Noticias del mercado

-

20:01

Dow -0.10% 17,484.34 -18.25 Nasdaq -0.10% 4,764.11 -4.75 S&P -0.23% 2,032.05 -4.66

-

18:24

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes lower on Thursday ahead of the long Easter weekend, as Wells Fargo led declines in financial stocks and gains in the dollar hurt commodities. Wells Fargo's (WFC) 2,2% drop was the biggest drag on the S&P 500. UBS started coverage of the bank's stock with a "sell" rating, citing cloudy revenue outlook and credit risks that extend beyond its energy portfolio.

Most of Dow stocks in negative area (20 of 30). Top looser - UnitedHealth Group Incorporated (UNH, -1,83%). Top gainer - Caterpillar Inc. (CAT, +1,33%).

Almost of all S&P sectors in negative area. Top looser - Financial (-1,3%). Top gainer - Utilities (+0,1%).

At the moment:

Dow 17339.00 -87.00 -0.50%

S&P 500 2019.25 -9.50 -0.47%

Nasdaq 100 4381.50 -14.00 -0.32%

Oil 39.46 -0.33 -0.83%

Gold 1221.10 -2.90 -0.24%

U.S. 10yr 1.90 +0.02

-

18:01

European stocks closed: FTSE 100 6,106.48 -92.63 -1.49% CAC 40 4,329.68 -94.30 -2.13% DAX 9,851.35 -171.58 -1.71%

-

17:58

WSE: Session Results

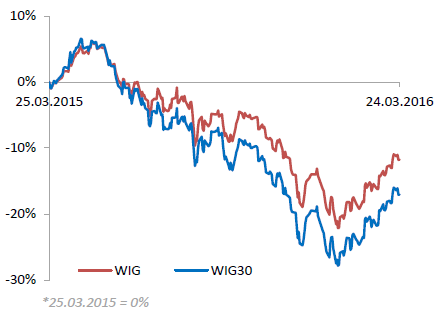

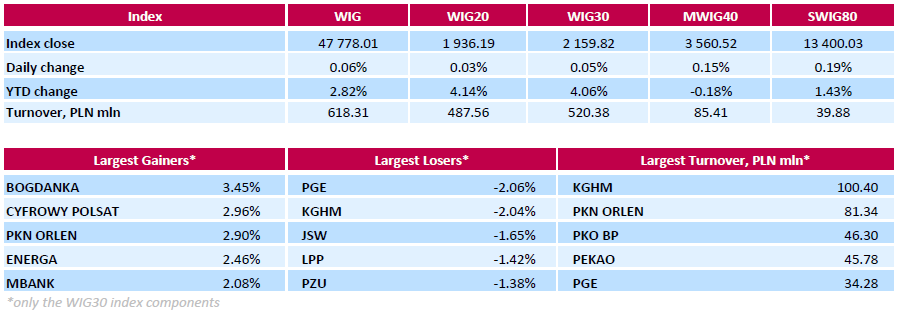

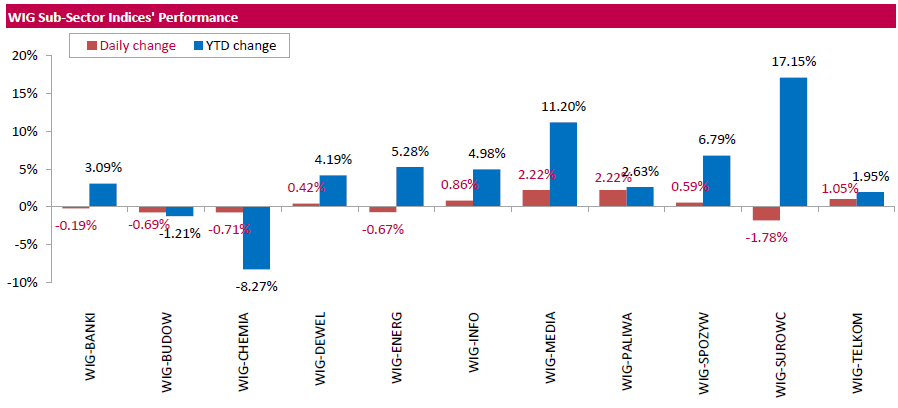

Polish equity market closed flat on Thursday. The broad market measure, the WIG Index, edged up 0.06%. Sector performance within the WIG Index was mixed. Media (+2.22%) and oil and gas (+2.22%) sectors outperformed, while materials (-1.78%) lagged behind.

