Noticias del mercado

-

21:00

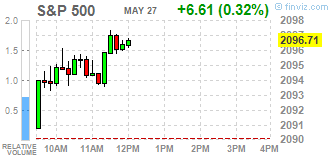

Dow +0.13% 17,850.86 +22.57 Nasdaq +0.47% 4,924.98 +23.21 S&P +0.27% 2,095.84 +5.74

-

18:07

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes higher in late morning trading on Friday, with the S&P 500 on track for its largest weekly gain since March, helped by gains in consumer discretionary and health stocks and ahead of a speech by Federal Reserve Chair Janet Yellen. Investors are looking for clues on the timing of the next rate hike from Yellen's speech, which comes after comments from several policymakers earlier this week that the U.S. economy has the capacity to absorb a rate hike.

Most of Dow stocks in positive area (21 of 30). Top looser - Wal-Mart Stores Inc. (WMT, -0,51%). Top gainer - UnitedHealth Group Incorporated (UNH, +1,02%).

S&P sectors mixed. Top looser - Basic Materials (-0,3%). Top gainer - Services (+0,6%).

At the moment:

Dow 17845.00 +28.00 +0.16%

S&P 500 2094.25 +4.50 +0.22%

Nasdaq 100 4510.75 +18.50 +0.41%

Oil 49.27 -0.21 -0.42%

Gold 1217.00 -5.70 -0.47%

U.S. 10yr 1.82 -0.05

-

18:00

European stocks close: stocks closed higher ahead Yellen’s speech

Stock closed slightly higher ahead a speech by the Fed Chairwoman Janet Yellen later in the day. She will speak at Harvard University. Market participants hope for hints for further interest rate hikes.

Several Fed officials said in the recent days that an interest rate hike in June or in July would be appropriate. These comments added to speculation that the Fed may raise its interest rate in June.

No major economic reports were released in the Eurozone today.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,270.79 +5.14 +0.08 %

DAX 10,286.31 +13.60 +0.13 %

CAC 40 4,514.74 +2.10 +0.05 %

-

18:00

European stocks closed: FTSE 100 6,270.79 +5.14 +0.08% CAC 40 4,514.74 +2.10 +0.05% DAX 10,286.31 +13.60 +0.13%

-

17:37

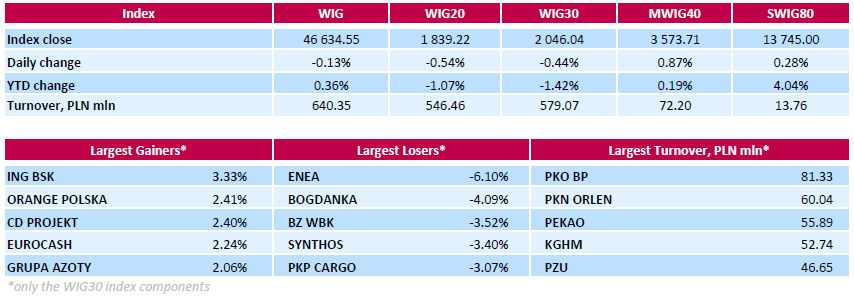

WSE: Session Results

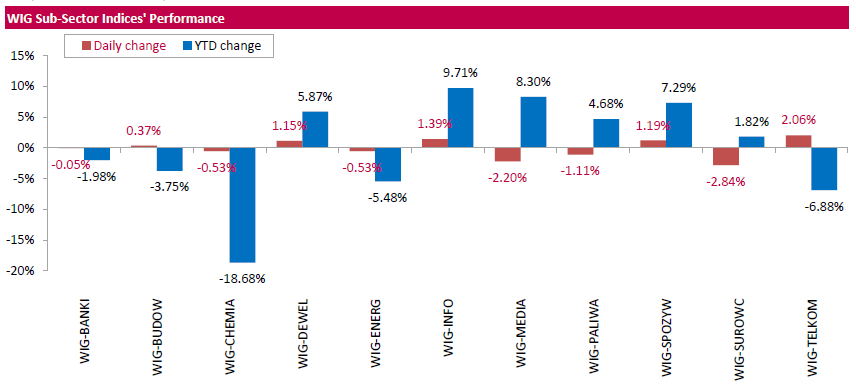

Polish equity market closed lower on Friday. The broad market measure, the WIG index, lost 0.13%. From a sector perspective, telecoms (+2.06%) recorded the biggest gains, while materials (-2.84%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, declined by 0.44%. Within the WIG30 Index components, genco ENEA (WSE: ENA) fared the worst, slumping by 6.1% after the company announced it had no plan to pay out dividend for 2015. It was followed by thermal coal miner BOGDANKA (WSE: LWB), bank BZ WBK (WSE: BZW) and chemical producer SYNTHOS (WSE: SNS), which fell by 4.09%, 3.52% and 3.4% respectively. On the other side of the ledger, bank ING BSK (WSE: ING), telecommunication services provider ORANGE POLSKA (WSE: OPL) and videogame developer CD PROJEKT (WSE: CDR) were the best performers, jumping by 3.33%, 2.41% and 2.4% respectively.

