Noticias del mercado

-

21:00

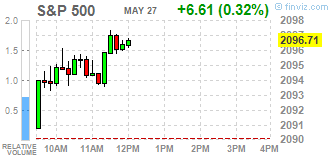

Dow +0.13% 17,850.86 +22.57 Nasdaq +0.47% 4,924.98 +23.21 S&P +0.27% 2,095.84 +5.74

-

19:58

American focus: the US dollar significantly strengthened against the euro

Dollar rose significantly against the euro, by updating the two-month high, aided by the statistics on the US and expectations of today's speech by Fed Janet Yellen. Previously published data showed that US GDP growth for the 1st quarter was revised upwards, which increases the likelihood of the Fed raising interest rates soon. Bureau of Economic Analysis reported that real GDP grew by 0.8 per cent per annum in the first quarter of 2016. In preliminary estimates, real GDP grew by 0.5 per cent. In the fourth quarter, real GDP increased by 1.4 percent. Real GDP growth in the first quarter primarily reflected positive contributions from personal consumption expenditures (PCE), residential investment in fixed assets, as well as the costs of state and local authorities, which were partially offset by a negative contribution from residential fixed capital investment, exports, private investment in inventories and federal government spending. Imports, which is deducted in the calculation of GDP, decreased.

Meanwhile, the final results of the studies submitted by Thomson-Reuters and Institute of Michigan, revealed in May US consumers felt more optimistic about the economy than in the previous month. According to the data, in May consumer sentiment index rose to 94.7 compared with a final reading of 89.0 in April and the preliminary value of 95.8 points in May. It is estimated that the index should make 95.4.

As for the performances Yellen, she noted that in case of further improvement in the economy and the labor market, it is advisable to gradually and gently raise rates. "Based on the data, economic growth accelerated. Probably, in the following months, the rate hike would be appropriate ", - said Yellen. "Almost all the indicators point to the fact that the labor market situation has really improved. We are close to reaching the level of unemployment, which, according to most economists, corresponds to full employment. However, productivity growth is very weak, and we do not see a significant acceleration of wage growth, suggesting the preservation of free resources on the labor market ", - added the head of the Fed. Today futures on interest rates Fed indicate that the probability of a rate hike in June is 34% against 28% before the speech Yellen. Meanwhile, the chances increase rates in July increased from 55% to 62%.

The yen fell against the dollar, returning to yesterday's low, which was caused by statements of Fed Yellen. Traders also remain cautious against the yen after the G7 leaders in a statement confirmed the commitment to avoid "competitive devaluation" of their currencies and cautioned against "disorderly" currency fluctuations. Group of Seven industrialized nations pledged to strive for sustainable global growth, leveling the differences in monetary policy and stimulate the economy. "Global growth - our top priority", - said G7 leaders. The Group also outlined the commitment to market exchange rates and the elimination of "competitive devaluation" of currencies, preventing sharp jerks exchange rates. It represents a compromise between Japan, which threatened to intervene to block the spike in the yen and the US who oppose market intervention.

On the trading dynamics have also influenced the news that Japanese Prime Minister Abe could once again defer the planned increase in sales tax in Japan. Today it is the first time he admitted this possibility, although according to his advisers, he considered it before. Earlier, Abe and others have provided the Government of Japan stated that the increase in sales tax next year will continue the planned scenario, if the global economy does not face a new world financial crisis.

-

18:07

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes higher in late morning trading on Friday, with the S&P 500 on track for its largest weekly gain since March, helped by gains in consumer discretionary and health stocks and ahead of a speech by Federal Reserve Chair Janet Yellen. Investors are looking for clues on the timing of the next rate hike from Yellen's speech, which comes after comments from several policymakers earlier this week that the U.S. economy has the capacity to absorb a rate hike.

Most of Dow stocks in positive area (21 of 30). Top looser - Wal-Mart Stores Inc. (WMT, -0,51%). Top gainer - UnitedHealth Group Incorporated (UNH, +1,02%).

S&P sectors mixed. Top looser - Basic Materials (-0,3%). Top gainer - Services (+0,6%).

