Noticias del mercado

-

23:58

Schedule for today, Thursday, Mar 24’2016:

(time / country / index / period / previous value / forecast)

07:00 Germany Gfk Consumer Confidence Survey April 9.5 9.5

09:00 Eurozone ECB Economic Bulletin

09:30 United Kingdom BBA Mortgage Approvals February 47.5

09:30 United Kingdom Retail Sales (MoM) February 2.3% -0.7%

09:30 United Kingdom Retail Sales (YoY) February 5.2% 3.8%

10:15 Eurozone Targeted LTRO 18.3 24.3

11:00 United Kingdom CBI retail sales volume balance March 10 15

12:15 U.S. FOMC Member James Bullard Speaks

12:30 U.S. Continuing Jobless Claims March 2235 2230

12:30 U.S. Durable Goods Orders February 4.9% -2.9%

12:30 U.S. Durable Goods Orders ex Transportation February 1.8% -0.2%

12:30 U.S. Durable goods orders ex defense February 4.5%

12:30 U.S. Initial Jobless Claims March 265 268

13:00 U.S. Housing Price Index, m/m January 0.4%

13:45 U.S. Services PMI (Preliminary) March 49.7

23:30 Japan Tokyo Consumer Price Index, y/y March 0.1% 0%

23:30 Japan Tokyo CPI ex Fresh Food, y/y March -0.1% -0.2%

23:30 Japan National Consumer Price Index, y/y February 0% 0%

23:30 Japan National CPI Ex-Fresh Food, y/y February 0% 0.1%

-

22:45

New Zealand: Trade Balance, mln, February 339 (forecast 50)

-

20:00

Dow -0.50% 17,494.59 -87.98 Nasdaq -1.01% 4,772.79 -48.87 S&P -0.64% 2,036.72 -13.08

-

19:20

American focus: the US dollar strengthened considerably against the pound

The US dollar rose modestly against the euro, updating yesterday's high, helped by comments Fed officials about a possible rate hike next month. Today the head of the St. Louis Fed Bullard said that there may be arguments in favor of a rate hike in April. "Question rate hike at the April meeting is not removed from the agenda at the same time is unreasonable to raise rates if inflation expectations will subside." - He added. Recall, Scatter the Fed indicates that the end of the year maybe two rate hikes. However, Bullard said that the regulator does not enter into commitments in this regard, and should respond to the economic data from meeting to meeting. Earlier the president of the Federal Reserve Bank of Philadelphia, Patrick Harker noted that there is good reason to continue raising rates, and added that he would like to see three raises before the end of the year. Meanwhile, Chicago Fed President Charles Evans said that he expects two per cent increase on loans until the end of the year if the economy will maintain a given rate. Also recall that yesterday the Federal Reserve Bank of Atlanta President Dennis Lockhart signaled that the Fed may raise interest rates in April.

In addition, a positive impact on the dollar have data on the housing market. The Commerce Department reported that sales of new buildings were restored in February, became another sign of continuing, albeit restrained, the momentum in the housing market. Sales of new buildings reached a seasonally adjusted annual rate of 512 000. This was the highest since December and was slightly above economists' forecast of 510 000. The February figure was 2% higher than in January, but 6.1% lower than a year ago. But the rate in February 2015 was unusual; 501,000 new homes sold during the year have been reported. January data, which originally reported (494,000) have been revised to 502 000. The median sale price was $ 301,400, which is 6.2% higher compared to January.

The pound continued to fall in price against the US currency came close to a week low. Since the beginning of the week the pound has lost more than 350 points against the dollar, which is mainly due to increasing concerns about the exit of Britain from the EU and the speculation about another rate hike by the Federal Reserve next month. Today, Rabobank analysts said, "if in a referendum on June 23 the majority of British citizens will vote for the exit from the EU, the GBP / USD pair may fall to $ 1.20, but if Britain decides to stay GBP / USD pair will reach $ 1.53 in 12 months." The uncertainty of trade relations between Britain and the EU in the case of the country's exit from the unit may put pressure on investment flows and lower demand for the pound, "- said the Rabobank.

A slight effect on the pound have experts study the results of the Central Bank of England on business conditions. The report noted that the annual rate of growth of activity in the UK slowed in the first quarter of 2016. As the cause of the last speakers, experts have identified a slowdown in global growth and the strengthening of economic uncertainty. Growth in consumer spending was reported to have remained stable, with little change in retail sales compared with the previous quarter. Meanwhile, activity in the services sector slowed down slightly, mainly due to falling rates in the field of tourism. Retail prices continued to fall against the backdrop of steady fall in the value of food. Analysts said that the increase in labor costs was moderate, and the company reported a decline in hiring needs. The company also noted that the volume of exports declined in comparison with the 1st quarter last year.

The Canadian dollar dropped more than 150 pips against the US dollar, which was mainly due to the resumption of the fall in oil prices after the publication in the US petroleum inventories report. US Department of Energy reported that crude oil inventories rose week of March 12-18 by 9.4 million barrels to 532.5 million barrels, a new record high for this time of year. Analysts had expected an increase to 3.5 mln. Barrels. Oil reserves in Cushing terminal fell by 1.3 million barrels to 66.2 million barrels. Gasoline inventories fell by 4.6 million barrels to 245.1 million barrels. Analysts had expected inventories to fall by 2 million barrels. The utilization of refining capacity fell by 0.6% to 88.4%. Analysts have suggested that the rate will fall to 0.1%. Meanwhile, oil production in the US in the week of March 12-18, dropped to 9.038 million. Barrels per day versus 9.068 million. Barrels per day from the previous week. Experts note that the decline in production rates are high enough, and if this trend continues over the next 1-2 weeks figure could fall below 9 million. Barrels per day.

-

18:49

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes slightly fell. energy stocks weighed on a quiet Wednesday as investors shied away from big bets after the Brussels attacks and ahead of the long Easter weekend. Oil prices fell more than 3% after data showing a rise in U.S. stockpiles last week rekindled worries about a global glut.

Dow stocks mixed (15 vs 15). Top looser - NIKE, Inc. (NKE, -2,43%). Top gainer - UnitedHealth Group Incorporated (UNH, +1,68%).

