Noticias del mercado

-

22:19

U.S. stocks closed

U.S. stocks rose for a second day as a rally in commodity shares ignited broader gains, while data showed consumer spending bolstered the economy amid slowing growth overseas.

The two most beaten-down industries this year, energy and raw-materials, led most of Tuesday's advance, keeping alive prospects for an anticipated year-end rally. Caterpillar Inc. surged 4.9 percent, while Wal-Mart Stores Inc. gained 1.7 percent as data showed consumers continued to spend. Chipotle Mexican Grill Inc. fell on an investigation into its links to a new spate of illnesses in three additional states.

The Standard & Poor's 500 Index climbed 0.9 percent to 2,039.07 at 4 p.m. in New York, as the gauge added to its rebound from a two-month low.

A report today showed the economy expanded at a revised 2 percent annualized rate in the third quarter, buoyed by consumer spending. Meanwhile, businesses struggled with weaker overseas growth and a strong dollar, which have weighed on net exports. Sustained growth in the U.S. combined with weakening in other parts of the globe, including in China, could widen the gap between exports and imports in the quarters ahead.

Investors have wavered between optimism on the U.S. economy and concern that slower growth overseas will spread. Federal Reserve policy makers last week signaled faith that the economy is performing well, while emphasizing they're in no hurry to further boost interest rates. Investors were initially soothed by that message, though oil's collapse below levels last seen during the 2008 global financial crisis has weighed on sentiment.

The S&P 500 historically rises in December, with the final two weeks delivering an average gain of 1.7 percent. The so-called Santa rally is under pressure this year, with the benchmark down 2 percent in December and in the midst of its worst final month since 2002. After rebounding as much as 13 percent from its summer low through early November, the S&P 500 has retreated 3.4 percent, putting it on track for its biggest annual drop since the 2008 financial crisis.

In addition to the GDP numbers, data this week on new-home sales, durable-goods orders and personal spending will offer further clues on the health of the economy, after the Fed's first rate increase in almost a decade. Officials at the central bank said any further rate hikes will be gradual and depend on the path of the recovery.

A separate report today showed sales of previously owned homes fell in November to the lowest level since April of last year as a change in industry rules lengthened the amount of time it took buyers to close on a deal.

-

21:00

DJIA 17409.86 158.24 0.92%, NASDAQ 4997.31 28.38 0.57%, S&P 500 2037.60 16.45 0.81%

-

18:00

European stocks closed: FTSE 6083.10 48.26 0.80%, DAX 10488.75 -9.02 -0.09%, CAC 40 4567.60 2.43 0.05%