At the moment:

Dow 17845.00 +28.00 +0.16%

S&P 500 2094.25 +4.50 +0.22%

Nasdaq 100 4510.75 +18.50 +0.41%

Oil 49.27 -0.21 -0.42%

Gold 1217.00 -5.70 -0.47%

U.S. 10yr 1.82 -0.05

-

18:00

European stocks close: stocks closed higher ahead Yellen’s speech

Stock closed slightly higher ahead a speech by the Fed Chairwoman Janet Yellen later in the day. She will speak at Harvard University. Market participants hope for hints for further interest rate hikes.

Several Fed officials said in the recent days that an interest rate hike in June or in July would be appropriate. These comments added to speculation that the Fed may raise its interest rate in June.

No major economic reports were released in the Eurozone today.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,270.79 +5.14 +0.08 %

DAX 10,286.31 +13.60 +0.13 %

CAC 40 4,514.74 +2.10 +0.05 %

-

18:00

European stocks closed: FTSE 100 6,270.79 +5.14 +0.08% CAC 40 4,514.74 +2.10 +0.05% DAX 10,286.31 +13.60 +0.13%

-

17:44

Oil quotes show a slight decrease

The cost of oil futures fell slightly, stepping back from seven-month highs as investors took profits and weighed the prospects of oil production due to the price increase in the area of $ 50 per barrel. Pressure on the quotes is also providing US dollar strengthening. However, disruptions in oil supplies from various regions of the world restrain the fall in prices.

Despite the recent decline, oil is almost 90% higher than the February 13-year low. The increase from February to May was the most rapid in February-May 2009. "Oil markets recover balance faster than expected, we have not seen any increase in global stocks in 2017, for the first time in four years." - Said UBS analyst Giovanni Staunovo.

Investors are waiting for the speech of US Fed Yellen, from which hope to hear signals on further actions of the Central Bank. The increase in interest rates would mean higher US dollar exchange rate, the higher the dollar will lead to more expensive oil, that could trigger the sale of commodities.

Focus today will be data Baker Hughes oilfield services company in the United States in the number of drilling rigs. Recall, at the end of the working week was reduced slightly ended May 20 - 2 units, and amounted to 404 units. In annual terms, a decline of 481 units or 54.4%. "Baker Hughes data will be very important The big question is whether the trend of reducing the number of drilling will be developed, as in the past few months, oil has risen." - Said Michael Poulsen, an expert Global Risk Management.

Gradually, the focus switches to the OPEC meeting, which is scheduled for June 2nd. Discussion will focus on the possibilities of raising prices and stabilize the market. "We do not expect that OPEC will come to some sort of agreement, and the Gulf countries are likely to increase production", - said the UBS. - Elimination of supply disruptions and rising OPEC production may increase the excess supply, and prices could go back to $ 40. "

WTI for delivery in July fell to $49.39 a barrel. Brent for July fell to $49.30 a barrel.

