Notícias do Mercado

-

23:54

USD/CHF Price Analysis: Fortnight-old resistance line, Doji prod bulls near 0.8950

- USD/CHF fades week-start recovery near short-term key resistance line, stays sidelined of late.

- Bearish candlestick formation, sluggish RSI also signal pullback moves.

- Convergence of 50-SMA, one-week-old ascending trend line restrict short-term downside.

- Bulls have a bumpy road to ride unless crossing 200-SMA.

USD/CHF seesaws around 0.8950-60 following a failure to cross a two-week-old resistance line during early Tuesday. In doing so, the Swiss Franc (CHF) pair justifies the previous day’s Doji candlestick while positing mild losses near the stated price after an upward start to the week.

With this, the USD/CHF price is likely to decline towards the 0.8925-20 support confluence comprising the 50-SMA and a one-week-old ascending support line.

In a case where the USD/CHF bears keep the reins past 0.8920, the 0.8900 round figure and the previous monthly low, also the yearly low around 0.8850, will be in the spotlight.

It’s worth noting that the pair’s weakness past 0.8850 will make it vulnerable to dropping toward the year 2021 low of around 0.8755.

On the flip side, the aforementioned resistance line, near 0.8965 by the press time, precedes the late April swing high of around 0.8975 to restrict the immediate USD/CHF upside.

Following that, a one-month-old downward-sloping resistance line and the 200-SMA, respectively near 0.9015 and 0.9060, will be in the spotlight.

Overall, USD/CHF remains depressed but the bears are likely running out of steam, which in turn highlights the 0.8925-20 support confluence.

USD/CHF: Four-hour chart

Trend: Further downside expected

-

23:41

Gold Price Forecast: XAU/USD finds a cushion around $1,980, downside seems favored ahead of Fed policy

- Gold price is defending its downside around $1,980.00, downside bias is deepening ahead of Fed policy.

- US labor market conditions are expected to lose further as Morgan Stanley has announced 3K more job cuts.

- Gold price is consolidating in a Symmetrical Triangle in which volatility contracts ahead of a critical event.

Gold price (XAU/USD) is continuously defending downside around the crucial support of $1,980.00 for the past few weeks. The precious metal is prone to downside as the appeal for the US Dollar Index (DXY) is improving ahead of the interest rate decision by the Federal Reserve (Fed).

A consecutive 25 basis point (bp) interest rate hike is expected from Fed chair Jerome Powell to continue to weigh pressure on United States inflation. One more 25bp rate hike from the Fed is widely expected, however, the event that is infusing anxiety among the market participants is the interest rate guidance.

Considering recent events of declining growth rate as US Gross Domestic Product (GDP) slowed to 1.1% on a quarterly basis due to lower inventories, ISM Manufacturing PMI landed below 50.0 straight for the sixth month and a downward revision to Retail Sales indicate that the Fed would sound neutral on guidance.

Apart from that, US labor market conditions are expected to lose further as Morgan Stanley has announced a planned lay-off of 3K more jobs as deals have slumped as reported by Bloomberg.

Meanwhile, S&P500 settled Monday’s session with some losses as investors are turning cautious ahead of the interest rate policy by the Fed. The USD Index is gathering strength for breaking above the immediate resistance of 102.20.

Gold technical analysis

Gold price is consolidating in a Symmetrical Triangle chart pattern on a four-hour scale in which volatility contracts significantly ahead of a critical event. The upward-sloping trendline of the aforementioned pattern is plotted from April 19 low at $1,969.26 while the downward-sloping trendline is placed from April 17 high at $2,015.23.

The 20-period Exponential Moving Average (EMA) at $1,987.20 seems sticky to the Gold price, indicating a rangebound auction.

Also, the Relative Strength Index (RSI) (14) is hovering in the 40.00-60.00 range, which hints at a sheer consolidation.

Gold four-hour chart

-

23:23

US House Speaker McCarthy: The senate and the president need to get to work — and soon

US House of Representatives Speaker Kevin McCarthy crossed wires, via Reuters, early Tuesday as he said, “House republicans did their job and passed a responsible bill that raises the debt ceiling, avoids default, and tackles reckless spending.”

-

23:19

RBNZ: Not currently seeing widespread financial distress among households or businesses

“Not currently seeing widespread financial distress amongst households or businesses, which reflects the strength in the economy,” said the Reserve Bank of New Zealand (RBNZ) in its Financial Stability Report (FSR) released early Tuesday per Reuters.

Additional statements

More borrowers may fall behind on their payments this year, given the ongoing repricing of mortgages and weakening in the labor market.

Household balance sheets remain resilient in the aggregate, with most households with a mortgage still having substantial equity buffers.

Market implication

With these statements, New Zealand’s central bank repeated the previous day’s announcements and hence the RBNZ failed to impress NZD/USD traders, grinding lower around 0.6170 by the press time.

Also read: NZD/USD pressured in a firmer US Dollar environment

-

23:13

AUD/USD eases towards 0.6600 with eyes on RBA Interest Rate Decision

- AUD/USD fails to extend week-start gains, remains pressured of late.

- First Republic Bank linked improvement in market sentiment, mixed Aussie PMI allowed buyers to prepare for RBA.

- US Dollar remains firmer despite unimpressive data, cheers upbeat yields, immediate solution to banking fallout.

- RBA is expected to keep the benchmark rates unchanged, future guidance is the key.

AUD/USD remains pressured near 0.6630-25 during the early hours of Tuesday’s Asian session, after paring the daily gains amid late Monday. In doing so, the Aussie pair portrays the trader’s anxiety ahead of the Reserve Bank of Australia’s (RBA) monetary policy decision.

The Aussie pair began the week on a firmer footing despite mixed data at home and in China. However, hopes of overcoming immediate challenges to the market sentiment from the First Republic Bank (FRB), which was finally dealt with, helped the risk barometer pair to remain firmer.

On Sunday, China’s official NBS Manufacturing PMI disappointed markets with 49.2 figures for April, versus 51.4 market forecasts and 51.9 prior readings. It’s worth noting that the Non-Manufacturing PMI rose past 50.4 expected figures to 56.4 but remained below 58.4 reported in March. With the downbeat numbers from Australia’s biggest customer, as well as the banking fears, the AUD/USD pair remains pressured of late.

At home, Australia’s S&P Global Manufacturing PMI for April eased to 48.1 versus 48.0 prior while TD Securities Inflation eased to 0.2% on MoM for the said month from 0.3% but improved to 6.1% YoY from 5.7% previous.

Elsewhere, the US regulators seized assets of the FRB and sold them to the new buyer, namely JP Morgan. “JPMorgan will pay $10.6 billion to the U.S. Federal Deposit Insurance Corp (FDIC) as part of the deal to take control of most of the San Francisco-based bank's assets and get access to First Republic's coveted wealthy client base,” said Reuters.

On the other hand, US ISM Manufacturing PMI improved to 47.1 for April versus 46.3 prior and 46.6 market forecasts while the S&P Global Manufacturing PMI for the said month eased to 50.2 versus 50.4 first estimations.

It should be noted that Friday’s upbeat US inflation clues via Core PCE Price Index joined the solution on First Republic Bank to underpin the market’s optimism. The same helped the Wall Street and AUD/USD prices. Further, the US Treasury bond yields also began the key week on a positive footing and allowed the US Dollar to extend the previous gains.

Looking forward, all eyes are on the Reserve Bank of Australia’s (RBA) Interest Rate Decision even as the market players expect no change in the benchmark interest rate or other monetary policy measures. The reason could be linked to the doubts over the Aussie central bank’s interest rate peak, which some in the market expected around 3.65%, versus the 3.60% level at the latest. Hence, the rate guidance and economic forecasts will be crucial to watch for AUD/USD traders in today’s RBA announcements.

Also read: Reserve Bank of Australia Preview: No change, nothing new for the Aussie

Technical analysis

A three-week-old descending resistance line, around 0.6655 by the press time, joins bearish MACD signals to restrict short-term AUD/USD upside.

-

23:08

AUD/JPY Price Analysis: Faces resistance around 91.00, with downside risks lingering

- AUD/JPY rallies for three straight days, though tests solid resistance at around 91.00.

- Three daily closes above the 200-day EMA would cement the AUD/JPY uptrend.

- Downside risks remain if AUD/JPY drops below 91.00, which could exacerbate a fall toward 90.00.

The AUD/JPY climbed above the 91.00 figure following the Bank of Japan’s (BoJ) decision last Friday to hold rates unchanged while maintaining its Yield Curve Control (YCC). Therefore, the AUD/JPY has gained since then 3.04%. As the Asian session begins, the AUD/JPY is trading at 91.14.

AUD/JPY Price Action

After clearing the latest cycle high achieved on April 20 at 90.78, the AUD/JPY extended its gains, breaking a downslope resistance trendline drawn from September 2022 highs of around 98.60. in addition, the 200-day Exponential Moving Average (EMA) at 90.75 was cleared, suggesting that the bearish bias is negated in the near term. To cement the bullish bias, the AUD/JPY must achieve three daily closes above the 200-day EMA. Once done, that could pave the way for further upside.

If AUD/JPY breaks above the January 9 daily high at 91.82, the 92.00 figure is up for grabs as buyers prepare to challenge the YTD high at 92.99.

However, if AUD/JPY tumbles below 91.00, a reversal toward the 200-day EMA at 90.75 is on the cards. If the May 1 low at 90.01 is compromised, a bearish engulfing candle pattern could form and, alongside the 200-day EMA, it could trigger a trend reversal that can challenge the YTD lows.

The next support would be the 50-day EMA at 89.71, immediately followed by the 20-day EMA at 89.64.

AUD/JPY Daily Chart

-

23:03

EUR/USD eyes more weakness below 1.0960 as focus shifts to Fed/ECB policy

- EUR/USD is expected to show further weakness if fails to keep the auction above 1.0960.

- S&P500 surrendered gains on settlement, portraying caution among market participants ahead of the Fed’s policy.

- US Manufacturing PMI continued to remain below the 50.0 threshold consecutively for the sixth time.

The EUR/USD pair is hovering near the eight-day-old support of 1.0960 in the early Asian session. The major currency pair is expected to display a sheer sell-off after breaking below the same. The downside bias for the shared currency pair looks solid as the US Dollar Index (DXY) is preparing for a fresh rally above 102.20 amid the monetary policy by the Federal Reserve (Fed), which will be announced on Wednesday.

S&P500 surrendered gains in the late New York session and ended Monday with some losses, portraying caution among market participants ahead of the Fed’s interest rate policy. Investors failed to capitalize on this despite easing United States banking jitters as JP Morgan buyout First Republic Bank from US regulators.

The USD Index has recaptured two-week-old resistance of 102.20 and is expected to remain in the driving seat as Fed policymakers are preparing for one more 25 basis points (bps) interest rate hike.