The large-cap WIG30 Index inched up 0.05%. Within the index components, thermal coal miner BOGDANKA (WSE: LWB) led the gainers with a 3.45% advance, followed by media group CYFROWY POLSAT (WSE: CPS) and oil refiner PKN ORLEN (WSE: PKN), growing by 2.96% and 2.9% respectively. At the same time, the session's most prominent losers were genco PGE (WSE: PGE) and copper producer KGHM (WSE: KGH), which quotations fell by 2.06% and 2.04% respectively.

The Warsaw Stock Exchange will be closed on Friday, Mar.25, and Monday, Mar. 28, due to Easter celebrations.

-

14:41

WSE: After start on Wall Street

This afternoon we met readings from the US economy.

Data from the US should not be a special surprise, as the labor market still shows up on the good side and the industrial sector on worse. Thus, the number of weekly applications for unemployment benefits falls very low (Initial Jobless Claims, March 265k - forecast 268k)

Weaker than expected fall orders for goods without means of transport (Durable Goods Orders ex Transportation, February -1.0% - forecast -0.2%), which means that the publication could be judge rather negatively. Strong labor market means that interest rates may be raised, and the low orders creates pressure on corporate earnings and GDP growth.

U.S. Stocks open: Dow -0.53%, Nasdaq -0.67%, S&P -0.63%

-

14:35

U.S. Stocks open: Dow -0.53%, Nasdaq -0.67%, S&P -0.63%

-

14:30

Before the bell: S&P futures -0.69%, NASDAQ futures -0.56%

U.S. stock-index fell.

Global Stocks:

Nikkei 16,892.33 -108.65 -0.64%

Hang Seng 20,345.61 -269.62 -1.31%

Shanghai Composite 2,961.12 -48.85 -1.62%

FTSE 6,098.47 -100.64 -1.62%

CAC 4,332.1 -91.88 -2.08%

DAX 9,878.15 -144.78 -1.44%

Crude oil $38.74 (-2.64%)

Gold $1223.00 (-0.08%)

-

13:59

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.19

-0.13(-1.3949%)

50430

ALTRIA GROUP INC.

MO

60.5

-0.91(-1.4818%)

9348

Amazon.com Inc., NASDAQ

AMZN

566.61

-3.02(-0.5302%)

18586

Apple Inc.

AAPL

105.67

-0.46(-0.4334%)

43303

AT&T Inc

T

38.4

-0.14(-0.3633%)

1744

Barrick Gold Corporation, NYSE

ABX

13.52

0.25(1.884%)

70681

Chevron Corp

CVX

92.48

-1.11(-1.186%)

4985

Cisco Systems Inc

CSCO

27.62

-0.21(-0.7546%)

1749

Citigroup Inc., NYSE

C

42.08

-0.29(-0.6844%)

33528

Exxon Mobil Corp

XOM

83

-0.75(-0.8955%)

24786

Facebook, Inc.

FB

112.1

-0.44(-0.391%)

85831

Ford Motor Co.

F

13.16

-0.10(-0.7541%)

20621

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

9.41

-0.34(-3.4872%)

182114

General Electric Co

GE

30.92

-0.15(-0.4828%)

31699

General Motors Company, NYSE

GM

31

-0.31(-0.9901%)

36923

Goldman Sachs

GS

152.98

-1.10(-0.7139%)

2190

Google Inc.

GOOG

733.45

-4.61(-0.6246%)

2186

Hewlett-Packard Co.

HPQ

12.03

0.01(0.0832%)

155

Home Depot Inc

HD

130

-0.22(-0.1689%)

1090

Intel Corp

INTC

31.82

-0.18(-0.5625%)

11261

International Business Machines Co...

IBM

144.5

-0.90(-0.619%)

7087

Johnson & Johnson

JNJ

107.94

-0.56(-0.5161%)

100

JPMorgan Chase and Co

JPM

59.5

-0.44(-0.7341%)

11035

McDonald's Corp

MCD

124.06

-0.13(-0.1047%)

1000

Microsoft Corp

MSFT

53.52

-0.45(-0.8338%)

2240

Nike

NKE

62.06

-0.38(-0.6086%)

18668

Procter & Gamble Co

PG

82.52

-0.30(-0.3622%)

600

Starbucks Corporation, NASDAQ

SBUX

58.75

-0.08(-0.136%)

712

Tesla Motors, Inc., NASDAQ

TSLA

217

-5.58(-2.507%)

79222

The Coca-Cola Co

KO

45.37

-0.09(-0.198%)

2076

Twitter, Inc., NYSE

TWTR

15.92

-0.09(-0.5621%)

40143

Verizon Communications Inc

VZ

52.75

-0.16(-0.3024%)