-

17:37

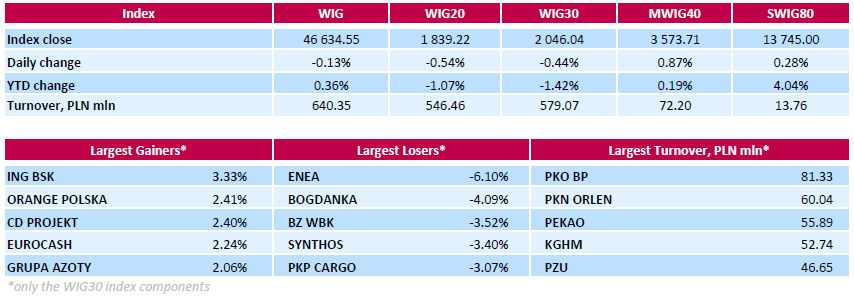

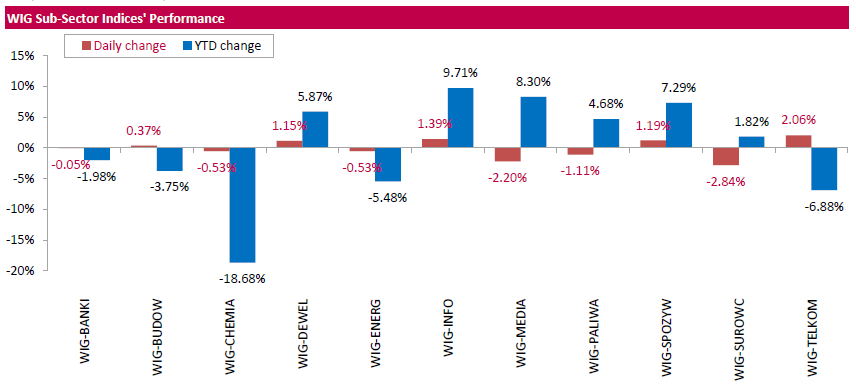

WSE: Session Results

Polish equity market closed lower on Friday. The broad market measure, the WIG index, lost 0.13%. From a sector perspective, telecoms (+2.06%) recorded the biggest gains, while materials (-2.84%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, declined by 0.44%. Within the WIG30 Index components, genco ENEA (WSE: ENA) fared the worst, slumping by 6.1% after the company announced it had no plan to pay out dividend for 2015. It was followed by thermal coal miner BOGDANKA (WSE: LWB), bank BZ WBK (WSE: BZW) and chemical producer SYNTHOS (WSE: SNS), which fell by 4.09%, 3.52% and 3.4% respectively. On the other side of the ledger, bank ING BSK (WSE: ING), telecommunication services provider ORANGE POLSKA (WSE: OPL) and videogame developer CD PROJEKT (WSE: CDR) were the best performers, jumping by 3.33%, 2.41% and 2.4% respectively.

-

17:22

Gold prices declined moderately

Gold moderately cheaper today, reaching an eight-week low, and headed to his fourth consecutive weekly fall. The cause of this trend is the strengthening of the US dollar and growing speculation that the Fed will raise interest rates in June.

It is worth emphasizing, lower prices for the precious metal is fixed for the seventh session in a row, which is the longest series in more than six months. Gold is beginning to become cheaper after the minutes of the last Fed meeting, released last week, indicated that the FOMC members do not rule out raising interest rates at its next meeting in June. Recall, higher interest rates have a downward pressure on the price of gold, which brings its holders to interest income and that is difficult to compete with the assets, bringing that income against the background of increasing interest rates.

"Expectations for improving the Fed in June changed over the past couple of weeks, and taking into account the strengthening of the US dollar and rising stocks, the fall in gold prices looks reasonable. Another reason for the reduction of the precious metal is the current positioning. The data from the CFTC, published last week, showed that net long positions accounted for about 98 percent from a record high, "- said an analyst at UBS Joni Tevez.

Meanwhile, yesterday the Fed Jerome Powell said that the rise in interest rates in the US could happen "pretty soon". However, he warned that it will depend on the state of the economy, including the labor market situation. "There are good reasons to believe that the underlying growth rate of higher" than one might think, based on the latest reports on consumer spending - Powell said. - Labor market data generally give the best signal in real time on the latent pace of economic activity "He stressed that, according to these data, the US economy is now." On a solid basis. "

Attention also focused on the market scheduled for today, the speech of Fed Yellen, which is expected to hear the signals for further actions of the Central Bank. Currently, futures on interest rates Fed indicate that the probability of a rate hike of 24% in June, against 4% last Monday. Meanwhile, the chances increase rate estimated at 55% in July.

The cost of the June gold futures on the COMEX fell to $ 1210.7 per ounce.

-

16:29

Thomson Reuters/University of Michigan final consumer sentiment index rises to 94.7 in May

The Thomson Reuters/University of Michigan final consumer sentiment index climbed to 94.7 in May from 89.0 in April, down from the preliminary estimate of 95.8 and missing expectations a rise to 95.4.

"Sespite the meager GDP growth as well as a higher inflation rate, consumers became more optimistic about their financial prospects and anticipated a somewhat lower inflation rate in the years ahead," the Surveys of Consumers chief economist at the University of Michigan Richard Curtin.

"The biggest uncertainty consumers see on the horizon is not whether the Fed will hike interest rates in the next few months, but the outlook for future government economic policies under a new president," he added.

The current economic conditions index increased to 109.9 in May from 106.7 in April, down from the preliminary reading of 108.6.

The index of consumer expectations rose to 84.9 in May from 77.6 in April, down from a preliminary reading of 87.5.

The one-year inflation expectations declined to 2.4% in May from 2.8% in April, down from the preliminary reading of 2.5%.