Meanwhile, the US ISM Manufacturing PMI (April) remained upbeat on Monday. The Manufacturing PMI continued to remain below the 50.0 threshold consecutively for the sixth month but rebounded from the annual lowest figure to 47.1. Also, New Orders Index improved to 45.7 from the consensus of 45.5.

On the Eurozone front, weak economic growth amid higher inflation is becoming a major problem for European Central Bank (ECB) policymakers. The shared continent has recorded a growth rate of 0.1% in the first quarter lower than the consensus of 0.2%.

This week, ECB President Christine Lagarde is set to raise interest rates further, however, uncertainty is building for the pace of rate hike to be opted by the central bank.

-

23:01

NZD/USD pressured in a firmer US Dollar environment

- NZD/USD bulls pressured back as US Dollar rises.

- US Dollar firms on JPMorgan Chase's takeover of First Republic Bank.

NZD/USD has been trading in a sideways fashion to start the week in choppy holiday conditions. The pair travelled between a low of 0.6161 and 0.6200.

The focus was on US and Chinese data and the calming of US regional bank jitters in the wake of the sale of First Republic Bank. JPMorgan Chase's takeover of First Republic Bank, ahead of Wednesday's policy decision by the US Federal Reserve. JPMorgan Chase has bought failed First Republic Bank's deposits and a "substantial amount of their assets and certain liabilities," JPMorgan Chase said in a press release Monday.

"Our government invited us and others to step up, and we did," JPMorgan Chase CEO Jamie Dimon said in a statement. "This acquisition modestly benefits our company overall, it is accretive to shareholders, it helps further advance our wealth strategy, and it is complementary to our existing franchise."

The US Dollar enjoyed the relief as well as ISM data surprised the upside and bond yields rose. Additionally, US construction spending increased more than expected in March. Weak economic data from China may have been a factor also with the manufacturing purchasing managers' index (PMI) declining to below contraction territory (50) with the data reading 49.2 from 51.9 in March for the world's second-biggest economy.

´´As we noted yesterday, this week is all about central banks globally and labour market data locally. And on that score, first cab off the rank is the RBA decision at 4.30pm NZT today,´´ analysts at ANZ Bank noted.

´´Almost nobody expects a hike, but many expect them in due course, and assuming we do see a pause, how the AUD (and by correlation, the NZD) react will depend on the RBA’s tone. NZ labour market data tomorrow may raise a few eyebrows for its strength, but it’s lagging data and FX markets may not give it the attention it deserves,´´ the analysts said.

Meanwhile, investors also await the Federal Reserve decision. ´´We expect a 25bp rate hike at next week's FOMC meeting and anticipate that post-meeting communication will: (i) emphasize that disinflation has been evolving slower than expected, leaving open the possibility of additional tightening, and (ii) acknowledge the more uncertain economic environment, especially with regard to credit conditions post SVB collapse,´´ analysts at TD Securities said.

-

22:21

EUR/JPY continues to rally on ECB and BoJ central bank divergence

- EUR/JPY extended its rally on central bank divergence between the ECB and the BoJ.

- BoJ’s decision to keep rates unchanged and maintain the YCC weighed on the JPY.

- Market participants estimate the ECB will raise rates by 25 or 50 bps.

The EUR/JPY remains rallying sharply to multi-year highs at 150.94, sponsored by central bank divergence, with the European Central Bank (ECB) expected to raise rates, while the Bank of Japan’s (BoJ) kept its policy unchanged. In addition, a risk-on impulse dented the appetite for safe-haven assets. At the time of writing, the EUR/JPY is trading at 150.93 after hitting a low of 150.02.

On Monday, a late risk-off impulse weighed on Wall Street as it registered minuscule losses. Last Friday, the BoJ’s decision to keep rates unchanged spurred a jump of more than 1.50%, or 240 pips, in the pair. However, the newest BoJ Governor, Kazuo Ueda, revealed that the central bank would conduct a review of its monetary policy.

Regarding its forward guidance, the BoJ removed to pledge to keep rates at “current or lower levels.” Uzeda’s added that if the central bank needs to shift policy, it will do it, regardless of finishing the review of the non-conventional use of monetary policy for 25 years.

On the ECB’s side, the ECB is expected to raise rates by 25 bps, though some ECB hawks are still pushing for a 50 bps increase. However, after Tuesday’s report of inflation in the EU, ECB policymakers would have a clearer view, alongside the release of S&P Global Manufacturing PMIs in the bloc.

TD Securities analysts estimate a 25 bps rate hike. They noted, “March lending data, and the ECB’s Q1 Bank Lending Survey, we expect the majority will opt for 25bps, with some clear hawkish dissents. Country-level inflation and growth data appear to have lessened the risk of a 50bps hike, but a material positive surprise in the BLS could still be enough to tip the decision. If the ECB hikes 25bps, the tone of the statement and press conference will likely be more important than the hike itself.”

EUR/JPY Technical Levels

-

22:17

WTI weighed by China woes and a firm US Dollar

- WTI is under pressure as US Dollar firms are on good news for the banking sector.

- China falls below contraction territory, weighing on oil.

West Texas Intermediate crude oil prices Monday lower and have traveled between a low of $74.58 and $76.65 so far.

The US Dollar index on Monday reached a to a 1-1/2 week high and has weighed on the price of commodities, including Oil while US data and Chinese data have been the focus to start the week. At the same time, the US Dollar has found a boost as investors digested news of JPMorgan Chase's takeover of First Republic Bank, ahead of Wednesday's policy decision by the US Federal Reserve.

JPMorgan Chase has bought failed First Republic Bank's deposits and a "substantial amount of their assets and certain liabilities," JPMorgan Chase said in a press release Monday.

"Our government invited us and others to step up, and we did," JPMorgan Chase CEO Jamie Dimon said in a statement. "This acquisition modestly benefits our company overall, it is accretive to shareholders, it helps further advance our wealth strategy, and it is complementary to our existing franchise."

In the Chinese economic news, the concerns have hit oil prices as China's April manufacturing and non-manufacturing activity slowed more than expected. The China Apr manufacturing PMI dropped -2.7 to a 4-month low of 49.2, weaker than expectations of 51.4. Also, the Apr non-manufacturing PMI fell -1.8 to 56.4, weaker than expectations of 57.0.

On the other side of the Pacific, the April ISM manufacturing index rose +0.8 to 46.1, stronger than expectations of 46.8. Also, Mar construction spending rose +0.3% MoM, stronger than expectations of +0.1% MoM and the largest increase in 4 months.

Specific to the industry, Reuters reported that last Wednesday's EIA report showed that (1) U.S. crude oil inventories as of April 21 were -0.5% below the seasonal 5-year average, (2) gasoline inventories were -7.2% below the seasonal 5-year average, and (3) distillate inventories were -12.4% below the 5-year seasonal average. U.S. crude oil production in the week ended April 21 fell -0.8% w/w to 12.2 million bpd, only 0.9 million bpd (-6.9%) below the Feb-2020 record-high of 13.1 million bpd.

Meanwhile, the Baker Hughes reported last Friday that active US oil rigs in the week ended April 28 were unchanged at 591 rigs, moderately below the 2-1/2 year high of 627 rigs posted on December 2. US active oil rigs have more than tripled from the 17-year low of 172 rigs seen in Aug 2020, signaling an increase in US crude oil production capacity.

Speculators have started to unwind their long exposure in WTI crude oil, while also adding short positions, analysts at TD Securities explained.

´´Despite the latest inventory statistics which continue to show robust product demand and dwindling inventories, crude markets were rocked by the reemergence of recessionary fears and bank liquidity concerns.´´

´´Prices have since collapsed, seeing the entirety of the OPEC+ driven rally reversed. But, as risk appetite stabilizes and fundamentals continue to look tighter in the second half of the year, CTAs could again turn buyers and offer support to crude oil markets in the coming weeks,´´ the analysts concluded.

-

20:53

Forex Today: US Dollar strengthens ahead of Fed

What you need to know on Tuesday, May 2:

Financial markets were quite volatile Monday, despite most major countries celebrating Labour Day, keeping local markets closed. The US Dollar edged higher against its rivals, initially extending Friday’s gains and later taking advantage of better-than-anticipated American data.

On Friday, month-end flows and position readjusting ahead of the multiple first-tier events this week pushed the Greenback higher. The rally continued at the beginning of the week but reverted during European hours, with thin volumes exacerbating the movements. It later resumed its advance following the release of US figures.

The United States (US) April ISM Manufacturing PMI improved more than anticipated, up to 47.1 from 46.3. Also, March Construction Spending rose by 0.3% MoM, better than the 0.1% decline expected by market players. Not so encouraging, the final estimate of the S&P Global Manufacturing PMI for the same month was downwardly revised from 50.4 to 50.2.

The US Dollar was also supported by rising US government bond yields. The 10-year Treasury note currently yields 360%, up 15 basis points (bps), while the 2-year note offers 4.13%, adding roughly 7 bps on Monday.

Meanwhile, central banks take center stage. The Bank of Japan (BoJ) announced its decision on Friday, and as widely anticipated, it left its interest rates unchanged in newly appointed Governor Kazuo Ueda’s first policy meeting. The central bank also kept the range for 10-year Japanese Government Bonds (JGB) unchanged at 50 basis points, around the 0% target.

The Reserve Bank of Australia (RBA) will be next, as it will announce its decision on Tuesday. The RBA is expected to pause rate hikes and maintain the cash rate at 3.50%. The United States (US) Federal Reserve (Fed) will be out on Wednesday, while the European Central Bank (ECB) will follow on Thursday.

Meanwhile, Wall Street advanced following news that JP Morgan bought most First Republic Bank assets, rescuing the troubled institution with blessings from the US regulator, the Federal Deposit Insurance Corporation (FDIC).

As for US data, the April ISM Manufacturing PMI improved more than anticipated, up to 47.1 from 46.3. Also, March Construction Spending rose by 0.3% MoM, better than the 0.1% decline expected by market players. Not so encouraging, the final estimate of the S&P Global Manufacturing PMI for the same month was downwardly revised from 50.4 to 50.2.

XAU/USD briefly traded above $2,000 but shed over $20 ahead of the close, opening the door for a bearish extension.

EUR/USD settled around 1.0960, maintaining the pressure at the lower end of its latest range and at risk of falling further. GBP/USD trades sub 1..2500, but the risk of another leg lower is limited.

The Japanese yen is the worst performer, as USD/JPY surged to the 137.50 region. Finally, commodity-linked currencies were the best performers against the US Dollar, finding support in the better tone of Wall Street.

