Noticias del mercado

-

22:34

U.S. stocks closed

U.S. stocks overcame an afternoon slump to rebound from the lowest level in 21 months, as crude surged toward $30 amid signals from China and Europe that officials will add to stimulus if needed. Treasuries fell with gold as haven demand waned.

The Dow Jones Industrial Average rose 115 points in a seesaw session that had the gauge erase almost all of a 270-point rally before ending higher. Investors piled into risk assets, boosting European equities to the biggest gain in a month and sending crude 4.2 percent higher, after the European Central Bank said it may bolster support as soon as March. China's vice president said the government would intervene to tamp down market volatility. The yield on the 10-year Treasury note rose to 2.02 percent.

ECB President Mario Draghi signaled at his briefing Thursday that additional support is available as soon as March as distress in China shows few signs of abating and oil's slump fuels disinflation. Risks to economic growth have increased amid the financial-market turmoil that has erased more than $15 trillion from global equity values as markets from Japan to Germany and Brazil plunged into bear territory.

Crude's climb above $29 a barrel in New York provided a glimmer of relief to commodities investors battered by an oversupply in resources from oil to copper and wheat. Calling the country's market "not yet mature," China's Vice President Li Yuanchao said the government would boost regulation in an effort to avoid too much volatility. Corporate earnings may also offer clues on the robustness of the U.S. recovery, with the few companies that have reported so far mostly exceeding estimates.

The S&P 500 rose 0.5 percent at 4 p.m. in New York, capping a session that saw it rise as much as 1.6 percent after falling 1.2 percent Wednesday to the lowest since April 2014. The index has swung from gains to losses for seven consecutive sessions as investors seek a bottom to a rout this year that's erased 8.3 percent from the benchmark.

Energy shares paced gains with a 3.1 percent advance. Chevron Corp. climbed 2.6 percent and Home Depot Inc. surged 3.5 percent as energy and consumer discretionary companies paced the rebound from yesterday's selloff. Verizon Communications Inc. gained 3.5 percent after its profit beat estimates. Union Pacific Corp. fell 4.9 percent after its earnings missed forecasts.

-

21:01

DJIA 15924.05 157.31 1.00%, NASDAQ 4492.55 20.86 0.47%, S&P 500 1874.47 15.14 0.81%

-

20:22

American focus: the euro fell on Draghi comments

The euro fell sharply against the US dollar after European Central Bank President Mario Draghi made it clear that the Governing Council may decide on additional stimulus measures at its next meeting in March. Draghi also said that the outlook for inflation "significantly" worsened.

Earlier Thursday, the ECB left its key interest rate unchanged, despite the fact that low energy prices and concerns about the impact on the world economy of China may attempt to disrupt the central bank to return inflation to the target level.

Speaking at a press conference Mario Draghi said the economic stimulus measures implemented by the central bank in June 2014 and most recently extended in December, "strengthened the stability of the euro zone to the recent global economic shocks."

However, he also added that the recent decline in oil prices suggests that the annual inflation rate in 2016 is likely to be "significantly" lower than the forecasts published in the last month.

Economists expect the ECB that inflation will rise from the December level of 0.2% this year to average 1%, and then continue to grow in 2017. However, Draghi said that under the current conditions in the coming months, prices could fall again.

"We re-evaluate our policies and may amend it at the next meeting in March," - said Draghi.

Later, the dollar lost some positions recruited, the dynamics of the US dollar affected the mixed US economic data. The report submitted by the Federal Reserve Bank of Philadelphia, showed that in January, the index of business activity showed a moderate increase, reaching at the same level of -3.5 points versus -5.9 points in December. It is worth noting that many economists had expected growth of this indicator only to the level of -5.0 points.

US Department of Labor said the number of Americans who first applied for unemployment benefits, increased dramatically in the last week, reaching the highest level since the beginning of July, and pointing to some loss of momentum of the labor market. According to the report for the week ended 16 January, the number of initial applications for unemployment insurance increased by 10,000, to a level of 293,000 (seasonally adjusted). Economists, however, expected to decline to 278 000. The figures for the previous week was revised up to 283 000 to 284 000. It is worth emphasizing the number of calls is below 300,000 for 46 consecutive weeks (the longest series since 1970).

The yen fell against the dollar under the influence of today's announcement of government officials. "The Bank of Japan should expand the easing of monetary policy," - said one of the assistants to the Prime Minister of Japan Shinzo Abe. He is sure that there are all necessary conditions. According to him, the volatility in the world markets threatens to undermine "abenomics", which was intended to revive Japan's economy. "The conditions for further easing have developed," - said the adviser, referring to Japan's stock market decline, the strengthening of the yen, sluggish economic growth and easing inflation expectations. Meanwhile, Adviser to the Prime Minister of Japan Abe Shibayama said it was too early to talk about new measures to mitigate the Bank of Japan, as falling stock markets may be temporary. "At this stage we need to closely monitor the situation and exchange information with financial authorities in other countries," - he added. This statement was made amid growing talk about the fact that the Central Bank may take action to stimulate already at the meeting on 28-29 January, increasing the amount of asset purchases.

-

19:27

Wall Street. Major U.S. stock-indexes rose

Major U.S. stocks higher on Thursday as oil prices rallied and ECB President Mario Draghi raised hopes of easing monetary policy further as soon as March.

The European Central Bank kept its main rates on hold and Draghi said the central bank would "review and possibly reconsider" its monetary policy stance in March. Many analysts had not expected a rate cut before June.

Oil prices recovered from earlier losses and were sharply higher.

Almost all of Dow stocks in positive area (28 of 30). Top looser - UnitedHealth Group Incorporated (UNH, -0,85%). Top gainer - The Home Depot, Inc. (HD, +4,34%).

All of S&P sectors in positive area. Top gainer - Basic Materials (+3,8%).

At the moment:

Dow 15916.00 +199.00 +1.27%

S&P 500 1877.00 +22.00 +1.19%

Nasdaq 100 4177.00 +44.00 +1.06%

Oil 30.12 +1.77 +6.24%

Gold 1093.60 -12.60 -1.14%

U.S. 10yr 2.03 +0.05

-

18:06

European stocks closed: FTSE 5773.79 100.21 1.77%, DAX 9574.16 182.52 1.94%, CAC 40 4206.40 81.45 1.97%

-

18:01

European stocks close: stocks closed higher on comments by the European Central Bank President Mario Draghi

Stock indices traded higher on comments by the European Central Bank (ECB) President Mario Draghi. He hinted at a press conference on Thursday that the central bank may add further stimulus measures at its meeting in March as downside risks rose.

