Noticias del mercado

-

22:17

US stocks closed

The Standard & Poor's 500 Index rose for a third day, erasing losses for the year, as energy shares surged the most in almost three months and consumer-spending data boosted optimism on the economy.

Commodity companies surged for a second day as crude climbed to a two-week high and industrial metals gained on optimism the Chinese and American economies will spark demand for resources. Chevron Corp. rallied 3.9 percent and copper miner Freeport-McMoRan Inc. jumped 16 percent for its biggest gain since in August. Celgene Corp. rose 9.8 percent after settling a patent dispute over its top-selling drug. Micron Technology Inc. lost 2.2 percent after its quarterly sales missed estimates.

The Standard & Poor's 500 Index increased 1.2 percent to 2,064.29 at 4 p.m. in New York, as a three-day rally of 2.9 percent erased its decline for the year. The Dow Jones Industrial Average climbed 184.93 points, or 1.1 percent, to 17,602.20. The Nasdaq Composite Index added 0.9 percent. Trading in S&P 500 shares was 16 percent lower than the 30-day average. U.S. exchanges will close early on Thursday for the Christmas holiday and reopen on Dec. 28.

Equities extended a rally in this holiday shortened week, recovering from a slide to a two-month low as data showing consumers' willingness to spend buoyed optimism toward the outlook for growth. Investors were loading up on some of the year's biggest losers in search of bargains among energy and raw-materials shares.

A report today showed an increase in consumer purchases in November was accompanied by rising wages and scant inflation, indicating the biggest part of the U.S. economy will continue to underpin growth. Separate data showed orders for U.S. capital goods dropped in November for the first time in three months, showing businesses began tempering new investment after a third-quarter surge.

The consumer spending data is the latest evidence that the economy is sturdy enough to weather tighter monetary policy from the Federal Reserve. Purchases climbed by the most in three months in November, which follows a report yesterday showing consumer spending bolstered the economy in the third quarter. Other gauges today showed consumer confidence rose to the highest since July, while new homes sold at a slower pace than projected in November.

Investors have wrestled with signals that are often at odds as they assess prospects for the global economy. Optimism on the pace of U.S. growth has tangled with concern that a slowdown overseas, particularly in China, will spread. Fed officials last week signaled faith that the economy is performing well, while emphasizing they're in no hurry to further boost interest rates.

The S&P 500 has rebounded more than 10 percent from the bottom of a summer selloff that was sparked by worries over weakness in China. The benchmark historically rises in December, but the so-called Santa rally is under pressure this year. The gauge is down 0.8 percent this month, after losing as much as 3.4 percent.

-

21:00

DJIA 17588.31 171.04 0.98%, NASDAQ 5043.90 42.79 0.86%, S&P 500 2062.86 23.89 1.17%

-

18:25

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes rallied for the third straight day, led by sharp gains in energy stocks, as a rebound in crude oil prices boosted sentiment heading into the Christmas holidays. Oil prices were up after U.S. inventories fell, but still hovered near multi-year lows as oversupply concerns continued to weigh.

U.S. stock markets will have a shortened session on Thursday and stay closed on Friday for Christmas. Trading volumes are expected to remain relatively light through the holiday period.

Most of all Dow stocks in positive area (27 of 30). Top looser - NIKE, Inc. (NKE, -2,63%). Top gainer - Chevron Corporation (CVX, +3.20%).

All S&P sectors in positive area. Top gainer - Basic Materials (+3,9%).

At the moment:

Dow 17477.00 +120.00 +0.69%

S&P 500 2051.50 +15.50 +0.76%

Nasdaq 100 4607.75 +16.75 +0.36%

Oil 37.60 +1.46 +4.04%

Gold 1069.00 -5.10 -0.47%

U.S. 10yr 2.26 +0.02

-

18:00

European stocks closed: FTSE 6240.98 157.88 2.60%, DAX 10727.64 238.89 2.28%, CAC 40 4674.53 106.93 2.34%