Like this article? Help us with some feedback by answering this survey:

Rate this content -

20:52

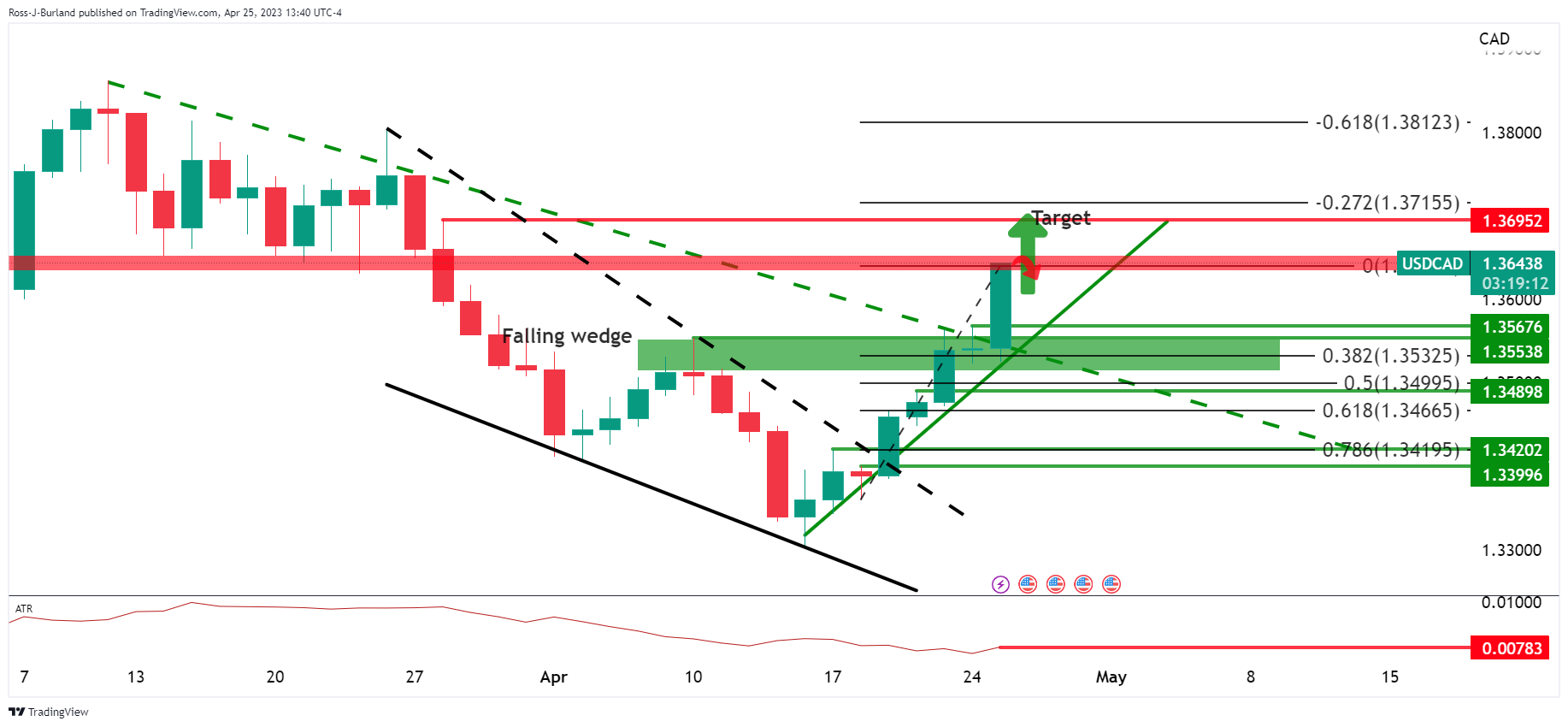

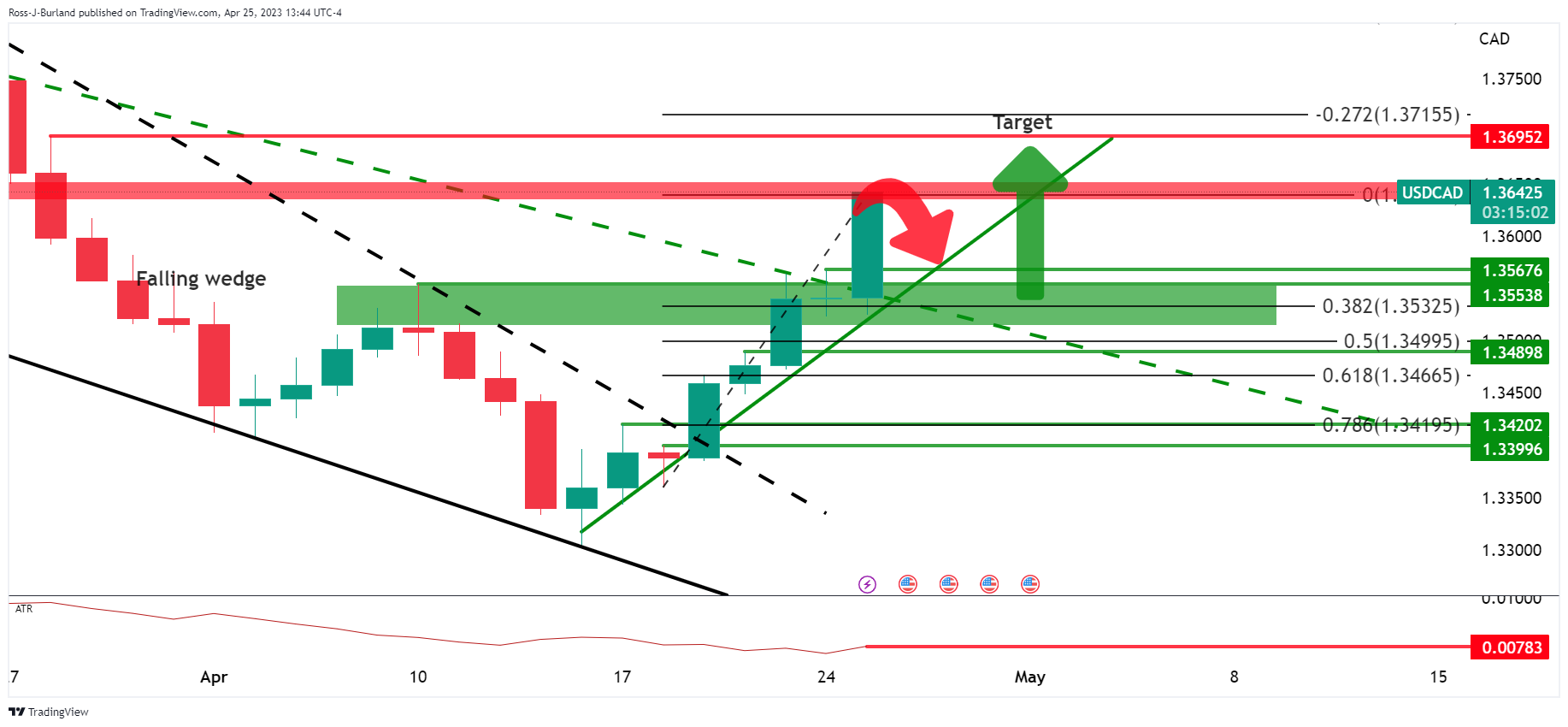

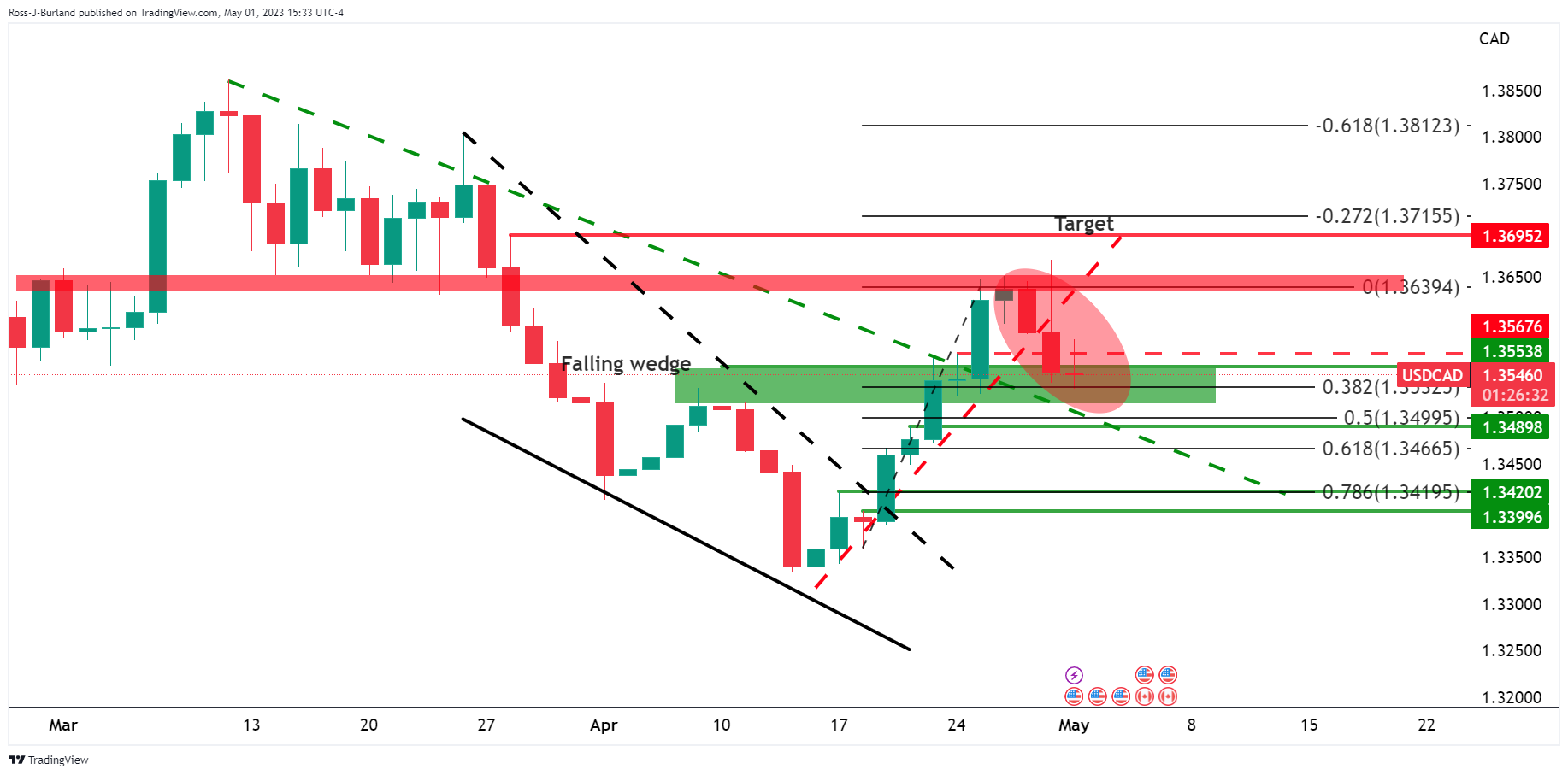

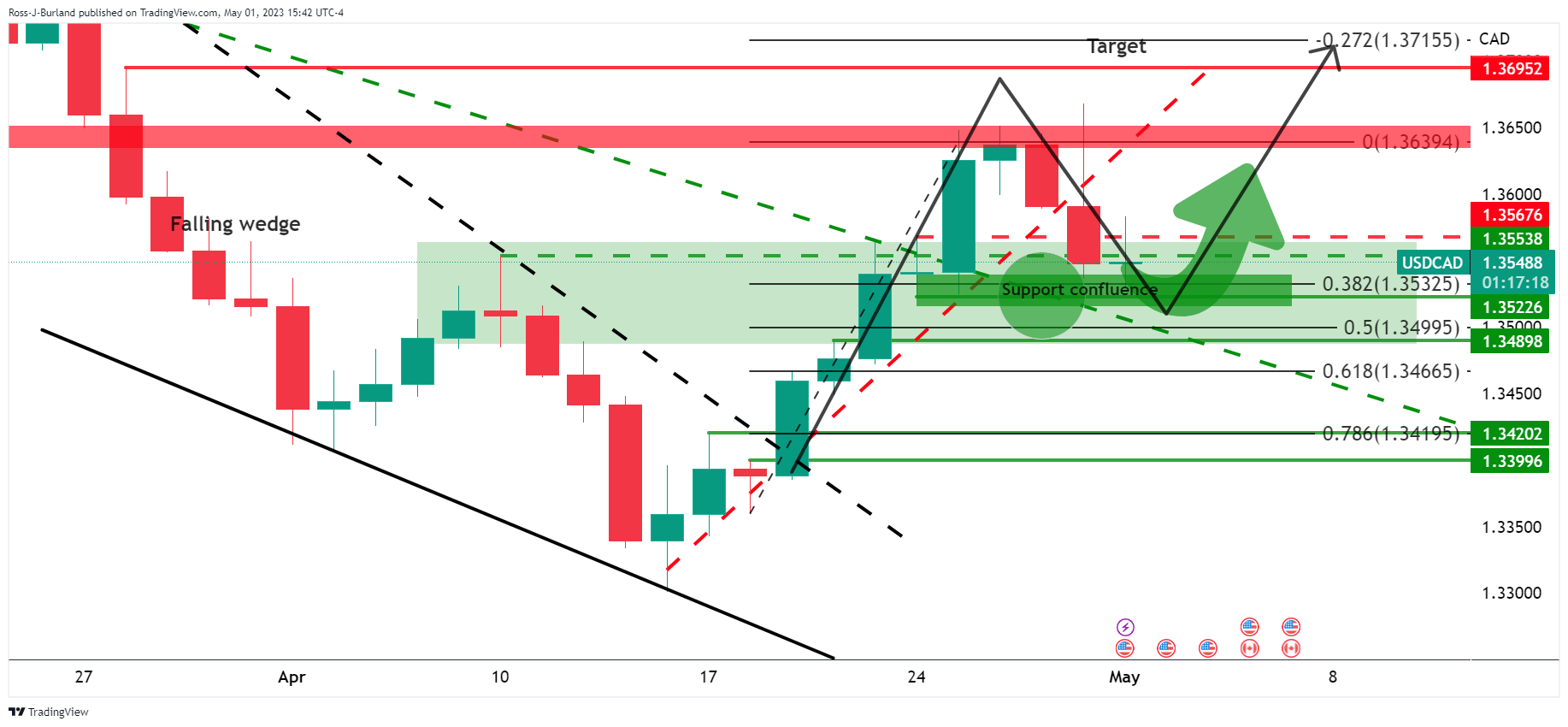

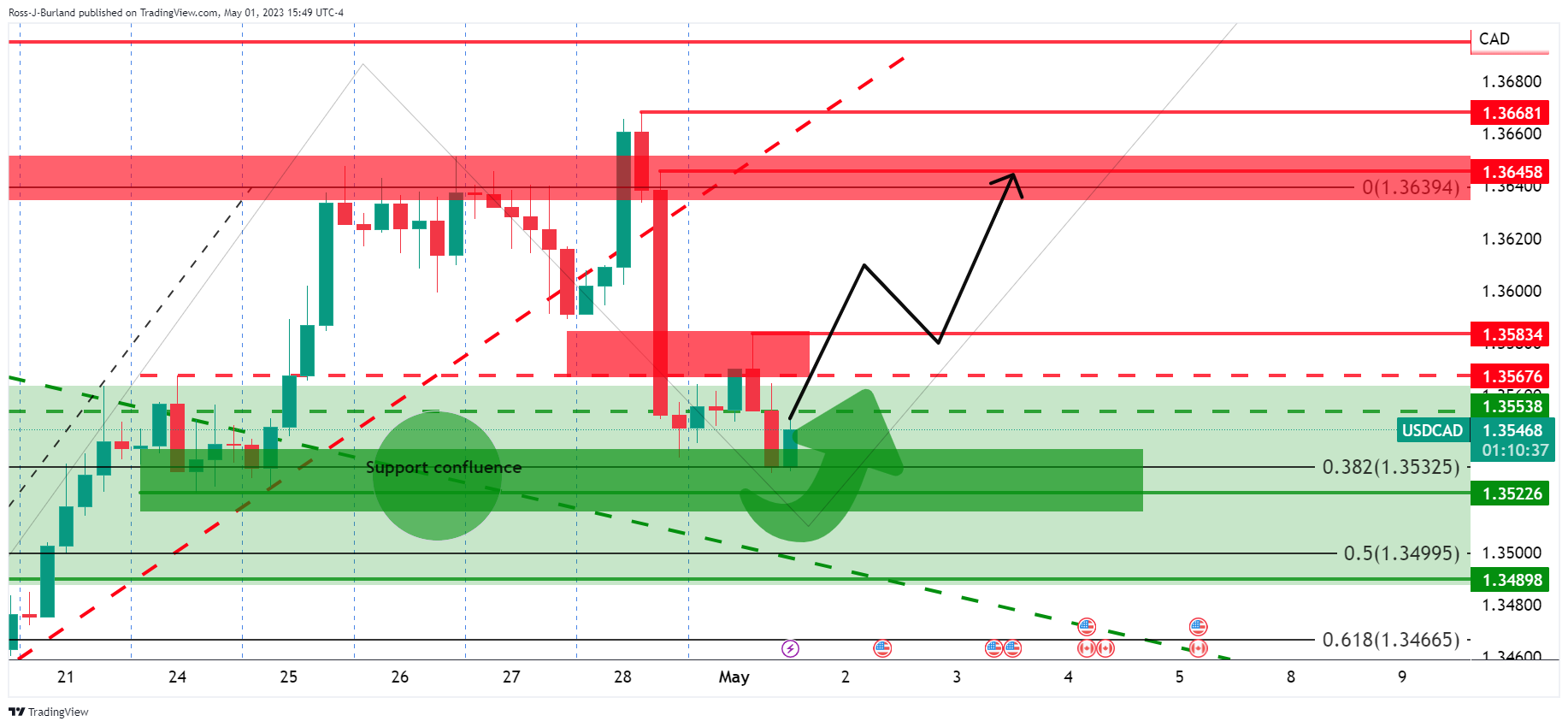

USD/CAD Price Analysis: Bulls are guarding critical support structures and eye 1.3700

- USD/CAD bulls could be on the verge of a rally through key 4-hour structure.

- Bulls eye a run to 1.3650 and then 1.3700.

As per the prior USD/CAD analysis, USD/CAD bulls eye a run towards 1.3700 as risk sentiment sours, bulls remain in the picture for a run towards 1.3700 in the near term so long as the following conditions are met:

- The bulls need to stay committed to the counter-trendline support.

- Bulls need to guard 1.3500.

- Bulls need to get above 4-hour 1.3580 structure and then 1.3650-70.

USD/CAD prior analysis

USD/CAD had broken old trendline resistance and was expected to act as a counter-trendline for the bulls to lean against should there be a meanwhile and significant correction.

The trendline support was eyed ahead of 1.3570, 1.3550 and then the 38.2% Fibonacci at 1.3532 ahead of a 50% mean reversion near 1.3500:

USD/CAD live updates

The correction has played out.

The bulls are starting to engage at the start of the week and the 1.3520s could be key in this regard where the counter trendlñinme support meets horizontal structures as illustrated above.

USD/CAD H4 chart

On the lower time frames, we can identify key levels as illustrated above. In this regard, the bulls really need to get above the 4-hour 1.3580 structure and then 1.3650-70.

-

19:52

AUD/USD remains resilient despite facing USD strength

- AUD/USD holds to its gains and remains above 0.6600 on overall risk sentiment.

- US manufacturing activity improved, though higher prices justify the need for further Fed tightening.

- Weaker than expected, China’s data capped the AUD/USD’s rally towards 0.6700.

The Australian Dollar (AUD) clings to some gains after hitting a daily high of 0.6668, though renewed US Dollar (USD) strength spurred a dip toward current exchange rates. That was sparked by the latest week’s inflation data, alongside an improvement in manufacturing activity. At the time of writing, the AUD/USD is trading at 0.6635.