All S&P sectors in negative area. Top looser - Basic Materials (-1,9%).

At the moment:

Dow 17458.00 -46.00 -0.26%

S&P 500 2032.75 -9.75 -0.48%

Nasdaq 100 4404.00 -30.50 -0.69%

Oil 40.09 -1.36 -3.28%

Gold 1224.10 -24.50 -1.96%

U.S. 10yr 1.89 -0.04

-

18:05

WSE: Session Results

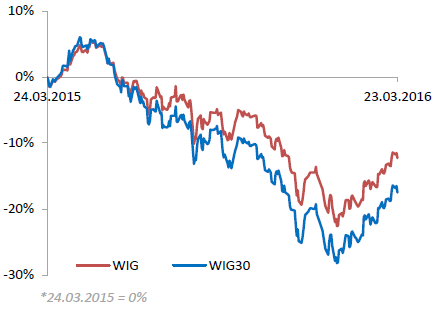

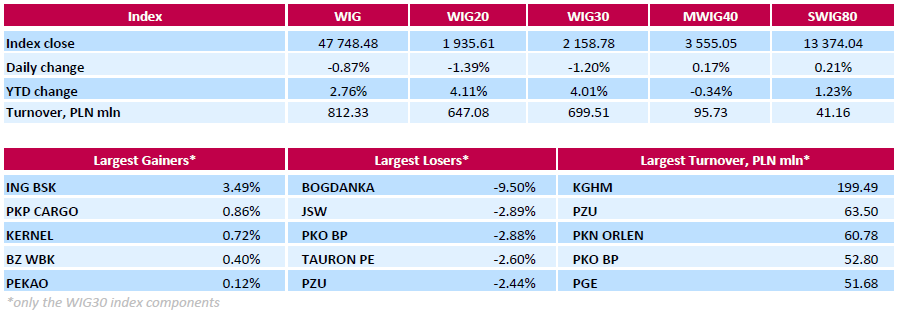

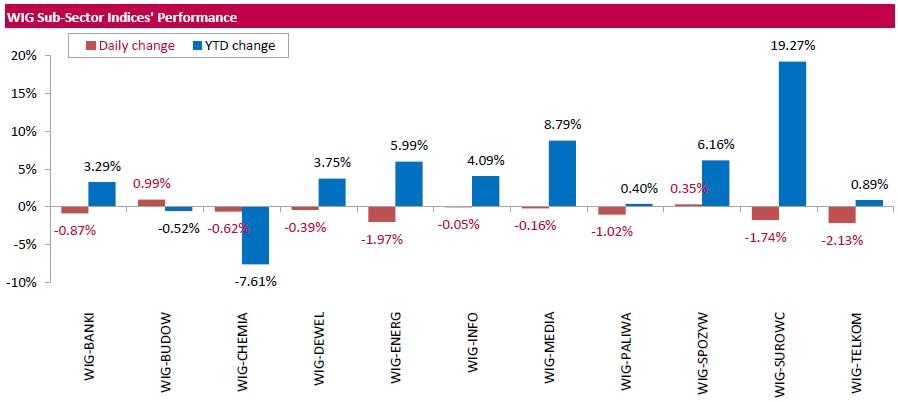

Polish equity market closed lower on Wednesday. The broad market measure, the WIG Index, slid down 0.87%. Except for construction sector (+0.99%) and food sector (+0.35%), every sector in the WIG Index fell, with telecommunication sector (-2.13%) lagging behind.

The large-cap stocks' measure, the WIG30 Index lost 1.2%. A majority of the index components recorded declines. Thermal coal miner BOGDANKA (WSE: LWB) was the weakest name, retreating by 9.5% after two consecutive sessions of solid gains. Among the other biggest losers were coking coal miner JSW (WSE: JSW), bank PKO BP (WSE: PKO), genco TAURON PE (WSE: TPE) and insurer PZU (WSE: PZU), plunging by 2.44%-2.89%. On the other side of the ledger, bank ING BSK (WSE: ING) led a handful of gainers with a 3.49% advance. It was followed by railway freight transport operator PKP CARGO (WSE: PKP) and agricultural producer KERNEL (WSE: KER), surging by 0.86% and 0.72% respectively.

-

18:00

European stocks closed: FTSE 100 6,199.11 +6.37 +0.10% CAC 40 4,423.98 -7.99 -0.18% DAX 10,022.93 +32.93 +0.33%

-

18:00

European stocks close: stocks closed mixed on lower oil prices

Stock indices closed mixed as oil prices declined on a higher-than-expected increase in U.S. crude oil inventories.

No major economic reports were released in the Eurozone.

European Central Bank (ECB) Governing Council member Jens Weidmann said in a speech on Wednesday that the latest stimulus measures by the ECB went too far and did not convince him.

The German Council of Economic Experts (GCEE) lowered its growth forecast on Wednesday. The German economy is expected to expand 1.5% in 2016, down from its previous estimate of 1.6%, and 1.6% in 2017. The downward revision was driven by weaker external demand.

Eurozone's inflation is expected to be 0.2% in 2016, down from its previous forecast of 1.1%, and 1.1% in 2017.

The experts expects the economy in Germany to continue to expand, driven by consumer spending, expansionary fiscal policy, and monetary policy.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,199.11 +6.37 +0.10 %

DAX 10,022.93 +32.93 +0.33 %

CAC 40 4,423.98 -7.99 -0.18 %

-

17:50

St. Louis Fed President James Bullard: an interest rate hike by the Fed in April is possible as the U.S. labour market continues to improve

St. Louis Fed President James Bullard said in an interview with Bloomberg TV that an interest rate hike by the Fed in April was possible as the U.S. labour market continued to improve.

He was concerned about inflation expectations, which showed signs of stabilisation, but seemed to correlate with oil prices.

St. Louis Fed president criticised the Fed's dot plot forecasts of interest rates.

Bullard is a voting member of the Federal Open Market Committee (FOMC) this year.

-

17:43

Oil prices dropped significantly today

Oil prices fell nearly 3 percent, came under pressure after the release of the US petroleum inventory report, which did not meet the expectations of experts. Another factor was the strengthening of the dynamics of today's US currency.