-

16:00

U.S.: Reuters/Michigan Consumer Sentiment Index, May 94.7 (forecast 95.4)

-

15:45

Option expiries for today's 10:00 ET NY cut

USD/JPY 108.00 (USD 200m) 110.75 (250m)

EUR/USD: 1.1100 (EUR 248m) 1.1150 (660m)

GBP/USD 1.4450 (GBP 526m) 1.4585 (493m)

EUR/GBP 0.7635 (EUR 730m) 0.7750 (875m) 0.7800 (420m)

AUD/USD 0.7210 (AUD 1.08bln) 0.7500 (340m)

USD/CAD 1.3000 (USD 560m) 1.3150 (360m)

-

15:32

U.S. Stocks open: Dow +0.04%, Nasdaq +0.05%, S&P +0.07%

-

15:32

Profits of industrial companies in China climb in April from a year earlier

China's National Bureau of Statistics (NBS) said on Friday that profits of industrial companies in China climbed 4.2% in April from a year earlier, after a 11.1% gain in March.

For the first months of 2016, industrial profits climbed 6.5% from a year earlier.

-

15:26

Before the bell: S&P futures +0.10%, NASDAQ futures +0.18%

U.S. stock-index futures were little changed.

Global Stocks:

Nikkei 16,834.84 +62.38 +0.37%

Hang Seng 20,576.77 +179.66 +0.88%

Shanghai Composite 2,821.54 -0.91 -0.03%

FTSE 6,261 -4.65 -0.07%

CAC 4,503.53 -9.11 -0.20%

DAX 10,286.05 +13.34 +0.13%

Crude $48.95 (-1.07%)

Gold $1218.20 (-0.18%)

-

14:58

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.54

0.03(0.3155%)

17102

Amazon.com Inc., NASDAQ

AMZN

715.99

1.08(0.1511%)

7617

American Express Co

AXP

65.33

0.10(0.1533%)

181

Apple Inc.

AAPL

99.37

-1.04(-1.0358%)

282017

AT&T Inc

T

38.92

0.08(0.206%)

968

Barrick Gold Corporation, NYSE

ABX

16.97

-0.16(-0.934%)

34266

Boeing Co

BA

129.07

-0.24(-0.1856%)

400

Chevron Corp

CVX

101.2

-0.30(-0.2956%)

2390

Cisco Systems Inc

CSCO

28.93

0.03(0.1038%)

8055

Citigroup Inc., NYSE

C

46.25

0.14(0.3036%)

4890

Facebook, Inc.

FB

119.62

0.15(0.1256%)

34556

Ford Motor Co.

F

13.49

0.03(0.2229%)

6544

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.43

0.09(0.7937%)

88875

General Electric Co

GE

30.03

0.01(0.0333%)

1272

General Motors Company, NYSE

GM

31.39

0.10(0.3196%)

2754

Goldman Sachs

GS

159.05

0.48(0.3027%)

125

Google Inc.

GOOG

726.91

2.79(0.3853%)

2801

Hewlett-Packard Co.

HPQ

13.04

-0.00(-0.00%)

500

Intel Corp

INTC

31.58

0.09(0.2858%)

570

JPMorgan Chase and Co

JPM

65.11

0.08(0.123%)

4138

Microsoft Corp

MSFT

51.9

0.01(0.0193%)

3033

Pfizer Inc

PFE

34.35

-0.08(-0.2324%)

550

Starbucks Corporation, NASDAQ

SBUX

55.49

0.20(0.3617%)

2071

Tesla Motors, Inc., NASDAQ

TSLA

225.79

0.67(0.2976%)

9114

The Coca-Cola Co

KO

44.71

0.02(0.0448%)

525

Twitter, Inc., NYSE

TWTR

14.28

-0.02(-0.1399%)

20130

Visa

V

79.15

0.15(0.1899%)

525

Wal-Mart Stores Inc

WMT

70.8

-0.05(-0.0706%)

641

Yahoo! Inc., NASDAQ

YHOO

36.92

0.16(0.4353%)

7853

Yandex N.V., NASDAQ

YNDX

19.91

0.06(0.3023%)

1200

-

14:48

U.S. revised GDP rises 0.8% in the first quarter

The U.S. Commerce Department released gross domestic product (GDP) figures on Friday. The U.S. revised GDP climbed 0.8% in the first quarter, up from the preliminary estimate of a 0.5% rise, after a 1.4% in the fourth quarter. Analysts had expected the U.S. economy to expand 0.9% in the first quarter.

The upward revision was partly driven by a downward revision of the trade deficit.