"Downside risks have increased again amid heightened uncertainty about emerging market economies' growth prospects, volatility in financial and commodity markets, and geopolitical risks. In this environment, euro area inflation dynamics also continue to be weaker than expected," he said.

"It will therefore be necessary to review and possibly reconsider our monetary policy stance at our next meeting in early March, when the new staff macroeconomic projections become available which will also cover the year 2018," Draghi added.

The ECB president pointed out that the central bank's quantitative easing was working, and interest rate is expected to remain "at present or lower levels for an extended period of time".

Earlier, the ECB kept its interest rate unchanged at 0.05%.

Indexes on the close:

Name Price Change Change %

FTSE 100 5,773.79 +100.21 +1.77 %

DAX 9,574.16 +182.52 +1.94 %

CAC 40 4,206.4 +81.45 +1.97 %

-

17:55

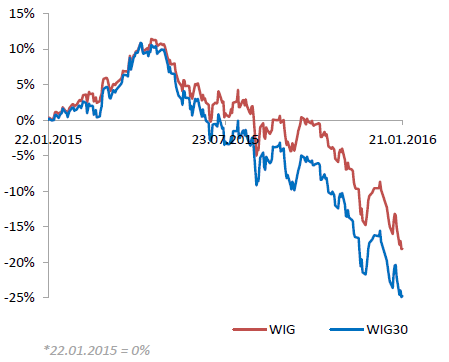

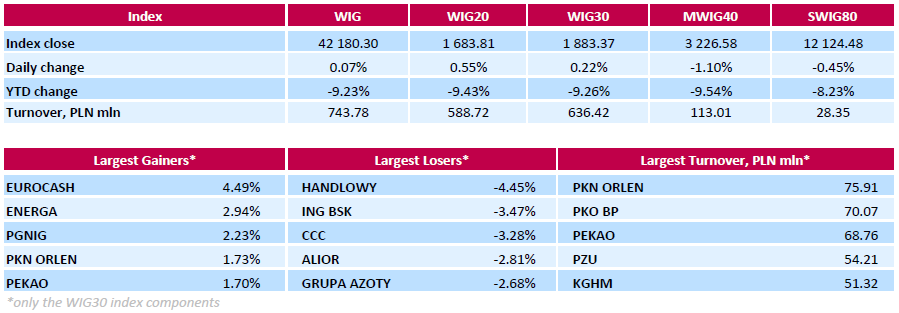

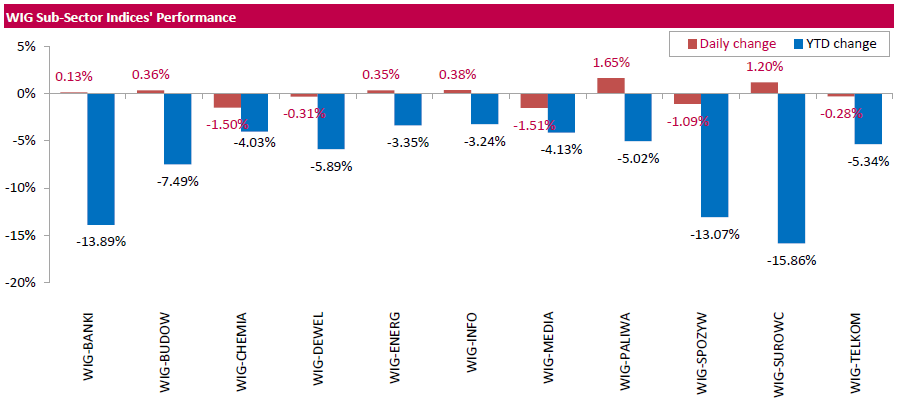

WSE: Session Results

Polish equity market closed slightly higher on Thursday. The broad market measure, the WIG index, added 0.07%. Sector performance within the WIG Index was mixed. Oil and gas sector (+1.65%) was best performer, while media sector (-1.51%) and chemicals (-1.50%) recorded the worst results.

The large-cap benchmark, the WIG30 Index, rose by 0.22%. Within the index components, FMCG wholesaler EUROCASH (WSE: EUR) led the advancers, climbing by 4.49%. It was followed by genco ENERGA (WSE: ENG), oil and gas companies PGNIG (WSE: PGN) and PNK ORLEN (WSE: PKN), and bank PEKAO (WSE: PEO), jumping by 1.7%-2.94%. On the other side of the ledger, banking sector names HANDLOWY (WSE: BHW), ING BSK (WSE: ING) and ALIOR (WSE: ALR) were among the weakest performers, tumbling by 4.45%, 3.47% and 2.81% respectively. Footwear retailer CCC (WSE: CCC) lost 3.28%.

-

17:52

Business NZ performance of manufacturing index for New Zealand rises to 56.7 in December

According to the Business NZ Survey published on late Wednesday evening, the Business NZ performance of manufacturing index (PMI) for New Zealand rose to 56.7 in December from 54.9 in November. It was the highest level since October 2014.

November's figure was revised up from 54.7.

A reading above 50 indicates expansion in the manufacturing sector.

The rise was mainly driven by a faster expansion in new orders, deliveries, production and finished stocks.

"Overall, it has been a solid and positive year for the sector. Although the PMI averaged 54.2 over 2015 compared with 56.0 for both 2013 and 2014, the slightly lower expansion level was partly due to the first half of 2015 experiencing a moderate patch of growth. However, results over the last few months have seen the sector in stronger expansion," Business NZ's executive director for manufacturing, Catherine Beard, said.

-

17:45

M3 money supply in Switzerland rises 1.6% in December

The Swiss National Bank (SNB) released its money supply data on Thursday. M3 money supply in Switzerland increased 1.6% year-on-year in December, after a 2.1% rise in November.

M1 money supply was down 1.6% year-on-year in December, after a 2.8% decrease in November.

-

17:42

Oil prices climb despite an increase in U.S. crude inventories

Oil prices rose despite an increase in U.S. crude inventories. The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Thursday. U.S. crude inventories increased by 3.98 million barrels to 486.5 million in the week to January 15.