US Department of Energy reported that crude oil inventories rose week of March 12-18 by 9.4 million barrels to 532.5 million barrels, a new record high for this time of year. Analysts had expected an increase to 3.5 mln. Barrels. Oil reserves in Cushing terminal fell by 1.3 million barrels to 66.2 million barrels. Gasoline inventories fell by 4.6 million barrels to 245.1 million barrels. Analysts had expected inventories to fall by 2 million barrels. Distillate stocks rose by 917,000 barrels to 162.3 million barrels. Analysts had forecast a drop in stocks at 800,000 barrels. The utilization of refining capacity fell by 0.6% to 88.4%. Analysts have suggested that the rate will fall to 0.1%. Meanwhile, oil production in the US in the week of March 12-18, dropped to 9.038 million. Barrels per day versus 9.068 million. Barrels per day from the previous week. Experts note that the decline in production rates are high enough, and if this trend continues over the next 1-2 weeks figure could fall below 9 million. Barrels per day. Also recall that yesterday the American Petroleum Institute reported that US crude inventories rose by 8.8 mln. Barrels last week, reaching 531.8 million. Analysts expected an increase of 5.7 mln. Barrels. "The latest data confirm that the experts who hoped to tighten conditions on the oil market, still can only hope for it," - said the IAF Advisors.

"Gasoline demand remains significantly stronger than expected," - said Jim Ritterbusch, head of consulting firm in the energy sector. He added that the decline in oil prices is constrained to continue the conversation about the level of extraction freezing.

Also today, a member of the leadership of the International Energy Agency said that the agreement between some of the oil-producing countries, OPEC and Russia to freeze production may not make sense, since the Saudi Arabia - the only country with the ability to increase production. Recall, Qatar invited all 13 members of OPEC and the oil producing countries outside the cartel to take part in the meeting in Doha on 17 April to discuss the possibility of freezing oil. According to the IEA forecast, the gap between demand and supply of oil will decrease later in the year, which will create conditions for the recovery of oil prices in 2017.

WTI for delivery in May fell to $40.13 a barrel. Brent for April fell to $40.63 a barrel.

-

17:29

European Central Bank Governing Council member Jens Weidmann: the latest stimulus measures by the ECB went too far

European Central Bank (ECB) Governing Council member Jens Weidmann said in a speech on Wednesday that the latest stimulus measures by the ECB went too far and did not convince him.

He noted that there was no risk of deflation.

Weidmann warned that low interest rates could lead to asset bubbles and to lower willingness to implement structural reforms.

-

17:22

Gold fell more than 2 percent

Futures Price of gold dropped significantly today, reaching the lowest level since February 26, helped by the strengthening of the US dollar and comments from the Fed, which suggest that the Central Bank may soon raise key interest rates.

The head of the Federal Reserve Bank of St. Louis Bullard said that the possible arguments in favor of a rate hike in April. "Question rate hike at the April meeting is not removed from the agenda at the same time is unreasonable to raise rates if inflation expectations will subside." - He added. Recall, Scatter the Fed indicates that the end of the year maybe two rate hikes. However, Bullard said that the regulator does not enter into commitments in this regard, and should respond to the economic data from meeting to meeting. Earlier the head of the Federal Reserve Bank of Philadelphia, Patrick Harker said that the Fed should consider the possibility of another rate rise next month. In turn, the president of the Federal Reserve Bank of Chicago Charles Evans said that waiting for two more rate increase this year. Higher interest rates will boost the dollar and make gold more expensive for investors who hold other currencies, which pushes the price down. Since the beginning of 2016 the price of gold rose 15%, reflecting the increase in demand for safe assets due to the instability in the financial markets ,.

"Comments from the Fed contributed to the decline in gold prices, but they are unlikely to block the long-term mood, promote the growth of prices", - said Georgette Belle of ABN Amro. Meanwhile, CitiFX noted that the closure of the day below $ 1225 would mean a move to $ 1191 in the short term, and possibly less for a more distant time.

A small impact on share prices also helped by US data. The Commerce Department reported that sales of new buildings were restored in February, became another sign of continuing, albeit restrained, the momentum in the housing market. Sales of new buildings reached a seasonally adjusted annual rate of 512 000. This was the highest since December and was slightly above economists' consensus forecast of 510 000. The February figure was 2% higher than in January, but 6.1% lower than a year ago. But the rate in February 2015 was unusual; 501,000 new homes sold during the year have been reported. January data, which originally reported (494,000) have been revised to 502 000. The median sale price was $ 301,400, which is 6.2% higher compared to January.

April futures price of gold on COMEX today fell to $ 1222.40 per ounce.

-

17:16

Japan’s government lowers its assessment of the economy

Japan's Cabinet Office released its monthly economic report on Wednesday. The government cut its assessment of the economy, saying that downward revision was driven by a weakness in consumer spending.

The government pointed out that Japan's economy continued to recover, adding that there were downside risks from the slowdown in emerging economies.

-

16:57

German Council of Economic Experts’ (GCEE) cuts its growth forecast

The German Council of Economic Experts (GCEE) lowered its growth forecast on Wednesday. The German economy is expected to expand 1.5% in 2016, down from its previous estimate of 1.6%, and 1.6% in 2017.

The downward revision was driven by weaker external demand.

Eurozone's inflation is expected to be 0.2% in 2016, down from its previous forecast of 1.1%, and 1.1% in 2017.

The experts expects the economy in Germany to continue to expand, driven by consumer spending, expansionary fiscal policy, and monetary policy.

The GCEE noted that investors expected longer period of low interest rates.

According to the experts, there are risks to the global outlook from the slowdown in emerging economies, turmoil on global financial markets, geopolitical conflicts, the resurgence of the euro crisis and possible Britain's exit from the European Union.

-

16:44

European Central Bank Executive Board member Sabine Lautenschlaeger: interest rates could be cut further but the balance between the costs and the benefits is needed

European Central Bank (ECB) Executive Board member Sabine Lautenschlaeger said on Wednesday that interest rates could be cut further but the balance between the costs and the benefits is needed.