AUD/USD oscillates around 0.6620s as traders brace for the Federal Reserve’s decision

Wall Street portrays an upbeat market sentiment after JP Morgan acquired the failed lender First Republic Bank. Market participants were bracing for another hike by the US Federal Reserve (Fed) and weighed on the AUD/USD’s pair.

A report by the Institute for Supply Management (ISM) revealed the Manufacturing PMI for April at 47.1, improving from March’s 46.3 but missed the chance to enter the expansionary territory. One of the subcomponents of the ISM’s poll, the Prices Index, surprisingly jumped to 53.2 from 49, indicating that inflation is picking up amongst US factories.

In the meantime, the US Dollar Index (DXY), a gauge for the buck’s value vs. a basket of six currencies, advances 0.43%, up at 102.112, a headwind for the AUD/USD pair. US Treasury bond yields climbed and underpinned the buck, as shown by the DXY

Aside from this, the Fed’s odds for a 25 bps rate hike stand at 88.9%, as shown by the CME Fed Watch Tool.

Aside from this, over the weekend, data from China increased concerns about its growth, with the National Bureau of Statistics (NBS) revealing that the Manufacturing PMI in April slowed down from 51.9 to 49.2. The Non- Manufacturing PMI rose to 56.4, down from 58.2 in March, while the composite Index stood at 54.4, from 57.

“A lack of market demand and the high-base effect from the quick manufacturing recovery in the first quarter” was among the factors that led to the contraction in April, said senior NBS statistician Zhao Qinghe.

Even though China’s outlook looks gloomy, the AUD/USD held to its earlier gains. Data from Australia witnessed the Judo Bank Manufacturing PMI rising to 48, below the prior’s month 49.1, while the TD-MI inflation gauge rose by 0.2%, below the latest month’s 0.3%.

In further data, Australia’s Labor government will reveal a vast improvement in the country’s budget bottom line next week, which has been helped by tax windfalls and job gains. Nevertheless, Treasurer Jim Chalmers has warned that fiscal challenges persist, and the government aims to be responsible with spending to avoid inflation, particularly since the Reserve Bank of Australia is aggressively lifting interest rates.