Analysts had expected U.S. crude oil inventories to rise by 2.75 million barrels.

Gasoline inventories increased by 4.6 million barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, climbed by 191,000 barrels.

U.S. crude oil imports decreased by 409,000 barrels per day.

Refineries in the U.S. were running at 90.6% of capacity, down from 91.2% the previous week.

Concerns over the global oil oversupply continued to weigh on oil prices. The chairman of Saudi Arabian Oil Co. (Saudi Aramco), Saudi Arabian state-owned oil producer, Khalid al-Falid said at the World Economic Forum in Davos on Thursday that Saudi Arabia can withstand low oil prices for a long period as production costs in Saudi Arabia are the lowest. But he expects higher prices by the end of the year.

al-Falid noted that the country is ready to cooperate with other oil producer to balance the oil market.

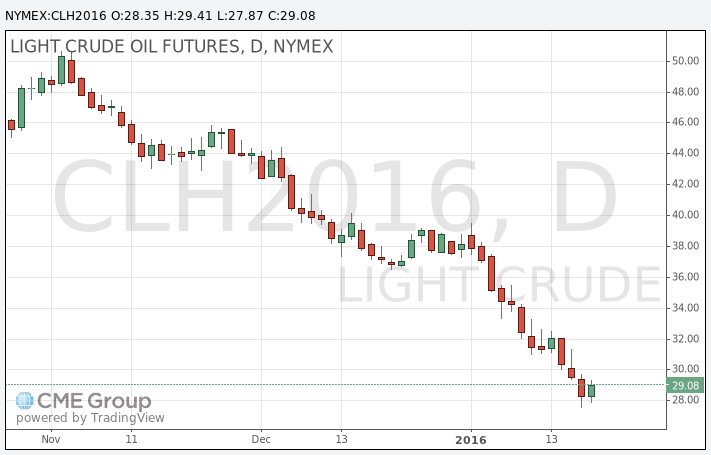

WTI crude oil for March delivery rose to $29.41 a barrel on the New York Mercantile Exchange.

Brent crude oil for March increased to $28.73 a barrel on ICE Futures Europe.

-

17:39

RICS house price balance for the U.K. increased to +50% in December

The Royal Institution of Chartered Surveyors' (RICS) released its house price data for the U.K. on Thursday. The monthly house price balance increased to +50% in December from +49% in November.

RICS Chief Economist, Simon Rubinsohn, said that a further heating up of the U.K. housing market is likely before April.

-

17:25

Gold declines on a stronger U.S. dollar

Gold price fell on a stronger U.S. dollar. The U.S. dollar rose on comments by the European Central Bank (ECB) President Mario Draghi. He hinted at a press conference on Thursday that the central bank may add further stimulus measures at its meeting in March as downside risks rose.

"Downside risks have increased again amid heightened uncertainty about emerging market economies' growth prospects, volatility in financial and commodity markets, and geopolitical risks. In this environment, euro area inflation dynamics also continue to be weaker than expected," he said.

"It will therefore be necessary to review and possibly reconsider our monetary policy stance at our next meeting in early March, when the new staff macroeconomic projections become available which will also cover the year 2018," Draghi added.

The U.S. economic data was mixed. The U.S. Labor Department released its jobless claims figures on Thursday. The number of initial jobless claims in the week ending January 16 in the U.S. rose by 10,000 to 293,000 from 283,000 in the previous week. Analysts had expected jobless claims to fall to 278,000.

The Philadelphia Federal Reserve Bank released its manufacturing index on Thursday. The index climbed to -3.5 in January from -10.2 in December, exceeding expectations for an increase to -5.0.

February futures for gold on the COMEX today dropped to 1092.50 dollars per ounce.

-

17:21

U.S. crude inventories climb by 3.98 million barrels to 486.5 million in the week to January 15

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Thursday. U.S. crude inventories increased by 3.98 million barrels to 486.5 million in the week to January 15.

Analysts had expected U.S. crude oil inventories to rise by 2.75 million barrels.

Gasoline inventories increased by 4.6 million barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, climbed by 191,000 barrels.

U.S. crude oil imports decreased by 409,000 barrels per day.

Refineries in the U.S. were running at 90.6% of capacity, down from 91.2% the previous week.

-

17:00

U.S.: Crude Oil Inventories, January 3.979 (forecast 2.750)

-

16:45

The People's Bank of China injects 400 billion yuan into market

The People's Bank of China (PBoC) said on its website on Thursday that it injected 400 billion yuan ($61 billion) into market to boost liquidity via short-term loans (reverse-repurchase agreements).

The central bank usually injects extra money before the Lunar New Year holiday.

-

16:36

Chinese Vice President Li Yuanchao: China will remain the global growth engine

Chinese Vice President Li Yuanchao said in an interview with Bloomberg News that China will remain the global growth engine.

He pointed out that the country's economy is expected to grow between 6% and 7% over the next five years.

Li noted that the weak global demand weighs on the Chinese economy, but he added that the country's economy "has enormous development potential".

-

16:28

Eurozone’s preliminary consumer confidence index falls to -6.3 in January

The European Commission released its preliminary consumer confidence figures for the Eurozone on Thursday. Eurozone's preliminary consumer confidence index fell to -6.3 in January from -5.7 in December. Analysts had expected the index to remain unchanged at -5.7.

European Union's consumer confidence index climbed by 0.3 points to -4.2 in January.

-

16:19

Chairman of Saudi Arabian Oil Co. Khalid al-Falid: Saudi Arabia can withstand low oil prices for a long period

The chairman of Saudi Arabian Oil Co. (Saudi Aramco), Saudi Arabian state-owned oil producer, Khalid al-Falid said at the World Economic Forum in Davos on Thursday that Saudi Arabia can withstand low oil prices for a long period as production costs in Saudi Arabia are the lowest. But he expects higher prices by the end of the year.

al-Falid noted that the country is ready to cooperate with other oil producer to balance the oil market.

-

16:08

The European Central Bank President Mario Draghi hints that the central bank may add further stimulus measures in March

The European Central Bank (ECB) President Mario Draghi hinted at a press conference on Thursday that the central bank may add further stimulus measures at its meeting in March as downside risks rose.