"You can always go lower with rates," she said.

Lautenschlaeger noted that she would support the exit from accommodative monetary policy.

-

16:12

NBB business climate for Belgium rises to -4.2 in March

The National Bank of Belgium (NBB) released its business survey on Wednesday. The business climate rose to -4.2 in March from -6.6 in February. Analysts had expected the index to rise to -6.0.

All 4 indicators climbed in March.

The business climate index for the manufacturing sector was up to -7.9 in March from -11.2 in February due to a more favourable assessments of total order books.

The business climate index for the services sector rose to 11.2 in March from 10.5 in February due to a more favourable assessment of the current activity and expectations for an increase general market demand.

The business climate index for the building sector increased to -3.9 in March from -4.1 in February due to an improvement of the demand-side components.

The business climate index for the trade sector climbed to -4.1 in March from -5.1 in February due to a rise in employment.

-

15:52

U.S. crude inventories rise by 9.36 million barrels to 532.5 million in the week to March 18

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories rose by 9.36 million barrels to 532.5 million in the week to March 18.

Analysts had expected U.S. crude oil inventories to rise by 3.5 million barrels.

Gasoline inventories decreased by 4.6 million barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, declined by 1.3 million barrels.

U.S. crude oil imports increased by 691,000 barrels per day.

Refineries in the U.S. were running at 88.4% of capacity, down from 89.0% the previous week.

-

15:41

New home sales in the U.S. increase 2.0% in February

The U.S. Commerce Department released new home sales data on Wednesday. New home sales increased 2.0% to a seasonally adjusted annual rate of 512,000 units in February from 502,000 units in January. January's figure was revised up from 494,000 units.

Analysts had expected new home sales to reach 510,000 units.

The increase was mainly driven higher sales in the West region. New home sales in the West region climbed 38.5% in February.

-

15:31

U.S.: Crude Oil Inventories, March 9.357 (forecast 3.5)

-

15:00

Belgium: Business Climate, March -4.2 (forecast -6)

-

15:00

U.S.: New Home Sales, February 512 (forecast 510)

-

14:56

The KOF Swiss Economic Institute lowers its growth forecasts for Switzerland

The KOF Swiss Economic Institute released its growth forecasts for Switzerland on Wednesday. The Swiss economy is expected to expand 1.0% in 2016, down from the previous estimate of 1.1%, and 2.0% in 2017, unchanged from its previous estimate.

The downward revision was driven by the global economic weakness and the structural adjustments in Switzerland.

"Following a difficult 2015 for the Swiss economy as a whole, the prospects are gradually brightening. The weak international development towards the end of 2015 curbed the opportunities for exporters. Thanks to the gradual recovery of the economies of Switzerland's trading partners, the local economy is expected to regain its footing," the KOF said in its statement.

The KOF forecasted that consumer prices in Switzerland would be at -0.7% year-on-year in 2016, down from the previous estimate of -0.5%, and 0.1% in 2017, down from the previous estimate of 0.2%.

The unemployment rate is expected to be 3.5% in 2016, down from the previous estimate of 3.6%.

-

14:53

WSE: After start on Wall Street

After the opening of Wall Street sessions, major indexes are in the red (U.S. Stocks open: Dow -0.25%, Nasdaq -0.22%, S&P -0.22%). This resulted in a prompt adjustment of the German market, where the DAX fell to daily lows and currently hovers below the level of today's opening. WIG20 index weakened further, and fell to the daily minimum on the way to the level of 1942 points (-1,04%). Another risk is the behavior of KGHM, which due to falling prices of raw materials and along with them the strengthening of the American currency, begun to decline (-0,18%).

-

14:45

Option expiries for today's 10:00 ET NY cut

USD/JPY 110.70 (USD 700m) 111.95 (360m) 113.65 (285m)

EUR/USD 1.1000 (EUR 654m) 1.1025 (298m) 1.1035 (299m) 1.1050 (657m) 1.10550-60 (1.03bln) 1.1075 (375m) 1.1195-00(1.65bln) 1.1245-50 (903m) 1.1300 (252m) 1.1338 (370m0

GBP/USD 1.3900 (GBP 281m) 1.4050 (261m) 1.4250 (262m) 1.4330-35 (362m)

USD/CHF 1.0000 (USD 301m)

AUD/USD 0.7300 (AUD 1.02bln) 0.7490-00 (512m) 0.7550 (163m) 0.7625 (249m)

USD/CAD 1.3100 (USD 210m) 1.3120 (340m)

NZD/USD 0.6745 (NZD 198m) 0.6790 (200m)

-

14:33

U.S. Stocks open: Dow -0.25%, Nasdaq -0.22%, S&P -0.22%

-

14:22

Before the bell: S&P futures -0.09%, NASDAQ futures -0.03%

U.S. stock-index were flat.

Global Stocks:

Nikkei 17,000.98 -47.57 -0.28%

Hang Seng 20,615.23 -51.52 -0.25%

Shanghai Composite 3,010.79 +11.43 +0.38%

FTSE 6,199.48 +6.74 +0.11%

CAC 4,448.99 +17.02 +0.38%

DAX 10,078.94 +88.94 +0.89%

Crude oil $40.96 (-1.18%)

Gold $1224.40 (-2.00%)

-

14:20

Foreign exchange market. European session: the U.S. dollar traded higher against the most major currencies, supported by comments by Philadelphia Fed President Patrick Harker

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) March -5.9 2.5

11:00 U.S. MBA Mortgage Applications March -3.3% -3.3%

The U.S. dollar traded higher against the most major currencies ahead the release of the new home sales data. New home sales in the U.S. are expected to rise to 510,000 units in February from 494,000 units in January.

The greenback was supported by comments by Philadelphia Fed President Patrick Harker. He said on Tuesday that the Fed should hike its interest rate in April if the U.S. economy continues to improve. Harker pointed out that he would like to see more than two interest rate hikes this year, adding that the monetary policy would remain accommodative.

The euro traded lower against the U.S. dollar in the absence of any major economic reports from the Eurozone.

