was down 14.8 in September from 16.7 in August.

The new orders index increased to 9.4 in September from 5.8 in August.

The prices paid index slid to 0.5 in September from 6.2 in August, while the prices received index decreased to -5.0 from -4.9.

The number of employees index rose to 10.2 in September from 5.3 last month.

According to the report, the future general activity index rose to 44.0 in September from 43.1 in August.

-

16:01

Construction production in the Eurozone rises 1.0% in July

The Eurostat released its construction production data for the Eurozone on Thursday. Construction production in the Eurozone increased 1.0% in July, after a 1.2% decline in June. It was the biggest rise since August 2014.

The rise was driven by higher output in civil engineering and in building. Civil engineering output climbed 1.0% in July, while production in the building sector was up 0.9%.

On a yearly basis, construction output increased 1.8% in July, after a 1.3% drop in June.

Civil engineering climbed by 3.9% year-on-year and building construction was up by 1.3%.

-

16:00

U.S.: Philadelphia Fed Manufacturing Survey, September -6.0 (forecast 6.0)

-

15:45

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.1100(E465mn), $1.1300(E330mn)

USD/JPY: Y120.00($500mn), Y120.25($450mn), Y121.00(2.8bn), Y121.10/15($800mn)

USD/CAD: Cad1.3125($300mn), Cad1.3300($600mn)

AUD/USD: $0.7195/00(A$1.8bn)

NZD/USD: $0.6275(NZ301mn)

EUR/JPY: Y133.00(E200mn), Y138.30(E275mn)

AUD/JPY: Y88.00(A$1.4bn)

AUD/NZD: $1.1335/40(A$460mn)

-

15:42

Greek unemployment rate falls to 24.6% in the second quarter

The Hellenic Statistical Authority released its labour market data for Greece on Thursday. The Greek unemployment rate declined to 24.6% in the second quarter from 26.6% in the previous quarter.

The number of unemployed people fell by 7.3% to 1.2 million in the second quarter.

The youth unemployment rate was down to 49.5% in the second quarter from 51.9% in the first quarter.

-

15:32

U.S. Stocks open: Dow -0.1%, Nasdaq -0.1%, S&P -0.12%

-

15:22

Before the bell: S&P futures -0.30%, NASDAQ futures -0.24%

U.S. equity-index futures dropped as investors split on whether the Federal Reserve will opt to raise interest rates.

Global Stocks:

Nikkei 18,432.27 +260.67 +1.43%

Hang Seng 21,854.63 -112.03 -0.51%

Shanghai Composite 3,086.6 -65.67 -2.08%

FTSE 6,189.38 -39.83 -0.64%

CAC 4,642.48 -3.36 -0.07%

DAX 10,235.35 +8.14 +0.08%

Crude oil $46.69 (-0.98%)

Gold $1116.80 (-0.2%)

-

15:07

U.S. current account deficit narrows to $109.7 billion in the second quarter

The U.S. Commerce Department released its current account data on Thursday. The U.S. current account deficit narrowed to $109.7 billion in the second quarter from $118.3 billion in the first quarter, beating expectations for a deficit of $111.3 billion. The first quarter's figure was revised up from a deficit of $113.3 billion.

The trade deficit decreased due to smaller deficits on goods and secondary income.

Exports of goods rose to $384.8 billion in second quarter from $382.8 billion in the first quarter, while goods imports fell to $573.1 billion from $575.0 billion.

The surplus on primary income climbed to $50.6 billion in the second quarter from $49.7 billion in the first quarter.

-

15:03

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

General Motors Company, NYSE

GM

31.35

0.48%

13.9K

Walt Disney Co

DIS

104.20

0.23%

0.2K

American Express Co

AXP

77.46

0.18%

1.7K

ALTRIA GROUP INC.

MO

55.40

0.07%

1.3K

Procter & Gamble Co

PG

70.13

0.04%

30.0K

Tesla Motors, Inc., NASDAQ

TSLA

262.35

0.04%

19.8K

Visa

V

71.00

0.01%

0.6K

United Technologies Corp

UTX

93.95

0.01%

0.1K

Intel Corp

INTC

29.77

0.00%

12.4K

Microsoft Corp

MSFT

44.30

0.00%

1.1K

Pfizer Inc

PFE

33.18

0.00%

0.6K

JPMorgan Chase and Co

JPM

64.12

-0.03%

29.3K

Home Depot Inc

HD

117.76

-0.05%

5.1K

Verizon Communications Inc

VZ

46.16

-0.06%

0.1K

Deere & Company, NYSE

DE

81.30

-0.06%

0.1K

Goldman Sachs

GS

188.50

-0.07%

1.0K

Cisco Systems Inc

CSCO

26.04

-0.12%

1.3K

Exxon Mobil Corp

XOM

74.21

-0.12%

2.2K

Johnson & Johnson

JNJ

94.50

-0.12%

0.5K

International Business Machines Co...