"Downside risks have increased again amid heightened uncertainty about emerging market economies' growth prospects, volatility in financial and commodity markets, and geopolitical risks. In this environment, euro area inflation dynamics also continue to be weaker than expected," he said.

"It will therefore be necessary to review and possibly reconsider our monetary policy stance at our next meeting in early March, when the new staff macroeconomic projections become available which will also cover the year 2018," Draghi added.

The ECB president pointed out that the central bank's quantitative easing was working, and interest rate is expected to remain "at present or lower levels for an extended period of time".

Draghi noted that the ECB is ready to act if needed.

-

16:00

Eurozone: Consumer Confidence, January -6.3 (forecast -5.7)

-

15:35

U.S. Stocks open: Dow +0.33%, Nasdaq -0.05%, S&P +0.20%

-

15:28

Before the bell: S&P futures +0.69%, NASDAQ futures +0.75%

U.S. stock-index futures rose.

Global Stocks:

Nikkei 16,017.26 -398.93 -2.43%

Hang Seng 18,542.15 -344.15 -1.82%

Shanghai Composite 2,880.8 -95.89 -3.22%

FTSE 5,758.92 +85.34 +1.50%

CAC 4,221.28 +96.33 +2.34%

DAX 9,610.74 +219.10 +2.33%

Crude oil $28.31 (-0.14%)

Gold $1095.70 (-0.95%)

-

15:05

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Twitter, Inc., NYSE

TWTR

17.95

3.28%

3.6K

ALCOA INC.

AA

6.89

2.23%

30.0K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

4.16

2.21%

9.5K

Tesla Motors, Inc., NASDAQ

TSLA

202.00

1.66%

28.5K

Google Inc.

GOOG

709.50

1.58%

1.9K

Citigroup Inc., NYSE

C

41.00

1.26%

5.4K

Verizon Communications Inc

VZ

44.94

1.17%

23.4K

Amazon.com Inc., NASDAQ

AMZN

578.44

1.17%

4.2K

Facebook, Inc.

FB

95.34

1.05%

28.0K

Walt Disney Co

DIS

93.39

0.92%

151.8K

Microsoft Corp

MSFT

51.24

0.89%

11.7K

AT&T Inc

T

34.20

0.88%

6.7K

General Electric Co

GE

28.24

0.86%

16.5K

Ford Motor Co.

F

12.00

0.84%

1.9K

Starbucks Corporation, NASDAQ

SBUX

57.40

0.84%

3.6K

Goldman Sachs

GS

155.00

0.81%

2.3K

Travelers Companies Inc

TRV

104.49

0.81%

0.2K

JPMorgan Chase and Co

JPM

55.95

0.79%

0.2K

FedEx Corporation, NYSE

FDX

124.15

0.79%

0.8K

Procter & Gamble Co

PG

76.42

0.78%

11.5K

Caterpillar Inc

CAT

59.25

0.75%

0.2K

Intel Corp

INTC

29.80

0.71%

5.3K

Cisco Systems Inc

CSCO

23.04

0.61%

0.2K

Yahoo! Inc., NASDAQ

YHOO

28.94

0.56%

3.8M

Apple Inc.

AAPL

97.32

0.55%

110.5K

Nike

NKE

59.35

0.53%

5.5K

International Business Machines Co...

IBM

122.50

0.53%

326.6K

Hewlett-Packard Co.

HPQ

9.60

0.52%

1.1K

Pfizer Inc

PFE

30.80

0.46%

2.1K

Visa

V

71.00

0.45%

0.2K

McDonald's Corp

MCD

116.24

0.40%

4.9K

Merck & Co Inc

MRK

50.75

0.40%

1.4K

Wal-Mart Stores Inc

WMT

61.02

0.30%

3.5K

The Coca-Cola Co

KO

41.45

0.17%

0.1K

Chevron Corp

CVX

79.11

0.16%

1K

General Motors Company, NYSE

GM

29.45

0.10%

51.8K

Exxon Mobil Corp

XOM

73.22

0.05%

21.5K

Boeing Co

BA

122.14

0.00%

7.0K

ALTRIA GROUP INC.

MO

57.17

-0.09%

4.9K

American Express Co

AXP

62.64

-0.62%

1.0K

AMERICAN INTERNATIONAL GROUP

AIG

54.54

-0.93%

15.9K

Barrick Gold Corporation, NYSE

ABX

7.99

-1.48%

0.9K

Yandex N.V., NASDAQ

YNDX

11.48

-2.71%

4.3K

-

15:02

Philadelphia Federal Reserve Bank’s manufacturing index climbs to -3.5 in January

The Philadelphia Federal Reserve Bank released its manufacturing index on Thursday. The index climbed to -3.5 in January from -10.2 in December, exceeding expectations for an increase to -5.0. December's figure was revised down from -5.9.

A reading above zero indicates expansion, while a reading below zero indicates contraction.

"Manufacturing conditions in the region contracted modestly this month, according to firms responding to the January Manufacturing Business Outlook Survey. The indicator for general activity remained negative this month; however, it rebounded from a lower reading in December," the Philadelphia Federal Reserve Bank said in its survey.

The shipments index was up to 9.6 in January from -2.1 in December.

The new orders index increased to -1.4 in January from -11.1 in December.

The prices paid index rose to -1.1 in January from -8.3 in December, while the prices received index climbed to -2.8 from -8.5.

The number of employees index dropped to -1.9 in January from 2.2 in December.

According to the report, the future general activity index slid to 19.1 in January from 24.1 in December.

-

14:51

Option expiries for today's 10:00 ET NY cut

USD/JPY 117.00 (USD 302m) 118.75-85 (305m)

EUR/USD 1.0850-60 ( EUR 1bln) 1.0870 (383m) 1.0900 (335m) 1.0925 (432m) 1.0950-60 (1.2bln)

USD/CHF 0.9825 (USD 318m)

USD/CAD 1.4500 (USD 595m)

AUD/USD 0.6900 (AUD 235m) 0.7000 (1.5bln) 0.7050 (300m)

NZD/USD 0.6425 (NZD 224m)

-

14:49

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

General Electric (GE) initiated with a Buy at Citigroup

Honeywell International (HON) initiated with a Buy at Citigroup

3M Company (MMM) initiated with a Buy at Citigroup

-

14:47

European Central Bank keeps its interest rate unchanged at 0.05% in January

The European Central Bank (ECB) kept its monetary unchanged on Thursday. The interest rate remained unchanged at 0.05%. This decision was widely expected by analysts.