3491

Visa

V

73.58

-0.33(-0.4465%)

1019

Walt Disney Co

DIS

96.5

-0.33(-0.3408%)

1756

Yahoo! Inc., NASDAQ

YHOO

34.84

0.04(0.1149%)

101479

-

13:56

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Hewlett Packard Enterprise (HPE) target raised to $18 from $15 at RBC Capital Mkts

-

12:36

WSE: Mid session comment

After the morning decline market came into stabilization, despite the fact that Europe's indexes descend to new session lows. Thus we distinguish a certain advantage, perhaps related also to the fact that yesterday the roles were different and locally Warsaw some profit taking has already experienced. Entering the southern phase of trading activity slowed, as indeed is also consistent with the mute of volatility. Also on the broad market it is calmer but in the third line (the WIG80 index) some single companies, like Asbis SA (WSE: ASB) behave much better today.

-

12:11

CBI retail sales balance declines to +7% in March

The Confederation of British Industry (CBI) released its retail sales balance data on Thursday. The CBI retail sales balance declined to +7% in March from +10% in February, missing expectations for a rise to +15%.

Sales are expected to rise next month, while orders are expected to be flat.

"Retailers are still face challenging global conditions but will welcome the Chancellor's Budget reforms to business rates, making it easier for them to operate on the high street. Continued low levels of inflation and more jobs will continue to boost household spending, also giving a helping hand to firms," CBI Director of Economics, Rain Newton-Smith, said.

-

12:00

European stock markets mid session: stocks traded lower on lower oil prices

Stock indices traded lower on a decline in oil prices. Oil prices fell on the U.S. crude oil inventories data, which the higher than expected by analysts.

Market participants also eyed the economic data from the Eurozone. Market research group GfK released its consumer confidence index for Germany on Thursday. German Gfk consumer confidence index fell to 9.4 in April from 9.5 in March. Analysts had expected the index to remain unchanged at 9.5.

The economic expectations index declined by 2.9 points to 0.5 points in March, while the willingness to buy index fell by 2.7 points to 50.0.

The income expectations index dropped by 6.2 points to 50.5 in March.

"The weak demand for German products in certain important markets will probably not leave economic growth in Germany unaffected. A signal of this is the decline in economic expectations this month," Gfk noted.

The French statistical office Insee released its manufacturing confidence index for France on Thursday. The French manufacturing confidence index declined to 101 in March from 103 in February.

The Office for National Statistics released its retail sales data for the U.K. on Thursday. Retail sales in the U.K. fell 0.4% in February, beating expectations for a 0.7% drop, after a 2.3% rise in January.

The decline was driven by a weak demand for clothing. Clothing and footwear sales fell 0.4% in February.

Food store sales were down 0.3% in February, while non-food store sales decreased 0.1%.

On a yearly basis, retail sales in the U.K. climbed 3.8% in February, in line with forecasts, after a 5.4% rise in January. January's figure was revised up from a 5.2% gain.

The British Bankers' Association (BBA) released the number of mortgage approvals in the U.K. on Thursday. The number of mortgage approvals declined to 45,982 in February from 46,900 in January. January's figure was revised down from 47,509.

"Mortgage borrowing remained buoyant in February. It appears that borrowers are continuing to try to get ahead of the increases in stamp duty for buy-to-let and second home buyers scheduled to come into effect next month," the chief economist at the BBA, Richard Woolhouse, said.

Current figures:

Name Price Change Change %

FTSE 100 6,114.18 -84.93 -1.37 %

DAX 9,877.28 -145.65 -1.45 %

CAC 40 4,340.65 -83.33 -1.88 %

-

11:50

European Central Bank’s monthly economic bulletin: the Eurozone’s economy continues to recover

The European Central Bank (ECB) released its monthly economic bulletin on Thursday. The central bank said that the Eurozone's economy continued to recover, but the growth was weaker than previously estimated. The ECB expects the economy to continue to recover moderately, supported the central bank's stimulus measures and a rise in employment. There are downside risks to the outlook from the slowdown in emerging countries, volatile financial markets, the balance sheet adjustments and the sluggish pace of implementation of structural reforms.

-

11:42

Japanese Prime Minister Shinzo Abe: the Bank of Japan’s monetary policy does not target to directly weaken the yen

Japanese Prime Minister Shinzo Abe said before the parliament on Thursday that the Bank of Japan's monetary policy did not target to directly weaken the yen. But a weaker yen was likely a result of the central bank's monetary policy actions, he noted.

-

11:36

Italian retail sales are flat in January

The Italian statistical office Istat released its retail sales data for Italy on Thursday. Italian retail sales were flat in January, after a 0.1% decrease in December.