AUD/USD Technical Levels

-

19:44

Silver whipsawed as US Dollar firms

- Silver is choppy on Monday surrounding US data and the banking sector.

- US Dollar firms on JPMorgan Chase's takeover of First Republic Bank.

Silver is trading at $25.0445 at the time of writing and has traveled in a wide range of between $24.8845 and $25.9123 so far.

It has been a particularly choppy session for the white metal as traders digested news of JPMorgan Chase's takeover of First Republic Bank, ahead of Wednesday's policy decision by the US Federal Reserve.

JPMorgan Chase has bought failed First Republic Bank's deposits and a "substantial amount of their assets and certain liabilities," JPMorgan Chase said in a press release Monday.

"Our government invited us and others to step up, and we did," JPMorgan Chase CEO Jamie Dimon said in a statement. "This acquisition modestly benefits our company overall, it is accretive to shareholders, it helps further advance our wealth strategy, and it is complementary to our existing franchise."

Analysts at Brown Brothers Harriman said that ´´while the deal leads to even greater consolidation of the US banking sector, it was a necessary one in order to address this long-festering problem.´´

´´We are cautiously optimistic that this resolution finally ends the banking sector turmoil that began nearly two months ago,´´ the analysts said.

Meanwhile, the US Dollar is firmly higher as per the DXY index that measures the Greenback vs. a basket of currencies. DXY rallied from a low of 101.624 to a high of 102.189 so far. The boost came in line with Monday's good news for the banking sector as well as US data. US Manufacturing pulled off a three-year low in April as new orders improved slightly and employment rebounded.

Additionally, US construction spending increased more than expected in March. Weak economic data from China may have been a factor also with the manufacturing purchasing managers' index (PMI) declining to below contraction territory (50) with the data reading 49.2 from 51.9 in March for the world's second-biggest economy.

Meanwhile, this week is shaping up to be an eventful one in terms of economic data and earnings news while investors await the Federal Reserve decision. ´´We expect a 25bp rate hike at next week's FOMC meeting, and anticipate that post-meeting communication will: (i) emphasize that disinflation has been evolving slower than expected, leaving open the possibility of additional tightening, and (ii) acknowledge the more uncertain economic environment, especially with regard to credit conditions post SVB collapse,´´ analysts at TD Securities said.

-

18:56

GBP/USD Price Analysis: Bulls about to make another move? 1.2450 is key

- GBP/USD bulls are in the market while above key trendline support.

- Bears are taking on the micro trendline but 1.2450 is key.

GBP/USD bulls took over on Friday to print a fresh bull cycle high and although we have seen a slide from those highs, so long as the bulls commit to above 1.2450, the bias remains bullish.

The following is a top-down technical analysis that arrives at a bullish conclusion.

GBP/USD daily chart

The failed right-hand shoulder of the head and shoulders pattern leaves the bias bullish considering the recent rally that took out the highs of the right-hand shoulder and the head:

GBP/USD H4 charts

The trendline supports are key in this regard:

While the above is a theoretical schematic, it identifies the key areas of support and resistances in the 4-hour time frame. The micro trendline is under pressure but so long as the broader trendline remains intact, meeting 1.2450, or thereabouts, then it would be reasonable to expect the bulls to move in again.

-

18:37

USD/JPY Price Analysis: Surges past 137.00, with buyers eyeing a new YTD high around 138.00

- USD/JPY continues to portray the Yen’s weakness, following the BoJ’s decision to keep its loose monetary policy.

- USD/JPY Price Analysis: The uptrend remains intact, above 137.00, with bulls eyeing 138.00.

The USD/JPY extends its gains in the New York session, rising above 137.00 on overall Japanese Yen (JPY) weakness after last week’s Bank of Japan’s (BoJ) decision to stick to its easy monetary policy. Therefore, the USD/JPY is trading at 137.42 after hitting a daily low of 136.11.

USD/JPY Price Action

From a daily chart perspective, the USD/JPY continues to trend up after last Friday’s price action witnessed more than 1.70% gains. As the pair edged higher, it broke several resistance levels, like the 20 and 100-day EMAs, each at 134.14 and 134.12, respectively. Additionally, the USD/JPY left behind the 200-day EMA at 133.79, cheered by buyers, who remain hopeful of lifting prices towards the last year’s high at 151.94.

If USD/JPY reclaims the November 30 cycle high at 138.17, that would expose the November 21 daily high at 142.25. A breach of the latter will expose the 145.00 figure.

Conversely, if USD/JPY drops below 137.00, it could pave the way for a downward correction. Once cleared, the USD/JPY following support would be the April 28 high at 136.56. Downside risks will emerge below the latter, and it might extend towards the April 19 swing high at 135.13, followed by the 20-day EMAat 134.14, closely followed by the 100-day EMA.

USD/JPY Daily Chart

-

17:42

US: Atlanta Fed GDPNow for Q2 rises to 1.8%

According to the Federal Reserve Bank of Atlanta's GDPNow model, the US economy is expected to grow at an annualized rate of 1.8% in the second quarter, up slightly from 1.7% on the April 28 estimate.

"After this morning’s construction spending release from the US Census Bureau and the Manufacturing ISM Report On Business from the Institute for Supply Management, the nowcast of second-quarter real gross private domestic investment growth increased from 0.3% to 1.0%," Atlanta Fed explained in its publication.

Market reaction

The US Dollar Index preserves its bullish momentum in the American session and was last seen rising 0.5% on the day at 102.15.

-

17:28

EUR/USD falls as ISM Manufacturing PMI improves, boosting USD on Fed tightening speculation

- EUR/USD dips as ISM Manufacturing PMI for April shows improvement but falls short of expansionary territory.

- IMF Chief Downplays de-dollarization concerns amid banking sector vulnerabilities.

- EU Inflation Figures and HCOB Manufacturing PMI to provide insight on the European Central Bank's chances for a 50 or 25 bps rate hike.

The EUR/USD dropped below 1.1000 after the ISM announced that manufacturing activity in April improved. However, it stood in contractionary territory, while a measure of inflation in the same data increased. Therefore, speculations for further tightening by the Federal Reserve (Fed) underpinned the US Dollar (USD). At the time of writing, the EUR/USD is trading at 1.0969 after hitting a high of 1.1035.

EUR/USD losses traction and creeps lower on US data

A risk-on impulse dominates the US equity markets, courtesy of JP Morgan's acquiring the troubled First Republic Bank. However, that's not happening in the FX space, as the EUR/USD fell after the ISM Manufacturing PMI for April improved to 47.1 from 46.3 in the prior's month. While there were improvements in the Orders and Production subcomponents, they fell short of reaching expansionary territory. The Prices Index increased by 4 points to 53.2, which led to speculation that the Federal Reserve might implement tighter monetary policies in the upcoming Wednesday.

Therefore, the EUR/USD retraced, past the daily pivot point and beneath the S1 daily pivot, at 1.0970. It should be said that the greenback underpinned by higher US T-bond yields, its printing losses of 0.46%, up at 102.149.

As of writing, comments from the IMF Managing Director Kristalina Georgieva on Monday said, "De-dollarization isn't on top of my worry list." She added, "There may be more vulnerabilities exposed in the banking sector," and warned that they would see quite a lot of regulatory and disclosure thinking in the wake of the banking crisis.

An absent Eurozone's (EU) economic docket kept EUR/USD traders leaning on the American Dollar (USD) dynamics and market sentiment. On Tuesday, the EU's agenda will feature inflation figures and the HCOB Manufacturing PMI in its final reading. The US economic calendar would feature the JOLTs Job Openings report and Factory Orders ahead of Wednesday's Federal Reserve monetary policy decision.

EUR/USD Technical Analysis

From a technical perspective, the EUR/USD is still upward biased but about to test the 20-day EMA at 1.0955. A fall below the latter will expose the 1.0900 figure, followed by the 50-day EMA at 1.0856. Conversely, if EUR/USD buyers reclaim 1.1000, further upside is warranted at around 1.1095.

-

16:53

IMF’s Georgieva: Don't see alternative to US Dollar any time soon

"De-dollarization isn't on top of my worry list," International Monetary Fund’s (IMF) Managing Director Kristalina Georgieva said on Monday and added that the doesn't see an alternative to the US Dollar any time soon.

"There may be more vulnerabilities exposed in the banking sector," Georgieva warned and further noted that they will see a quite a lot of regulatory and disclosure thinking in the wake of the banking crisis.

Market reaction

The US Dollar preserves its strength in the American session and the US Dollar Index was last seen rising 0.5% on a daily basis at 102.15.

-

16:11

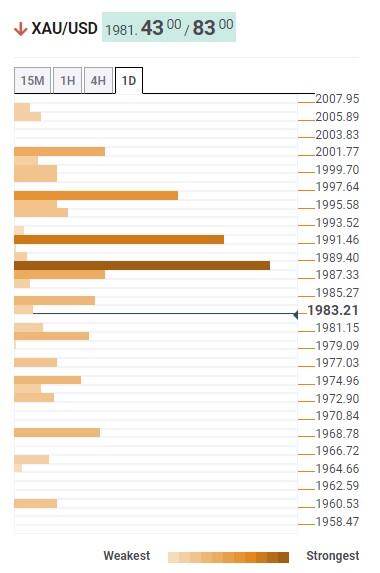

Gold Price Forecast: XAU/USD dips below $2000 on improved ISM report, as high inflation looms

- Gold price dips below $2000, extending its fall beneath the 20-day EMA.

- The ISM showed that manufacturing activity in the US improved but flashed that prices jumped compared to last month’s data.

- XAU/USD Price Analysis: To continue to fall as the RSI indicator approaches the 50-midline.

Gold price slides below the $2000 barrier on a report by the Institute for Supply Management (ISM), showing that manufacturing activity is improving. However, a jump in the prices subcomponent justifies the need for higher rates in the United States (US). The XAU/USD is trading at $1982.70.

US ISM Manufacturing PMI improved but stayed at recessionary levels

Wall Street opened with gains after JP Morgan Chase, of the largest banks in the US, acquired the troubled First Republic Bank. That improved the market mood, though the ISM’s data triggered a leg down in XAU/USD’s price.

The ISM Manufacturing PMI for April remained in contractionary territory for the fifth month, after expanding for 30 consecutive months, at 47.1, higher than March’s 46.3. Delving into the data, the Orders and Production subcomponents improved but lacked the strength to enter the expansionary territory. The Prices Index jumped 4 points to 53.2, sparking speculations that the Federal Reserve (Fed) will tighten monetary conditions next Wednesday.

The XAU/USD reacted downwards, down 0.11% in the early New York session. US Treasury bond yields increased, with the 10-year benchmark note rate yielding 3.513%, gaining eight bps, a headwind for the yellow metal.

The US Dollar Index (DXY), which measures the performance of six currencies vs. the greenback, is climbing 0.33%, up at 102.009, courtesy of elevated US Treasury bond yields.