Consumer spending rose by 1.9% in the first quarter, in line with the previous estimate.

Exports fell 2.0% in the first quarter, up from the preliminary estimate of a 2.6% fall, while imports were down 0.2%, down from the preliminary estimate of a 0.2% rise.

The PCE price index increased 0.3% in the first quarter, in line with the preliminary estimate, after a 0.3% rise in the fourth quarter.

The PCE price index excluding food and energy costs increased 2.1% in the first quarter, in line with the preliminary estimate, after a 1.3% rise in the fourth quarter.

The PCE price index is the Fed's preferred gauge for inflation.

-

14:31

U.S.: PCE price index ex food, energy, q/q, Quarter I 2.1% (forecast 2.1%)

-

14:30

U.S.: GDP, q/q, Quarter I 0.8% (forecast 0.9%)

-

14:30

U.S.: PCE price index, q/q, Quarter I 0.3% (forecast 0.3%)

-

14:16

Foreign exchange market. European session: the U.S. dollar traded mixed to higher against the most major currencies ahead of the release of the U.S. economic data

The U.S. dollar traded mixed to higher against the most major currencies ahead of the release of the U.S. economic data. The revised personal consumer expenditures (PCE) price index excluding food and energy is expected to increase 2.1% in the first quarter.

The revised U.S. GDP is expected to rise 0.9% in the first quarter, after a 1.4% growth in the fourth quarter.

The Fed Chairwoman Janet Yellen will speak at 17:15 GMT. Market participants hope for hints for further interest rate hikes.

The euro traded lower against the U.S. dollar in the absence of any major economic data from the Eurozone.

The British pound traded lower against the U.S. dollar in the absence of any major economic data from the U.K.

fk released its consumer confidence index for the U.K. on late Thursday evening. GfK's U.K. consumer confidence index rose to -1 in May from -3 in April. 4 of 5 measures rose in May.

"Despite the tiny uptick this month, our confidence in economic matters, whether we look back or ahead 12 months, remains way below last year," Joe Staton, Head of Market Dynamics at GfK, said.

"Is it because the Brexit gremlins are hard at work? Almost certainly yes," he added.

EUR/USD: the currency pair declined to $1.1162

GBP/USD: the currency pair fell to $1.4619

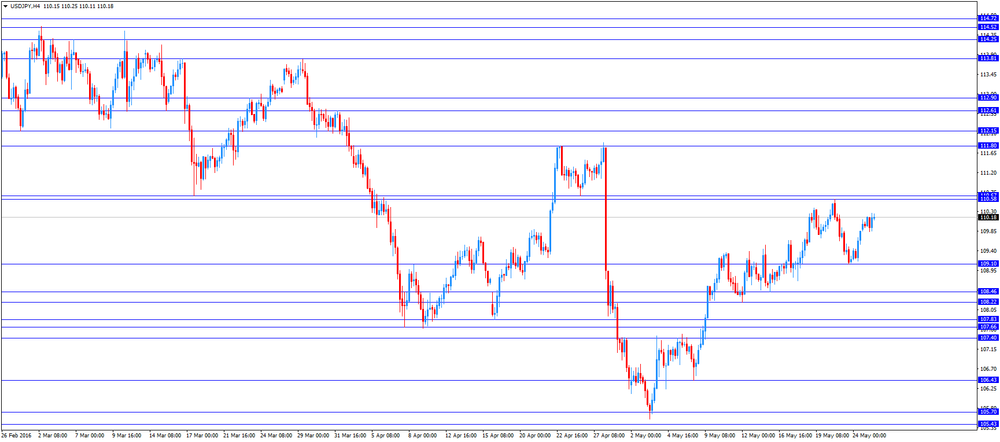

USD/JPY: the currency pair was down to Y109.55

The most important news that are expected (GMT0):

12:30 U.S. PCE price index, q/q (Revised) Quarter I 0.3% 0.3%

12:30 U.S. PCE price index ex food, energy, q/q (Revised) Quarter I 2.1% 2.1%

12:30 U.S. GDP, q/q (Revised) Quarter I 1.4% 0.9%

14:00 U.S. Reuters/Michigan Consumer Sentiment Index (Finally) May 89 95.4

17:15 U.S. Fed Chairman Janet Yellen Speaks

-

14:04

European stock markets mid session: stocks traded higher ahead Yellen’s speech

Stock indices traded higher ahead a speech by the Fed Chairwoman Janet Yellen later in the day. She will speak at Harvard University. Market participants hope for hints for further interest rate hikes.