Sales of food products were flat in January, while sales of non-food products increased by 0.1%.

On a yearly basis, retail sales in Italy declined 0.8% in January, after a 0.7% gain in December. December's figure was revised up from a 0.6% rise.

-

11:32

Industrial orders in Italy rise at a seasonally adjusted rate of 0.7% in January

The Italian statistical office Istat released its industrial orders data for Italy on Thursday. Industrial orders in Italy rose at a seasonally adjusted rate of 0.7% in January, after a 2.8% drop in December.

Domestic orders were up 0.6% in Japan, while non-domestic orders rose 0.8%.

On a yearly basis, the unadjusted industrial orders in Italy increased 0.1% in January, after a 1.5% rise in December.

The seasonally adjusted industrial turnover in Italy climbed 1.0% in January, after a 1.6% decrease in December.

Domestic turnover increased 1.2% in January, while non-domestic turnover rose 0.4%.

On a yearly basis, the adjusted industrial turnover in Italy declined 0.3% in January, after a 3.0% decrease in December.

-

11:09

French manufacturing confidence index declines to 101 in March

The French statistical office Insee released its manufacturing confidence index for France on Thursday. The French manufacturing confidence index declined to 101 in March from 103 in February.

Past change in production index was down to -6 in March from -3 in February.

Personal production expectations index fell to 14 in March from 19 in February, while general production outlook index rose to -1 from -4.

-

11:01

UK retail sales fall 0.4% in February

The Office for National Statistics released its retail sales data for the U.K. on Thursday. Retail sales in the U.K. fell 0.4% in February, beating expectations for a 0.7% drop, after a 2.3% rise in January.

The decline was driven by a weak demand for clothing. Clothing and footwear sales fell 0.4% in February.

Food store sales were down 0.3% in February, while non-food store sales decreased 0.1%.

On a yearly basis, retail sales in the U.K. climbed 3.8% in February, in line with forecasts, after a 5.4% rise in January. January's figure was revised up from a 5.2% gain.

-

10:49

Number of mortgage approvals in the U.K. declines to 45,982 in February

The British Bankers' Association (BBA) released the number of mortgage approvals in the U.K. on Thursday. The number of mortgage approvals declined to 45,982 in February from 46,900 in January. January's figure was revised down from 47,509.

"Mortgage borrowing remained buoyant in February. It appears that borrowers are continuing to try to get ahead of the increases in stamp duty for buy-to-let and second home buyers scheduled to come into effect next month," the chief economist at the BBA, Richard Woolhouse, said.

He added that consumer confidence was robust.

-

10:28

WSE: Puławy SA to offer PLN 10.5 dividend per share from 2015 profits

Listed chemicals firm Puławy SA (WSE: ZAP), a unit of Azoty group, will offer its shareholders a dividend payment of PLN 200.7 mln or PLN 10.5 per share.

The payment constitutes 42.9% of the 2015 profit of PLN 468.2 mln.

-

10:17

German construction orders increase 1.0% in January

Destatis released its construction orders data on Thursday. German construction orders rose by a seasonally and working-day-adjusted rate of 1.0% in January.

On an annual basis, German construction orders climbed by a seasonally adjusted rate of 12.6% in January.

Turnover of companies with 20 or more persons fell 1.5% year-on-year in January.

-

10:11

German import prices decline 0.6% in January

Destatis released its import prices data for Germany on Thursday. German import prices declined by 5.7% in February from last year, after a 3.8% fall in January. It was the biggest drop since October 2009.

The decline was driven by a drop in energy prices, which plunged 34.1% year-on-year in February.

Import prices decline since January 2013.

On a monthly base, import prices decreased 0.6% in February, after a 1.5% fall in January.

On a yearly base, import prices excluding crude oil and mineral oil products fell by 2.8% in February.

Export prices dropped 1.2% year-on-year in February, after a 0.5% decrease in January.

On a monthly base, export prices were down 0.5% in February, after a 0.2% fall in January.

-

10:06

German Gfk consumer confidence index falls to 9.4 in April

Market research group GfK released its consumer confidence index for Germany on Thursday. German Gfk consumer confidence index fell to 9.4 in April from 9.5 in March. Analysts had expected the index to remain unchanged at 9.5.

The economic expectations index declined by 2.9 points to 0.5 points in March, while the willingness to buy index fell by 2.7 points to 50.0.

The income expectations index dropped by 6.2 points to 50.5 in March.

"The weak demand for German products in certain important markets will probably not leave economic growth in Germany unaffected. A signal of this is the decline in economic expectations this month," Gfk noted.