The interest rate remains unchanged since September 2014.

The ECB lowered its deposit rate to -0.3% from -0.2% in December.

-

14:44

Initial jobless claims rise to 293,000 in the week ending January 16

The U.S. Labor Department released its jobless claims figures on Thursday. The number of initial jobless claims in the week ending January 16 in the U.S. rose by 10,000 to 293,000 from 283,000 in the previous week. The previous week's figure was revised down from 284,000.

Analysts had expected jobless claims to fall to 278,000.

Jobless claims remained below 300,000 the 46th straight week. This threshold is associated with the strengthening of the labour market.

Continuing jobless claims declined by 56,000 to 2,208,000 in the week ended January 09.

-

14:36

Foreign exchange market. European session: the euro traded lower against the U.S. dollar after the European Central Bank's (ECB) interest rate decision

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

00:00 Australia HIA New Home Sales, m/m November -3.0% -2.7%

00:00 Australia Consumer Inflation Expectation January 4.0% 3.6%

05:30 Japan All Industry Activity Index, m/m November 1.0% -0.7% -1.0%

09:00 Switzerland World Economic Forum Annual Meetings

12:45 Eurozone ECB Interest Rate Decision 0.05% 0.05% 0.05%

The U.S. dollar traded mixed to higher against the most major currencies ahead of the release of the U.S. economic index. The number of initial jobless claims in the U.S. is expected to decline by 6,000 to 278,000 last week.

The Philadelphia Federal Reserve Bank' manufacturing index is expected to rise to -5 in January from -10.2 in December.

The euro traded lower against the U.S. dollar after the European Central Bank's (ECB) interest rate decision. The ECB kept its interest rate unchanged at 0.05%.

The ECB President Mario Draghi will speak at 13:30 GMT.

The British pound traded lower against the U.S. dollar in the absence of any major economic reports from the U.K.

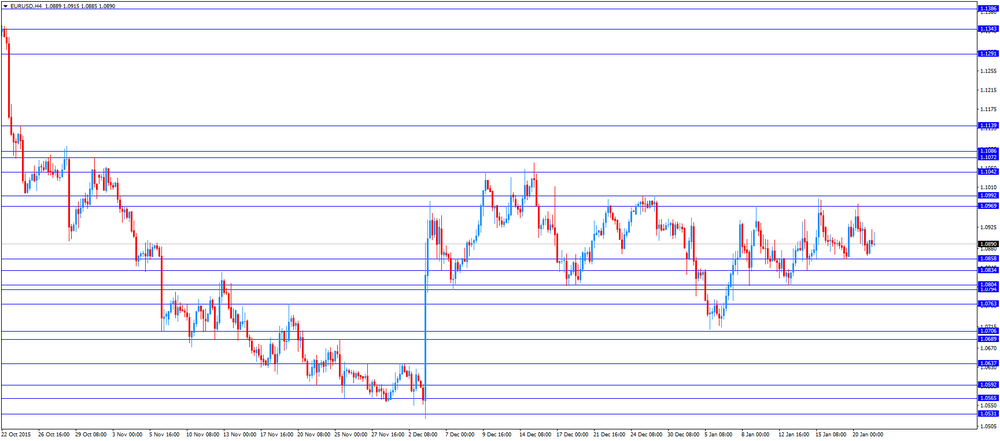

EUR/USD: the currency pair traded mixed

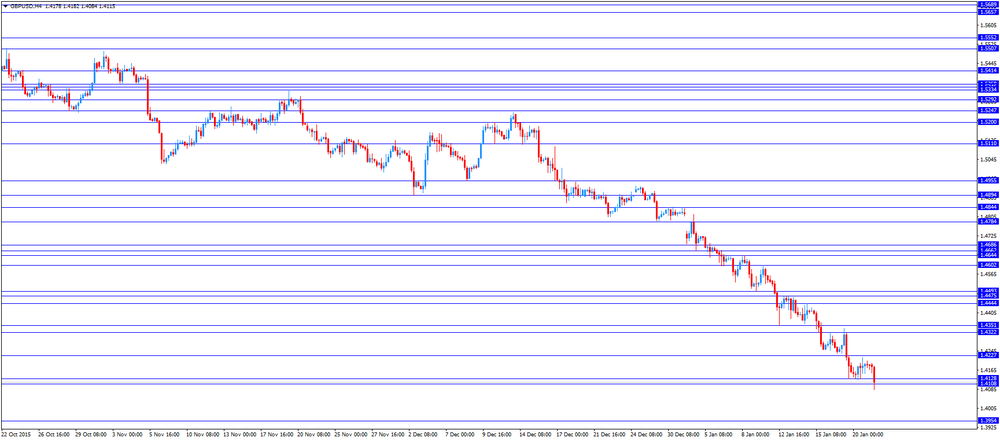

GBP/USD: the currency pair declined to $1.4084

USD/JPY: the currency pair rose to Y117.17

The most important news that are expected (GMT0):

13:30 Eurozone ECB Press Conference

13:30 U.S. Continuing Jobless Claims January 2263 2248

13:30 U.S. Initial Jobless Claims January 284 278

13:30 U.S. Philadelphia Fed Manufacturing Survey January -10.2 -5

15:00 Eurozone Consumer Confidence (Preliminary) January -5.7 -5.7

16:00 U.S. Crude Oil Inventories January 0.234 2.750

-

14:31

U.S.: Philadelphia Fed Manufacturing Survey, January -3.5 (forecast -5)

-

14:30

U.S.: Initial Jobless Claims, January 293 (forecast 278)

-

14:30

U.S.: Continuing Jobless Claims, January 2208 (forecast 2248)