IBM

148.22

-0.13%

0.7K

Wal-Mart Stores Inc

WMT

64.60

-0.14%

0.6K

Chevron Corp

CVX

78.90

-0.15%

0.8K

Amazon.com Inc., NASDAQ

AMZN

526.52

-0.16%

0.7K

Citigroup Inc., NYSE

C

52.50

-0.17%

2.0K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.82

-0.17%

38.7K

General Electric Co

GE

25.65

-0.19%

7.8K

AT&T Inc

T

32.85

-0.27%

1.8K

Yahoo! Inc., NASDAQ

YHOO

31.31

-0.29%

25.0K

ALCOA INC.

AA

9.83

-0.30%

10.1K

Facebook, Inc.

FB

93.17

-0.30%

11.3K

The Coca-Cola Co

KO

39.03

-0.31%

0.9K

Starbucks Corporation, NASDAQ

SBUX

57.03

-0.40%

3.3K

FedEx Corporation, NYSE

FDX

149.00

-0.42%

4.0K

Twitter, Inc., NYSE

TWTR

27.60

-0.54%

17.6K

Caterpillar Inc

CAT

75.19

-0.59%

0.9K

Ford Motor Co.

F

14.55

-0.61%

0.1K

Apple Inc.

AAPL

115.68

-0.63%

233.9K

Barrick Gold Corporation, NYSE

ABX

6.65

-0.75%

5.4K

Yandex N.V., NASDAQ

YNDX

13.19

-0.98%

1.3K

Hewlett-Packard Co.

HPQ

27.88

-2.07%

2.3K

-

14:59

Housing starts in the U.S. decline 3% in August

The U.S. Commerce Department released the housing market data on Thursday. Housing starts in the U.S. declined 3.0% to 1.126 million annualized rate in August from a 1,161 million pace in July, missing expectations for an increase to 1.170 million.

July's figure was revised down from 1.206 million units.

The decrease was driven by falls in starts of single-family and multifamily homes.

Housing market benefits from the strengthening of the labour market.

Building permits in the U.S. rose 3.5% to 1.170 million annualized rate in August from a 1.130 million pace in July.

Analysts had expected building permits to climb to 1.160 million units.

Starts of single-family homes fell 3.0% in August. Building permits for single-family homes were up 2.8%.

Starts of multifamily buildings decreased 3.0% in August. Permits for multi-family housing jumped 4.7%.

-

14:56

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Tesla Motors (TSLA) target raised to $365 from $360 at Jefferies

FedEx (FDX) target lowered to $157 at RBC Capital Mkts

FedEx (FDX) target lowered to $190 from $210 at Cowen

FedEx (FDX) removed from Conviction Buy List at Goldman

-

14:48

Initial jobless claims decline by 11,000 to 264,000 in the week ending September 12

The U.S. Labor Department released its jobless claims figures on Thursday. The number of initial jobless claims in the week ending September 12 in the U.S. declined by 11,000 to 264,000 from 275,000 in the previous week. Analysts had expected the initial jobless claims to remain unchanged at 275,000.

Jobless claims remained below 300,000 the 28th straight week. This threshold is associated with the strengthening of the labour market.

Continuing jobless claims decreased by 26,000 to 2,237,000 in the week ended September 5.

-

14:30

U.S.: Current account, bln, Quarter II -107.7 (forecast -111.3)

-

14:30

U.S.: Initial Jobless Claims, September 264 (forecast 275)

-

14:30

U.S.: Housing Starts, August 1126 (forecast 1170)

-

14:30

U.S.: Building Permits, August 1170 (forecast 1160)

-

14:30

U.S.: Continuing Jobless Claims, September 2237 (forecast 2260)

-

14:28

European Central Bank’s economic bulletin: the downside risk to the growth and inflation increased

The European Central Bank (ECB) released its economic bulletin on Thursday. The central bank noted that the downside risk to the growth and inflation increased.