-

16:29

Thomson Reuters/University of Michigan final consumer sentiment index rises to 94.7 in May

The Thomson Reuters/University of Michigan final consumer sentiment index climbed to 94.7 in May from 89.0 in April, down from the preliminary estimate of 95.8 and missing expectations a rise to 95.4.

"Sespite the meager GDP growth as well as a higher inflation rate, consumers became more optimistic about their financial prospects and anticipated a somewhat lower inflation rate in the years ahead," the Surveys of Consumers chief economist at the University of Michigan Richard Curtin.

"The biggest uncertainty consumers see on the horizon is not whether the Fed will hike interest rates in the next few months, but the outlook for future government economic policies under a new president," he added.

The current economic conditions index increased to 109.9 in May from 106.7 in April, down from the preliminary reading of 108.6.

The index of consumer expectations rose to 84.9 in May from 77.6 in April, down from a preliminary reading of 87.5.

The one-year inflation expectations declined to 2.4% in May from 2.8% in April, down from the preliminary reading of 2.5%.

-

15:32

U.S. Stocks open: Dow +0.04%, Nasdaq +0.05%, S&P +0.07%

-

15:32

Profits of industrial companies in China climb in April from a year earlier

China's National Bureau of Statistics (NBS) said on Friday that profits of industrial companies in China climbed 4.2% in April from a year earlier, after a 11.1% gain in March.

For the first months of 2016, industrial profits climbed 6.5% from a year earlier.

-

15:26

Before the bell: S&P futures +0.10%, NASDAQ futures +0.18%

U.S. stock-index futures were little changed.

Global Stocks:

Nikkei 16,834.84 +62.38 +0.37%

Hang Seng 20,576.77 +179.66 +0.88%

Shanghai Composite 2,821.54 -0.91 -0.03%

FTSE 6,261 -4.65 -0.07%

CAC 4,503.53 -9.11 -0.20%

DAX 10,286.05 +13.34 +0.13%

Crude $48.95 (-1.07%)

Gold $1218.20 (-0.18%)

-

14:58

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.54

0.03(0.3155%)

17102

Amazon.com Inc., NASDAQ

AMZN

715.99

1.08(0.1511%)

7617

American Express Co

AXP

65.33

0.10(0.1533%)

181

Apple Inc.

AAPL

99.37

-1.04(-1.0358%)

282017

AT&T Inc

T

38.92

0.08(0.206%)

968

Barrick Gold Corporation, NYSE

ABX

16.97

-0.16(-0.934%)

34266

Boeing Co

BA

129.07

-0.24(-0.1856%)

400

Chevron Corp

CVX

101.2

-0.30(-0.2956%)

2390

Cisco Systems Inc

CSCO

28.93

0.03(0.1038%)

8055

Citigroup Inc., NYSE

C

46.25

0.14(0.3036%)

4890

Facebook, Inc.

FB

119.62

0.15(0.1256%)

34556

Ford Motor Co.

F

13.49

0.03(0.2229%)

6544

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.43

0.09(0.7937%)

88875

General Electric Co

GE

30.03

0.01(0.0333%)

1272

General Motors Company, NYSE

GM

31.39

0.10(0.3196%)

2754

Goldman Sachs

GS

159.05

0.48(0.3027%)

125

Google Inc.

GOOG

726.91

2.79(0.3853%)

2801

Hewlett-Packard Co.

HPQ

13.04

-0.00(-0.00%)

500

Intel Corp

INTC

31.58

0.09(0.2858%)

570

JPMorgan Chase and Co

JPM

65.11

0.08(0.123%)

4138

Microsoft Corp

MSFT

51.9

0.01(0.0193%)

3033

Pfizer Inc

PFE

34.35

-0.08(-0.2324%)

550

Starbucks Corporation, NASDAQ

SBUX

55.49

0.20(0.3617%)

2071

Tesla Motors, Inc., NASDAQ

TSLA

225.79

0.67(0.2976%)

9114

The Coca-Cola Co

KO

44.71

0.02(0.0448%)

525

Twitter, Inc., NYSE

TWTR

14.28

-0.02(-0.1399%)