Several Fed officials said in the recent days that an interest rate hike in June or in July would be appropriate. These comments added to speculation that the Fed may raise its interest rate in June.

No major economic reports were released in the Eurozone today.

Current figures:

Name Price Change Change %

FTSE 100 6,270.59 +4.94 +0.08 %

DAX 10,277.84 +5.13 +0.05 %

CAC 40 4,512.87 +0.23 +0.01 %

-

11:44

Italian consumer confidence index decreases to 112.7 in May

The Italian statistical office Istat released its consumer confidence index for Italy on Wednesday. The Italian consumer confidence index decreased to 112.7 in May from 114.1 in April. April's figure was revised down from 114.2.

The decrease was driven by declines in economic, current and future components.

The business confidence index fell to 102.1 in May from 102.7 in April.

The decline was driven by a less favourable assessment on order books.

-

11:37

GfK’s U.K. consumer confidence index rises to -1 in May

Gfk released its consumer confidence index for the U.K. on late Thursday evening. GfK's U.K. consumer confidence index rose to -1 in May from -3 in April.

4 of 5 measures rose in May.

"Despite the tiny uptick this month, our confidence in economic matters, whether we look back or ahead 12 months, remains way below last year," Joe Staton, Head of Market Dynamics at GfK, said.

"Is it because the Brexit gremlins are hard at work? Almost certainly yes," he added.

-

11:32

Retail sales in Spain rise at a seasonally adjusted rate of 0.6% in April

The Spanish statistical office INE released its retail sales data on Friday. Retail sales in Spain rose at a seasonally adjusted rate of 0.6% in April, after a 0.5% gain in March.

Food sales were up 1.4% in April, while non-food sales increased by 0.8%.

On a yearly basis, retail sales climbed at a seasonally adjusted rate of 4.1% in April, after a 4.4% rise in March.

Sales of non-food products jumped 5.8% in April from a year ago, while food sales rose 1.1%.

-

11:28

French consumer confidence index climbed to 98 in May

French statistical office INSEE released its consumer confidence index for France on Friday. French consumer confidence index climbed to 95 in May from 94 in April. It was the highest level since October 2007.

The index of the outlook on consumers' saving capacity rose to -2 in May from -5 in April.

The index of households' assessment of their financial situation in the past twelve months remained unchanged at -25 in May.

The index of the outlook on consumers' financial situation for next twelve months increased to -9 in May from -14 in April.

The index of the outlook on unemployment rising in coming months dropped to 21 in May from 49 in April.

The index for future inflation expectations remained fell to -39 in May from -36 in April.

-

11:06

Fed Governor Jerome Powell: the Fed could raise its interest rate soon

Fed Governor Jerome Powell said in a speech on Thursday that the Fed could raise its interest rate soon.

"Depending on the incoming data and the evolving risks, another rate increase may be appropriate fairly soon," he said.

"Several factors suggest that the pace of rate increases should be gradual," Powell added.

Fed governor noted that the referendum on Britain's membership in the European Union could weigh on the Fed's interest rate decision in June.

Powell is a voting member of the Federal Open Market Committee (FOMC).

-

10:56

St. Louis Fed President James Bullard: financial markets have an appropriate view on the Fed’s monetary policy in June after the release of the Fed’s April minutes

St. Louis Fed President James Bullard said on Thursday that financial markets had an appropriate view on the Fed's monetary policy in June after the release of the Fed's April monetary policy meeting minutes.

"I think they read the minutes correctly," he said.

Bullard noted that the Fed's interest rate decision in June would depend on the incoming economic data.

-

10:43

Bloomberg Consumer Comfort Index: consumers’ expectations for U.S. economy decline to 42.0 in in the week ended May 22

According to data from the Bloomberg Consumer Comfort Index, consumers' expectations for U.S. economy declined to 42.0 in in the week ended May 22 from 42.6 the prior week.

The decrease was driven by drops in 2 of 3 sub-indexes. The measure of views of the economy was down to 31.7 from 32.4, the buying climate index remained unchanged at 38.9, while the personal finances index fell to 55.3 from 56.5.