The economy in the Eurozone is expected to grow at a weaker pace than previously projected. The ECB pointed out that it could extend its asset-buying programme if needed.

-

14:11

Foreign exchange market. European session: the Swiss franc traded higher against the U.S. dollar after the release of the Swiss National Bank’s interest rate decision

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

01:30 Australia RBA Bulletin

06:35 Japan BOJ Governor Haruhiko Kuroda Speaks

07:30 Switzerland SNB Interest Rate Decision -0.75% -0.75% -0.75%

07:30 Switzerland SNB Monetary Policy Assessment

08:30 United Kingdom Retail Sales (MoM) August 0.1% 0.2% 0.2%

08:30 United Kingdom Retail Sales (YoY) August 4.1% Revised From 4.2% 3.8% 3.7%

The U.S. dollar traded mixed against the most major currencies ahead of the release of the U.S. economic data. Housing starts in the U.S. are expected to decline to 1.170 million units in August from 1.206 million units in July.

The number of building permits is expected to rise to 1.160 million units in August from 1.130 million units in July.

The number of initial jobless claims in the U.S. is expected to remain unchanged at 275,000 last week.

The Philadelphia Federal Reserve Bank' manufacturing index is expected to decrease to 6.0 in September from 8.3 in August.

The Fed will release its interest rate decision at 18:00 GMT.

The euro traded higher against the U.S. dollar in the absence of any major economic reports from the Eurozone.

The British pound traded higher against the U.S. dollar after the mixed U.K. retail sales data. The Office for National Statistics released its retail sales data for the U.K. on Thursday. Retail sales in the U.K. increased 0.2% in August, in line with expectations, after a 0.1% rise in July.

The higher growth was partly driven by higher sales of clothing and footwear, which climbed 2.3% in August.

Food sales fell 0.9% in August.

On a yearly basis, retail sales in the U.K. climbed 3.7% in August, missing forecasts of 3.8% increase, after a 4.1% rise in July. July's figure was revised down from a 4.2% gain.

The Swiss franc traded higher against the U.S. dollar after the release of the Swiss National Bank's (SNB) interest rate decision. The central bank kept the rates on sight deposits at minus 0.75% and said that the bank will remain active in the forex market as the Swiss franc is significantly overvalued and effects inflation and economic growth.

Inflation was downgraded to -1.2% in 2015 from the previous forecast of -1.0% and to be -0.5% in 2016, down from the previous forecast -0.4%. The SNB upgraded to 0.4% in 2017, up from the previous forecast of 0.3%.

The central bank noted that the Swiss economy rose slightly in the second quarter, while employment declined further.

The SNB expects the Swiss economy to return to positive growth in the second half of 2015. Real GDP for 2015 is expected to be about 1%.