20130

Visa

V

79.15

0.15(0.1899%)

525

Wal-Mart Stores Inc

WMT

70.8

-0.05(-0.0706%)

641

Yahoo! Inc., NASDAQ

YHOO

36.92

0.16(0.4353%)

7853

Yandex N.V., NASDAQ

YNDX

19.91

0.06(0.3023%)

1200

-

14:48

U.S. revised GDP rises 0.8% in the first quarter

The U.S. Commerce Department released gross domestic product (GDP) figures on Friday. The U.S. revised GDP climbed 0.8% in the first quarter, up from the preliminary estimate of a 0.5% rise, after a 1.4% in the fourth quarter. Analysts had expected the U.S. economy to expand 0.9% in the first quarter.

The upward revision was partly driven by a downward revision of the trade deficit.

Consumer spending rose by 1.9% in the first quarter, in line with the previous estimate.

Exports fell 2.0% in the first quarter, up from the preliminary estimate of a 2.6% fall, while imports were down 0.2%, down from the preliminary estimate of a 0.2% rise.

The PCE price index increased 0.3% in the first quarter, in line with the preliminary estimate, after a 0.3% rise in the fourth quarter.

The PCE price index excluding food and energy costs increased 2.1% in the first quarter, in line with the preliminary estimate, after a 1.3% rise in the fourth quarter.

The PCE price index is the Fed's preferred gauge for inflation.

-

14:04

European stock markets mid session: stocks traded higher ahead Yellen’s speech

Stock indices traded higher ahead a speech by the Fed Chairwoman Janet Yellen later in the day. She will speak at Harvard University. Market participants hope for hints for further interest rate hikes.

Several Fed officials said in the recent days that an interest rate hike in June or in July would be appropriate. These comments added to speculation that the Fed may raise its interest rate in June.

No major economic reports were released in the Eurozone today.

Current figures:

Name Price Change Change %

FTSE 100 6,270.59 +4.94 +0.08 %

DAX 10,277.84 +5.13 +0.05 %

CAC 40 4,512.87 +0.23 +0.01 %

-

11:44

Italian consumer confidence index decreases to 112.7 in May

The Italian statistical office Istat released its consumer confidence index for Italy on Wednesday. The Italian consumer confidence index decreased to 112.7 in May from 114.1 in April. April's figure was revised down from 114.2.

The decrease was driven by declines in economic, current and future components.

The business confidence index fell to 102.1 in May from 102.7 in April.

The decline was driven by a less favourable assessment on order books.

-

11:37

GfK’s U.K. consumer confidence index rises to -1 in May

Gfk released its consumer confidence index for the U.K. on late Thursday evening. GfK's U.K. consumer confidence index rose to -1 in May from -3 in April.

4 of 5 measures rose in May.

"Despite the tiny uptick this month, our confidence in economic matters, whether we look back or ahead 12 months, remains way below last year," Joe Staton, Head of Market Dynamics at GfK, said.

"Is it because the Brexit gremlins are hard at work? Almost certainly yes," he added.

-

11:32

Retail sales in Spain rise at a seasonally adjusted rate of 0.6% in April

The Spanish statistical office INE released its retail sales data on Friday. Retail sales in Spain rose at a seasonally adjusted rate of 0.6% in April, after a 0.5% gain in March.

Food sales were up 1.4% in April, while non-food sales increased by 0.8%.

On a yearly basis, retail sales climbed at a seasonally adjusted rate of 4.1% in April, after a 4.4% rise in March.

Sales of non-food products jumped 5.8% in April from a year ago, while food sales rose 1.1%.

-

11:28

French consumer confidence index climbed to 98 in May

French statistical office INSEE released its consumer confidence index for France on Friday. French consumer confidence index climbed to 95 in May from 94 in April. It was the highest level since October 2007.

The index of the outlook on consumers' saving capacity rose to -2 in May from -5 in April.

The index of households' assessment of their financial situation in the past twelve months remained unchanged at -25 in May.

The index of the outlook on consumers' financial situation for next twelve months increased to -9 in May from -14 in April.

The index of the outlook on unemployment rising in coming months dropped to 21 in May from 49 in April.

The index for future inflation expectations remained fell to -39 in May from -36 in April.

-

11:06

Fed Governor Jerome Powell: the Fed could raise its interest rate soon

Fed Governor Jerome Powell said in a speech on Thursday that the Fed could raise its interest rate soon.

"Depending on the incoming data and the evolving risks, another rate increase may be appropriate fairly soon," he said.

"Several factors suggest that the pace of rate increases should be gradual," Powell added.