-

17:56

WSE: Session Results

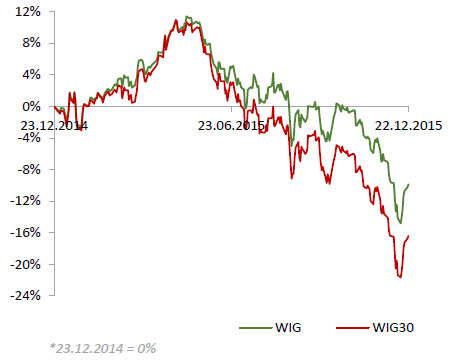

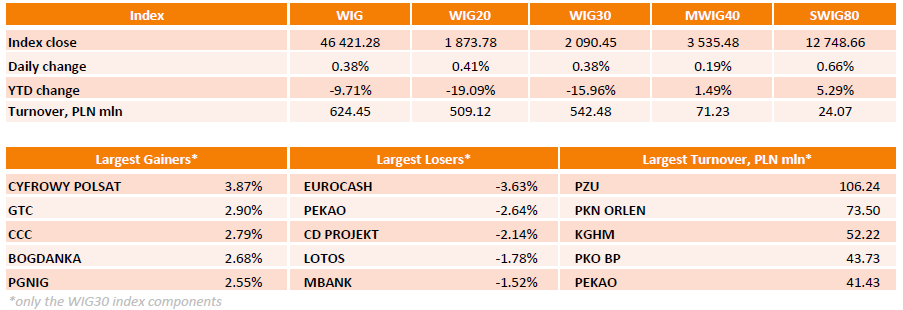

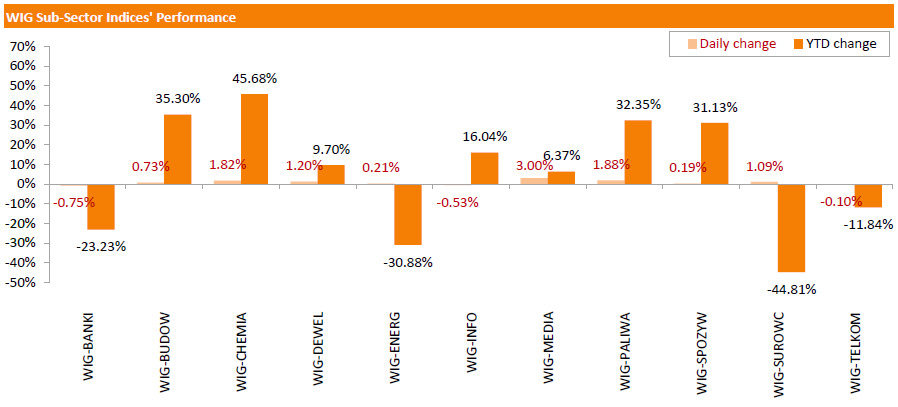

Polish equity market closed higher on Tuesday. The broad market measure, the WIG Index, surged by 0.38%. Sector-wise, media stocks (+3%) fared the best, while banking names (-0.75%) lagged behind.

The large-cap stocks advanced by 0.38%, as measured by the WIG30 Index. In the index basket, media group CYFROWY POLSAT (WSE: CPS) led the outperformers, climbing by 3.87% on analyst upgrade. It was followed by property developer GTC (WSE: GTC), footwear retailer CCC (WSE: CCC) and thermal coal miner BOGDANKA (WSE: LWB), which gained 2.9%, 2.79% and 2.68% respectively. On the other side of the ledger, FMCG wholesaler EUROCASH (WSE: EUR) was the session's weakest name, tumbling by 3.63%. Other major laggards included bank PEKAO (WSE: PEO) and videogame developer CD PROJEKT (WSE: CDR), losing 2.64% and 2.14% respectively.

-

17:19

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes rose on Tuesday as GDP data for the third quarter showed stronger-than-expected growth and crude oil prices eased off multi-year lows. Trading volumes are expected to be relatively light this week, with U.S. stock markets operating a shortened session on Thursday and closing on Friday for Christmas.

Most of Dow stocks in positive area (18 of 30). Top looser - Apple Inc. (AAPL, -0,77%). Top gainer - Caterpillar Inc. (CAT, +3.49%).

Most of S&P index sectors in positive area. Top looser - Financial (-0.1%). Top gainer - Basic Materials (+1,5%).

At the moment:

Dow 17203.00 +25.00 +0.15%

S&P 500 2016.50 +1.50 +0.07%

Nasdaq 100 4561.25 -1.75 -0.04%

Oil 36.12 +0.31 +0.87%

Gold 1074.90 -5.70 -0.53%

U.S. 10yr 2.22 +0.02

-

15:35

U.S. Stocks open: Dow +0.31%, Nasdaq +0.27%, S&P +0.33%

-

15:26

Before the bell: S&P futures +0.12%, NASDAQ futures +0.02%

U.S. stock-index futures fluctuated.

Global Stocks:

Nikkei 18,886.7 -29.32 -0.16%

Hang Seng 21,830.02 +38.34 +0.18%

Shanghai Composite 3,652.24 +9.77 +0.27%

FTSE 6,074.87 +40.03 +0.66%

CAC 4,558.91 -6.26 -0.14%

DAX 10,474.75 -23.02 -0.22%

Crude oil $35.96 (+0.42%)

Gold $1075.20 (-0.50%)

-

14:59

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.32

1.28%

24.8K

Ford Motor Co.

F

13.89

1.17%

50.4K

Caterpillar Inc

CAT

66

1.16%

17.2K

Nike

NKE

131

0.92%

3.1K

ALCOA INC.

AA

9.39

0.75%

2.0K

McDonald's Corp

MCD

118.49

0.68%

0.2K

General Motors Company, NYSE

GM

34.06

0.68%

1.0K

Tesla Motors, Inc., NASDAQ

TSLA

234

0.62%

2.9K

Hewlett-Packard Co.