-

17:54

WSE: Session Results

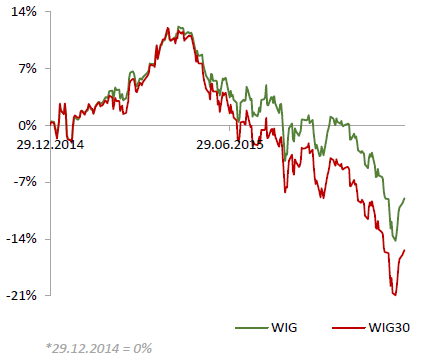

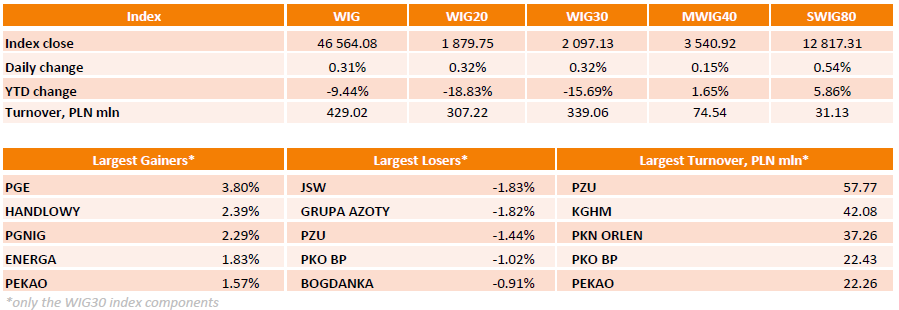

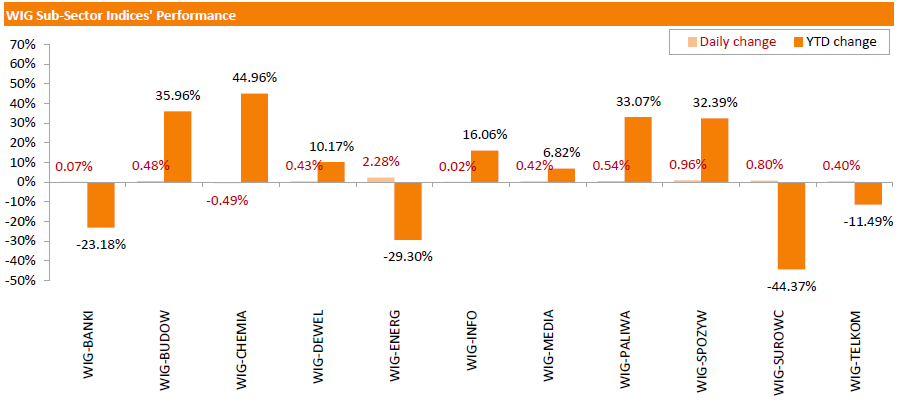

Polish equity market closed higher on Wednesday. The broad market measure, the WIG Index, rose by 0.31%. Chemicals sector (-0.49%) was sole decliner within the WIG Index, while utilities (+2.28) outpaced.

The large-cap stocks' measure, the WIG30 Index, added 0.32%. Within the index components, genco PGE (WSE: PGE) led the gainers with a 3.80% advance, followed by bank HANDLOWY (WSE: BHW) and oil and gas company PGNIG (WSE: PGN), growing by 2.39% and 2.29% respectively. At the same time, the session's most prominent losers were coking coal miner JSW (WSE: JSW), chemical producer GRUPA AZOTY (WSE: ATT), insurer PZU (WSE: PZU) and bank PKO BP (WSE: PKO), which quotations fell by 1.02%-1.83%.

The Warsaw Stock Exchange will be closed on Thursday, Dec.24, and Friday, Dec. 25, due to Christmas holidays.

-

15:35

U.S. Stocks open: Dow +0.73%, Nasdaq +0.50%, S&P +0.62%

-

15:29

Before the bell: S&P futures +0.29%, NASDAQ futures +0.34%

U.S. stock-index futures rose.

Global Stocks:

Nikkei was closed.

Hang Seng 22,040.59 +210.57 +0.96%

Shanghai Composite 3,637.28 -14.48 -0.40%

FTSE 6,212.21 +129.11 +2.12%

CAC 4,661.45 +93.85 +2.05%

DAX 10,683.11 +194.36 +1.85%

Crude oil $36.70 (+1.55%)

Gold $1070.20 (-0.36%)

-

14:56

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

3M Co

MMM

149.50

0.36%

0.5K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.70

4.36%

61.0K

Nike

NKE

135.55

2.81%

93.6K

ALCOA INC.

AA

9.75

1.99%

51.3K

Chevron Corp

CVX

91.80

1.69%

9.6K

E. I. du Pont de Nemours and Co

DD

65.59

1.49%

0.2K

Caterpillar Inc

CAT

69.22

1.18%

6.9K

Exxon Mobil Corp

XOM

78.57

1.18%

7.7K

Goldman Sachs

GS

181.70

0.92%

4.3K

Visa

V

78.05

0.87%

0.2K

General Motors Company, NYSE

GM

34.58

0.85%

1.1K

Cisco Systems Inc

CSCO

27.05

0.60%

2.2K

Tesla Motors, Inc., NASDAQ

TSLA

231.30

0.59%

1.4K

Amazon.com Inc., NASDAQ

AMZN

667.00

0.58%

4.1K

Twitter, Inc., NYSE

TWTR

22.69

0.58%

0.7K

Johnson & Johnson

JNJ

103.30

0.57%

1.0K

Walt Disney Co

DIS

107.35

0.57%

2.6K

General Electric Co

GE

30.66

0.56%

1.1K

Ford Motor Co.