-

13:59

Orders

EUR/USD

Offers 1.0925 1.0945-50 1.0985 1.1000 1.1025 1.1050 1.1080 1.1100

Bids 1.0880 1.0855-60 1.0840 1.0825 1.0800 1.0785 1.0765 1.0750 1.0730 1.0700

GBP/USD

Offers 1.4185 1.4200 1.4225-30 1.4250 1.4280 1.4300 1.4325-30 1.4350

Bids 1.4150 1.4120-25 1.4100 1.4085 1.4060 1.4030 1.4000

EUR/GBP

Offers 0.7720-25 0.7750-55 0.7780 0.7800 0.7830 0.7850 0.7875 0.7900

Bids 0.7675-80 0.7650 0.7630 0.7600 0.7580-85 0.7550

EUR/JPY

Offers 127.60 127.80 128.00 128.30 128.50 128.80 129.00 129.30 129.50

Bids 127.00 126.80 126.50 126.30 126.00 125.75 125.50 125.00

USD/JPY

Offers 117.20 117.50 117.85 118.00 118.20 118.50 118.80 119.00

Bids 116.75-80 116.50 116.20 116.00 115.85 115.50 115.30 115.00

AUD/USD

Offers 0.6900 0.6920-25 0.6950 0.6980 0.7000 0.7025-30 0.7050-55

Bids 0.6875-80 0.6850 0.6825-30 0.6800 0.6785 0.6750 0.6730 0.6700

-

13:55

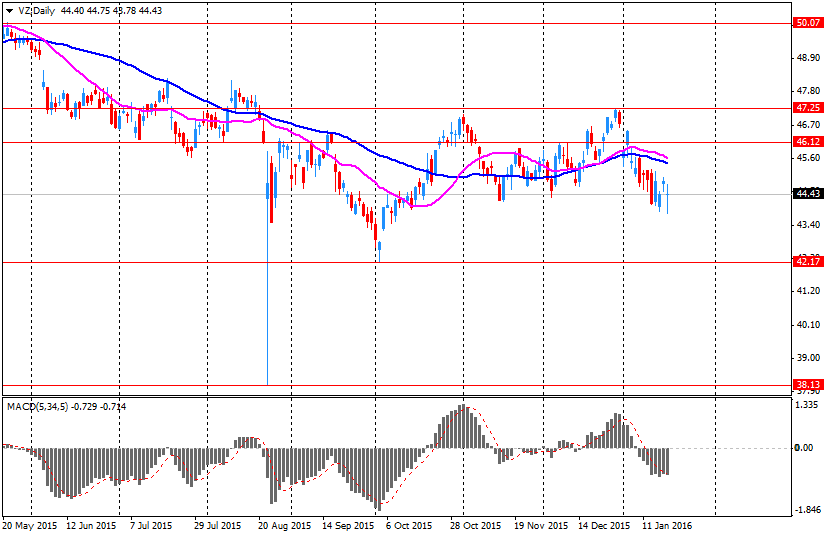

Company News: Verizon (VZ) Quarterly Results Beat Estimates

Verizon reported Q4 FY 2015 earnings of $0.89 per share (versus $0.71 in Q4 FY 2014), beating analysts' consensus of $0.88.

The company's quarterly revenues amounted to $34.254 bln (+3.2% y/y), slightly beating consensus estimate of $34.118 bln.

Verizon reaffirmed guidance for FY 2016, projecting EPS comparable to $3.99 (versus analysts' consensus of $3.97).

VZ rose to $44.75 (+0.74%) in pre-market trading.

-

13:45

Eurozone: ECB Interest Rate Decision, 0.05% (forecast 0.05%)

-

13:33

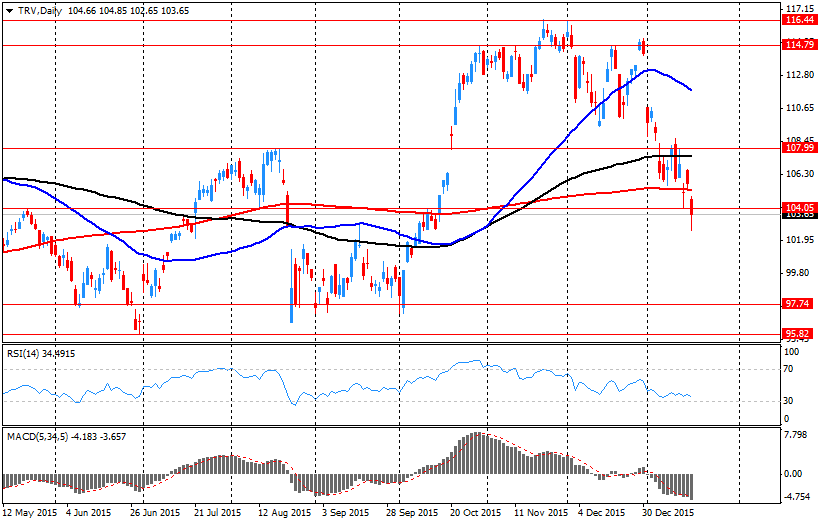

Company News: Travelers (TRV) Q4 Earnings Beat Estimates

Travelers reported Q4 FY 2015 earnings of $2.90 per share (versus $3.07 in Q4 FY 2014), beating analysts' consensus of $2.66.

The company's quarterly revenues amounted to $6.023 bln (+0.7% y/y), generally in line with consensus estimate of $6.068 bln.

TRV rose to $104.20 (+0.53%) in pre-market trading.

-

12:01

European stock markets mid session: stocks traded higher ahead of the release of the European Central Bank’s interest rate decision

Stock indices traded higher ahead of the release of the European Central Bank's (ECB) interest rate decision. Analysts expect the central bank to keep its monetary policy unchanged.

Market participants were disappointed in December because they hoped for more stimulus measures by the ECB. The ECB kept its interest rate unchanged at 0.05%, but lowered its deposit rate to -0.3% from -0.2%. The asset-buying programme will be extended until the end of March 2017. Earlier, the asset buying programme was intended to run until September 2016. The volume of the monthly purchases remained unchanged.

International Monetary Fund (IMF) Managing Director Christine Lagarde said at the World Economic Forum in Davos on Wednesday that risks to the global economic growth are bigger than previously expected. According to Lagarde, the risks are falling oil prices, the slowdown in the Chinese economy and diverging monetary policies.

Current figures:

Name Price Change Change %

FTSE 100 5,699.28 +25.70 +0.45 %

DAX 9,447.46 +55.82 +0.59 %

CAC 40 4,157.33 +32.38 +0.78 %

-

11:47

Spain’s trade deficit widens to €1.85 billion in November

Spain's Economy Ministry released its trade data on Thursday. The trade deficit widened to €1.85 billion in November from €1.60 billion in November a year ago.