HPQ

11.5

0.61%

0.6K

Starbucks Corporation, NASDAQ

SBUX

59.87

0.55%

1.7K

Visa

V

77.55

0.49%

0.9K

UnitedHealth Group Inc

UNH

117.98

0.49%

0.7K

Twitter, Inc., NYSE

TWTR

22.24

0.45%

25.5K

International Business Machines Co...

IBM

135.97

0.35%

0.5K

Google Inc.

GOOG

750.3

0.34%

0.3K

Goldman Sachs

GS

178.29

0.30%

1.7K

AT&T Inc

T

34.19

0.29%

2.0K

Chevron Corp

CVX

89.5

0.29%

1.2K

Intel Corp

INTC

34.34

0.29%

1.4K

Exxon Mobil Corp

XOM

77.48

0.28%

1.7K

Facebook, Inc.

FB

105.05

0.27%

47.8K

JPMorgan Chase and Co

JPM

65.71

0.26%

6.6K

Wal-Mart Stores Inc

WMT

59.7

0.25%

0.2K

Cisco Systems Inc

CSCO

26.7

0.24%

14.8K

Microsoft Corp

MSFT

54.95

0.22%

4.2K

Verizon Communications Inc

VZ

46

0.22%

0.2K

Walt Disney Co

DIS

106.75

0.15%

1.4K

Citigroup Inc., NYSE

C

51.87

0.15%

2.7K

Yahoo! Inc., NASDAQ

YHOO

33.01

0.14%

2.1K

Pfizer Inc

PFE

32.5

0.12%

3.0K

General Electric Co

GE

30.41

0.03%

9.6K

FedEx Corporation, NYSE

FDX

145.8

0.03%

0.6K

Amazon.com Inc., NASDAQ

AMZN

664.62

0.02%

3.4K

Apple Inc.

AAPL

106.95

-0.35%

96.0K

The Coca-Cola Co

KO

42.6

-0.42%

3.6K

Barrick Gold Corporation, NYSE

ABX

7.41

-0.80%

34.1K

-

14:55

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Apple (AAPL) target lowered to $130 from $135 at Cowen

American Express (AXP) initiated with a Market Perform at JMP Securities

-

07:04

Global Stocks: U.S. stock indices gained

U.S. stock indices rose by the end of Monday session despite declines in European equities and persistent low oil prices. Trading volumes are likely to be relatively low this week.

The Dow Jones Industrial Average rose 122.87 points, or 0.7%, to 17,251.42. The S&P 500 gained 15.60 points, or 0.8%, to 2,021.15. The Nasdaq Composite gained 45.84 points, or 0.9% to 4,968.92.

Data showed that the Chicago Fed National Activity Index declined to -0.30 in November from -0.17 in October marking the fourth negative reading in a row. Analysts had expected the index to climb to +0.10. A reading below 0 suggests that the economy's growth pace was below average.

This morning in Asia Hong Kong Hang Seng edged down 0.04%, or 8.73, to 21,782.95. China Shanghai Composite Index fell by 0.35%, or 12.86, to 3.629.62. The Nikkei climbed 0.09%, or 16.25, to 18,932.27.

Asian indices traded mixed. Japanese stocks were supported by gains in U.S. stocks.

Chinese stocks traded range-bound after the country's government signaled it may stimulate the economy further.

-

03:03

Nikkei 225 18,867.88 -48.14 -0.25%, Hang Seng 21,781.49 -10.19 -0.05%, Shanghai Composite 3,646.09 +3.62 +0.10%

-

00:30

Stocks. Daily history for Sep Dec 21’2015:

(index / closing price / change items /% change)

S&P/ASX 200 5,109.05 +2.39 +0.05%

TOPIX 1,531.28 -5.82 -0.38%

SHANGHAI COMP 3,642.63 +63.67 +1.78%

HANG SENG 21,791.68 +36.12 +0.17%

FTSE 100 6,034.84 -17.58 -0.29%

CAC 40 4,565.17 -60.09 -1.30%

Xetra DAX 10,497.77 -110.42 -1.04%

S&P 500 2,021.15 +15.60 +0.78%

NASDAQ Composite 4,968.92 +45.84 +0.93%

Dow Jones 17,251.62 +123.07 +0.72%

-