-

10:23

Japan's national CPI declines to an annual rate of -0.3% in April

Japan's Ministry of Internal Affairs and Communications released its inflation data on late Thursday evening. Japan's national consumer price index (CPI) declined to an annual rate of -0.3% in April from -0.1% in March, in line with expectations.

Inflation was mainly driven by declines in fuel and communication prices. Fuel prices slid 9.1% year-on-year in April, while communication prices declined 2.5%.

Japan's national CPI excluding fresh food remained unchanged at an annual rate of -0.3% in April, beating expectations for a drop to -0.4%.

The Bank of Japan's inflation target is 2%.

-

10:12

U.S. pending home sales increases 5.1% in April

The National Association of Realtors (NAR) released its pending home sales figures for the U.S. on Thursday. Pending home sales in the U.S. increased 5.1% in April, exceeding expectations for a 0.6% gain, after a 1.6% rise in March. March's figure was revised up from a 1.4% gain.

The increase was led by rises in almost all regions. Only pending home sales in the Midwest region declined in April

"The building momentum from the over 14 million jobs created since 2010 and the prospect of facing higher rents and mortgage rates down the road appear to be bringing more interested buyers into the market," the NAR's chief economist Lawrence Yun said.

"Even if rates rise soon, sales have legs for further expansion this summer if housing supply increases enough to give buyers an adequate number of affordable choices during their search," he added.

-

10:08

Option expiries for today's 10:00 ET NY cut

USD/JPY 108.00 (USD 200m) 110.75 (250m)

EUR/USD: 1.1100 (EUR 248m) 1.1150 (660m)

GBP/USD 1.4450 (GBP 526m) 1.4585 (493m)

EUR/GBP 0.7635 (EUR 730m) 0.7750 (875m) 0.7800 (420m)

AUD/USD 0.7210 (AUD 1.08bln) 0.7500 (340m)

USD/CAD 1.3000 (USD 560m) 1.3150 (360m)

-

08:34

Options levels on friday, May 27, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1406 (5101)

$1.1319 (3670)

$1.1254 (3695)

Price at time of writing this review: $1.1192

Support levels (open interest**, contracts):

$1.1112 (5530)

$1.1077 (5191)

$1.1036 (3311)

Comments:

- Overall open interest on the CALL options with the expiration date June, 3 is 71409 contracts, with the maximum number of contracts with strike price $1,1400 (5101);

- Overall open interest on the PUT options with the expiration date June, 3 is 87843 contracts, with the maximum number of contracts with strike price $1,1200 (7968);

- The ratio of PUT/CALL was 1.23 versus 1.24 from the previous trading day according to data from May, 26

GBP/USD

Resistance levels (open interest**, contracts)

$1.4901 (2024)

$1.4803 (1717)

$1.4707 (2056)

Price at time of writing this review: $1.4660

Support levels (open interest**, contracts):

$1.4594 (964)

$1.4497 (1238)

$1.4399 (1906)

Comments:

- Overall open interest on the CALL options with the expiration date June, 3 is 32846 contracts, with the maximum number of contracts with strike price $1,4600 (2470);

- Overall open interest on the PUT options with the expiration date June, 3 is 34981 contracts, with the maximum number of contracts with strike price $1,4200 (3023);

- The ratio of PUT/CALL was 1.07 versus 1.05 from the previous trading day according to data from May, 26

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:25

Asian session: The dollar stayed

The dollar stayed in consolidation mode on Friday after its rally to two-month highs ran out of steam with bulls looking for fresh guidance from the head of the U.S. central bank. It is still up nearly 2.3 percent this month, among the top performing currencies, after a string of Federal Reserve officials bolstered expectations for a hike in interest rates as early as next month. Traders are now keen to hear from Fed Chair Janet Yellen, who is due to speak at an event hosted by the Harvard University Radcliffe Institute for Advanced Study at 1715 GMT. Also closely watched is the second estimate of the March quarter U.S. gross domestic product. Analysts polled by Reuters expect to see an upgrade of the earlier reading, which showed the economy grew at its slowest pace in two years.

There was little reaction to the outcome of a two-day Group of Seven summit. The G7 industrial powers pledged on Friday to seek strong global growth, while papering over differences on currencies and stimulus policies.