Despite the backdrop, the latest report for growth in the US), recessionary fears linger around the US economy. The Advanced Gross Domestic Product (GDP) for ¡2 2023 at 1.1% showed that the economy is slowing down. But the Core PCE, the Fed’s preferred gauge for inflation, stood at around 4.6% for the second straight month,

Therefore, the CME FedWatch Tool flashes an 88.9% chance the Fed will raise rates by 25 bps to 5.00% 5.25%. Notably, the swaps market shows a 40% chance for the first rate cut in November’s meeting.

Following today’s data, the US economic agenda will feature the JOLTs Job Openings report and Factory Orders on Tuesday. On Wednesday, the Federal Reserve monetary policy decision will be highlighted.

XAU/USD Technical Analysis

After hitting a daily high of $2005.99, the XAU/USD retreated sharply, exchanging hands below the 20-day Exponential Moving Average (EMA), which lies at $1988.60. Oscillators like the Relative Strength Index (RSI) indicators continued to show that sellers are gathering momentum, about to cross beneath the 50-midline. If that happens, XAU/USD could extend its losses toward the 50-day EMA at $1954.44, which, if cleared, the Gold price can extend its losses toward the 100-day EMA at $1906.42.

-

15:00

United States ISM Manufacturing Prices Paid above expectations (50.4) in April: Actual (53.2)

-

15:00

United States ISM Manufacturing PMI above forecasts (46.6) in April: Actual (47.1)

-

15:00

United States Construction Spending (MoM) above expectations (-0.1%) in March: Actual (0.3%)

-

15:00

United States ISM Manufacturing Employment Index registered at 50.2 above expectations (47.9) in April

-

15:00

United States ISM Manufacturing New Orders Index registered at 45.7 above expectations (45.5) in April

-

14:46

United States S&P Global Manufacturing PMI below expectations (50.4) in April: Actual (50.2)

-

14:45

GBP/USD bounces off daily low, holds steady around mid-1.2500s ahead of US ISM PMI

- GBP/USD reverses modest intraday losses amid the emergence of some USD selling.

- Rising US bond yields, looming recession risks underpin the USD and cap the upside.

- Traders now look to the US ISM PMI for some impetus ahead of the FOMC meeting.

The GBP/USD pair attracts some buying in the vicinity of the 1.2500 psychological mark on Monday and turns neutral during the early part of the North American session. The pair is currently placed around the 1.2550 region and remains well within the striking distance of its highest level since June 2022 touched on Friday.

The US Dollar (USD) surrenders a major part of its modest intraday gains amid the uncertainty over the Federal Reserve's (Fed) rate-hike path and turns out to be a key factor lending some support to the GBP/USD pair. In fact, the markets have fully priced in another 25 bps lift-off at the end of a two-day FOMC monetary policy meeting on Wednesday, which remains supportive of a modest uptick in the US Treasury bond yields and acts as a tailwind for the USD.

Investors, however, seem convinced that the US central bank will then hold rates steady for the rest of the year, which, in turn, holds back the USD bulls from placing aggressive bets. Apart from this, firming expectations that the Bank of England (BoE) will also hike interest rates by 25 bps in May assists the GBP/USD pair to attract some dip-buying at lower levels, though the upside seems limited ahead of the highly-anticipated FOMC meeting, starting on Tuesday.

Furthermore, looming recession risks might continue to benefit the Greenback's relative safe-haven status and contribute to capping gains for the GBP/USD pair, at least for the time being. From a technical perspective, Friday's sustained breakthrough and acceptance above the 1.2500 psychological mark, along with the emergence of some dip-buying on Monday, favours bulls and suggests that the path of least resistance for spot prices is to the upside.

Next on tap is the release of the US ISM Manufacturing PMI. This, along with the US bond yields and the broader risk sentiment, will drive the USD demand and provide some meaningful impetus to the GBP/USD pair. The immediate market reaction, however, is more likely to remain limited, warranting some caution before placing aggressive directional bets.

Technical levels to watch

-

14:36

Canada: S&P Global Manufacturing PMI improves to 50.2 in April vs. 50.5 expected

- S&P Global Manufacturing PMI for Canada recovered above 50 in April.

- USD/CAD stays in daily range at around 1.3550.

Business activity in the Canadian manufacturing sector expanded at a soft pace in April with S&P Global Manufacturing PMI improving to 50.2 from 48.6 in March. This reading came in below the market expectation of 50.5.

Commenting on the survey's findings, “although Canada’s manufacturing sector returned to growth in April, it did so only marginally with underlying data suggesting the recovery remained on shaky ground," noted Paul Smith, Economics Director at S&P Global Market Intelligence.

"Output and employment growth were sustained, but another drop in new orders is probably the most notable development," Smith added. "Clients are hesitant in their spending decisions, unsure of the direction of the economy at a time when prices remain high."

Market reaction

USD/CAD showed no immediate reaction to this report and was last seen trading modestly higher on the day at 1.3558.

-

14:31

Canada S&P Global Manufacturing PMI came in at 50.2, below expectations (50.5) in April

-

14:00

Chile Unemployment rate climbed from previous 8.4% to 8.8% in March

-

13:58

Gold Price Forecast: XAU/USD jumps back above $2,000 mark, upside seems limited

- Gold price reverses an intraday dip and climbs back above the $2,000 psychological mark.

- Looming recession fears weigh on investors’ sentiment and benefit the safe-haven metal.

- A modest US Dollar strength might cap gains ahead of this week’s central bank event risks.

Gold price attracts some dip-buying near the $1,977 region on Monday and climbs to a fresh daily high heading into the North American session. The XAU/USD is currently placed just above the $2,000 psychological mark, though remains confined in a familiar trading range held over the past two weeks or so.

Looming recession fears benefit Gold price

The weaker Chinese manufacturing data released on Sunday adds to market worries about economic headwinds stemming from rising borrowing costs and turns out to be a key factor acting as a tailwind for the safe-haven Gold price. In fact, the official Chinese Manufacturing Purchasing Managers' Index (PMI) declined to 49.2 in April from 51.9 previous. This comes on the back of the Advance Gross domestic product (GDP) report released from the United States (US) last week, which showed that the world's largest economy slowed more than expected in the first quarter. Furthermore, factory activity in Japan - the world's third-biggest economy - contracted for the sixth straight month in April and fueled recession fears. This, in turn, weighs on investors' sentiment and drives some haven flows towards the XAU/USD.

Modest US Dollar strength caps gains for Gold price

Apart from this, speculations that the Federal Reserve (Fed) will hold rates steady for the rest of the year beyond May further seem to lend support to the non-yielding Gold price. The markets, however, have fully priced in another 25 basis points (bps) lift-off at this week's Federal Open Market Committee (FOMC) policy meeting, starting on Tuesday. The expectations remain supportive of a modest uptick in the US Treasury bond yields and assist the US Dollar (USD) to gain some positive traction for the third successive day. Adding to this, expectations that the European Central Bank (ECB) could surprise with an outsized 50 bps lift-off on Thursday might hold back traders from placing aggressive bets around the XAU/USD and further contribute to keeping a lid on any meaningful upside, at least for the time being.

The aforementioned fundamental backdrop makes it prudent to wait for strong follow-through buying before positioning for any further appreciating move ahead of the key central bank event risks. The focus will then shift to the release of the closely-watched US monthly employment details on Friday. The popularly known Nonfarm Payrolls (NFP) report will play a key role in influencing the near-term USD price dynamics and determine the next leg of a directional move for the US Dollar-denominated Gold price. In the meantime, traders on Monday will take cues from the release of the US ISM Manufacturing PMI print for April to grab short-term opportunities around the XAU/USD.

Gold price technical outlook

From a technical perspective, any subsequent move-up is likely to confront some resistance near the $2,010-$2,012 supply zone, which if cleared decisively will negate any near-term negative bias and prompt some technical buying. The Gold price might then climb to the $2,039-$2,040 region before aiming to challenge the YTD peak, around the $2,048-$2,049 region touched on April 13.

On the flip side, the $1,975-$1,970 zone might continue to protect the immediate downside. A convincing break below the said support will mark a bearish breakdown through a short-term trading range and make the Gold price vulnerable to decline further. The XAU/USD might then accelerate the downfall towards the $1,948 resistance breakpoint, now turned support, en route to the 50-day Simple Moving Average (SMA), currently around the $1,937-$14,936 area.

Key levels to watch

-

12:04

US Dollar firm as First Republic gets closure – BBH

"We finally have some closure on First Republic; the deal clears the deck for global monetary tightening to continue unabated," not analysts at BBH.

Recent data have been dollar-supportive

"The dollar is firm as First Republic gets closure. DXY is trading higher for the third straight day just below 102 as the deal should help dial down banking sector risk in the U.S. With most of Europe on holiday, the euro is trading lower near $1.10 and sterling is trading lower near $1.2520. USD/JPY is trading at the highest since March 10 and is testing the 200-day moving average near 137. It should eventually break above and near 137 and test the March 8 high near 138."

"Recent data have been dollar-supportive but until rate cuts this year are finally priced out, the dollar is likely to remain vulnerable. Perhaps the First Republic deal and a hawkish Fed this week will open up the next stage higher for the greenback."

"After marathon talks, regulators seized the troubled bank and will sell the bulk of the assets to JPMorgan Chase. JPMorgan will assume all of First Republic’s $92 bln in deposits as well as most of its assets, including nearly $175 bln in loans and $30 bln in securities. In order to help facilitate the deal, the FDIC will share losses on Frist Republic’s loans and estimated it would see a $13 bln hit from the deal. While the deal leads to even greater consolidation of the U.S. banking sector, it was a necessary one in order to address this long-festering problem. We are cautiously optimistic that this resolution finally ends the banking sector turmoil that began nearly two months ago."

-

12:00

USD/JPY stalls intraday positive move near 200 DMA, still well bid above mid-136.00s

- USD/JPY climbs to its highest level since March 10, albeit struggles to break through the 200 DMA.

- The BoJ’s dovish outlook weighs heavily on the JPY and acts as a tailwind amid a modest USD strength.

- Investors now look to the US ISM Manufacturing PMI for some impetus ahead of the FOMC meeting.

The USD/JPY pair builds on Friday's blowout rally and gains strong follow-through traction on the first day of a new week. The momentum lifts spot prices to the highest level since March 10, though pauses near a technically significant 200-day Simple Moving Average (SMA) resistance just ahead of the 137.00 mark. The pair, however, maintains its bid tone through the first half of the European session and is currently placed just above mid-136.00s, still up around 0.25% for the day.

The Japanese Yen (JPY) continues to be weighed down by the Bank of Japan's (BoJ) dovish outlook, which, along with a modest US Dollar (USD) strength, acts as a tailwind for the USD/JPY pair. It is worth recalling that the Japanese central bank on Friday left its ultra-loose monetary policy settings unchanged and also made no tweaks to its yield curve control (YCC) by a unanimous vote. Adding to this, the new BoJ Governor Kazuo Ueda said that the risk from tightening too hastily is larger than monetary policy falling behind the curve and added that it will be appropriate to continue monetary easing to achieve the 2% inflation target.