Reuters reported on Tuesday that according to a draft of Germany's Finance Ministry, the government plans to raise its spending by €30.9 billion to €347.8 billion by 2020, while the budget should remain balanced.

The British pound traded lower against the U.S. dollar in the absence of any major economic reports from the U.K. Concerns over the possible Britain's exit from the European Union (EU) continued to weigh on the pound.

The Swiss franc traded mixed against the U.S. dollar. A survey by the ZEW Institute and Credit Suisse Group showed on Wednesday that Switzerland's economic sentiment index climbed to 2.5 in March from -5.9 in February.

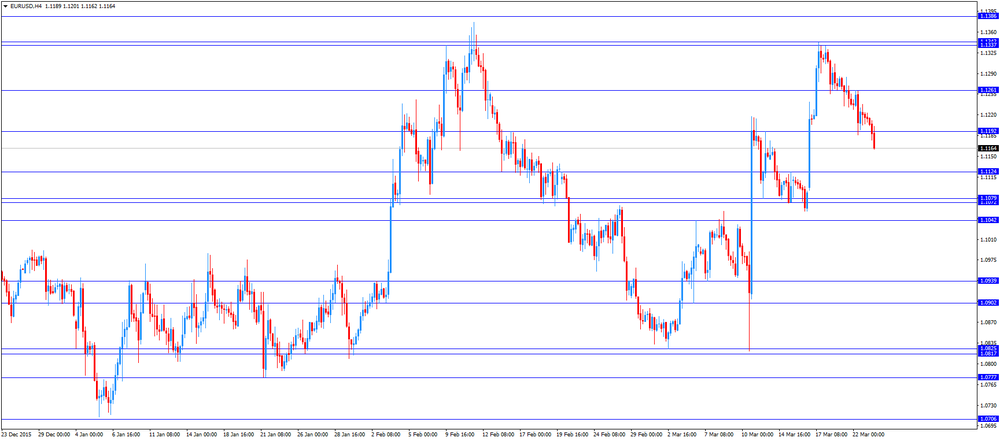

EUR/USD: the currency pair fell to $1.1162

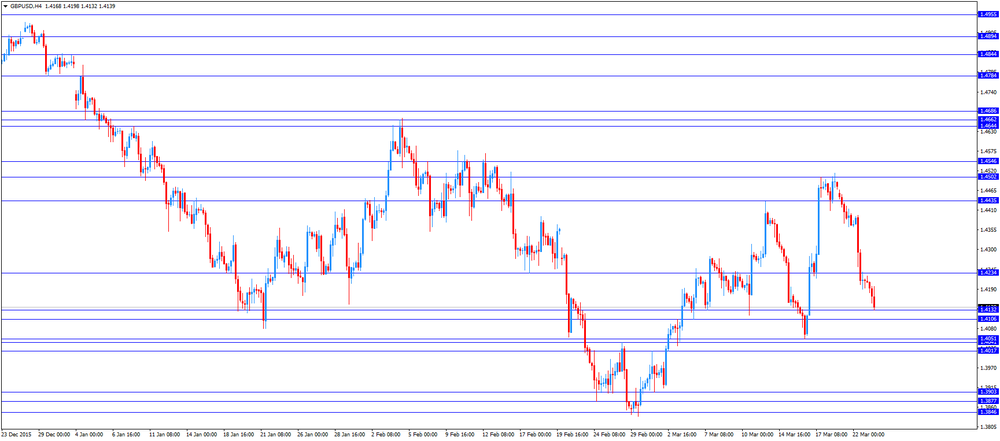

GBP/USD: the currency pair declined to $1.4132

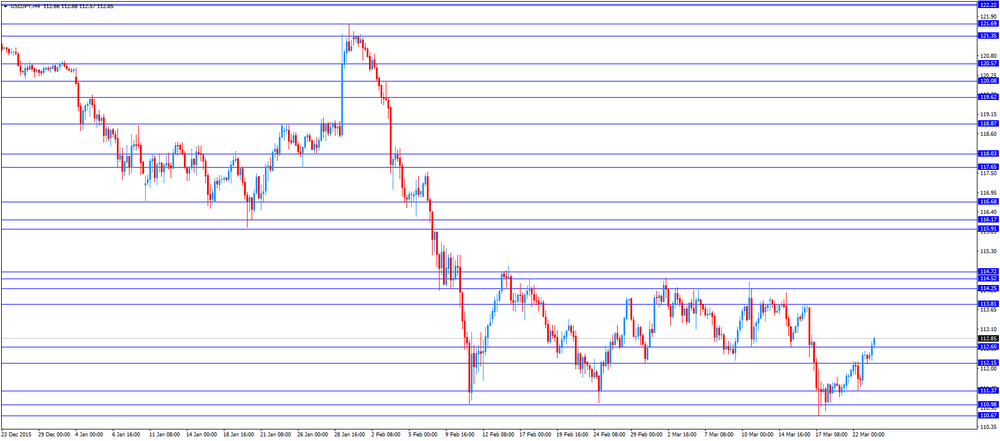

USD/JPY: the currency pair rose to Y112.88

The most important news that are expected (GMT0):

14:00 Belgium Business Climate March -6.6 -6

14:00 Switzerland SNB Quarterly Bulletin

14:00 U.S. New Home Sales February 494 510

14:30 U.S. Crude Oil Inventories March 1.317 3.5

21:45 New Zealand Trade Balance, mln February 8 50

-

14:07

European stock markets mid session: stocks traded higher in the absence of any major economic reports from the Eurozone

Stock indices recovered after terrorist attacks at the international airport in Brussels. At least 34 people have been killed and about 250 injured.

No major economic reports were released in the Eurozone.

Reuters reported on Tuesday that according to a draft of Germany's Finance Ministry, the government plans to raise its spending by €30.9 billion to €347.8 billion by 2020, while the budget should remain balanced.

Current figures:

Name Price Change Change %

FTSE 100 6,200.26 +7.52 +0.12 %

DAX 10,089.45 +99.45 +1.00 %

CAC 40 4,450.5 +18.53 +0.42 %

-

13:53

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.76

-0.09(-0.9137%)

45956

ALTRIA GROUP INC.