F

14.28

0.56%

1.1K

JPMorgan Chase and Co

JPM

66.04

0.55%

15.2K

McDonald's Corp

MCD

118.35

0.54%

0.2K

Barrick Gold Corporation, NYSE

ABX

7.51

0.54%

4.1K

Deere & Company, NYSE

DE

78.00

0.53%

0.3K

Google Inc.

GOOG

754.00

0.53%

1.3K

Yandex N.V., NASDAQ

YNDX

15.88

0.51%

20.0K

Starbucks Corporation, NASDAQ

SBUX

60.29

0.50%

0.8K

Procter & Gamble Co

PG

79.97

0.46%

1.2K

AMERICAN INTERNATIONAL GROUP

AIG

61.00

0.44%

1.5K

Microsoft Corp

MSFT

55.59

0.43%

2.6K

Pfizer Inc

PFE

32.66

0.43%

2.3K

Citigroup Inc., NYSE

C

52.23

0.42%

9.1K

International Business Machines Co...

IBM

138.50

0.41%

0.6K

Yahoo! Inc., NASDAQ

YHOO

34.33

0.41%

14.9K

ALTRIA GROUP INC.

MO

58.00

0.40%

1.5K

Wal-Mart Stores Inc

WMT

60.77

0.38%

0.2K

The Coca-Cola Co

KO

43.45

0.37%

0.6K

Verizon Communications Inc

VZ

46.51

0.37%

1.9K

Facebook, Inc.

FB

105.90

0.37%

19.1K

Intel Corp

INTC

34.85

0.35%

14.9K

AT&T Inc

T

34.50

0.26%

5.4K

Apple Inc.

AAPL

107.35

0.11%

55.9K

-

14:45

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

NIKE (NKE) target raised to $144 from $142 at Telsey Advisory Group

NIKE (NKE) target raised to $152 from $150 at Jefferies

NIKE (NKE) target raised to $150 from $140 at Deutsche

Apple (AAPL) target lowered to $150 from $175 at FBR Capital

Apple (AAPL) target lowered to $140 from $150 at Stifel

General Electric (GE) target raised to $36 from $34 at Argus

-

07:20

Global Stocks: U.S. stock indices gained

U.S. stock indices rose on Tuesday on better-than-expected economic reports and stabilization in commodity prices.

The Dow Jones Industrial Average rose 165.65 points, or 1%, to 17,417.27. The S&P 500 gained 17.82 points, or 0.9%, to 2,039.97 (of of its 10 sectors closed higher). The Nasdaq Composite gained 32.19 points, or 0.7% to 5,001.11.

The U.S. economy expanded by a slower pace in the third quarter compared to preliminary estimations. Nevertheless the result was better than economists' expectations. The GDP rose by 2.0% in the third quarter on a seasonally adjusted basis. The preliminary report showed a 2.1% increase. Economists had expected the index to be revised to 1.9% compared to the fourth quarter final reading of 3.9%.

This morning in Asia Hong Kong Hang Seng rose 0.94%, or 205.51, to 22,035.53. China Shanghai Composite Index gained 0.37%, or 13.41, to 3.665.18. Japanese markets are on holiday.

Chinese stocks started gaining after on Monday the country's government signaled it may stimulate the economy further.

-

03:03

Hang Seng 22,015.28 +185.26 +0.85 %, Shanghai Composite 3,648.84 -2.93 -0.08 %

-

01:04

Stocks. Daily history for Sep Dec 22’2015:

(index / closing price / change items /% change)

Nikkei 225 18,886.7 -29.32 -0.16 %

Hang Seng 21,830.02 +38.34 +0.18 %

Shanghai Composite 3,652.24 +9.77 +0.27 %

FTSE 100 6,083.1 +48.26 +0.80 %

CAC 40 4,567.6 +2.43 +0.05 %

Xetra DAXт10,488.75 -9.02 -0.09 %

S&P 500 2,038.97 +17.82 +0.88 %

NASDAQ Composite 5,001.11 +32.19 +0.65 %

Dow Jones 17,417.27 +165.65 +0.96 %

-