Apart from this, data released earlier this Monday showed that factory activity in Japan - the world's third-biggest economy - contracted for the sixth straight month in April, which, in turn, exerts additional downward pressure on the JPY. The USD, on the other hand, edges higher for the third successive day amid the prospects of the Federal Reserve (Fed) raising interest rates by another 25 basis points (bps) at the end of a two-day meeting on Wednesday. The markets, however, seem convinced that the US central bank will then hold rates steady for the rest of the year. This holds back the USD bulls from placing aggressive bets and caps the pair.

Furthermore, worries about economic headwinds stemming from rising borrowing costs could lend some support to the safe-haven JPY and contribute to keeping a lid on the USD/JPY pair, at least for the time being. In fact, the Advance USD GDP report released last week showed that growth in the world's largest economy slowed more than expected in the first quarter. Moreover, the official Chinese Manufacturing PMI declined to 49.2 in April from 51.9 in March and further fueled recession fears. Market participants now look forward to the release of the US ISM Manufacturing PMI, due later during the early North American session.

Apart from this, the broader market risk sentiment might further contribute to producing short-term opportunities around the USD/JPY pair. The focus, meanwhile, will remain glued to the outcome of the FOMC meeting on Wednesday and the closely-watched US monthly employment details, popularly known as the NFP report on Friday. This will play a key role in influencing the near-term USD price dynamics and help determine the next leg of a directional move for the major.

Technical levels to watch

-

11:22

USD/CAD clings to gains near 1.3575 area amid sliding Oil prices, modest USD strength

- USD/CAD regains positive traction on Monday and draws support from a combination of factors.

- Sliding Crude Oil prices undermines the Loonie and acts as a tailwind amid a modest USD strength.

- Traders now look to the US ISM Manufacturing PMI for some impetus ahead of the FOMC meeting.

The USD/CAD pair attracts some buyers near the 100-day Simple Moving Average (SMA) on Monday and stalls Friday's sharp retracement slide from the 1.3665-1.3670 region, or one-month high. The pair maintains its bid tone around the 1.3570-1.3575 area through the first half of the European session and for now, seems to have snapped a two-day losing streak.

Crude Oil prices struggle to capitalize on Friday's goodish rebound from a one-month low and come under renewed selling pressure amid worries that rising borrowing costs could slow economic growth, which, in turn, will hit fuel demand. Apart from this, weaker Chinese manufacturing data aggravates the bearish pressure surrounding the black liquid. This, in turn, is seen undermining the commodity-linked Loonie and acting as a tailwind for the USD/CAD pair. Apart from this, a modest US Dollar (USD) strength further contributes to the bid tone surrounding the major.

The prospects for further interest rate hikes by the Federal Reserve (Fed), along with looming recession risks, push the USD higher for the third successive day on Monday. In fact, the markets have fully priced in another 25 bps lift-off at the end of the highly-anticipated two-day FOMC policy meeting on Wednesday. Furthermore, growing market concerns about economic headwinds stemming from rising borrowing costs benefit the Greenback's relative safe-haven status and provide an additional lift to the USD/CAD pair ahead of the key central bank event risk.

In the meantime, traders on Monday will take cues from the release of the US ISM Manufacturing PMI, due later during the early North American session. Apart from this, the broader risk sentiment will drive the USD demand and provide some impetus to the USD/CAD pair. This, along with Oil price dynamics, should further contribute to producing short-term trading opportunities around the major.

Technical levels to watch

-

11:21

Inflation will be important in determining size of ECB hike – TDS

Analysts at TD Securities see the European Central Bank (ECB) raising its policy rate by 25 basis points (bps) at this week's meeting but note that they can't rule out a bigger hike.

We wouldn't completely rule out a 50bps hike

"Easing financial system stress, persistent high inflation, strong wage growth, and avoidance of a winter recession are enough for the ECB to comfortably hike rates by 25bps in May and re-introduce guidance that more tightening is to come. We wouldn't completely rule out a 50bps hike should data ahead of the decision surprise significantly but that would come without guidance."

"The Bank Lending Survey (BLS) and inflation data will be important inputs in determining the size of rate hike at the May ECB meeting. We expect the BLS to show some easing in lending conditions, in part due to the improved economic outlook since Q4. Moreover, a decline in core and a steady headline rate (TDS: 6.9%, mkt: 7.0%) should skew risks further away from a 50bps hike."

-

11:15

ECB is not in position to pause tightening cycle – ANZ

Analysts ANZ think that the European Central Bank (ECB) is not in a position to pause its tightening cycle.

We forecast a 25bp rate rise this week

"The ECB is not yet able to contemplate pausing its tightening cycle. We forecast a 25bp rate rise this week as the ECB balances the lagged effects of previous rate hikes, recent banking turmoil and further tightening."

"Prior to the meeting, however, the updated ECB bank lending survey, M3 data, unemployment and preliminary April HICP data will be published. The ECB will factor this information into deciding the magnitude of its rate rise."

"Clearly, if core inflation is still ratcheting higher in annual terms and both bank lending conditions and credit are holding up well, the ECB could opt for a 50bp rise. Hawks have said that a 50bp rise is on the table."

"The question for the ECB is how persistent inflation will be and if second round effects are emerging. We expect future rate rises to be determined meeting by meeting and see a risk that tightening could extend into Q3."

-

11:11

Fed to emphasize disinflation has been evolving slower than expected – TDS

Previewing this week's key events and data releases from the United States (US), analysts at TD Securities noted that they expect the US central bank to raise the policy rate by 25 basis points (bps).

US payrolls likely slowed for a third consecutive month

"We anticipate that post-meeting communication will: (i) emphasize that disinflation has been evolving slower than expected, leaving open the possibility of additional tightening, and (ii) acknowledge the more uncertain economic environment, especially with regard to credit conditions post SVB collapse."

"US payrolls likely slowed for a third consecutive month to a still firm pace in April, though the slowest since 2020. We also look for the UE rate to rise to 3.6%, and wage growth to print 0.3% m/m."

"Surveys already released point to a small rebound for both the ISM manufacturing and services indexes in April following their twin declines in March to 46.3 and 51.2, respectively. We look for the ISM manufacturing index to advance modestly to a less dire level at 47.5. The services index likely rose as well but to 52.2, indicating a modest improvement in the pace of expansion for the sector."

-

11:05

US: Downward revision to retail sales responsible for GDP miss – ABN Amro

Commenting on the US growth data, "GDP growth slowed to 1.1% q/q annualised, according to the advance estimate, which was well below our and consensus forecasts for a 2% expansion, and down from 2.6% growth in Q4," said Bill Diviney, Senior Economist at ABN Amro.

Consumption still grew very strongly in the first quarter

While the main drag came from a drop in inventories (which subtracted a whopping 2.7pp from growth), a large downward revision to retail sales also meant consumption was not as strong as expected. Indeed, the Atlanta Fed’s GDP Now tracker had already suggested a big miss the day prior to the release of the GDP report, due to the revision to retail sales. Despite that downward revision, consumption still grew very strongly in the first quarter, by 3.7% annualised, with a 16.9% surge in durable goods consumption responsible for the strength (services consumption growth was much more moderate at 2.3%).

The exceptional strength in goods consumption has been a surprise in the first quarter, given that for much of last year goods consumption had been on a cooling trend. Still, looking at more recent high frequency data does suggest goods consumption has since resumed its cooling trend, with for instance Redbook weekly department store sales slowing sharply of late. At the same time, there has been a tendency for repeated downward revisions to consumption data in the post-pandemic period, likely reflecting difficulty in measuring price effects in the current high inflation environment. As such, it would not be a surprise if the Q1 strength in consumption is further revised away in future GDP estimates.

-

10:31

NZD/USD flat-lines below 0.6200 mark, modest USD strength caps the upside

- NZD/USD lacks any firm intraday direction on Monday and oscillates in a narrow band.

- A combination of factors pushes the USD higher and acts as a headwind for the major.

- Traders look to the US ISM PMI for some impetus ahead of the FOMC on Wednesday.

The NZD/USD pair struggles to capitalize on its modest uptick and seesaws between tepid gains/minor losses through the first half of trading on Monday. The pair is currently placed around the 0.6175 region, nearly unchanged for the day and just below a one-and-half-week high touched during the Asian session.

The prospects for further interest rate hikes by the Federal Reserve (Fed), along with looming recession risks, help the US Dollar (USD) to gain traction for the third successive day and turn out to be a key factor capping gains for the NZD/USD pair. In fact, the markets have fully priced in another 25 bps lift-off at the end of the highly-anticipated two-day FOMC policy meeting on Wednesday. Furthermore, weaker Chinese manufacturing data released on Sunday weigh on investors' sentiment and benefits the safe-haven Greenback.

In fact, the official Chinese Manufacturing Purchasing Managers' Index (PMI), released on Sunday, declined to 49.2 in April from 51.9 in March. The data comes on the back of the Advance US GDP report last week, which showed that growth in the world's largest economy decelerated at a faster-than-expected pace during the first quarter, and adds to worries about economic headwinds stemming from rising borrowing costs. This, in turn, drives some haven flows towards the buck and contributes to keeping a lid on the NZD/USD pair.

The markets, meanwhile, seem convinced that the US central bank will hold rates steady for the rest of the year beyond May, which is holding back the USD bulls from placing aggressive bets and lending some support to the NZD/USD pair. Traders also prefer to wait on the sidelines ahead of the key central bank event risk. In the meantime, Monday's release of the US ISM Manufacturing PMI, along with the broader risk sentiment, might influence the USD price dynamics and produce short-term trading opportunities around the major.

Technical levels to watch

-

09:42

GBP/USD drops to fresh daily low amid stronger USD, holds above 1.2500 mark

- GBP/USD retreats from a multi-month high touched on Friday amid a modest USD strength.

- The fundamental backdrop warrants some caution before positioning for any further losses.

- Investors now look to the US ISM PMI for some impetus ahead of the FOMC on Wednesday.

The GBP/USD pair comes under some selling pressure on the first day of a new week and erodes a part of Friday's strong gains to the 1.2580-1.2585 region, or its highest level since June 2022. Spot prices extend the steady intraday descent through the early part of the European session and drop to a fresh daily low, around the 1.2520 area in the last hour.

A combination of supporting factors assists the US Dollar (USD) to gain positive traction for the third successive day, which, in turn, is seen dragging the GBP/USD pair lower. The prospects of the Federal Reserve (Fed) raising interest rates by another 25 basis points (bps) at the end of a two-day meeting on Wednesday, along with looming recession risks, continue to act as a tailwind for the safe-haven Greenback.