MO

61.14

0.14(0.2295%)

900

Amazon.com Inc., NASDAQ

AMZN

561.99

1.51(0.2694%)

4335

Apple Inc.

AAPL

106.84

0.12(0.1124%)

42773

AT&T Inc

T

38.67

0.04(0.1035%)

5282

Barrick Gold Corporation, NYSE

ABX

14.01

-0.49(-3.3793%)

231848

Boeing Co

BA

135.55

0.43(0.3182%)

821

Caterpillar Inc

CAT

75.16

-0.39(-0.5162%)

2920

Chevron Corp

CVX

95

-0.50(-0.5236%)

567

Cisco Systems Inc

CSCO

28.29

0.01(0.0354%)

554

Citigroup Inc., NYSE

C

43.32

-0.06(-0.1383%)

9754

Exxon Mobil Corp

XOM

83.83

-0.29(-0.3447%)

1886

Facebook, Inc.

FB

112.43

0.18(0.1604%)

55964

Ford Motor Co.

F

13.65

0.06(0.4415%)

29500

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

10.76

-0.23(-2.0928%)

134654

General Electric Co

GE

31.03

-0.03(-0.0966%)

34471

General Motors Company, NYSE

GM

31.75

-0.15(-0.4702%)

333

Google Inc.

GOOG

745.22

4.47(0.6034%)

2774

Hewlett-Packard Co.

HPQ

12.21

-0.05(-0.4078%)

1550

Intel Corp

INTC

32.39

0.07(0.2166%)

3517

International Business Machines Co...

IBM

147.97

-0.13(-0.0878%)

473

JPMorgan Chase and Co

JPM

60.24

0.00(0.00%)

1600

McDonald's Corp

MCD

123.96

0.14(0.1131%)

800

Merck & Co Inc

MRK

54

0.97(1.8292%)

10124

Microsoft Corp

MSFT

54.2

0.13(0.2404%)

13283

Nike

NKE

61.34

-3.56(-5.4854%)

438393

Pfizer Inc

PFE

30.48

0.10(0.3292%)

3568

Tesla Motors, Inc., NASDAQ

TSLA

233.8

-0.44(-0.1878%)

18026

The Coca-Cola Co

KO

45.48

-0.02(-0.044%)

2570

Twitter, Inc., NYSE

TWTR

16.96

0.10(0.5931%)

35880

United Technologies Corp

UTX

98.8

0.14(0.1419%)

1685

Verizon Communications Inc

VZ

53.18

-0.03(-0.0564%)

2140

Visa

V

72.99

0.03(0.0411%)

1288

Wal-Mart Stores Inc

WMT

68

0.13(0.1915%)

1722

Walt Disney Co

DIS

97.8

0.22(0.2255%)

1967

Yahoo! Inc., NASDAQ

YHOO

35.35

-0.06(-0.1694%)

1403

-

13:49

Orders

EUR/USD

Offers: 1.1200 1.1220 1.1235 1.1250 1.1275-80 1.1300 1.1320 1.1350

Bids: 1.1170-75 1.1150 1.1130 1.1100 1.1080-85 1.1050 1.1030 1.1000

GBP/USD

Offers: 1.4200 1.4220 1.4235 1.4250 1.4280 1.4300 1.4325 1.4350

Bids: 1.4140-50 1.4120 1.4100 1.4085 1.4065 1.4050 1.4025-30 1.4000

EUR/JPY

Offers: 126.00 126.20 126.50 126.80 127.00 127.30 127.50

Bids: 125.50 125.25-30 125.00 124.80 124.50 124.00

EUR/GBP

Offers: 0.7910 0.7925-30 0.7950 0.7975-80 0.8000

Bids: 0.7880 0.7850-60 0.7830 0.7800 0.7785 0.7750

USD/JPY

Offers: 112.75-80 113.00 113.20 113.50 113.80 114.00

Bids: 112.20 112.00 111.80-85 111.50 111.20 111.00 110.80 110.50

AUD/USD

Offers: 0.7625-30 0.7650 0.7680 0.7700 0.7725-30 0.7750

Bids: 0.7580-85 0.7565 0.7550 0.7530 0.7500 0.7485 0.7450

-

13:45

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Barrick Gold Corp (ABX) downgraded to Hold from Buy at Deutsche Bank

Other:

NIKE (NKE) target lowered to $57 rom $66 at Canaccord Genuity

Dow Chemical (DOW) target raised to $62 from $60 at RBC Capital Mkts

-

13:11

WSE: Mid session comment

Rally in European markets - especially Germany - have gained momentum, although trading retains low volatility. The DAX doubled increase from the morning and, the pressure from the environment seems to mount. Warsaw Stock Exchange today did not display similar sentiment, and as of the middle of the session WIG20 is trading at a loss of about 0.15 per cent to the previous close.

At the same time, the futures contracts for S&P500 increased by almost 0.2 percent, so the Wall Street seems to keep the distance ahead of Europe. We expect this to be one of the major considerations for the second half of the session.

-

12:53

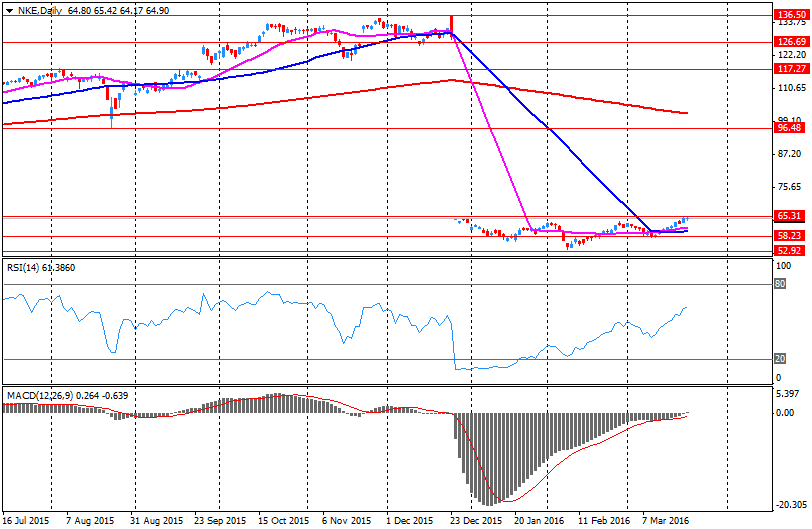

Company News: NIKE (NKE) Q3 Earnings Beat Expectations

NIKE reported Q3 FY2016 earnings of $0.55 per share (versus $0.89 in Q3 FY 2015), beating analysts' consensus of $0.47. The company's quarterly revenues amounted to $8.032 bln (+7.7% y/y), slightly missing consensus estimate of $8.201 bln.