Exports rose at an annual rate of 8.6% in November, while imports climbed 9.3%.

In the January to November period, the trade deficit totalled €22.38 billion, down 1.2% from the same period of 2014.

Exports increased 4.3% in the January to November period, while imports gained 3.8%.

-

11:44

Japan’s all industry activity index slides 1.0% in November

Japan's Ministry of Economy, Trade and Industry (METI) released its all industry activity index on Thursday. The index slid 1.0% in November, missing expectations for a 0.7% fall, after a 0.9% rise in October. October's figure was revised down from a 1.0% increase.

Construction industry activity index dropped 3.0% in November, industrial production index fell 0.9%, while tertiary industry activity declined 0.8%.

-

11:36

MI consumer inflation expectations in Australia decline to 3.6% in January

The Melbourne Institute (MI) released its inflation expectations for Australia on Thursday. The MI consumer inflation expectations in Australia declined to 3.6% in January from 4.0% in December.

72.1% respondents expected inflation to decline within the 0‐5% range, down from 74.2% in December.

-

11:30

HIA new home sales in Australia drop 2.7% in November

The Housing Industry Association (HIA) released its new home sales data for Australia on Thursday. New home sales fell 2.7% in November, after a 3.0% drop in October.

The HIA's chief economist Harley Dale said that a drop was driven by the slowing population growth, higher mortgage costs, and easing property price growth in Sydney and Melbourne.

Sales of detached homes increased 1.1% in November, while sales for multi-units slid 15.1%.

-

11:17

French manufacturing confidence index rises to 102 in January

The French statistical office Insee released its manufacturing confidence index for France on Thursday. The French manufacturing confidence index increased to 102 in January from 101 in December. December's figure was revised down from 103.

Past change in production index was down to -1 in January from 1 in December.

Personal production expectations index rose to 10 in January from 9 in December, while general production outlook index increased to 2 from 0.

-

11:00

International Monetary Fund Managing Director Christine Lagarde: risks to the global economic growth are bigger than previously expected

International Monetary Fund (IMF) Managing Director Christine Lagarde said at the World Economic Forum in Davos on Wednesday that risks to the global economic growth are bigger than previously expected. According to Lagarde, the risks are falling oil prices, the slowdown in the Chinese economy and diverging monetary policies.

She noted that the global economy is expected to expand moderately this year.

-

10:49

Fitch Ratings expects WTI crude price to be $45 a barrel in 2016

Fitch Ratings said on Wednesday that it expects WTI crude price to be $45 a barrel in 2016. In stress case, WTI crude price is expected to $35 a barrel.

"Fitch believes oil prices in the current $30/barrel spot range are not sustainable over a protracted period, as they cover cash costs but not the replacement of developed reserves," the agency said.

-

10:41

Option expiries for today's 10:00 ET NY cut

USD/JPY 117.00 (USD 302m) 118.75-85 (305m)

EUR/USD 1.0850-60 ( EUR 1bln) 1.0870 (383m) 1.0900 (335m) 1.0925 (432m) 1.0950-60 (1.2bln)

USD/CHF 0.9825 (USD 318m)

USD/CAD 1.4500 (USD 595m)

AUD/USD 0.6900 (AUD 235m) 0.7000 (1.5bln) 0.7050 (300m)

NZD/USD 0.6425 (NZD 224m)

-

10:28

Venezuela calls for an OPEC emergency meeting

Reuters reported on Wednesday that according to OPEC sources, Venezuela called for an emergency meeting to discuss the stabilisation of the oil market as oil prices hit the lows of 2003.

It is unlikely that an emergency meeting will be held as Saudi Arabia's strategy is to defend market shares.

The next scheduled OPEC meeting is scheduled to be on June 02.

-

10:15

Iran cuts crude prices for its European consumers

Iran lowered crude prices for its European consumers. The reason for this step is the competition with Saudi Arabia.

Iran's discount for European consumers is $6.55 a barrel on heavy crude, while Saudi Arabia's discount is $4.85 a barrel.

International sanctions on Iran were lifted over the weekend after the International Atomic Energy Agency announced that Tehran had fulfilled its commitment.

Iran said on Sunday that it plans to raise its exports by 500,000 barrels per day.

Iran is a member of the Organization of the Petroleum Exporting Countries (OPEC), and is the fifth biggest OPEC oil producer.

-

08:30

Foreign exchange market. Asian session: the yen recovered

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:00 Australia HIA New Home Sales, m/m November -3.0% -2.7%

00:00 Australia Consumer Inflation Expectation January 4.0% 3.6%

The yen recovered in the second half of the Asian session as higher volatility in stocks increased demand for safe-haven assets.

At the beginning of the session the yen declined against the U.S. dollar after Prime Minister Abe's advisor said there was ground for further monetary policy easing. He added that lack of action from the central bank can contradict basic principles of abenomics.

Market participants are waiting for today's European Central Bank meeting to find hints to further steps to stimulate inflation. The global economic outlook has worsened since the latest ECB meeting in December. Stocks and commodities plunged, concerns over the Chinese economy intensified. Economists believe the euro zone consumer price index may turn negative. Investors hope that authorities will take steps to support inflation.

EUR/USD: the pair fluctuated within $1.0865-00 in Asian trade

USD/JPY: the pair traded around Y117.00

GBP/USD: the pair traded within $1.4170-00

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

09:00 Switzerland World Economic Forum Annual Meetings

12:45 Eurozone ECB Interest Rate Decision 0.05% 0.05%

13:30 Eurozone ECB Press Conference

13:30 U.S. Continuing Jobless Claims January 2263 2248

13:30 U.S. Initial Jobless Claims January 284 278

15:00 Eurozone Consumer Confidence (Preliminary) January -5.7 -5.7

15:00 U.S. Philadelphia Fed Manufacturing Survey January -10.2 -5

16:00 U.S. Crude Oil Inventories January 0.234 2.750

-

08:30

Options levels on thursday, January 21, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1062 (4336)

$1.1004 (3083)

$1.0962 (1822)

Price at time of writing this review: $1.0910

Support levels (open interest**, contracts):

$1.0844 (1188)

$1.0802 (2754)

$1.0744 (7143)

Comments:

- Overall open interest on the CALL options with the expiration date February, 5 is 40048 contracts, with the maximum number of contracts with strike price $1,1000 (4336);

- Overall open interest on the PUT options with the expiration date February, 5 is 60602 contracts, with the maximum number of contracts with strike price $1,0700 (7714);

- The ratio of PUT/CALL was 1.51 versus 1.41 from the previous trading day according to data from January, 20

GBP/USD

Resistance levels (open interest**, contracts)

$1.4403 (625)

$1.4306 (316)

$1.4210 (138)

Price at time of writing this review: $1.4162

Support levels (open interest**, contracts):

$1.4091 (715)

$1.3994 (389)

$1.3896 (311)

Comments:

- Overall open interest on the CALL options with the expiration date February, 5 is 22898 contracts, with the maximum number of contracts with strike price $1,4700 (3151);

- Overall open interest on the PUT options with the expiration date February, 5 is 21735 contracts, with the maximum number of contracts with strike price $1,4550 (2011);

- The ratio of PUT/CALL was 0.95 versus 0.95 from the previous trading day according to data from January, 20

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:07

Oil prices declined

West Texas Intermediate futures for March delivery fell to $28.11 (-0.85%), while Brent crude declined to $27.68 (-2.12%) amid concerns over health of the global economy, which cast a shadow over demand prospects. The International Monetary Fund revised its 2016 global economic growth forecast to 3.4% from 3.6% projected earlier. Market participants are also concerned about China's slowing economy, which could cut demand. Meanwhile Iran is preparing to raise exports and add to the existing oversupply issue.

Venezuela has requested an emergency OPEC meeting, however many experts believe that such a meeting was unlikely.

-

07:51

Gold steadied

Gold is currently at $1,102.30 (-0.35%). The precious metal gave up some of its Wednesday gains, but stayed close to a one-and-a-half-week high. Investors turned to gold as stocks and oil prices continued to fall. The latest downward revision of the global economic growth forecast from the International Monetary Fund added to concerns over health of the global economy.

Expectations for the Federal Reserve to raise its interest rates in March declined after the US. Department of Labor reported weaker inflation in December. Nevertheless the central bank of the U.S. is still expected to continue raising interest rates. This limits gold's upward potential. The dollar, bullions major opponent, is likely to do well amid higher rates.

-

07:13

Global Stocks: U.S. stock indices fell following oil prices

U.S. stock indices plunged on Wednesday following oil prices. A slight rebound in oil prices helped stocks step away from session lows by the end of the session.

The Dow Jones Industrial Average fell 249.28 points, or 1.6% higher, to 15,766.74. The S&P 500 fell 22 points, or 1.2%, to 1,859 (its energy sector lost 2.9%). The Nasdaq Composite declined 5.26 points, or 0.1%, to 4,471.69 after an initial drop of 145 points.

The U.S. Department of Labor reported that consumer prices unexpectedly declined in December as lower energy costs offset higher prices in the services sector. The consumer price index fell by 0.1% in December after being unchanged in November. However on an annualized basis the index rose by 0.7% marking the biggest gain over the year. Experts said that inflation growth may slow down because of persistent declines in oil prices. Economists had expected readings of 0.0% m/m and 0.8% y/y.

This morning in Asia Hong Kong Hang Seng lost 0.85%, or 160.38, to 18,725.92. China Shanghai Composite Index fell 1.02%, or 30.25, to 2,946.44. The Nikkei fell 0.76%, or 124.26, to 16,291.93.

Asian stock indices gave up early gains and turned red. The selloff was encouraged by declines in U.S. stocks and oil, as well as by concerns over global economic growth outlook. A stronger yen put additional pressure on Japanese exporters.

-

03:08

Nikkei 225 16,624.41 +208.22 +1.27 %, Hang Seng 19,181.12 +294.82 +1.56 %, Shanghai Composite 2,937.35 -39.35 -1.32 %

-

01:00

Australia: HIA New Home Sales, m/m, November -2.7%

-

01:00

Australia: Consumer Inflation Expectation, January 3.6%

-

00:30

Commodities. Daily history for Jan 20’2016:

(raw materials / closing price /% change)

Oil $28.28 -4.78

Gold $1,101.00 -0.47

-

00:29

Stocks. Daily history for Sep Jan 20’2016:

(index / closing price / change items /% change)

S&P/ASX 200 4,841.53 -61.54 -1.26%

TOPIX 1,338.97 -51.44 -3.70%

SHANGHAI COMP 2,976.52 -31.22 -1.04%

HANG SENG 18,886.3 -749.51 -3.82%

FTSE 100 5,673.58 -203.22 -3.46 %

CAC 40 4,124.95 -147.31 -3.45 %

Xetra DAX 9,391.64 -272.57 -2.82 %

S&P 500 1,859.33 -22.00 -1.17 %

NASDAQ Composite 4,471.69 -5.26 -0.12 %

Dow Jones 15,766.74 -249.28 -1.56 %

-

00:29

Currencies. Daily history for Jan 20’2016:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0888 -0,17%

GBP/USD $1,4190 +0,24%

USD/CHF Chf1,004 +0,09%

USD/JPY Y116,94 -0,58%

EUR/JPY Y127,33 -0,75%

GBP/JPY Y165,91 -0,34%

AUD/USD $0,6905 -0,03%

NZD/USD $0,6428 +0,28%

USD/CAD C$1,4502 -0,52%

-

00:01

Schedule for today, Thursday, Jan 21’2016:

(time / country / index / period / previous value / forecast)

00:00 Australia HIA New Home Sales, m/m November -3.0%

00:00 Australia Consumer Inflation Expectation January 4.0%

05:30 Japan All Industry Activity Index, m/m November 1.0% -0.7%

09:00 Switzerland World Economic Forum Annual Meetings

12:45 Eurozone ECB Interest Rate Decision 0.05% 0.05%

13:30 Eurozone ECB Press Conference

13:30 U.S. Continuing Jobless Claims January 2263 2248

13:30 U.S. Initial Jobless Claims January 284 278

15:00 Eurozone Consumer Confidence (Preliminary) January -5.7 -5.7

15:00 U.S. Philadelphia Fed Manufacturing Survey January -10.2 -5

16:00 U.S. Crude Oil Inventories January 0.234

-