EUR/USD: the currency pair increased to $1.1337

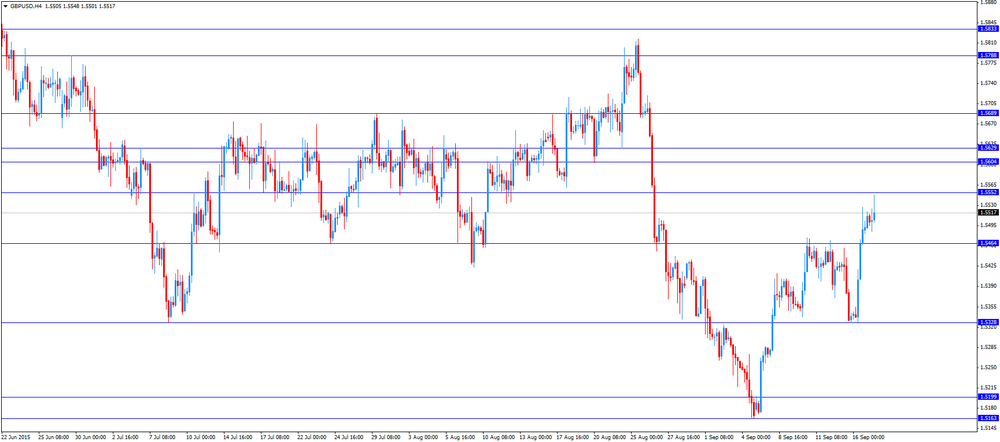

GBP/USD: the currency pair rose to $1.5548

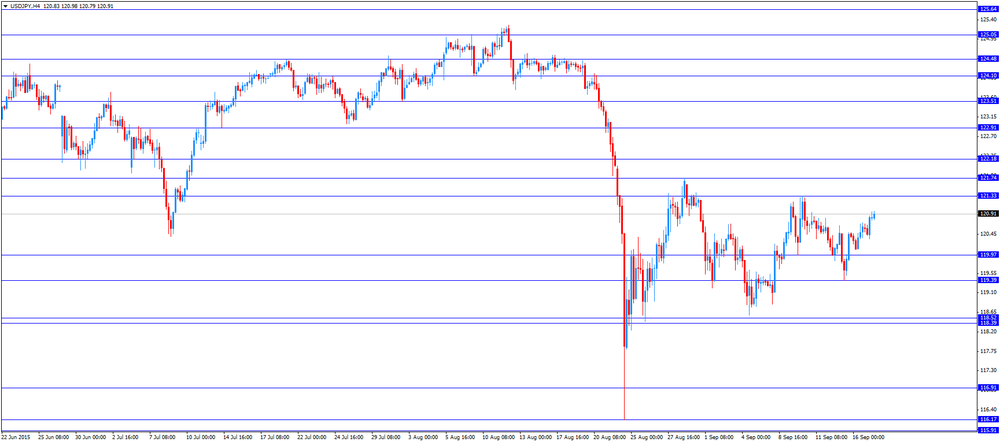

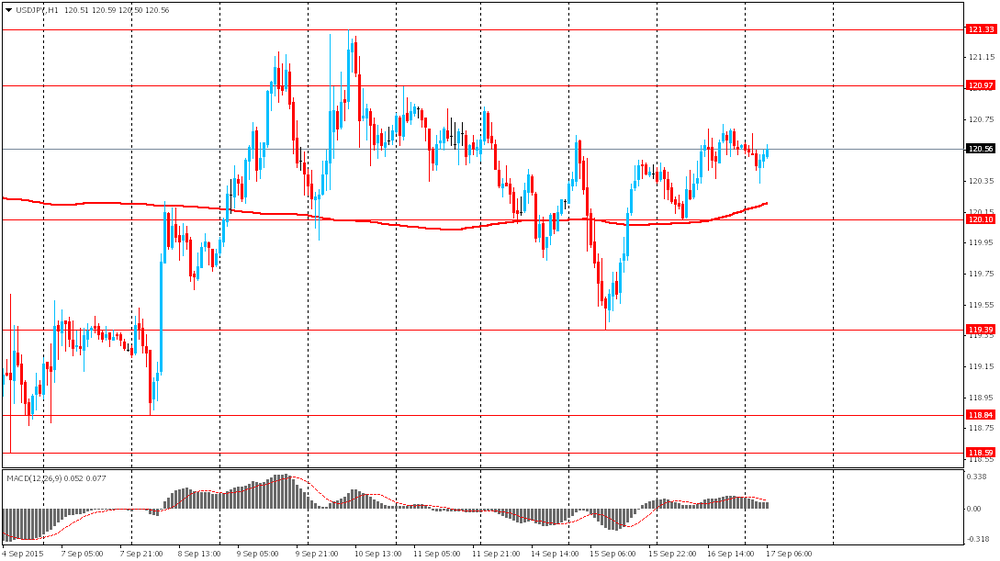

USD/JPY: the currency pair climbed to Y120.98

The most important news that are expected (GMT0):

12:30 U.S. Continuing Jobless Claims September 2260 2260

12:30 U.S. Current account, bln Quarter II -113.3 -111.3

12:30 U.S. Housing Starts August 1206 1170

12:30 U.S. Building Permits August 1130 1160

12:30 U.S. Initial Jobless Claims September 275 275

14:00 U.S. Philadelphia Fed Manufacturing Survey September 8.3 6.0

18:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

18:00 U.S. FOMC Economic Projections

18:00 U.S. FOMC Statement

18:30 U.S. Federal Reserve Press Conference

23:30 Australia RBA's Governor Glenn Stevens Speech

23:50 Japan Monetary Policy Meeting Minutes

-

13:59

Orders

EUR/USD

Offers 1.1320 1.1330-35 1.1355-60 1.1375 1.1390-1.1400 1.1420 1.1450

Bids 1.1285 1.1260 1.1245 1.1225 1.1200 1.1185 1.1165 1.1150 1.1130 1.1100

GBP/USD

Offers 1.5530 1.5550 1.5580-85 1.5600 1.5620 1.5650 1.5685 1.5700-10

Bids 1.5500 1.5485 1.5465 1.5450 1.5425-30 1.5400 1.5380 1.5350 1.5330 1.5300

:

EUR/GBP

Offers 0.7325-30 0.7355-60 0.7380-85 0.7400 0.7425 0.7450

Bids 0.7280-85 0.7260-65 0.7250 0.7230 0.7200

EUR/JPY

Offers 137.00 137.50 138.00

Bids 136.00-10 135.25 135.00 134.80-85 134.65 134.50 134.30 134.00

USD/JPY

Offers 121.00 121.15 121.25 121.50 121.80 122.00 122.30 122.50 122.75 123.00

Bids 120.65 120.50 120.25-30 120.00-10 119.85 119.65 119.50 119.30 119.00 118.85 118.50

AUD/USD

Offers 0.7200 -10 0.7225 0.7250 0.7265 0.7280 0.7300

Bids 0.7155-60 0.7125-30 0.7100 0.7085 0.7065 0.7045-50 0.7020 0.7000

-

12:01

European stock markets mid session: stocks traded mixed ahead of the Fed’s interest rate decision today

Stock indices traded mixed ahead of the Fed's interest rate decision today. The results are scheduled to be released at 18:00 GMT. According to analysts' forecasts, the Fed will not raise its interest rate in September due to concerns over a slowdown in the global economy and low inflationary expectations in the U.S.

The Office for National Statistics released its retail sales data for the U.K. on Thursday. Retail sales in the U.K. increased 0.2% in August, in line with expectations, after a 0.1% rise in July.

The higher growth was partly driven by higher sales of clothing and footwear, which climbed 2.3% in August.

Food sales fell 0.9% in August.

On a yearly basis, retail sales in the U.K. climbed 3.7% in August, missing forecasts of 3.8% increase, after a 4.1% rise in July. July's figure was revised down from a 4.2% gain.

Current figures:

Name Price Change Change %

FTSE 100 6,207.46 -21.75 -0.35 %

DAX 10,240.63 +13.42 +0.13 %

CAC 40 4,644.69 -1.15 -0.02 %

-

11:45

Bank of Japan (BoJ) Governor Haruhiko Kuroda reiterates the central bank will adjust its asset-buying programme if needed

Bank of Japan (BoJ) Governor Haruhiko Kuroda said on Thursday that the central bank will adjust its asset-buying programme if needed.

"The bank will make necessary adjustments on monetary policy, while examining both upside and downside risks on the economy and prices," he said.

Kuroda pointed out that the BoJ's 2% inflation target will be reached once the oil prices stabilise.

The BoJ governor also said that the global economy continued to grow moderately due to a strong growth in U.S. and other advanced economies.

-

11:35

State Secretariat for Economic Affairs upgrades its GDP forecast for 2015

The State Secretariat for Economic Affairs (SECO) released its GDP and inflation forecasts on Thursday. The agency upgraded its 2015 growth forecast to 0.9% from 0.8%. GDP for 2016 was downgraded to 1.5% from 1.6%.

"The economy will remain very subdued in the second half of the year and is likely to only start to strengthen again during the course of 2016," the SECO.

The agency noted that the downside risk to the Swiss economy increased since June due to the slowdown in emerging market.

The average annual unemployment rate is expected to be 3.3% this year and 3.6% next year.

The consumer price inflation is expected to be -1.1% in 2015 and +0.1% in 2016.

-

11:11

Swiss National Bank keeps its rates steady at -0.75%, but it downgrades its inflation forecasts

The Swiss National Bank (SNB) released its interest rate decision on Thursday. The central bank kept the rates on sight deposits at minus 0.75% and said that the bank will remain active in the forex market as the Swiss franc is significantly overvalued and effects inflation and economic growth.

Inflation was downgraded to -1.2% in 2015 from the previous forecast of -1.0% and to be -0.5% in 2016, down from the previous forecast -0.4%. The SNB upgraded to 0.4% in 2017, up from the previous forecast of 0.3%.

The central bank noted that the Swiss economy rose slightly in the second quarter, while employment declined further.

The SNB expects the Swiss economy to return to positive growth in the second half of 2015. Real GDP for 2015 is expected to be about 1%.