NIKE provided financials guidance targets for Q4 and FY 2017. The company expects its revenue to grow at mid-single digit rate in Q4 (analysts forecast an increase of 8.9% y/y). For FY2017, NIKE projects its revenue to grow at high single digit rate and EPS to grow at low teen rate.

NKE fell to $61.50 (-5.24%) in pre-market trading.

-

12:00

U.S.: MBA Mortgage Applications, March -3.3%

-

11:40

Spanish producer prices decline 1.3% in February

The Spanish statistical office INE released its producer price index (PPI) data for Spain on Wednesday. The Spanish producer prices dropped 1.3% in February, after a 2.5% fall in January.

On a yearly basis, producer price inflation in Spain fell 5.7% in February, after a 4.2% decline in January. Producer prices have been declining since July 2014.

Energy prices slid 19.8% year-on-year in February, capital goods prices rose 0.8%, and consumer goods prices increased 0.2%, while intermediate goods prices declined 2.1%.

-

11:22

ZEW Institute and Credit Suisse Group’s survey: Switzerland's economic sentiment index climbs to 2.5 in March

A survey by the ZEW Institute and Credit Suisse Group showed on Wednesday that Switzerland's economic sentiment index climbed to 2.5 in March from -5.9 in February.

"The economic expectations reach a slightly positive balance. Still, a majority of 71.1 per cent of analysts expect economic growth in Switzerland to remain unchanged," the ZEW said.

The current conditions rose to -2.7 in March from-6.0 in February.

-

11:07

Bank of Japan board member Yukitoshi Funo: the central bank is ready to add further stimulus measures if risks to the economy increase

Bank of Japan (BoJ) board member Yukitoshi Funo said on Wednesday that the central bank was ready to add further stimulus measures if risks to the economy increase. He added that there was limit to interest rate cuts.

Funo noted that further stimulus measures will depend on the economic data.

Funo voted for negative interest rate at the January monetary policy meeting.

-

11:00

Switzerland: Credit Suisse ZEW Survey (Expectations), March 2.5

-

10:53

Canadian 2016-2017 budget deficit is larger than previously estimated

Canadian Finance Minister Bill Morneau presented 2016-2017 (starting on April 1) budget on Tuesday. The government plans to spend more than C$47 billion ($36 billion) over the next five years, beginning with the 2016-2017 fiscal year. This spending should add to the Canadian economic growth 0.5% in 2016 and 1% in 2017, according to the government. The budget deficit is expected to be C$29.4 billion ($23 billion), or 1.5% of GDP, in fiscal year 2016-2017, up from the previous estimate of a C$18.4 billion ($14 billion), and up from the forecasted C$5.4 billion deficit in the fiscal year 2015-2017.

The government expects the debt-to-GDP ratio to be 32.5% in 2017.

-

10:39

German government plans to raise its spending by €30.9 billion to €347.8 billion by 2020

Reuters reported on Tuesday that according to a draft of Germany's Finance Ministry, the government plans to raise its spending by €30.9 billion to €347.8 billion by 2020, while the budget should remain balanced. The government expect to boost its spending by €8.6 billion to €325.5 billion in 2017. The 2017 budget and financing plan up to 2020 are expected to be approved on July 06.

-

10:23

Philadelphia Fed President Patrick Harker: the Fed should hike its interest rate in April if the U.S. economy continues to improve

Philadelphia Fed President Patrick Harker said on Tuesday that the Fed should hike its interest rate in April if the U.S. economy continues to improve. He pointed out that he would like to see more than two interest rate hikes this year, adding that the monetary policy would remain accommodative.

Harker is not a voting member of the Federal Open Market Committee (FOMC) this year.

-

10:13

Chicago Fed President Charles Evans expects two interest rate hikes by the Fed this year

Chicago Fed President Charles Evans said on Tuesday that he expected two interest rate hikes by the Fed this year but declined to say when the Fed should raise interest rate.

He also said that the Fed should wait until inflation in the U.S. will pick up toward 2% target before hiking interest rate further.

Evans pointed out that a weak corporate spending, low commodities prices, the slowdown in the Chinese economy and market volatility weigh on the U.S. economic growth.

Evans is not a voting member of the Federal Open Market Committee (FOMC) this year.

-

09:49

Option expiries for today's 10:00 ET NY cut

USD/JPY 110.70 (USD 700m) 111.95 (360m) 113.65 (285m)

EUR/USD 1.1000 (EUR 654m) 1.1025 (298m) 1.1035 (299m) 1.1050 (657m) 1.10550-60 (1.03bln) 1.1075 (375m) 1.1195-00(1.65bln) 1.1245-50 (903m) 1.1300 (252m) 1.1338 (370m0

GBP/USD 1.3900 (GBP 281m) 1.4050 (261m) 1.4250 (262m) 1.4330-35 (362m)

USD/CHF 1.0000 (USD 301m)

AUD/USD 0.7300 (AUD 1.02bln) 0.7490-00 (512m) 0.7550 (163m) 0.7625 (249m)

USD/CAD 1.3100 (USD 210m) 1.3120 (340m)

NZD/USD 0.6745 (NZD 198m) 0.6790 (200m)

-

09:24

WSE: After opening

WIG20 index opened at 1959.07 points (-0.20%)*; other indexes:

WIG 48171.20 0.01%

WIG20 1959.07 -0.20%

WIG30 2184.81 -0.01%

mWIG40 3549.45 0.01%

*/ change to previous close

Europe begins trading on increases which in turn puts upward pressure on the Warsaw Stock Exchange, however the WSE selects a scenario of consolidation and extension of the drift at the levels achieved at the end of the last week. The WIG20 index after the first few minutes has placed in the region of 1,966 pts. Due to indicators the market is heavily bought, so the task for the bulls to play 2,000 points is not easy. Nevertheless, defeated the resistance in the region of 1,905 points and pending resistance in the region of 2,000 points make an opening in the region of 1,960 points technically neutral.