China's official Manufacturing PMI declined to 49.2 in April from 51.9 in March. This comes on the back of the Advance US GDP report released last week, which showed that growth in the world's largest economy decelerated more than expected during the first quarter. This, in turn, adds to worries about economic headwinds stemming from rising borrowing costs and drives some haven flows towards the buck.

The markets, however, seem convinced that the US central bank will then hold rates steady for the rest of the year beyond May, which might hold back the USD bulls from placing aggressive bets. Apart from this, rising bets for a 25 bps lift-off by the Bank of England (BoE) might further contribute towards limiting the downside for the GBP/USD pair, warranting some caution before positioning for any further downfall.

Traders might also prefer to wait on the sidelines amid relatively thin trading volumes on the back of a holiday in Europe and ahead of the highly-anticipated two-day FOMC policy meeting, starting on Tuesday. The Fed is scheduled to announce its decision on Wednesday, which will play a key role in influencing the USD price dynamics and help determine the near-term trajectory for the GBP/USD pair.

In the meantime, traders on Monday will take cues from the release of the US ISM Manufacturing PMI, due later during the early North American session. Apart from this, the broader risk sentiment will drive demand for the safe-haven buck and contribute to producing short-term opportunities around the GBP/USD pair.

Technical levels to watch

-

08:54

AUD/USD steady climbs closer to mid-0.6600s, upside potential seems limited

- AUD/USD kicks off the new week on a positive note and climbs to a four-day high.

- A combination of factors could cap any further gains and warrants caution for bulls.

- Traders now look to the US ISM Manufacturing PMI ahead of the RBA on Tuesday.

The AUD/USD pair attracts some buyers on the first day of a new week and builds on Friday's bounce from the 0.6575-0.6570 area, or its lowest level since March 10. Spot prices build on the steady intraday ascent through the early North American session and climb to a four-day high, closer to mid-0.6600s in the last hour.

Traders opt to lighten their bets ahead of this week's key central bank event risks, which, in turn, is seen as a key factor pushing the AUD/USD pair amid relatively thin liquidity conditions on the back of a holiday in Europe. The Reserve Bank of Australia (RBA) is scheduled to announce its monetary policy decision on Tuesday. This will be followed by the outcome of the highly-anticipated two-day FOMC meeting on Wednesday.

The upside for the AUD/USD pair, however, seems limited amid a modest US Dollar (USD) strength, bolstered by the prospects for another 25 bps lift-off by the Federal Reserve (Fed). Apart from this, looming recession fears drive some haven flow towards the Greenback and act as a headwind for the risk-sensitive Aussie. Furthermore, weaker Chinese manufacturing data released on Sunday might contribute to capping the AUD/USD pair.

In fact, the official Chinese Manufacturing Purchasing Managers' Index (PMI), released on Sunday, declined to 49.2 in April from 51.9 in March. The data comes amid worries about economic headwinds stemming from rising borrowing costs and tempers investors' appetite for riskier assets, which is evident from the cautious mood around the equity markets. This warrants some caution before placing bullish bets around the AUD/USD pair.

Market participants now look to the release of the US ISM Manufacturing PMI, due later during the early North American session. This, along with the broader risk sentiment, should influence the USD price dynamics and contribute to producing short-term trading opportunities around the AUD/USD pair.

Technical levels to watch

-

08:22

Forex Today: US Dollar extends recovery to start action-packed week

Here is what you need to know on Monday, May 1:

Financial markets stay relatively quiet to start the new week after month-end flows ramped up volatility ahead of the weekend. Nevertheless, the US Dollar manages to stay resilient against its rivals early Monday with the US Dollar Index extending its recovery toward 102.00. The trading is action is likely to remain subdued during the first half of the day due to Labor Day holiday. In the American session, the ISM Manufacturing PMI survey for April will be watched closely by investors.

US ISM Manufacturing PMI April Preview: Gloom persists despite expanding US economy.

On Friday, the data from the US showed that the Core Personal Consumption Expenditures (PCE) Price Index, the Fed's preferred gauge of inflation, edged lower to 4.6% on a yearly basis in March from 4.7% in April. Moreover, the US Bureau of Labor Statistics reported that the Employment Cost Index, compensation costs for civilian workers, increased by 1.2% in the first quarter, compared to 1% increase recorded in the previous quarter.

Over the weekend, roughly a dozen banks, including PNC Financial Services Group, JPMorgan Chase & Co and Citizens Financial Group Inc, have reportedly submitted bids for first Republic Bank as US regulators are trying to finalize the sale. US stock index futures trade modestly higher on the day following this development and the benchmark 10-year US Treasury bond yield stays below 3.5% despite having retraced a small portion of Friday's decline.

EUR/USD stays under modest bearish pressure and trades near 1.1000 in the European morning on Monday.

GBP/USD reached its highest level since June 2022 at 1.2585 on Friday but struggled to preserve its bullish momentum at the beginning of the week. The pair was last seen trading in negative territory below 1.2550.

Following Friday's impressive rally that was fueled by the Bank of Japan's dovish language, USD/JPY continues to push higher early Monday and was last seen trading at its highest level since early March at 136.80.

AUD/USD has gained traction and advanced toward 0.6650 early Monday. In the Asian trading hours on Tuesday, the Reserve Bank of Australia will announce its policy decision.

Reserve Bank of Australia Preview: No change, nothing new for the Aussie.

Gold price came under renewed selling pressure on Monday and declined to $1,980 area, pressured by recovering US T-bond yields.

Following a quiet weekend, Bitcoin turned south early Monday and was last seen losing more than 2% on the day at around $28,650. After having failed to reclaim $1,900, Ethereum lost its traction and lost more than 1% on Sunday. ETH/USD continues to edge lower toward $1,800 on Monday.

-

08:07

Silver Price Analysis: XAG/USD struggles to break through 100-period SMA on H4

- Silver struggles to gain any meaningful traction and oscillates in a narrow band on Monday.

- The technical setup favours bullish traders and supports prospects for some intraday gains.

- A convincing break below the 23.6% Fibo. is needed to negate the near-term positive bias.

Silver reverses an intraday dip to sub-$25.00 levels and touches a three-day daily high during the early European session on Monday, though lacks follow-through. The white metal has been struggling to make it through the 100-period Simple Moving Average (SMA), warranting some caution for bullish traders and before positioning for an extension of the recent bounce from the $24.50-$24.40 horizontal support.

Looking at the broader picture, the XAG/USD is holding comfortably above the 23.6% Fibonacci retracement level of the March-April rally. Moreover, technical indicators on the daily chart maintain their bullish bias and have been gaining positive traction on hourly charts. This, in turn, supports prospects for some intraday appreciating move back towards the $25.50 supply zone. Some follow-through buying will negate any negative bias and pave the way for additional gains.

The XAG/USD might then make a fresh attempt to conquer the $26.00 round-figure mark and retest a one-year high touched on April 14. The positive momentum could get extended further towards the next relevant hurdle near the $26.25-$26.30 region en route to the 2022 swing high, just ahead of the $27.00 round-figure mark.

On the flip side, the $24.50-$24.40 region might continue to act as immediate strong support, which if broken decisively might prompt some technical selling. The subsequent downfall has the potential to drag the XAG/USD below the $24.00 mark, towards testing the 38.2% Fibo. level, around the $23.70 area. The corrective decline could get extended further towards the $23.35-$23.30 horizontal support before the metal drops to the $23.00 confluence, comprising the 50% Fibo. level and the 50-day SMA.

Silver 4-hour chart

Key levels to watch

-

08:00

US ISM Manufacturing PMI April Preview: Gloom persists despite expanding US economy

- The ISM Manufacturing PMI is set to rise to 47.0 from 46.9, New Orders seen higher at 45.5.

- The ISM Prices Paid Index is seen expanding to 50.4 from 49.2 in the previous month.

- Purchasing Managers’ Index will be released by the ISM at 14:00 GMT.

The main Manufacturing Purchasing Managers’ Index (PMI) in the United States will be released by the Institute of Supply Management (ISM) in its Report on Business, where the latest manufacturing business survey result is displayed, at 14:00 GMT this Monday.

What to expect from the ISM manufacturing PMI report?

The most important manufacturing PMI in the United States is expected to have risen slightly to 47.0 in April from the 46.3 figure booked in March.

Among the sub-components of the report, the focus will be on Prices Paid as it reflects business sentiment around future inflation. The Manufacturing Prices Paid sub-index is likely to return to expansion, with a 50.4 expected for April. In March, the gauge stood at 49.2.

The ISM Manufacturing Employment Index is also seen a tad higher at 47.9 in the fourth month of the year while the New Orders Index for April is foreseen at 45.5 vs. March’s 44.3.

In March, the ISM survey showed that all subcomponents of its manufacturing PMI were below the 50 threshold for the first time in 14 years. The headline index tumbled to its lowest level in three years, as new orders plunged. The US Federal Reserve’s (Fed) relentless tightening to fight inflation raised borrowing costs and cooled demand for goods.

The data will provide a fresh update on the health of the US manufacturing sector amid tighter financial conditions and growing recession risks, especially after Thursday’s US Gross Domestic Product (GDP) data for Q1.

Apart from the US economic data, investors will track the broader market sentiment in the lead-up to Wednesday’s Federal Reserve policy announcements.

Analysts at TD Securities offer a brief preview of the key macro data and explain:

“Surveys already released point to a small rebound for both the ISM manufacturing and services indexes in April following their twin declines in March to 46.3 and 51.2, respectively. We look for the ISM Manufacturing index to advance modestly to a less dire level at 47.5. The services index likely rose as well but to 52.2, indicating a modest improvement in the pace of expansion for the sector."

When will the ISM manufacturing Purchasing Managers’ Index report be released and how could it affect EUR/USD?

The ISM Manufacturing PMI report is scheduled for release at 14:00 GMT, on May 1. Ahead of the key release, the US Dollar staged a decent comeback from two-week lows, fuelling a corrective downside in the EUR/USD pair toward 1.1000. The main currency pair hit a new 13-month high at 1.1096 last Wednesday.

A stronger headline print will bolster bets for a 25 basis points (bps) Fed rate hike move in early May. This, in turn, should fuel a fresh leg higher in the US Treasury bond yields, aiding the recovery of the US Dollar.

Last week, even though the headline US Q1 GDP number missed estimates of 2.0% QoQ by a wide margin at 1.1%, resilient personal consumption, inventories accumulation and a higher inflation component grabbed investors’ attention and ramped up odds of a quarter percentage point Fed rate hike next week to 86%. At the start of the week, the probability of a 25 bps Fed May rate hike stood at around 75%.

However, a softer report could act as a headwind to the ongoing recovery momentum in the US Dollar. The US Dollar decline could follow, driving the EUR/USD pair back toward the yearly top.

Traders will also pay close attention to the ISM survey's forward-looking New Orders sub-index, the Prices Paid component and the measure of factory employment for fresh implications on the Fed’s interest rates outlook. Markets could resort to repositioning ahead of the all-important Federal Reserve interest rates decision, which could affect the pair’s reaction to the ISM survey.