Fed governor noted that the referendum on Britain's membership in the European Union could weigh on the Fed's interest rate decision in June.

Powell is a voting member of the Federal Open Market Committee (FOMC).

-

10:56

St. Louis Fed President James Bullard: financial markets have an appropriate view on the Fed’s monetary policy in June after the release of the Fed’s April minutes

St. Louis Fed President James Bullard said on Thursday that financial markets had an appropriate view on the Fed's monetary policy in June after the release of the Fed's April monetary policy meeting minutes.

"I think they read the minutes correctly," he said.

Bullard noted that the Fed's interest rate decision in June would depend on the incoming economic data.

-

10:43

Bloomberg Consumer Comfort Index: consumers’ expectations for U.S. economy decline to 42.0 in in the week ended May 22

According to data from the Bloomberg Consumer Comfort Index, consumers' expectations for U.S. economy declined to 42.0 in in the week ended May 22 from 42.6 the prior week.

The decrease was driven by drops in 2 of 3 sub-indexes. The measure of views of the economy was down to 31.7 from 32.4, the buying climate index remained unchanged at 38.9, while the personal finances index fell to 55.3 from 56.5.

-

10:23

Japan's national CPI declines to an annual rate of -0.3% in April

Japan's Ministry of Internal Affairs and Communications released its inflation data on late Thursday evening. Japan's national consumer price index (CPI) declined to an annual rate of -0.3% in April from -0.1% in March, in line with expectations.

Inflation was mainly driven by declines in fuel and communication prices. Fuel prices slid 9.1% year-on-year in April, while communication prices declined 2.5%.

Japan's national CPI excluding fresh food remained unchanged at an annual rate of -0.3% in April, beating expectations for a drop to -0.4%.

The Bank of Japan's inflation target is 2%.

-

10:12

U.S. pending home sales increases 5.1% in April

The National Association of Realtors (NAR) released its pending home sales figures for the U.S. on Thursday. Pending home sales in the U.S. increased 5.1% in April, exceeding expectations for a 0.6% gain, after a 1.6% rise in March. March's figure was revised up from a 1.4% gain.

The increase was led by rises in almost all regions. Only pending home sales in the Midwest region declined in April

"The building momentum from the over 14 million jobs created since 2010 and the prospect of facing higher rents and mortgage rates down the road appear to be bringing more interested buyers into the market," the NAR's chief economist Lawrence Yun said.

"Even if rates rise soon, sales have legs for further expansion this summer if housing supply increases enough to give buyers an adequate number of affordable choices during their search," he added.

-

06:27

Global Stocks

European stocks logged a modest gain Thursday as energy shares got a brief boost from Brent crude futures, which extended their gains to touch the $50-a-barrel level. Meanwhile, Spanish banks put the pan-European index under pressure as Banco Popular Español SA plunged. Earlier stocks had benefited from a rise in crude but relinquished those gains as crude futures retreated. Still, the Stoxx Europe 600 managed to close at its best level in 5 weeks after a three straight days of gains, FactSet data show.

U.S. stocks closed little changed Thursday after two days of strong gains as crude-oil futures failed to hang on to a move above $50 a barrel and investors brushed off better-than-expected economic reports. Orders for durable goods manufactured in the U.S. jumped in April, fueled by higher demand for new cars, trucks and commercial jets. But a key measure of business investment fell again. Meanwhile, jobless claims declined to a one-month low last week, suggesting the labor market remained robust.

Asian stock markets were mostly higher Friday as investors maintained a cautiously optimistic outlook while they waited for U.S. economic data and remarks by the Fed chief. Investors will be watching to see what Federal Reserve chair Janet Yellen has to say about monetary policy

Based on MarketWatch materials

-

04:03

Nikkei 225 16,837.51 +65.05 +0.39 %, Hang Seng 20,308.91 -88.20 -0.43 %, Shanghai Composite 2,813.66 -8.78 -0.31 %

-

00:30

Stocks. Daily history for Sep Apr May 26’2016:

(index / closing price / change items /% change)

Nikkei 225 16,772.46 +15.11 +0.09 %

Hang Seng 20,397.11 +29.06 +0.14 %

S&P/ASX 200 5,388.09 +15.58 +0.29 %

Shanghai Composite 2,822.57 +7.49 +0.27 %

FTSE 100 6,265.65 +2.80 +0.04 %

CAC 40 4,512.64 +31.00 +0.69 %

Xetra DAX 10,272.71 +67.50 +0.66 %

S&P 500 2,090.1 -0.44 -0.02 %

NASDAQ Composite 4,901.77 +6.88 +0.14 %

Dow Jones 17,828.29 -23.22 -0.13 %

-