-

08:29

Options levels on wednesday, March 23, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1306 (2435)

$1.1275 (3138)

$1.1252 (3120)

Price at time of writing this review: $1.1184

Support levels (open interest**, contracts):

$1.1141 (2057)

$1.1109 (2383)

$1.1078 (3428)

Comments:

- Overall open interest on the CALL options with the expiration date April, 8 is 46601 contracts, with the maximum number of contracts with strike price $1,1500 (4483);

- Overall open interest on the PUT options with the expiration date April, 8 is 67683 contracts, with the maximum number of contracts with strike price $1,0900 (6141);

- The ratio of PUT/CALL was 1.45 versus 1.44 from the previous trading day according to data from March, 22

GBP/USD

Resistance levels (open interest**, contracts)

$1.4503 (1688)

$1.4405 (1832)

$1.4308 (949)

Price at time of writing this review: $1.4173

Support levels (open interest**, contracts):

$1.4092 (747)

$1.3995 (2038)

$1.3897 (1013)

Comments:

- Overall open interest on the CALL options with the expiration date April, 8 is 20205 contracts, with the maximum number of contracts with strike price $1,4400 (1832);

- Overall open interest on the PUT options with the expiration date April, 8 is 22175 contracts, with the maximum number of contracts with strike price $1,3850 (2244);

- The ratio of PUT/CALL was 1.10 versus 0.94 from the previous trading day according to data from March, 22

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:28

WSE: Before opening

Tuesday's trading on Wall Street brought modest changes in the major indices. The sessions were in many respects similar to Europeans ones. The broad market index S&P500 fell by 0.09 percent. Here we can talk about the extension of the stabilization observed at the end of yesterday's session in Europe and the USA. The same is true of the Asian markets and the FX market.

Maintaining a similar atmosphere to 9:00 should lead to small changes in the opening of indexes for today's trading in Europe. In the following hours, it is difficult to expect from return of any excessive optimism. In total, the exchange already operate under the upcoming holidays.

The most important report on today's macroeconomic calendar will be the read of fuel stocks levels in the United States.

On the Warsaw market, we expect today to observe core markets and move in correlation with major global indices.

-

08:20

Asian session: The yen fell

The euro edged down as Asian investors reacted to overnight news of attacks in Brussels. Attacks on Brussels airport and a rush-hour metro train in the Belgian capital, which occurred late in Tuesday's Asian session, killed dozens and triggered security alerts across western Europe.

The yen fell as Japan officially selected Makoto Sakurai, a supporter of negative interest rates, as a new Bank of Japan board member Wednesday, a move likely to tip the balance of opinion on the board more in favor of Gov. Haruhiko Kuroda. The upper house of Japan's parliament approved Sakurai to take the post, following a similar decision in the lower house the previous day.

EUR / USD: during the Asian session, the pair was trading in the $ 1.1200-25

GBP / USD: during the Asian session the pair fell to $ 1.4180

USD / JPY: during the Asian session, the pair was trading in range Y112.10-45

Based on Reuters materials

-

07:33

Global Stocks: stocks closed lower after explosions at the Brussels Airport

Europe's main stock benchmark closed lower Tuesday, albeit well off session lows, after explosions at the Brussels Airport and a local subway station left dozens dead and injured.

U.S. stocks gave up meager gains to end slightly lower Tuesday as a decline in financial and consumer-staples shares weighed on the main benchmarks. Wall Street spent most of the session lower as investors wrestled with the fallout from deadly attacks in Belgium.

Equity markets in the Asia-Pacific region were largely quiet on Wednesday, despite losses in Europe following the deadly attacks in Brussels. Analysts say investors are reluctant to place large bets ahead of the Good Friday and Easter holidays.

Based on MarketWatch materials

-

03:04

Nikkei 225 17,082.47 +33.92 +0.20 %, Hang Seng 20,683.82 +17.07 +0.08 %, Shanghai Composite 2,995.58 -3.78 -0.13 %

-

01:03

Commodities. Daily history for Mar 22’2016:

(raw materials / closing price /% change)

Oil 41.28 -0.41%

Gold 1,248.40 -0.02%

-

01:02

Stocks. Daily history for Sep Mar 22’2016:

(index / closing price / change items /% change)

Nikkei 225 17,048.55 +323.74 +1.94 %

Hang Seng 20,666.75 -17.40 -0.08 %

Shanghai Composite 3,000.67 -18.13 -0.60 %

FTSE 100 6,192.74 +8.16 +0.13 %

CAC 40 4,431.97 +4.17 +0.09 %

Xetra DAX 9,990 +41.36 +0.42 %

S&P 500 2,049.8 -1.80 -0.09 %

NASDAQ Composite 4,821.66 +12.79 +0.27 %

Dow Jones 17,582.57 -41.30 -0.23 %

-

01:01

Currencies. Daily history for Mar 22’2016:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1215-0,21%

GBP/USD $1,4212 -1,10%

USD/CHF Chf0,9729 +0,25%

USD/JPY Y112,37 +0,37%

EUR/JPY Y126,01 +0,11%

GBP/JPY Y159,68 -0,73%

AUD/USD $0,7614 +0,46%

NZD/USD $0,6747 -0,28%

USD/CAD C$1,3043 -0,41%

-

00:02

Schedule for today, Wednesday, Mar 23’2016:

(time / country / index / period / previous value / forecast)

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) March -5.9

11:00 U.S. MBA Mortgage Applications March -3.3%

14:00 Belgium Business Climate March -6.6 -6

14:00 Switzerland SNB Quarterly Bulletin

14:00 U.S. New Home Sales February 494 510

14:30 U.S. Crude Oil Inventories March 1.317

21:45 New Zealand Trade Balance, mln February 8 90

-