Domestic demand should provide further support to the economy, according to the SNB.

-

10:56

UK retail sales rise 0.2% in August

The Office for National Statistics released its retail sales data for the U.K. on Thursday. Retail sales in the U.K. increased 0.2% in August, in line with expectations, after a 0.1% rise in July.

The higher growth was partly driven by higher sales of clothing and footwear, which climbed 2.3% in August.

Food sales fell 0.9% in August.

On a yearly basis, retail sales in the U.K. climbed 3.7% in August, missing forecasts of 3.8% increase, after a 4.1% rise in July. July's figure was revised down from a 4.2% gain.

-

10:43

New Zealand's economy expanded at 0.4% in the second quarter

Statistics New Zealand released its GDP data on late Wednesday evening. New Zealand's GDP rose 0.4% in the second quarter, missing expectations for a 0.5% increase, after a 0.2% gain in the first quarter.

On a yearly basis, New Zealand's GDP climbed by 2.4% in the second quarter, missing expectations for a 2.5% gain, after a 2.7% rise in the first quarter. The first quarter's figure was revised up from a 2.6% rise.

The increase was driven by a rise in the service and primary industries.

The services sector rose 0.5% in the second quarter, while agriculture climbed 3.0% in Q2 as the meat and dairy production increased.

-

10:35

Bank of England Governor Mark Carney: it will become clearer “around the turn of this year" whether to start raising interest rates or not

Bank of England (BoE) Governor Mark Carney repeated on Wednesday that it will become clearer "around the turn of this year" whether to start raising interest rates or not.

Carney pointed out that it is necessary that GDP and wages will to continue to rise and the inflation will start to firm up before start raising interest rates.

"Then the decision comes into sharper relief and it may become appropriate to begin to withdraw stimulus," he said.

-

10:30

United Kingdom: Retail Sales (MoM), August 0.2% (forecast 0.2%)

-

10:30

United Kingdom: Retail Sales (YoY) , August 3.7% (forecast 3.8%)

-

10:22

French Finance Minister Michel Sapin: the government spending is falling

French Finance Minister Michel Sapin said on Wednesday the government spending is falling, and the government will meet its budget target for the "first time in years."

The government forecasted the country's economy to expand 1% this year and 1.5% next year. The budget deficit is expected to be 3.8% of GDP in 2015, 3.3% in 2016 and below 3% in 2017.

The government debt is expected to below 100% of GDP in 2016, Sapin said.

-

10:10

Japan's trade deficit widens to ¥569.7 billion in August

The Ministry of Finance released its trade data for Japan on the late Wednesday evening. Japan's trade deficit widened to ¥569.7 billion in August from a deficit of ¥268.1 billion in July. Analysts had expected a deficit of ¥541.3 billion.

The adjusted trade deficit was ¥358.8 billion in August, down from a deficit of ¥375.1 billion in July. July's figure was revised up from a deficit of ¥368.8 billion.

Exports rose 3.1% year-on-year, while imports dropped 3.1%.

Exports to Asia climbed by 1.1% year-on-year, exports to the United States increased by 11.1%, exports to China dropped by 4.6%, while exports to the European Union were down 0.2%.

Imports from Asia climbed 7.4% year-on-year, imports from the United States jumped 5.4%, and imports from China gained 14.6%, while imports from the European Union rose 21.8%.

-

09:32

Switzerland: SNB Interest Rate Decision, -0.75% (forecast -0.75%)

-

08:50

Oil prices advanced

West Texas Intermediate futures for October delivery climbed to $47.27 (+0.25%), while Brent crude rose to $50.09 (+0.68%) still supported by Energy Information Administration's data released yesterday. However gains are slowing as the focus returns to the Federal Reserve's two day meeting, which ends today.

Yesterday's report showed a 2.1 million barrel drop in U.S. crude inventories in the week to September 11 including a 1.9 million barrel decline at the Cushing trading hub.

Some analysts note that non-OPEC and non-U.S. supply started to decline as low prices weigh on producers. Output cuts would lead to a combined reduction of 400 million barrels per day by the end of the year, but the global glut would persist through 2016.

-

08:33

Gold climbed ahead of Federal Reserve meeting

Gold climbed to $1,119.50 (+0.04%) as weak inflation data from the U.S. eased concerns about a possible rate hike by the Federal Reserve today. Expectations that the central bank would raise rates this month had already declined due to recent concerns over China's economic slowdown and volatility in financial markets. However uncertainty persists. Higher rates could harm demand for non-interest-paying precious metal.