The yen showed limited reaction to media reports that Japanese Prime Minister Shinzo Abe is considering delaying a sales tax hike, originally planned in April 2017, by around two years. If Japan were to delay the planned sales tax hike, some market participants say the initial reaction may be for Tokyo shares to rise, which could weigh on the safe haven yen. Still, a possible postponement of the sales tax hike has probably been mostly factored in, said a trader for a Japanese bank in Singapore, so any market impact may be limited even in the event of an official announcement to that effect.

EUR/USD: during the Asian session the pair traded in the range of $1.1185-00

GBP/USD: during the Asian session the pair traded in the range of $1.4655-80

USD/JPY: during the Asian session the pair climbed to Y110.00

Based on Reuters materials

-

06:27

Global Stocks

European stocks logged a modest gain Thursday as energy shares got a brief boost from Brent crude futures, which extended their gains to touch the $50-a-barrel level. Meanwhile, Spanish banks put the pan-European index under pressure as Banco Popular Español SA plunged. Earlier stocks had benefited from a rise in crude but relinquished those gains as crude futures retreated. Still, the Stoxx Europe 600 managed to close at its best level in 5 weeks after a three straight days of gains, FactSet data show.

U.S. stocks closed little changed Thursday after two days of strong gains as crude-oil futures failed to hang on to a move above $50 a barrel and investors brushed off better-than-expected economic reports. Orders for durable goods manufactured in the U.S. jumped in April, fueled by higher demand for new cars, trucks and commercial jets. But a key measure of business investment fell again. Meanwhile, jobless claims declined to a one-month low last week, suggesting the labor market remained robust.

Asian stock markets were mostly higher Friday as investors maintained a cautiously optimistic outlook while they waited for U.S. economic data and remarks by the Fed chief. Investors will be watching to see what Federal Reserve chair Janet Yellen has to say about monetary policy

Based on MarketWatch materials

-

04:03

Nikkei 225 16,837.51 +65.05 +0.39 %, Hang Seng 20,308.91 -88.20 -0.43 %, Shanghai Composite 2,813.66 -8.78 -0.31 %

-

01:31

Japan: National Consumer Price Index, y/y, April -0.5% (forecast -0.3%)

-

01:31

Japan: Tokyo CPI ex Fresh Food, y/y, May 0.5% (forecast -0.4%)

-

01:31

Japan: National CPI Ex-Fresh Food, y/y, April -0.5% (forecast -0.4%)

-

01:30

Japan: Tokyo Consumer Price Index, y/y, May -0.5% (forecast -0.4%)

-

00:30

Commodities. Daily history for May 26’2016:

(raw materials / closing price /% change)

Oil 49.40 -0.16%

Gold 1,219.80 -0.05%

-

00:30

Stocks. Daily history for Sep Apr May 26’2016:

(index / closing price / change items /% change)

Nikkei 225 16,772.46 +15.11 +0.09 %

Hang Seng 20,397.11 +29.06 +0.14 %

S&P/ASX 200 5,388.09 +15.58 +0.29 %

Shanghai Composite 2,822.57 +7.49 +0.27 %

FTSE 100 6,265.65 +2.80 +0.04 %

CAC 40 4,512.64 +31.00 +0.69 %

Xetra DAX 10,272.71 +67.50 +0.66 %

S&P 500 2,090.1 -0.44 -0.02 %

NASDAQ Composite 4,901.77 +6.88 +0.14 %

Dow Jones 17,828.29 -23.22 -0.13 %

-

00:29

Currencies. Daily history for May 26’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1192 +0,34%

GBP/USD $1,4664 -0,26%

USD/CHF Chf0,989 -0,22%

USD/JPY Y109,75 -0,38%

EUR/JPY Y122,83 -0,05%

GBP/JPY Y160,91 -0,66%

AUD/USD $0,7223 +0,48%

NZD/USD $0,6740 +0,34%

USD/CAD C$1,2974 -0,35%

-

00:01

Schedule for today, Friday, May 27’2016:

(time / country / index / period / previous value / forecast)

12:30 U.S. PCE price index, q/q Quarter I 0.3% 0.3%

12:30 U.S. PCE price index ex food, energy, q/q Quarter I 2.1% 2.1%

12:30 U.S. GDP, q/q Quarter I 1.4% 0.9%

14:00 U.S. Reuters/Michigan Consumer Sentiment Index May 89 95.4

17:15 U.S. Fed Chairman Janet Yellen Speaks

-