-

09:59

German cabinet approves fiscal plans for 2017

The German cabinet approved fiscal plans for 2017 on Wednesday. Fiscal plans include higher spending on migrants, security and infrastructure without new debt.

"We are investing in infrastructure, education and research, we are doing what is needed to guarantee domestic and external security and we are helping migrants - all without new borrowing," German Finance Minister Wolfgang Schaeuble said.

Germany plans to spend on migrants €10 billion in 2017. The government's spending is expected to rise by €30.9 billion to €347.8 billion by 2020.

-

09:47

New Zealand’s trade surplus widens to NZ$339 million in February

Statistics New Zealand released its trade data on late Wednesday evening. New Zealand's trade surplus widened to NZ$339 million in February from NZ$13 million in January. January's figure was revised up from a surplus of NZ$8 million.

Analysts had expected the surplus to rise to NZ$50 million.

Exports climbed 9.3% year-on-year in February, mainly driven by fish, crustaceans, and molluscs, and wine, while imports increased by 2.8%, mainly driven by a rise in pharmaceuticals, toys, and sporting equipment.

"Export results were mixed in February 2016, with many commodities rising in value. But falls for some of our main commodities, including beef, lamb, and milk powder, meant that the rise was limited," Statistics NZ international statistics senior manager Stuart Jones said.

-

09:13

WSE: After opening

The WIG20 futures (WSE: FW20M16) started the day on a slight increase by 0.1% to 1,924 points. In Germany, a contract for DAX-a very cosmetically lose its value. In general, the beginning of quotations should be regarded as neutral after yesterday's declines. Nearby is a psychological support level of 1,900 points., which achieve at this point seems more likely than growth towards 2000 points.

WIG20 index opened at 1933.12 points (-0.13%)*

Other major Indices open change:

WIG 47656.19 -0.19%

WIG30 2151.84 -0.32%

mWIG40 3562.72 0.22%

*/ - change to previous close

Declines at the opening of the German DAX reach 0.8%. Moods are still so corrective. Today, in the first few bars, volatility of large companies it is not so big, and character of trade reminds of upcoming holidays.

-

08:24

WSE: Before opening

Today's session will be the last before starting tomorrow the Easter break (on 25 and 28 of March there is no sessions on the Warsaw Stock Exchange). The activity of the trade should not be large, as well as volatility. We have to remembered that the Americans are back on the market as early as Monday. This can affect supply, as investors will not want to be on shares during the holiday. Also important are the global trends.

More and more members of the FOMC starts to mention of the impending rate hike, indicating April as a possible date.

Yesterday the dollar strengthened and there have been declines in raw materials as well as emerging markets, including the WSE.

The mood in the morning is slightly offset, yesterday's session in the US ended with a decline of 0.6%, and the contracts go down by a further 0.3%. Asia is dominated by the red color and raw material prices remain at yesterday's minima. All this affects the mood, and for further growth, as well as crossing the psychological barrier of 2,000 points in case of the WIG20 will not be so easy.

-

06:23

Global Stocks: shares slipped after the U.S. dollar strengthened

European stocks erased earlier gains and closed in negative territory for a third straight day on Wednesday as a selloff in oil and metals pushed commodity companies lower.

U.S. stocks ended lower Wednesday as crude futures suffered their worst percentage decline in a month, which hammered energy and materials shares and dragged down the main stock indexes.

Asian shares slipped Thursday after the U.S. dollar strengthened against regional currencies. The dollar gained overnight against a basket of major currencies after St. Louis Federal Reserve Bank President James Bullard suggested there was a chance that interest rates could be raised in April.

Based on MarketWatch materials

-

03:03

Nikkei 225 16,946.03 -54.95 -0.32 %, Hang Seng 20,439.24 -175.99 -0.85 %, Shanghai Composite 2,977.87 -32.09 -1.07 %

-

00:29

Stocks. Daily history for Sep Mar 23’2016:

(index / closing price / change items /% change)

Nikkei 225 17,000.98 -47.57 -0.28 %

Hang Seng 20,615.23 -51.52 -0.25 %

Shanghai Composite 3,010.79 +11.43 +0.38 %

FTSE 100 6,199.11 +6.37 +0.10 %

CAC 40 4,423.98 -7.99 -0.18 %

Xetra DAX 10,022.93 +32.93 +0.33 %

S&P 500 2,036.71 -13.09 -0.64 %

NASDAQ Composite 4,768.86 -52.80 -1.10 %

Dow Jones 17,502.59 -79.98 -0.45 %

-