-

08:19

Options levels on thursday, September 17, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1458 (3232)

$1.1408 (1435)

$1.1354 (652)

Price at time of writing this review: $1.1291

Support levels (open interest**, contracts):

$1.1224 (441)

$1.1186 (934)

$1.1136 (2229)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 49391 contracts, with the maximum number of contracts with strike price $1,1600 (4733);

- Overall open interest on the PUT options with the expiration date October, 9 is 65940 contracts, with the maximum number of contracts with strike price $1,1000 (6711);

- The ratio of PUT/CALL was 1.34 versus 1.32 from the previous trading day according to data from September, 16

GBP/USD

Resistance levels (open interest**, contracts)

$1.5803 (1128)

$1.5705 (1391)

$1.5608 (1372)

Price at time of writing this review: $1.5502

Support levels (open interest**, contracts):

$1.5391 (861)

$1.5294 (1169)

$1.5196 (2742)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 22283 contracts, with the maximum number of contracts with strike price $1,5500 (1637);

- Overall open interest on the PUT options with the expiration date October, 9 is 20786 contracts, with the maximum number of contracts with strike price $1,5200 (2742);

- The ratio of PUT/CALL was 0.93 versus 0.99 from the previous trading day according to data from September, 16

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:16

Global Stocks: U.S. and Asian indices rose

U.S. stock indices rose in a range-bound session on Wednesday as investors prepared for a Federal Reserve's interest rate decision.

The Dow Jones Industrial Average gained 140.10 points, or 0.8%, to 16,739.95 (29 out of its 30 components rose). The S&P 500 rose 17.22 points, or 0.9%, to 1,995.31. The Nasdaq Composite Index added 28.72 points, or 0.6%, to 4,889.24.

Energy companies led the gains amid higher oil prices.

Bureau of Labor Statistics reported on Wednesday that consumer prices declined slightly in August marking their first decline in January. Prices were generally dragged down by low energy costs. The consumer price index fell by 0.1% in August after a 0.1% rise in July. The core index rose by 0.1%. Economists expected the CPI to stay unchanged, while the gain in the core CPI was in line with forecasts.

This morning in Asia Hong Kong Hang Seng rose 0.77%, or 169.70 points, to 22,136.36. China Shanghai Composite Index gained 0.51%, or 16.04 point, to 3,168.31. The Nikkei added 1.20%, or 218.95 points, to 18,390.55.

Asian stock indices rose amid gains in U.S. equities and oil prices. Investors are also waiting for news from the Federal Reserve.

Japanese stocks rose despite weak trade data. The country's exports rose 3.1% in August on an annualized basis vs a 7.6% gain in the previous month and a 4.0% yearly increase expected by analysts. Imports fell by 3.1% y/y, exceeding expectations for a 2.2% decrease.

This led to a monthly deficit of 569.7 billion yen.

-

08:13

Foreign exchange market. Asian session: the euro gained

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

01:30 Australia RBA Bulletin

The euro climbed slightly against the U.S. dollar amid a weak inflation report from the U.S. However the single currency was also weighed by euro zone inflation data. U.S. Bureau of Labor Statistics reported on Wednesday that consumer prices declined slightly in August marking their first decline since January. Prices were generally dragged down by low energy costs. The consumer price index fell by 0.1% in August after a 0.1% rise in July. The core index rose by 0.1%. Economists expected the CPI to stay unchanged, while the gain in the core CPI was in line with forecasts.

At the beginning of this session the New Zealand dollar declined against the greenback amid disappointing GDP data. New Zealand's GDP rose by 0.4% in the second quarter compared to +0.2% reported previously, but it fell short of expectations for a 0.5% rise. On an annualized basis the index came in at 2.4% vs 2.7% previous and 2.5% expected. However later on the NZD recovered amid the greenback's general weakness.

Investors are cautious ahead of the end of the FOMC's meeting. A survey by the Wall Street Journal showed that approximately 46% of the economists surveyed last week expect the Fed to raise rates in September. 35% of economists said the Fed would raise rates in December and 9.5% said they expect a liftoff in 2016. At the same time Barclays surveyed 700 investors last week and only 36% of the respondents believe that the central bank of the U.S. will raise rates in September.

EUR/USD: the pair fluctuated within $1.1285-15 in Asian trade

USD/JPY: the pair fluctuated around Y120.60

GBP/USD: the pair traded within $1.5495-15

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

06:35 Japan BOJ Governor Haruhiko Kuroda Speaks

07:30 Switzerland SNB Interest Rate Decision -0.75% -0.75%

07:30 Switzerland SNB Monetary Policy Assessment

08:30 United Kingdom Retail Sales (MoM) August 0.1% 0.2%

08:30 United Kingdom Retail Sales (YoY) August 4.2% 3.8%

12:30 U.S. Continuing Jobless Claims September 2260 2260

12:30 U.S. Current account, bln Quarter II -113.3 -111.3

12:30 U.S. Housing Starts August 1206 1170

12:30 U.S. Building Permits August 1130 1160

12:30 U.S. Initial Jobless Claims September 275 275

14:00 U.S. Philadelphia Fed Manufacturing Survey September 8.3 6.0

18:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

18:00 U.S. FOMC Economic Projections

18:00 U.S. FOMC Statement

18:30 U.S. Federal Reserve Press Conference

23:30 Australia RBA's Governor Glenn Stevens Speech

23:50 Japan Monetary Policy Meeting Minutes

-

04:03

Основные фондовые индексы Азиатско-Тихоокеанского региона начали торги в плюсе: Nikkei 225 18,406.73 +235.13 +1.29 %, Hang Seng 22,075.01 +108.35 +0.49 %, Shanghai Composite 3,117.93 -34.33 -1.09 %

-

01:53

Japan: Trade Balance Total, bln, August -569.7 (forecast -541.3)

-

00:46

New Zealand: GDP y/y, Quarter II 2.4% (forecast 2.5%)

-

00:45

New Zealand: GDP q/q, Quarter II 0.4% (forecast 0.5%)

-

00:43

Commodities. Daily history for Sep 16’2015:

(raw materials / closing price /% change)

Oil 47.13 -0.04%

Gold 1,118.40 -0.05%

-

00:41

Stocks. Daily history for Sep 16’2015:

(index / closing price / change items /% change)

Nikkei 225 18,171.6 +145.12 +0.81 %

Hang Seng 21,966.66 +511.43 +2.38 %

S&P/ASX 200 5,098.86 +80.43 +1.60 %

Shanghai Composite 3,152.66 +147.49 +4.91 %

FTSE 100 6,229.21 +91.61 +1.49 %

CAC 40 4,645.84 +76.47 +1.67 %

Xetra DAX 10,227.21 +39.08 +0.38 %

S&P 500 1,995.31 +17.22 +0.87 %

NASDAQ Composite 4,889.24 +28.72 +0.59 %

Dow Jones 16,739.95 +140.10 +0.84 %

-

00:38

Currencies. Daily history for Sep 16’2015:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1288 -0,25%

GBP/USD $1,5492 +0,43%

USD/CHF Chf0,9708 -0,30%

USD/JPY Y120,58 +0,15%

EUR/JPY Y136,13 +0,37%

GBP/JPY Y186,8 +1,13%

AUD/USD $0,7189 +0,77%

NZD/USD $0,6372 +0,35%

USD/CAD C$1,3173 -0,59%

-

00:03

Schedule for today, Thursday, Sep 17’2015:

(time / country / index / period / previous value / forecast)

1:30 Australia RBA Bulletin

06:35и Japan BOJ Governor Haruhiko Kuroda Speaks

07:30 Switzerland SNB Interest Rate Decision -0.75%

07:30 Switzerland SNB Monetary Policy Assessment

08:30 United Kingdom Retail Sales (MoM) August 0.1% 0.2%

08:30 United Kingdom Retail Sales (YoY) August 4.2% 3.8%

12:30 U.S. Continuing Jobless Claims September 2260 2260

12:30 U.S. Current account, bln Quarter II -113.3 -111.3

12:30 U.S. Housing Starts August 1206 1170

12:30 U.S. Building Permits August 1130 1160

12:30 U.S. Initial Jobless Claims September 275 275

14:00 U.S. Philadelphia Fed Manufacturing Survey September 8.3 6.0

18:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

18:00 U.S. FOMC Economic Projections

18:00 U.S. FOMC Statement

18:30 U.S. Federal Reserve Press Conference

23:30 Australia RBA's Governor Glenn Stevens Speech

23:50 Japan Monetary Policy Meeting Minutes

-